Findings

The federal government has played a significant role in supporting the growth of the semiconductor industry since its inception.1 The industry has benefited from close cooperation with government, both through generous procurement contracts such as those related to defense and space exploration, and through research consortia. This support for industry research and development is fully justified. The semiconductor industry’s technological progress has enabled major advances in technologies directly relevant to core government missions including those in national security, communications, health, weather, the environment, and education. In addition, there is growing recognition of the importance of the industry’s contributions to the productivity growth of the U.S. economy.2

The contribution of new technologies to growth, especially information technologies, is now recognized at the highest levels of U.S. policy making. Notably,

Federal Reserve Chairman Alan Greenspan has affirmed the contribution of new technologies to the low inflation, low unemployment, and the continued high growth rates that characterized the U.S. economy in the latter half of the 1990s.3 Much of the technological advance that has made these productivity gains possible is dependent on the unprecedented decrease in cost of increasingly more powerful semiconductors.4

I.THE SEMICONDUCTOR INDUSTRY: A HISTORY OF COMPETITION AND COOPERATION

Firms in the U.S. semiconductor industry have a deserved reputation as fierce competitors in both American and foreign markets. Yet, at key points in the history of the American semiconductor industry, particularly in the decade of the 1980s, the industry launched cooperative efforts through organizations such as the Semiconductor Research Corporation (SRC—1982) and SEMATECH (1987).5 This cooperative research has pooled expertise, lowered costs, and encouraged the dissemination of knowledge across the industry.6 After two decades of relative declines, the decade of the 1990s witnessed a major resurgence in the competitive position of American industry in many sectors.7 As

previous analysis by the National Research Council suggests, an important part of the improvement in the competitive position of American industry can be attributed to the growth in the application of information technologies, particularly after 1995.8 A key challenge of the new century is to sustain the high rate of technological advance that has characterized the semiconductor industry, which underpins the information technologies which have in turn contributed to the growth of the American economy as a whole.9

A.A Steady Increase in U.S. R&D Investments

In aggregate terms, the outlook for R&D investments in the United States appears favorable. On December 20, 2001, Congress approved a record federal R&D budget for FY 2002 of $103.7 billion—a 13.5 percent increase over FY 2001. Total R&D funding reached a preliminary $264.6 billion in 2000, or 2.68 percent of total GDP. This amount reflects an increased R&D share of GDP from 2.63 percent in 1999.10 Total U.S. R&D expenditures show a steady increase. For example, between 1995 and 2000, R&D expenditures increased at an average rate of 7.74 percent.11

B.Increases Mask Substantial Shifts

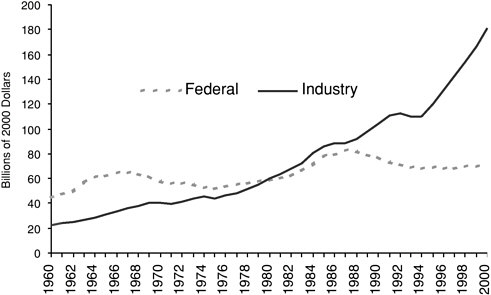

Overall, increases in R&D investments are widely recognized as a good thing in that the social returns on such investments (that is, the gains for society as a whole) are very high, on the order of 40 to 50 percent.12 However, the composition of R&D investments also matters and, in this regard, current trends are a cause for concern. Federal support for R&D has not kept pace with private-sector investments, which have risen dramatically (see Figure 1). In 1980, the federal share of R&D was roughly 48 percent. In 1999, it had fallen to 28 percent of the

FIGURE 1. Total Real R&D Expenditures By Source of Funds 1960–2000.

SOURCE: National Science Foundation, National Patterns of R&D Resources.

total. In part, this reflects U.S. industry’s commitment to developing new products and processes, and, in part, the declines reflect the budgetary constraints and uncertainties of the mid-1990s. Whatever the cause, the current differential trends are a source of concern because, as noted below, the government and industry focus on different phases of the innovation system.

The Nature of Industry R&D

The contribution of industry to the R&D budget has focused more on product development than on basic research. Of the $43.5 billion of federal R&D devoted solely to research in FY2001, $22 billion, or 50.7 percent, was channeled into basic research.13 The semiconductor industry devotes $14 billion to R&D, or 14 percent of sales per year (as of 2000).14 The industry also devotes a significant portion of its R&D effort to university-based research through the Semiconductor

|

BOX A THE MICROELECTRONICS ADVANCED RESEARCH CORPORATION (MARCO)a MARCO, a cooperative program organized under the auspices of SRC, funds and operates a number of university-based research centers in microelectronics as part of its Focus Center Research Program (FCRP).

|

Research Corporation, the jointly funded Focus Center Research Programs (see Box A), and industry R&D collaboration through SEMATECH.15

In general, however, industry has been less inclined to fund the basic research on which the future growth of the economy ultimately depends.16 Yet, much of the current technological progress the United States and, indeed, the rest

of world enjoys today rests on inventions and investments made 30 and 40 years ago.17 In addition, many of the large industry laboratories that once supported major technological advances, such as the transistor, no longer exist or have seen their research strategies substantially modified.18

C.The Expansion of Foreign National R&D Programs

As noted above, governments around the world have played an active role in the development of the semiconductor industry. In its early years, the U.S. industry received substantial support for research and development from the federal government, particularly to achieve national missions in defense (e.g., the Minuteman program) and in space exploration (e.g., the Apollo program). Governments around the world have also taken an active approach in supporting the entry of their national firms into the global semiconductor market.19

Japan’s early VSLI program, for example, helped bring its producers to the forefront of the industry in only a few years.20 In 1987, SEMATECH was founded to aid a beleaguered U.S. industry. Korea followed in the late 1980s and 1990s with generous state-supported financing for DRAM production by its chaebols. Taiwan’s innovative policy mix of equity finance, technical support, favorable tax treatment, and the development of the Hsinchu Science and Technology Park Complex helped propel its industry forward in the 1990s. Enhanced R&D support and other programs are not confined to new entrants. Several European countries, operating in conjunction with the European Union, have put in

place programs that have contributed to a strengthened competitive position for European producers.

A wide variety of policy instruments—ranging from substantial government funding for national R&D programs to favorable tax treatment (e.g., short depreciation allowances) and, in the past, trade measures such as tariffs and private restraints of trade (i.e., restrictive internal market arrangements)—have been used to promote domestic semiconductor firms. Given the perceived contributions of SEMATECH, countries and regions interested in supporting the semiconductor industry have adopted the consortium model as a means of encouraging cooperation among firms within a national industry and as a vehicle for providing government support.

The combination of technical challenges facing the semiconductor industry and the perceived success of cooperative programs in the United States have led policy makers in several countries to increase government funding in support of their national semiconductor industries.21Box B describes current trends in national programs to support national semiconductor industries.

II.THE SEMICONDUCTOR INDUSTRY FACES SIGNIFICANT CHALLENGES

The substantial increases in semiconductor power—predicted by Moore’s Law—are becoming more challenging to continue. To do so, the industry must overcome a series of technical hurdles, including the need for both new materials and designs. It must also address the need for skilled labor required to overcome these hurdles amidst emerging changes in the structure of the industry.

Given the economic importance of the industry, there is very limited research on the impact of SEMATECH on R&D in the semiconductor industry, its role in the resurgence of the U.S. industry, and its potential lessons for other U.S. consortia.22 With regard to the industry as a whole, there is limited economic research as to the sources of the industry’s pronounced cyclical swings, its contributions to productivity, and its subsequent impact on the economy at large. Scant public policy attention has been focused, as well, on the research requirements needed to keep this industry on its positive course, and on the skilled labor and advanced training needed to sustain this trajectory.

|

Box B Significant Global Trends in the Semiconductor Industry as a Result of National Programs

|

A.Need for Highly Skilled Human Capital

1.Continued Progress Depends on the Supply of Talented and Skilled Labor.

In order for the semiconductor industry to maintain high growth rates and respond to the growing challenges within the industry, the United States faces a long-term need to bolster support for highly skilled workers. While, at this writing, the industry is showing the effects of a historically sharp downturn, this cyclical feature should not mask the growing long-run demand for the skilled workers needed to keep the industry on its current growth path. Sustaining the industry’s remarkable rate of technological advance requires persistent creativity and ingenuity. Such an innovative environment is sustained by a trained workforce well grounded in the disciplines—such as physics, mathematics, and engineering—that underpin the semiconductor industry. This long-term growth in the demand for skilled labor has emerged against the decline in U.S. federal funding for these disciplines (see Figure 1). The United States is also competing globally to generate and attract the human capital necessary to the long-term health and development of the semiconductor industry.23

2.Generating a Skilled and Qualified Workforce in the Microelectronics Industries.

Despite ongoing initiatives to address the skilled manpower needs of the industry by organizations such as the Semiconductor Research Cooperation (SRC), there is concern within the industry as to whether there will be enough skilled graduate students to meet future demand—a problem some believe is worsening. The SRC has documented a significant drop in the graduation rate of electrical engineering students in the United States from 1988 to the present and projects no recovery from these low levels in coming years.24

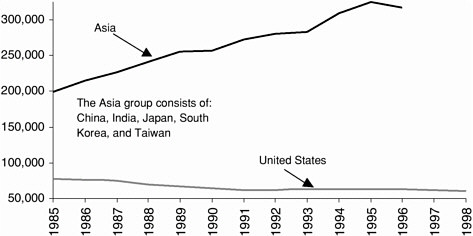

To compound this challenge, competition for the limited pool of talented workers in engineering fields is global, and U.S. industry will face increased difficulty in attracting the young, skilled workers it needs to continue growing. The United States exhibits one of the lowest yields, 5.3 percent, in producing engineers when comparing the number of bachelor’s degrees in engineering to all bachelor’s degrees. In the sheer production of engineers on a yearly basis, the U.S. is surpassed by Asian nations as a group by almost six times.25 Other na

FIGURE 2 Bachelor’s Degrees in Engineering: Asian and U.S. Universities.

SOURCE: National Science Foundation.

tions in Europe and Asia have recognized this growing demand for skilled labor in microelectronics and appear to be making a concerted effort to address this global challenge (see Figure 2).26

Recommendations for a resolution to this general trend are beyond the purview of this report. The declines in the supply of engineers and the reductions in the federal spending on these disciplines are likely to augment the challenge faced by the industry as it seeks new solutions to pressing technical problems.

B.Structural Changes in the Industry Present New Challenges and Opportunities

1.Vertical Specialization and the Emergence of the Foundry Model.

The semiconductor industry is becoming more vertically specialized. For example, the foundry model—low-cost, state-of-the-art fabrication facilities (“fabs”) found in Taiwan and other Asian nations, where firms produce semiconductors under contract with other companies—is revolutionizing the industry. The foundry model of production can offer substantial cost savings in manufacturing new generations of chips. In some cases, these cost savings may be the result of lower costs of capital reflecting preferential tax treatment or more direct government subsidies for industries that are viewed as strategic by government policy makers.

The emergence of design houses—firms which specialize in the design of semiconductors only and do not produce them—is yet another sign of vertical specialization in the industry and functions congruently with the foundry model of production. Some analysts are concerned that, over time, the development of new technologies, especially manufacturing technologies, may become more closely associated with the foundries themselves. To the extent that offshore design houses are involved in this process, significant technical capability and know-how may be transferred. The consequences of this phenomenon are not clear, nor are they unidirectional. For example, in the near-term, the availability of these fabrication facilities can work to the benefit of some U.S. firms—espe-cially those that focus on design. This specialization stands in contrast to the U.S. industry, which has typically housed both of these functions under one roof. In part, these trends reflect the global scale of the industry; they reflect as well the active industrial policies of leading East Asian economies. For example, Singapore and Malaysia have contributed significant public funds and have extended tax incentives to companies constructing “fabs,” while Taiwan has approximately 100 “design houses,” also supported through various government incentives.27

While far from certain, one foreseeable outcome of the growth in this model could entail a steady increase in U.S. manufacturers’ commissioning “design houses” in Taiwan or Europe, and then contracting a foundry-firm to manufacture that particular design.28 In any case, U.S. merchant device producers may face increasing challenges from the substantial capacity generated by government-supported fabrication facilities abroad.29 At the same time, as noted above

and in the Introduction, fabless producers in the United States benefit from greater opportunities to obtain lower-cost access to state-of-the-art fabrication facilities. If the rate of growth and ultimate impact of this vertical disintegration within the industry are unclear, there is growing concern about the impact of these trends on the R&D funding that drives the industry. To date, the foundries have tended to be fast followers—rapidly adopting the new manufacturing technologies that drive the industry. As foundries gain market share, it is not clear that the necessary levels of R&D investment required to sustain the industry’s growth will be made.

2.The Risk of Knowledge and Technology Transfers.

A further possible challenge to consider from a U.S. perspective concerns the relationship between the foundries and the design manufacturers. In order to take advantage of the foundry model as an outsourcing alternative to in-house production, designs must be shared with the foundries. As particular aspects of semiconductor design are necessarily shared with foreign-owned and controlled fabrication facilities, over time some elements of the U.S. industry may see their comparative advantage in design erode. At the same time, reverse engineering is immensely complex, time-consuming, and, in principle, limited by intellectual property protection. Nonetheless, a great deal of production knowledge occurs on a “learning by doing” basis. Again, the long-term consequences of this process are not clear, but the potential consequences of these developments for U.S. industry, economic growth, and national security suggest that better data collection and further analysis would be appropriate.30

C.Significant Technical Challenges

Discovering a method that allows for the continued improvement in semiconductor productivity presents another significant challenge to the semiconductor industry. Much of the progress to date has been the result of scaling—progressively shrinking component size. This process has been the basis of the growth in the semiconductor industry for the past 30 years. Once scaling reaches its limits, the productivity growth of the industry may also diminish. The long-term challenge will be to find new methods to continue the progress in semiconductor productivity, which entails development of new materials and design structures. (Some of these major material challenges are listed and described in Box C.)

Another prominent challenge involves the evolution of lithography toward the use of smaller wavelengths. In the past, the industry has produced several generations of chips by using a specific lithography system with a particular wave-length.31 This system of lithography has now evolved to one where new wavelengths are introduced and the system is changed in fewer generations. This development has placed a large burden on the equipment industry to keep pace with these rapid changes. For instance, in some cases where the limits of prevailing systems have been approached, companies have resorted to using other, less efficient methods to circumvent the true material barriers. These methods of circumvention, however, do not present real, long-term solutions and in many cases represent a “huge tax on the industry in terms of time and resources.”32

The future of shorter wavelengths needed for the increase in semiconductor productivity appears to be approaching, and thus there is a need to prepare the shift to new lithographic systems such as EUV (Extreme Ultra-Violet).33 However, these changes require significant research and development. Some experts have suggested that with current levels of investment, it is not reasonable to expect to find solutions relatively soon.34

III.INTERNATIONAL TRENDS

A.International Convergence in Semiconductor Technology

The gap between the United States and countries such as Taiwan and South Korea in semiconductor industry technology is narrowing. Korea and Taiwan exhibit global strength and significant progress in memory technologies and foundry-based fabrication facilities. Over time, these trends point towards a shared global leadership. Complacency about the strength of the U.S. industry vis-à-vis its global competitors would be misplaced. As one recent Academy analysis observed:

The revival of the U.S. semiconductor industry is an impressive feat, for which government policymakers and industry managers, engineers, and researchers should share in the credit. But the unexpected nature of this revival, its rather complex causes, the contributions to it of cyclical factors, and the fragility of its foundation all suggest that competitive strength in this industry cannot be taken for granted….In other words, U.S. semiconductor firms must maintain their stra

|

BOX C Long-Term Challenges in the Semiconductor Industrya Over the long termb, some of the majorPerformance Enhancementchallenges in the semiconductor industry entail:

Some of the major challenges in the long run forCost-Effective Manufacturingin semiconductors are:

|

tegic agility and strength in product innovation while avoiding significant erosion in their manufacturing capabilities in order to maintain their strength. The task will require imagination and collaboration among government, industry, and academia.35

B.An Increase in Global Partnerships

Global partnerships have become very common in the semiconductor industry. Both Europe and Asian countries have established consortia in order to cre

|

ate industry standards, map out future issues and challenges, and conduct collaborative research. In both Asia and Europe, policy makers recognize the potential contributions of consortia to overcoming the myriad technical challenges facing the semiconductor industry. Many of the leading figures in the industry, though not all, believe the effort to overcome the multiple technological challenges faced by the industry should be international in scope if these challenges are to be met in the required timeframes.36 National and international consortia are likely to be a key element in encouraging the research that will aid in meeting these challenges.

1.Private partnerships and government-industry partnerships represent an integrated national approach to develop semiconductor technology.

a. Japan’s Pre-competitive R&D Programs. In Japan, Selete (SEmiconductor Leading Edge Technology Corporation), a joint-venture company established in 1996, conducts R&D on behalf of the Japanese semiconductor industry. Selete, which is not directly funded by government, has been successful in the promotion and evaluation of technologies, developing advanced technologies, and carrying out special projects. By comparison, ASET (Association of Super-Advanced Electronics Technologies) is completely funded by the government and focuses on equipment and chip R&D for 70- to 100-nm technology.

b. Europe’s Multinational, Multi-firm Partnerships. MEDEA (Microelectronics Development for European Applications) is a multinational, multifirm partnership. It is similar to SEMATECH in that it was jointly financed by government and industry. MEDEA has helped develop a better understanding between semiconductor suppliers and system houses, helped develop a better idea of where to focus R&D resources, and fostered closer cooperation among companies in different European countries—both vertically and horizontally. MEDEA officials report that these efforts demonstrate that collaboration in the semiconductor industry can have positive effects for society (employment in the industry increased) and that it can be a productive use of public funds. As a result of MEDEA’s success, MEDEA-Plus was initiated in 2001 to address the challenges facing the semiconductor industry noted above.

c. Government-industry Partnering in Taiwan. The semiconductor industry in Taiwan was born out of government support and partnerships in the mid-1970s. Today, the major semiconductor companies in Taiwan are world leaders in their specialties. One of the most successful joint ventures between industry and government is Taiwan Semiconductor Corporation (TSMC). TSMC is a positive example of a government-industry equity partnership in terms of return to society on public investments.37 The dynamic effects for the Taiwanese economy associated with the establishment of a rapidly growing, highly competitive industry are substantial.38

IV.THE IMPACT OF SEMATECH: A GOVERNMENT-INDUSTRY PARTNERSHIP

SEMATECH is widely perceived as effective in accomplishing its goals. The consortium’s members believe that participation in the consortium has been worthwhile, as evidenced by their continued participation and contributions. This positive assessment is further reflected in the industry’s willingness to discontinue public funding while continuing to support the consortium.

The foreign competitors of the U.S. industry share the perception that SEMATECH contributed to the resurgence of the American semiconductor industry and have established a variety of similar programs. These programs are often on a significantly larger scale and have greater underlying political support. Furthermore, a significant number of foreign producers have affirmed their belief in the program’s effectiveness by joining SEMATECH since it became an international consortium in 1999.39

These trends underscore the importance of public-private cooperation to support research and technology development in the semiconductor industry. In light of the growing significance of R&D collaboration in both the equipment and device industries, providing policy and financial incentives to encourage such cooperation is an increasingly important way to sustain the investments needed to transition to successive generations of new technologies.40

A.Sources of SEMATECH Contributions

1.Flexible Objectives and Industry Leadership

By definition, an R&D consortium’s contributions (Box D) are due in part to its ability to adapt its goals to the conditions of a rapidly evolving industry.41 The cost sharing arrangement with the government and industry management of the research agenda has contributed to this flexibility. Indeed, while it benefited from strong leadership, no single entity dominated the consortium or determined its direction. Members, including Department of Defense officials, reached a broad consensus on technical goals and then left the consortium management to implement the program.

The industry interaction within the consortium, and between the consortium members and the suppliers, improved the dynamics between the device makers and the equipment industry, with collaboration generating new technical perspectives for the participants and encouraging the give-and-take between manufacturer and supplier necessary to expedite the technology development process.

2.Analyzing SEMATECH

Measuring the contributions of research consortia is a difficult task (Box E). As noted in this report, there have been relatively few empirical analyses of the impacts of R&D cooperation on industrial R&D.42 For the semiconductor industry, some empirical analysis suggests that the consortium has boosted the “effec

|

Box D Contributions of the Consortium SEMATECH has made a variety of important contributions to the health of the semiconductor industry in the United States. For example, the consortium has:

|

|

Box E Organizing Successful Consortia Because of its contributions, SEMATECH is sometimes considered a model for future public-private partnerships.a Some of its lessons for organizing a successful consortium are:b

|

tive” R&D level of its members.43 The work of Flamm and Wang suggests that SEMATECH reduced the R&D expenditures of its membership somewhat, in part by eliminating duplication.44 In essence, if the number of dollars spent on similar R&D projects across firms is reduced, and the yield of overall industry R&D is unchanged, then this is a better outcome from both a social standpoint, for society, and for industry since resources are freed which can be put to productive use elsewhere. This is a positive result both for the firms and for society as a whole. Moreover, this outcome lends credence to the idea that a consortium can add to the dynamic efficiency of both its member firms and the industry as a whole.

While the precise measurement of contributions is difficult, SEMATECH is widely believed, within the industry, both in the United States and abroad, to have made a positive contribution to the resurgence of the U.S. semiconductor industry. More indirectly, the consortium’s activities have contributed to greater cooperation among producers, suppliers, and the government. For example, the current promising cooperation on next-generation lithography tools, (i.e. the EUV Consortium) illustrates this enhanced willingness to collaborate in innovative ways. This positive perception of SEMATECH has contributed to its emulation, notably in foreign programs to support national or regional semiconductor industries and among other U.S. industries, (e.g. in optoelectronics and nanotechnologies).45 More broadly, SEMATECH helped sustain the rapid technological progress of the industry as projected by Moore’s Law. This technical progress was facilitated by the collaborative research encouraged by the consortium, including the development of the Semiconductor Industry Roadmap.

For its part, the government partner achieved many of its objectives. The Department of Defense achieved its goal of maintaining a robust, technologically advanced manufacturing capability within the United States. SEMATECH thus helped the government achieve a key objective, namely, sustaining a U.S.-based industry able to provide cutting-edge, low-cost devices to support defense requirements46 and thereby avoiding the risk of dependency on foreign suppliers for U.S. defense systems.47 Throughout the decade of the 1990s, the Defense Department was able to acquire higher-performance, lower-cost components from

|

43 |

See Flamm and Wang, op. cit. |

|

44 |

Ibid. |

|

45 |

See Box B in the Introduction in this volume. See also National Research Council, Small Wonders, Endless Frontiers: A Review of the National Nanotechnology Initiative, Washington, D.C.: National Academy Press, 2002. |

|

46 |

A healthy U.S. industry also ensures a surge capacity for the defense industrial base, should it be required. |

|

47 |

The erosion of the U.S. semiconductor industry’s position was a source of growing concern to federal defense officials and was reflected in the creation of the National Advisory Commission on Semiconductors (NACS). One of the NACS’ missions concerned the dependency of modern weap |

commercial suppliers than would have been available from a dedicated defense production facility. This trend contributed to dual-use defense acquisition designed to benefit from the rapid evolution of commercially available semiconductors characterized by rapidly increasing performance and falling costs.48

The combination of rapid gains in semiconductor capabilities and sharply falling costs has contributed to the government’s capacity to carry out many other non-defense missions more efficiently. These contributions are reflected in the economy as a whole. Also, as noted above, the U.S. economy recorded substantial gains in productivity growth between 1995 and 1999, with productivity growth more than double that of the 1973-1995 period. The Council of Economic Advisers attributed “these extraordinary economic gains” to three factors, namely, technological innovation, organizational changes in businesses, and public policy.49 Two of these factors concern information technology, in particular the simultaneous advances in information technologies—computers, hardware, software, and telecommunications—which combine these new technologies in ways that sharply increase their economic potential. Progress in semiconductor capabilities enabled advances in information technologies, driving innovation in each of these product areas. In short, the government and the economy as a whole have benefited from the contributions of a robust U.S. industry.50

|

|

ons systems on state-of-the-art semiconductor devices. Specifically, under the legislation creating the Commission, Congress notes in its findings that: “Modern weapons systems are highly dependent on leading-edge semiconductor devices, and it is counter to the national security interest to be heavily dependent upon foreign sources for this technology.” The charter further states that this Committee shall “identify new or emerging semiconductor technologies that will impact the national defense or United States competitiveness or both.” For the objectives set forth for NACS, see <http://www4.law.cornell.edu/uscode/15/4632.html>. |

As described in greater detail in the Introduction, the SEMATECH consortium’s contributions to the resurgence of the U.S. industry were significant but are best understood as one element of a series of public policy initiatives that collectively provided a positive policy framework for U.S. semiconductor producers. Overall, SEMATECH’s record of accomplishment was achieved in no small part through the flexibility granted its management and the sustained support provided by DARPA, the public partner, complemented by the close engagement of its members’ senior management and leading researchers.

Recommendations

The Committee’s recommendations outline a series of modest steps that nonetheless may prove important to the long-term welfare, economic growth, and security of the United States.

RESOURCES FOR UNIVERSITY-BASED SEMICONDUCTOR RESEARCH

To better address the technical challenges faced by the semiconductor industry and to better ensure the foundation for continued progress, more resources for university-based research are required.

The Committee believes that universities have an important role in maintaining a balance between applied science and fundamental research. This balance is key in generating ideas for future research.

The Committee suggests consideration of the development of three-way partnerships among industry, academia, and government to catalyze progress in the high-cost area of future process and design. These partnerships would:

-

Sponsor more initiatives that encourage collaboration between universities and industry, especially through student training programs, in order to generate research interest in solutions to impending and current industry problems.

-

Increase funding for current programs.51 Research programs that are already operational, such as the Focus Center Research Program developed by the SRC, could usefully be augmented through substantially increased direct government funding. These centers also represent opportunities for collaborative research with other federal research programs, such as those supported by the National Science Foundation.

-

Create Incentives for students. A key role for universities is to ensure the flow of technical innovation and skills that originate with students. In order to address the undersupply of talented workers and graduate students in the industry, more incentive programs should be established. Since professors typically respond to appropriate research incentives, augmented federal support for programs that encourage research in semiconductors would attract professors and graduate students.52 In addition, specific incentive programs could be established to attract and retain talented graduate students.