8

Malaria Control

INTRODUCTION

This chapter reviews malaria control over the last century, tracking malaria’s retreat from much of the world to its current lines of demarcation. It also describes individual control methods targeting both the mosquito vector and the human reservoir of infection and the current status of diagnosis and vaccine development. The chapter concludes with a discussion of malaria control strategies, including national and regional policies and programs operating today.

HISTORICAL OVERVIEW

Historically, malaria’s reach extended far beyond the tropics. Until the 19th century, transmission occurred in much of the temperate world, including parts of England, Holland, Germany, central and southeastern Europe, Asia, India, China, and the Americas (Shiff, 2002). In North America, the disease reached as far north as New York, and even Montreal (Barber, 1929). In the early 20th century, the Tennessee Valley Authority brought hydroelectric power to the southeastern United States, modernizing the region. As housing and lifestyles improved, and the human reservoir of infection decreased, malaria retreated (Desowitz, 1999). Malaria also disappeared during the first half of the 20th century from most of Europe following changes in land use, agricultural practices, house construction, and targeted vector control (Greenwood and Mutabingwa, 2002).

Then came the golden days of DDT, a highly effective insecticide first used as a delousing agent at the end of World War II. During the 1950s and 1960s, indoor residual spraying with DDT was the centerpiece of global malaria eradication efforts. DDT’s months-long ability to kill or deter adult female mosquitoes resting on treated walls after feeding led to further declines in malaria in India, Sri Lanka, the former Soviet Union, and other countries. By 1966, campaigns using DDT spraying, elimination of mosquito breeding sites, and mass treatment had freed more than 500 million people (roughly one-third of the population previously living in malarious areas) from the threat of disease (Shiff, 2002). Unfortunately, eradication was not sustained due to high program costs, community resistance to repeated house spraying, and the emergence of resistance to DDT. By the late 1960s, the hope of eradicating malaria through vector control was finally abandoned (Guerin et al., 2002). In many countries, the pendulum then swung to overreliance on chloroquine, a widely available antimalarial drug.

Sub-Saharan Africa was always a special case. With the exception of a few pilot programs, no sustained malaria control efforts were ever mounted there (Greenwood and Mutabingwa, 2002). The biggest obstacle was the widespread distribution of Anopheles gambiae, a long-lived and aggressive malaria vector. The entomological inoculation rate (EIR) (which measures the frequency with which a human is bitten by an infectious mosquito) rarely exceeds five per year in Asia or South America. In contrast, EIRs of over 1,000 have been recorded in several parts of sub-Saharan Africa (Greenwood and Mutabingwa, 2002).

Today, the global burden of malaria is concentrated in sub-Saharan Africa where stable, endemic disease is linked to poverty and highly efficient vectors. The insecticide-treated bednet (ITN)—first shown in The Gambia to reduce overall childhood mortality by 60 percent when combined with malaria chemoprophylaxis (Alonso et al., 1991)—is the vector control tool with the greatest promise for Africa. At the Africa Summit on Roll Back Malaria in Abuja, Nigeria in 2000, leaders from 44 African countries set a target of 60 percent ITN coverage of pregnant women and infants in Africa by 2005, an ambitious goal requiring roughly 160 million ITNs at an estimated cost of US$1.12 billion (Nahlen et al., 2003). Sadly, the goal is still far from being met. At the same time, insecticide resistance (involving pyrethroids and DDT) is a growing problem in Africa, along with environmental change brought by agriculture and other types of development that foster mosquito breeding. International sponsors also have withdrawn support for DDT due to environmental concerns.

With respect to malaria’s human reservoir, the overriding challenge facing Africa is the development of drug resistance by Plasmodium falciparum to cheap and effective treatments (chloroquine and sulfadoxine-

pyrimethamine [SP]), compounded by large and, in some cases, mobile infected populations.

BASIC PRINCIPLES OF MALARIA CONTROL

Successful malaria control programs traditionally use multiple interventions. In 1952, Paul Russell (a noted Rockefeller Foundation malariologist, and former head of the Allied antimalaria campaign in Italy) listed five approaches to malaria eradication (Russell, 1952):

-

Measures to prevent mosquitoes from feeding on humans (human-vector contact)

-

Measures to prevent or reduce the breeding of mosquitoes

-

Measures to destroy mosquito larvae

-

Measures to kill or reduce the lifespan of adult mosquitoes

-

Measures to eliminate malaria parasites from humans

Since Russell’s era, an increasing emphasis on the control of human disease has produced three additional strategies (Beales and Gilles, 2002):

-

Measures to prevent and reduce malaria mortality (especially in high-risk groups)

-

Measures to reduce malaria morbidity

-

Measures to reduce malaria transmission

Today’s control efforts mainly rely upon the interruption of human-vector contact and treatment of infected persons. Personal protection via ITNs or curtains is generally preferred in settings where vectors feed indoors during nighttime sleeping hours. ITNs also kill malaria vectors and reduce the local intensity of transmission (the “mass effect”). Indoor residual spraying (IRS) with DDT or a pyrethroid insecticide is another way to reduce bites by vectors whose feeding and resting habits render them susceptible, as long as the majority of houses in a targeted community are sprayed. IRS also is the preferred vector control method during malaria epidemics and in refugee camps since trained spray teams can rapidly cover likely areas of transmission.

Case management—which encompasses prompt access to health care, an accurate diagnosis, and effective treatment—is the other cornerstone of malaria control. The current failure to control malaria with drugs often starts with a failure to deliver appropriate case management to many malaria sufferers, particularly at the periphery of health systems.

Other control strategies outlined by the World Health Organization (WHO) in 1993 include early forecasting of malaria epidemics and the

development of epidemiological information systems; capacity-building in basic and applied research; and ongoing assessment of ecological, social, and economic determinants of disease within affected countries and regions (WHO, 1993). Effective field operations also require expertise and teamwork. Qualified personnel with the scientific knowledge, skills, and authority are perhaps the single most important resource needed for effective vector control (Roberts et al., 2000). The same need for knowledge applies to those rendering clinical care to malaria patients: from parents, village health care workers, drug sellers, and traditional healers to laboratory workers, nurses, doctors, and other health care professionals.

INSECTICIDES AND INSECTICIDE RESISTANCE

Insecticides in Public Health

Immediately after World War II, DDT and other chlorinated hydrocarbon insecticides formed the mainstay of malaria control. DDT was initially developed as a public health insecticide prior to its widespread agricultural use and recognition as an environmental pollutant (Curtis and Lines, 2000). Of note, when used indoors in limited quantities, DDT’s entry into the global food chain is minimal (Attaran et al., 2000). (For a full summary of DDT’s role in public health, readers are referred to a recent review [Taverne, 1999]).

Today, despite concerns over their environmental effects and possible inactivation by mosquito vectors, chemical insecticides remain key elements in malaria control.

A WHO-coordinated research program is now in place to develop new candidate insecticides and test their activity and safety(WHO, 1996a). The specifications for pesticides used in public health are part of the WHO Pesticide Evaluation Scheme (WHOPES).

Classified by chemical characteristics, the most common insecticides currently used in public health practice are:

-

Petroleum oils and their derivatives

-

Active constituents of flowers of pyrethrum (pyrethrins) or newer synthetic compounds of this group (pyrethroids)

-

Chlorinated hydrocarbons (e.g., dichloro-diphenyl-trichloroethane (DDT), hexachlorocyclohexane (HCH), and dieldrin)

-

Organophosphorous insecticides (e.g., malathion, and temephos)

-

Carbamates (e.g., propoxur, and carbaryl)

-

Insect growth regulators (e.g., diflubenzuron, methoprene, and pyriproxyfen)

Pyrethrum, an extract of dried chrysanthemum flowers, is the oldest effective insecticide known. Both pyrethrum and its natural and synthetic relatives (pyrethrins and pyrethroids) are nerve poisons that rapidly permeate and kill adult insects with high margins of mammalian safety. They also demonstrate rapid knock down (i.e., immobilizing) and repellant effects. The chief drawback of the class is its relatively short-lived action, although newer synthetic compounds such as permethrin and deltamethrin are more stable than naturally occurring products. The residues of DDT, in contrast, remain active for up to a year following application to impervious surfaces such as plastered walls (on mud brick, DDT loses its insecticidal effect faster). DDT’s long-term repellant, and contact irritant effects probably contribute as much or more than its direct insecticidal action in controlling malaria transmission (Roberts et al., 2000).

On a molecular level, all major classes of chemical insecticide exert their principal effects within the nerve tissue of targeted insects. DDT and pyrethroids cause persistent activation of sodium channels (Soderlund and Bloomquist, 1989), while pyrethroids also act on receptors that normally govern inhibitory neurotransmission, and organophosphates and carbamates target acetylcholinesterase.

Insecticide Resistance

Levels of resistance in insect populations reflect the amount and frequency of insecticide contact as well as inherent characteristics of the target species. Thus far, DDT resistance has not developed in long-lived disease vectors such as tsetse flies or triatomid bugs (definitive hosts of African sleeping sickness and Chagas’ disease, respectively). Mosquitoes, in contrast, have several characteristics suited to rapid development of resistance, including a short life cycle and abundant progeny.

In 1946, only two species of malaria vector were resistant to DDT. However, by 1966 the emergence of resistance was clear: 15 species were resistant to DDT, and 36 species were resistant to dieldrin (WHO Expert Committee on Insecticides, 1970). By 1991, 55 anopheline vectors demonstrated resistance to one or more insecticides. Of these, 53 were resistant to DDT, 27 to organophosphates, 17 to carbamates, and 10 to pyrethroids (WHO, 1992a,b). A decade later, some form of pyrethroid resistance (either decreased mortality, or decreased excito-repellancy of mosquitoes by pyrethroid-impregnated ITNs) had been reported from countries in Asia, Africa, and South America (Takken, 2002).

Three major groups of inactivating enzymes (glutathione S-transferases, esterases, and monooxygenases) are responsible for metabolic resistance to DDT, pyrethroids, organophosphates, and carbamates in Anopheles mos-

quitoes. Knock-down resistance (kdr) is a separate resistance phenotype linked to a point mutation in sodium channels targeted by both pyrethroids and DDT. Although prevalent in A. gambiae in West Africa, kdr has not impaired ITN efficacy in the region (Sina and Aultman, 2001; Hemingway and Bates, 2003). In southern Africa, in contrast, the local vector A. funestus has acquired metabolic resistance to pyrethroids, rendering ITNs ineffective (Chandre et al., 1999; Brooke et al., 2001). A looming concern for the future is that A. gambiae in equatorial Africa will acquire the same metabolic resistance to pyrethroids seen in A. funestus in southern Africa. Currently, metabolic resistance to pyrethroids in A. gambiae is limited to focal areas of West Africa and Kenya (Ranson et al., 2002).

In coming years, strategies to decrease insecticide resistance may include rotations, mosaics, and mixtures of agricultural and environmental insecticides guided by mathematical models (Tabashnik, 1989). Until now, little field-testing of models has been conducted; however, with new biochemical and molecular field tools, large-scale trials of resistance management are feasible. Treating ITNs with two insecticides with differing mechanisms of action is another approach that may be implemented in the near future. In West Africa, bi-treated nets pairing pyrethroids with carbosulfan (a carbamate insecticide), or chlorpyrifos-methyl (an organophosphate insecticide) are currently under evaluation (Muller et al., 2002).

INSECTICIDE-TREATED BEDNETS AND INDOOR RESIDUAL SPRAYING

History of ITNs

More than two thousand years before Ronald Ross and Giovanni Battista Grassi showed that mosquitoes transmit malaria, human beings used nets to fend off night-biting insects. Mosquito nets appear in historical records from the Middle East to West Africa to Papua New Guinea (Lindsay and Gibson, 1988). The Greek writer Herodotus (484 - ?425 BC) described how Egyptians living in marshy lowlands protected themselves with fishing nets.

|

Every man there has a net which he uses in the daytime for fishing, but at night he finds another use for it: he drapes it over the bed … and then crawls in under and goes to sleep. Mosquitoes can bite through any cover or linen blanket … but they do not even try to bite through the net. Herodotus, The Histories |

By the early 19th century, British colonists in India—most likely inspired by the example of Punjabi fishermen—also were sleeping under nets. However, it was not until World War II that textiles and insecticides were combined. In central Asia, the Soviet army applied juniper oil to bednets to repel mosquitoes, and sand flies bearing malaria and leishmaniasis (Blagoveschensky et al., 1945), while the American military in the Pacific theater impregnated bednets and jungle hammocks with 5 percent DDT to ward off malaria and filariasis (Harper et al., 1947).

Interest in insecticide-impregnated nets as a malaria control tool resurfaced in the late 1970s and early 1980s. By then, synthetic pyrethroids were the logical insecticide choice because of their low mammalian toxicity and known efficacy in killing and repelling a variety of nuisance and disease-bearing insects. Several governments including the Philippines, Solomon Islands, and Vanuatu began to include ITN promotion as one of their malaria control objectives (Chavasse et al., 1999). However the most successful government-financed ITN programs today are found in China and Vietnam, where the public sector’s chief contribution is to offer regular net re-treatment services. When re-treatment is provided free of charge (e.g., China and Vietnam), coverage is generally high (Curtis et al., 1992). Conversely, in Africa, where many nets and insecticides have been provided free or at subsidized prices through local projects and NGOs, less than 5 to 20 percent of nets are re-treated (Snow et al., 1999; Rowley et al., 1999; Guillet et al., 2001).

Individual and Community Effects of ITNs

Child Mortality

After a number of small-scale studies in the 1980s showed favorable effects, the first large-scale study of ITNs plus chemoprophylaxis reported a 60 percent reduction of all-cause child mortality (Alonso et al., 1991). These results prompted the UNDP/World Bank/WHO Special Programme for Research and Training in Tropical Diseases (TDR) to sponsor four randomized controlled trials in Africa to assess the effect of ITNs on all-cause mortality in African children in different epidemiologic settings. A cluster randomization design was used in all four trials. In The Gambia (D’Alessandro et al., 1995), a 25 percent reduction in all-cause mortality was seen in children less than 9 years old. In Kenya (Nevill et al., 1996) and Ghana (Binka et al., 1996), the introduction of ITNs was associated with 33 and 17 percent reductions in all-cause child mortality, respectively, in children under 5 years of age. Study populations in all three sites ranged from 60,000 to 120,000 (Table 8-1).

The fourth randomized controlled trial in Burkina Faso (Habluetzel et

TABLE 8-1 Protective Efficacy of ITNs: Reductions in Child Mortality in Five Randomized Controlled Trials

|

Country in Which Study Was Performed |

Percent Reduction in Child Mortality |

EIR |

|

The Gambia (D’Alessandro et al., 1995)a |

25% |

1-10 |

|

Kenya (Nevill et al., 1996) |

33% |

10-30 |

|

Ghana (Binka et al., 1996) |

17% |

100-300 |

|

Burkina Faso (Habluetzel et al., 1997) |

15% |

300-500 |

|

Kenya (Phillips-Howard et al., 2003) |

16% |

200-300 |

|

aThis study was considered an effectiveness, as opposed to an efficacy, study. |

||

al., 1997) examined insecticide-treated curtains (ITCs) rather than bednets in roughly 100,000 residents of a region with alternating high and low malaria seasons. Baseline mortality, approaching 45 per thousand, was the highest to date among the four African ITN trials (Diallo et al., 1999). After 2 years of tracking, the use of ITCs was associated with a 15 percent decrease in all-cause mortality in Burkina Faso, concentrated in the first year of use.

Viewed as a group, the four TDR-sponsored randomized controlled trials demonstrate decreasing ITN efficacy with increasing transmission pressure, since sites experiencing higher EIRs (100-500 infective bites per person per year, i.e., Ghana, and Burkina Faso) witnessed lower ITN benefits.

The most recent group-randomized controlled trial of permethrin-treated bednets conducted in western Kenya (Hawley et al., 2003a) was designed to assess ITN efficacy at an upper range of year-round transmission. This study yielded an overall protective efficacy of 16 percent in all-cause child mortality; thus, ITN benefits were validated in an area of very high transmission. Maximum effect was dependent on regular re-treatment of ITNs, however. For example, the protective efficacy of ITNs in children aged 1-11 months fell from 26 to 17 percent when re-treatment was delayed beyond 6 months. The Kenyan trials also demonstrated roughly 90 percent transmission reduction from a baseline EIR of 60-300 (Gimnig et al., 2003b). When ITNs are combined with highly effective therapy such as artemisinin combination therapies (ACTs)—even in highly endemic areas—it is possible that the EIR could decline even further, approaching 0 (Personal communication, N. White, Mahidol University, February, 2004).

Child and Maternal Morbidity

Acute and chronic consequences of childhood malaria include uncomplicated febrile episodes with parasitemia, and anemia. Data from a large meta-analysis suggest that ITN use under stable transmission conditions roughly halves mild malaria episodes in children under five (Lengeler, 2001). In a nonrandomized trial of ITNs in southwestern Tanzania, treated nets conferred protective efficacy of 62 and 63 percent, respectively, on parasitemia and anemia in children under 5 (Abdulla et al., 2001). In an area of high perennial transmission in western Kenya, ITNs delayed the time to first infection in infants from 4.5 to 10.7 months (ter Kuile et al., 2003a).

Repeated malaria infection also causes anemia and morbidity in pregnant women and newborns. Four randomized controlled trials of ITNs in pregnancy have shown variable benefits in different transmission settings. In Thailand and The Gambia (areas with lower, seasonal transmission), ITNs significantly reduced malaria parasitemia and maternal anemia (Dolan et al., 1993; D’Alessandro et al., 1996); in The Gambia, they also increased birth weight (D’Alessandro et al., 1996). However, similar benefits were not seen in areas with more intense transmission (coastal Kenya and Ghana) (Shulman et al., 1998; Browne et al., 2001), raising concern that ITNs might not protect pregnant women in areas with a very high EIR. This concern was allayed by the most recent findings.

In the western Kenya trial, complete data were available in nearly 3,000 pregnancies (ter Kuile et al., 2003b). Before the study began, up to one-third of all infants were born preterm, small for gestational age, or with low birth weight. ITN-using pregnant women (gravidae 1-4) experienced a 38 percent reduction in maternal parasitemia, a 47 percent reduction in malarial anemia, and a 35 percent reduction in placental malaria at the time of delivery, while their newborns demonstrated a 28 percent reduction in low birth weight.

Community and Population Effects

In addition to conferring benefits upon individual users, ITNs can protect nonusers within ITN households as well as nonusers in nearby houses. Such effects were first noted in early village-scale ITN trials in Burkina Faso (Robert and Carnevale, 1991), Tanzania (Magesa et al., 1991), Kenya (Beach et al., 1993), and Zaire (Karch et al., 1993). More recent ITN studies have confirmed community-wide reductions in vector populations (Hii et al., 1997; Binka et al., 1998; Hii et al., 2000; Howard et al., 2000; Maxwell et al., 2002). Some ITN trial data have even demonstrated spatial effects on health. In Ghana, child mortality increased by 6.7 percent for every 100 m away from an intervention compound (Binka et al., 1998),

while in western Kenya, mortality, parasitemia, and anemia decreased in unprotected children living within 300 m of households from ITN villages (Gimnig et al., 2003a). The minimum ITN coverage needed to achieve community benefits is 50 to 60 percent of households within a neighborhood with suitable indoor, night-biting vectors (Hawley et al., 2003b). In Asia, in contrast, ITNs have had mixed results because vectors often bite outdoors in the late evening (or sometimes in the early morning), and both children and adults are susceptible.

Long-Lasting Insecticidal Nets

At present a single insecticide treatment of a conventional cotton or nylon mosquito net lasts for 6 to 12 months. “Long-lasting insecticidal nets” (with insecticide incorporated directly in net fibers) would eliminate the need for regular re-treatment. Two prototypes (Olyset and Permanet) are now on the market while others are being developed (Moerman et al., 2003). One early problem with the Vestergaard-manufactured Permanet was inconsistency among batches; in a study of randomly-sampled new unwashed, traditionally washed, and up to 18 months field-used products, insecticide concentration was much reduced after two washes, and mosquito mortality reached unacceptably low levels after only 12 months (Muller et al., 2002). These problems have presumably been rectified since Permanets produced by Vestergaard are now approved by WHO and production is slated to increase to one million nets per month (Personal communication, B. Greenwood, London School of Hygiene and Tropical Medicine, March 2004).

Indoor Residual Insecticide Spraying

Sprayed insecticides to kill adult mosquitoes were introduced on a large scale in the mid-1930s. Pyrethrum was first used for indoor residual spraying (IRS) in southern Africa and India and later replaced by DDT after World War II. IRS is most effective in reducing mosquitoes that rest indoors following a blood meal. To be effective, IRS does not have to kill all Anopheles at once but simply prevent a large proportion from surviving 12 to 14 days (the time it takes for a malaria parasite to develop to the infective stage within the mosquito). Even with the hardiest vectors, this can be achieved with a daily mortality of 40 to 50 percent. In places with lower malaria endemicity, daily mosquito mortality of 20 to 25 percent generally is adequate (Beales and Gilles, 2002).

Just as ITNs extend benefits to nonusers in the community, IRS is especially effective when applied on a large scale, since this maximizes the reduction in mosquito lifespan, and overall transmission. This so-called

mass effect has been well documented in a number of IRS trials. Specific examples include three demonstration projects in Africa: an observational study in the Pare-Taveta Malaria Scheme in Tanzania where dieldrin reduced malaria transmission from an annual EIR of 10-50 to <1 (Pringle, 1969; Bradley, 1991); a trial in Kisumu, Kenya, where IRS with fenitrothion reduced malaria transmission by 96 percent compared to baseline over 2 years (Payne et al., 1976); and the Garki project in northern Nigeria where IRS with propoxur also substantially decreased transmission and improved infant and child mortality (Molineaux, 1985) (Box 8-1).

Over the last 30 years, DDT-based IRS has declined, in part, because of DDT resistance among malaria vectors. A lack of sustained government support and financing as well as general disapproval of DDT by the international community also have contributed to IRS’s restricted use in sub-Saharan Africa. In parts of Asia, Latin America, and southern and northeastern Africa where IRS is still used, it is typically organized and paid for by governments (for example, government-funded DDT house spraying was recently reinstated in KwaZulu Natal, South Africa, and the Madagascar highlands because of rising prevalence of pyrethroid-resistant A. funestus vectors and human malaria cases [Hargreaves et al., 2000]). IRS also is used in urban epidemics and refugee camps worldwide, and sometimes provided by foreign and multinational companies for the protection of employees and local communities in malaria-endemic areas (Sharp et al., 2002a).

The implementation of IRS is not trivial, and, if incorrectly performed, may be quite ineffective (Shiff, 2002). Houses and animal shelters within a target area should receive IRS before the start of the transmission season and at regular intervals thereafter. Before application of insecticide, all furniture, hanging clothing, cooking utensils, food and other items should be removed from human habitations, and left covered outside. Emulsions or solutions of insecticide are often preferred over suspensions of water-dispersible powders, which leave whitish deposits. Mud and porous plaster walls retain less IRS insecticide than wood or non-absorptive surfaces.

Barriers to ITN and IRS Use

ITNs and IRS both require user cooperation, albeit in different ways. Current-generation ITNs must be properly installed, faithfully used, and retreated with insecticide every 6 to 12 months in order to maintain extended efficacy. IRS, in comparison, is passive but intrusive. Some residents of endemic areas forfeit IRS benefits by painting or replastering sprayed walls, while other families evade IRS altogether by locking their houses during the spraying round (Mnzava et al., 2001; Goodman et al., 2001). In addition, some housing or shelter materials such as plastic sheeting are not amenable to residual spraying.

|

BOX 8-1 In the early 1970s, an ambitious malaria control experiment was undertaken to determine whether malaria transmission could be interrupted in a highly endemic area of Africa. The experiment was conducted in a group of villages near the town of Garki in northern Nigeria. Villages were allocated to three intervention groups.

The main findings of the Garki project were as follows:

The Garki project was planned at a time when eradication of malaria was still viewed as a serious option for highly endemic areas such as Nigeria. The experiment showed that interrupting transmission was not possible even when a full armamentarium of malaria control tools was applied. Its findings helped to redirect attention from eradication to controlling the clinical effect of malaria in Africa. Although the study did not focus on malaria-related morbidity and mortality to the same degree as would be likely today, its parasitemia data suggest that mortality and morbidity from malaria would have fallen dramatically in study villages during the 2-year period of integrated malaria control. Brian Greenwood, London School of Hygiene and Tropical Medicine |

Despite its proven benefits, current ITN use in sub-Saharan Africa also is low. Most households in malaria endemic areas do not possess any net, insecticide-treated or not. In nine African countries surveyed between 1997 and 2001, a median 13 percent of households had one or more nets of any kind; a median 1.3 percent of households in three countries owned at least one ITN; and across 28 countries, only 15 percent of children under age 5 were sleeping under any net (WHO/UNICEF, 2003). Not surprisingly, net ownership and use are lowest in poor households.

In addition to purchase cost and re-treatment, one additional barrier to ITN use is the common misconception that ITNs are meant to control mosquitoes as opposed to malaria. In urban areas with untreated wastewater and high year-round populations of “nuisance” culicine mosquitoes, this misconception favors ITN use. In rural areas, however, mosquito densities and mosquito nuisance are generally lower despite year-round biting by clandestine female anophelines. As a result, ITN use is rarely sustained night after night, especially during the dry season (Gyapong et al., 1996; Binka et al., 1996; Binka and Adongo, 1997).

In western Kenya, the use of ITNs was observed directly in nearly 800 households (Alaii et al., 2003a). About 30 percent of ITNs in homes were unused. Children less than 5 years of age were less likely to use ITNs than older individuals, and ITNs were more likely to be used in cooler weather. Neither mosquito numbers, relative wealth, number of house occupants, nor educational level of the head of the household influenced adherence. Excessive heat was often cited as a reason for not using a child’s ITN. Researchers also commented on the effort required of caregivers to store and rehang the ITN on a daily basis (Alaii et al., 2003a).

Finally, misunderstandings about malaria also lower incentives to use ITNs and/or IRS. In southern Ghana, the Adangbe people believe that asra, a local disease that resembles malaria, is the result of prolonged exposure to heat (Agyepong, 1992). In Bagamoyo District, Tanzania, degedege—a local term for fever and convulsions—is often blamed on a bird-spirit instead of cerebral malaria (Makemba et al., 1996). In western Kenya, many ITN trial participants believed that malaria was a multicausal disease and that ITNs were therefore only partly effective (Alaii et al., 2003b).

OTHER VECTOR CONTROL MEASURES

Household and Community Measures

In areas of high malaria transmission, prevalence of infection may vary significantly over relatively short distances. This has been observed not only in Africa (Greenwood, 1999) but in other countries, such as Papua New

Guinea (Graves et al., 1988), and Pakistan (Strickland et al., 1987). Local factors (in addition to IRS and insecticide-impregnated materials) that affect the microepidemiology of malaria are house siting, screening and construction, proximity of animals to human dwellings, and use of mosquito deterrents such as repellants, aerosols, and fumigants.

House Siting and Construction

Despite the fact that anopheline mosquitoes can fly substantial distances, the proximity of houses or villages to a breeding site strongly influences malaria risk, especially where breeding sites are restricted. In a suburb of Dakar, Senegal, malaria prevalence rose steeply from the center to the edge of town adjacent to marshy breeding sites of Anopheles arabiensis (Trape et al., 1992). In Sri Lanka, the risk of malaria was much higher among those who lived in poor quality houses within 2.5 km of a river where A. culicifacies bred (Gunawardena et al., 1998).

House design and construction also influence the risk of malaria (Schofield and White, 1984). Eaves—which allow interior ventilation, and the escape of smoke from cooking fires—are a common feature that facilitate mosquito access to sleeping areas in houses in the tropics. Using mud or plaster to fill in eaves (Lindsay and Snow, 1988), or hanging eaves curtains (Curtis et al., 1992) reduce human-vector contact. In Sri Lanka, Gunawardena et al. (1998) estimated that the cost of upgrading all low-quality housing (whose residents suffered a fourfold risk of malaria compared to families living in well-constructed houses in the same locale) would be balanced by savings in malaria treatment costs over a period of 7 years.

Animals

In some communities, animals live in or near houses. Zooprophylaxis is a term that suggests the possible diversion of mosquito bites from humans to nearby animals. However, this diversion depends entirely on the biting habits of the local vector and varies from species to species. In some cases, livestock may actually attract certain mosquitoes that would otherwise avoid human habitats, resulting in increased malaria exposure to household members (Hewitt et al., 1994; Bouma and Rowland, 1995; Mouchet, 1998). In Pakistani and Afghan refugee camps, malaria cases were concentrated in communities that kept cattle, presumably because the local vectors A. culicifacies and A. stephensi were preferentially attracted to these households (Bouma and Rowland, 1995).

Repellants, Aerosols, and Fumigants

Many communities use aromatic smokes to deter mosquitoes. In The Gambia, tree bark combined with synthetic perfumes (locally known as churai) reduced the number of mosquitoes entering a room but not the incidence of malaria (Snow et al., 1987). In contrast, traditional fumigants in Sri Lanka decreased malaria (van der Hoek et al., 1998). In Thailand, a mixture of DEET (N,N-diethyl-m toluamide) and a paste made from a local tree (wood apple) was an effective repellant when applied to the skin (Lindsay et al., 1998).

Commercially manufactured coils containing pyrethroids or DDT also repel mosquitoes (Charlwood and Jolley, 1984; Bockarie et al., 1994). Although coils are cheap, households may spend substantial sums of money on items of this kind. In Dar es Salaam, Tanzania, average household expenditure on antimosquito measures was in the region of US$2-3 per month (Chavasse et al., 1999).

Environmental and Biologic Management

Since A. gambiae can breed in virtually any puddle, larval control in sub-Saharan Africa has always been challenging. Where vector breeding sites are few in number and easily identified, however, environmental or biologic control of larval breeding sites is often feasible. Petroleum oil larvicides have played an important part in mosquito control since the beginning of the 20th century. Breeding sites also may be eliminated by draining or filling in pools, modifying the boundaries of rivers or their run-off systems, and creating impoundments (reservoirs behind dams). Intermittent drying of rice fields, stream sluicing or flushing, salination of coastal marshes or lagoons (for example, using tidegates), shading of stream banks, and clearing of vegetation are naturalistic manipulations that proved beneficial in controlling certain vectors, primarily in India and southeast Asia. Although eclipsed by residual insecticides for several decades, many of these environmental methods of vector control are now back in vogue with strong WHO endorsement.

Biological control strategies, including use of bacteria such as Bacillus thuringiensis subsp. israelensis (Bti), or larvivorous fish, also have been combined with other control measures with variable success (Romi et al., 1993; Karch et al., 1993; WHO, 1999; Kaneko et al., 2000). Bti spores produce a toxin that is poisonous to mosquitoes and other aquatic insects but harmless to plants, animals, and humans. Bacillus sphaericus (Bsph) multiplies in polluted waters, and produces a longer-acting toxin than Bti; however, resistance to Bsph toxin is present in some mosquito populations in India, Brazil, and France (WHO, 1999).

Genetic Control

Genetic control refers to any method that reduces an insect’s reproductive or disease-transmitting potential through alteration of its hereditary material. The oldest form of genetic control is sterile insect technology (SIT), a proven strategy in past campaigns against screw worm, tsetse flies, and Mediterranean fruitflies. Unfortunately, when mass hybrid sterility was tried against A. gambiae in Burkina Faso, West Africa, few matings actually took place between the sterile males and wild female anophelines. Producing large numbers of sterile yet competitive male mosquitoes, and successfully releasing them in the wild remain major operational hurdles.

First predicted decades ago by Curtis (Curtis, 1968), genetically modified mosquitoes are now another potential means of vector control. The reasoning is as follows. Since only some anopheline mosquitoes transmit malaria, genes encoding the nontransmitting phenotype, or genes that prevent malaria parasites from developing within mosquitoes altogether, could be inserted into vector genomes (Collins, 1994; James et al., 1999). The feasibility of this approach was recently shown when a synthetic gene inserted into A. stephensi almost fully prevented its ability to transmit a strain of rodent malaria (Ito et al., 2002). However, the same practical obstacle facing SIT—namely, the rapid replacement of native mosquito populations—affects genetically modified mosquitoes. Concerns also have been raised about the fitness of genetically modified mosquitoes, the negative consequences of unstable genetic modifications, and public reservations regarding deployment of genetically altered organisms (Clarke, 2002).

TREATMENT AND CHEMOPREVENTION

The primary aim of malaria treatment is saving lives. Prompt, effective treatment in the early stages of falciparum malaria reduces the risk of death as much as 50-fold, whereas effective treatment after progression to severe illness produces only a five-fold reduction in the risk of dying (White, 1999). However, malaria treatment also can reduce malaria transmission in endemic areas. This section reviews the role of treatment as a control measure capable of reducing malaria transmission, as well as past and present chemoprevention strategies in residents of malaria-endemic areas. (See Chapter 9 for more detailed information regarding antimalarial drugs, drug resistance, and treatment protocols.)

Antimalarials and Reduction of Malaria Transmission

A key objective of many early studies of widespread antimalarial distribution was interrupting malaria transmission (Greenwood, 2004). Two approaches were tried: treatment of symptomatic cases; and mass drug

administration, which included mass chemoprophylaxis, and the Pinotti method—the systematic addition of antimalarial drugs to salt.

Treatment of Symptomatic Cases

The notion that treating symptomatic individuals might indirectly protect an entire malaria-exposed population dates back to Robert Koch and the early years of the 20th century (Harrison, 1978). At that time, with this goal partly in mind, quinine was used extensively in Italy and elsewhere. Since quinine has little effect on gametocytes, however, it had little effect on transmission overall.

Today, in contrast, artemisinin-based drugs (which do kill early-stage gametocytes as well as asexual parasites) have helped to decrease transmission in selected areas of Asia and Africa. On the Thai-Burmese border, where field studies using ACTs were first undertaken in 1991, replacing mefloquine with mefloquine-artesunate as first-line treatment for symptomatic malaria substantially reduced the incidence of local P. falciparum infection (Nosten et al., 2000). Widespread use of artemisinins and ACTs—along with ITNs or IRS—also contributed to a marked decline in the overall incidence of falciparum malaria in Vietnam (Hung et al., 2002) and South Africa (Barnes et al., 2003) (Box 8-2)—both areas with relatively low EIRs. Whether widespread use of ACTs will bring about a similar outcome in areas of higher malaria transmission (EIR > 100) is still unknown.

Mass Drug Administration

Unlike Southeast Asia and South Africa, many malaria infections in sub-Saharan Africa—especially in older children and adults—are asymptomatic and untreated but have parasite densities sufficient for transmission (von Seidlein et al., 2002). Under these conditions, reducing malaria transmission by use of a gametocytocidal drug requires that asymptomatic as well as symptomatic carriers be treated. This led to the concept of mass drug administration (MDA). During MDA, the entire population of a community known to contain many asymptomatic infected subjects receives treatment without first determining who is actually parasitemic.

MDA as a method of reducing malaria transmission gained momentum after the 8-aminoquinolones (of which primaquine is the leading prototype) were discovered. This class of drugs is highly effective at killing gametocytes of P. falciparum. One of the first trials to investigate 8-aminoquinolones as MDA agents took place in a Liberian rubber plantation in 1930. Mass treatment with plasmoquine led to a marked decrease in parasite prevalence and a reduction in infected mosquitoes in two treated camps (Barber et al., 1932). During the 1960s and 1970s, several more

|

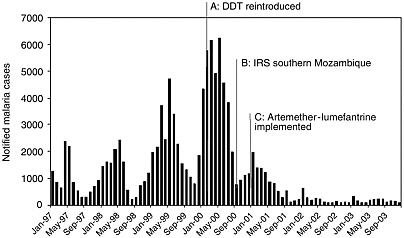

BOX 8-2 Ingwavuma district in northern KwaZulu Natal carried the highest malaria burden in South Africa until 2000. This changed after improvements in vector control in KwaZulu Natal and neighboring southern Mozambique during 2000, and the implementation of an artemisinin combination therapy (ACT), artemether-lumefantrine (AL), in January 2001. These interventions were followed by a 78 percent decrease in malaria case notifications in the province within 1 year. There was a further 75 percent decrease in notifications in 2002, and this decrease was sustained throughout 2003 (Figure 8.2-1).  FIGURE 8.2-1 The synergistic effect of improved vector control and artemisinin combination therapy, artemether-lumefantrine, on malaria transmission in KwaZulu Natal, South Africa.

SOURCE: Muheki C, Barnes K, McIntyre D. 2003. Economic Evaluation of Recent Malaria Control Interventions in KwaZulu, South Africa: SEACAT Evaluation. SEACAT. |

|

The success of this dual intervention is further reflected by the 89 percent decrease in both malaria-related hospital admissions (range 81-92 percent), and deaths (range 78-93 percent) across the three rural district hospitals that serve the Ingwavuma community. Despite KwaZulu Natal also carrying South Africa’s highest burden of the HIV/AIDS epidemic, the total number of “all cause” hospital admissions also was reduced following improved malaria control. Dr Hervey Vaughan Williams, medical superintendent of Mosvold hospital, a rural district hospital in Ingwavuma, reports that “during the peak of the 2000 malaria epidemic, hospital admissions were averaging three patients per bed.” Following the reduction in the overall number of hospital admissions, it is expected that the standard of care for all patients could be improved. These improvements in malaria control also have been welcomed by the local communities. During focus group discussions on malaria, there was general enthusiasm for the change in malaria treatment. One female household head reported “Every year I used to have malaria. This year I heard that new pills were coming. I was very sick with malaria. They gave me the new pills … the (next) morning I was very fine. … I have cultivated and harvested and I’ve never had malaria again this year.” These comments are in contrast with the opinion of female household heads on SP, e.g., “Those tablets that were used before the present ones … most of us didn’t like taking them … because after taking them you would feel as if the malaria has become more severe than before.” The community perceptions that those with malaria should seek health care urgently at public-sector facilities, is likely to have contributed to the marked public health effect observed following the implementation of AL. These perceptions were described during focus group discussions: “There is no way to treat malaria besides taking him to the clinic”; “Once you waste time at the sangoma [traditional healer], you die.” The sustained benefits to public health following the implementation of artemether-lumefantrine in KwaZulu Natal are most encouraging. These reflect the benefits of ACT in significantly decreasing treatment failure and gametocyte carriage rates, within a context of effective vector control, and a relatively well developed rural primary health care infrastructure. Karen Barnes, University of Cape Town (2003) |

MDA trials took place in Africa and Asia with the primary aim of interrupting transmission (von Seidlein and Greenwood, 2003). By today’s standards, the studies were poorly designed and their results difficult to assess; however, in nearly all cases, MDA failed to interrupt transmission, although it did markedly reduce parasite prevalence (Greenwood, 2004) (Box 8-1, The Garki Project). In 1981, the largest-ever MDA program produced essentially the same outcome. After a single round of chloroquine plus primaquine was given to roughly eight million people in Nicaragua, there was an immediate, marked decrease in clinical P. vivax malaria, but transmission continued and the incidence of malaria soon returned to its previous level (Garfield and Vermund, 1983).

In most MDAs, tablets have been given, sometimes under supervision. Although this ensures effective dosing, it is onerous. As an alternative to tablets, Pinotti devised the concept of drug delivery using medicated salt (Pinotti, 1954). During the 1950s, a number of trials of medicated salt were conducted in malaria-endemic areas (Payne, 1988); they generally led to a reduced incidence of clinical episodes of malaria at the cost of rapid emergence of antimalarial resistance (Meuwissen, 1964; Giglioli et al., 1967). It is now known that exposing malaria parasites to suboptimal doses of antimalarial drugs over time is an ideal way to induce resistance. Thus, medicated salt has no place in malaria control today.

One MDA program that incorporated other control interventions was recently reported from the island of Aneityum, Vanuatu. In this case, the effort was successful. Eight rounds of MDA with chloroquine-SP-primaquine combined with ITNs and environmental control measures eliminated falciparum infection from the island (Kaneko et al., 2000).

Chemoprophylaxis

Antimalarial chemoprophylaxis is often used by short-term, nonimmune visitors to high-risk areas. Its direct benefits to individuals are obvious, while its indirect benefits include expanded international tourism, business travel, and economic development of malarious regions. However, the use of antimalarial drugs to protect the resident population of malaria-endemic areas has always been more controversial (Greenwood, 2004). The following two sections summarize past data and current trends regarding the use of drugs to protect high-risk individuals within P. falciparum endemic areas from acute infection.

Chemoprophylaxis in Children

In 1956, McGregor and others reported the results of a trial in The Gambia in which children received chloroquine weekly from birth until

age 2. Children who received chemoprophylaxis had fewer episodes of malaria, grew better, and had higher mean hemoglobin values than children in the control group (McGregor et al., 1956). These findings were later reproduced in studies in several other African countries (Prinsen Geerligs et al., 2003).

In the 1980s, a 5-year trial using weekly Maloprim (pyrimethamine plus dapsone) during the rainy season in children under 5 was conducted in The Gambia (Greenwood et al., 1988). Overall mortality was approximately 35 percent lower in children on prophylaxis. Protected children also had fewer clinical attacks of malaria, and a higher mean packed cell volume than control children. These results were sustained over several years (Allen et al., 1990), and are at least as impressive as results obtained with ITNs. A more recent study in Tanzanian infants using Maloprim also showed a marked reduction in clinical attacks of malaria, and the incidence of severe anemia (Menendez et al., 1997).

Chemoprophylaxis in Pregnant Women

Antimalarial chemoprophylaxis in pregnant women was first studied in a Nigerian mission hospital in 1964 (Morley et al., 1964). Chemoprophylaxis with pyrimethamine substantially increased birth weight overall, but particularly in infants born to primigravidae (women pregnant for the first time). Later studies in other African countries confirmed chemoprophylaxis’s positive effects on birth weight (Garner and Gulmezoglu, 2000), and maternal hemoglobin levels (Greenwood et al., 1989), particularly during first and second pregnancies (Greenwood, 2004). Drugs used for chemoprophylaxis in pregnancy include chloroquine, pyrimethamine, proguanil, Maloprim, and mefloquine. Although rarely implemented on any scale until recently, WHO recommended that all pregnant women in areas of moderate or high malaria transmission receive weekly chemoprophylaxis with chloroquine during their second and third trimesters. Because of drug resistance, this policy no longer offers much benefit.

Obstacles to Targeted Chemoprophylaxis

Despite impressive results in clinical trials, targeted chemoprophylaxis has never been recommended for children residing in malaria-endemic countries, and it has rarely been implemented in pregnant women. Concerns over cost, sustainability, and safety have all contributed to its poor uptake (Greenwood, 2004). In addition, some experts are concerned that young children routinely administered chemoprophylaxis may fail to develop natural immunity. In The Gambia, children who received chemoprophylaxis for 4-5 years did experience a statistically significant increase in clinical attacks

of malaria in the year after prophylaxis ended; however overall protection from death extended to age 10 following antimalarial prophylaxis during early years of life (Greenwood et al., 1995).

A final theoretical objection to chemoprophylaxis for high-risk individuals in malaria-endemic regions is its possible induction of drug resistance. Although medicated salt and the unrestricted use of chloroquine and pyrimethamine in the 1960s contributed to the initial emergence and spread of drug resistance (Payne, 1988), there is little evidence to suggest that targeted chemoprophylaxis produces the same effect to any meaningful degree. Chemoprophylaxis will inevitably lead to an increase in drug pressure, but this may be an acceptable price to pay if benefits are large. The minimal risk of drug resistance also is likely to be mitigated by the future use of combination therapy.

Intermittent Preventive Treatment

Intermittent preventive treatment (IPT) is a full therapeutic course of antimalarial treatment administered at specified times whether or not a recipient is infected. Unlike chemoprophylaxis (which aims to sustain blood levels above the mean inhibitory concentration for a prolonged period), IPT yields shorter bursts of protective drug levels separated by periods when drug levels are too low to inhibit parasite growth. In general, there are still many unknowns regarding IPT’s mechanisms of action. In the case of SP (the drug most widely used for IPT in children and pregnant women), for example, it is still not clear if IPT works primarily by eliminating existing parasites, or through a long-acting prophylactic effect of the drug (Greenwood, 2004).

IPT in Pregnant Women (IPTp)

In Malawi, Schultz and others found that a full course of SP given twice during pregnancy protected against low birth weight to a significantly greater degree than weekly chloroquine chemoprophylaxis (Schultz et al., 1994). In Kenya, a controlled trial with IPTp with SP given two or three times during pregnancy also reduced severe anemia in women pregnant for the first or second time (Shulman et al., 1999). In another area of Kenya, however, HIV-infected women required more than two or three doses of IPTp to prevent placental infection (Parise et al., 1998). Since all trials were conducted when P. falciparum was more sensitive than it is now, it is unlikely that IPT using SP would achieve the same effects today.

WHO now recommends that IPTp with SP be given at each antenatal clinic attendance after quickening (usually between the 16th and 18th week of pregnancy), replacing chemoprophylaxis as the preferred method for the

prevention of malaria in pregnancy (WHO/UNICEF, 2003). Benefits in HIV-infected women are unclear, however, as is the efficacy of IPTp in areas where malaria transmission is highly seasonal or endemicity is low (SP resistance is particularly widespread in low transmission areas). In addition, it is not yet clear what drug or combination of drugs will eventually replace SP for intermittent preventive treatment in pregnancy.

IPT in Infants (IPTi)

The IPT concept has recently been applied to the prevention of malaria in infants. In Tanzania, administration of a full dose of SP to infants concurrent with the second and third doses of diphtheria-pertussistetanus, and measles vaccines reduced the incidence of clinical malaria attacks and severe anemia during the first year of life by 59 and 50 percent, respectively (Schellenberg et al., 2001). Amodiaquine given in full therapeutic dose three times during the first year of life yielded similar results (Massaga et al., 2003). Also important, no rebound in malaria attacks or anemia occurred during the second year of life in children who received IPTi as infants. Trials of IPTi using SP are nearing completion in Ghana and Kenya, and further trials have recently started in Mozambique, Gabon, and Kenya. These trials will help to determine under what conditions IPTi will prove most effective, as well as the EIR threshold below which it will not be useful.

IPT in Children (IPTc)

In many areas of Africa, perhaps covering as much as 50 percent of the population at risk, the major burden of malaria is not in infants but in older children. This is especially true in countries of the Sahel and sub-Sahel where malaria transmission is intense but seasonal. A pilot study in Senegal employing SP plus artesunate at 1-month intervals throughout the transmission season is currently exploring whether the IPT principle also can be applied to older children (Greenwood, 2004).

DIAGNOSTIC METHODS

The correct and timely diagnosis of malaria is critically important to the individual patient in whom the disease may quickly progress to a life-threatening stage. Rapid diagnosis, both on an individual and a population level, also is an important tool in overall malaria control. This section reviews currently available methods of diagnosis, with emphasis on newer rapid tests that require relatively little technical expertise to perform. Such tests are now facilitating the delivery of effective treatment in a variety of

low-transmission settings, and will eventually find their place in malaria case management in high-transmission settings as well.

Clinical (Presumptive) Diagnosis

Although studies reveal that health providers cannot reliably identify malaria by clinical signs and symptoms alone (Weber et al., 1997; Perkins et al., 1997; Chandramohan et al., 2002), the use of clinical diagnosis is common in endemic areas. Ease, speed, and low cost are the advantages of presumptive diagnosis; disadvantages include overdiagnosis—which contributes in turn to wasted drugs, adverse drug effects, and accelerating drug resistance—as well as underdiagnosis of malaria. Since other common diseases—acute lower respiratory tract infection in children, in particular—may mimic the signs and symptoms of malaria, clinical diagnosis also can result in missed diagnoses of other treatable conditions (Redd et al., 1992; Rey et al., 1996). In fact, the difficulty of differentiating malaria from pneumonia was one of the major factors that led to the establishment of Integrated Management of Childhood Illnesses (IMCI)—an algorithmic approach to the treatment of sick children now used in many developing countries (Personal communication, B. Greenwood, London School of Hygiene and Tropical Medicine, March 2004). Whatever the theoretical pros and cons of presumptive diagnosis, however, it often is all that is available.

Light Microscopy

The current gold standard for the routine laboratory diagnosis of malaria and monitoring of cure is the microscopic examination of thin and thick blood films stained with Giemsa’s, Wright’s, or Field’s stain (Warhurst and Williams, 1996). In the thick film technique, a “thick” layer of blood, containing several layers of red blood cells (RBCs), is concentrated on a small area of a microscope slide. The red and white cell membranes are lysed, and the intracellular remnants examined for the presence of plasmodial forms. The thin film technique produces a monolayer of RBCs, facilitating species identification, and serial counting of parasites. Thin films are particularly helpful in severe malaria, both as a fast diagnostic test (White and Silamut, 1989), and a prognostic tool (Silamut and White, 1993; Phu and Day, 1995).

Although experienced microscopists may detect as few as 10-50 parasites/uL, and identify the species of 98 percent of parasites seen (Moody, 2002), in actuality, obtaining such results requires a high level of skill and time, as well as optimal maintenance of equipment and reagents. Such conditions almost never exist on the periphery of health care in Africa, and other poor, malaria-endemic locales worldwide.

In one African trial, malaria diagnosis by light microscopy was shown to reduce drug use (Jonkman et al., 1995). However, the current reality in many endemic settings is that clinicians question the reliability of light microscopy results, or frankly disregard them (Barat et al., 1999). Mixed infections (involving more than one plasmodial species) also are routinely underreported by light microscopy (Personal communication, N. White, Mahidol University, March 2004).

Fluorescent Microscopy

The quantitative buffy coat test (QBC, Becton Dickinson) is a modification of light microscopy which exploits the affinity of parasite nucleic acid for acridine orange, a fluorescent dye. This test was adapted for malaria diagnosis using patented microhematocrit tubes pre-coated with acridine orange and fitted with a plastic float that spreads the buffy coat (the white blood cell and parasite fraction of blood) against the edge of the tube. When centrifuged, malaria parasites and leukocytes take up dye and collect at a predictable location within the tube where they can then be seen under ultraviolet light.

In field trials, QBC was slightly more sensitive than conventional light microscopy (Rickman et al., 1989; Tharavanij, 1990). Disadvantages of QBC are its need for electricity, special equipment, and supplies; its increased cost relative to light microscopy; and its inability to differentiate P. falciparum from other human malaria species.

Rapid Diagnostic Tests (RDTs)

A third diagnostic approach involves “dipstick” tests, which eliminate the need for a microscope and detect parasite antigens in blood by rapid immunochromatography using various antibodies. More than 20 such tests are currently marketed, and several are made in malaria-endemic countries. The majority are based on histidine-rich protein 2 (HRP-2) found in P. falciparum. Compared with light microscopy and QBC, HRP-2 tests yield a rapid and highly sensitive diagnosis of falciparum infection (WHO, 1996b; Craig and Sharp, 1997). The main drawbacks of HRP-2 tests are their high per-test cost (lowest price circa 50 U.S. cents) and inability to quantify the intensity of infection. In addition, HRP-2 antigen may persist for days or weeks following successful treatment. As a result, HRP-2 tests do not distinguish cured from nonresolving (i.e., drug-resistant) infections (WHO, 1996b). Several tests using HRP-2 to detect P. falciparum also include a second antigen to distinguish P. falciparum from other malaria species, although sensitivity generally is lower for P. vivax, and other non-P. falciparum species (Murray et al., 2003).

The OptiMAL dipstick detects the parasite enzyme lactate dehydrogenase (pLDH), which is actively produced by all malaria parasites during growth in human red cells (Piper et al., 1999). Unlike HRP-2, pLDH disappears from the bloodstream along with malaria parasites following successful treatment. OptiMAL also distinguishes P. falciparum from the other malaria species without differing levels of sensitivity for other species of malaria. In general, performance of OptiMAL in field studies has been high, but sensitivity in some recent trials has been erratic, perhaps due to batch problems or poor test handling (Murray et al., 2003). Quality control procedures for all rapid test types need improvement.

Field Application of Rapid Diagnostic Tests

In selected tropical countries and resource-poor settings where microscopy is either unavailable or unreliable, RDTs have great potential to reduce inappropriate antimalarial chemotherapy. For one thing, it is much easier to train someone to perform an RDT reliably than to be a reliable microscopist. RDTs have been used successfully in remote tribal groups in forested areas of central India (Singh et al., 2000), in refugee camps on the Thai-Burma border (Bualombai et al., 2003), and in rural health centers in Cambodia (Rimon et al., 2003). However, none of these areas approach the transmission levels of certain highly endemic areas of sub-Saharan Africa.

The utility of antigen detection in areas of Africa hyperendemic for malaria is less clear, because the tests are not quantitative, and the mere finding of parasites may be insufficient grounds for a diagnosis of malaria. One study in Zimbabwe indicated that mistreatment was reduced by up to 81 percent when ParaSight-F was used compared to presumptive diagnosis (Mharakurwa et al., 1997). However, the improvement in diagnostic accuracy was most marked in the hypodendemic part of the study region.

In summary, when to introduce RDTs into areas of sub-Saharan Africa hyperendemic for falciparum malaria remains an open question. One perspective on the use of RDTs comes from Asia, where providing the means to diagnose and treat malaria on the village level has coincided with a dramatic fall in morbidity and mortality. The fact that drug pressure is a major contributor to transmission of resistant parasites is another reason why universal treatment without RDTs should not be permitted indefinitely anywhere in the world. However, in high prevalence areas of sub-Saharan Africa, universal treatment of clinically suspected cases with ACTs is the safest near-term strategy, given the desperate need for rapid, in- or near-home treatment in order to save lives. Eventually, combining RDTs and ACTs in areas of Africa of low and medium malaria prevalence could

reduce the number of illnesses misdiagnosed as malaria and yield major savings in terms of drug cost and delayed onset of drug resistance. In the meantime, following the introduction of ACTs in Africa, pilot programs and operational research combining ACTs and RDTs in a variety of epidemiologic settings and at-risk populations should be encouraged.

Molecular Methods

When malaria patients are parasitemic, their blood also contains malaria DNA and RNA. Applying a DNA probe to a filter paper with a small spot of human blood can identify malaria genetic material, including mutations or gene amplifications conferring drug resistance (Plowe and Wellems, 1995). Today, such methods are increasingly being used to detect molecular markers of drug resistance to chloroquine and SP. As long as the filter papers are properly handled, DNA can be recovered from them months after obtaining the samples (Farnert et al., 1999).

DNA and RNA techniques for rapid malaria diagnosis are currently impractical in most endemic regions, but their role may expand in selected populations as the tests become simpler and cheaper. Sensitive PCR techniques can detect parasites at a density as low as 1 per microliter, in contrast to 10-50 parasites per microliter with expert light microscopy (Greenwood, 2002).

MALARIA VACCINES

No malaria vaccine has yet entered routine use, and a safe and effective vaccine is at least another 10 years away (Greenwood and Alonso, 2002). This fact alone supports the central argument of this report, namely that a subsidy for effective treatment is an urgent priority that cannot wait until another control measure such as a vaccine is implemented. Nonetheless, the last 2 decades have seen significant progress in malaria vaccine research (Greenwood and Alonso, 2002). Highlights are summarized below.

The malaria vaccine era launched in the 1970s when, building on earlier work in rodent models, investigators at the University of Maryland demonstrated that irradiated sporozoites of P. falciparum and P. vivax protected naïve volunteers against challenge by infective mosquitoes (Clyde, 1975). For the next 2 decades, advances came mainly in experimental models rather than in human trials (Kwiatkowski and Marsh, 1997). In 1990, the first report of a vaccine field trial in an endemic area was published: a study of pre-erythrocytic vaccine in Burkina Faso (Guiguemde et al., 1990). A recent meta-analysis of malaria vaccine trials documented 18 trials with 10,971 participants using pre-erythrocytic and blood-stage vaccines (Graves and Gelband, 2003). Table 8-2 lists vaccines in field trials as

TABLE 8-2 Candidate Malaria Vaccines in Clinical Trials

|

Group (field collaboration) |

Vaccines (type) |

Target |

|

Apovia, USA; New York University, USA |

ICC-1132 (protein) |

Pre-erythrocytic |

|

GlazoSmithKline Biologicals, Belgium; and WRAIR, USA (Medical Research Council [MRC] Laboratories, The Gambia; Centro de investigacao em Suade de Manhica [CISM], Mozambique) |

RTS,S (protein) |

Pre-erythrocytic |

|

Malaria Vaccine Development Unit, National Institutes of Health, USA |

Pvs25, AMA-1 (protein) |

Transmission blocking, blood stage |

|

Naval Medical Research Center (NMRC), USA; Vical USA |

Pf-CS, Pf-SSP2/TRAP, Pf-LSA-1, Pf-EXP-1, Pf-LSA-3 (DNA vaccines) |

Pre-erythrocytic |

|

New York University, USA |

CS (synthetic polymers, MAPs, polyoximes) |

Pre-erythrocytic |

|

Oxford University, UK (MRC Laboratories, The Gambia; Wellcome-Kenya Medical MVA Research Institute [KEMRI] collaboration, Kilifi, Kenya) |

DNA ME-TRAP, ME-TRAP, FP9 ME-TRAP, MVA-CS (DNA and recombinant viral) |

Pre-erythrocytic |

|

Statens Serum Institut (SSI), Copenhagen; Institut Pasteur; Institute of Lausanne, Switzerland |

GLURP, MSP-3 (synthetic peptide) |

Pre-erythrocytic, blood stage |

|

Walter and Eliza Hall Institute of Medical Research, Melbourne; Queensland Institute of Medical Research (QIMR), Brisbane; Swiss Tropical Institute; Biotech Australia Pty (Papua New Guinea Institute of Medical Research) |

MSP-1, MSP-2, RESA (protein) |

Blood stage |

|

Walter Reed Army Institute of Research (WRAIR), USA (KEMRI, Kisumu, Kenya) |

FMP-1 (protein) |

Blood stage |

|

EXP = exported protein. LSA = liver stage antigen. MAP = multiple antigen peptide. Pvs = Plasmodium vivax surface protein. AMA-1 = apical membrane antigen-1. RESA = ring infected erythrocyte surface antigen. SSP2 and TRAP are synonyms: sporozoite surface protein 2 and thrombospondin-related adhesion protein. Only vaccines being tested in clinical trials as of May 2003 are listed. Field collaborations are listed only if field trials of the candidate had begun as of May 2003. SOURCE: Moorthy et al. (2004). |

||

of May 2003 (Moorthy et al., 2004). Additional single and combination antigens are currently in various stages of pre-clinical assessment.

A comprehensive discussion of all malaria vaccines is beyond the scope of this report; however, certain basic concepts and prototype vaccines are covered below. For further details of specific vaccine antigens and strategies, readers are directed to several excellent published reviews (Moore et al., 2002; Carvalho et al., 2002; Mahanty et al., 2003; Moorthy et al., 2004).

Natural Immunity to Malaria

In malaria-endemic areas, natural human infection with P. falciparum induces some degree of immunity which first protects against severe, then mild malaria (McGregor, 1974). Maintaining functional immunity requires repeated infective mosquito bites, however (Cohen et al., 1961; Marsh and Howard, 1986). Of the 5,300 antigens encoded by P. falciparum, possibly 20 trigger key protective immune responses of both major types—antibody, and T-cell dependent—that follow natural exposure (Moorthy et al., 2004).

Vaccine Strategies Based on Parasite Life Cycle Stages

Unlike natural infection, experimental vaccines have traditionally targeted one of malaria’s three biologic stages in its human or mosquito host: sporozoite, merozoite, or gametocyte. The goal of pre-erythrocytic (or sporozoite) vaccines is to block the initial entry of sporozoites into human liver cells. A current candidate of this class is RTS,S—a recombinant protein vaccine which pairs hepatitis B surface antigen DNA with DNA encoding a large portion of P. falciparum circumsporozoite protein. In a randomized controlled trial of three-dose RTS,S in Gambian adults, vaccine efficacy was 34 percent over a 15-week surveillance period (falling from 71 percent efficacy in the first 9 weeks to 0 percent in the next 6 weeks) (Church et al., 1997). Although short-lived, this vaccine-induced defense constituted the first protection against natural P. falciparum infection by a pre-erythrocytic vaccine. Phase I trials of RTS,S in children aged 1-11 years in The Gambia and Mozambique have now been completed, and a trial in children 1-4 years in Mozambique is currently under way. However, it is likely to be 10 years at least before RTS,S finds a place in routine immunization programs, even if the current pediatric trials are successful (Personal communication, B. Greenwood, London School of Hygiene and Tropical Medicine, March 2004).

In contrast to the all-or-none protective action of pre-erythrocytic vaccines, merozoite (or blood stage) vaccines have two potential effects: limiting RBC invasion, and reducing disease complications. Merozoite surface

protein-1 (MSP-1) is the best characterized antigen mediating RBC invasion; it forms the basis of several candidate vaccines. Although some data suggest that vaccine-induced antibodies to MSP-1 may block natural malaria-protective antibodies (Holder et al., 1999), an anti-invasion vaccine based on MSP-1 has now moved to an adult phase I study in western Kenya.

Intravascular attachment of schizonts to endothelial cells in the brain, kidneys, and placenta is the most serious consequence of falciparum malaria. PfEMP-1 antigen is the main ligand for this sequestration event. Unfortunately, this antigen’s high degree of variability, rapid rate of antigenic variation, and high copy number within individual parasites complicates vaccine development. Some investigators remain hopeful that conserved regions of PfEMP-1 may yield protective responses in humans (Moorthy et al., 2004).

Sexual-stage vaccines, rather than protecting vaccinated individuals, are meant to reduce malaria transmission, especially in combination with other control methods. Their principle is as follows. Anti-gametocyte antibodies induced in vaccinated humans enter female anophelines via blood meals. These antibodies interfere with parasite development in the vector’s midgut, preventing further transmission. One major drawback to sexual stage vaccine candidates is their lack of commercial appeal to major pharmaceutical companies. Unlike sporozoite vaccines in particular (which could find a sizable market in tourists, migrants, and military personnel entering malarious zones) (Hoffman, 2003), sexual-stage vaccines are unlikely to be marketed outside malaria-endemic countries. An NIH-sponsored clinical trial of a recombinant protein (Pfs25) P. falciparum gametocyte vaccine is currently in development.

What Is Really Needed from a Malaria Vaccine?

Modern malaria vaccine development has followed a somewhat chance course thus far, guided by discoveries of particular antigens or enthusiasms of individual investigators (Greenwood and Alonso, 2002). However, as resources increase and more potential vaccine antigens are identified, defining the primary characteristics needed in a malaria vaccine becomes essential.

A perfect malaria vaccine would induce lifelong sterilizing immunity, provide cross-species protection, protect the very young, and be compatible with routine EPI (Expanded Programme on Immunization) vaccines. Since none of these goals will be achieved quickly, vaccine researchers are faced with a choice: either to work on a safe, highly efficacious and commercially viable vaccine (such as a pre-erythrocytic vaccine) for the short-term traveler or to work on a vaccine that offers more long-lasting protection, aug-

menting (as opposed to replacing) natural immunity in residents of malaria-endemic areas. For example, among semi-immune recipients, a blood-stage vaccine that lowered parasite density might prove beneficial even if it had little effect on the incidence of infection. Similarly, a partially effective preerythrocytic vaccine might protect against death from malaria just as ITNs do. Whether or not an imperfect malaria vaccine justifies use in a particular setting will depend upon its efficacy relative to other available control tools, its acceptability, and its cost.

Pregnant women in malaria-endemic areas, especially primigravidae, have a special need for enhanced malaria protection because of malaria’s damaging effects in pregnancy. In some areas, it is becoming difficult to provide this protection through any other means (e.g., chemoprophylaxis, or intermittent treatment). A vaccine that prevented sequestration of P. falciparum parasites in the placenta might lessen the chance of a pregnant woman giving birth to a low-birth weight baby, but would not protect her from anemia.

Single versus Combination Candidates

For various reasons, including malaria’s antigenic variation and protein polymorphisms, it is unlikely that any single malaria antigen will be found that meets all of the criteria for a perfect vaccine. Thus, the most effective malaria vaccines are likely to contain a “cocktail” of antigens from the same stage of the parasite’s life cycle, or different antigens from different stages. The most extensively tested combination vaccine thus far is SPf 66, which includes several erythrocytic-stage antigens originally found protective in Colombia (Pattarroyo and Armador, 1999). However, trials using SPf66 in holoendemic areas of Africa showed marginal, if any, protection (Alonso et al., 1994; D’Alessandro et al., 1995), nor did the vaccine confer protection upon Tanzanian infants when administered as part of their initial EPI vaccine package (Acosta et al., 1999). The vaccine also failed to protect Karen children in a malarious region of northwestern Thailand (Nosten et al., 1996).

The first multistage, multiantigen P. falciparum vaccine candidate was NYVAC-Pf7, an attenuated vaccinia virus genetically engineered to include seven P. falciparum genes encoding the pre-erythrocytic antigens CSP and LSA1; the asexual blood stage antigens MSP1, AMA1 and SERA; and the transmission-blocking antigen PFs25 (Tine et al., 1996). Initial studies did not demonstrate protection against P. falciparum in human volunteers, although detectable immune responses were elicited (Ockenhouse et al., 1998). MuStDO (Multi-Stage Malaria DNA Vaccine Operation) is an ongoing collaboration involving several scientific institutions worldwide, including the Naval Medical Research Center (NMRC), the U.S. Agency for

International Development (USAID), the Noguchi Memorial Institute of Medical Research in Accra, Ghana, and the Navrongo Health Research Centre in Navrongo, Ghana. Experimental development of the MuStDO vaccine is currently focused on 15 P. falciparum antigens (5 pre-erythrocytic and 10 erythrocytic proteins) (Kumar et al., 2002), although future versions also may incorporate transmission-blocking antigens.

Practical Realities of Vaccine Testing and Use

Selecting which malaria antigens should enter clinical trials was not a major problem when there were relatively few candidates to choose from. However, characterization of the P. falciparum genome has now identified hundreds of parasite proteins that could potentially be tested as individual vaccine components. Selecting future vaccine components should rest upon: 1) evidence that the antigen plays an important role in the survival or pathogenicity of the parasite; 2) evidence from animal experiments that the antigen induces protective immunity in vivo; and 3) evidence that immune responses to the antigen are associated with protection (Greenwood and Alonso, 2002). If a vaccine candidate passes Phase I and Phase II testing, further considerations in designing phase III trials include study site, study population, study size, and appropriate clinical end points (Table 8-3). Another important factor that will influence whether a partially effective malaria vaccine is introduced into routine use will be its cost effectiveness relative to other malaria control measures, such as ITNs (Graves, 1998; Goodman et al., 1999).

TABLE 8-3 Possible End Points for Phase-III Malaria Vaccine Trials

|

End Point |

Advantages |

Disadvantages |

|

Death |

Most important public health end point |

Requires large trial |

|

Malaria mortality rate |

|

Difficult to measure |

|

Severe clinical malaria |

Important end point |

Requires high hospital admission rate |

|

Mild, clinical malaria |