1

Introduction

In A Shared Destiny: Community Effects of Uninsurance, the fourth report of the Institute of Medicine (IOM) Committee on the Consequences of Uninsurance, the Committee expands its focus from the adverse impacts of lack of health coverage on uninsured individuals and their families to examine the potential and likely indirect effects of the failure to insure all on their community. The Committee hypothesizes that the community overall experiences these effects largely through the problems that uninsurance poses for local health care institutions and services. In its phased study of the widespread and persistent lack of health insurance in the United States, the Committee has tried to convey the interrelated and systemic nature of the problems related to uninsurance. That perspective is especially important for this report, in which the Committee develops a series of hypotheses about community effects, assesses the evidence pertaining to these hypotheses, and proposes a research agenda to better document and understand those effects that cannot now be quantified or are poorly documented.

The towns, cities, and rural areas of the United States are home to a substantial number of uninsured persons. In 2000, an estimated 58 million people lived in families in which at least one member was uninsured (IOM, 2002b). In 2001, approximately 41 million Americans lacked health insurance coverage (Mills, 2002). The proportion of uninsured Americans rose steadily between the late 1970s and the late 1990s (IOM, 2001a). After a slight dip in 1999 and 2000, the national uninsured rate and number are increasing once again, with one out of six (16.5 percent) of those under age 65 lacking health care coverage.

The South and West, the most populous regions in the United States, are home to the greatest numbers of uninsured persons (an estimated 16.6 million and 11.2 million, respectively) (Mills, 2002; all numbers are for persons under 65 years

old and for the year 2001). The West South Central, Pacific, and Mountain regions, with uninsured rates of 24.3 percent, 19.7 percent, and 18.6 percent, respectively, have uninsured rates well above the national average (16.5 percent). The states with the highest number of uninsured persons tend to be those with the largest populations, including California (6.7 million uninsured), Texas (4.9 million), New York (2.9 million), and Florida (2.8 million). Uninsured rates show less of a direct relationship with population size; the border state of New Mexico, for example, is home to just 1 percent of the uninsured population nationally (an estimated 400,000 uninsured persons) but has one of the highest uninsured rates (23.9 percent) of all the states. Reflecting the predominantly urban location of the U.S. population, 82 percent of uninsured persons live in urban areas. However, urban and rural (non-urban) residents are about equally likely to be uninsured (rates of 16.5 percent and 16.8 percent, respectively). See Tables C.1, C.2, and C.3 for more information about the regional distribution of the uninsured population.

Coverage Matters: Insurance and Health Care, the Committee’s first report, shows that uninsured persons in the United States are predominantly workers or members of families in which someone had paid employment. It finds that many Americans lacked coverage because their employers did not offer it and workers were unable to afford policies without an employer contribution. Coverage Matters also identifies the unstable nature of health insurance coverage for Americans younger than 65—those with coverage today could lose it tomorrow for any number of reasons. However, at age 65, virtually everyone becomes permanently entitled to Medicare coverage.

The second report, Care Without Coverage: Too Little, Too Late, compares health outcomes for insured and uninsured adults, concluding that the lack of health insurance results in consistently worse health outcomes, including premature death, for adults. These poor outcomes result from deficits in access, use, and quality of health care across the spectrum of preventive, acute, and chronic care services.

Health Insurance Is a Family Matter, the Committee’s third report, breaks new ground in examining the effects of a lack of coverage by anyone in a family on the family as a whole and the implications for children’s health when they or their parents do not have coverage. The Committee concludes in its third report that the health, emotional well-being, and financial stability of families are at risk when even one member is uninsured. Thus, at a time when an estimated 38 million Americans lacked coverage (2000), another 20 million insured family members shared the financial risk and threats to peace of mind and even to their own health.

The lack of health insurance coverage within a population is frequently understood as a problem only for those who are immediately affected, namely, those without coverage and their families. A Shared Destiny explores whether and how many of us can be affected by the stark differences in financial access and resources available to those who have and those who don’t have health insurance. Our health care institutions and the vitality of our neighborhoods, cities, towns,

and rural communities can be imperiled by the lack of financing for and access to health services for some of us. Our major medical institutions of care and healing are not, nor should they be, gated communities. They should serve everyone.

The provision of health insurance is both a private and a public undertaking. Fully 25 percent of Americans have insurance through public programs.1 More than three-fifths of the population is covered by employment-based health plans (Mills, 2002). Despite the characterization of Americans as proudly self-reliant and individualistic, we nonetheless participate in each other’s fate in sickness and in health. This report contributes to our understanding of how this sharing occurs.

A SYSTEMS APPROACH TO THE PROBLEMS OF UNINSURANCE

Statements of value and purpose articulated by the IOM Committee on the Quality of Health Care in America in Crossing the Quality Chasm provide a unifying focus for this report (IOM, 2001b, pp. 1,6):

Americans should be able to count on receiving care that meets their needs and is based on the best scientific knowledge … the single, overarching purpose of the American health care system as a whole … is to continually reduce the burden of illness, injury and disability, and to improve the health and functioning of the people of the United States.

These goals for the nation’s health care system are not conditioned on having health insurance; all Americans should be able to receive needed and effective care. Care Without Coverage and Health Insurance Is a Family Matter have documented the lesser effectiveness of health care received by uninsured persons, notably for those with chronic conditions, which are a major priority for quality improvement efforts. Yet uninsured populations undermine health systems’ quality improvement for reasons beyond the kind of care that uninsured persons themselves receive. To the extent that health care institutions have uncompensated care burdens, investments in state-of-the-art information technology, creating multi-disciplinary care teams, and other aspects of the health services infrastructure are less feasible (IOM, 2001b).

The importance of understanding the health care enterprise as a complex system is a contribution of the recent national movement to improve the quality and safety of health care services. This joint public–private effort has focused on increasing the reliability of ever more complex medical care and broadening the understanding of effective health care interventions to encompass the patient or consumer at the center, teams of professionals, and community-based health-related activities.

The Institute of Medicine’s recent work in quality of care—Primary Care: America’s Health in a New Era (Donaldson et al. 1996), To Err Is Human (Kohn et al., 1999), Crossing the Quality Chasm (IOM, 2001b), and Envisioning the National Health Care Quality Report (Hurtado et al., 2001)—contribute comprehensive and system-focused visions of the proper and attainable goals of the American health care enterprise. These reports also propose strategies for achieving such goals. Likewise, Unequal Treatment: Confronting Racial and Ethnic Disparities in Health Care (Smedley et al., 2002) and a related report, Guidance for the National Healthcare Disparities Report (Swift, 2002) examines systemic biases and inequities in health services delivery and proposed strategies and diagnostic tools to remedy them. The capacity and performance of the nation’s public health infrastructure have also been the subject of a comprehensive assessment and prescription for improvement in The Future of the Public’s Health in the 21st Century (IOM, forthcoming 2003).

A Shared Destiny extends these diagnoses of systemic weaknesses and opportunities for improvements in American health care to consider the effects of uninsurance and of the current strategies for addressing it. These factors present both challenges to the quality and equity of health care and opportunities to improve the sector’s performance for all Americans.

This report makes three contributions that advance the understanding of health insurance dynamics at the population level. First, it identifies what is known and assesses the strength of evidence about possible health, institutional, and economic consequences of sizable uninsured populations for communities. Meeting this first objective engaged a second, more ambitious task, namely, to articulate a new analytic framework that traces plausible causal pathways from uninsurance to a number of effects on population groups or communities. This conceptual work allows the Committee to identify probable steps involved in moving from a hypothesized causal factor, such as a metropolitan area’s higher-than-average uninsured rate, to effects such as changes in the area’s health services capacity. Questions that emerge from such an examination include the following:

-

Which services and facilities do those who have health insurance and those without it share, and how does the degree of integration or segregation of these two populations within particular institutions affect health care service quality and capacity throughout the community?

-

Who ultimately pays for the care that uninsured Americans receive?

-

How and to what extent are health care facilities and, more broadly, civic institutions and community economic development affected by the presence of a sizable uninsured population?

-

How does the health status and access to health services of uninsured community residents affect the health and access of others within the same community?

The Committee hypothesizes that indirect and sometimes obscure “spillover” or “secondhand” effects of uninsurance on the community at large can be consid-

erable. These spillover effects have not been fully articulated or well documented in studies and evaluations, however. Many of these questions about community-level impacts of uninsurance cannot be answered satisfactorily with currently available statistical information and studies. Hence, the third contribution of this report is to propose an agenda for additional conceptual and empirical research that would examine community-level effects of uninsurance more directly and thoroughly.

DEFINITION OF “COMMUNITY”

Just which collective of people is considered to be a community depends on what activities or interests are at issue. In health policy analysis, the term “community” has evoked a variety of social, political, and economic concerns that have changed over time (Schlesinger, 1997; Ricketts, 2002). Communities may be defined broadly along a number of dimensions, alone or in combination:

-

Geographically (in terms of patterns of settlement)

-

Politically (in terms of government units or jurisdictions)

-

Socially (in terms of schools, clubs, voluntary associations)

-

Economically (in terms of market or health services areas)

-

Culturally and historically (in terms of shared identities or interests)

The size of an area defined as a community, and what characteristics are taken into consideration in this definition, ideally are related to the questions of concern and influence the ability to observe the processes and outcomes hypothesized to be taking place (Diez-Roux, 2001). The units in which data about health care utilization, health status, and health resources are collected and reported shape the Committee’s approach to assessing community effects. In practical terms, the particular unit of analysis specified as a community also reflects issues of data availability. Throughout this report, the actual unit of analysis is noted in discussing the results and findings of specific studies.

For the purposes of this report, the Committee defines a community as a group of people that (1) lives in a particular geographic area and (2) has access to a specific set of health resources for which there are data about financial and health-related outcomes. Most statistical information is collected and organized around politically and economically defined communities that are also geographically distinct, for example, single political jurisdictions (cities, counties, states) or the catchment area of a hospital. Consequently, much of the information available about uninsured people is aggregated into these units of analysis. In addition, like many forms of services, health care is delivered and received in person; thus, geographically defined communities are the predominant unit of analysis in this report.

Because of the variation in existing evidence regarding community effects, the Committee uses the term community in this report to refer to locations as

small as neighborhoods and as large as states. How expansive a community is specified to be depends partly on the patterns of social and economic interaction that are being analyzed and also on population density. For example, the community that shares primary care resources such as physician practices and clinics may be relatively small and local, while the community sharing an advanced trauma care facility may encompass an entire metropolitan area and adjacent rural counties.

CONCEPTUALIZING COMMUNITY EFFECTS OF UNINSURANCE

Although we often think of the impact of an injury in very personal terms, an injury to one may also be an injury to all. Consider the following examples. When a local hospital can no longer absorb the costs of serving uninsured patients in need of care and cuts back on staffed inpatient beds as a result, all members of the community served by the hospital are likely to experience reduced access to care. The effects do not stop there. In an effort to keep beds staffed, the hospital may contain costs by cutting staff in other departments, or, if the hospital cuts back its nursing staff, patient safety and the quality of care would be reduced for all patients. Alternatively, the hospital may turn to local, state, or federal governments for revenue to offset the costs of caring for uninsured persons, thereby increasing the tax burden on all residents or reducing other public services. Also, if public health department funds are diverted from communicable disease control programs to support hospital services for medically indigent residents, the health of all community members is put at risk. As these scenarios illustrate, the effects of uninsurance can be wide-ranging and significant.

The experiences of uninsured individuals and of families within a community influence the collective and aggregate effects of uninsurance on their community. These collective and aggregate effects are the subject of this report. This section first illustrates how these collective and aggregate effects can be distinguished from individual and family effects and presents the broader conceptual framework in which this report’s analysis is grounded. The next section discusses research methods used in this report, and the section following that sets out the working hypotheses about specific community effects that guided the Committee’s investigation.

The Committee’s analysis in each of its reports has been based on a general framework presented in Coverage Matters.2 This framework links individual and collective factors, including health status, financial resources, and health services capacity to the use of health care services and ultimately to a variety of health-related and financial outcomes. These include aggregate community characteristics

such as population health and uninsured rate, as well as ecological characteristics such as economic vitality and social cohesion, measures that are not reducible to individuals’ characteristics. Factors at both the individual and the community levels determine the extent and quality of individuals’ access to health care (Andersen et al., 2002). Appendix A depicts both the general conceptual framework and the Committee’s modification of it to guide the analysis in this report.

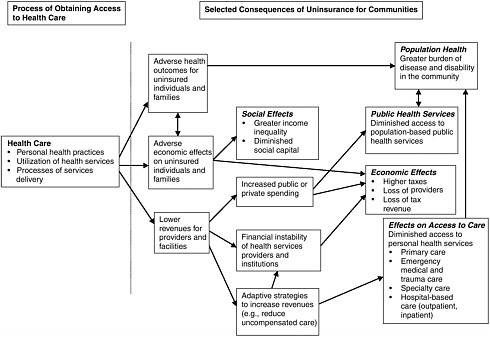

The causal pathways hypothesized for community effects incorporate the experiences of uninsured individuals and families as well as the performance of health care institutions and providers. The Committee’s conceptual framework for hypothesizing about pathways through which community effects are exerted and the breadth and scope of community effects builds selectively on a widely used behavioral model of access to health services (Andersen, 1995; Andersen and Davidson, 2001; see Figure 1.1).

The conceptual framework focuses primarily on the economic, financial, and coverage-related factors that facilitate or impede access to health services. The health, social, and economic consequences of delayed or forgone health care for uninsured individuals and families (as depicted in the two boxes labeled “adverse health outcomes for uninsured” and “adverse economic effects”) can result in a greater burden of disease and disability for the community overall as well as erosion of the capacity for timely and appropriate health services delivery in the community. To the extent that uninsured individuals and their families obtain health services, the uncompensated care burden on local providers and facilities (as depicted in the box labeled “lower revenues for providers and facilities”) serves as another pathway to community effects because it leads to (1) pressures to increase public spending to subsidize care for uninsured persons, (2) increased costs for health care and for health insurance, and (3) financially destabilized local health services. As a result, all members of the community may potentially experience diminished access to and quality of health services, as well as a greater burden of disease and disability. These hypothesized pathways and effects will be discussed in greater depth in the sections that follow; see Appendix A for a more detailed discussion of the conceptual framework.

The Committee’s definitions of health insurance and uninsured status are consistent with those adopted in its previous reports. Health insurance is defined by the Committee as financial coverage for basic hospital and ambulatory care services provided through employment-based indemnity, service-benefit, or managed care plans; individually purchased health insurance policies; public programs such as Medicare, Medicaid, and the State Children’s Health Insurance Program, and other state-sponsored health plans for specified populations. Uninsured refers to persons without any form of public or private coverage for hospital and outpatient care for any length of time. The Committee does not attempt to address the condition of underinsurance, by which is meant individuals or families whose health insurance policy or benefits plan offers less than adequate coverage. The problems faced by the underinsured are in some respects similar to those faced by the uninsured, although they are generally less severe. Uninsurance and underin-

surance, however, involve distinctly different policy issues, and the strategies for addressing them may differ. Throughout the Committee’s series of reports, the main focus is on persons with no health insurance and thus no assistance in paying for health care beyond what is available through charity and safety net arrangements.

This report looks at what happens, and what reasonably may be expected to happen, to a community when one community-level variable, namely, the local uninsured rate, is relatively high or on the rise. Of course, the uninsured rate within a community is closely related to a number of other aggregate characteristics that affect health or economic outcomes such as educational attainment, family income, and industrial composition (Shi, 2000, 2001; IOM, 2001a). Studies that attempt to measure the impact of uninsurance on community-level outcomes face the challenge of factoring out or analytically accounting for these covariates of health insurances that can be expected to affect the outcomes of interest. Throughout this report, the extent and nature of any analytic controls for covarying community characteristics are included in the descriptions of studies cited.

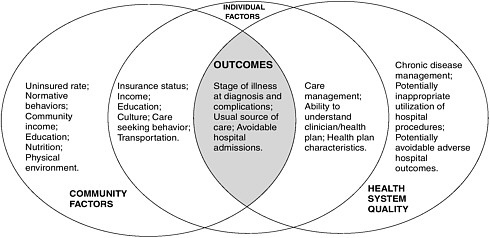

Figure 1.2 graphically depicts the overlap and interplay of individual characteristics, including health insurance status, with community-level factors, including the local uninsured rate, with another factor, the quality of the health care system, to determine individual and population-wide access to appropriate health care and other health outcomes. Insurance status functions as both a community-level and an individual-level characteristic that influences receipt of appropriate care in conjunction with characteristics of the health care system. The shaded portion of the figure, where all three spheres overlap, represents individual and aggregate population outcomes for a particular health condition. As depicted in this diagram, the outcome at the individual level is affected not only by the individual’s own features but also by those of the community collectively. The outcome at the population level is more than the summation of individuals’ independent experiences; it includes the effect of community factors such as the local uninsured rate.

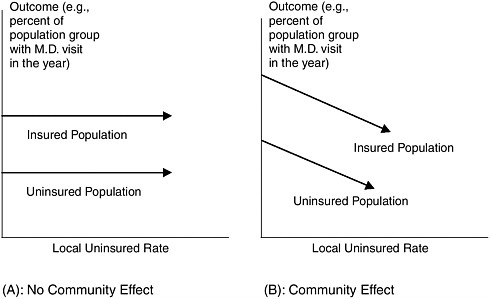

Figure 1.3 presents two graphs for comparison to illustrate the phenomenon of a community-level effect of the local uninsured rate on individuals’ access to care, over and above the effect of personal health insurance status. This pair of diagrams simplifies what is a much more complicated set of relationships among multiple individual and community factors that affect measures of access such as a physician visit within the year (e.g., those shown in Figure 1.2), but its simplicity allows for a clearer depiction of the hypothesized community-level effect. Graphs A and B each chart the percentage of two distinct population groups, Insured and Uninsured, that have a physician visit within a year (an outcome variable) against the local uninsured rate for a number of different communities (e.g., metropolitan areas). In both graphs, Insured populations are more likely to have had a physician visit than are Uninsured populations. Graph A represents the case in which there is no community effect on this outcome variable (a relatively crude measure of access to health care) because the lines plotted are parallel to the horizontal axis.

FIGURE 1.3 Community effects diagram.

The outcome for each group, Insured and Uninsured, remains constant as the local uninsured rate increases. Graph B represents the case in which there is a community effect on the outcome variable because, as the local uninsured rate increases, the percentage of both the Insured and the Uninsured with a physician visit within a year decreases, indicated by the downward-sloping line.

METHODS

Despite the acknowledged importance of community effects of uninsurance, they have rarely been studied directly. As a result, the research literature is slim on some topics and non-existent on others, making a systematic literature review impractical for the purposes of this report. Instead, the Committee has chosen to work from its conceptual framework, discussed above, modified from the framework used for the series of reports and first presented in Coverage Matters.

Search terms for use with PubMed were identified for the topics described in a background paper prepared for the Committee (Needleman, 2000) and articles were gathered for the years from 1985 onward, with reference articles and books included from earlier years. In addition to the bibliography collected for and cited in the Committee’s previous three reports, a non-systematic literature review was conducted, using the following terms, singly and in combination: academic medical centers; charity care; community health centers; cost control; cost-shifting; costs and cost analysis; crowding; economic development; economics, hospital; emergency medical services; health facility merger; hospitals, urban; managed

care; Medicaid; medical indigency; primary care; public assistance; public hospitals; rural health services; rural population; social capital; state government; trauma centers; uncompensated care. In addition, copies of relevant studies were collected from foundation, research center, and trade association websites.

For historical framing of current issues, interpretive weight was given to publications covering the period from the late 1970s through the mid-1990s. For interpretation of current issues, more interpretive weight was given to publications covering the period since the mid-1990s, given the changes in the organization and financing of health services delivery, for example, the advent of Medicare prospective payment in the early 1980s and the spread of state Medicaid managed care contracting in the early 1990s.

The variation in state and local uninsured rates offers one of the best opportunities to detect the effects of uninsurance on community health care services, institutions, and population health. The Committee attempts to identify the nature, size, and significance of these community effects by comparing geographically defined communities in which differing proportions of the population lack health insurance, focusing in particular on areas (municipalities, metropolitan areas, rural counties, states, and regions) that have disproportionately large uninsured populations. Because the impacts on rural communities are likely to differ from those in urban areas, rural areas are examined separately and in some detail throughout the report. In addition, states and larger geographic regions exhibit different patterns of health insurance coverage and uninsurance, with some states having relatively uniform uninsured rates throughout and others encompassing communities and substate areas with highly disparate uninsured rates. Appendix B describes and provides examples of distinctive patterns of uninsurance within and among states across the country.

The Committee has described and noted the limitations of the major national databases and surveys that provide information about health insurance coverage, health care expenditures, service utilization, and access to health care in its previous three reports. The reader is referred to those sources, particularly Coverage Matters, Appendix B (IOM, 2001a), and Care Without Coverage, Chapter 2 (IOM, 2002a), for reviews of the data sets that are the basis for much of the national-level research reported in this report. When particular studies are cited in this report, the accompanying discussion notes the relevant features and limitations of the data and methodology used.

WORKING HYPOTHESES ABOUT COMMUNITY EFFECTS

According to the Committee’s conceptual framework (Figure 1.1), the components and users of the health care system are interrelated, with the process of health care influenced by individual, family, and community-level resources, characteristics, and needs and with feedback or adaptation as part of this process. On the basis of this framework, the Committee hypothesizes that a community with

both insured and uninsured residents—that is to say, all American communities— is likely to be affected by the incomplete coverage status and diminished access to health care experienced by its uninsured population. In other words, uninsurance is likely to have spillover effects on the lives of people with insurance as well as those without it. For example, low- to moderate-income residents in cities with a higher-than-average uninsured rate report having less access to health services, compared to residents in cities with a lower-than-average uninsured rate (Brown et al., 2000; Andersen et al., 2002; see discussion in Chapter 2). At the same time, some members of a single community and some communities overall may be less subject to spillover effects from uninsured populations than others are. In the case of community-wide access to care cited above, it is low-income residents, not higher-income residents, whose access to care is affected by high community uninsured rates.

This section sets out the working hypotheses that motivate the lines of investigation the Committee pursued to determine whether and how communities as a whole are affected by the presence of substantial uninsurance among their populace. In each chapter that follows, the Committee specifies the strength and quality of the evidentiary base upon which its findings are drawn. Where there are few or no data or evidence on which to base conclusions about questions central to the Committee’s hypothesis, questions meriting further research are proposed.

Availability of Health Care Services in the Community

How does uninsurance within a community affect the availability of local health services? As depicted in Figure 1.1, the Committee hypothesizes that when faced with uninsured persons who need care, providers such as physician practices, hospitals, clinics, health departments, and the state and local governments that fund and operate facilities take measures to increase revenues from other sources and to contain their costs in order to balance the effects of uncompensated care. In the case of privately sponsored providers, they may adopt management strategies that reduce their exposure to uncompensated care costs. Public and private providers have similar options. They may

-

restrict access to or the general availability of health services for uninsured persons, leaving them to go elsewhere for care or to forgo care;

-

raise the funds necessary to cover the uncompensated care costs incurred by uninsured patients (by means of taxes, higher prices charged to those who do pay for services, or philanthropy);

-

reduce costs significantly, which can affect access (e.g., fewer hours of service), quality, or safety; or

-

provide no care at all to anyone (e.g., close the service).

Any community resident may experience the results of decisions made about care for those without health insurance when they encounter the local public

health infrastructure, need emergency medical services, seek primary or specialized health care, or use their local hospital for outpatient or inpatient care.

Especially for institutions that serve a high proportion of uninsured patients such as public hospitals, community health centers, and some academic health centers, a large or growing number of uninsured persons seeking health care may destabilize them financially and “tip” a hospital or clinic’s financial margins from positive to negative. A health care provider’s efforts to avoid this tipping or to respond in ways that protect the provider’s financial viability may trigger a series of events, for example, a reduction in hours that services are available or in the number of staff or active beds (which can lead to increased waiting times or reduced responsiveness to patients). To protect their financial viability, health care providers might also eliminate certain services or close the practice or facility. These events may result in the loss of access to care or lesser quality care.

Primary Care

Does a high or increasing demand for uncompensated care by uninsured patients adversely affect the economic viability of ambulatory care clinics and of private physician practices or lessen the availability of primary care in a community? The Committee hypothesizes that it does. Community health centers and other nonprofit clinics depend on public subsidies as well as patient revenues, and many already are providing services at their capacity. Without new funds to support their operations, they may not be able to expand to serve new clients (Cunningham, 1996; McAlearney, 2002). In areas experiencing increasing or high uninsured rates, physicians may refuse to accept new patients who are uninsured or publicly insured (to limit their financial losses), decline to establish a practice in an area, or decide to leave the area, resulting in less availability of services for all community residents.

Emergency Medical Services

Do large numbers of uninsured patients within a community increase utilization of local hospital emergency departments? Does a heavy uninsured patient load lead hospitals to cut back on emergency and trauma services? The Committee hypothesizes that relatively high or increasing local uninsured rates could result in greater emergency department (ED) utilization and overcrowding. However, hospital ED overcrowding is also affected by a number of other factors (including, for example, the availability of staffed inpatient beds in the same hospital and fewer restrictions on the use of ED services by managed care plans), which makes it difficult to tease out any contribution that the use of EDs by those without insurance makes to overcrowding. Evidence from the 1980s suggests that some of the closings of hospital trauma services may be attributable to a high uncompensated care burden, in turn associated with a heavy uninsured patient load (Dailey et al., 1992; Fleming et al., 1992).

Specialty Services3

Do high uninsured rates jeopardize the availability of specialty services from physicians, clinics, and hospitals? The Committee hypothesizes that relatively high uninsured rates discourage the provision of specialty care in a community. In the 1980s, for-profit hospitals were less likely to offer unprofitable services viewed as community benefits, such as emergency and trauma services, and certain kinds of specialty care, such as burn units or pediatric intensive care, that are disproportionately used by uninsured patients and are also less likely to be reimbursed fully by insurers (Gray, 1986; Needleman, 1999). Similar strains on hospitals that disproportionately serve uninsured patients may adversely affect access to care for all community residents, since these hospitals, which are often public facilities or academic health centers, are more likely than other facilities to provide health professions training and specialty services (burn, pediatric neonatal intensive care, trauma, psychiatry, AIDS care). Many of these highly specialized services and community resources are particularly crucial when natural or manmade disasters strike and could be considered an aspect of “homeland security.”

Hospital Outpatient and Inpatient Care

How are hospital outpatient services and inpatient care affected by the level of uninsurance within the community? The Committee hypothesizes that because hospitals are the locus of much of the more costly care provided to uninsured Americans, hospitals in communities with relatively high uninsured rates would show evidence of financial stress and fewer services as a result. Hospitals are particularly likely to be faced with the cumulative effects of inadequate care for chronic conditions, exacerbated acute illnesses, and delayed treatment among uninsured patients (IOM, 2002a). Many hospitals operate with narrow financial margins that leave little room to subsidize the uncompensated care associated with treating uninsured patients. A high uninsured rate over time or an increase in the number of uninsured patients is likely to reduce a hospital’s financial margin or even result in operating losses. Without a source of public or private funds to cover the costs of uncompensated care, hospitals may trim the hours and availability of services, particularly of its emergency department, obtain private capital through conversion from public to private status (with the potential loss of access to care previously guaranteed at a public facility), or close some or all of their operations entirely, leaving all community residents to seek services elsewhere.

Economic Consequences

Taxation and Spending Implications for Localities, States, and the Nation

How does the uncompensated care provided to uninsured persons affect public revenues and spending? As depicted in Figure 1.1, the Committee hypothesizes that state and local tax rates are affected by the demands for uncompensated care within these jurisdictions. Because subsidized and free care is supported by government and philanthropic funds as well as by revenues generated from insured patients, economic effects on communities with relatively high uninsured rates may include higher taxes, fewer philanthropic dollars available for other purposes, and higher costs for health services. In some states, tobacco settlement dollars have been devoted to improving access to care for uninsured persons, providing a new revenue stream to subsidize uncompensated care and delaying the need to limit services if other revenues, such as increased taxes, are not forthcoming. However, tobacco settlement monies need not be spent on health programs, and states are increasingly using these funds for other purposes, including covering general budget deficits (Dixon and Cox, 2002).

Economic Base

If physicians, clinics, or hospitals cut their services or close their doors for reasons related to a high or growing uninsured rate, would employees in the health and local service sectors lose their jobs and is the local economy affected as a result? The Committee hypothesizes that local economies are affected by reductions in health services capacity and that such impacts are more easily documented in rural than in urban communities. In rural areas, the loss of local health professionals and jobs may mean less income generated and spent locally, with less tax revenue available for the entire range of public endeavors including education, social services, and health care. In urban areas, where there are more options for health services and a greater number of employers, the relationship between uninsurance and the local economy is likely to be mediated by many other factors and thus be harder to detect.

Community Health

How does the local or state uninsured rate affect the health of the whole population? As depicted in Figure 1.1, the Committee hypothesizes that communities with relatively high uninsured rates have worse overall population health than those with relatively low uninsured rates. Further, it hypothesizes that these differences can be attributed not only to the worse health status of uninsured persons within the population but also to spillover effects of uninsured populations on those with health insurance. Measures of population health that might be

affected in this way include general health status, rates of communicable disease, disability rates, and hospitalizations for conditions amenable to treatment on an ambulatory basis.

A high or rising uninsured rate within a community may result in the reallocation of public funds and staff resources away from public health programs that serve all members of the community and toward direct services delivery urgently needed by low-income uninsured persons (IOM, 1988, forthcoming 2003). This is especially likely if there is little political support for raising state or local tax revenues to support direct services delivery and if other revenue sources (e.g., tobacco settlement monies) are not available.

The redeployment of public health agency resources away from population health activities to provide personal health care services to uninsured residents, along with the general underutilization of and limited access to care by uninsured members of the community can fuel the spread of disease and undermine communicable disease control efforts (e.g., tuberculosis, sexually transmitted diseases); prevention activities, such as immunization programs and antismoking educational campaigns; health protection activities such as food safety inspections and pollution control; and the increasingly essential surveillance of unusual disease outbreaks that can indicate the possibility of bioterrorism.

LIMITATIONS OF THIS STUDY

Identifying and interpreting potential community effects poses several analytical challenges. As noted above, many factors are correlated with both individual and community-level health insurance status (e.g., educational attainment, income, and job type). In addition, the relationships between a community’s attributes (e.g., median educational attainment, income, employment opportunities) and the effects of uninsurance (e.g., population health status) are interdependent. Because the studies reviewed in this report are observational and (for the most part) cross-sectional in design, it is more difficult to infer causal relationships than to demonstrate statistical associations among these various factors. Throughout the report, the kinds of analytic controls and limits on interpretation that apply to cited studies are noted in the discussion.

Another important issue in considering the evidence base is that information about impacts of uninsurance on the community as a whole is often inferred rather than observed directly. For example, the inverse relationship between the funding of public health activities in relation to state and local health departments’ provision of personal health services has been documented over several decades (IOM, 1988, forthcoming 2003; Fairbrother et al., 2000), but the extent of the provision of uncompensated care to medically indigent residents has not necessarily been analyzed as a function of local uninsured rates. It may take several logical steps or links to make a connection between the hypothesized cause and effects. One objective of this report is to describe these steps and point out the linkages that can be made with existing data and research.

The lack of empirically validated measures by which community-level attributes, such as the adequacy of specialty care resources within a neighborhood, can be identified also limits the characterization and recognition of effects of uninsurance on communities (Andersen et al., 2002). While individuals’ demographic, social, economic, and health characteristics are commonly collected and aggregated for population-level analyses (e.g., rates of uninsurance or immunization), ecological variables, which are population-level characteristics that are not created by aggregation of individual-level measures, are much less frequently used in health services research (Sampson and Morenoff, 2000; Diez-Roux, 2001). One example of such an ecological variable would be the presence or absence of a trauma care center within a city to serve its residents. Another quite different ecological measure would be the degree of mutual trust among the city’s residents, based on attitudinal surveys.

Assessing community-level impacts of uninsured populations is made more difficult by ongoing and rapid changes in the organization and financing of health services. Not only do changes in a community’s uninsured rate affect the financial margins of community hospitals, but so do changes in Medicare payment policy and in the relative bargaining power of private insurers and health care institutions. Finally, institutional and program data often are not available for analysis until several years later, whereas economic and public policy environments are in constant flux. This dynamic environment makes it difficult to describe today’s situation with yesterday’s statistics, because policies, markets, and populations have changed in the interval.

Recognizing these limitations, the Committee nonetheless believes that the picture of community-level impacts of uninsured populations provided by this report, although tentative in some respects, is an important starting point for developing more definitive evidence in the future. The Committee also believes that the picture is clear enough to inform some policy choices now.

ORGANIZATION OF THE REPORT

This report provides a new framework for thinking about potential community effects of uninsurance. It assesses the evidence that exists and proposes the research that would be needed to determine the existence and magnitude of other population effects. In Chapter 2, the Committee describes the context for its exploration of potential community effects in the history and present functioning of health care system financing and care for uninsured persons. It presents the public policies and fiscal structures that support the care of uninsured Americans as they have evolved to their current form within the larger context of American health care financing. Chapters 3, 4, and 5 present the Committee’s findings. Chapter 3 examines how the availability of health care for all members of a community is affected by local levels of uninsurance. The results of original

analyses of hospital services and financial margins as affected by local uninsured rates are presented here. Chapters 4 and 5 discuss the hypothesized mechanisms for economic impacts on communities and explore likely effects on the health of the community. A sixth and final chapter presents the Committee’s findings and conclusions and consolidates the data needs and research questions included in the earlier chapters into a research agenda.