3

Spending on Health Care for Uninsured Americans: How Much, and Who Pays?

This chapter considers estimates of expenditures for health care services used by uninsured Americans, both the out-of-pocket spending of those without insurance and the value of the health care services they use that are uncompensated or donated. Persons without health insurance, on average, spend less for health care out of pocket than do those with health insurance because they use fewer and less costly services. Uninsured families pay for a higher proportion of their total health care costs out of pocket than do insured families, however, and are more likely to have high medical expenses relative to income (IOM, 2002b).1

The health care services received by uninsured individuals that they do not pay for themselves are picked up or “absorbed” by a number of parties, including:

-

practitioners and institutions, both public and private, that serve the uninsured at no charge or reduced charges;

-

the federal government, localities, and states that support the operation of hospitals and clinics, both through direct appropriations and implicit subsidies like the Medicare and Medicaid disproportionate share hospital payments; and

-

philanthropic donations.

The claim is often made that hospitals and physicians shift the costs of uncompen-

|

1 |

The differences in service utilization costs between uninsured and insured individuals reported in this chapter have not been adjusted for differences between the two groups in age composition and family income, which also affect health services use and spending. In contrast, the projections reviewed in Chapter 5 of service use and expenditures for those without insurance if their utilization was the same as for those with coverage do adjust for demographic and socioeconomic factors. |

sated care onto the bills of insured patients, and the Committee also considers the evidence for such cost shifting.

The chapter is organized as follows. The first section briefly compares the average overall health expenditures for uninsured and privately insured populations. The following section examines the out-of-pocket spending by the uninsured and the distribution of their out-of-pocket expenses by service. The third section presents estimates developed by Jack Hadley and John Holahan of the Urban Institute of the amount of uncompensated health care services used by people uninsured for part or all of a year. The fourth and last section examines the incidence of the burden of uncompensated care costs across public and private payers, and more specifically how it is shared among the federal, state, and local governments.

UNINSURED PEOPLE USE LESS MEDICAL CARE THAN DO THOSE WITH COVERAGE

Finding: Uninsured children and adults are less likely to incur any health care expenses in a year than their counterparts who have coverage. On average, those without any form of coverage over the course of a year incur health care costs less than half of per capita health care spending for those under age 65 who have coverage.2

Uninsured people are both less likely than those with coverage to use any health services in a given year and have lower expenditures for services on average (Taylor et al., 2001). As earlier Committee reports demonstrated, this lower level of utilization is the source of one hidden cost of uninsurance—higher morbidity and mortality as a result of using fewer and less appropriate health care services. The Committee does not mean to imply by this comparison, however, that all of the additional use of services by those with coverage is effective and appropriate, but simply that the greater amounts of services used by insured populations are associated with and contribute to their better health outcomes, relative to those of uninsured populations.

Table 3.1 presents data from the 1996 Medical Expenditure Panel Survey (MEPS), comparing the experience of full-year uninsured and full-year privately insured individuals under age 65 who used any health services of a particular kind in that year.3 Sixty-two percent of full-year uninsured persons incurred any health care expenses, compared with 89 percent of those with private insurance for the

|

2 |

This reflects the statistics reported in Table 3.2 that are not adjusted for differences in the age and sex composition of insured and uninsured populations. It is also consistent with analyses that are adjusted for demographic differences, as illustrated by the statistics in Table 5.3 in Chapter 5. |

|

3 |

The 1996 MEPS is a two-year panel of about 22,000 respondents that is nationally representative of the U.S. noninstitutionalized population. |

TABLE 3.1 Use of Services by Full-Year Uninsured and Full-Year Privately Insured Individuals Under Age 65, 1996 (percentage with use)

|

Service |

Uninsured |

Privately Insured |

|

Any service |

62.0 |

89.0 |

|

Inpatient hospital |

2.9 |

4.6 |

|

Outpatient hospital |

6.2 |

13.4 |

|

Emergency room |

11.5 |

11.0 |

|

Office-based physician |

41.3 |

71.3 |

|

Office-based nonphysician |

13.6 |

25.8 |

|

Prescription medications |

40.6 |

66.1 |

|

Dental |

20.4 |

53.1 |

|

SOURCE: Taylor et al., 2001. MEPS 1996. |

||

full year (Taylor et al., 2001). Except for emergency room services, which are used comparably by about 11 percent of privately insured and uninsured persons, the proportion of the uninsured population using any other kind of health service is one-half to two-thirds of the proportion of the privately insured population using each type of service.

Persons uninsured for the full year incur total average annual expenses for health care services that are less than two-fifths of those of someone with either full-year private or full-year public coverage. Box 3.1 reviews the Committee’s findings from Health Insurance Is a Family Matter about the dependence of children’s receipt of care on their parents’ health insurance status. Efforts to ensure that children have coverage and receive appropriate health care should take into account these interactions within families.

Table 3.2 presents estimated expenditures for fulland part-year uninsured individuals and compares them with those for persons covered the entire year. For 2001, estimated per capita spending for the population under age 65 overall was $2,163.4 For the full-year uninsured, per capita spending was $923, 43 percent of the overall average and just 37–38 percent of the average for those with any kind of coverage for the entire year. Those with private health insurance for the full year and those with public coverage (Medicaid) for the full year had roughly comparable estimated spending of $2,484 and $2,435, respectively. Those uninsured for part of the year and with either private or public coverage part of the year had estimated per capita expenditures that ranged from $1,331 for those with private coverage for 5 or fewer months to $2,511 for those with public coverage for between 6 and 11 months.

|

BOXs 3.1 Health Insurance and Use of Services Within Families Health insurance status affects families’ relationships with health care providers and the delivery system. One way families with uninsured members manage health care expenses is by not using services. The data comparing use of services and spending on health care for insured and uninsured individuals and families demonstrates this vividly. This discussion illustrates the mechanisms by which children with uninsured parents are harmed by the lack of coverage within the family. Among adults under age 65, 59 percent who were uninsured throughout 1996 did not have a physician office visit that year, twice the 29 percent of those who had private insurance (Taylor et al., 2001). Among children under age 18 who were uninsured throughout 1996, 49 percent did not have a physician office visit, twice the 24 percent of children with private insurance. Among children who had visits, the average number of visits among those who were uninsured was 2.7. Among children with private coverage, the average was 4.2 visits, half again as many as among uninsured children (McCormick et al., 2001). Children without health insurance are less likely to have a usual source of care than children with health insurance. The parent of a child without health insurance is less likely to have an answer to the question, “Where do I go if my child becomes sick?” An evaluation of a Pennsylvania program to expand health insurance for children found the share of children with a regular source of care increased from 89 percent at baseline to 99 percent at 12 months, and the share with a regular dentist increased from 60 percent to 85 percent (Lave et al., 1998). Children benefit from the greater access to health care services that health insurance brings only when their parents or guardians act. They acquire health insurance when adults enroll them and receive health care when parents bring them to a provider. The Committee concluded in Health Insurance Is a Family Matter that a child whose parent has health insurance is more likely to receive care. Children whose parents do not have health insurance are less likely to use health services, even if the child has health insurance (Newacheck and Halfon, 1986; Hanson, 1998; Minkovitz et al., 2002). In one comparison, having an uninsured parent decreased the probability that a child had any visit with a medical provider by 6.5 percent and a well-child visit by 6.7 percent, compared to children whose parent had health insurance (Davidoff et al., 2002). If all parents had health insurance, a larger share of children could be expected to receive the regular medical attention that is of proven value for children’s health and development. |

When people who lack insurance do obtain care, it is paid for by a number of parties, including the uninsured themselves. The remainder of this chapter examines who provides and also pays for this care, and the economic implications of uncompensated care burdens on health care providers, payers, governments, and taxpayers.

TABLE 3.2 Total and Per Capitaa Medical Care Spending, by Insurance Status, 2001 (estimated)

|

Insurance Status |

Total Spending ($ billions) |

Per Capitaa Spending ($) |

|

Private Insurance, Full Year |

375.1 |

2,484 |

|

Public Insurance, Full Year |

42.5 |

2,435 |

|

Uninsured, Part Year |

|

|

|

Private insurance for 1–5 months |

10.4 |

1,331 |

|

Private insurance for 6–11 months |

25.9 |

1,796 |

|

Public insurance for 1–5 months |

5.0 |

1,729 |

|

Public insurance for 6–11 months |

12.0 |

2,511 |

|

Uninsured, Full Year |

30.0 |

923 |

|

Total Uninsured (full and part year) |

83.1b |

1,335b |

|

500.9 |

2,163 |

|

|

aCivilian, noninstitutionalized population under age 65, excluding people with any Medicare coverage, nursing home, and long-term hospital care. bNo adjustment for MEPS undercount of uncompensated care. cEntries do not sum to total because of rounding. SOURCE: Hadley and Holahan, 2003a. Pooled data from the 1996, 1997, and 1998 MEPS, projected to 2001 levels. |

||

OUT-OF-POCKET COSTS FOR UNINSURED INDIVIDUALS AND FAMILIES

Finding: People who lack health insurance for an entire year have out-of-pocket expenditures comparable to those of people with private coverage, but they also have much lower family incomes. Out-of-pocket spending for health care by the uninsured is more likely to consume a substantial portion of family income than out-of-pocket spending by those with any kind of insurance coverage.

Families with members who do not have health insurance face substantial financial risks. The nature and consequences of those risks were addressed in the committee’s third report, Health Insurance Is a Family Matter. While the mean out-of-pocket expenses for someone uninsured for the full year is only slightly higher than for someone privately insured for the full year ($426, compared with $402 in 1996), the average family income of someone without health insurance is substantially lower than that for the privately insured.5 In 2001, the median annual family

income of uninsured persons was between $20,000 and $29,000 and that for those with private coverage was over $50,000 (Fronstin, 2002). In addition, the average for those without insurance includes a higher proportion of families that have not incurred any costs than does the average for those with health insurance, so the expense is spread less evenly across the population. Fifteen percent of families in which all members were without health insurance for all of 1996 had health costs that exceeded 5 percent of their income and 4 percent of uninsured families had expenses that exceeded 20 percent of their annual income (compared with 1 percent of privately insured families). Among uninsured families with incomes of less than 125 percent of the federal poverty line, however, between 8 and 9 percent had health care expenses greater than 20 percent of income (Taylor et al., 2001).

Families with some or all members uninsured for longer than a year are more likely to experience a period in which their medical expenses are substantial. Assuming for simplicity that years in which medical expenses are high are statistically independent (not likely to be true because these expenses are correlated across time), a family with no members insured for 5 years would be slightly more likely than not to have at least one year with health care costs that exceeded 5 percent of its income (Merlis, 2001).

Food, shelter, transportation, and clothing account for 85 percent on average of the expenditures of families without health insurance. With few assets to use up, medical expenses lead to a lower standard of living. For some families, medical costs may mean bankruptcy (IOM, 2002b.) Hospital stays are the most expensive kind of health care service. Because hospitals frequently reduce, or write off as bad debt, charges to uninsured patients, families are spared some of the financial adjustments that would be required to meet the full cost of treatment. Accepting charity care or incurring bad debt exposes families to other kinds of costs. Box 3.2 reviews some of the implications for individuals and families of receiving care for which they cannot pay.

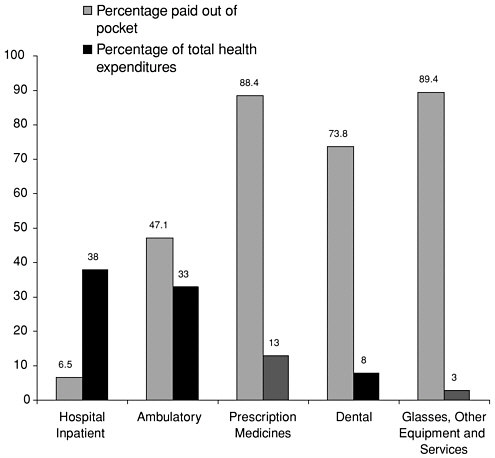

Uninsured individuals pay for a larger share of services received on an ambulatory basis than they do for inpatient care. Figure 3.1 displays the proportion of costs that uninsured individuals pay out of pocket for various kinds of services and the share of total health expenditures represented by each kind of service.

Both the chances of substantial illness and asset levels tend to increase with age. Older persons without health insurance are both more likely to experience illness and have fewer years until retirement to replace assets depleted by the costs of illness. One in every six people ages 51 to 61 participating in the Health and Retirement Survey who were initially uninsured experienced a new diagnosis of cancer, heart disease, or stroke within the next 6 years (Levy, 2002). Those who did not have health insurance had substantially lower levels of wealth than those who did at the start of the study. Median nonhousing wealth totaled $61,000 for those with health insurance and $19,000 for those without health insurance. Liquid assets, such as amounts in checking, savings, or money market accounts, amounted to $7,000 for the median insured person who went on to experience a

|

BOX 3.2 Charity Care and Bad Debts A person or family that seeks charity care must submit to probing questions about their financial means, and may feel stigmatized or shamed by having to accept charity. Stigma is one reason those who are eligible for assistance often do not apply (Moffitt, 1983). If an individual or family does not apply for charity care when the patient obtains hospital services, they receive a bill that asks for payment of the hospital’s charges. The amount billed to patients without insurance coverage is not reduced by any “contractual allowances,” reductions from the hospital’s charges that payers negotiate (or in the case of public payers like Medicaid or Medicare, set unilaterally) (Wielawski, 2000; Lagnado, 2003a,b). In time, a hospital may write off as bad debt the amount that an uninsured patient does not pay. But between initial receipt of a bill and a bad debt writeoff, the patient and family receive monthly billings that may exceed the family’s income. Even if the collection process ends with a hospital or collection agency writing off the unpaid amount, a family faces ongoing consequences. A report by a hospital or other health care provider that a family did not pay for its health care remains part of the family’s credit report for up to 7 years (Federal Trade Commission, 1999). A person who while uninsured experienced a costly episode of health care can find that years later his or her or another family member’s health care shapes whether he or she obtains credit to buy a house or lease a car or rent an apartment. If a family has a home, it may find that a health care provider has placed a lien on the home to satisfy an unpaid health care bill (Lagnado, 2003a; Schneider, 2003). A lien must be satisfied at the time the property is sold, potentially separating the time a family incurred an expense and its payment by 20 or more years. These repeat billings and collection efforts on the part of the hospital are dictated by standard hospital accounting and audit practices, which require hospitals to demonstrate efforts to collect before writing off an outstanding account balance as bad debt (Herkimer, 1993; Lagnado, 2003a,b). These repeat billings also add to hospitals’ administrative costs. |

new diagnosis and just $900 for the median uninsured person who similarly had a new diagnosis (Levy, 2002.)

Public subsidies for coverage make health insurance financially more feasible for lower-income persons and families, yet many who are eligible are not enrolled in public programs or cannot afford to take up workplace offers. Public coverage through Medicaid offers health insurance without paying a premium for those with very low income.6 State Children’s Health Insurance Programs (SCHIPs) and state-only insurance programs may require income-related premiums for families with incomes above the Medicaid or SCHIP full-subsidy level (SCHIP limits

FIGURE 3.1 Share paid out of pocket by uninsured persons under age 65, within each type of service and share of total health expenditures that each type of service represents, 1997.

SOURCE: Agency for Healthcare Research and Quality, 2001. Data from 1997 Medical Expenditure Panel Survey.

cost sharing to less than 5 percent of income). The tax treatment of health insurance allows workers to obtain health insurance without paying income or payroll tax on the premium paid by the employer. Despite Medicaid requiring no premiums and SCHIP relatively modest ones, if any, many who are eligible for these programs are not enrolled. Based on eligibility simulations by the Urban Institute, in 2001 an estimated 5.26 million children were eligible for either SCHIP or Medicaid but not enrolled, and an estimated 3 million lower-income (family income less than 200 percent of the federal poverty level) adults under age 65, both parents and those without children, were eligible for but not enrolled in Medicaid (Schneider, 2002). Among children who are eligible for Medicaid but

not enrolled, nearly 85 percent live in families that had some health costs over a one-year period, and 29 percent had out-of-pocket costs that were greater than $500 (Davidoff et al., 2000). Although the reasons why so many children are eligible but not enrolled vary, their lack of coverage entails both health and financial losses within the family (IOM, 2002b).

If people without health insurance were to gain coverage, the change in their out-of-pocket costs for health care would depend both on the scope of benefits of and the cost sharing required by the policy or program they enrolled in, and on any increase in the amount or cost of care they received as a result of being insured. The change in the financial circumstances of persons without health insurance who gained health insurance would also depend on how their care-seeking behavior changed. The Committee’s second report, Care Without Coverage, addressed the adverse health consequences for persons who do not have health insurance from not obtaining preventive and regular chronic disease care. If the previously uninsured were to use services more frequently, approximating the use patterns of those with coverage, their out-of-pocket costs could increase, depending on the nature of their plan’s coverage and cost-sharing requirements because of the increase in their average spending on health care, including insurance premiums. (See Chapter 5 for benchmark estimates of the expected increase in health services costs if those without insurance gained coverage similar to that of the currently insured population.) Whether or not enrollees’ out-of-pocket costs for health care, including insurance premium payments, are higher or lower than they would be without insurance depends on the time period considered, their health status, and the extent of any premium subsidy.

UNCOMPENSATED CARE TO UNINSURED PERSONS

Finding: The best available estimate of the value of uncompensated health care services provided to persons who lack health insurance for some or all of a year is roughly $35 billion annually, about 2.8 percent of total national spending for personal health care services.

The Committee’s fourth report, A Shared Destiny, provided an overview of the level and sources of uncompensated health care in the United States in order to elucidate the mechanism by which uninsurance affected communities, their health care agencies and institutions, and economic resources. This information is also a central component of this report because it bears on how the costs of care received by those without coverage are distributed. Most of the costs of uncompensated care provided to those without coverage do not represent new economic costs attributable to uninsurance per se, but are instead transfers of resources from public and private sources to those receiving health care.

To the extent that individuals who lack coverage receive less effective or more costly health care than do those with coverage, the overall costs of their care

will include some amount of true economic costs attributable to the condition of lacking coverage. These economic costs are borne by taxpayers and others that support the provision of uncompensated services, as well as by the out-of-pocket payments of uninsured individuals. Box 3.3 presents studies that have documented and attempted to estimate the relative magnitude of one aspect of inefficient and costly care among uninsured populations—potentially avoidable hospitalizations.

A recent analysis and comprehensive set of estimates of the value of health care services provided to Americans without health insurance were prepared by economists Jack Hadley and John Holahan of the Urban Institute (2003a). They used two independent approaches and sources of data for their estimates of the value of free hospital, physician, and clinic services the uninsured use annually, adjusted to reflect estimated spending in 2001.

The first estimate used pooled data from the 1996, 1997, and 1998 Medical Expenditure Panel Survey (MEPS) of the civilian, noninstitutionalized population to calculate the volume of services provided to individuals who were uninsured for part or all of the year.7 From this source the authors were able to distinguish between the expenditures on behalf of full- and part-year uninsured. Combining periods without coverage for those uninsured for only part of the year to calculate full-year-equivalent periods of uninsurance and adding these uninsured years to those of individuals uninsured for the full year resulted in an overall average of 45 million person-years of uninsurance for each year, 1996–1998. To offset MEPS’ systematic undercounting of uncompensated services by private hospitals and other private facilities and of general government appropriations and payments to hospitals, the authors increased the MEPS-based estimates of care received by the uninsured by 25 percent. This reflects a reconciliation of MEPS-reported health expenditures with the more comprehensive National Health Accounts estimates of the Centers for Medicare and Medicaid Services (Selden et al., 2001).

The authors’ estimate for 2001 of the value of uncompensated health care services received by people uninsured for either part or all of a year was $34.5 billion, $24.6 billion of which was for those uninsured for the entire year and $9.9 billion for those uninsured part of the year (see Table 3.3). Free or uncompensated care accounted for 61 percent of the value of services used by those uninsured for the full year and 17 percent of the value of services provided to those uninsured for part of the year.8 This amount represents 2.8 percent of the projected total personal health care expenditures nationally for 2001 (Hadley and Holahan, 2003a).

|

BOX 3.3 Potentially Avoidable Hospitalizations:Costs of Inefficient Utilization While uninsured individuals bear the direct costs to health of inappropriate (in-cluding inadequate) use of health care services, when care is received too late or in settings such as hospital emergency departments, additional economic costs are created. These economic losses are subsumed in the estimates of both out-of-pocket spending and uncompensated care expenditures for the uninsured. One avenue by which these costs are introduced is potentially avoidable hospitalization for conditions that, if medical attention is prompt and appropriate, can often be effectively managed on an outpatient basis. Measured across areas or population groups, rates of potentially avoidable hospitalizations not only serve as an indicator of the acuity of illness experienced within a population, these rates also reflect the efficiency with which health care is provided. If some hospitalizations could be avoided with earlier, more appropriate, and less costly care, then some portion of uncompensated care costs could be eliminated. Because uninsured persons themselves pay less than 7 percent of the expenditures for hospital care that they incur, public programs and other sources of support pay the rest (AHRQ, 2001). Uninsured patients are more likely to experience avoidable hospitalizations than are privately insured patients when measured as the proportion of all hospitalizations (Pappas et al., 1997). Nationally, the proportion of hospitalizations that were potentially avoidable for persons younger than 65 have grown more substantially over the past two decades for uninsured persons than for those with Medicaid or private insurance: from 5.1 to 11.6 percent between 1980 and 1998 for the uninsured, compared with increases for Medicaid enrollees from 7 to 9.8 percent and for those with private insurance from 4.1 to 7.5 percent (Kozak et al., 2001). Pappas and colleagues (1997) examined rates of hospitalization for diagnoses1 that they identified as potentially treatable on an outpatient basis (adjusted for age and sex) in relation to median income within ZIP-code areas. They estimated that these conditions accounted for between 3 million and 5 million hospitalizations in 1990 (12 to 19 percent of all hospitalizations in that year, excluding those related to childbirth and for psychiatric conditions). They used the rates of hospitalization for these designated conditions that residents in areas with the highest median household incomes ($40,000 or more) experienced as the baseline rates below which such hospitalizations presumably could not be reduced. The authors then calculated that nearly 30 percent of such hospitalizations (between 844,000 and 1.4 million nationally) could represent excessive prevalence and severity of illness, and poorer access to ambulatory care, within lower-income neighborhoods. Age-adjusted rates of potentially avoidable hospitalizations per 1,000 population were higher for uninsured compared with privately insured groups (4 per 1,000 for the uninsured group and 3 per 1,000 for the privately insured population). Less than 6 percent of the uninsured had household incomes of $40,000 or more, so their experience is reflected almost entirely in the differentially high rates of avoidable hospitalizations. Notably, the differences in rates of hospitalization by income class diminished substantially after age 65, when everyone gained Medicare coverage (Pappas et al., 1997). |

TABLE 3.3 Medical Care Expendituresa and Sources of Payment for People Under Age 65 Uninsured for at least Part of the Year, 2001 ($ billions, estimated)

|

Source of Payment |

Uninsured Full Yearb |

Uninsured Part Yearc |

All Uninsured |

|

Free Carea |

24.6 |

9.9 |

34.5 |

|

Other public sources |

5.0 |

1.5 |

6.5 |

|

Other private and unknown sources |

8.9 |

3.4 |

12.3 |

|

In-kindd |

10.8 |

5.0 |

15.8 |

|

Out of Pocket |

14.1 |

12.3 |

26.4 |

|

Private Insurance |

1.9e |

22.3 |

24.2 |

|

Public Insurance |

0.0 |

13.8 |

13.8 |

|

All Sources |

40.6 |

58.3 |

98.9a |

|

aAdjusted for MEPS undercount of uncompensated care relative to National Health Accounts. bAverage of 32.4 million people per year from 1996–1998 MEPS. cAverage of 29.9 million people per year from 1996–1998 MEPS. dEstimated from the difference between payments and charges. ePayments by workers’ compensation. SOURCE: Hadley and Holahan, 2003a. Derived from pooled data from the 1996, 1997, and 1998 MEPS projected to 2001 levels. |

|||

In their second set of estimates, Hadley and Holahan calculated the value of uncompensated care to the uninsured from private provider surveys (e.g., by the American Hospital Association and the American Medical Association) and public provider budgets and appropriations (for clinics and other government direct care programs, such as Department of Veterans Affairs services). In this calculation, the authors also estimated the proportion of uncompensated or charity care that was provided to uninsured patients by each provider type (e.g., hospitals, clinics, physicians in private practice).

Uncompensated Hospital Care

In 1999, hospitals reported $20.8 billion in expenses for all services to all patients who did not pay their bills in full, an amount representing 6.2 percent of total hospital expenses in that years (MedPAC, 2001).9 Because hospitals apply

different billing policies for patients in similar circumstances, this amount represents both charity care and bad debt reported by the hospitals in the annual American Hospital Association (AHA) survey. This amount is certainly an overestimate of the uncompensated care costs of the uninsured because some proportion of bad debt is attributable to insured patients who do not pay some part of the hospital bill for which they are responsible—the deductible, coinsurance, or noncovered services. Increasing this 1999 estimate to projected Medicare payment increases by 2001 yields an estimate of $23.6 billion in uncompensated care in the latter year.

Clinics and Direct Care Programs

The Committee’s previous report, A Shared Destiny, provided an overview of the federal, state, and local governmental programs involved in the direct provision of personal health care services to underserved and vulnerable populations, including those Americans who lack health insurance. Hadley and Holahan (2003a) estimate the value of health care services that the various governmental grant and direct care programs provide to those without health insurance, including

-

the community health center and other programs of the federal Bureau of Primary Health Care,

-

Maternal and Child Health clinics and services,

-

National Health Service Corps,

-

HIV/AIDS care,

-

Indian Health Service,

-

Department of Veterans Affairs (VA), and

-

local health departments.

Table 3.4 presents the budgets or expenditures for each of these service categories or providers, an estimate of the proportion of total program clients or expenditures that the uninsured represent, and the authors’ resulting estimate of total expenditures on care to the uninsured. The authors note that these separate program appropriation and expenditure figures may double count some expenditures for the uninsured because many clinics and health centers are grantees of multiple federal and state programs. For local health departments, for which client health insurance status is not available, the authors assumed that the same proportion of local public health clinic expenditures were attributable to uninsured users as for Bureau of Primary Health Care programs, 32 percent. As shown in Table 3.4, the estimate of expenditures for care to the uninsured from community health and other providers of direct care is $7.11 billion, of which the VA accounts for more than half of the total.

TABLE 3.4 Estimated Expenditures for Care for the Uninsured, Community Health Care Providers and Government Direct Care Programs, FY2001

|

Source |

Total Expenditures ($ billions) |

Uninsured (%) |

Total Expenditures on Care to Uninsured ($ billions) |

|

Bureau of Primary Health Care |

3.46a |

31.8b |

0.84c |

|

Maternal and Child Health Bureau |

2.45d |

12.7e |

0.31 |

|

National Health Service Corps |

0.65f |

18.3b |

0.12c |

|

HIV/AIDS Bureau |

1.75g |

39.0e |

0.68 |

|

Indian Health Service |

1.86h |

37.0i |

0.69 |

|

Veterans Affairs |

18.5j |

21.0 |

3.89 |

|

Local Health Departments |

1.81k |

32.0 |

0.58 |

|

Total |

30.48 |

|

7.11 |

|

aCY2001 data on medical and other professional health services (excluding dental), “Uniform Data System (UDS) Rollup Report,” ftp.hrsa.gov/bphc/pdf/uds. bSelf-pay patients’ share of total charges. cNet of payments collected from self-pay patients. dFY2000 data on direct medical services, trended forward, “Federal-State Title V Block Grant Partnership Budget,” http://www.mchdata.net/reports. eShare of users who were uninsured. fCY2000 data trended forward, “NHSC UDS National Rollup Report.” gFY2001 appropriation for Emergency Relief-Part A and Comprehensive Care-Part B, “HRSA FY 2002 Budget,” http://newsroom.hrsa.gov/NewsBriefs. Includes $0.24 billion in state spending reported by National Association of State Budget Officers (NASBO), 2001. hFY2001 appropriation for clinical services, http://www.ihs.gov/adminmngrresources/budget. Includes $0.06 billion in state spending from NASBO (2001). iPercent of Native Americans reporting only Indian Health Service or no insurance coverage, calculated from the 1997–1999 Current Population Surveys. jFY2001 appropriation for medical care, excluding nursing home, subacute, and residential care. kNASBO, 2001. SOURCE: Hadley and Holahan, 2003a. |

|||

Physicians

By waiving or reducing their fees to uninsured patients and volunteering their time in free clinics and similar settings, physicians provide a significant amount of charity care. One American Medical Association (AMA) survey reports that physicians provided about equal amounts of reduced-price and free care (Emmons, 1995). Unlike the case with hospitals and publicly supported clinics, physicians and others in individual and small-group practices usually do not receive explicit subsidies for uncompensated care nor do they have the organizational superstructure and capacity of larger providers to absorb and balance the financial burdens of uncompensated care.

The Committee’s previous report, A Shared Destiny, reviews the several sources of information about physicians’ provision of charity care, primarily the American Medical Association’s periodic surveys of practicing physicians (Emmons, 1995; Kane, 2002) and the Center for Studying Health System Change’s Community Tracking Study (CTS) (Cunningham et al., 1999; Reed et al., 2001; Cunningham, 2002). These two sources provide similar estimates of the proportion of practicing physicians who provide any charity care and quite different estimates of the average amount of charity care provided by those physicians who provide any.10 One factor that may contribute to the high estimate from the AMA surveys is that salaried physicians who provide uncompensated care within an institutional setting report it as charity care.

Hadley and Holahan based their estimate of the value of uncompensated care physicians provide to uninsured persons on the midpoint of the range of average weekly hours of charity care reported for the 1994 AMA survey (7.2 hours, Emmons, 1995) and the 1999 CTS estimate. The authors used the earlier AMA survey because it included estimates of physicians’ average gross earnings per hour for that year ($105) and a breakdown of charity care into that which was entirely free and that for which physicians reduced their prices. They assumed that all of the free care and one-third of the reduced-price care were provided to uninsured patients. Applying the same estimate of gross hourly earnings (updated to 2001 by the medical care consumer price index) to the hours per week of charity care reported by the AMA and CTS surveys, Hadley and Holahan estimated a range of values from $4.5 to $9.1 billion in physician-provided charity care in 2001. The midpoint of the range is $6.8 billion. As a final adjustment to eliminate the double counting of charity care provided by salaried physicians practicing in teaching hospitals, public clinics and hospitals, and community health centers, the authors used the CTS survey estimate that 25 percent of the time physicians reported as spent providing charity care was as salaried employees to reduce the $6.8 billion to $5.1 billion.

Sum of Provider Budget Estimates of Uncompensated Care

Combining the estimates of uncompensated care reported by hospitals through the AHA survey ($23.6 billion), services to uninsured clients by clinics and community health care providers ($7.1 billion), and charity care by physicians in private practice and as volunteers ($5.1 billion), the overall estimate of uncompensated care provided to uninsured Americans based on providers’ financial and

practice information is $35.8 billion for 2001, $1.3 billion more than the estimate based on the MEPS (Hadley and Holahan, 2003a).

The Committee concludes that $35 billion is a reasonable, “ballpark” estimate of the monetary value of the uncompensated care that uninsured individuals used in 2001. The study’s authors derived their estimates from two sets of data sources independently and thoroughly documented and justified the assumptions they made in developing the estimates. Nonetheless, the point estimate of $35 billion is simply the approximate midpoint of a range of values that could be used with equal confidence.

WHO BEARS THE COSTS OF UNCOMPENSATED CARE FOR THOSE WHO LACK COVERAGE?

Finding: Public subsidies to hospitals amounted to an estimated $23.6 billion in 2001, closely matching the cost of uncompensated services that hospitals reported providing. Overall, public support from the federal, state, and local governments accounts for between 75 and 85 percent of the total value of uncompensated care estimated to be provided to uninsured people each year.

Spending for personal health care services and supplies amounted to $1.236 trillion nationally in 2001 (Levit et al., 2003). An estimated $99 billion (8 percent of all personal health care spending) was for the 62 million people estimated to be uninsured for all or part of the year (Hadley and Holahan, 2003a). Of this total, private health insurance paid for an estimated $22.3 billion of the care received by those with some period of uninsurance within the year and public coverage (primarily Medicaid) paid $13.8 billion for services used by the part-year uninsured (Table 3.3). The estimated $35 billion burden of uncompensated care is shared among governments and private sponsors, although ultimately individuals bear the costs of these uncompensated services as taxpayers, providers, employees, and health care consumers.

Table 3.5 summarizes the distribution of funding that Hadley and Holahan estimate is available from public and private sources. The amounts available from these sources for uncompensated care exceed the authors’ point estimate of $34.5 billion derived from MEPS by $3 to $6 billion annually, as shown in the table.

Federal, state, and local governments support uncompensated care to uninsured Americans and others who cannot pay for the costs of their care, primarily as hospital ($23.6 billion) and clinic services ($7 billion). Sixty percent of governmental support for uncompensated care in hospitals is federal, through Medicare and Medicaid disproportionate share hospital (DSH) payments to general hospitals, a portion of Medicare payments for indirect medical education that supports services to medically indigent patients, and other supplemental Medicaid financing

TABLE 3.5 Sources of Funding Available for Free Care to the Uninsured, 2001 ($ billions)

such as upper-payment limit (UPL) mechanisms. State and local governmental support for uncompensated hospital care is estimated at $9.4 billion, through a combination of $3.1 billion in tax appropriations for general hospital support (which the Medicare Payment Advisory Committee [MedPAC] treats as funds available for the support of uninsured patients), $4.3 billion in support for indigent care programs, and $2.0 billion in Medicaid DSH and UPL payments (Hadley and Holahan, 2003a).11

Although hospitals reported uncompensated care costs in 1999 of $20.8 billion (projected to increase to $23.6 billion in 2001), it is difficult to determine how much of this cost ultimately resides with the hospitals (MedPAC, 2001; Hadley and Hollahan, 2003a). As just discussed, federal, state, and local subsidies of various kinds appear to equal the estimate of hospital uncompensated care costs. Philanthropic support for hospitals in general accounts for between 1 and 3 percent of hospital revenues (Davison, 2001) and, because much of this support is dedicated to other purposes (e.g., capital improvements), only a fraction is available for uncompensated care, estimated to fall in the range of $0.8 to $1.6 billion

for 2001. Another $1.5 to $3 billion in hospitals’ own-source funds (from payments from private payers in excess of hospital costs) may be available to support uncompensated services, according to Hadley and Holahan.

Hospitals had a private payer surplus of $17.4 billion in 1999 (based on AHA and MedPAC reporting). These surplus payments, however, tend to be inversely related to the amount of free care that hospitals provide. A study of urban safety-net hospitals in the mid-1990s found that safety-net hospitals’ case loads on average included 10 percent self-pay or charity cases and 20 percent privately insured, whereas among nonsafety-net hospitals, just 4 percent were self-pay or charity cases and 39 percent were privately insured (Gaskin and Hadley, 1999a,b). Thus, those hospitals with private payer surplus revenues (and revenues from sources other than patient care, such as parking fees) are not the hospitals that bear most of the load of uncompensated care. Based on this reasoning, Hadley and Holahan assume that between 10 and 20 percent of these surplus revenues subsidize care to the uninsured. The issue of cross-subsidies of uncompensated care from private payers and the impact of uninsurance on the prices of health care services and insurance are discussed in the following section.

Physicians in private capacities, within their own practices and as volunteers in clinics, are the predominant source of private contributions to uncompensated care for the uninsured, with an estimated $5.1 billion in donated services accounting for 15 percent of the $35 billion total.

Increases in Prices of Health Care Services and Insurance Premiums12

Finding: There is mixed evidence that uncompensated care is subsidized by private payers. The impact of any such shifting of costs to privately insured patients and insurers is unlikely to be so large as to affect the prices of health care services and insurance premiums.

Have the 41 million uninsured Americans contributed materially to the rate of increase in medical care prices and insurance premiums through cost shifting? Health care prices and health insurance premiums have increased more rapidly than other prices in the economy for many years. In 2002, medical care prices rose by 4.7 percent, while all prices rose by only 1.6 percent. Since the last benchmarking of the series between 1982 and 1984, overall prices have risen by about 80 percent, while medical care prices have risen by 185 percent (BLS, 2002).

Health insurance premiums rose by 12.7 percent between 2001 and 2002, the largest increase since 1990 (Kaiser Family Foundation and HRET, 2002). These high rates of increases in medical care prices and health insurance premiums have been attributed to a number of factors, including medical technology advances (e.g., prescription drugs), aging of the population, multiyear insurance underwriting cycles, and, more recently, the loosening of controls on utilization by managed care plans (Strunk et al., 2002).

If people without health insurance paid the full bill when they were hospitalized or used physician services, there would seem to be no reason to believe that they contributed any more to the large increases in medical care prices and insurance premiums than insured persons. Although uninsured patients are not the only people who account for uncompensated care, the estimates presented assume that they are responsible for much of it. It is certainly an overestimate to attribute all hospital bad debt and charity care to uninsured patients, as Hadley and Holahan acknowledge, because patients who have some insurance but cannot or do not pay deductible and coinsurance amounts account for some of this uncompensated care. Of those physicians reporting that they provided charity care, about half of the total was reported as reduced fees, rather than as free care (Emmons, 1995). To reach their final estimate, Hadley and Holahan assumed that all of the free care by physicians and one-third of the reduced price care were provided to uninsured patients. Although 60 to 80 percent of the users of publicly funded clinic services, such as provided by federally qualified community health centers, the VA, and local public health departments are publicly or privately insured, these providers are not likely to be able to shift costs to private payers.

Little information is available for investigating the extent to which private employers and their employees subsidize the care given to uninsured persons through the insurance premiums they pay or the size of this subsidy. Because uninsured patients are disproportionately served by safety-net facilities, which serve relatively low proportions of privately insured patients (Gaskin and Hadley, 1999a,b; Lewin and Altman, 2000; IOM, 2003a), the opportunity for crosssubsidy is limited. Using the example of South Carolina, about seven-eighths of the private subsidies for uninsured care from nongovernmental sources came from philanthropies and other hospital (nonoperating) revenue, while the remaining one-eighth came from surpluses generated from private-pay patients (Conover, 1998).

It is difficult to interpret the changes in hospital pricing because published studies have examined individual hospitals rather than the overall relationships among uncompensated care, high uninsured rates, and pricing trends in the hospital services market overall. If for-profit hospitals are presumed to be profit maximizers (as standard economic theory predicts), they would have little or no opportunity to raise prices to private payers to compensate for providing services to the uninsured (Needleman, 1994; Zwanziger et al, 2000). One analyst argues that there has been little or no cost shifting during the 1990s, despite the potential to

do so, because of “price sensitive employers, aggressive insurers, and excess capacity in the hospital industry,” which suggests a relative lack of market power on the part of hospitals (Morrisey, 1996). Finally, the total burden of utilization and expenses by uninsured people has remained quite stable over the past decade or so (Taylor et al., 2001). For uncompensated care utilization by the uninsured to affect the rate of increase in service prices and premiums, the proportion of care that was uncompensated would have to be increasing as well.

There is somewhat more evidence for cost shifting among nonprofit hospitals than among for-profit hospitals because of their service mission and their location (Hadley and Feder, 1985; Dranove, 1988; Frank and Salkever, 1991; Morrisey, 1993; Gruber, 1994; Morrisey, 1994; Needleman, 1994; Hadley et al., 1996). Private hospitals have become less able to shift costs as health services markets have become more competitive (Morrisey, 1993; Bamezai et al., 1999; Keeler et al., 1999), although some analysts argue that the ability to shift costs remains substantial (Zwanziger et al., 2000). Some studies have demonstrated that the provision of uncompensated care has declined in response to increased market pressures (Gruber, 1994; Mann et al., 1995).

The concern with cost shifting from the uninsured to the insured population as a phenomenon may be changing to a focus on the transference of the burden of uncompensated care from private hospitals to public institutions due to decreased profitability of hospitals overall (Morrisey, 1996). Instead of shifting costs, private hospitals are cutting costs and reducing uncompensated care (Campbell and Ahern, 1993; Gruber, 1994; Zwanziger et al., 1994; Hadley et al., 1996; Morrisey, 1996; Dranove and White, 1998).

Private subsidies and cost shifting may also take place among communitybased providers, particularly in rural areas. Coburn (2002) argues that physicians in private practice are able to provide the 20 to 40 percent of uncompensated care in rural communities that they do because they are supported or subsidized by their community’s hospital. For employers in rural areas, the seriousness of the question of cross-subsidy is a function of scale. It is a greater burden in small towns, where there are fewer employers across whom to spread the cross-subsidy when it occurs in the form of higher costs for health care and for health insurance premiums. As a result, there is a competitive disadvantage that accrues to employers who offer more generous or greater subsidies of their employment-based coverage.

The extent to which cost shifting exists and thus the extent to which it influences medical care price increases are probably quite small. As reported in the previous section, the uninsured used an estimated $35 billion in uncompensated care in 2001. Hospitals received an estimated $23.6 billion in government subsidies basically earmarked for the care of the uninsured. Philanthropic support for hospital care to the uninsured has been estimated at another $800 million to $1.6 billion. Hadley and Holahan (2003a) assume that cross-subsidies from private insurance revenues to cover the costs of care provided to uninsured patients amount to 10 to 20 percent of the profit from hospital care provided to privately

insured patients ($1.5 to $3 billion). Physician charity care to uninsured patients accounted for 1.6 percent of national spending on physician and clinical services in 2001 (Hadley and Holahan, 2003a; Levit et al., 2003).

The Committee concludes that there is little reason to believe that uncompensated hospital and physician care appreciably inflates the prices that providers charge their private patients.

Comparing Public Financing of Direct Services with Insurance Programs

Finding: The costs of direct provision of health care services to uninsured individuals fall disproportionately on the local communities where they reside.

Most of the costs of care for uninsured Americans are passed down to taxpayers and consumers of health care in the forms of higher taxes and fewer resources available for other public purposes. A high uninsured rate locally may both reflect and contribute to an area’s economic challenges because the rate reflects the lack of employment-based coverage. Such coverage is less likely to be available in areas with a lower-waged labor force (IOM, 2001a). The tax burden of funding care for uninsured residents is more concentrated locally than is the burden of Medicaid finance or other insurance-based public programs in which the federal government participates (IOM, 2003a).

As the Committee noted in A Shared Destiny, given the differences in scope of public finance arrangements and the range of strategies employed to finance uncompensated care and safety-net arrangements from community to community, there is no generalized, simple relationship between a community’s uninsured rate and its tax burden. One would expect an increasing uninsured rate to create pressures to increase taxes and reallocate public funds devoted to other activities, if the legal structures of taxation and spending allow. Thus, a relatively greater or rapidly increasing uninsured rate may result in higher local and state tax burdens than in areas with proportionately fewer uninsured residents. On the other hand, states and localities are constrained in their ability to raise additional revenues through taxes to subsidize care for uninsured persons (Desonia, 2002). States with low per capita income or depressed economies, characteristics that are positively associated with uninsurance, experience even more fiscal stress financing care than do more prosperous states (Holahan, 2002; IOM, 2003a).

During the middle to late 1990s, the fiscal capacity and resources of all levels of government for spending on health programs grew. Starting in 1999, states increasingly have been experiencing hard times, with economic recession, federal cuts to Medicare and Medicaid, and public resistance to raising taxes (Dixon and Cox, 2002; Lutzky et al., 2002). Many states plan to cut Medicaid spending in 2003 and in the coming years (NASBO, 2002; Smith et al., 2002). The consequences of these responses are likely to result simultaneously in lower public

funding for health insurance, fewer public funds available for other purposes, and higher taxes.

The entitlement nature of most state government support for health financing means that these programs tend to absorb discretionary revenues (Hovey, 1991). Once funding levels for health entitlement programs have been decided, substantial pressure is placed on the remaining items in state and local budgets, including direct financing of public hospital and clinic services. States’ ability to levy taxes and their tax structures constrain revenue increases to support care for uninsured persons. Box 3.4 illustrates the health services funding crisis recently faced by Los Angeles County, a metropolitan area with approximately 8.7 million people under the age of 65, of whom nearly one-third lack any form of coverage.

Medicaid represents 20 percent, on average, of states’ budgets, and the financial incentives of the federal match as well as federal program requirements draw state funds away from more discretionary spending on the uninsured and into the Medicaid program (Miller, 2002b).13 Changes in a state’s spending on Medicaid are likely to affect its uninsurance rate and the demand for uncompensated care. Fifty-seven percent of national Medicaid expenditures are paid for by the federal government and 70 percent of SCHIP spending nationally has been paid for by the federal allocation.14 Health care provided through federally matched insurance programs like Medicaid and SCHIP are supported by a broader public financing base than is direct support for uncompensated care programs, which rely primarily on local or a combination of local and state financing (IOM, 2003a).

SUMMARY

The Committee has sketched the range of costs involved in providing health care services for uninsured people, both those borne out of pocket by the uninsured themselves and uncompensated care costs borne by a variety of public programs, providers of services, philanthropy, and possibly by other payers as well.

The full costs of being uninsured for uninsured individuals themselves, however, are not limited to their own payments for the services that they do receive. Uninsured persons, and children in families with uninsured members, on average use less health care than do insured persons and members of fully insured families. This “lost” utilization is hidden from view, yet it can prove costly in terms of subsequent ill health, disability, and premature death (IOM, 2002a). When uninsured persons do use health services, they and their families bear a disproportion-

|

BOX 3.4 Los Angeles County, CA California is home to the greatest number of uninsured people of any state in the nation. Los Angeles County, with nearly a third of its 8.7 million population under age 65 uninsured, has more uninsured people than do each of 46 states. About three-quarters of the 800,000 patients seen annually through the county public health system are believed to be uninsured. Over the past year, county officials have responded to the prospect of a large projected budget shortfall by 2005 by closing health clinics and hospitals and by laying off health care workers. Financial strains on the county health department’s budget, attributable to the sheer number of uninsured persons and their need for health care (which has been only partially met) have pressed the county to reduce its capacity to provide uncompensated care and safety net services. In the face of threatened cuts in emergency medical services and trauma care, Los Angeles voters took the unusual step in November 2002 of approving a property-tax increase, the first property-tax referendum since 1978, to raise about $170 million in additional revenues annually to secure these services. The economic downturn in the state, mirroring national trends, and rising costs for health care and for health insurance premiums have increased demand for uncompensated care. In the mid-1990s, a 5-year federal Medicaid waiver allowed the county to continue operating its public hospitals and to promote the use of outpatient, primary care rather than hospital emergency departments for nonurgent needs. This waiver was renewed for a second 5 years in 2000. Without the continued support of federal and state dollars, public-sector health care services for both insured and uninsured low-income county residents threaten simply to collapse. The current fiscal crisis for the county anticipates the end of the Medicaid waiver, which is scheduled to expire in 2005. California’s governor has declined to make up the loss of federal funds with state dollars and the state is also likely to cut back on Medicaid eligibility, which will increase the number of uninsured Los Angelenos. Closings within the county to date in response to budget shortfalls include 16 clinics and 2 public hospitals (High Desert in Lancaster, which will reopen as an outpatient clinic, and Rancho Los Amigos National Rehabilitation Center in Downey). Because these two hospitals did not have emergency departments, they were considered less central to the preservation of safety net arrangements in the county. SOURCES: Brown et al. (2002); Cardenas and Briscoe (2002); Cohn (2002); Riccardi (2002); Riccardi and Ornstein (2002); Rundle (2002); Sanchez (2002); Briscoe and Ornstein (2003); IOM (2003a); Ornstein (2003). |

ately higher proportion of the cost of care in relationship to their often lower incomes, in comparison to insured families and their higher incomes, on average. For uninsured persons and families, utilization is more likely to lead to higher out-of-pocket expenditures and greater financial stress (IOM, 2002b).

Health care services used by uninsured people often are uncompensated in

part or whole, resulting in costs to providers, communities, and society, as well as being a source of financial stress, anxiety, and possibly shame for recipients. The burden of uncompensated care is distributed widely and unevenly across providers and sponsors, depending on local configurations of health care services and institutions and on the structure of state and local revenue sources (IOM, 2003a).

Uncompensated care costs may beget additional external costs in the forms of higher local taxes to subsidize or reimburse uncompensated care, diversion of public funds from other public programs, and reduced availability of certain kinds of services within communities. These costs are discussed in the following chapter.