|

BOX 4.1 David doesn’t know where to turn.1 He’s facing mounting medical bills and can’t pay them off. He and 900 of his colleagues were laid off when the bank he worked for merged with another. They were told their health benefits were protected by the Consolidated Ominibus Budget Reconciliation Act (COBRA) and they could maintain coverage if they wanted to, but they would have to pay the full amount of the premium plus 2 percent extra. That’s $600 per month for family coverage, four times more than they had been paying on the job. Without a salary, David as well as many of his colleagues decided they could not afford to maintain the coverage. David’s wife had given up her job with an accounting firm 10 months ago to be an independent contractor because it looked as if she would eventually make more money, could work from home, and would have more time to spend with the kids. Unfortunately, her business has been growing very slowly and she has no access to group health benefits. Then John, the oldest boy, broke his ankle at a neighborhood soccer game. He had a multiple fracture that was treated quickly at the emergency room. John needed follow-up surgery, had complications from the anesthesia, and stayed in the hospital for four nights, and the bills are starting to pile up from the doctor, surgeon, lab, and radiology. Soon John will need physical therapy to regain full functioning of the joint, and they will have to pay cash up front for each visit. The medical bills already have eaten into the savings they need until David finds another job. David is afraid to let their 8-year-old play sports now because they cannot risk another injury. David has been having stomach pains but refuses to go to the doctor since he cannot pay the bill now. He hopes it is just stress and not too serious. He fears the growing debt might force them into bankruptcy if he doesn’t find a job soon. |

4

Financial Characteristics and Behavior of Uninsured Families

Though it is much more than this, a family can be thought of as a collection of individuals that is grouped into a single financial unit sharing both resources and risks. In this sense, health insurance coverage can be viewed as a shared family resource. It is often obtained through the employment of a single member of the family, but it reflects a shared resource in other ways as well. When individuals in a family obtain coverage through means-tested government programs, their eligibility often depends on the combined income of the family unit. Conversely, the risk that out-of-pocket health care expenditures will severely strain a family’s finances can be seen as a shared family risk. So can a family’s decision about how many of its members to cover if employment-related family health care coverage is available to a member of the family.

This chapter examines the impact of health care expenses on the finances of families where one or more of the members are not covered by employer-provided or publicly provided health insurance. It first offers a picture of the typical financial position of such families—their income, assets, and borrowing capacity. Then it examines their health care expenditures. Next, the ways in which they meet these expenditures and the burden this imposes on family finances are explored. The chapter ends with a brief summary.

INCOME, ASSETS, AND BORROWING POWER OF UNINSURED FAMILIES

Finding: Families with at least one uninsured member are predominantly lower income.

As discussed in Chapter 2, uninsured families have lower family incomes on average than do families with health coverage. More than half of all families with at least one uninsured member have incomes that are at or below 200 percent of the federal poverty level (FPL). Two out of every five lower-income1 families have at least one uninsured member, whereas just 9 percent of families with moderate and high incomes have at least one uninsured member.2 Poverty, lack of insurance, and poor health are factors that are often present in families concurrently, and are interrelated so that it is difficult to identify the causal directions and impacts.

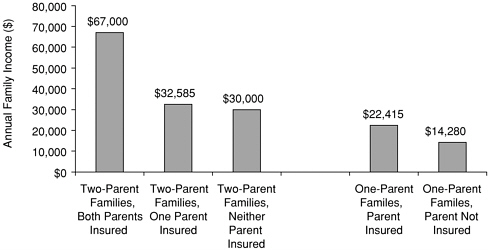

This relationship between lack of insurance coverage and low family income is underscored by the insurance and income characteristics of families with children. The median income for two-parent families in which both parents are covered by insurance is $67,000 compared to $30,000 for two-parent families in which neither parent is covered. The median income of one-parent families in which the single parent does not have health insurance is only $14,280 (Figure 4.1). As noted in Chapter 2, virtually all (98 percent) families with both parents insured have all of their children covered by insurance and are associated with the higher median income, while only 44 percent of one-parent families in which the parent is uninsured have all children covered.3 Given the lower median income of uninsured single-parent families, many of their uninsured children would be eligible for public coverage.

Finding: Families with uninsured members tend to have fewer assets than do fully insured families and are unlikely to have the capacity to borrow to cover major unexpected health care costs.

Not only do families with uninsured members have lower incomes than fully insured families, they also have extremely limited financial resources such as savings and lines of credit with which to pay medical expenses. Public insurance programs have both income and asset requirements for eligibility that leave many low-income families with uninsured members. Among families in which no one had health insurance in 1989, 45 percent had no financial assets. (Starr-McCluer, 1996).4 In 1989, the median amount of financial assets for families with no members insured was $50.

|

1 |

“Low-income family” is defined as a family reporting its income to be at or below 100 percent of FPL and, “lower-income family” is a family reporting its income to be at or below 200 percent of FPL. |

|

2 |

Calculated from data in Table 2.1. |

|

3 |

Analyses conducted for this report are based on tabulations of the 2001 Current Population Survey (CPS) public use tapes by Matthew Broaddus of the Center on Budget and Policy Priorities. |

|

4 |

This survey includes singles and childless couples as families. Assets include balances in checking and savings accounts, stocks, bonds, mutual funds, and individual retirement accounts (IRAs) and other retirement savings. The statements about asset levels are based on the Survey of Consumer Finances (SCF). The SCF is a national survey carried out every three years by the Board of Governors of the Federal Reserve Board. In the SCF, a family is a subset of the household unit referred to as the |

FIGURE 4.1 Families with children, median family income, 2000, by extent of parental health insurance coverage.

SOURCE: See Appendix D.

People of late middle age who are uninsured are at a higher risk of needing to use their assets for health services because they have an increased risk of chronic disease (IOM, 2002a). They also have fewer years before retirement to replenish savings depleted by health care costs. Families with older members in which no one has health insurance have only marginally greater financial assets than younger uninsured families (Starr-McCluer, 1996). Among uninsured families headed by 55 to 64-year-olds in 1989, median financial assets were $200.

Other assets beyond financial ones could help a family cope with medical expenses, but a majority of families in which no one has health insurance have limited assets of any kind. Net worth is the broadest measure of accumulated wealth. It is the sum of financial wealth and other assets, including homes, other real estate, business equity, and vehicles, minus liabilities. Liabilities include mortgages, home equity loans, automobile loans, other loans, and credit card debt. Across families of all ages, median net worth for families with all members uninsured was $1,000 in 1989, compared to $60,175 for families with all members insured (Starr-McCluer, 1996).

A third way in which uninsured families might cover health care costs, especially non-routine health care costs such as hospitalization, is through borrowing, but this avenue is also likely to be of limited help to many uninsured families. The large share of families with lower incomes have a limited ability to pay off loans from future income. Because they do not have significant assets, they cannot offer such assets as security to a lender. Families who own their own homes have their home equity as a resource for meeting health care expenses, but uninsured families are less likely to be homeowners. In 1987, half of the families in which some or all members did not have health insurance were homeowners, compared to two-thirds of families of all types and ages in which everyone had health insurance (Miller, 1990). Low income and very limited assets and borrowing capacity are all indicators of poverty among uninsured families (see Box 4.2).

|

BOX 4.2 Poverty Standards

|

HEALTH SERVICES COSTS FOR UNINSURED FAMILIES

Finding: On average, families with some or all members uninsured spend less on health care in absolute dollars than do families with all members covered by private insurance and they use fewer services. Paradoxically, families with uninsured members are more likely to have higher health expenditures as a proportion of family income than are insured families.

One reason that uninsured families have lower health spending than insured families is because they use fewer health services on average. An examination of family spending patterns of those with and without health insurance provides an indication of how the uninsured family might accommodate health bills and the costs of purchasing insurance.

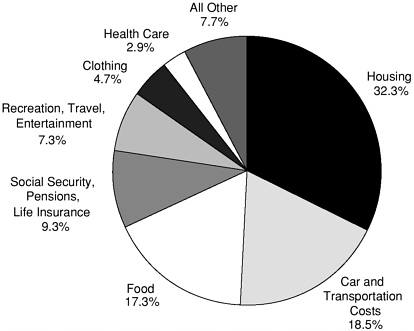

Across households, regardless of insurance status, housing is the largest expenditure, transportation (primarily automobile ownership and operation) the second largest, and food eaten at home the third.5 These three basic necessities accounted for 59 percent of consumption for fully insured families and 64 percent for uninsured families. In terms of absolute dollars spent for these three purposes, fully insured families spend more than families with no insurance (Paulin and Weber, 1995). After spending for housing, transportation, and food, uninsured families spend both a smaller percentage of income and fewer dollars on other items compared to insured families. Among all uninsured families, those in the lowest quartile based on total spending use their “extra” money (not spent on insurance premiums) for more or better food at home and housing, while those in the top quartile spend their “extra” money across all expenditure categories, not just necessities (Levy and DeLiere, 2002). Figure 4.2 shows the average annual expenditures of families with no members insured and the share they spent on different consumption categories in 1993. Their health spending was 3 percent of total spending. In 2000, the median income for a two-parent family with neither parent insured was $30,000. If such a family spent 3 percent of income on health, it would have health expenditures of roughly $900.

Forty-three (43) percent of working-age adults without health insurance and 31 percent of those currently insured but recently uninsured report that in the past year they did not seek a physician’s care when they had had a medical problem, compared to 10 percent of those who were insured all year. In families with incomes below $35,000, 40 percent of those without insurance went without a doctor’s visit when sick, compared to less than 10 percent of those with coverage

FIGURE 4.2 Spending in families with no members insured.

NOTE: Expenditure units include single people.

SOURCE: Data from 1993 Consumer Expenditure Survey in Paulin and Weber, 1995.

(Duchon et al., 2001). Fifteen (15) percent of uninsured adults reported being unable to pay for basic necessities because of medical bills (Duchon et al., 2001).

Utilization differs between insured and uninsured children. Children who were uninsured for all of 1996 were less likely to use any health care services than were those with insurance, particularly office visits, dental visits and prescription medicines (see Table 4.1 and Box 4.3). Utilization by insured adults also tends to be higher than that by uninsured persons (IOM, 2002a). While the greater use by insured people may be for needed and appropriate services and the uninsured may be lacking needed care, it is also possible that some of the increased care for those with insurance may be unnecessary and contribute to excessive costs.

Average health care expenditures of uninsured families are lower than those of insured families because there are disproportionately more uninsured families with no or very limited use of services. However, uninsured families with health problems requiring care are more likely to find themselves at the other end of the spending spectrum with out-of-pocket costs that can be very large. One example comes from a study of uninsured people between ages 51 and 61 who experienced the onset of cancer, heart conditions, stroke, or lung disease.6 In that group, half

TABLE 4.1 Children Age ≤ 17 Using No Health Care Services, 1996

|

|

Percentages |

|||||

|

Hospital Inpatient |

Hospital Outpatient |

Hospital Emergency Department |

Office Visits |

Dental Visits |

Prescription Medicines |

|

|

Any private |

97.6 |

92.2 |

87.5 |

23.8 |

49.9 |

38.6 |

|

Public only |

94.6 |

92.7 |

84.5 |

33.2 |

71.4 |

44.0 |

|

Uninsured |

98.1 |

96.3 |

89.2 |

49.3 |

79.3 |

57.2 |

|

SOURCE: MEPS 1996 data in McCormick et al., 2001. |

||||||

|

BOX 4.3 What Counts as an Expense for Health Care Services? The most comprehensive data on who uses what health care services and how much is paid for those services comes from the Medical Expenditure Panel Survey (MEPS). MEPS began in 1996 and is ongoing. Similar surveys in earlier years were the National Medical Care Expenditure Survey (NMCES) in 1977 and the National Medical Expenditure Survey (NMES) in 1987. The data presented in this chapter on who pays how much for health care are derived from MEPS. In the MEPS, an expenditure is what is paid for health care services. Total expenditures are the sum of amounts that patients and their families pay out-of-pocket and payments by private insurance, Medicaid, Medicare, and other sources. Payments for over-the-counter drugs such as aspirin or cold remedies and for alternative care services such as massage or homeopathy are not included. This definition of expenditure requires someone to make a payment in order for a medical service to generate an expenditure. Amounts that are not collected from patients, including both bad debt and charitable care, are not counted as expenditures because no payment has been made, even though a provider may have incurred some cost to provide those services. An exception is made for public clinics and hospitals. For those settings, amounts are counted toward expenditures even in the cases where no one makes a payment for a service. The payment-based definition of expenditure is a change from the 1977 and 1987 surveys, in which the definition of an expenditure was tied to a provider’s cost rather than the payment the provider received. The 1996 definition is more useful for this report, which examines health expenditures from the perspective of the family, but it does not give a complete picture of the value of services rendered from the health care provider’s perspective. |

had out-of-pocket costs below $1,060 over a two-year period; 1 in 10 had out-of-pocket payments that exceeded $16,500, 1 in 20 had payments that exceeded $30,500, and at the very top, 1 in 50 paid more than $64,700 out-of-pocket over the two years (Smith, 1999).

Unless a new health condition is disabling, even persons with large health expenses are unlikely to qualify for Medicaid unless they have a very low income and meet other eligibility criteria. Among families with uninsured members who are eligible to enroll in Medicaid but who are not enrolled (primarily families with children), out-of-pocket costs could be reduced if eligible family members enrolled. As noted in Chapter 2, most uninsured children are eligible for Medicaid and SCHIP but are not enrolled. Almost 85 percent of Medicaid-eligible uninsured children live in families that have some health care costs; in 1993 and 1994, 29 percent had out-of-pocket expenses greater than $500 (Davidoff et al., 2000a). An analysis of the 1997 National Health Interview Survey shows that only about half of Medicaid-eligible working-age adults are enrolled and more than a quarter remain uninsured. Those families with an uninsured adult are twice as likely to report out-of-pocket spending of between $500 and $2,000 as are families of Medicaid-enrolled adults, 21 percent and 10 percent, respectively (Davidoff et al., 2001a).

Among all individuals under age 65, the average out-of-pocket cost in 1996 was lower for persons who did not have health insurance ($253) than for those who had private insurance ($326), including costs of the latter that some would view as examples of underinsurance.7 Among those who actually used any health care service and paid for it out-of-pocket, however, the difference in mean levels of expense paid out of pocket is roughly the same for insured and uninsured patients (around $400) (Taylor et al., 2001a). Although those with health insurance had some expenses covered by their plan, their out-of-pocket expenses were about the same as those of uninsured persons because, on average, insured people use more services.

Lack of insurance affects the health care costs of uninsured families in another way. Insurance plans serve a less obvious purpose of negotiating competitive prices with providers of services. Uninsured families do not enjoy the agency of a large insurer or managed care company when they pay for their own care. Thus uninsured persons may be charged and pay a higher price for the same service than the price paid by an insurer on behalf of an enrollee. Anecdotal evidence suggests that the prices providers charge the uninsured can be two to three times the payment amount negotiated by insurers on behalf of the privately insured (Wielawski, 2000; Kolata, 2001). This pricing practice can affect both the out-of-pocket expenses a family pays for services used by an uninsured member and the amount of debt resulting if the uninsured family cannot pay the full amount

charged. This practice also affects the amounts paid by other sources on behalf of uninsured medically indigent patients.

Finding: Most uninsured families would not have sufficient funds in their budget to purchase health insurance without a substantial premium subsidy.

The primary reason that uninsured families spend a smaller share of their family budget on health is that they do not pay for health insurance (Acs and Sabelhaus, 1995). Surveys show that the most common reason given for not being insured is the perceived unaffordability of the premium (Thorpe and Florence, 1999; Orne et al., 2000). This section shows how purchasing health insurance would affect the budget of the typical uninsured family.

Determining the cost of purchasing private health insurance other than an employment-based group plan is not easy. A wide range of plans and premiums are available, with substantial variation in benefits covered and cost sharing required, including copayments and deductibles. In addition, an individual’s age and medical condition will affect whether the person can get coverage at all and, if so, at what price and whether certain conditions are excluded from coverage. Given all these variables affecting the cost of independently purchased insurance and a lack of comprehensive data, it is impossible to put a specific price tag on an average policy. However, a 1999 study of web-marketed policies available in 15 major cities reports a median premium for a plan with a $250 deductible of $1,700 for a 25-year-old and $5,700 for a 60-year-old (Simantov et al., 2001). With a deductible of $1,000, the median premiums for a 25-year-old and 60-year-old were $1,100 and $4,000, respectively. A related survey of 1,500 people aged 50– 64 reports that half of those with individually purchased coverage for a single person paid more than $3,500 in premiums and out-of-pocket expenses, compared with 17 percent of those in employment-based plans who had that level of expenses. A policy with terms similar to those in a group plan would likely cost more if purchased independently, however, because of the higher administrative costs and greater risks faced by the insurer.

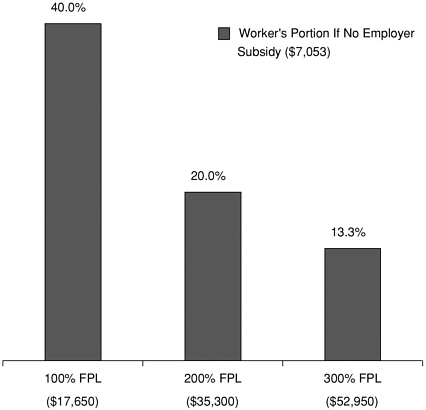

Figure 4.3 shows the relationship between the cost of employment-based health insurance and income for a four-person family. For the cost of insurance, the figure uses the cost for the average employment-based health plan. At the 2001 FPL of $17,650 for a four-person family, the full premium represents 40 percent of income, a larger share than either food or shelter typically consumes. Individuals who sought to purchase that average plan on their own would likely pay even more; they might also seek to reduce their costs by purchasing a plan with less generous benefits and greater out-of-pocket costs than provided in the average employment-based plan. In any case, the family that purchases coverage outside employment would lose the tax advantage that comes from not paying income tax on the employer contribution, which averages 73 percent of the total premium for family coverage (Kaiser-HRET, 2001). If a middle-income family received the employer’s share of the insurance premium as income instead of a health benefit,

FIGURE 4.3 Share of a four-person family’s income compared to premium costs to purchase family coverage in 2001.

SOURCE: Kaiser-HRET, 2001.

it would owe taxes of about 15 percent on the Federal Insurance Contributions Act (FICA) for Social Security and Medicare and 28 percent on federal income tax.

At the median income of families in which neither parent has health insurance ($30,000 in 2000, Figure 4.1) the annual cost of a typical plan would have required that more than one-fifth of family income be devoted to health insurance. Among single-parent families where the parent did not have health insurance, the median income in 2000 was $14,280, and the typical plan would have required almost half of the family’s income. If a family were to spend that amount on health insurance, its remaining income would place the family below the poverty threshold (Kaiser-HRET, 2001).

Affordability of health insurance can also be evaluated in terms of a “minimally adequate” family budget. In contrast to the “privation” standard of the poverty threshold, assessments based on family budgets have tried to estimate the amount of income that provides for a modest standard of living, one that is more generous than that provided by the poverty threshold and that reflects the variety

of goods and services a family typically buys.8 Such a “basic needs” budget that included costs for housing, transportation, food, health care, telephone service, and taxes, using prices in Baltimore as a reference amount, was estimated to be $34,732 for a family of four in 1998. This amount is twice the poverty threshold for the same size family. Still, a family with an income below the basic needs level must do without or with fewer of the things than most families have. This budget includes $3,200 for employment-based health insurance and out-of-pocket expenses, based on typical costs for a family of this size. In this basic needs budget, health care amounts to 9.2 percent of a family’s spending (Bernstein et al., 2000). This contrasts sharply with the 21 percent of family income cited above as being required just to purchase private health insurance for a non-insured family having a median income of $30,000 per year. Uncovered out-of-pocket health expenses for such a family would be an additional expense.

FINANCIAL BURDEN OF HEALTH CARE COSTS FOR UNINSURED FAMILIES AND HOW THESE FAMILIES COPE

The average levels of health care expenditures faced by uninsured families cited above mask a high variation in such costs. Lack of insurance exposes the uninsured to the financial risks represented by this high variation. Most vulnerable, clearly, are uninsured families in which one or more members have significant needs for health care.

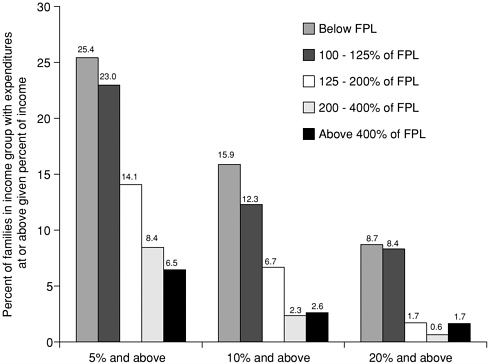

Finding: Among families with no health insurance the entire year and incomes at or below the poverty level, more than one in four have out-of-pocket expenses that exceed 5 percent of income. Among all uninsured families, 4 percent have expenses that exceed 20 percent of annual income.

Low-income families with no members insured for the full year are at greater risk of incurring high medical expenses (greater than 5 percent of income) than are totally uninsured families with higher incomes (Taylor et al., 2001b). Regardless of income, 4 percent of uninsured families experience exceedingly high medical expenses (greater than 20 percent of income) (Taylor et al., 2001a). Having some insurance in the family for at least part of the year tends to reduce the risk of high expenditures relative to income. Families with some members insured and others uninsured are somewhat more likely to have out-of-pocket costs for medical services that exceed 5 percent of income in a year than are families with all

members insured (Table 4.2). Families with no members insured at any time in the year are almost twice as likely as those with all members insured for the full year to exceed the 5 percent threshold. Insurance offers protection against large, unpredictable expenses. The higher the threshold, the higher must a family’s expenses relative to income be to exceed the threshold. Families without health insurance will be at greater risk than insured families of exceeding each higher threshold. Families with some insurance, either for some members or for some part of the year, are 1.5 times as likely to exceed the 10 percent threshold as fully insured families, and families in which no one has health insurance are 2.7 times as likely to have out-of-pocket costs exceeding 10 percent of family income. Table 4.3 provides a finer breakdown of out-of-pocket expenses among uninsured families of different types and shows that those who are uninsured for the full year are more likely to have no expenses during the year than are those families insured for part of the year. That is true whether the uninsured families are single- or two-parent or a single person or couple with no children at home. However, families uninsured for the full year are also more likely to have expenditures that exceed 5 percent of income than are those that are uninsured for part of the year.

Health care expenses in a year equal a small proportion of income for many families but a large proportion for a small share of families (Table 4.3). A majority of families, whether their members were with or without health insurance, have medical expenses that are less than 2 percent of income.

Lower incomes, poorer health, and lack of health insurance interact to create financial hardship. For example, a person with serious health problems may have difficulty holding a job, particularly one that would offer health benefits. Such an individual would also be more likely to have trouble obtaining coverage independently because of underwriting practices. The health problem could result in both a limited income and many health bills. Being uninsured is associated with poor health and financial problems paying bills, but the causal relationships are unclear.

TABLE 4.2 Out-of-Pocket Expenses as Percent of Family Income, by Insurance Coverage and Duration, Non-Medicare Families, 1996a

TABLE 4.3 Out-of-Pocket Health Care Expense as a Share of Income, by Family Type and Insurance Status, 1996a

A recent national survey of working-age Americans reports that 55 percent of those who were currently or recently uninsured had problems paying medical bills and about three in ten of those uninsured report needing to change their way of life in order to pay medical bills (see Box 4.4 for a description of procedures used for collecting medical bills). Only one-quarter of insured adults had problems paying medical bills and one-tenth of insured adults had to change their life-style (Duchon et al., 2001).9

|

BOX 4.4 Collections Procedures for Medical Bills If a family experiences difficulty paying a bill for medical services promptly, it may also experience one or more common collection procedures. Standard references for hospital financial administrators suggest they use collection agencies to pursue debt (Herkimer, 1993). More than a third of uninsured adults in a national survey reported being contacted by a bill collector for payment of medical bills (Duchon et al., 2001). The process used to collect debt is regulated by the Fair Debt Collection Practices Act (15 U.S.C. § 1692) The act allows collection efforts by writing letters or making phone calls but forbids certain abusive practices such as using obscene language and threatening personal harm. Even if a health care provider does write off a bill as a bad debt a family could still face adverse effects if the provider reported the debt to a credit reporting agency. Credit agencies can continue to report the bad debt for seven years (Federal Trade Commission, 1999), thus affecting the family’s credit rating for many years. |

For families without health insurance the burden of out-of-pocket expenditures falls as income rises (Figure 4.4). Among all types of families and singles, those who live in families with low incomes are more likely to be burdened by health care expenses. The burden is also greater for families with poorer health (Taylor et al., 2001b). Among all families in which no members are insured, twice as many families report no out-of-pocket expenses when the household head reports his or her health as good or better, as when the family head reports fair or poor health (23 compared to 12 percent). Less than half as many are likely to have out-of-pocket expenses that exceed 5 percent of family income (13 percent where the household head has good or excellent health compared to 34 percent where the household head reports fair or poor health) (Taylor et al., 2001b).

The degree to which high out-of-pocket expenses persist year after year affects the strategies a family can use to meet high costs. Borrowing or using available savings might be feasible if high costs are a one-time event, but if high costs are ongoing they must be offset by reducing other spending. No currently available survey provides the data to determine what share of uninsured families face high out-of-pocket expenses year after year. The overlap in the sample between the 1996 and 1997 rounds of the Medical Expenditure Panel Survey (MEPS) does shed some light on the extent to which high costs persist over two years. Among all non-Medicare families, 17 percent (whether insured or not) experienced high out-of-pocket costs (more than 5 percent of income) in either of 1996 or 1997, and of these, one in five had high costs in both years (Merlis, 2001).

FIGURE 4.4 Uninsured families with high medical expenses, by poverty level, 1996.

NOTE: The dollar level of health expenditures required to reach 5 percent of income varies by family income. The 1996 FPL for a family of four was $15,600, 5 percent of expenditures at a family income of 100 percent FPL is $780; and at a family income of 400 percent FPL is $3,120.

SOURCE: Tabulations from the 1996 Medical Expenditure Panel Survey (MEPS), Center for Cost and Financing Studies, Agency for Healthcare Research and Quality, Taylor et al., 2001b.

How Uninsured Families Cope with the Financial Burden of Medical Expenses Borrowing

The Committee has noted earlier in this chapter that uninsured families typically have low borrowing power. Still, some do manage to borrow. A recent national phone survey of working-age adults reports that among uninsured people, almost 20 percent used all or most of their savings, 17 percent borrowed from family or friends, and 7 percent reported needing a loan or mortgage on their home in order to pay medical bills (Duchon et al., 2001).

The growing availability of credit cards provides another way for the uninsured to pay medical bills but at a very high cost in terms of interest. A family might use cash to pay health care bills and credit cards to purchase things that otherwise would have been purchased with cash. Alternatively, the family may make pay-

ment to a health care provider with a credit card. The debt arises as a result of health care expenses but would appear on a listing of family assets and liabilities as credit card debt. Thus, the extent to which medical expenses contribute to debt remains hidden, but some researchers consider it to be significant for middle-class families (Sullivan et al., 2000).

Declaring Bankruptcy

For some in financial stress, bankruptcy may be perceived as an option. The 1.5 million personal bankruptcy filings in 2001 were five times the level of a generation earlier (Administrative Office of the U.S. Courts, 2002). Bankruptcy is often described as a response by financially stressed families to some adverse event—losing a job, being sick, or becoming divorced (Stanley and Girth, 1971; Sullivan et al., 2000). Bankruptcy gives a “fresh start” to debtors, because many but not all unsecured debts can be discharged in bankruptcy. The largest class of unsecured debt for individuals is credit card debt.10

The most direct evidence on the relationship of bankruptcy and health insurance comes from a survey of almost 1,500 cases involving about 2,000 debtors in bankruptcy courts across eight judicial districts that asked if any family member did not have health insurance. Twenty-one (21) percent reported that no family members had health insurance (Jacoby et al., 2000). The survey did not ascertain whether an individual was without health insurance at the time of the survey or at the time the medical debt was incurred. The same survey of bankruptcy filers found medical problems associated with nearly half of all bankruptcies.11 Those with no health insurance in their families do not disproportionately cite medical problems. Thus, it is difficult to determine from this survey what causal relationship may exist between being uninsured and bankruptcy.

The bankruptcy filings by some who are without health insurance may be attributed to high out-of-pocket medical expenses. While there is evidence that those who have medical debts that exceed 2 percent of income are far more likely to file for bankruptcy, it is not known what share of those who have high medical debts are currently uninsured or were uninsured at the time they incurred the debt (Domowitz and Sartain, 1999). None of the current surveys of nationally representative samples provide the detail about medical expenses, insurance status, and financial circumstances to illuminate how families with high out-of-pocket medical expenses deal with these costs. The relationship of high medical expenses and forms of financial stress such as bankruptcy is not clear.

Other Sources of Payments for Family Health Expenses

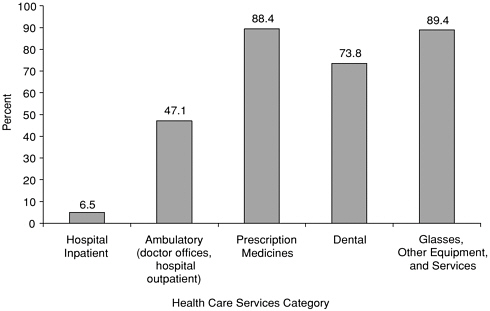

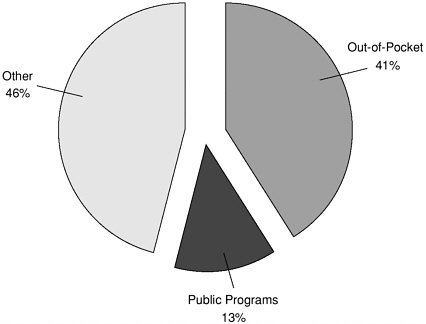

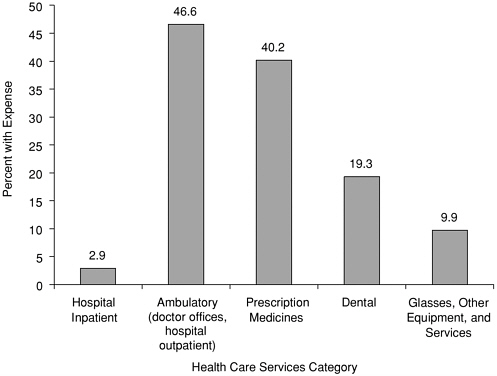

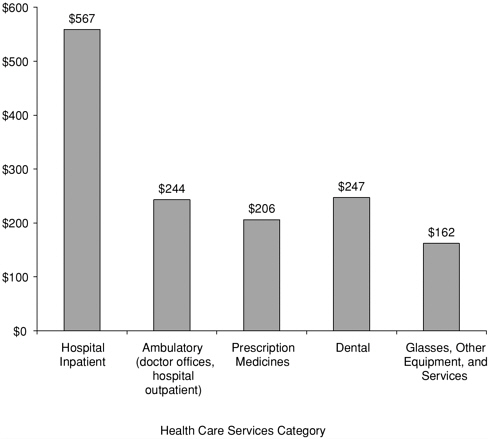

Not all health care expenses incurred by uninsured persons are borne by family budgets. Uninsured family budgets absorb 41 percent of total family health care expenses, but this varies by type of service; families pay for between 7 percent (hospital inpatient services) and 89 percent (glasses, other equipment, and services) of particular categories of service (see Figures 4.5 and 4.6). For example, while the average percentage paid out of pocket by uninsured families for a hospital stay is almost 7 percent (Figure 4.5), very few uninsured people under age 65 experience a hospitalization. Almost 3 percent of uninsured individuals have an inpatient expense (see Figure 4.7), and the average out-of-pocket amount paid by them is $567 (see Figure 4.8).

Apart from family spending, medical expenses for persons without health insurance are met by other forms of insurance such as automobile insurance and workers’ compensation; public support for public hospitals, clinics, and community health centers; and philanthropy and provider sources.

Fifty-eight (58) percent of expenses for uninsured children are paid out of pocket (McCormick et al., 2001). In part, the larger share paid out of pocket for children reflects the fact that hospital services, where support from sources outside family budgets is greatest, are a smaller share of children’s use of services than adults’ use.

FIGURE 4.5 Share paid out-of-pocket by uninsured persons under age 65, within each type of service, 1997.

SOURCE: Data from Medical Expenditure Panel Survey in Agency for Healthcare Research and Quality, 2001a.

FIGURE 4.6 Sources of payment for expenses of the uninsured, 1997.

NOTE: Public programs exclude Medicare and Medicaid. They include state and local payments for clinics, health departments, and other programs and at the federal level some payments by the Department of Veteran Affairs, Indian Health Service, military treatment facilities, and other federally provided care. SOURCE: Data from Medical Expenditure Panel Survey in Agency for Healthcare Research and Quality, 2001b.

Prescription medicines and medical supplies receive the least external support, and the family’s share of those expenses is greater than for other services. Almost as large a share of the uninsured had expenses for prescription medicines as had outpatient expenses in 1997 (40 percent compared with 47 percent) (Figure 4.7). Prescription expenditures were less than half those of outpatient costs among those who had any costs (mean of $517 for outpatient costs and $233 for prescription medicines; median of $164 for outpatient costs and $58 for prescription medicines). Despite the higher cost of outpatient services, average out-of-pocket payments for uninsured persons were nearly the same for these services, about $200 (Figure 4.8). The relative lack of subsidies for prescription drug costs, only 7 percent of expenses, largely accounted for an equal out-of-pocket burden from two categories so different in total expense (AHRQ, 2001a).

Hospital Care

A health event that requires an inpatient hospital stay leads to significant expense. Among those without health insurance who had a hospital stay in 1997, the average amount paid by all sources was $8,730 for the stay. However, just 6.5

percent ($567, on average) was paid by the uninsured or their families. About one-fifth (22 percent) came from government programs (other than Medicare and Medicaid) such as local programs to make payments for uncompensated care and services provided by the Department of Veterans Affairs. The largest share (72 percent) came from payments from other forms of insurance such as workers’ compensation and automobile accident insurance and as hospital charity care. (MEPS counts uncompensated care as expenses when provided by public hospitals [AHRQ, 2001a]). The hospital sector differs from other providers of health care used by those without health insurance. Under the Emergency Medical Treatment and Active Labor Act (EMTALA), hospitals with emergency departments are required to provide treatment to patients needing emergency care whether they are insured or not.12 Many hospitals, particularly those that are public or not for profit have as part of their mission serving uninsured patients. Regardless of ownership status, however, accounting standards require hospitals to have a standard set of procedures to decide who qualifies for charity care (Box 4.5).

Hospital inpatient stays and resulting out-of-pocket payments are comparatively infrequent; only 3 percent of those who were uninsured throughout the year had expenses for hospital inpatient stays in 1997 (Figure 4.7). Expenses for ambulatory services, including services provided in hospital outpatient departments, the area of a hospital that includes emergency departments and physician offices, are more common and account for a much larger share of the amount families with uninsured members pay from their own pockets. Almost half of uninsured people had expenses for ambulatory services in 1997. The average amount paid by families was $244 (see Figure 4.8).

Outside Supports, Trade-offs, Fairness, and Accountability

Because uninsured people do not bear all the costs of their care, the existence of outside financial support and the availability of services rendered at no or reduced charge enters the calculus for uninsured families when they weigh the value of insurance against competing demands on the family budget. Many of the largest financial risks families face from being without health insurance may be mitigated by a patchwork of arrangements involving trading off inconvenience or loss of dignity for avoidance of financial harm (Collins et al., 2002; Doty and Ives, 2002; Hughes, 2002). However, if families without health insurance have the resources and choose to buy insurance, they may lose access to these supports and face paying more in total (including premiums, copayments, and deductibles) for health care than they had previously. The greater financial cost of having health

FIGURE 4.7 Share with expense in the service category, full-year uninsured individuals under age 65, 1997.

SOURCE: Data from Medical Expenditure Panel Survey in Agency for Healthcare Research and Quality, 2001a.

insurance creates a dilemma both for persons without health insurance and for a society that cares enough about those who do not have health insurance to not withhold all health care services from those who cannot pay for all services they receive (Coate, 1995). This conundrum will be examined further in the Committee’s next report, which addresses community-wide impacts of uninsurance.

There are two issues related to the provision of financial support for families facing large medical expenses: (1) how to promote consistency and fairness across similar situations, and (2) how to ensure documentation of and accounting for what is spent. Laws and regulations ensure that the federal tax code treats families in similar circumstances the same way. Medicaid law and regulations at the federal level provide some consistency in establishing an eligibility floor while allowing considerable variability among states in the upper limits of eligibility and benefits. The financial support that uninsured families receive, most notably from hospitals, cannot be described by a set of rules and regulations to ensure that similarly situated persons are treated equally regardless of the institution where they are served. Likewise, physicians’ provision of free or reduced-cost care to uninsured

FIGURE 4.8 Mean out-of-pocket expense among uninsured persons with expense, in the service category, full-year uninsured individuals under age 65, 1997.

SOURCE: Data from Medical Expenditure Panel Survey in Agency for Healthcare Research and Quality, 2001a.

patients varies among practitioners and across communities (Cunningham et al., 1999). Data concerning bad debt and free care are very limited, particularly for health service providers other than hospitals.

Unlike assistance to families through Medicaid and the tax code, much of the financial support received by uninsured patients directly from providers of services and from charitable organizations is hard to document and quantify. The assistance is generally not allocated through a public or transparent process, and there are no consistent rules for reporting the costs. One year’s data from seven hospitals in one state suggest that financial assistance from hospital decisions to offer charity care and write off bad debt flows to those with lowest income (Weissman et al., 1999). Eighty percent of the cost of free care went to individuals from families with incomes below the poverty threshold; another ten percent went to individuals with family incomes between the poverty threshold and twice the threshold.

|

BOX 4.5 How Do Hospitals and Community Health Centers Handle Uninsured Families and Bill for Care? Few generalizations are possible about what a person without health insurance can expect when seeking care. Some providers may be willing to offer services at a reduced price; others may not. Some hospitals may defer elective admissions until a financial plan for payment has been agreed upon. Some people without health insurance will find they are required to pay cash up front. Others without financial resources may be denied care. The American Institute of Certified Public Accountants’ audit and accounting guide requires hospitals to establish billing and collections policies to determine the circumstances under which uncompensated care is considered charity care. While data are limited on the nature of such policies, the Committee notes the following widely varying practices:

|

Families with incomes below the poverty threshold also accounted for two-thirds of the bad debt dollars written off. Even after the debt is written off by the hospital or other provider, a family may still lose its credit rating if the debt is reported to a credit bureau (see Box 4.4).

SUMMARY

Uninsured families are more likely to face high medical bills with less income, savings, and other assets than are insured families (see Box 4.6). Managing without health insurance is part of a broader experience for uninsured families of managing with fewer resources in general. Their choices are constrained and their limited resources may be a contributing factor to their lack of coverage. If workers are not offered heavily subsidized health insurance with their job (often the case for lower wage workers), it is unlikely that they would be able to afford to purchase a plan independently for themselves and their dependents. The Committee has shown that most uninsured families have little leeway in their budgets to accommodate payments for an insurance premium, given the relatively high costs of coverage. Such families could face difficulties with even routine medical bills; a major hospitalization or chronic condition requiring frequent medical services might easily destabilize them.

The evidence shows that uninsured families do not use the health system to the same extent that insured families do. This means that the children are less likely to see a doctor, receive hospital outpatient or emergency care, visit a dentist,

|

BOX 4.6 Summary of Findings

|

or receive prescription medicines than are children who are privately insured or covered by public programs. Also, proportionally more uninsured families record no medical expenses during the year than do insured families. Limiting purchases is a common way for families to survive with reduced resources, but using health care is sometimes unavoidable and families may suffer ill effects when their members do not receive timely, appropriate care. Chapter 6 details the consequences for children and pregnant women of delaying care and not maintaining contact with a routine source of care.

Even though uninsured families are more likely than their insured counterparts to have no medical expenses, those at the other end of the spending spectrum who cannot avoid using services, are also more likely to have burdensome medical expenses of more than 5 percent of family income. The extent to which uninsured families resort to borrowing and filing for bankruptcy compared to insured families cannot be readily determined. It is clear, however, that high medical bills can cause problems for families with health insurance as well as for those without. It is unknown how many more uninsured families would face high levels of expenditures if it were not for the availability of subsidized care and the use of safety-net providers. These external supports exist to assist uninsured families; it is not clear how many families may benefit from them, or to what extent, and how many do not have these options or choose not to use them.

There is much that we do not fully understand about the interaction of economic and health pressures on families and what influences how they respond. It is an area ripe for further inquiry.