Economic Impacts of International R&D Coordination: SEMATECH and the International Technology Roadmap

Kenneth Flamm

University of Texas at Austin

The 1990s were an important and dynamic period in the evolution of the global semiconductor industry. During this decade, three major forces transformed the face of the industry. First, there was a marked acceleration in the rate of technological change in the sector starting in the middle of the decade. Second, a new U.S. R&D strategy emerged. Third, a global dispersion of the production infrastructure for the industry that had begun in the mid-1960s increasingly extended into R&D. This paper describes how these three developments were linked, how changing institutional arrangements used to organize semiconductor R&D shaped technological change, and the economic impacts of innovation in this industry.

THE PACE OF TECHNOLOGICAL CHANGE

The acceleration of technological change in semiconductors in the late 1990s is now well appreciated. Table 1 shows that an increased pace of technological progress was evident throughout the industry, but that two sectors—memory and microprocessors—forged ahead at a significantly faster speed.

Microprocessors are of particular interest for many reasons. First, they had the highest rate of improvement in price performance for any class of semiconductor product in the 1990s and afterward. (See Table 1.)

TABLE 1 Rates of Decline in Quality-Adjusted Price for Semiconductors, 1991-1999

|

|

Compound Annual Decline Rates (%) |

||

|

CAGR 91-95 |

CAGR 95-99 |

CAGR 91-99 |

|

|

MOS MPU |

−40.36 |

−61.89 |

−52.3 |

|

MOS Memory |

−8.02 |

−47.87 |

−30.8 |

|

of which, DRAM |

−7.76 |

−53.46 |

−34.5 |

|

MOS MPR |

−3.89 |

−23.01 |

−14.0 |

|

Other MOS Logic |

−6.76 |

−19.13 |

−13.2 |

|

Thyristors & Rectifiers |

−0.84 |

−12.94 |

−7.1 |

|

MOS MCU |

0.36 |

−13.87 |

−7.0 |

|

Power Transistors |

−0.78 |

−10.27 |

−5.6 |

|

Small Signal Transistors |

0.26 |

−10.50 |

−5.3 |

|

Optoelectronics |

3.25 |

−10.04 |

−3.6 |

|

Diode & All Other Discrete |

4.28 |

−9.03 |

−2.6 |

|

Digital Bipolar |

5.37 |

−4.01 |

0.6 |

|

SOURCE: Author’s calculation based on data in Aizcorbe, Flamm, and Khurshid (2004). |

|||

Second, microprocessors are the largest single semiconductor input, in terms of value, in personal computers1 and are the technological core of all computers, big and small. Technological improvements in the semiconductors alone have been estimated to account for 40 percent to 60 percent of price-performance improvement in personal computers (PCs) in the late 1990s.2 Quality-adjusted improvement in computer prices, in turn, is credited with a major role in the rapid improvement in U.S. productivity growth in the late 1990s.3

Finally, microprocessors have increasingly become the dominant product in semiconductor production facilities located in the United States, as semiconductor manufacturing, in turn, became the largest U.S. manufacturing industry (measured

by value added) in the 1990s. In 2004, microprocessors accounted for in excess of 46 percent of all U.S. semiconductor shipments, compared to 29 percent in 1995.4 To an ever-increasing extent, the future of U.S. semiconductor manufacturing has become synonymous with the technological health of microprocessors.

A NEW RESEARCH STRATEGY5

The roots of a newly aggressive U.S. technology policy in semiconductors in the 1990s reach back to the late 1970s, another period of radical industrial change in a global semiconductor industry previously dominated by U.S. producers. In that epoch, Japan had launched a series of government-industry semiconductor R&D consortia—the so-called very large-scale integration (VLSI) projects. These efforts were perceived by most observers to have greatly advanced the technological and manufacturing competence of Japanese semiconductor producers.

In 1987, the U.S. Defense Science Board issued a report noting a rapid deterioration in the relative position of U.S. semiconductor manufacturers, characterizing this as a national security issue. Responding, the U.S. government decided to have the Defense Department pay half of the cost of a joint industry consortium—dubbed SEMATECH (for semiconductor manufacturing technology) and budgeted at $200 million annually.

The objective of improving U.S. semiconductor manufacturing technology may have been fairly clear, but the means by which SEMATECH was to do it sparked considerable debate. In its first few years of existence, SEMATECH’s organizational focus shifted about and was not always wholly effective. One constant was that it was restricted to U.S. companies; Japanese producer NEC, which had a U.S. production plant, was turned away when it sought to join in 1988.

SEMATECH refocused its structure and research direction in 1992, when William Spencer joined SEMATECH, replacing its founding CEO, Robert Noyce. Even in earlier years, there had been an increasing emphasis at SEMATECH on projects aimed at improving the equipment and materials that U.S. semiconductor makers procured from suppliers. Under Spencer, SEMATECH carried out an internal reorganization and explicitly defined a new long-range strategy (SEMATECH II), focusing on reduction of the elapsed time between introductions

of new technology “nodes” into manufacturing plants by SEMATECH members from 3 years between nodes, to 2 years.

A crucial element in this strategy was the institutionalization and acceptance within the U.S. semiconductor industry of a so-called roadmap process, a systematic attempt by all major players in both the U.S. integrated circuit industry and its materials and equipment suppliers to jointly work out the details of the complex array of likely new technologies required for manufacturing next-generation chips, coordinate the required timing for their introduction, and intensify R&D efforts on the pieces of technology that were likely to be “showstoppers” and required further work if the overall schedule was to succeed.

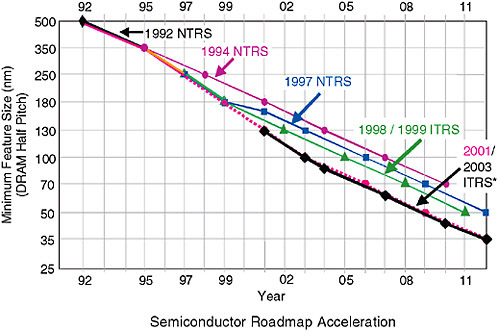

The National Advisory Council on Semiconductors (NACS), set up by the federal government at the same time as SEMATECH, took the first step down the roadmap road by convening a “Microtech 2000” workshop in 1992. A report was also published in 1992 detailing the goals for semiconductor manufacturing technology produced by participants at this workshop. SEMATECH continued to provide technological leadership for the roadmap process. The first official “National Technology Roadmap for Semiconductors,” issued in 1994, still had new technology nodes being introduced at the historical pace of approximately three-year intervals. But the effort to step up the pace succeeded: The 250-nanometer technology node came online a year earlier than predicted by the time the 1994 Roadmap came out. The 1997 National Technology Roadmap called for maintaining the two-year intervals rather than returning to the historical three-year pattern for the next technology node (180 nanometers) and those to follow.

This acceleration in the rate of manufacturing technology improvement within what had become a globalized semiconductor industry clearly was assisted by factors beyond the walls of the U.S. SEMATECH consortium. Intensifying competitive pressures were felt around the world, and quickening the pace of new technology deployment was a logical economic response. However, the open discussion of industry-wide R&D needs and explicit coordination of R&D efforts across companies through an industry-wide program was a significant new development.

The industry-wide embrace of an accelerated, two-year rhythm for technology introductions coincided with a major structural change within SEMATECH. The consortium decided in 1995 to join with foreign producers in an international partnership to quicken deployment of materials and equipment designed for use with 300mm (12-inch) silicon wafers (I300I). U.S. government funding for SEMATECH was terminated by mutual consent in 1996. A new International SEMATECH was formed in 1998 to house the increasing number of projects involving foreign chip producers. Finally, in 1999, the original SEMATECH reorganized itself as International SEMATECH. Today, the share of world semiconductor output accounted for by SEMATECH members greatly exceeds the share held when the original U.S.-only consortium formed in late 1980s.

SEMATECH’s reorganization as an international entity implicitly recognized that technological capability, and the best manufacturing technology, resided in a geographically dispersed network of global equipment and materials suppliers. The internationalization of SEMATECH, another Spencer initiative, was actively encouraged by U.S. policymakers, particularly at the Department of Defense.6 By all accounts, the prior recovery and stabilization of the health of the U.S. semiconductor industry played a critical role in building the political support for this decision by all parties.

SEMATECH’s activities today have little resemblance to the classical vision of an industrial research laboratory. As an organization, it is mainly concerned with coordination and standards, bringing materials and equipment suppliers together with its members to work on technology projects largely executed outside its walls, serving as executive agent for the industry roadmap, and uniting a broad array of firms to organize industry standards for tools, software, and metrics for manufacturing.

SEMATECH was viewed as a major success in Japan. The SEMATECH model (ironically, a U.S. reaction to the Japanese VLSI consortia of the 1970s) became the inspiration for a new generation of Japanese semiconductor R&D consortia in the mid-1990s. Japan’s semiconductor industry formed its own R&D consortium, SELETE, with a single non-Japanese member—Korean producer Samsung. As the new century dawned, two transnational R&D organizations coexisted within the international semiconductor industry—SELETE, headquartered in Japan, and International SEMATECH, with headquarters in the United States. The 1997 roadmap became the last “national” technology roadmap, replaced by “International Technology Roadmaps” sponsored and coordinated through these two global R&D consortia and semiconductor industry associations in the United States, Europe, Japan, Korea, and Taiwan.

In September 2004, SEMATECH once again transformed itself, dropping the term “international” from its name. SEMATECH public communications spun this as a “branding” issue, perhaps indicating that in today’s thoroughly globalized semiconductor industry the very word “international” has become redundant.

SEMATECH continues to have many international members, including, most recently, Korean giant Samsung. SEMATECH also spun off a subset of its R&D activities into the International Semiconductor Manufacturing Initiative (ISMI) in 2004. Members of ISMI gain access to a variety of semiconductor manufacturing technology projects but are walled off from access to the “highest tech” (e.g., lithography) R&D, which remain within the main SEMATECH organization. All nine “full” SEMATECH members (AMD, Freescale, Hewlett-Packard, IBM, Infineon, Intel, Philips, Samsung, Texas Instruments) also get membership in ISMI. But six ISMI-only members (TSMC, Panasonic/Matsushita Electric, Spansion, NEC, Renesas ) do not get access to the full SEMATECH information

set. In 2005 Panasonic became the first Japanese firm to join ISMI, and it has since been followed by NEC and Renesas.

To summarize, SEMATECH transformed itself from a national (U.S.) R&D consortium, designed to strengthen the competitive fortunes of U.S.-based semiconductor firms, to a fully international consortium. Although it no longer receives an annual subsidy from the federal government (though U.S. government agencies have been invited to help fund specific projects of interest to them), it now receives significant subsidies from the states (Texas and New York) in which it has facilities located.

Perhaps the most enduring impact of the internationalization of SEMATECH was the globalization of the international roadmap it now leads. The creation of the International Technology Roadmap for Semiconductors (ITRS) is a unique phenomenon. In no other global high technology industry do all major producers, worldwide, come together to coordinate, in detail, the direction and pace of introduction of new manufacturing technologies. That the ITRS is global recognizes that the leading edge firms in semiconductors are true multinationals, scattered about the globe.

The continuing support by this global community for the roadmap reflects a common belief that close coordination among specialized suppliers of manufacturing equipment and materials and with the users has indeed served to accelerate innovation in the industry. Two-year nodes have continued to be introduced on a regular basis. Indeed, given the high fixed costs of R&D and investment in new manufacturing technology, there have been repeated calls to slow down the pace of introduction of the new nodes from the breakneck two-year cycle to improve profitability (see Figure 1). To date, these calls have gone unanswered; once on the technology bullet train, it is difficult for any firm to slow down its introduction of new technology as long as there is a decent probability that its rivals will continue to maintain the accelerated pace and beat it to market with newer and higher-performance manufacturing technology.

Interestingly, the close coordination of the introduction of new technology across firms might normally be expected to be the sort of thing that government antitrust authorities might view skeptically. However, a U.S. law passed in the 1980s carved out a specific exception by granting limited antitrust immunity for registered R&D consortia such as SEMATECH. Under this sheltering umbrella, and because the United States tends to be a leader in international antitrust enforcement, the SEMATECH-guided national technology roadmap, and its successor, the ITRS, have flourished.

THE INTERNATIONALIZATION OF R&D

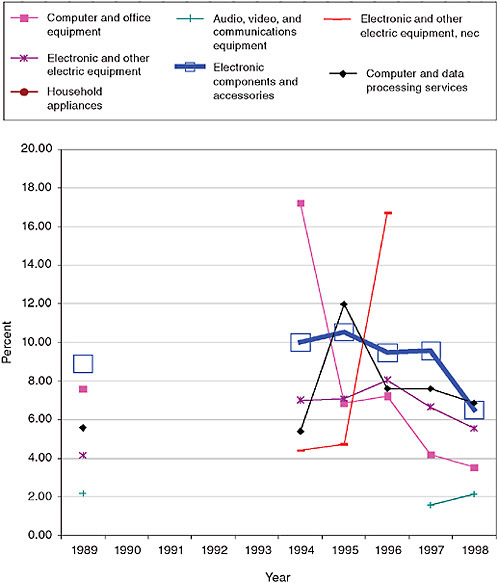

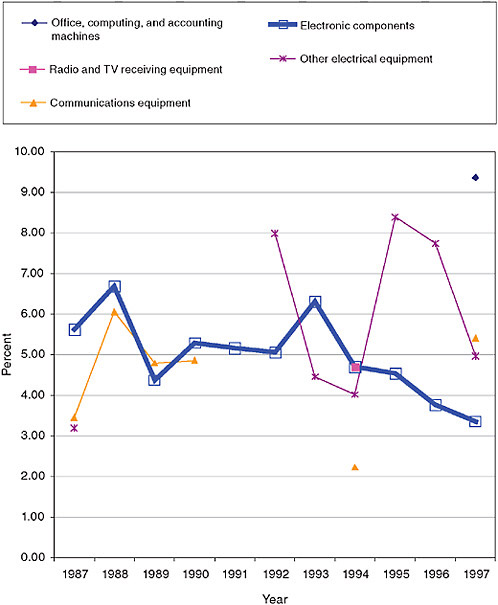

The shift in the late 1990s to an international focus did not mirror a trend in U.S.-based semiconductor producers toward performing more of their R&D in other countries. Two sources of data—the Commerce Department’s survey

FIGURE 1 Relation of ITRS to 2-year cycle.

NOTE: The 2003 ITRS timing is unchanged from the 2001 ITRS.

SOURCE: Spencer, W. J., L. Wilson, and R. Doering. 2004. “The Semiconductor Technology Roadmap.” Future Fab International 18.

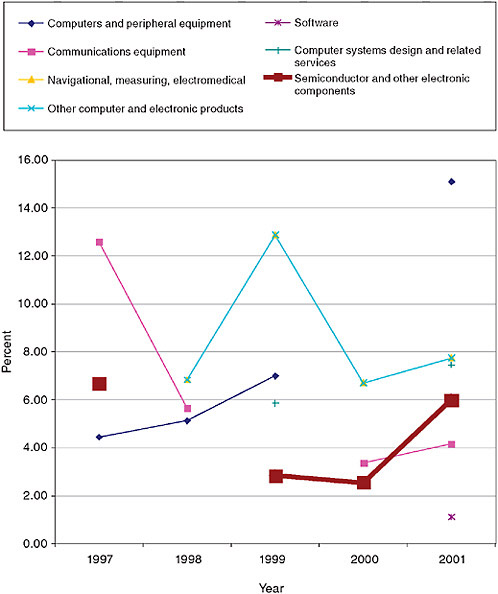

of the R&D performed by U.S. multinationals and their majority-owned foreign affiliates (Figure 2), and the National Science Foundation’s survey of U.S. industrial R&D performed by domestic companies and their foreign subsidiaries (Figure 3)—show that the ratio of R&D performed overseas by subsidiaries to R&D performed domestically by their parents actually declined in the electronic component industry (which is dominated by semiconductors) in the late 1990s.

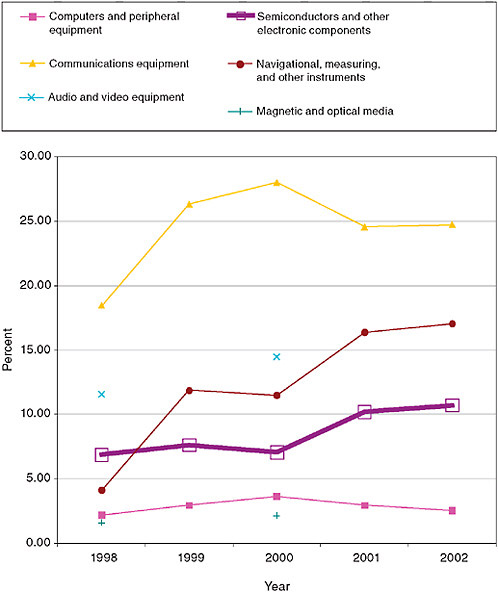

Most recently, however, there has been an apparent shift toward a true internationalization of R&D performed by U.S. semiconductor makers. Figure 4 (majority-owned foreign affiliate R&D relative to parent R&D) and Figure 5 (subsidiary R&D relative to U.S. domestic company) both show a recent trend toward a significant increase in the role of U.S. companies’ overseas R&D in semiconductors after the millennium.

What are we to make of this? One credible explanation is that throughout the late 1990s, U.S. companies occupied a position at the technological frontier in virtually all areas of semiconductor manufacture. There was little incentive to build overseas labs and listening posts. R&D cooperation through the roadmap process created an alternative information and coordination mechanism that

FIGURE 2 Majority-owned foreign affiliate R&D as percent parent R&D.

SOURCE: Bureau of Economic Analysis.

provided a way of cooperating with foreign materials and equipment suppliers in those areas where “best of breed” manufacturing technology did not reside in the United States.

Since the turn of the century, however, it has been increasingly evident that a steadily increasing share of manufacturing and technology development is being undertaken outside the United States by increasingly competent and techno-

FIGURE 3 Subsidiary R&D as a percent of U.S. domestic company R&D.

SOURCE: National Science Foundation.

logically progressive foreign producers. Indeed, many U.S. firms now have joint technology development activities with these foreign firms. A rational response to improving competence outside the United States is to gain access to these overseas developments by establishing offshore R&D activities that afford some access to foreign technology.

FIGURE 4 Majority-owned foreign affiliate R&D as a percent of parent R&D.

NEW MODELS OF INTERNATIONAL R&D COOPERATION

Although SEMATECH (itself inspired by the Japanese VLSI technology consortia of the 1970s) was the pioneer in first creating an international cooperation mechanism (the roadmap) and later in transforming itself from a national technology initiative into an international consortium, it is no longer the only player in this space. Today, there are alternative models for truly international

FIGURE 5 Subsidiary R&D as a percent of U.S. domestic company R&D.

consortia that have brought new energy and dynamism to the globalization of semiconductor R&D.

One model is a national or regional government-subsidized center or lab, in which a number of international semiconductor producers participate in a broad research program. One such example is the “Crolles 2” research consortium, in which Philips, STM, and Freescale participate. The government subsidy is

provided by the French nuclear agency, the EU, and regional authorities.7 Like SEMATECH, the Crolles 2 participants all fund a common research agenda.

Another, substantially larger effort built around a central R&D lab is IMEC in Leuven, Belgium, subsidized mainly by the Flanders regional government in Belgium, but also with some EC funding.8 Unlike SEMATECH, IMEC historically has had university research tightly coupled with private participants on the premises of its facility. Also unlike the original SEMATECH model, IMEC allows private participants to pick and choose from individual projects to fund and participate in. Much of what IMEC does is contract research undertaken for individual participants; in 2000-2001, this accounted for about 70 percent of IMEC’s budget.9 Nonetheless, IMEC’s 2005 budget was about $280 million,10 roughly double SEMATECH’s budget.

Yet another new model of international semiconductor R&D cooperation relies on a private company to provide the organizational framework. IBM has what might be characterized as a “hub and spoke” arrangement with a variety of global semiconductor producers, including Toshiba, Sony, Samsung, Infineon, Chartered, and AMD. IBM’s own facilities in New York serve as the common R&D location, and foreign participants send engineers and technical personnel to IBM to participate in technology development, and share in the results. IBM also receives government subsidies from the state of New York for some of the inputs to this activity.11

One interesting common thread that runs through all of these new international R&D arrangements is that the bulk of the funding no longer is coming from national governments. Instead, regional governments and funding entities—whether states, provinces, or larger regions—are funding global technology development in the hopes of creating technology spillovers that stimulate the growth of new industrial “clusters” in the home region. This is true for Texas and New

|

7 |

See for example, Peter Clarke, “LETI, Crolles alliance open $350-million 32-nm research fab,” EE Times, April 24, 2004, Acessed at <http://www.eetimes.com/showArticle.jhtml?articleID=18902684>. |

|

8 |

Interestingly, IMEC was actually established by the Flanders regional government back in 1984, before SEMATECH was started. IMEC’s budget remained under 50 million Euros through the mid-1990s, in contrast to SEMATECH’s initial $200 million budget. However, IMEC budget al.most quintupled over the decade from 1996 to 2006, while SEMATECH’s total budget shrank. Presentation of Anton De Proft, IMEC, at Symposium on “Synergies in regional and national policies in the global economy,” Leuven, Belgium, September 2006. |

|

9 |

Gail Purvis, “Moving into the Real World,” Electronic Business July 1, 2002. |

|

10 |

Presentation of Anton De Proft, IMEC, at the National Academies Symposium on “Synergies in Regional and National Policies in the Global Economy,” Leuven, Belgium, September 2006. |

|

11 |

For discussions of these relationships, see, “IBM & AMD aim alliance at the 22nm frontier,” Semiconductor Fabtech November 1, 2005; “IBM, Sony, Toshiba take technology alliance beyond 32nm,” Semiconductor Fabtech December 1, 2006; ”IBM and partners ready 45nm low power process,” Semiconductor Fabtech August 30, 2006; “Governor Pataki Announces Historic Investments by IBM Global High-Tech Leaders In Nanoelectronics Manufacturing And Development,” January 6, 2005,Accessed at <http://www.nanotechwire.com/news.asp?nid=1453>; Peter Clarke, Mark LaPedus and Mike Santarini, “IBM-led Consortium to Build Fab in N.Y.,” EE Times January 5, 2005. |

York funding for SEMATECH, New York funding for IBM facilities used with its research partners, Flemish funding for IMEC, and French national and regional funding for Crolles 2.

IMEC and Flanders is an extreme case of this phenomenon. Although Flanders founded IMEC in 1984 to jumpstart a Belgian semiconductor manufacturing industry, there is still not a single major semiconductor device or equipment manufacturing plant located anywhere in Belgium. The historical record in creating a Belgian semiconductor cluster does not seem particularly strong from a U.S. perspective. From 1984 through 2002, for example, there were 20 spin-offs from IMEC, only a few of which seem directly related to semiconductor device, materials, and equipment manufacturing, and none of which has gone on to become a major industry player.12 Nonetheless, Flanders is pouring tens of millions of Euros into the development of technology used by semiconductor manufacturers.

Semiconductor manufacturing firms from around the globe are essentially co-funding the development of their technology in Belgium, but none appear to have actually located a major semiconductor design or manufacturing facility making use of this technology in Belgium. Although it is certainly true that a skilled and trained technical workforce is growing in Flanders, to date this has not created a broader and wider manufacturing cluster that extends much beyond the R&D services being performed for the benefit of foreign multinationals that do some design in Flanders but all of their manufacturing elsewhere. The IMEC model may ultimately prove a useful economic development strategy, but so far it has not fulfilled its initial objectives.

Yet IMEC has experienced enormous growth over the past 5-10 years, and it may well be that the local industrial spillovers from this burgeoning activity are still to come. There is every sign that global semiconductor producers perceive IMEC to be a very successful R&D enterprise, even if its downstream industrial success remains to be proven. SEMATECH, for example, has recently started (with a subsidy from Texas) a research consortium with the University of Texas at Austin (the Advanced Materials Research Consortium), much as IMEC built its activities around relationships with university researchers in Leuven and elsewhere in Belgium. Historically, success has bred imitation, and by this metric, IMEC certainly appears to be a successful R&D consortium.

THE IMPACT OF R&D COORDINATION ON THE SEMICONDUCTOR INDUSTRY: THE CASE OF MICROPROCESSORS

To recap the analysis above, the 1990s saw the convergence of three distinct trends—the evolution of SEMATECH and a drive to create a roadmap to guide the development of semiconductor manufacturing technology in the United States, a

globalization of semiconductor R&D and the internationalization of the U.S.-led semiconductor roadmap process, and an acceleration in the rate of technological progress in semiconductor manufacturing. How closely were these phenomena linked?

Studies by economists measuring semiconductor prices show accelerating declines in quality-adjusted semiconductor prices in the late 1990s for virtually all types of semiconductors after the move to a two-year cycle in 1995.13 Faster semiconductor prices declines, in turn, had large effects on price declines for computer and communications equipment, which in turn had a major impact on aggregate economic growth and productivity improvement in recent years.14

A simple model of semiconductor manufacturing costs can be used to predict how an acceleration of the cycle between new technology nodes from 3 years to 2 years will effect manufacturing costs for a semiconductor component with given functionality.15 Using a model of this sort, we can decompose improvements in semiconductor price-performance into two broad sources of change—declines in price for given quality (or functionality) flowing from lower manufacturing costs associated with new technology and qualitatively improved capabilities and functionality (performance) provided by chips. We can estimate the first element as the contribution of lower-cost manufacturing to quality-adjusted chip price, and measure the second as a residual after deducting off the first element from some measure of total quality-adjusted price declines for semiconductors.

Although this framework attempts to distinguish between “pure” manufacturing cost improvement and all other sources of innovation in chips (which we label “design innovation”), we need to recognize that design innovations are often stimulated by the availability of lower-priced semiconductor functionality. Also, improved manufacturing technology may create quality improvement as an incidental by-product of the manufacturing process and thus have an impact beyond simply reducing the cost of given functionality on a chip. For example, smaller feature sizes on a chip, which lower the manufacturing cost for some given set of transistors, may also mean potentially faster logic gates or clock speeds, simply because electrons have to travel shorter distances between transistors. By the same token, architectural innovations may be required in order to fully exploit the faster potential clock speeds. Thus, while we can partition sources of quality-adjusted

|

13 |

See Table 1. |

|

14 |

See D. Jorgenson and K. Stiroh, “Raising the Speed Limit: U.S. Economic Growth in the Information Age,” op. cit.; Jorgenson, “Information Technology and the U.S. Economy,” op. cit. |

|

15 |

See K. Flamm, “Microelectronics Innovation: Understanding Moore’s Law and Semiconductor Price Trends,” International Journal of Technology, Policy, and Management 3(2), 2003; K. Flamm, “The New Economy in Historical Perspective: Evolution of Digital Technology,” in New Economy Handbook, St. Louis, MO: Academic Press, 2003; K. Flamm, “Moore’s Law and the Economics of Semiconductor Price Trends,” in National Research Council, Productivity and Cyclicality in Semiconductors: Trends, Implications, and Questions, D. W. Jorgenson and C. W. Wessner, ed., Washington, D.C.: The National Academies Press, 2004. |

price declines in semiconductor parts to a contribution of lower manufacturing costs for given functionality and a contribution of all other sources of chip improvement (“design innovation”), we need to recognize that these two factors are not in fact independent and that two are synergistic. Lower-cost transistors on a chip may also be faster transistors and stimulate new designs, while new designs are needed to take full advantage of vastly cheaper transistors.

I have elsewhere looked at the relative contributions of cheaper functionality flowing from manufacturing innovation and design innovation in the semiconductor chip with the highest rate of decline in the late 1990s—the microprocessor.16 My estimate is that roughly half of the decline in quality-adjusted price over this period came from lower manufacturing costs for the transistors in a given chip design, with the other half of quality-adjusted price improvement coming from other sources, including architectural and design innovation.17

Within the half of quality-adjusted price decline attributable to introduction of new technology nodes, perhaps one-sixth to one-third of the improvement is attributable to acceleration in the introduction of new nodes from 3 years to 2 years. While this is significant, it underestimates the total impact of improvement in manufacturing technology, since as argued above, it neglects incidental quality improvements associated with smaller feature sizes not captured in price per transistor.

Furthermore, the indications are that the relative importance of manufacturing technology improvement in microprocessors has greatly increased in the past several years. This is because microprocessors hit a “brick wall” associated with power and heat dissipation in 2003-2004, reducing the rate at which processor speeds have since increased over time.

Rather than adding qualitatively new capabilities and features to microprocessor architectures, the current emphasis is on replicating and linking multiple microprocessors (multiple “cores”) on a single chip, as the primary direction for continuing utilization of the cheaper transistors flowing from manufacturing innovation. From a software perspective, using multiple cores on a single task is inherently more difficult and demanding, than speeding up the rate at which a single processor operates. Indeed, the difficulties of writing software that easily coordinates multiple processors on a single problem form the critical bottleneck for current research on design of supercomputers.18 One would therefore expect

the problem of writing software for multiple core microprocessors to increasingly dominate the perceived benefits of higher numbers of cores on processors, and for economic measures of decline in the quality-adjusted price of microprocessors to slow as these problems increasingly dominate the utilization of the cheaper transistors supplied by continuing manufacturing innovation in microprocessors. Ironically, perhaps, scalable solutions to the problem of harnessing the power of multiple processors on a single task, which now pace cutting edge research on supercomputers, will now become a major issue for microprocessors.

After a sharp reduction in the rate at which prices were declining over 2003-2005, the rate of decline in quality-adjusted microprocessor prices rebounded and is currently declining at a rate where most of the price decline can be attributed to cost-improvement associated with the introduction of new technology nodes. Thus, in microprocessors, the poster child for rapid improvement in semiconductor price performance over the past decade, the role of the shift from a 3-year to 2-year technology node cycle played a significant but not predominant role in accelerating innovation in the late 1990s and early 2000s. Currently, however, manufacturing innovation is relatively more important than in the 1990s, accounting for the vast bulk of continuing decline in quality-adjusted microprocessor prices. Thus, it seems reasonable to propose that the relative economic importance of manufacturing innovation in semiconductors more generally and, therefore, of R&D coordination through institutional mechanisms like the ISTR and the current crop of global R&D consortia has increased substantially.

CONCLUSION

The 2-year cycle for the introduction of new technology nodes remains a feature of recent roadmaps, which continue to call for a reversion to the slower-paced 3-year cycle in later years. Calls for a slower cycle have mainly gone unanswered.

Before there was a roadmap, semiconductor companies organized their technology planning around something approximating Gordon Moore’s prediction of a doubling of transistors per integrated circuit every 18 months. As it continued to hold approximately true, companies organized technical plans around the Moore’s Law timetable. This was not because that schedule necessarily maximized their profit but because they believed that all their competitors would be introducing new products and technology on the Moore’s Law schedule, and that they too had to stick to the plan to stay competitive.

This changed in the 1990s, when the U.S. SEMATECH consortium sponsored the roadmap coordination mechanism in pursuing its goal of technology acceleration. By explicitly coordinating an increasingly complex array of decentralized pieces of technology, requiring simultaneous improvement to create a new generation of manufacturing systems, the roadmap appears to have succeeded in altering the tempo of innovation. This effort was extended and internationalized, and today

it is a unique and important institutional feature of the industrial organization of the global semiconductor industry.

Indeed, the industry’s unsuccessful (to date) efforts to get off the “technology treadmill” and return to an older, slower pace of technological change in roadmaps for the end of this decade may indicate that the acceleration impulse, once launched, cannot easily be damped. An individual company gains no competitive advantage if it slows innovation and is matched by the rest of the industry, whereas it may lose greatly if the rest of the industry continues at the original, faster pace.

The speedup in manufacturing innovation, we have seen, was felt across the breadth of the semiconductor industry. Even in microprocessors, where rates of price decline greatly outpaced most other products, the acceleration of node introduction played a significant, if not predominant, role in the late 1990s and early 2000s. Currently, the introduction of new technology nodes seems to have become the primary driver of quality-adjusted price declines in microprocessors.

Economists are largely accustomed to thinking of the speed of technological change as something that is exogenous, dropping in gracefully from outside their models. One moral of the history of SEMATECH and the technology roadmap is that the pace of technological change may have an internal policy component as important as its external scientific foundations. Particularly where many complex items of technology secured from a broad variety of sources must be coordinated in a fairly precise manner in order to create economically viable new technology platforms, vague and diffuse factors like expectations and even political coalitions may play an important role.

REFERENCES

Aizcorbe, A., K. Flamm, and A. Kurshid. 2002. “The Role of Semiconductor Inputs in IT Hardware Price Decline: Computers vs. Communications.” Federal Reserve Finance and Economics Discussion Paper 2002-37. Washington, D.C.: The Federal Reserve Board of Governors. August 2002; revised 2004.

Aizcorbe, A., S. Oliner, and D. Sichel. 2006. “Shifting Trends in Semiconductor Prices and the Pace of Technological Progress.” Federal Reserve Board Finance and Economics Discussion Series Working Paper No. 2006-44. September.

Browning, L., and J. Shetler. 2000. SEMATECH: Saving the U.S. Semiconductor Industry. College Station, TX: Texas A&M University Press.

Clarke, P. 2004. “LETI, Crolles Alliance Open $350-million 32-nm Research Fab.” EE Times April 24, 2004.

Clarke, P., M. LaPedus and M. Santarini. 2005. “IBM-led Consortium to Build Fab in N.Y.” EE Times January 5.

De Proft, A. 2006. Presentation at symposium on “Synergies in Regional and National Policies in the Global Economy.” Leuven, Belgium. September.

Flamm, K. 2003. “Microelectronics Innovation: Understanding Moore’s Law and Semiconductor Price Trends.” International Journal of Technology, Policy, and Management 3(2).

Flamm, K. 2003. “The New Economy in Historical Perspective: Evolution of Digital Technology.” in New Economy Handbook. St. Louis, MO: Academic Press.

Flamm, K. 2006. “The Economics of Innovation in Microprocessors.” Draft. December.

Hennessy, J. L., and D. A. Patterson 2002. Computer Architecture: A Quantitative Approach. 3rd Edition. San Francisco, CA: Morgan Kaufmann Publishers Inc.

Jorgenson, D. 2001. “Information Technology and the U.S. Economy.” American Economic Review 91(1). March.

Jorgenson, D., and K. Stiroh. 2000. “Raising the Speed Limit: U.S. Economic Growth in the Information Age.” Brookings Papers on Economic Activity. G. Perry and W. C. Brainard, eds. Washington, D.C.: Brookings Institution Press.

Nanotechwire. 2005. “Governor Pataki Announces Historic Investments by IBM Global High-Tech Leaders in Nanoelectronics Manufacturing and Development.” January 6. Accessed at <http://www.nanotechwire.com/news.asp?nid=1453>.

National Research Council. 2003. Securing the Future: Regional and National Programs to Support the Semiconductor Industry. Charles W. Wessner, ed. Washington, D.C.: The National Academies Press.

National Research Council. 2004. Getting Up to Speed: The Future of Supercomputing. Washington, D.C.: The National Academies Press.

National Research Council. 2004. Productivity and Cyclicality in Semiconductors: Trends, Implications, and Questions, D. W. Jorgenson and C. W. Wessner, ed. Washington, D.C.: The National Academies Press.

Purvis, G. 2002. “Moving into the Real World.” Electronic Business July 1.

Semiconductor Fabtech. 2005. “IBM & AMD Aim Alliance at the 22nm Frontier.” November 1.

Semiconductor Fabtech. 2006. “IBM and Partners Ready 45nm Low Power Process.” August 30.

Semiconductor Fabtech. 2006. “IBM, Sony, Toshiba Take Technology Alliance Beyond 32nm.” December 1.

Spencer, W. J., L. Wilson, and R. Doering. 2004. “The Semiconductor Technology Roadmap.” Future Fab International 18.