6

Employers and Business

The main function of American employers is the production and sale or direct provision of goods and services. Through these economic activities, employers provide jobs and incomes to America’s families. As noted in Chapter 2, employment and the workplace are important determinants of health that can generate protective health effects through income and social ties as well as adverse health effects (i.e., poor work conditions and job strain). This chapter provides information regarding the ways in which employers (both public and private), as actors in the public health system, can make important contributions to the health of the population through activities that are specifically directed toward health concerns.

The chapter begins with a discussion of how American employers, as providers of health care benefits to their employees, contribute significantly to supporting the conditions for health of a large proportion of American workers and their dependents. The discussion then addresses the important role that employers play in ensuring quality and accountability for the health care services purchased by and for their employees. The chapter then discusses the rationale for employer investment in the health of employees and how sponsoring health promotion and disease prevention activities in the workplace and improving workplace conditions promote employee health. Finally, the chapter ends with a discussion of a range of health-promoting activities—lessening environmental pollution and involvement in civic activities in the community, for example—in which employers and the business sector at large can engage to help promote the health of the population.

EMPLOYERS’ ROLE IN HEALTH INSURANCE COVERAGE

Employers make a major contribution to population health and health security because of the important role they play in providing health insurance. Employers are primarily motivated to offer health insurance benefits to recruit and retain employees and to be competitive in the marketplace. Employees value health insurance and benefits and the opportunity to extend such coverage to their dependents.

For a number of historical reasons, employment is the foundation of the private health insurance system in the United States. Ninety percent of persons under the age of 65 who are privately insured obtain their health insurance through employers. Voluntary employer-sponsored health insurance is offered to employees and their dependents as part of a typical compensation package. In 2002, 62 percent of all firms (including both public and private employers) offered health benefits to their employees, a decline from a high of 67 percent in 2000 (Kaiser Family Foundation, 2002).

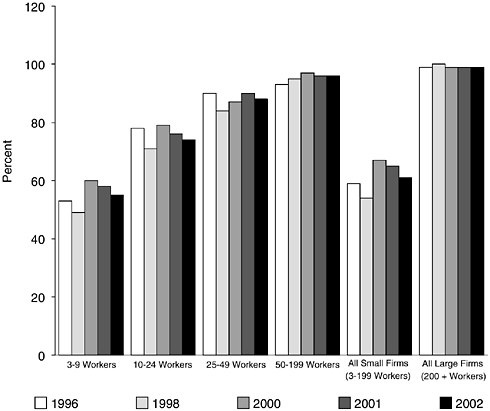

The percentage of firms offering health benefits varies by the size of the firm. For example, in 2002, 99 percent of firms with more than 200 workers offered health benefits to their employees, whereas less than 61 percent of small firms (those with 3 to 199 employees) offered such benefits (see Figure 6–1) (Kaiser Family Foundation, 2002).

Small firms are less likely to offer health insurance for a number of reasons, including the increased cost of a comparable insurance package because of higher administrative costs, lower employee wages, and more part-time workers (Custer and Ketsche, 2000).

Employees place a high value on health insurance. According to the Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc.’s Value of Benefits Survey, 60 percent of employees rank health insurance as the most important benefit. Employees also report that benefits (e.g., health insurance and retirement plans) continue to be a very important factor in job selection (EBRI, 2002; Lave et al., 1999; Peele et al., 2000).

Most employers (both private and public) believe that they play an important role in providing health insurance coverage and that they can provide better coverage than employees could buy on their own. However, changing economic pressures are causing employers, particularly private firms, to reconsider the nature of their health insurance offerings. Pressures resulting from the slowing of the U.S. economy, rising health care costs associated in part with increasingly looser forms of managed care, rising prescription drug prices, and employee demands are making it more difficult for small employers to offer insurance coverage and for large employers to maintain premiums at affordable levels (Custer and Ketsche, 2000; Lambrew, 2001; Kaiser Family Foundation, 2002). Data indicate that pre-

FIGURE 6–1 Percentage of firms offering health benefits, by firm size, 1996– 2001.

NOTE: Nationwide, there are an estimated 5,355,412 firms with 3 to 199 workers and 86,957 with 200 plus workers. Firms include both public and private employers.

SOURCES: Kaiser Family Foundation (2000, 2001, 2002); KPMG (1996, 1998).

miums have already begun to rise. Premiums for employer-based health insurance increased an average of 11 percent in 2001, the largest increase since 1992. Large employers faced, on average, a 10.2 percent increase in health insurance costs, whereas the smallest employers (those with three to nine employees) experienced an average increase in premiums of 16.5 percent (Kaiser Family Foundation, 2002). As their costs rise, many employers expect to ask employees to pay more for insurance in the years to come and to pay for a higher proportion of the costs of care in terms of higher deductibles or copayments when they actually use services.

Increasing health insurance premiums influence whether an employee (as well as dependents) has coverage or joins the ranks of the uninsured. Employees typically pay between one-quarter and one-third of the total

cost of the insurance premium, in addition to deductibles, copayments, and the costs of health services that are not covered or that are covered only in part. The proportion of employees who choose to participate in employer-sponsored health insurance is inversely related to the employee’s contribution to the cost. The expense and competing demands on family income are the main reasons individuals report for declining an offer of employment-based coverage (Cooper and Schone, 1997; Rowland et al., 1998; Hoffman and Schlobohm, 2000). Individuals who decline employer-based health insurance are typically covered through a spouse or some other type of coverage, and about 4 percent remain uninsured. The consequences of being uninsured are described in Chapter 5 and in past reports of the Institute of Medicine (IOM, 2001a, 2002).

EMPLOYERS’ ROLE IN ASSURING HEALTH CARE QUALITY

As purchasers for the health services of a large proportion of American families, the employer sector has an important role to play in ensuring the availability of high-quality health care services. Recent Institute of Medicine (IOM) reports have noted that the American health care delivery system is in need of fundamental change and that purchasers (employers and governmental agencies such as the Centers for Medicare and Medicaid Services) can play an important role in demanding health care services that are safe, effective, patient centered, timely, efficient, and equitable (IOM, 2001a).

Over the years, many employers (both private and public) have been strong partners of health plans and other health care organizations in efforts to improve health care quality. They were active participants in the National Committee for Quality Assurance initiative to develop the Health Plan Employer Data and Information Set in the early 1990s. The data set attempts to standardize a process for assessing and comparing health plan performance so that purchasers and consumers have a better sense of the quality of services provided. Another partnership, the Washington Business Group on Health, has worked over the past 27 years with approximately 170 employer members to improve employee health and productivity through attention to employee mental health issues and clinical preventive service guidelines, among others.

More recently, the Leapfrog Group, founded in 1999 and composed of growing numbers of Fortune 500 companies and other large health care purchasers, has joined forces to “trigger a giant leap forward in quality, customer service and affordability of health care.” The two-pronged strategy to achieve this goal involves educating the public about patient safety and defining a set of purchasing principles designed to promote safety and increase the value of health care. Other employer-based initiatives include

the National Business Coalition on Health, a membership organization of nearly 85 employer-led coalitions representing more than 11,000 mid- and large-sized employers and approximately 21 million employees and their dependents. These coalitions have joined together to collectively purchase health care, to proactively challenge high costs and the inefficient delivery of health care, and to share information on quality. Through these efforts and others across the country, the business community can be proactive in shaping the health care delivery system and promoting quality.

Illustrations of other employment-based efforts to improve health care quality include specific activities of the California Public Employees Retirement System (CalPERS) and the Minnesota Health Plan Initiative to Improve Health Care. Many employer groups are also involved in prevention activities sponsored by the Partnership for Prevention, a national nonprofit organization dedicated to increasing the resources for and knowledge about effective disease prevention and health promotion policies and practices.

CalPERS is one of the oldest purchasing coalitions in the country, representing one-third of public agencies in California; it holds the purchasing power of more than 1 million people and $1.7 billion a year in premiums. CalPERS pioneered the use of patient satisfaction and medical quality reports to encourage the provision of high-quality medical care from its participating plans (CalPERS, 2002). The combination of consumerism and strong purchasing influence is working to help improve the quality of health care for CalPERS members.

In another pioneering move to improve health care quality, five health plans (HealthPartners, Blue Cross and Blue Shield of Minnesota, Medica, PreferredOne, and UCare Minnesota) covering the majority of Minnesota residents came together to endorse evidence-based standard treatments and prevention procedures. This was the first time that the majority of health plans in a state have collaborated around setting and adopting evidence-based standards. Under the auspices of the Institute for Clinical System Improvements, a not-for-profit corporation, physicians and other health care professionals reviewed the scientific evidence and recommended the best course of action for 50 health problems such as urinary tract infection, hypertension, diabetes, and lower back pain. The health plans believe that use of the treatment guidelines is responsive to the health care quality concerns raised by IOM (2001b) and will lead to improved and more consistent care across the state (Freudenheim, 2001).

Recognizing that employers often have a difficult time balancing decisions about which benefits to purchase for their employees, the Partnership for Prevention convened a 25-member advisory panel to provide guidance on the clinical and preventive services that provide the “best bang for the buck.” To begin, the panel—composed of public- and private-sector purchasers of care, health plan medical directors, state and local public health

officials, clinicians, and consumer advocates—identified 30 clinical and preventive services and groups of services recommended by the U.S. Preventive Services Task Force (USPSTF)1 for average-risk patients (AHRQ, 2002). The relative value of these services was then assessed on the basis of two dimensions: health impact and value. Health impact refers to the portion of disease, injury, and premature death that would be prevented if the service was delivered—that is, the clinical preventive burden. The value of the service refers to cost-effectiveness, in which the net cost of the service is compared to its health impact. Cost-effectiveness provides a standard measure for comparing services’ return on investment (ROI). The results of the assessment identified 14 services that employers may want to purchase to improve the delivery of clinical preventive services (see Box 6–1). The Partnership for Prevention has disseminated its results to employers through its publication Prevention Priorities: Employers’ Guide to the Highest Value Preventive Health Services (Partnership for Prevention, 2001b).

The committee acknowledges the crucial role that employers, particularly large employers, play in creating health security for millions of Americans as providers of employer-based health insurance coverage and purchasers of health care services. It also notes that, to the extent that the quality improvement activities lead to improvements in the processes of care, these improvements should benefit not only the employees of specific companies but all people who use the health care system.

In recent years, however, the current role of employer-sponsored health has been challenged. Some of the criticism points out that employers are under no legal mandate to offer health insurance and that the employer is an unstable source of insurance for some employees, particularly those who work for small firms or firms that hire a disproportionate number of low-income employees (Long and Marquis, 2001). Other criticism is directed at the employer’s “role” per se (Reinhardt, 1999). A number of critics have argued that the employer should be removed from these decisions and that the employee, not the employer, should make decisions about what type of insurance to hold (Gavora, 1997; American Medical Association, 1999; Health Policy Consensus Group, 1999). In addition, critics point out that although employees ultimately bear the cost of insurance through lower wages, they are not aware of the trade-offs that are being made between wages and benefits and are demanding more benefits (or resisting cost containment) because such benefits are viewed as being “free” (Pauly, 1986,

|

1 |

The USPSTF is a panel of independent experts in prevention and primary care tasked with identifying a core set of clinical preventive services known to improve health. The USPSTF recommendations are published in the Guide to Clinical Preventive Services, 2nd edition (U.S. Preventive Services Task Force, 1996), and most recent updated recommendations are available at www.ahrq.gov/clinic/uspstfix.htm. |

|

BOX 6–1 Priorities for Employers: Recommended Clinical Preventive Services with High Health Impact and Value

NOTE: DTP/DtaP = diphtheria, tetanus, pertussis/diphtheria, tetanus, acellular pertussis; FOBT = fecal occult blood testing; Hep B = hepatitis B; Hib =Haemophilus influenzae type b; IPV = poliovirus vaccine, inactivated; MMR = measles, mumps, rubella; PKU = phenylketonuria. SOURCE: Partnership for Prevention (2001a). |

1997). Furthermore, critics point out that employer-sponsored health insurance distorts the labor market by favoring large businesses over small ones, encourages employers to outsource certain workers, and affects workers’ decisions about work and retirement (Congressional Budget Office, 1994; Gruber and Madrian, 1996). These critics recommend changes in tax policy so that tax incentives for the purchase of health insurance would not favor employer-sponsored coverage (Pauly, 1986; Congressional Budget Office, 1994; Gruber and Madrian, 1996; Gavora, 1997; American Medical Association, 1999; Health Policy Consensus Group, 1999).

Until reforms are enacted to assure access to affordable health insurance for all Americans, the committee urges employers to continue to provide and improve health insurance coverage for their employees. Employers should endorse the purchase of evidence-based benefits and work diligently to ensure the quality of the services that they purchase. The committee recommends that the federal government develop programs to assist small employers and employers with low-wage workers to purchase health insurance at reasonable rates.

EMPLOYER INTEREST IN PROMOTING THE HEALTH OF EMPLOYEES: A RATIONALE FOR CORPORATE INVESTMENT IN HEALTH

Employers should be concerned about the health and well-being of their employees for a number of reasons. Healthy employees consume fewer benefits in the form of benefit payments for medical care, short- and long-term disability, and workers’ compensation. Furthermore, healthy employees are more productive than their nonhealthy counterparts because they are absent less often and are more focused on their tasks while at work.

Through health insurance premiums and self-insured plans, employers pay large sums of money for the treatment of diseases and disorders, many of which are lifestyle related and often preventable. The leading causes of death in the United States are heart disease, followed by cancer, stroke, chronic lower respiratory disease, accidents, diabetes, pneumonia/influenza, Alzheimer’s disease, nephritis, nephritic syndrome and nephrosis, and septicemia (NCHS, 2002). A significant proportion of some of these diseases and disorders can be attributed to lifestyle habits and behaviors. For example, one study suggests that about 57 percent of heart disease deaths, 37 percent of cancer cases, 50 percent of strokes, 60 percent of accidents, 23 percent of pneumonias, 34 percent of diabetes cases, 60 percent of suicides, and 70 percent of chronic liver disease and cirrhosis cases are related to habits and behavior (NCHS, 1999). In the case of cancer and cardiovascular disease, seven modifiable risk factors account for 23 and 65 percent of the cases of morbidity, respectively (Amler and Dull, 1987).

More than 10,000 peer-reviewed articles in scientific journals show a clear causal relationship between specific modifiable risk factors and adverse health consequences. The following modifiable risk factors increase rates of mortality, morbidity, disability, and, in many cases, productivity loss: tobacco use, alcohol and drug use, sedentary behavior, poor nutrition, being overweight, having elevated serum cholesterol levels and high blood pressure, exhibiting high levels of stress and hostility, a lack of social support networks, and having unsafe sex. About half of all deaths in the United States are attributable to nine modifiable risk factors, including tobacco use (Box 6–2), diet and activity patterns, alcohol use (Box 6–3), firearm use, sexual behavior, motor vehicle accidents, and illicit drug use (McGinnis and Foege, 1993). Tobacco use alone caused approximately 440,000 premature deaths annually from 1995 to 1999 (CDC, 2002).

A number of studies have presented information on the distribution of illnesses in different companies. In a comprehensive study of Fortune 500 companies, coronary artery disease was the most costly disease for employers and represented 6.72 percent of total payments (Goetzel et al., 2000). The annual mean payment for claims related to coronary artery disease was $4,639 per patient and more than double the average payment of $2,230

|

BOX 6–2 Smoke-Free Policies in the Workplace Tobacco use is the number one cause of preventable disease and death in the United States (DHHS, 2000). Private-sector restrictions on smoking in the workplace are effective strategies that can make a difference for a significant number of employees. A comprehensive review of workplace smoking policies from the National Cancer Institute’s tobacco use supplement to the Current Population Survey found that slightly more than 80 percent of workers are covered by an official workplace smoking policy; however, less than half are protected by smoking policies that prohibit smoking in both the work area and the public or common areas of the workplace (smoke-free policy). Furthermore, the study found that those workers who work indoors—an estimated 58 million Americans, 40 million of whom are nonsmokers—are not protected by a smoke-free workplace policy. These data suggest that access to smoke-free workplace environments could be improved (Gerlach et al., 1997). |

|

BOX 6–3 Creating Work Environments That Discourage Alcohol Misuse Drinking while at work and heavy drinking outside of work are a real headache for employers. Alcohol-related performance problems include absenteeism, tardiness, feeling ill at work, and sleeping. Alcohol misuse can undercut productivity (quality and quantity) and can aggravate problems between coworkers (Bernstein and Mahoney, 1989; Ames et al., 1997; Mangione et al., 1999). Health care costs for employees with alcohol problems are typically double those for other employees (Schneider Institute for Health Policy, 2001). Moreover, workers who drink even relatively small amounts of alcohol can raise the risk of alcohol-related death and injury in occupational accidents, especially if they drink before operating a vehicle (Partnership for Prevention, 2001a). In 1994, more than 8 percent of full-time workers (more than 6.5 million employees) engaged in heavy drinking, defined as five or more drinks on 5 or more days in the past 30 days. To stem the cost of lost productivity, work-site accidents, and excess health care because of alcohol and drug use, employers can do the following:

|

The U.S. Department of Labor’s Working Partners program offers resources to help employers develop drug and alcohol-free workplaces (Partnership for Prevention, 2001a). Promoting Mental Health in the Workplace The employer community can take active steps to ensure that employees with depression remain productive. Estimates show that the annual cost of depression in the United States due to work loss and work cutback reaches $33 billion (Greenberg et al., 1995). Evidence suggests that the gains in productivity from effective treatment for depression could far exceed the direct costs of treatment (Simon et al., 2001). Employers who cut back on mental health benefits face increased costs for non-mental health services and more sick days (Rosenheck et al., 1999). Therefore, the business community has an economic incentive to ensure the timely, high-quality treatment of depression in employees. One option is for businesses to become more active in improving employee awareness of the importance of the detection and treatment of depression. Another option is to require quality care for depression through private health insurance. Businesses increasingly finance mental health care for their employees through contracts with managed care organizations (OPEN MINDS, 1999). These contracts can be used as a means to require managed care organizations to improve the quality of care for depression via quality improvement programs. |

for all conditions examined. These very large payments are for the treatment of heart disease and not its prevention.

Other high-cost health conditions highlighted in the study of Fortune 500 companies either were caused by or were the consequence of lifestyle factors. Some were highly prevalent but the cost of treatment was relatively low, such as diseases of the gastrointestinal tract (2.49 percent of total payments), essential hypertension (2.23 percent of total payments), and back disorders (2.07 percent of total payments) (Goetzel et al., 2000). Other conditions had lower prevalence rates but high average treatment costs and high total payments, such as cerebrovascular disease (1.65 percent of total payments) and cholecystitis and cholelithiasis (1.58 percent of total payments).

The analysis of Fortune 500 companies also uncovered costly mental health and substance abuse disorders that may be initiated or exacerbated by stress. Bipolar disorders with major depressive episodes were the most costly (1.25 percent of total payments), followed by neurotic, personality, and nonpsychotic disorders (1.11 percent of total payments) and depression (0.77 percent of total payments). Alcoholism, with an average cost of $3,012 per patient, is the most costly substance abuse disorder on a per patient basis, although it accounts for less than 1 percent of total payments (Goetzel et al., 2000).

A clear relationship exists between modifiable risk factors in a typical employed population and the employers’ health care expenditures for the treatment of the diseases and disorders caused by these risk factors. For example, in a study of 10,000 employees of the Control Data Corporation, researchers documented lower health care costs for employees who exercised regularly, ate nutritious foods, abstained from smoking cigarettes, and had low blood pressure (Brink, 1987). A 5-year study of Steelcase Corporation employees showed that as modifiable health risks increased for employees, so did their medical expenditures (Yen et al., 1992). Another study examined the effects of 10 risk factors (obesity, high serum cholesterol levels, high blood pressure, stress, depression, smoking, inappropriate diet, excessive alcohol consumption, physical fitness and lack of exercise, and high blood glucose levels) on employer health care costs (Goetzel et al., 1998a; Anderson et al., 2000).

The study examined medical claims for more than 46,000 employees from both private- and public-sector organizations for 6 years. These 10 modifiable risk factors accounted for about 25 percent of all health care expenditures for the six employers in the study (Anderson et al., 2000). Interestingly, the two risk factors with the greatest effect on health care expenditures within 3 years were psychosocial: depression and stress. Health care expenditures for employees who reported depression were 70 percent greater than those for employees not reporting depression. Health care expenditures for employees with high levels of stress were 46 percent greater than those for employees who did not have high levels of stress, after controlling for demographics and other risk factors. When risk factors were combined, as they normally are for individuals at risk in multiple categories, health care expenditures increased to a far greater extent. For example, when health care expenditures for individuals with multiple risks for heart disease (i.e., smoking, hypertension, hypercholesterolemia, high stress, sedentary lifestyle, and obesity [Box 6–4], high blood glucose) were examined, they were found to be more than 200 percent greater than the expenditures for those without these risk factors. Similarly, health care expenditures for individuals at high risk for the two psychosocial risks, depression and stress, were nearly 150 percent greater than those for individuals lacking these risks.

|

BOX 6–4 Obesity and Employers Employers represent another group of stakeholders adversely affected by the growing epidemic of obesity in America, but they also have ample opportunities to reverse this trend. As the problem of obesity in America grows, businesses are confronted with escalating health care costs, missed days of work, lost productivity, and much more. Because more than 134 million Americans (BLS, 2001) spend a majority of their day at work, businesses can help promote healthy lifestyles through work-site policies, changes in the physical and social work environment, educational programs, and connections with resources and programs in the surrounding community. Employers must first understand the direct and indirect costs of obesity and the return on investment that can be realized when obesity prevention and treatment strategies are implemented. Then, employers can communicate their commitment to helping employees be healthy by creating flexible work schedules that permit regular physical activity; providing healthy, accessible, and affordable food options at or near work; establishing on-site exercise facilities or creating incentives for employees to join or participate in other fitness-oriented activities; working with health insurers to provide healthy eating and physical activity counseling for all employees and their families; and offering incentives (e.g., time off and decreased insurance rates) to employees who participate in exercise or weight maintenance programs. |

Furthermore, there is growing evidence that these modifiable risk factors not only increase health care costs but also increase worker absenteeism and decrease on-the-job productivity (Golaszewski et al., 1989; Bertera, 1991; Yen et al., 1994; Burton et al., 1999; Pronk et al., 1999; Edington, 2001). One of these studies found a consistent relationship between obesity, stress, multiple risk factors, and subsequent health care expenditures (Aldana, 2001). A similar relationship existed between modifiable risk factors and illness-related employee absenteeism.

For an employer, the implications of this research are enormous. When all else is held constant, the risk profile for the population covered by the employer’s medical plan and human resource policies can significantly affect labor costs. What options does an employer have for managing the risk of its labor pool? It cannot fire employees, for self-evident legal and ethical reasons. However, the employer can institute risk reduction programs that, if successful, will significantly reduce the employer’s costs.

One company undertook a study of the implications of undertaking a risk reduction program. In a study of 56,000 employees of Union Pacific Railroad, investigators estimated that the company would save $20.7 million over 10 years compared with the amount that it would spend in a “do-nothing” scenario if it were able to reduce each of 10 modifiable risk

factors by 0.1 percent during those 10 years (Leutzinger et al., 2000). If risk reduction programs were even more successful and the risk factors were reduced by 1 percent per year, economic models predicted that the company would save $77.4 million over 10 years. As a result of this study, senior management at Union Pacific Railroad decided that improving the health and productivity of its employees was a priority for the railroad and elevated this initiative to the status of a “big financial deal” in 2001 (Leutzinger, 2001).

Changing the Health Risk Profiles of Employees

In many ways, the workplace should be an ideal setting for the introduction and maintenance of health promotion and disease prevention programs. Employees are concentrated in a finite number of geographic sites, they share a common purpose and a common culture, and communication and information exchanges are relatively straightforward. Individual goals and organizational goals are generally aligned with one another. Social support is available when changes are tried, and organizational norms can encourage certain behaviors and discourage others. Financial or other incentives can be introduced to encourage participation in programs, and the consequences of the programs can be measured by using existing administrative systems for data collection and analysis. Employers can also create a set of programs to encourage employees to participate in risk reduction activities. It is important, however, that employers conduct health promotion activities and implement incentives programs in ways that assure nondiscrimination and privacy for persons with disabilities. Nondiscrimination and privacy are required under the Americans with Disabilities Act of 1990 and represent good practices for any employer.

If the work site represents an ideal setting for changing people’s behaviors and improving their risk profiles, do workplace health promotion and disease prevention programs actually work? Can the workplace serve as a catalyst for health improvement and risk reduction? Certainly, a number of companies have introduced workplace health promotion and disease prevention programs. Twenty years ago, less than 10 percent of U.S. businesses with 50 or more employees offered some kind of health promotion or disease prevention programs to their workforces. Today, many more companies are offering such programs. Twenty years ago there was little credible evidence that such programs were effective. Companies invested in them because they believed it was the right thing to do. Today’s employers are seeking information that these programs work to retain or enhance them.

There is increasing evidence that health promotion and disease prevention programs based in the workplace can change the behavior, psychoso-

cial risk factors, and biometric values for individual employees and the overall risk profile of the employed population (Bly et al., 1986; Bertera, 1990, 1993; Fries et al., 1993, 1994; Breslow et al., 1994; Goetzel et al., 1994, 1996; Wilson et al., 1996; Heaney and Goetzel, 1997; Pelletier, 1999; Gold et al., 2000; Ozminkowski et al., 2000).

Overall Cost Savings and Returns on Investment

Employers are concerned not only whether health promotion and disease prevention programs work in the sense that they can change the behavior, psychosocial risk factors, and biometric values for individuals employees but also whether these programs save money overall. They are concerned about whether investment in these activities has a positive rate of return.

Growing evidence shows that well-designed and well-resourced health promotion and disease prevention programs can produce savings in medical costs and possibly a positive rate of ROI in the program. The return on investment for health programs and for demand and disease management programs has been reported to range from $1.40 to $13 in benefits per dollar spent on the program, depending on the type of program (Goetzel et al., 1999). Traditional health promotion programs had a median return on investment of $3.14 per dollar spent; demand management programs had a median return on investment of $4.50 per dollar spent; and disease management programs achieved a median return on investment of $8.88 per dollar spent. Multiple-category programs that combined the elements of health programs and demand and disease management programs achieved returns on investment ranging from $5.50 to $6.50 per dollar spent, with a median value of about $6 (Goetzel et al., 1999). Other studies report an average benefit–cost ratio of $3.48 for every dollar spent. For example, in one of the programs studied, Citibank invested $1.9 million in a health promotion program. It saved $8.9 million in medical expenditures as a result of the program and realized a return on investment of $4.56 to $4.73 per dollar spent (Ozminkowski et al., 1999, 2000). Additionally, the health care costs of participating employees with preexisting chronic medical conditions (heart disease, diabetes, back problems, and hypertension) were less than those of employees who did not participate.

Need for More Information on the Effectiveness of Health Promotion Programs

Although evidence indicates that workplace programs can work to reduce risk factors and that programs that are well designed can lead to cost savings, much still remains to be determined about such programs.

Much more needs to be known about which interventions are the best

for facilitating behavioral change and risk reduction. For example, although individualized risk reduction counseling is effective in creating behavioral change, there are many ways of providing risk reduction counseling. However, the most effective way of providing this service is not known. Does this intervention work best when delivered in person, by telephone, or through tailored print communication? Which messages work best for which people? What social factors can be brought into play? What is the ideal balance between individual and group change processes? Should employers use social marketing techniques to influence employee behavior?

In addition to learning more about the effectiveness of specific intervention strategies, more needs to be known about how to structure these programs. Health promotion and disease prevention programs vary considerably in intensity, comprehensiveness, content, the communications media used, the staff involved, and other characteristics. Such programs include the following components:

-

Program awareness. Health promotion and disease prevention must be “sold” to eligible employees in the same way that Band-Aids, Tylenol, and detergents are sold. Eligible employees need to be aware, at an individual level, of the importance of health promotion and disease prevention and the availability of programs to address health risk factors. This is accomplished through successful implementation of communications, public relations, and marketing programs.

-

Participation. A large proportion of eligible employees must be engaged in the program and participate in its activities. Program participation rates significantly affect program savings and estimates of return on investment because program expenses are typically spread across an entire eligible population, whereas program savings apply only to participants.

-

Employee attitudes. Attitudes, health beliefs, feelings of being in control, readiness to change behaviors, stress management, and other psychosocial factors significantly influence an individual’s health and well-being (see also Chapter 2). Changing employee attitudes and altering behavior are critical because a change in behavior cannot be maintained unless individuals believe intrinsic psychological or social value is associated with the change.

-

Behavioral change and risk reduction. The extent to which corporate programs achieve significant and long-lasting changes in employee health and well-being will influence the likely economic benefits that follow.

Finally, more needs to be known about how to measure the effectiveness of such programs. The benefits of these programs should be measured in terms of health care cost savings, decreases in absenteeism, and improvements in productivity. Absenteeism can be used to measure employee pro

ductivity. As discussed earlier, health promotion and disease prevention activities have been shown to improve health and decrease costs, and one indication of improved health may be a decrease in absenteeism.

Employee health and productivity are apparently closely related, and effective management of one will positively affect the other (Goetzel et al., 1998b; Burton et al., 1999; Claxton et al., 1999; Cockburn et al., 1999). However, of the three benefits of these programs, measuring on-the-job productivity is the most difficult. On-the-job productivity losses are harder to measure than absenteeism because traditional ways of measuring productivity (i.e., counting the number of widgets produced per unit of time) are quickly becoming outdated as the U.S. economy changes from a manufacturing economy to a service economy, in which quality is more important than quantity. Nonetheless, several tools and systems are under development to assess gains or losses in on-the-job productivity. These include self-assessment tools, simulation studies, and sophisticated tracking and monitoring systems (Reilly et al., 1993; Van Roijen et al., 1996; Endicott and Nee, 1997; Berger et al., 2001; Burton et al., 2001; Goetzel et al., 2001; Kessler et al., 2001; Lerner et al., 2001). Once these tools and systems are perfected, the potential impact of health promotion and disease prevention programs on employee productivity and overall business performance should be easier to document. Results from these studies are expected to overshadow any savings realized from cost-cutting and expense management initiatives.

Workplace Safety Programs Promoting the Health of Employees

Promoting the health of the workforce requires a safe workplace and a healthy workforce. At the turn of the century, premature death often resulted from diseases, injuries, and unhealthy work conditions. The Department of Labor’s Bureau of Labor Statistics documented that 23,000 workers died from work-related injuries in 1913; this is equivalent to a rate of 61 deaths per 100,000 workers (CDC, 1999). However, with the identification of the etiologic factors that contribute to occupational health hazards and the implementation of federal legislation to assure safe and healthy working conditions, data from multiple sources indicate that work-related deaths, injuries, and illnesses have declined dramatically over time.

In 1970, the Occupational Safety and Health Act was specifically framed “to assure so far as possible every working man and woman in the nation safe and healthful working conditions.” That act established, in 1971, both the Occupational Safety and Health Administration (OSHA), which is part of the Department of Labor, and the National Institute for Occupational Safety and Health (NIOSH) (2000a), which is part of the Centers for Disease Control and Prevention.

|

BOX 6–5 Federal Legislation to Promote Occupational Safety and Health The first federal legislation pertaining to occupational health and safety granted limited compensation benefits to civilian service workers for injuries sustained during employment (1908, Federal Workers’ Compensation Act). Subsequent legislation established occupational health and safety standards for employees of federal contractors (1936, Walsh-Healey Public Contracts Act) and regulations to protect mine workers (1969, Federal Coal Mine Health and Safety Act). The Occupational Safety and Health Act of 1970 authorized the federal government to develop and set mandatory occupational safety and health standards and to establish the National Institute for Occupational Safety and Health to conduct research on workplace standards. The Toxic Substances Control Act of 1976 requires industry to provide data on the production, use, and health and environmental effects of chemicals. The act also led to the development of “right-to-know” laws, which provide employees with information on the nature of potential occupational exposures. The Federal Mine Safety and Health Act of 1977 (Mine Act) strengthened and expanded the rights of miners and enhanced the protection of miners from retaliation for exercising such rights. The Pollution Prevention Act of 1990 established policy to ensure that pollution is prevented or reduced at the source, recycled or treated and disposed of, or released only as a last resort. The act also led to the substitution of less toxic substances in a wide range of industrial processes, with significant reductions in worker exposure to toxic substances. |

OSHA was created to assure safe and healthy workplaces in America by enforcing workplace safety and health regulations (see Box 6–5). Since 1971, workplace fatalities have been halved and occupational injury and illness rates have declined 40 percent. Over the same period, U.S. employment nearly doubled from 56 million workers at 3.5 million work sites to 105 million workers at nearly 6.9 million sites. OSHA forms cooperative relationships with labor and management through Voluntary Protection Programs, which “recognize and promote effective safety and health management” at numerous sites around the United States and in more than 180 industries (OSHA, 2002b). These programs have resulted in millions of dollars in savings each year because injury and illness rates have declined below the averages for the industries at the participating sites. In addition, OSHA’s Strategic Partnership Program focuses on safety and health programs and includes outreach and training components along with enforcement (OSHA, 2002a).

Although the reductions in workforce injuries and the improvements in working conditions have been impressive, an average of 137 individuals die

each day from work-related diseases; an additional 16 die from injuries received while on the job. Every 5 seconds a worker is injured; every 10 seconds a worker is temporarily or permanently disabled (NIOSH, 1996).

NIOSH is the only federal agency responsible for conducting research and making evidence-based recommendations on the prevention of work-related diseases and injuries. NIOSH is responsible for conducting research on the full scope of occupational diseases and injuries, ranging from lung disease in miners to carpal tunnel syndrome in computer users. In addition, NIOSH investigates potentially hazardous working conditions; makes recommendations and disseminates information on preventing work-related diseases, injuries, and disabilities; and trains occupational safety and health professionals.

NIOSH data show that the direct and indirect costs of occupational injuries and illnesses are $171 billion annually for all businesses, compared to “$33 billion for AIDS, $67.3 billion for Alzheimer’s disease, $164.3 billion for circulatory diseases, and $170.7 billion for cancer” (NIOSH, 2000b).

NIOSH has brought together numerous organizations and individuals to focus on the creation of a research agenda. NIOSH and its public and private sponsors have developed the National Occupational Research Agenda (NORA) to provide a framework to guide the entire occupational safety and health community to help reduce the high toll of occupational injuries and illnesses. NORA priorities reflect a significant degree of concurrence among the large number of stakeholders. The priority research areas have been grouped into three broad categories: disease and injury, work environment and workforce, and research tools and approaches (see Table 6–1). NIOSH and its partners, through NORA, will guide and coordinate research for the entire occupational safety and health community. Fiscal constraints on occupational safety and health research are increasing, however, making it important for NIOSH to focus on the topics that will benefit workers and the nation and to ensure a coordinated research agenda.

In addition to implementing NORA, NIOSH operates programs in every state to improve the health and safety of workers. NIOSH evaluates workplace hazards, builds state worker safety and health capacity through grants and cooperative agreements, funds occupational safety and health research, and supports occupational safety and health training programs.

Occupational safety and health programs are specific to the work site and operations. Programs usually focus on basic principles of control technology that include engineering controls, work practices, personal protective equipment, and monitoring of the workplace for emerging hazards. Work site safety and health training and a long-term commitment to such programs are also critical to achieving occupational safety and health goals. However, the majority of safety and health regulations and enforcement

TABLE 6–1 NORA Priority Research Areas

|

Category |

Illness or Injury |

|

Disease and injury |

Allergy and irritant dermatitis Asthma and chronic obstructive pulmonary disease Fertility and pregnancy abnormalities Hearing loss Infectious diseases Lower back disorders Musculoskeletal disorders of the upper extremities Traumatic injuries |

|

Work environment and workforce |

Emerging technologies Indoor environment Mixed exposures Organization of work Special populations at risk |

|

Research tools and approaches |

Cancer research methods Control technology and personal protective equipment Exposure assessment research Risk assessment methods Social and economic consequences of workplace illness and injury Surveillance research methods |

|

SOURCE: NIOSH (1996). |

|

efforts have been designed to focus on large employers. Therefore, small businesses face specific challenges in ensuring a safe and healthy workplace.

Small employers employ more than half of the employees in private industry, and they experience higher levels of work-related hazards. Data from a survey of businesses in 1994–1995 found that about one-third of all work-related deaths occur at workplaces with 10 or fewer employees, although they employ only 15 percent of all workers in private industry. The challenges to ensuring safe workplaces and healthy workers include a lack of onsite occupational safety and health professionals, difficulties in recognizing the magnitudes of specific hazards, and a lack of strategies for dealing with hazards in a small-business environment (NIOSH, 2002c).

The importance of occupational hazard assessment and worker protection is exemplified by the recovery, demolition, and site-clearing operations at the World Trade Center (WTC) in the aftermath of September 11, 2001, when occupational hazard assessment and worker protection were critical. First-response workers—firefighters, police, rescue workers, and volunteers—faced numerous occupational exposures, including fire and smoke, falling debris, and air contaminants such as asbestos, lead, silica, and volatile organic compounds, to name a few. OSHA became an integral part of

response efforts at WTC. Box 6–6 provides a summary of OSHA activities performed to identify and abate serious hazards and to protect the workers in WTC site operations.

The committee acknowledges the progress that has been made in reduc

|

BOX 6–6 OSHA’s Role at the World Trade Center Emergency Project After the September 11, 2001, terrorist attack, the Occupational Safety and Health Administration (OSHA) worked at the World Trade Center site 24 hours a day, 7 days a week, to help protect rescue and recovery workers involved in recovery, demolition, and site-clearing operations. By September 21, 2002, about 800 federal and state OSHA staffers and several private-sector Voluntary Protection Program volunteers from throughout the United States assisted in the following roles: Risk Assessment and Monitoring

Respiratory Distribution and Fit Checking

Safety Monitoring

Site Safety and Health Support

|

Site Safety and Health Coordination

SOURCE: OSHA (2002c). |

ing work-related mortality, injuries, and diseases, especially among large employers. The committee also acknowledges that employers and employees must continue to be vigilant and proactive in recognizing hazards in the workplace. The committee encourages a greater sharing between large and small employers of the best practices and strategies that can reduce work-related mortality, injuries, and diseases and protect workers’ health.

Other Workplace Policies That Promote Health

Employers implement a number of policies related to family leave, flexible work practices, and other benefits and organize work (e.g., through the creation of teams and the assignment of multiple tasks) in ways that may have important health consequences. Employers implement some of these policies voluntarily; they implement others to comply with the law. For example, the federal Family and Medical Leave Act of 1993 requires employers with 50 or more employees to provide up to 12 weeks of unpaid leave for the birth or adoption of a child; to take care of a seriously ill child, parent, or spouse; and to recover from a serious illness. The business and public health sectors rarely consider these policies and practices as influential determinants of health. Chapter 2 presents evidence that job characteristics, such as job demands and control, job insecurity, and issues related to part-time, shift work, and current practices on outsourcing have important effects on health. A range of policies related to work organization, the interface between work and family, and long-term employment practices have often been evaluated for their effects on employee productivity and

satisfaction. The committee believes that these same work practices, along with the more traditional concerns about occupational health and safety practices, have important consequences for health. These types of private-sector policies may be among the most important determinants of population health. Evaluation of the effects of these policies and practices on health is a high priority.

ROLE OF BUSINESSES AND INDUSTRIES IN PROMOTING A HEALTHY ENVIRONMENT

The private and public sectors significantly influence health when their goals are incompatible with conditions that promote healthy behaviors or physical environments. When such goals are in conflict and significant health hazards arise, governmental agencies have a responsibility to act. Over the past 30 years, the U.S. government has passed numerous environmental laws and regulations to protect the health of the public (see Table 6–2). These laws have often been passed in response to industrial contami

TABLE 6–2 Selected Environmental Legislation

|

Legislation |

Purpose |

|

Safe Drinking Water Act, 1974 |

Passed to protect the public from waterborne diseases, chemicals, and heavy metals in drinking water |

|

Clean Air Act Amendments, 1977 |

Established the regulatory structure and an enforceable timetable for reducing urban air pollution |

|

Clean Water Act, 1977 |

Sought to make rivers and lakes safe for fishing and swimming |

|

Comprehensive Environmental Response, Compensation, and Liability Act (Superfund statute), 1980 |

Passed in response to the contamination at Love Canal, New York and Times Beach, Missouri to protect communities from health dangers at hazardous waste disposal sites |

|

Federal Insecticide, Fungicide, and Rodenticide Act, 1972, and Toxic Substances Control Act, 1976 |

Enacted to require analysis of chemicals to which the public might be exposed through food and other pathways |

|

Toxics Release Inventory, 1987, mandated by the Emergency Planning and Community Right-to-Know Act of 1986 |

Enacted to inform citizens about toxic chemicals in the environment; it is also known as Title III of the Superfund amendments and is based on the premise that citizens have a right to know |

nation. In recent years, however, the roles of private-sector businesses and industry and of the public sector have become important in improving the environments of the communities in which they operate. Additionally, the private sector has formed partnerships with governmental agencies to help promote the health of the public.

One example is the Environmental Protection Agency’s (EPA’s) Design for the Environment (DfE) program. Through voluntary partnerships with businesses, industries, and others (e.g., public interest groups, universities, and research institutions), EPA provides businesses and industry with information to make environmentally informed choices regarding their products, processes, and practices (EPA, 1998). According to EPA, the DfE program strives to promote the incorporation of environmental considerations into the traditional parameters of cost and performance on which businesses base their decisions.

Businesses and industries have come to realize that responsible entrepreneurship can play a major role in protecting human health by improving the environmental quality of the community through the efficient use of resources and the minimization of waste. Businesses and industries are developing techniques that reduce harmful environmental impacts. Some business and industry leaders are also fostering openness and dialogue with employees and the public and carry out environmental audits and assessments of their compliance with environmental laws and regulations. An example of a company initiative to improve community health is described in Box 6–7.

Thus, investing in community and environmental health not only is an example of corporate responsibility but also can provide economic returns to the business or industry. These programs succeed when there is a commitment from the leadership of the organization and, in many cases, when they are part of the business’s mission and vision statements. Another example is provided in Box 6–8.

The food and beverage industry generates products that may contribute to disease and disability if consumers make choices potentially incompatible with good health. In light of the intensifying obesity epidemic in the United States, the industry has been asked to work in partnership with other sectors to help consumers in their efforts to make healthier lifestyle decisions that will promote health by reducing obesity. In October 2002, the Health and Human Services Secretary, Tommy Thompson, and the Agriculture Secretary, Anne Veneman, met with officials from the National Restaurant Association and the National Council of Chain Restaurants to begin a dialogue about how the food and beverage industries can help to reduce obesity. Potential strategies to be considered are delivering healthy food choices, providing easy-to-understand nutritional information, integrating healthiness into mass-marketing strategies, and offering an increased

|

BOX 6–7 Dow Chemical Company: Improving Environmental Health The Dow Chemical Company has 40 global manufacturing sites. The third largest is in Midland, Michigan, with 550 buildings and 40 chemical production plants on a 1,900-acre facility. Air emissions were such that, in the late 1990s, the attitude and belief inside the company were that no further gains could be made in emission control at the facility. However, Dow set two important goals: (1) to accrue by April 30, 1999, capital that could be used to cut waste and emissions by 35 percent and (2) to begin to foster institutional changes within Dow to shift the corporation’s thinking from compliance to pollution prevention and to further integrate health and environmental concerns into core business practices. Working with the community, activists, and pollution control consultants, Dow engineers identified pollution prevention opportunities. The result of this activity reduced waste and emissions by 12 million pounds per year, a 37 percent reduction. Yet, the common belief in this facility had been that there were no cost-effective pollution prevention projects left to pursue. Ultimately, 17 projects were identified with a combined return on investment of 180 percent, or a savings of $5.4 million per year. |

|

BOX 6–8 Intel: Improving Environmental Health Through Corporate Vision and Mission Intel, a manufacturer of microprocessors, changes it manufacturing processes every 2 years as it miniaturizes the next generation of microprocessors. Intel considers this an opportunity for environmental improvement, for example, through chemical selection, facility design, waste management, ergonomics, and manufacturing equipment selection. Other aspects of planning include projecting environmental health and safety impacts over 10 years, or five generations of manufacturing. It sets goals that must be integrated into the design and development processes. For example, Intel reduced water use by 40 percent in one process that uses hydrofluoric acid to etch wafers and achieved better management of the exhaust, which reduced energy use. In another process, it recycled hazardous wastes and reduced emissions of volatile organic compounds. A key to Intel’s success in improving the environmental health of the community has been the company’s vision to develop a “green” plan that integrates design for the environment while aiming for sustainable activities as part of its operations. |

variety of healthy meals. The secretaries will also engage other organizations in the attempt to help combat the obesity epidemic, including fruit and vegetable growers, grocery manufacturers, public health groups, and state leaders through the National Governors’ Association and the National Conference of State Legislatures, as well as physical fitness groups (DHHS, 2002). This example shows how federal leadership can be used to encourage voluntary change. Other voluntary efforts, such as those made to develop standards to protect children on the Internet, demonstrate that industries can be mobilized to deal with problems of social significance. In the absence of voluntary agreements, potential legislative and regulatory strategies could be developed; for example, federal school lunch grants could be contingent upon schools’ removal of soft drinks and other fast-food sources from junior high schools and high schools.

A CASE FOR IMPROVING THE HEALTH AND WELL-BEING OF COMMUNITIES

Although the primary contribution of businesses to creating the conditions for health is the provision of jobs and creation of economic wealth, major employers as leaders of the business sector can also consider investing in community health as an example of corporate social responsibility. The investment, in turn, can provide social and economic returns to the company. These programs succeed only if senior and middle managers view them as directly aligned with the company’s mission and vision. Company mission and vision statements, such as “becoming the preferred employer in the community,” “attracting and retaining the best and brightest,” and “emphasizing worker safety above all else,” can be leveraged by champions of health promotion and disease prevention programs to, very simply, “help the company achieve its mission and vision.”

Beyond the theoretical, philosophical, or even emotional reasons for supporting investments in employee and community health, there are practical reasons for these investments. A company, especially one that is large and dominant, that assumes a leadership position in improving community health and emphasizing disease prevention, health promotion, and accountability is likely to stand out in that community and is likely to affect the norms and practice patterns of health care practitioners for the better.

Another rationale for increased employer leadership and corporate investment in community health is the scarcity of mentally and physically capable employees able to take the place of employees who retire or voluntarily leave the organization. This scarcity is most pronounced in the service and high-technology sectors, where “knowledge workers” are in high demand. Many companies have begun to invest in the educational infrastructures of their communities to produce a large pool of well-educated and

technologically advanced workers from which the company can recruit new employees with the skills that the companies need (see Box 6–9). A similar philosophy could be applied to health. Corporate investment in an improved community health infrastructure can create a larger pool of healthy and productive employees who are better able to face the physical and mental challenges of today’s work environment.

Many corporate leaders seek to present an image of their companies as caring and responsible employers, and many companies try to distinguish themselves by being the preferred place to work (Johnson & Johnson, 1989; Levering and Moskowitz, 1994; Goetzel et al., 1998b; Mercer, 2000; Fortune Magazine, 2002). Investing in health promotion and disease prevention can also expand a corporation’s social connections with the community. Organizations that are actively engaged in their communities and that act in socially responsible ways can also achieve a sense of purpose, relevance, social connectedness, and leadership in the community. They can do this by, for example, implementing no-smoking rules in buildings, in company vehicles, in front of company premises, and at client meetings; instituting work–life balance policies such as flexible working hours and telecommuting; allowing employees to take time off to participate in health promotion programs; offering healthy food choices in workplace eating facilities; and limiting air and water pollution in the community. Some businesses have begun to offer employees computers and access to e-health programs (i.e., that use the Internet) to help them better manage their own health (Box 6–9).

Organizations that are socially responsible and that exhibit a sense of caring for employees and the community can realize significant business gains as well, even when the gains are measured in traditional accounting terms. Across every financial outcome measured, socially responsible businesses perform no worse and, perhaps, perform better than non-socially responsible firms (Stalling, 1998). Furthermore, consumers are more likely to purchase products from companies, such as Ben & Jerry’s Ice Cream, that they believe are more socially responsible (Stalling, 1998) (see Box 6–10).

The reasons and incentives for companies to enhance their cooperation with the community described in this section have also been summarized by Helperin (2000). The author notes that the public perception that “your company is a good corporate citizen isn’t just for nice guys anymore; it’s for everyone.” The involvement of corporations in aligning or branding themselves with a social cause (i.e., a strategic, stakeholder-based approach to integrating social issues into business strategy, brand equity, and an organization’s identity) affects employee recruitment and retention, employee morale, community and supplier relationships, public affairs, and the company’s overall operating philosophy. A recent example of corpo-

|

BOX 6–9 Ford Motor Company: Model E Program In February 2000, the Ford Motor Company, together with United Auto Workers leadership, launched the Model E Program for its employees. This program, the first of its kind, provides computer and Internet access to 350,000 Ford employees and their families in their homes for a nominal fee. The program is intended to help employees enhance their computer skills and comfort with the Internet environment, as well as their access to Internet learning opportunities. Ford management also envisions benefits for the company: employees will gain a deeper understanding of customer needs, communications with plant workers who do not have desktop computers will improve, and the costs of some human resource and other corporate services will be lower. By February 2002, 93 percent of employees had accepted the offer (Denise Clement, personal communication, February 4, 2002). Other companies have followed Ford’s lead in sponsoring employees to become computer savvy (e.g., Fleet Bank-Boston, General Motors and Daimler-Chrysler, Intel Corp., Ollin Corporation, and the U.S. Army) (www.hconline.org/industry.php). With large numbers of employees participating in the Model E Program, in July 2001 Ford moved to provide access to online tools that help empower employees in the management of their health. Through a licensing agreement, Ford provides access to the WellMed Personal Health Manager, a product of WellMed Inc., for 170,000 U.S.-based Ford employees and their families. According to WellMed: The product allows employees and their families to assess, record and improve their health on a daily basis. It includes general and gender-specific health risk assessment tools that cover past health issues, family history, and lifestyle habits; a secure location for individuals to create, gather, and store health records; a source of education information on conventional and alternative treatment options for important health topics such as allergies, asthma, depression, diabetes, cancer, and stress; and interactive, self-paced programs designed to assist individuals in achieving positive, healthful change such as quitting smoking, improving nutrition and fitness, or preparing for a healthy pregnancy. (www.wellmed.com/wellmed/c/c0802pr.asp?prID=62) |

rate alignment with a significant social issue involves Viacom, a global media company. It has embraced its role as a participant in the public health system by strategically aligning itself with the Kaiser Family Foundation to launch a major media campaign to foster HIV awareness and prevention domestically and internationally (www.kff.org). This campaign is described more fully in Chapter 7.

Engaging Corporate Partnership in the Public Health System

As discussed above, the arguments for corporate investment in promoting the health of workers and their communities are compelling. However, more must be done to encourage American business leaders to view them

|

BOX 6-10 Vignettes of Business Involvement in Community Activities Mellon Bank, Pittsburgh, Pennsylvania The Mellon Bank Chief Executive Officer, Martin McQuinn, serves as the Chair of the Community Health Committee for the University of Pittsburgh Medical Center and is a member of the Healthy Communities Business Advisory Panel for the Institute for Healthy Communities. One of Mellon’s projects is the Community Bridge Project, a model designed to show how local businesses can partner with other agencies to address critical social and economic issues in their communities. Community Bridge Project The program model calls for the formation of community advisory committees consisting of business managers, educators, human services professionals, and local residents. The committees will assess their communities’ business climates and recruit a pool of local residents willing to volunteer as mentors for welfare clients. A Penn State Cooperative Extension Program facilitator will be hired to coordinate existing extension resources and to work with volunteer mentors. Mentors will be trained to offer support and guidance for clients, helping them to identify workable strategies for improving their circumstances. Participants will also undergo employment skills assessments and take part in appropriate job skills training. In addition, clients will receive help in matching their current skills to available training opportunities in the community, and they will be coached to match employment goals with realistic employment opportunities. Mellon Financial Corporation Foundation The Mellon Financial Corporation Foundation provides support for initiatives in economic development, health and human services, culture, and education. Mellon is a leader in workforce development and job readiness initiatives. In addition to the Community Bridge Project, Mellon has partnerships with the National Council on Aging as well as welfare-to-work programs in Pittsburgh, Philadelphia, and Boston. In 1999, Mellon was awarded the Goodwill Industries of Pittsburgh’s Power of Work award (Stefani McAullife, Director of Community Planning at the Institute for Healthy Communities, personal communication, 2001). Manufacturer’s Association of Mideastern Pennsylvania Darlene Robbins of the Manufacturer’s Association of Mideastern Pennsylvania has seen a return on the investment that her organization made when it began focusing on the wellness of employees. Having programs such as Wellness in the Workplace decreased turnover, decreased absenteeism, and improved employee retention and morale. Through this program, the association invites small-, mid-, and large-sized organizations to attend a breakfast to discuss wellness in the workplace and the important role that it plays in production. The breakfasts are attended by several dozen business representatives who exchange a variety of useful information. The Manufacturer’s Association wants to attract high-quality employees to Schuylkill County and realizes that a community with a high quality of life attracts the type of potential employees who will bring revenue to the business community. In addition, the association aims to attract new businesses into the |

|

area and recognizes that executives look at the quality of the community when deciding whether to move their families and businesses there. Representatives from potential new businesses explore factors such as competition, wages, cost of living, and the employee base, as well as the educational system, economic development potential, and the attitude of the community. The association and other Schuylkill County partners recognize that collaborative efforts are needed to bring new resources to the communities but note that a community does not have to be big to be successful (McAullife, personal communication, 2001). GTE GTE, which has recently merged with Bell Atlantic to form Verizon, is a founding member of the Georgia Healthcare Leadership Council. The council is an organization of managed care plans and local employers such as Delta Air Lines, Georgia Pacific, Lockheed, GTE, UPS, and pharmaceutical companies. Its goal is to improve the medical care provided to Atlanta residents. The primary focus of the council, formed in the fall of 1999, has been the development of preventive care standards based on evidence-based medicine. The council distributed posters to 3,500 metropolitan Atlanta doctors outlining standard prevention measures for children and adults. Upcoming initiatives include issuing guidelines for women’s health and standardizing treatments for asthma and allergies. GTE also has provided funding to support a Washington Business Group on Health project, Community Partnerships to Prevent Violence. The project will create a forum consisting of Texas-based employers; community organizations; school, mental health, and public health organizations; and parents. Its objective is to jointly develop strategies for businesses to assist parents (including their own employees) and schools in working to prevent school and youth violence. Forum participants will assess the community’s inherent ability to work cooperatively on these issues and identify their roles and responsibilities in meeting this challenge. The participants will develop a set of goals and recommendations. They will also identify resources to share, such as information to be provided to parents on identifying risk behavior, working with school personnel on children’s emotional and behavioral issues, and identifying community resources for children who need educational, mental health, and other services (WBGH, 2000). 3M A core value at 3M is to embrace a commitment to strengthening the communities that are home to 3M locations. Through the 3M Foundation and the 3M Community Affairs Department, 3M links resources to community needs. 3M employees volunteer in multiple activities, such as tutoring programs and visiting scientist programs in local schools. Employees who participate are given paid time off from work to provide these services (WBGH, 2000). |

selves as engaged partners in the public health system. Groups such as the Washington Business Group on Health are leading efforts to identify strategies to build greater collaboration between corporate leaders and governmental public health agencies.

In 1999, the Washington Business Group on Health hosted a public health forum for employers that brought together large employers and governmental public health leaders to discuss maternal and child health. A summary of the findings from the forum highlights the difficulties that employers and public health agencies must overcome if collaborative actions toward common health goals are to be achieved (WBGH, 2000). These findings include:

-

Employers and governmental public health agencies have had little interaction; this situation needs to change, and both will benefit from such a change.

-

There is a need for a common language and for dialogue among public health employers about issues related to health care costs.

-

Employers need data on pressing community health problems, but the data gathered need to be interpreted in ways that are meaningful to corporate health leaders.

-

There are significant limits to both the extent and the efficacy of employee health education.

-

There is a need to improve employee utilization of preventive health services that are covered but not being accessed by employees.

The findings from the forum also noted that partnership and collaboration could bring needed public health expertise to employers and business expertise to public health agencies (WBGH, 2000).

Governmental public health officials and business leaders would benefit from a formal dialogue on the health issues facing communities and the workforce. For example, corporate leaders should be invited to participate in community assessments and health planning and promotion activities (see Chapter 4). Such communication with corporate leaders and the participation of corporate leaders would allow the exchange of data on employee health as well as population-based health data from the community that are interpreted in ways that are meaningful to both public health officials and corporate health leaders. Such a dialogue would also provide the public health community with a better understanding of the processes that business leaders use to diagnose problems, review options, make decisions, and implement actions. Business leaders would gain a better understanding of the reasoning behind public health statutes, regulations, and other requirements that may affect businesses. Moreover, such a dialogue

would help businesses leaders better understand their critical role as partners in the public health system.

The scientific basis of the health promotion and disease prevention programs needs to be better explained so that employers can better determine the most effective and efficient strategies to promote and sustain employee health, lower costs, and increase worker productivity. The public health community, the business community, and philanthropies may all play a role in such an effort. Public health researchers and philanthropies could be active partners in helping employers who want to develop, manage, and evaluate these types of programs.

Strong communications strategies must be developed to disseminate information on the costs (to employers and businesses) of modifiable health risk factors and the evidence-based interventions available to reduce these risk factors. This is especially critical if employees (as noted in the forum of the Washington Business Group on Health) are not taking advantage of covered preventive services. The corporate world is already steeped in marketing techniques but could benefit from the social marketing and media advocacy strategies described in Chapter 7 to motivate behavioral change among individuals (e.g., to increase the levels of use of preventive services) or to change public policies that would contribute to a healthier community and workforce (e.g., support educational programs in the community).