6

Finance Reform Proposals

Reforms Within the Present Framework

Chapters 2 and 4 examined two potential threats to the viability of present transportation program finance arrangements: decline of the tax base because of motor vehicle fuel economy improvements and erosion of the principles and practices, in particular user fee finance, that have been associated with the finance system’s stability and success. Those chapters concluded that the present system shows signs of stress, and while it is not in immediate jeopardy of failing, improvements in pricing and financing practices probably will be necessary to slow or reverse deterioration of transportation system performance. In Chapter 5, examination of the prospects for tolls and mileage charges, alternative funding sources to replace or supplement the fuel tax, indicated that comprehensive implementation of satisfactory alternative road user charging mechanisms is still some years in the future. Because of the potential benefits of these alternatives, delay in developing them probably would be costly. Nevertheless, it will be necessary to continue to rely on present finance arrangements for most of the next 20 years and to take every opportunity to reinforce the proven features of the system, in particular, user fee finance in the highway program.

This chapter describes several kinds of finance reform measures that do not depend on developing major new revenue sources or on fundamentally altering institutional arrangements:

-

Measures to increase available resources:

-

Reducing evasion and limiting exemptions

-

Indexing tax rates

-

Reforming use of debt finance

-

-

Measures to improve pricing:

-

Refining user fees

-

Incorporating new vehicle technologies in the user fee structure

-

-

Measures to direct spending more effectively:

-

Improving project selection and reducing project costs

-

Developing alternatives for transit finance

-

Redefining federal, state, and local government responsibilities

-

This list includes the short-term reform options in the state finance studies reviewed in Chapter 1, as well as proposals from other sources that have gained prominence. It was noted in the introduction to Chapter 5 that proposals from these sources tend to concentrate on particular aspects of the finance structure rather than on comprehensive reform. The descriptions in this chapter organize the proposals, somewhat arbitrarily, into three categories according to their main objectives: measures to increase available funds (including accelerating spending with debt financing), to improve pricing (that is, adjusting existing user fees to better match the costs of travel), and to guide spending more effectively to the best uses. In practice, many of the proposed actions could serve multiple purposes. For example, reducing tax evasion increases revenue but also is necessary for fairness and public acceptance and to maintain the integrity of the fee structure.

The subsections below describe the intent of each proposal and review available information about the possible consequences of implementing it, in order to identify those that appear to be practical and beneficial. Inclusion of a proposal in this list is not intended as an endorsement. Committee recommendations with regard to some of the proposals are presented in Chapter 7.

MEASURES TO INCREASE AVAILABLE RESOURCES

Reducing Evasion and Limiting Exemptions

Tax administrators have long recognized that a substantial amount of motor fuel excise tax revenue is lost to tax evasion. In a survey (Denison et al. 2000), state tax administrators reported their estimates that 5 percent of state gasoline tax revenues and 10 percent of diesel revenues are lost to evasion. Common evasion techniques reported were bootlegging fuel across state lines to take advantage of rate differences, taking advantage of the lower federal tax rate on gasohol by falsely labeling gasoline or a blend with less than 10 percent ethanol as gasohol, counterfeiting documentation of tax payments, and abusing tax exemptions (for example, exemptions for off-road and agricultural use). Diversion of aviation fuel (which pays a lower federal excise tax rate than diesel fuel for motor vehicle use) for use in diesel trucks is also recognized as an important evasion method. It reduces federal revenue by $900 million per year according to one estimate (Peters 2002).

Enforcement efforts in some states and by the federal government have had success in reducing fuel tax evasion. Methods include more intensive auditing, improvements in record keeping, and intergovernmental cooperation. Moving the point of tax collection upstream in the distribution chain also has been shown to reduce evasion (Peters 2002).

The 2005 federal surface transportation program reauthorization legislation [Safe, Accountable, Flexible, Efficient Transportation Equity Act: A Legacy for Users (SAFETEA-LU), Section 1115] increases funding for enforcement of federal excise tax collections and requires upgrades in government records systems and other measures. The legislation includes a provision (Section 1161) intended to stop diversion of aviation fuel by requiring tax payment at the highway motor fuel rate for certain purchases of aviation fuel and requiring purchasers to apply for a refund with documentation that the fuel was used for aviation. Congressional estimates predicted $4 billion in additional revenue over 6 years as a result of the new enforcement provisions (Fischer 2004, 11).

Tax exemptions are a related drain on revenue. Federal and state fuel tax laws contain numerous provisions exempting classes of uses from liability for the fuel tax. Common exemptions are for government-owned vehicles and school buses. The special provisions of the federal excise tax on gasohol amounted to a partial exemption. (After changes in the law in 2004, the Federal Highway Trust Fund no longer loses revenue from these provisions.) Other loopholes include evaporation allowances for fleet purchasers. States commonly exempt fuel purchased for agricultural uses from taxation. To the extent that this fuel is actually used off public roads, this is not a violation of the user fee principle.

Certainly exemptions can serve legitimate functions. However, as the survey of tax administrators revealed, abuse of exemptions is a common form of tax evasion. A version of the 2005 federal surface transportation program reauthorization legislation before enactment contained a provision tightening requirements for documenting entitlement to exemptions. The provision was credited with significant revenue-generating potential (Fischer 2004, 12); however, it was not fully enacted.

Indexing Tax Rates

As Chapter 1 described, one of the most serious of transportation program administrators’ complaints about present revenue provisions is that revenues are vulnerable to erosion by inflation because legislatures are slow to revise rates to maintain buying power. A few states have provisions allowing for administrative adjustment of fuel tax rates (see Chapter 2), but the rates in the majority of states and the federal tax rates can be changed only by legislation. Consequently, although revenues from cents-per-gallon fuel taxes and dollars-per-vehicle registration fees rise with increasing highway use, they decline with inflation until the legislature acts. It was

also shown in Chapter 2 that, although rate adjustments have been sufficient to maintain a fairly constant inflation-adjusted average user fee rate of $0.03 to $0.035 per mile, the timing of adjustments has been erratic and has lagged inflation. (See Table 2-3 and Figure 2-1 in Chapter 2.) This situation has complicated the administration of highway programs.

States have experimented with two mechanisms for removing this source of uncertainty and stabilizing revenues: replacing the cents-per-gallon fuel tax with an ad valorem tax (i.e., a tax that is a fixed percentage of the sale price) and indexing the cents-per-gallon rate. Under the second mechanism, periodic administrative adjustments are made to the rate proportional to the change in a specified measure of inflation, for example, the Consumer Price Index (CPI) or the highway construction cost and operating and maintenance cost indices compiled by the Federal Highway Administration (FHWA).

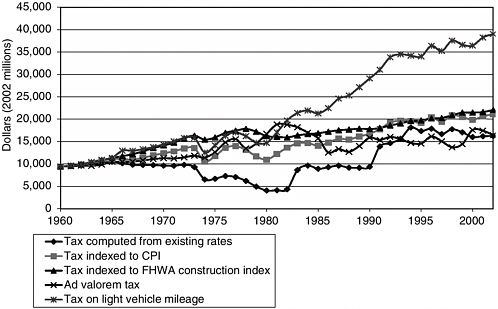

The greatest financial disruption experienced by transportation programs in recent decades was from about 1974 to 1982. During this period, high inflation, slow growth in travel, and the impact of the corporate average fuel economy standards in federal law combined to cause constant-dollar fuel tax revenue to decline by more than 50 percent (Table 2-3 and Figure 6-1). Several states reacted by enacting variable-rate fuel taxes. A review of this experience (Ang-Olson et al. 2000) found that the consequences were not satisfactory in several states. States that enacted ad valorem taxes in the 1970s saw revenues plunge along with fuel prices in the early 1980s, and states enacting such taxes in the 1980s, anticipating

FIGURE 6-1 Federal gasoline tax revenues under various indexing methods.

a steady rise in rates, were surprised by the overall level price trend over the subsequent 15 years. Michigan tried an indexing formula in which the fuel tax rate was proportional to a highway maintenance construction cost index and inversely proportional to state fuel consumption. After the formula produced a 36 percent rate increase from 1982 to 1984, it lost political support and was allowed to expire. About 15 states tried indexing according to a variety of formulas in the 1980s, but most such taxes were rescinded because of public reaction and unpredictable revenue results. The review concluded that indexing to the CPI had proved to be the best way to keep revenue in pace with inflation and that limiting annual changes, by indexing an increment of the gas tax rather than the entire tax or by capping the annual change in the rate, would increase public acceptance.

Figure 6-1 shows annual constant-dollar revenue of the federal excise tax on gasoline since 1960 and estimates of annual revenues if the tax had been indexed to the CPI or the FHWA highway construction cost index in 1960. In the figure, revenues under the actual tax are computed as gallons of gasoline sold each year multiplied by the constant-dollar federal excise tax rate in the year, for comparability with the other curves in the graph. Also shown are revenues from an ad valorem tax on gasoline and from a light-duty vehicle mileage tax (at a cents-per-mile rate that rises proportionally to the CPI). Both start at rates in 1960 that would have yielded the same revenue as the actual tax. The revenue estimates take into account the probable effect of the change in the tax rate on gasoline consumption in each year.

The purpose of the estimates is not to show which tax rate scheme would have raised the most revenue. The differences among the various schemes in the absolute level of revenue in each year are not meaningful, because Congress would be expected to adjust the rate from time to time to yield revenue commensurate with its transportation spending plans. Rather than increasing total revenue, the intent of the variable tax rate would be to smooth out irregularities such as the decline in constant-dollar revenue from 1973 to 1980. Among the two tax indexing methods and the ad valorem tax, the CPI-indexed tax appears to be the most stable over the entire period. The construction cost–indexed tax rose rapidly until 1980 and more slowly than the CPI-indexed tax since then, but it also appears stable within those periods.

For Congress or a state legislature, the goal of authorizing indexing would be to ensure that the revenues it intended to raise were actually available, regardless of inflation. However, the legislature might oppose indexing if it believed that the practice would lessen its control over transportation programs because the state transportation department would be less dependent on the legislature’s enactment of rate adjustments. The legislature might also be concerned about the public reaction to automatic tax increases. If indexing had the effect of insulating transportation programs from regular legislative review, the long-term consequence could be reduced political and public understanding of and support for these programs.

Reforming Use of Debt Finance

As Chapter 2 described, debt finance is little used in state highway programs (other than by toll authorities), and no trend toward greater use of debt is evident. In part, this aspect of financing practice reflects the structure of the federal-aid program, which has been the major funding source for most large highway capital projects over the past 50 years. Congress designed a pay-as-you-go program. It enacts multi-year authorizations to allow the states to plan, but the rate of disbursement of federal grants is governed by the rate of federal user fee collections (because the balance in the Highway Trust Fund is usually kept to less than 1 year’s spending). On the basis of formulas, states receive annual apportionments, which must be used within a fixed period.

Debt financing allows state and local governments to complete a project earlier rather than postponing the project’s benefits while waiting to accumulate funds or building it in increments. Borrowing also shifts some of the project’s costs from present to future taxpayers or toll payers. Changes in the federal-aid program in the past decade have been aimed at facilitating borrowing. States may issue debt backed by anticipated federal grants [known as GARVEEs (Grant Anticipation Revenue Vehicles)], and federal law provides for the creation of state infrastructure banks (SIBs), revolving funds capitalized partially with federal grants that states and local governments can borrow from for highway construction. The programs are small compared with total capital spending: from their inception through mid-2004, 32 SIBs had issued loans totaling $5 billion, and 10 states had issued $5 billion in GARVEE bonds (USDOT 2004, 22–26; CBO 1998, x–xii).

A set of proposals for creating additional opportunities for use of debt finance was published in 2003 by the American Association of State Highway and Transportation Officials (AASHTO) (although not adopted as a policy of that organization) for consideration during debate over federal surface transportation program reauthorization legislation. The proposals included expansion of the SIB program and expansion of the existing Transportation Infrastructure Finance and Innovation Act program, which provides federal credit assistance to large public-sector transportation projects funded at least in part by user charges or other dedicated revenue sources (AASHTO 2003a). As described in Chapter 5, in the 2005 federal surface transportation aid reauthorization legislation (SAFETEA-LU), Congress did expand both of these programs, and it authorized use of tax-exempt private activity bond financing of toll roads.

The most ambitious proposal in the AASHTO document was for creation of a Transportation Finance Corporation, a federally chartered, nonprofit corporation that would issue $60 billion in tax credit bonds. The proceeds would be allocated by Congress in a manner similar to that in which federal highway and transit aid funds are now distributed. Tax credit bonds are bonds on which the interest is paid in the form of credits against federal income tax liabilities (CBO 2003). In

the Transportation Finance Corporation proposal, the general fund would be reimbursed for the tax cost of the program by transfers from the Highway Trust Fund (AASHTO 2003b). The objective of the proposal, which was not enacted, was to fund an immediate large increase in the federal-aid program. Proponents presumably saw tax credit bonds as a way to allow an increase in the program without immediately raising the rates of the federal fuel tax or other fees and without overtly breaking the link between user fee revenue and spending.

Tax credit bonds for transportation finance would have a number of drawbacks. They would allow spending before Congress had authorized highway user fees to pay for it. The bond scheme might pose a threat to the user-pays principle: if Congress failed to enact fees to cover debt service, then either highway spending for other purposes would have to be curtailed or the cost of the bonds would have to be shifted to the federal general fund. Tax credit bonds in general have been criticized on the grounds that their cost to the federal government is greater than if the funds were raised through conventional treasury borrowing. Furthermore, they tend to obscure the cost of borrowing in the federal budget if the issuing entity is not regarded as part of the federal government for budget purposes (CBO 1998).

MEASURES TO IMPROVE PRICING

Refining User Fees

Refinements within the present schedule of highway user fees or modest extensions to the structure could improve the performance of the transportation finance system. The objective would be to allow highway agencies to recover some costs that current fees do not fully recover and to provide incentives for more cost-conscious use of highways.

User fees, which were described in Chapter 2, include federal and state fuel taxes; state registration, license, and permit fees; the federal excise taxes on tires and on new heavy trucks and trailers; and the federal Heavy Vehicle Use Tax. These charges are imperfect as prices for road use because they do not correspond well to costs. For example, the fuel tax paid for operating a particular vehicle varies little from mile to mile, but the costs imposed by that vehicle on other users and on the highway agency vary greatly depending on the road and traffic conditions. Also, the fuel tax paid per mile depends on the vehicle’s fuel efficiency, but costs probably vary little with vehicle size for passenger vehicles. Consequently, the fees paid for a particular trip can be much higher or lower than the actual cost of the trip to the highway agency and other road users. The fees will therefore discourage some valuable trips and fail to discourage trips that have small value to the traveler compared with their costs.

Annual vehicle registration fees have been criticized as a particularly unsatisfactory form of fee because they do not vary with miles of travel (Road User Fee

Task Force 2003, 23–24). However, registration fees do affect highway use by affecting vehicle ownership. Because of their simplicity and familiarity, registration fees can be a practical and worthwhile pricing mechanism. For example, many states charge truck registration fees graduated by weight to reflect the higher costs imposed by larger vehicles.

The special taxes paid by large trucks are the most important features in the present user fee schedule for aligning fees with the costs imposed by different users. Truck traffic is a major determinant of highway construction, maintenance, and operating costs. The characteristics of the largest trucks determine the design of pavements and roadway foundations; the strength requirements of bridges; the geometric design of grades, curves, and ramps; and maintenance costs for pavement and roadside appurtenances. The pavement wear caused by the passage of a vehicle axle increases proportionally to the third or fourth power of the load carried by the axle. Therefore, one passage of a 20,000-pound axle on a large truck will cause wear equal to several thousand passages of a 2,000-pound axle on a passenger vehicle. A large truck in congested traffic causes more delay than a car, and truck crashes on urban expressways are major causes of delay.

The federal government and the states periodically conduct highway cost allocation studies to determine their costs for providing roads for various kinds of vehicles. The studies face methodological challenges, but their results give an indication of the relative cost implications of truck and light vehicle traffic. The most recent federal study estimated that the revenue from fees paid by operators of combination trucks (a truck or tractor pulling a trailer, the principal highway freight vehicle) equals 80 percent of the highway agency expenditures attributed to this class of vehicle. However, the heaviest combination trucks were estimated to pay smaller shares of their costs than lighter combination trucks (USDOT 1997, Table VI-21). As noted in Chapter 2, combination trucks account for 5 percent of vehicle miles and pay 19 percent of all user fees.

The federal Heavy Vehicle Use Tax is intended to recover a part of the extra costs of serving large trucks. It is an annual fee of $550 on trucks with registered gross weight of 75,000 pounds or more and $100 to $550, depending on weight, on trucks of 55,000 to 75,000 pounds. The revenue from the tax is dedicated to the Highway Trust Fund. It raised $940 million in 2003, 3 percent of federal highway user fee revenue (FHWA 2004, Table FE-9). The rate schedule was last changed in 1984. The 1983 federal-aid highway act, which included a provision liberalizing federal truck size and weight limits, raised the top rate to $1,900 per year on trucks with gross weight of 80,000 pounds or more, rising in steps from $50 per year on 33,000-pound trucks. The adjustment corresponded to the findings of a U.S. Department of Transportation (USDOT) highway cost allocation study. However, the next year, following industry objections, Congress rolled back the use tax to the present rates and raised the diesel fuel tax to make up the revenue. Operators of large trucks also pay a federal excise tax on purchases of trucks,

trailers, and tires. The revenue, which is dedicated to the trust fund, was $2.1 billion in 2003, or 6 percent of federal user fee revenue. There is no federal excise tax on light vehicles.

Three possible refinements to federal and state user fee schedules merit consideration:

-

Graduating the federal Heavy Vehicle Use Tax and state annual truck registration fees to correspond more closely to relative cost responsibility as indicated in federal and state cost allocation studies. Ideally, rates would take into account axle configuration as well as gross weight, because reducing loads per axle reduces pavement and bridge costs.

-

Introducing a federal weight–distance tax. A few states charge trucks a tax that depends on weight and miles traveled. The Oregon tax produces the most revenue, $178 million in 2003 (FHWA 2004, Table MV-2). Oregon rates are from $0.04 to $0.185 per mile, depending on the truck’s registered weight and number of axles (ODOT 2004). Fuel consumed by trucks paying the weight–distance tax is exempt from the state fuel tax. Truck operators must periodically report their miles and submit payments. A 1988 USDOT study commissioned by Congress concluded that a federal weight– distance tax would be feasible to administer because large trucks must already file federal tax reports to pay the Heavy Vehicle Use Tax, and reported mileage would be auditable because operators already keep mileage records to show compliance with state tax laws (CBO 1992, 21–23). The recent European experience with mileage charging described in Chapter 5 suggests that such fees may become standard there and that technology to automate reporting and fee collection is developing rapidly.

-

Introducing a mechanism to align light-duty vehicle user fee payments more closely with costs. Larger light-duty vehicles pay higher average user fees per mile than do small vehicles because they consume more fuel, yet the cost of providing highways for these vehicles is not much greater than costs associated with the smallest vehicles. The 1997 federal cost allocation study estimated that the ratio of fees to allocated costs was 30 percent higher for pickups and vans than for cars (USDOT 1997, Table VI-21). One way to eliminate the discrepancy would be through adjustments in registration fees, although the impact of such a change would require study. The question of appropriate charges for small and large passenger vehicles is identical to the problem of deciding how future advanced-technology vehicles should be charged for road use, which is discussed below.

Any of these suggestions would encounter political obstacles. Truck operators successfully opposed the previous attempt to graduate the Heavy Vehicle Use Tax more steeply and have vigorously opposed weight–distance taxes for many years.

They have won repeals of these taxes in several states. They object that weight– distance taxes have high administrative costs and high rates of evasion, and they may believe that introduction of weight–distance taxes would be an occasion for increasing trucking’s share of highway user fee payments. Criticism could be expected that adjustment of light-vehicle taxes would constitute a tax on energy conservation, and the adjustment would reduce revenue if fees for other vehicles were not increased.

None of the measures would be expected to yield large net revenues (although the financial impact of misalignment of truck fees with costs is growing because the volume of large truck traffic is growing faster than that of other vehicles). Their main justification is that they would improve the efficiency of the transportation system: truckers would have an incentive to operate equipment that reduced road wear, and highway travel by high-mpg vehicles would not be subsidized.

An evaluation of the Oregon axle-weight-distance tax (Rufolo et al. 2000) found that since introduction of the tax, a small increase has occurred in the average number of axles per truck in each weight class, which has reduced pavement wear costs. Because of data limitations, it was not possible to show that the tax was the cause of the trend in axle configurations. Under the Oregon tax, the fee per mile decreases with increasing number of axles on the truck within each weight class. Past Transportation Research Board policy study committees have argued that more significant savings for highway agencies and shippers could be attained by coupling axle-weight-distance taxes with less restrictive truck size and weight regulations, which would give carriers flexibility to optimize their equipment and operating practices (TRB 2002, 190–191).

Road Use Charging for Advanced-Technology Vehicles

Chapter 4 described the incentives that the federal and state governments are offering to promote alternative automotive propulsion technologies and high-mpg vehicles. Ideally, incentives would be structured to avoid accidental impacts on transportation finance (such as, for example, the impact of the federal gasohol tax preference). Also, because highway user fees function to an extent as prices reflecting the cost of providing roads, exempting owners of alternative-technology vehicles from payment of the fees discourages cost-conscious travel decisions. Whether they receive special subsidies or not, operators of high-mpg vehicles will pay less in user fees per mile of travel than operators of conventional vehicles as long as cents-per-gallon fuel taxes are the main component of the fees.

An incentive that subsidizes road use by forgiving payment of highway user fees can unnecessarily increase the cost of meeting the conservation or emissions goal. For example, if high-mpg cars are allowed free use of high-occupancy/toll (HOT) lanes, all other users of the highway will pay costs in the form of extra congestion caused by the free access or higher congestion tolls needed to keep traffic

flowing. For some trips, this cost to others (which should equal the toll the vehicle would have paid to use the HOT lane) will be greater than the value of the free access to the owner of the high-mpg vehicle. A cash subsidy—for example, a rebate of part of the purchase price of the high-mpg car—might attain the improvement in fuel economy at lower public cost, and the cost could be borne by all taxpayers rather than solely by other users of the expressway.

In recognition of these problems, California’s Commission on Transportation Investment (whose report was described in Chapter 1) recommended taxing alternative fuels at rates such that vehicles consuming the fuels pay the same tax per mile as the average for gasoline vehicles (CTI 1996, 27). Excise taxes or registration fees would be other mechanisms for charging road user fees to operators of advanced-technology vehicles. In 2002, Oregon began charging hybrid vehicles a higher annual registration fee to make up for lost fuel tax revenue (Rufolo and Bertini 2003, 33), but fees were again equalized in 2003.

The 2004 federal legislation that restored the revenue to the Highway Trust Fund that had been lost on account of the federal gasohol subsidy set a precedent for structuring alternative fuel incentives so that transportation programs do not bear the brunt of the revenue impact.

MEASURES TO DIRECT SPENDING MORE EFFECTIVELY

Improving Project Selection and Reducing Project Costs

Avoiding spending on projects and activities that yield poor returns and economizing on project costs are means of augmenting the resources available to transportation programs. The report on state highway finance of the Citizens Research Council of Michigan described in Chapter 1 concluded that user tax increases would be justified only if they were accompanied by management reforms in the highway program: “Unless the system is restructured both financially and administratively, it is very likely that any additional dollars will not purchase the improvement in transportation services that might be expected” (Citizens Research Council of Michigan 1997, 5). The report’s administrative proposals called for the following:

-

Improved methods of determining priorities. “The state has no structure for systematically determining which construction or maintenance projects should be carried out in what order” (p. 12).

-

Adoption of more durable designs and an increase in the share of funds devoted to maintenance, which, according to available data, would increase the cost-effectiveness of the program. The report concluded that the state does not know whether its design standards and maintenance practices minimize life-cycle costs.

-

Increased contracting out and streamlined state–local cooperation to improve administrative efficiency.

The council’s observations about decision making in Michigan are paralleled by the findings of a Government Accountability Office (GAO) review of state and local transportation investment decisions nationwide. GAO found that governments do perform various analyses of projects. However, there is no consensus understanding of the most useful methods, federal agencies provide only limited guidance on methods for the analyses that federal-aid programs require, and quantitative comparisons of benefits of alternatives play little role in decisions. The report acknowledges that other considerations, especially the availability of federal aid, public and political preferences, and constraints on intergovernmental cooperation, will exert major influence on decisions, but it concludes that the benefits of transportation investments could be increased through better use of analytical tools (GAO 2004b, 16–17, 39–40).

The report of California’s Commission on Transportation Investment (also described in Chapter 1) contained similar recommendations for overhauling the state’s planning and programming practices and for changes in state law to promote contracting out of certain transportation agency functions (CTI 1996).

A form of contracting that is attracting increasing attention as a means of reducing costs and accelerating schedules of transportation projects is the arrangement in which a private firm takes responsibility for design, construction, and often maintenance of a facility and bears part of the risk of cost or schedule overruns or performance failures. These contracts are commonly referred to as public– private partnerships (USDOT 2004; CBO 1998, xii). A USDOT review cites case studies showing that such contracts have reduced project costs by 6 to 40 percent, reduced the time to complete projects, and reduced the risk of cost overruns because of the performance incentives they provide to the private participants and the efficiencies of concentrating responsibilities for all phases of construction and operation (USDOT 2004, 2).

Developing Alternatives for Transit Finance

As described in Chapter 2, 10 percent of federal, state, and local highway user fee revenue was dedicated to mass transit in 2003, an amount equal to 25 percent of all transit spending. Highway user fee revenues devoted to transit in 2003 were as follows (FHWA 2004, Table HF-10):

|

Item |

Amount ($ billions) |

|

Distributions from the mass transit account of the Highway Trust Fund |

4.7 |

|

Distributions from highway account of the Highway Trust Fund and devoted to transit |

1.1 |

|

State and local highway user revenue devoted to transit |

4.4 |

Total highway user receipts in 2003 were $104.1 billion (FHWA 2004, Table HF-10), and total public transit spending was $40.1 billion (APTA 2005, Tables 52 and 61). In addition to the highway user fee revenues dedicated to transit by federal law (and deposited in the mass transit account of the Federal Highway Trust Fund), transit receives funds from the highway account of the trust fund through the flexible fund program: states or local governments may use the grants they receive in two federal-aid program categories (the Congestion Mitigation and Air Quality Improvement Program and the Surface Transportation Assistance Program) for transit or highway purposes. In recent years, governments have devoted about one-sixth of the total funding available through these two programs to transit (FTA 2004).

Because the impetus for this study was concern for the viability of present highway user fees as a revenue source, the committee has considered transit funding only insofar as it is linked to highway user fees. Within this scope are two policy questions regarding transit finance: First, if a transition from fuel taxes to mileage charges and tolls takes place at some time, will it be appropriate to continue present practice and dedicate a portion of the revenues from these new sources to transit? Second, in the search for ways to cope with the threat of erosion of revenues (from inflation, improved fuel economy, or other causes) under present finance arrangements, should the link between highway user revenues and transit funding be modified? Modifications might increase or decrease the share of highway revenue available for transit. For example, increasing the flexibility of state and local governments to apply their shares of highway user fee revenues for nonhighway purposes might be expected to increase transit funding. In the other direction, replacing highway user fee revenue with another dedicated revenue stream for transit and retaining highway user fee revenue for highway purposes might be considered. Such proposals should be evaluated according to how they would affect the fiscal health of transportation programs and public acceptability of user fees.

In Chapter 3 it was argued that providing subsidies to transit can be justified by benefits conferred on highway users and that charging highway users fees that exceed the highway agency’s cost of providing roads also can be a justifiable practice. However, the policy of dedicating a part of highway user revenue to transit does not in itself enhance the efficiency of the transportation system, compared with the alternative of providing transit subsidies from other dedicated sources or the general fund. The advantage of the policy is practicality. It has two important limitations. First, if highway user taxes are too high, the total public benefits of highway travel will be reduced. Second, if the effect of dedicating a portion of highway user fee revenue to transit is to decrease highway spending and increase transit spending, then the policy is beneficial only if the benefit of the increased transit spending is greater than the benefit that would have been derived from the lost highway spending.

After an evaluation of the trade-offs, one analysis of local transit funding options (Parry 2001) concluded that a mix of sources is necessary and that the capacity of highway user fees to support transit is limited. The possible revenue sources evaluated were the gasoline tax or other highway user fees, transit fares, the property tax, income taxes, and sales taxes. Raising property, sales, and income tax rates will cause economic dislocations that have costs. Raising transit fares will increase pollution and congestion from highway travel. Increasing the gasoline tax rate or other highway user fees would reduce pollution and congestion but also would cause the loss of some benefits of highway travel. The broadly based taxes (income, sales, and property taxes) have the advantage that relatively small increases in rates can generate large revenue relative to transit budgets.

This conclusion suggests that a reasonable policy may be to limit taxes on highway users for transit to fairly modest rates and to employ dedicated, broadly based taxes to support any expansion of transit programs. The present level of contributions at the state level—6 percent of all state highway user fee revenue devoted to transit—seems sustainable, although the federal contribution is much higher, at 17 percent (FHWA 2004, Table HF-10).

Many U.S. transit systems already receive support from dedicated, broad-based taxes. A 2004 report of the Metropolitan Washington (D.C.) Council of Governments’ Metro Funding Panel concluded that a dedicated regional sales tax would be the most desirable and practical revenue source to make up the shortfall between existing revenue and the system’s targeted spending level. The panel observed that the broad tax base (including visitors as well as residents) would match the breadth of the system’s benefits and that a dedicated tax would provide needed revenue stability (Metro Funding Panel 2004, 6–8).

The practice of subsidizing a local service like transit with the revenue of a nationwide tax like the federal fuel tax may appear in the future to be especially difficult to justify. One proposal for a more essential role for the federal government in aiding local transportation programs would be to relieve local governments of the cost of serving nonlocal traffic on their roads (Gramlich 1990, 226–228). The arrangement could be similar to the so-called pass-through tolls that recent legislation authorizes the state of Texas to pay to the state’s Regional Mobility Authorities—that is, payments would be made by the federal government to each local government proportional to the volume of nonlocal traffic on its roads. In return, local governments would accept responsibility for funding purely local transportation services. Compensation in the form of pass-through tolls would leave the local government in possession of the roads. This arrangement avoids the objection that local governments raised to Michigan’s plan (described in the section above on federal, state, and local roles) to transfer major commercial routes to the state—that the local governments did not want to give up planning control over these components of their systems.

In summary, the following are some guidelines worth considering as the process of reforming highway user fees gives rise to needs for revisiting the relationship of highway and transit funding:

-

The present rate of transfers of highway revenues to transit probably has small impact on highway programs, and highway travelers benefit where transit has alleviated congestion. However, greatly increasing the rate to fund expanded transit services would risk the loss of highway travel benefits that could be greater than the transit benefits gained.

-

Transit requires stable and broad-based tax support. Developing and expanding such support will be necessary in order to expand transit services. Most transit agencies already derive some support from dedicated broad-based taxes. (For example, as Table 2-4 shows, 16 percent of funding in 2000 was from dedicated sales taxes.) However, these sources account for a minority of nonfare funding, and some jurisdictions make little use of them.

-

Federal and state transportation aid ought to relieve local governments of the burden of serving nonlocal needs, rather than subsidize predominantly local services. Applying this rule would lead to some reallocation of external aid among American cities, but this outcome would be fair, since cities that were previously being undercompensated for the service they provided to interregional traffic would receive more aid.

-

With effective road pricing, a substantially larger share of transit spending could be funded from fare box revenue. If at some time in the future true road pricing is instituted (for example, road use metering on all roads in metropolitan areas, with charges varying with traffic conditions), the economic justification for transit subsidies from highway user fees or other sources will be diminished. If each highway trip were charged the cost that that trip imposed on other road users and on the highway agency, highway travel would no longer be subsidized, and adding extra charges to pay for transit would reduce the economic benefit of the transportation system. Transit would increase ridership and would be able to charge higher fares because travelers would have to pay road user charges if they chose automobile travel.

Redefining Federal, State, and Local Government Responsibilities

The focus of the federal-aid highway program from 1956 until the 1980s was construction of the Interstate highway system. Since the completion of the Interstates, successive reauthorization acts have attempted to define new goals for the federal-aid program, and reauthorization debates have brought forth proposals for terminating or greatly scaling back the program. Support for devolution sometimes has come from states that historically have received less in federal transportation aid than the federal highway user fee tax revenues collected within their boundaries

(although certainly not all donor states can be associated with this position). In California, a state that currently receives 90 cents in federal highway aid per dollar of federal highway user taxes collected within the state and deposited into the highway account of the Highway Trust Fund (FHWA 2004, Table FE-221), the 1996 report of the Commission on Transportation Investment recommended that the state seek to have the federal government repeal the federal gasoline tax and return to California its share of the balance of the Federal Highway Trust Fund (CTI 1996).

Parallel debates have occurred at the state level with regard to the balance of responsibilities between state and local governments. For example, the highway finance reports of the Citizens Research Council of Michigan that were described in Chapter 1 proposed guidelines for a realignment of highway responsibilities between the state government and local governments, including state assumption of control of locally owned roads that were important through routes (Citizens Research Council of Michigan 1996; Citizens Research Council of Michigan 1998).

Before a local government could successfully take on any additional responsibility for transportation systems, it would need adequate funding sources and administrative capacity. The spending trends summarized in Chapter 2 show that nationwide, the scale of local government responsibility has not changed greatly in recent decades. However, the extent of local government responsibilities varies greatly. This diversity of practice suggests that alternative institutional arrangements are feasible. For example, although nationwide 19 percent of all road miles are owned by state governments, the state mileage is more than 60 percent of the total in five states (Delaware, North Carolina, South Carolina, Virginia, and West Virginia) and under 10 percent in 12 (including California, Florida, Michigan, and Washington). The great majority of local mileage is secondary roads and streets, and nearly all expressway mileage is state owned, but local governments own one-third of the mileage of urban arterial highways other than expressways.

Toll road authorities offer an institutional model for independent management of expressways on a metropolitan or regional level. Most toll roads in the United States are operated by independent authorities. The major turnpike authorities are subject to state political control, but locally controlled authorities operate toll roads in California, Colorado, Florida, Texas, and Virginia (FHWA 2004, Tables HM-10, HM-50, LGF-3B). The organization of local toll expressways in California, Texas, and Colorado was described in Chapter 5. Another institutional model is provided by the independent authorities, many of them organized on a metropolitan basis, that operate most large U.S. public transit systems. As Chapter 2 described, federal surface transportation legislation has promoted greater local government responsibility and capability for metropolitan transportation decision making; at the end of this section a proposal for federal action to strengthen these local capabilities is described.

The proposals outlined below, which were taken from several sources, are presented to illustrate the variety of conceptions of the extent of devolution that should occur and the scope of responsibilities that the federal government should retain.

Reorienting the Federal Program

These proposals concentrate on adjusting the rules and procedures of the federal-aid program to improve its performance in carrying out legitimate federal responsibilities. Under one reasonable definition of the scope of federal responsibility for highways, the federal government should ensure the supply of capacity that is beneficial from a national perspective but that state and local governments would not adequately supply on their own. State and local governments will have little interest in providing capacity to serve through traffic if it contributes little to local taxes and local residents’ incomes.

Federal grants can fulfill this responsibility by paying state and local governments to supply the increment of capacity beyond their own requirements that would be beneficial for the nation as a whole. However, a long-standing criticism of federal-aid highway grants is that their structure provides little incentive for states to spend more on capacity than they would in the absence of the federal program. The state or local matching share is small (20 percent for most projects), and the total amount of federal grants for which a state is eligible is capped. Under these rules, if a state is undertaking more capital spending from its own funds than the minimum needed to match all available federal aid, then a large share of the federal aid probably is simply displacing state funds rather than adding to the net total of state capital spending (GAO 2004a; Gramlich 1990; Oates 1999).

A representative proposal for measures to increase the effectiveness of federal highway grants in fulfilling the core federal responsibilities of the federal government had the following provisions (Gramlich 1990):

-

Roads serving predominantly state (or local) travel should be the responsibility of state (or local) governments.

-

Roads with national significance should be eligible for federal aid; these roads could be identified according to the share of their traffic that is non-local or interstate travel.

-

The federal matching share in highway grants should be reduced and the cap on available aid eliminated. For any project that a state undertakes on a road eligible for aid, the state should receive a federal grant representing the percentage share of out-of-state benefits. This share could be approximated by the percentage share of out-of-state traffic on the road and often would be small compared with the present federal contribution.

-

Restrictions on the use of federal grants for maintenance should be eliminated so that decisions about the optimum mix of capital and maintenance spending on federal-aid roads would not be biased by federal restrictions.

A grant program following these rules would maximize federal leverage over the quantity of state spending on the eligible roads for a given total federal outlay, since all projects would be eligible for federal aid.

Comprehensive Devolution

Legislation proposed in Congress in 1996 (the Transportation Empowerment Act, Congressional Record, July 19, 1996: S8372), before enactment of the 1998 surface transportation act (the Transportation Equity Act for the 21st Century), and during debate before the 2005 legislation (SAFETEA-LU) would have phased out most of the federal-aid program over a period of years (Utt 2003). The elements of the 2003 bill (H.R. 3113, which was not enacted) were the following:

-

The federal gasoline tax dedicated to the Highway Trust Fund would be reduced in five steps from the present $0.183 per gallon to $0.02 per gallon after 6 years.

-

A category of essential federal highway programs would be retained:

-

The Interstate Maintenance Program, a federal categorical grant program now funded at $6 billion per year,

-

Federal spending for roads on public lands and Indian reservations,

-

Surface transportation research, and

-

Certain highway safety and motor carrier safety programs.

-

-

During the transition period, the difference between spending each year on the essential federal programs and federal highway user fee revenues would be distributed to the states proportionally to tax collections in each state.

-

Crediting of a portion of federal gasoline tax revenue to the mass transit account of the Highway Trust Fund would end immediately. A new, smaller federal transit grant program would continue.

Although such proposals have not progressed far, they indicate sentiment, particularly among officials in some states that contribute more federal highway user fee revenue than they receive in federal aid. The National Surface Transportation Infrastructure Financing Commission created in the 2005 legislation (SAFETEA-LU, Section 11142), is to evaluate, as part of its charge, a proposal to allow any state not to participate in the federal-aid highway program in return for a suspension of federal highway user fee collections within the state.

Empowering Local Governments

The underlying rationale of devolution proposals is that most highway and transit problems are primarily local in their scope and impacts and that therefore the federal government lacks competence to solve them. A series of proposals published by the Brookings Institution calls for devolution of decision making and revenue raising, but with active federal engagement to realign authority in favor of local governments relative to the states (Boarnet and Houghwout 2000; Puentes 2004). The highlights of these proposals are the following:

-

The federal government should provide financial incentives for states to transform metropolitan planning organizations (which are creatures of federal transportation programs) into regional infrastructure authorities, with taxation, programming, and spending power, and to tie state decisions more closely to the priorities of metropolitan governments.

-

Most federal funding should be replaced with regionally levied user fees.

-

The retained federal responsibilities should be

-

Preservation of portions of the network that provide truly national benefits,

-

Provision of assistance to poorer regions,

-

Cooperation with states and metropolitan governments on standards setting and research, and

-

Environmental protection.

-

SUMMARY

This chapter has surveyed options for adjustments to the system of charging and paying for highways and transit in ways that would improve the delivery of transportation services. The measures described have been prominent in discussions of transportation finance reform. They include a variety of adjustments to existing charges and changes in management practices, which their proponents believe would augment resources, better align fees with costs, or improve the effectiveness of transportation spending, and which could be carried out without fundamentally altering the existing framework of user fees and revenue sources.

Among the measures listed, several appear to hold promise for improving the stability of transportation funding and the performance of the transportation system. They include adjusting fees according to the cost of providing service to different kinds of road users, in particular, large trucks; improving tax compliance and limiting exemptions from payment of user fees; providing additional dedicated funding sources for transit; and better aligning the responsibilities of federal, state, and local governments with the character of the transportation services provided. Committee recommendations for actions on some of these measures are

presented in the next chapter. Individually, none of these measures would dramatically affect user fee revenue or system performance. Nevertheless, striving for small gains on multiple fronts may be the most productive short-term strategy available to governments that operate highways and transit.

REFERENCES

Abbreviations

AASHTO American Association of State Highway and Transportation Officials

APTA American Public Transportation Association

CBO Congressional Budget Office

CTI Commission on Transportation Investment (California)

FHWA Federal Highway Administration

FTA Federal Transit Administration

GAO Government Accountability Office

ODOT Oregon Department of Transportation

TRB Transportation Research Board

USDOT U.S. Department of Transportation

AASHTO. 2003a. Innovative Finance: Expanding Opportunities to Advance Projects. Washington, D.C., March.

AASHTO. 2003b. Transportation Finance Corporation: Leveraging New Revenue to Fill the Gap. Washington, D.C., March.

Ang-Olson, J., M. Wachs, and B. Taylor. 2000. Variable State Gasoline Taxes. Transportation Quarterly, Vol. 54, No. 1, Winter, pp. 55–68.

APTA. 2005. 2005 Public Transportation Factbook. April.

Boarnet, M., and A. Houghwout. 2000. Do Highways Matter? Evidence and Policy Implications ofHighways’ Influence on Metropolitan Development. Brookings Center on Urban and Metropolitan Policy, March.

CBO. 1992. Paying for Highways, Airways, and Waterways: How Can Users Be Charged?May.

CBO. 1998. Innovative Financing of Highways: An Analysis of Proposals. Jan.

CBO. 2003. A Comparison of Tax-Credit Bonds, Other Special-Purpose Bonds, and Appropriations inFinancing Federal Transportation Programs. June.

Citizens Research Council of Michigan. 1996. Michigan Highway Finance and Governance: In Brief. Nov.

Citizens Research Council of Michigan. 1997. Michigan Highway Finance and Governance.

Citizens Research Council of Michigan. 1998. Michigan Highway Finance and Governance: A One-YearReport Card.

CTI. 1996. Final Report. Jan.

Denison, D.V., R.J. Eger III, and M.M. Hackbart. 2000. Cheating Our State Highways: Methods, Estimates, and Policy Implications of Fuel Tax Evasion. Transportation Quarterly, Vol. 54, No. 2, Spring, pp. 47–58.

FHWA. 2004. Highway Statistics 2003. U.S. Department of Transportation.

Fischer, J.W. 2004. Highway and Transit Program Reauthorization Legislation in the 2nd Session, 108thCongress. Congressional Research Service, April 21 (update).

FTA. 2004. Trends in the Flexible Funds Program: Annual Status Report 2002. U.S. Department of Transportation.

GAO. 2004a. Federal-Aid Highways: Trends, Effect on State Spending, and Options for Future ProgramDesign.

GAO. 2004b. Surface Transportation: Many Factors Affect Investment Decisions. June.

Gramlich, E. 1990. How Should Public Infrastructure Be Financed? In Is There a Shortfall in PublicCapital Investment?(A. Munnell, ed.), Federal Reserve Bank of Boston, Boston, Mass.

Metro Funding Panel. 2004. Report of the Metro Funding Panel: Final Draft for Public Release andComment: Key Findings. Metropolitan Washington Council of Governments, Dec. 17.

Oates, W.E. 1999. An Essay on Fiscal Federalism. Journal of Economic Literature, Vol. 37, Sept., pp. 1120–1149.

ODOT. 2004. Mileage Tax Rates. July.

Parry, I.W.H. 2001. Finding the Funds to Pay for Our Transportation Crisis: A Look at Options for Solving Washington, D.C.’s Traffic Woes. Resources, Issue 144, Summer, pp. 17–19.

Peters, M. 2002. Statement of Mary E. Peters, Administrator, Federal Highway Administration, Before the Committee on Finance, United States Senate: Hearing on Schemes, Scams, and Cons: Fuel Tax Fraud. Senate Finance Committee, July 17.

Puentes, R. 2004. Cement and Pork Don’t Mix. MetroView, Brookings, May 10.

Road User Fee Task Force. 2003. Report to the 72nd Oregon Legislative Assembly on the PossibleAlternatives to the Current System of Taxing Highway Use Through Motor Vehicle Fuel Taxes. March.

Rufolo, A.M., and R.L. Bertini. 2003. Designing Alternatives to State Motor Fuel Taxes. TransportationQuarterly, Vol. 57, No. 1, Fall, pp. 33–46.

Rufolo, A.M., L. Bronfman, and E. Kuhner. 2000. Effect of Oregon’s Axle-Weight-Distance Tax Incentive. In Transportation Research Record: Journal of the Transportation Research Board, No.1732, Transportation Research Board, National Research Council, Washington, D.C., pp. 63–69.

TRB. 2002. Special Report 267: Regulation of Weights, Lengths, and Widths of Commercial Motor Vehicles. National Academies, Washington, D.C.

USDOT. 1997. 1997 Federal Highway Cost Allocation Study. Aug.

USDOT. 2004. Report to Congress on Public–Private Partnerships. Dec.

Utt, R.D. 2003. Proposal to Turn the Federal Highway Program Back to the States Would Relieve Traffic Congestion. Backgrounder, No. 1709, Heritage Foundation, Washington, D.C., Nov. 21.