Executive Summary

The discontinuity of coverage and complete lack of health insurance among tens of millions of Americans every year entail costs for our society in

-

lost health and longevity, including health deficits leading to developmen-tal and educational losses for children;

-

financial risk, uncertainty and anxiety within families with one or more uninsured members;

-

financial stresses for and instability of health care providers and institutions in communities with relatively high uninsured rates that reduce the scope and amount of available health services, including public health services; and

-

lost workforce productivity.

As a nation and as public law, we invest in the health of those who have health insurance, through tax subsidies and publicly sponsored coverage. About 85 percent of the U.S. population benefit from this investment. As a society, we also spend substantial public resources for health care services to the remaining 15 percent of Americans—the more than 41 million people who lack coverage every year. Despite this public spending on health services for the uninsured, those who lack coverage have worse health outcomes than do similar individuals with insurance, because dollars alone do not confer the health benefits that continuous coverage does. If all members of society bear certain risks and costs from spillover effects of uninsurance, all should realize some benefit, at least indirectly, from a public policy ensuring that everyone has coverage.

Hidden Costs, Value Lost: Uninsurance in America tallies some of the most clearly identifiable economic and social costs of uninsurance, as described in the

Committee’s previous four reports. The Committee concludes that maintaining an uninsured population of 41 million results in a substantial loss of economic value that improved health would provide uninsured individuals. The Committee also believes that, as health care interventions become ever more effective in improving health and extending life, unequal access to such care, as documented in Care Without Coverage and Health Insurance Is a Family Matter, becomes increasingly unjust.

Americans devote more economic resources to health care than people in any other nation in the world, both in total dollars spent ($1.236 trillion for personal health care services in 2001) and as a percent of the gross domestic product (14 percent) (Levit et al., 2003). Access to health care is valued highly and widely throughout American society. In this report, the Committee takes a broad, societal perspective as it examines the performance of economic resources devoted to health care, health insurance, and alternative uses for these resources, which include personal resources, firms’ investments, and public monies.

The societal perspective allows the Committee to evaluate our society’s failure to invest in health insurance for 15 percent of the population from the standpoint of the public interest, rather than the interest of any particular individual or group within society. Practically, the societal perspective reflects the kind of aggregate, population-based information and national data sets that the Committee was able to use in its analyses. More importantly, as a matter of principle or ethical choice, the societal perspective values the interests of each individual member of society equally and allows the Committee to examine the fairness of the distribution of the costs and benefits of public policies and investments in health (Gold et al., 1996a).

WHAT ARE COSTS OF UNINSURANCE?

What do we mean by cost? This report draws on information developed within several different analytic frameworks because of the breadth of the issues encompassed by the “costs of uninsurance.” When uninsured people obtain coverage, their use of health services would be expected to increase as a result of improved financial access. The majority of the costs due to being uninsured that the Committee has identified are not health services costs (that is, uncompensated care or expensive hospitalizations because of delayed treatment) but rather result from the poorer health outcomes of uninsured individuals.

Families with uninsured members bear costs resulting from the financial burdens and risks of out-of-pocket health care spending and, because children’s receipt of health care in practice depends on their parents’ coverage status, children in families with uninsured parents are less likely to receive adequate services.

The spillover costs of uninsurance experienced within communities result from both the poorer health of uninsured populations and the demands made on local public budgets and on providers to support care for those without coverage. Thus, this report considers both the extent and the source of resources devoted to

the care of people without health insurance and the economic cost implications of the poorer health they experience because they lack coverage.

THE VALUE LOST IN POORER HEALTH

Given the key role of health coverage in improving health outcomes, how much health is lost with a population of more than 41 million uninsured? In this report, the Committee adapts an analytic strategy that has been used to assess the value of life-saving and health-improving medical interventions, imputing a monetary value to the years of expected life that an individual is estimated to have in particular states of health (e.g., excellent, fair, poor; with controlled hypertension, or prostate cancer in remission, or no functional limitations).

The present value in money terms of the “stock” of years of life in certain expected states of health has been coined “health capital” (Grossman, 1972; Cutler and Richardson, 1997). This analytic concept of health capital is related to the approach used by government agencies that regulate public health and safety (e.g., Food and Drug Administration, Department of Transportation, Environmental Protection Agency) to evaluate and compare alternative public policies that mitigate risk and improve health. This approach involves estimating the value of averted risk as expressed by the expected number of lives saved (statistical or anonymous lives when the policy is implemented) to determine whether the benefit of reducing a particular risk or harm justifies the costs involved in adopting such a policy. The Committee has applied the analytic concept of health capital to the health risk it has been concerned with—the risk of being uninsured, compared to having coverage. Stated in the converse, the Committee has estimated the aggregate personal economic value that would be added if the entire U.S. population had health insurance coverage, compared with the status quo, which leaves 16.5 percent of the population under age 65 without coverage.

The Committee commissioned an analysis estimating the value of diminished health and longevity within the U.S. population as a result of uninsurance. Economist Elizabeth Richardson Vigdor combined information on the longevity, prevalence of health conditions, and health-related quality of life for insured and uninsured populations. The relative mortality rates for insured and uninsured populations were drawn from the Committee’s earlier systematic literature review of health outcomes as a function of health insurance status and reflect a 25 percent higher mortality rate within the uninsured population (IOM, 2002a,b). Vigdor’s estimates constitute a range of values for the forgone health of uninsured individuals, based on different assumptions about the relative health status of insured and uninsured populations.

Imputing a value of $160,000 to a year of life in perfect health and calculating the present value of future years with an annual discount rate of 3 percent, Vigdor estimated that the economic value of the healthier and longer life that an uninsured child or adult forgoes because he or she lacks health insurance ranges between $1,645 and $3,280 for each additional year spent without coverage

(Vigdor, 2003). This value differs for people of different ages and for men and women because of differences in underlying health status and life expectancy. These estimated benefits could be either greater or smaller if unmeasured personal characteristics were responsible for part of the measured difference in morbidity and mortality between those with and those without coverage.

The Committee’s best estimate of the aggregate, annualized cost of the diminished health and shorter life spans of Americans who lack health insurance is between $65 and $130 billion for each year of health insurance forgone. These are the benefits that could be realized if extension of coverage reduced the morbidity and mortality of uninsured Americans to the levels for individuals who are comparable on measured characteristics and who have private health insurance. This estimate does not include spillover losses to society as a whole of the poorer health of the uninsured population. It accounts for the value only to those experiencing poorer health and subsumes the losses to productivity that accrue to uninsured individuals themselves.

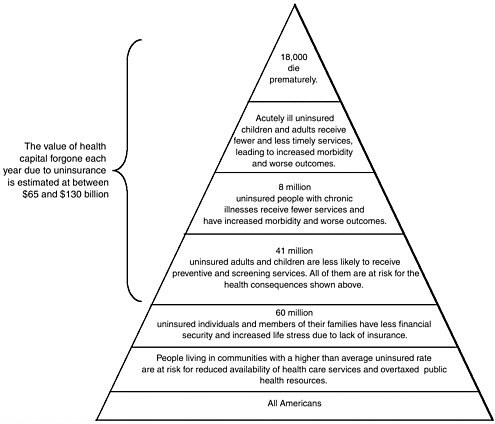

These estimates constitute an initial effort to develop an integrated and coherent framework for evaluating a number of economic costs attributable to the lack of health insurance; they are not definitive but suggest the direction that further research and analysis might take. Figure ES.1 illustrates the costs of uninsurance that the Committee has documented in its work to date. The bracket to the left of the pyramid shows the costs that are captured in the estimate of the economic value of forgone health by those who lack coverage, and the costs that are additional to that estimate.

HEALTH CARE COSTS OF THE UNINSURED

In its analysis of the costs of health care now used by those who lack health coverage, the Committee finds that

-

Uninsured children and adults are less likely to incur any healthcare expenses in a year and, on average, incur health care costs well below half of average spending for services by all those under age 65.

-

People who lack health insurance for an entire year have out-of-pocket expenditures comparable, in absolute dollar amounts, to those of people with private coverage. Uninsured individuals pay for a higher proportion of the total costs of care rendered to them out of pocket, however, compared to insured individuals under age 65 (35 percent, compared with 20 percent), and they also have much lower family incomes. Out-of-pocket spending for health care by the uninsured is more likely to consume a substantial portion of family income than out-of-pocket spending by those with any kind of insurance coverage.

-

The total cost of health care services used by individuals who are

FIGURE ES.1 Consequences of uninsurance.

-

uninsured for either part of or the entire year is estimated to be $98.9 billion for 2001.

-

The best available estimate of the value of uncompensated healthcare services provided to persons who lack health insurance for some or all of a year is roughly $35 billion annually, about 2.8 percent of total national spending for personal health care services.

The direct costs of uncompensated care provided to uninsuredpeople are largely borne by those who pay taxes. Public support from the federal, state, and local governments accounts for between 75 and 85 percent of the total value of uncompensated care estimated to be provided to uninsured people each year (Hadley and Holahan, 2003a). Public subsidies to hospitals are paid through

-

federal Medicaid and Medicare disproportionate share hospital (DSH) pay-ments and other financing mechanisms, and

-

state Medicaid DSH payments and other state and local subsidies and budget allocations for hospital care and institutional operating costs.

These subsidies amounted to an estimated $23.6 billion in 2001, approxi-mately the same as the value of hospital bad debts and charity care projected for that year from the American Hospital Association’s annual financial survey results. The Committee finds mixed evidence that private payers subsidize uncompensated hospital care. Analysts have proposed that possibly $1.6 to $3 billion annually in hospital revenues from private payers are used to cover hospitals’ uncompensated care costs (Hadley and Holahan, 2003a). The Committee concludes that the impact of any such “shifting” of costs to privately insured patients and insurers is unlikely to affect the prices of health care services and insurance premiums.

Even with the considerable federal support for uncompensated care (particularly to hospitals), when states provide health care in kind to medically indigent residents rather than through insurance programs like Medicaid and the State Children’s Health Insurance Program, the costs of direct provision fall disproportionately on the local communities where care is provided (IOM, 2003a). Given the lower average incomes of uninsured Americans and the associated socioeconomic profiles of the communities in which rates of uninsurance are higher than average, these communities have relatively little capacity to support the provision of health care services. Financing the health care of those who now lack health insurance through federal or federal and state coverage mechanisms would spread the burden of publicly supported care over a broader tax base than that which supports uncompensated care for those without coverage.

QUALITY OF LIFE AND SECURITY FOR FAMILIES

Uninsured individuals and families bear the burden of increasedfinancial risk and uncertainty as a consequence of being uninsured. Although the estimated monetary value of the potential financial losses that those without coverage bear is relatively small (compared to the full cost of their services) because of uncompensated care, the psychological and behavioral implications of living with financial and health risks and uncertainty may be significant. The Committee estimates that the financial risk borne by those without coverage has an economic cost of - $1.6 to $3.2 billion. This would be the value, to those now lacking coverage, of the financial protection provided by health insurance.

Even in families in which all members are insured, the concern about losing coverage remains genuine. One, some, or all members can lose health insurance at some point, because of lifecycle events such as leaving school or retiring or because of economic conditions that result in the loss of income or workplace benefits, such as becoming unemployed or changing jobs. This lack of social and economic security, experienced by virtually all Americans except for those who

have gained Medicare coverage on a permanent basis (i.e., those over age 65 or with end-stage renal disease), is truly a hidden cost of our patchwork approach to health insurance.

OTHER COSTS OF UNINSURANCE

Developmental Losses for Children

Uninsured children are at greater risk than children with healthinsurance of suffering delays in development that may affect their educational achievements and prospects later in life. Good health and meeting developmental milestones in infancy and childhood affect individuals’ educational attainment, earning capacity, and long-term health. The Committee’s estimate of health capital forgone by uninsured children and adults that was presented earlier subsumes these developmental losses. The Committee includes its review of studies and earlier findings regarding worse health outcomes among uninsured children to provide an empirical underpinning to its approach to estimating health capital losses resulting from the lack of health insurance.

Costs to Public Programs

The Committee considered other costs that are attributable to uninsurance without attempting to quantify them. Although the costs of morbidity and productivity losses associated with individual health conditions have been estimated, there is no body of research with which to investigate these effects as a function of health insurance status in a systematic way. Thus the Committee has identified public program and workforce impacts of health insurance status that can be inferred from related evidence about the effects of health status on disability and productivity and the effects of health insurance on health status, largely based on the Committee’s reports Care Without Coverage and Health Insurance Is a Family Matter.

Based on its findings and conclusions about health outcomes as a function of health insurance status in its earlier reports, the Committee concludes that public programs, including Medicare, Social Security Disability Insurance, and the criminal justice system almost certainly have higher budgetary costs than they would if the U.S. population in its entirety had health insurance up to age 65. It is not possible, however, to estimate the extent to which such program costs are increased as a result of worse health due to lack of health insurance.

As calculated for this study, the value of healthy years of life forgone by those without health insurance does not include any health and longevity impacts that occur after age 65, when Medicare covers virtually the entire population. The Committee’s conservative assumption in estimating the value of health lost likely underestimates the health benefits enjoyed by individuals who would gain addi-

tional health and longevity after age 65 if they had health insurance continuously prior to that age. It is also likely to underestimate the potentially reduced costs to the Medicare program of financing services for persons with pent-up demand for care or health “deficits” as a result of having been without coverage previously. For example, individuals who have poorly controlled hypertension or diabetes or undetected high cholesterol because of irregular or no medical attention to their condition enter the Medicare program with more comorbidities and worse health status than do persons whose conditions have been treated over time.

Likewise, increasing disability among the working-age population (even as the disability rate has decreased over the past two decades for those older than 65), suggests that health and functional status improvements that health insurance provides could reduce disability insurance claims.

In the case of serious mental illness, for example, there can be substantial spillover costs of uninsurance to society. More than 3 million adults in the United States have either schizophrenia or bipolar disorder (manic-depressive disease), which can involve psychosis and aberrant behavior. Fully 20 percent of the adults with one of these conditions who do not reside in institutions lack health insurance. Although being insured is no guarantee that mental health services are a covered benefit or that one will be treated appropriately for mental health problems, persons with either public or private health insurance are more likely to receive some care for their condition than are those without any coverage. Between 600,000 and 700,000 persons with severe mental illness are jailed each year. Ironically, contact with the criminal justice system increases the chances that someone with a severe mental illness will receive specialty mental health services. The costs of less effective treatment resulting from lack of health insurance likely contribute to the costs of incarcerating people with serious mental illness.

Workforce Participation, Productivity, and Employers

Illness and functional limitations impair people’s abilities to work and conse-quently impose the costs of forgone income and productive effort on those who are sick and disabled, their families, and potentially on their employers as well. The costs for employers of productivity losses on the job for workers with particular illnesses have been increasingly well studied within the past decade. The impact that providing workers with health insurance has on workplace productivity, however, is less well documented. What evidence exists suggests that, although workers’ health status may improve as a result of having coverage, individual employers probably do not lose financially, on net, as a result of impaired productivity on the job if they do not currently offer their workers health insurance benefits. Any systemic, regional, or national losses of productivity or productive capacity as a result of uninsurance among nearly one-fifth of the working-age population cannot be measured with the data now available.

Costs for Communities

Not only those who lack coverage but others in their communitiesmay experience reduced access to and availability of primary care, specialty, and hospital services resulting from relatively high rates of uninsurance that imperil the financial stability and viability of health care providers and institutions. Communities that have higher than average rates of uninsurance are more likely to experience reduced availability of hospital-based services and critical community benefits such as emergency services and advanced trauma care (IOM, 2003a; Gaskin and Needleman, 2003; Needleman and Gaskin, 2003).

In addition, population health resources and programs, including disease surveillance, communicable disease control, emergency preparedness, and community immunization levels, have been undermined by the competing demands for public dollars for personal health care services for those without coverage. Because uninsured individuals and families are much less likely than are those who have coverage to have a regular health care provider, they are not well integrated into systems of care. Consequently, population-level disease surveillance and health monitoring is reduced in communities with large uninsured populations.

THE COST OF THE HEALTH CARE THATUNINSURED PEOPLE WOULD USE IF THEY HAD COVERAGE

In order to evaluate fairly the cost of the better health that uninsured Ameri-cans could be expected to achieve if they had health insurance, the Committee reviewed estimates of the value of the additional health services that would be provided to the uninsured once they became insured. Estimates of the incremental costs of health services that the population that now lacks insurance could be expected to use if they gained coverage range from $34 to $69 billion (in 2001 dollars). These estimates should not be construed as the costs of any particular plan to reform health care financing to provide health insurance to those now without it. This range of estimates, derived from three independent analyses, assumes no other structural changes in the systems of health services delivery or finance, scope of benefits, or provider payment (Long and Marquis, 1994; Hadley and Holahan, 2003b; Miller et al., 2003). The ultimate cost of any reform will depend on the specific features of the approach taken. These estimated costs amount to 2.8–5.6 percent of national spending for personal health care services in 2001, equivalent to roughly half of the 8.7 percent increase in personal health care spending between 2000 and 2001.

COSTS AND BENEFITS CONSIDERED TOGETHER

Table ES.1 summarizes the Committee’s estimates of the amounts and sources of payment for the health care currently provided to uninsured Americans, the

TABLE ES.1 Estimates of Current Annual Cost of Health Care Services for Full- and Part-Year Uninsured Individuals, Projected Incremental Annual Costs of Services If Insured, and Economic Value Gained by Uninsured Individuals If Insured, Annualized

|

|

Billions $, estimated for 2001 |

|

Current cost of care for full- and part-year uninsured |

98.9 |

|

Amount paid out of pocket by full- and part-year uninsured |

26.4 |

|

Insurance payments (for part-year uninsured only) and workers’ compensation |

|

|

Private |

24.2 |

|

Public |

13.8 |

|

Uncompensated care |

34.5 |

|

Projected annual costs of additional utilization with coverage |

34–69 |

|

Benefits of insuring the uninsured |

|

|

Aggregate value of health capital forgone by the uninsured, annualized |

65–130 |

|

Aggregate annual value of risk borne by uninsured |

1.6–3.2 |

|

SOURCES: Hadley and Holahan, 2003a,b; Vigdor, 2003. |

|

projected cost of the additional health care that the presently uninsured population would receive if insured, and the aggregate, annualized economic value of lost health and financial security that those who lack coverage forgo, despite the substantial health care expenditures made on their behalf.

The next step in the Committee’s analysis is to consider the potential benefits of providing the uninsured with coverage in conjunction with the new economic costs of the additional health services that would improve their health. In order to do this, both the average per capita gain in health due to an additional year of health insurance for the uninsured population and the average per capita annual cost of the additional health services that the uninsured population would use if they had coverage must be made comparable. Because the estimate of the value of health gained with an additional year of coverage is calculated as a discounted present value of the gain for a cohort of uninsured people over the course of their lives (with a range of $1,645 to $3,280 as presented earlier), the estimate of the annual cost of the additional health care that the uninsured would use if insured also must be calculated as the present value for an uninsured cohort over the course of their lives.

Using the projected annual cost of the additional utilization by those without coverage from Hadley and Holahan (2003b), the Committee estimated that the discounted present value of the cost of an additional year of health insurance ranges from $1,004 to $1,866, depending on whether the incremental service costs

are based on the cost of public or private health insurance. The range of estimated benefits from the incremental coverage ($1,645 to $3,280) is higher than the range of estimated incremental service costs ($1,004 to $1,866) and, for most values within each range, results in a benefit-cost ratio of at least one.

REALIZING SOCIAL VALUES AND IDEALS

Finally, the Committee reflected on several other benefits that our national community and local communities within the United States might gain if health insurance coverage were extended throughout the population. Economic goods that can be valued in monetary terms are not the only kinds of goods that we value having. Providing certain important goods like health care to all members of society has its own value (Walzer, 1983; Coate, 1995). In addressing normative questions, the Committee has attempted to start from values that are widely endorsed throughout American society, such as equality of opportunity, and then to make judgments about whether public policy and economic practices in health care accord with a reasonable characterization of those values. The Committee does not attempt to make a freestanding argument about objective morality but rather claims that collective actions can express or achieve existing social norms and ideals.

Because health care relieves pain and suffering and enhances our ability to function and achieve over the course of a lifetime, making sure that everyone in society has adequate access to this good is a matter of fairness and social decency (Daniels, 1985; Sen, 1993). A commitment to equal opportunity obligates us as a society to ensure that all Americans have sufficient access to health care such that they are not disadvantaged in pursuing the career and other opportunities offered by American society.

Health insurance contributes essentially to obtaining the kind and quality of health care that can express the equality and dignity of every person. Despite the absence of an explicit Constitutional or statutory right to health care (beyond access to emergency care in hospitals, required by the Emergency Medical Treatment and Labor Act), disparities in access to and the quality of health care of the kind that prevail between insured and uninsured Americans contravene widely accepted, democratic cultural and political norms of equal consideration and equal opportunity. The increasing effectiveness of medical interventions in improving health and survival (Cutler and Richardson, 1997; Murphy and Topel, 1999; Heidenreich and McClellan, 2003) make considerations of equity in access to effective care through health insurance more urgent.

Uninsurance in America not only has hidden costs, it represents lost opportunities to more fully realize important social and political ideals that account for our nation’s political stability and vitality (Dionne, 1998; NASI, 1999). Extending the social benefit of health insurance would help us make our implicit and explicit democratic political commitments of equal opportunity and mutual concern and respect more meaningful and concrete.