Panel I

Partnering for Photovoltaic Technologies

Moderator:

Congresswoman Gabrielle Giffords (D-Arizona)

Congresswoman Giffords said that many people assumed that her strong support for photovoltaic technologies was a reflection of representing the 8th Congressional District, in the southeast corner of Arizona. While it is true that her district receives more sun than most, she said, the entire country has abundant solar energy. Yet the country leading the world in deployment of PV, she said, was Germany, “which gets about as much sun as Anchorage, Alaska. So the United States has a natural advantage when it comes to solar.â€

She said that she thinks about three “serious global challenges†every day on the way to work: (1) Foreign energy dependence: How have we reached this condition, and what resources do we need to break this dependence and ensure our energy supply in the future? (2) Climate change: How fast is the globe warming, and how might climate instability lead to real problems for the United States and the world? (3) How can the decline of the U.S. economy best be reversed so as to ensure our economic competitiveness?

“The great power of solar energy,†she said, “is that it provides elegant solutions to each of these three critical problems.†It addresses energy independence, she said, by reducing the nation’s use of foreign energy; it helps stabilize the climate by producing power without increasing carbon dioxide in the atmosphere; and it promises to contribute to economic competitiveness by creating new jobs in solar-related industries.

She, like Senator Udall, emphasized that the United States was not alone in recognizing the economic potential of solar energy. The country has historically been a leader in solar technology, she said, but it is not a leader in PV manufacturing. She said that she hoped the symposium would provide guidance on how to create that leadership.

OVERCOMING POLITICAL RESISTANCE

One of the most daunting barriers, Congresswoman Giffords said, is political resistance. “The lobbyists for renewable energy are far outnumbered,†she said. A survey by the Center for Public Integrity of self-identified lobbyists working on climate questions reported that only 1 out of 10 lobbyists actually identified themselves as interested in renewable energy. She summarized the amounts spent by various energy lobbies during the first quarter of 2009, as follows: American Petroleum Institute, $1.9 million; British Petroleum, $3.6 million; Marathon Oil, $3.4 million; Conoco Phillips, $5.9 million; Chevron, $7 million; Exxon Mobil, $9.6 million. The American Coalition for Clean Coal Energy has an annual budget of $45 million. For renewable sources of energy, the wind power lobby spent some $1.6 million in the first quarter, and SEIA, the solar energy lobbying effort, spent $410,000.

“This is what we’re up against,†she said. “I’m not putting this up so we can get discouraged, because obviously with few resources, the solar industry has made tremendous strides. But now we have to figure out how to get this technology out there and installed and making a difference for our country and our world.†To do this, she suggested that supporters should “organize, advertise, and educate.â€

“I know that the solar resource in the United States is greater than the fossil resource,†she said. “And I know that it’s ecologically and economically feasible for solar to be a major power generator. But many of my colleagues don’t know this—primarily because they just don’t have the information.†She urged her audience to communicate more directly and aggressively with Congress and others in positions of influence.

She closed by observing that much of the effort currently expended by solar companies is directed at demonstrating the strength of their own particular technologies. While this is essential, she said, the PV industry is unlikely to achieve its potential without more collaboration between all solar companies to educate the public about the solar opportunity. She said that in Arizona, her office makes education a key part of its solar strategy. They offer “Solar 101†classes to the public at schools, libraries, and other locations to explain how the average consumer can benefit from solar installations at their home or business. She has created a “Solar Hot Team,†consisting of solar leaders from across Arizona that engages in weekly check-ins to share information and insights on recent developments.

“The bottom line,†she said, “is that we have a lot to do. Some of my frustration with the technology folks getting into clean energy is that they have not fully appreciated how energy is different from Silicon Valley and the computing industry. Many of them have not understood the challenges of going into these very traditional energy markets, where they have to deal with regulations at the federal, state, and local levels. Add to that the fact that the lobbying power of

traditional energy industries is enormous. Ensuring adoption of solar power is not just about price or level of technology; it’s also about culture, politics, and figuring out ways to get into the system. People must understand all of these issues before we can make the really necessary changes.â€

U.S. PHOTOVOLTAIC ROADMAP:

PERSPECTIVE OF THE MANUFACTURING INDUSTRY (1)

Subhendu Guha

United Solar Ovonic (Uni-Solar)

Dr. Guha’s company, Uni-Solar produces flexible thin-film panels of amorphous silicon. These light-weight products, he pointed out, are well suited to large-area installations such as rooftops. He put on view a photograph of world’s largest rooftop system, a 12 MW Uni-Solar installation in Zaragoza, Spain. Further illustrating the potential of thin-film panels, he also displayed a photo of the “Zephyr airship,†which had set a record for the longest flight in the stratosphere powered by solar energy.

Uni-Solar, he said, wholly owned by Energy Conversion Devices, is the world’s largest manufacturer of flexible solar cells. It makes its solar cells by a roll-to-roll manufacturing process based on thin-film silicon multijunction technology. The company is relatively small, with manufacturing plants in Michigan that employ about 1,000 people, but it has been growing rapidly. In 2003, it shipped less than 5 MW of product; in 2008, it shipped more than 100 MW of product.

Flexible Rooftop Products

Its flexible rooftop products are made as 18-foot-long laminate with a paper-lined adhesive on one side. When the rolls arrive at an installation site, the paper is removed and the material is attached directly to the roof or other surface, greatly reducing installation cost.

Dr. Guha reviewed some key events of the company’s history and early commercialization. From the beginning, the technological concept was to pass a roll of stainless steel through machines where successive layers of the solar cell are deposited. The first prototypes were built in 1981. In 1986 came the first prototype plant, producing 500 kW of capacity a year, and in 1991 came a plant with 2 MW of capacity.

“In those days,†he said, “amorphous silicon was an unknown entity, and no one knew how well the products would work.†They sent samples to NREL, and found that it performed as projected. NREL continues to evaluate Uni-Solar products, which “has given us and our customers a lot of confidence that you can have product that is going to last 20 to 25 years.â€

At around the same time, the company started developing new triple junction solar technology to achieve higher efficiency. It built its first 5 MW production machine in 1996 using a triple junction processor, and began to see that these flexible products could be applied to rooftops. In 1997, Uni-Solar made its first building-integrated PV (BIPV) demonstration and continued to grow. In 2003, they built their first 30 MW production line, in Auburn Hills, using six rolls of stainless steel, each 1.5 miles long. In 60 hours, he said, the plant can make nine miles of solar cell. Today the company has expanded to about 180 MW of capacity, including a production line opened in Greenville, Michigan, in 2007.

During this time, the world market has grown steadily from about 1,000 MW in 2004 to more than 5,000 MW in 2008. The remarkable growth in the last three years, he said, was the product of feed-in tariffs and other incentives offered outside the United States. Of the 5,000 MW worldwide solar market in 2008, he said, just over 300 MW was sold in the United States; Germany, helped by the feed-in tariffs, sold six times that amount.

Incentives Offered by Other Countries

One reason incentives are offered by some countries, Dr. Guha said, is that solar power is not yet competitive with the large power stations producing electricity from conventional fuels. Germany offers incentives ranging from 41 cents per kilowatt-hour to 51 cents/kWh. France offers about 40 cents/kWh; for BIPV they give about 70 cents/kWh. Many of the incentives have a downward scale, dropping every year. The incentives work because they allow construction of large manufacturing plants. As these plants bring economies of scale, their costs come down. The incentive for rooftop solar systems is higher because in many urban areas there is insufficient vacant space for crystalline silicon PV installations, so this kind of incentive is meant to hasten the use of otherwise unused roof area. It also avoids transmission losses, with electricity generated at the point of consumption.

Dr. Guha made a strong economic case for PV usage. He said that deployment of 100 MW of PV to electrify 200 commercial buildings or schools could create some 2,400 green jobs. He said that Germany, which has traditionally been the auto capital of Europe, today employs fewer people in the auto industry than in the PV industry, which has created 180,000 new jobs. “And Germany has no more sunlight than my state of Michigan,†he added. “If it can be done in Germany, I’m sure it can be done in every state in the United States.â€

Costs Are Coming Down

Dr. Guha repeated that the industry was not yet cost-competitive, but said that the price was coming down. In 1990, the cost of solar power ranged from 40 to 80 cents/kWh. Today, he said, costs are much lower, in some places cost-competitive with conventional electricity at peak usage times. According to the DoE, he said,

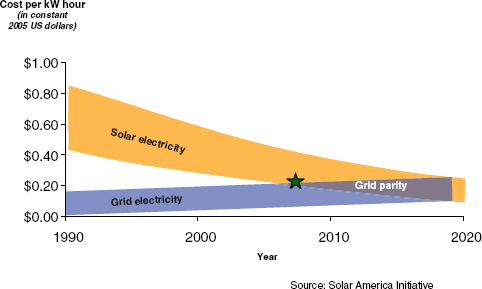

FIGURE 1 Challenge for PV: How to reach grid parity.

SOURCE: Subhendu Guha, Presentation at July 29, 2009, National Academies Symposium

on “State and Regional Innovation Initiatives—Partnering for Photovoltaics Manufacturing

in the United States.â€

PV can generate electricity in California for 20 cents/kWh, which is on a par with peak-time prices. “We are just there,†he said. “For many residential users, they have time-of-day pricing that is more than 20 cents.†He noted that pricing is subject to wide disparities, depending on the amount of sunshine and other factors. “But we still have to come down farther,†he emphasized. “The PV manufacturers do not want to depend on subsidies. We want to stand on our own feet. We want to reach grid parity, and we have shown that we can make progress toward that goal.â€

The way to reduce the cost of PV, he said, is to work with the entire PV value chain. “You make the solar cell, then you make the module, which is interconnected solar cells; then the PV array, for which you need inverters and other components to convert the DC solar electricity to AC current. Finally, you sell it to the customer. Through it all, you have to hear the voice of the customer. You cannot just work on materials, or solar cells. You need the big picture. What does the customer want? Most of them want to know how much money they are going to spend to put the PV on the roof, and how much electricity are they going to get over the next 20 years. In any innovation we do, we must focus on that: how to reduce the cents per kilowatt-hour.â€

Crucial Role for Government

In addition, Dr. Guha said, the government has a crucial role in bringing the industry to grid parity. That role is to help create a sufficient demand base through

incentives and grants. The United States can have the best technology in the world, he said, but if it does not have a demand base, it will not create manufacturing jobs. At present, U.S. companies are building plants in Europe—because the demand is there. He also stressed the need to remove barriers, develop uniform codes, and improve net metering.

He argued that industry has done its part in moving PV toward maturity. “When you talk about needing new R&D to reach grid parity,†he said, “I have a bone to pick. We talk about new, disruptive technologies, about how we have to think out of the box. We have been thinking out of the box and developing disruptive technology for decades. Now is the time to build on the foundation we have established. I am not opposed to doing something new, because there is no single choice; there will be many choices. But what industry has already done to reduce costs is phenomenal. And they will continue to do that. There will be both challenges for the established technologies, and challenges for the new technologies.â€

To extend his discussion of building on what exists, he emphasized the system as a whole. He recalled the late 1990s and early 2000s when government focused its funding on components. Around 2005, however, the emphasis shifted to a more integrated, program-oriented approach that brought industries, universities, and national labs into collaboration. “Trust me,†he said, “this was not easy. Academia does not want to be told by industry what to work on. But slowly we accepted each other, and it was a wonderful experience to see a bunch of people with diverse backgrounds working together toward common ground.†Slowly what was understood, he said, was that a focus on components was not sufficient. A systems approach was needed to reduce the cost. “For the first time, the main topic was not how do you increase the efficiency of a solar cell, or an inverter. It was how do you reduce the cost of electricity, which is well underway.â€

He concluded by noting that “clean electricity is not a choice—it is a necessity. We cannot afford to pollute the world with greenhouse gases.†He quoted the words of the historian Edith Hamilton, who wrote about Athens, “ ‘In the end, more than they wanted freedom, they wanted a comfortable life, and they lost both comfort and freedom.’ When the Athenians wanted not to give to society,†he said, “but for society to give to them, when the freedom they wished for most was freedom from responsibility, then Athens ceased to be free. We cannot afford that.â€

PERSPECTIVE OF THE MANUFACTURING INDUSTRY (2)

David Eaglesham

First Solar

Dr. Eaglesham said he would give the industry’s perspective on both current and anticipated future conditions for photovoltaic technologies. He showed an opening photo of a 10 MW First Solar installation in Boulder, Nevada, that feeds the Southern California Edison grid. “This is an example of a type of installation

FIGURE 2 PV industry has grown to GW scale and <$1.00/W.

SOURCE: David Eaglesham, Presentation at July 29, 2009, National Academies Symposium on “State and Regional Innovation Initiatives—Partnering for Photovoltaics Manufacturing in the United States.â€

that’s becoming possible,†he said. “We can do multiple installations of this size. This is a fairly significant contribution even at today’s scale.â€

He began with a skeptical assessment of various goals that had been suggested for solar and other renewable sources of electricity, such as a global capacity of 5 terawatts for renewable sources by 2020, projected by the International Panel on Climate Change. “Think about the growth rate you would need to get even close to that goal. If you want PV to be even a small component, it would have to grow at an astonishing rate of about 70 percent annually. I do not believe that any industry has grown at a sustained growth rate of 70 percent compounded annually. The real question is how big a piece should solar be of the U.S. energy mix, and what can we do to make PV play the biggest possible role.â€

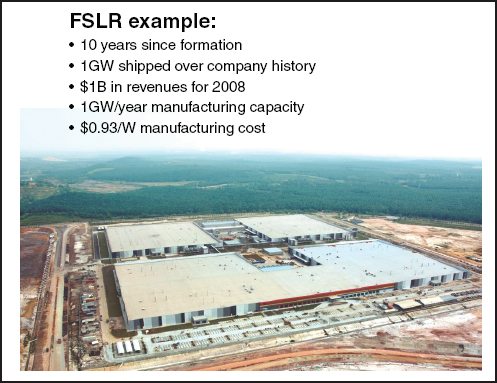

The PV industry has just recently reached gigawatt size, he said. “It is still juvenile, at a technically early stage,†he said, “but it has become a real industry.†He said that First Solar itself is now producing a gigawatt a year of manufacturing capacity, with a fully operational 800 MW factory in Malaysia, and had surpassed

$1 billion in sales in the previous year. The company had also lowered manufacturing costs to 93 cents a watt in the previous quarter’s actual results.

A Plea for Incrementalism

Dr. Eaglesham said he wanted to emphasize several messages. The most important, he said, was a “plea for incrementalism.†If you hit “reset†and start the industry again from scratch, he said, then even a 70 percent compound annual growth rate would not achieve 2020 goals. It was necessary to move ahead from the current industry baseline to reach such a goal, rather than expecting some “disruptive†technology to set the industry on a new course.

“We have a technology that’s in hand,†he said. “I’m citing First Solar data because I’m from First Solar, but there are other companies with comparable costs, improvement targets, and expansion targets. It is my expectation that multiple companies will be able to achieve this kind of cost and scale in a short time. We have a technical solution in hand, and a cost point that gets us to where we need to be to drive toward the 2020 goal. Let’s keep pushing forward in that direction.â€

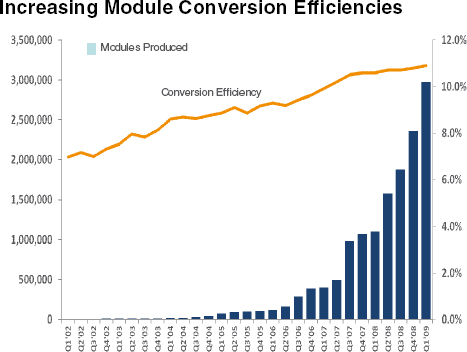

The primary reason why First Solar is able to contain its costs, he said, is that “it doesn’t change technology every couple of years.†Manufacturing learning, he said, drives continuous improvement. “This is boring for academics,†he said, “but critical for an industry—just regular old learning, cranking the handle, grinding on continuous improvements. It’s a key piece of why you want to stick with things that leverage existing production platforms.†He illustrated the company’s increasing module conversion efficiencies with a graph showing a rapid rise in efficiency from 7 percent in 2002 to about 11 percent at present. (See Figure 3 on Increasing Module Conversion Efficiencies.)

Costs Have Been Dropping Steadily

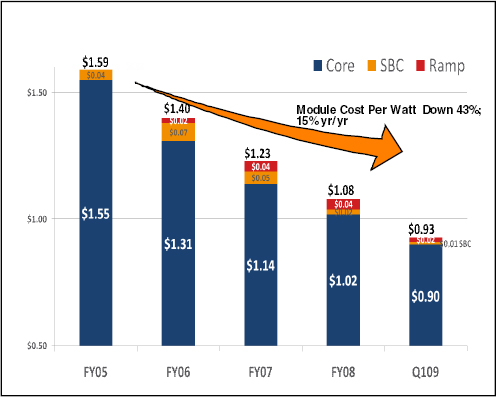

At the same time, costs has been dropping steadily, with the module cost per watt lower by 43 percent from FY2005 through the first quarters of FY2009, or an average decrease of 15 percent per year. “Again,†Dr. Eaglesham said,†First Solar happens to be first out of the gate, but my expectation is that multiple companies in this room are going to have a downward cost curve like this, if a little behind. I think there’s a clear message that you don’t have to radically reinvent the technology.â€

He paused to clarify his message about R&D. “Long-term R&D is needed to bring the new technology for manufacturing in the year 2020, so we need to do that as well. But it’s important to continue the investment in these more incremental stages.â€

Dr. Eaglesham turned to the company’s future cost reduction roadmap, which projects the cost per watt at the module level as falling from 93 cents at present

FIGURE 3 Manufacturing learning drives continuous improvement.

SOURCE: David Eaglesham, Presentation at July 29, 2009, National Academies Symposium on “State and Regional Innovation Initiatives—Partnering for Photovoltaics Manufacturing in the United States.â€

to about 52 cents in 2014. There is also a comparable roadmap for the balance of system components, he said. “When you add those two things, you have a business plan that gets you to where you need to be in terms of grid parity.â€

Toward a Sustainable Market

Dr. Eaglesham then discussed the point at which the rising global PV demand line crosses the falling PV cost line to enable sustainable markets. The lines had already crossed for natural gas peaking prices, he said. For other sources of energy, including coal, gas combined, and nuclear, the crossing point might be around 15 cents/kWh, depending on the number of sunny days per year, a price placed on carbon emissions, the cost of capital, and other factors. A critical variable, he said, stems from the value proposition inherent in all forms of renewable energy: that the consumer must pay up front for the entire system—in return for free energy for the lifetime of the system. Therefore, both interest rates and availability of financing are key determinants of the crossing point to grid parity and the rate of end-user adoption.

FIGURE 4 Improvements are delivering cost reductions.

SOURCE: David Eaglesham, Presentation at July 29, 2009, National Academies Symposium on “State and Regional Innovation Initiatives—Partnering for Photovoltaics Manufacturing in the United States.â€

He said that First Solar had already projected substantial growth in its planned or contemplated gigawatts of PV in the U.S., rising from about 50 GW in 2009 to 760 GW in 2013. “We are projecting big markets,†he said. “We have a pipeline of projects already under discussion with utilities.â€

Another significant feature of PV development, he said, is the development timeline. This line is now quite long, primarily because of the permitting cycle, which is now about two years. He made a strong plea for government policy makers to work toward reducing this cycle so that PV can be more responsive to market demand. The government can also take other steps in setting policy, he said, including simplifying rules and regulations and creating a national renewable electricity standard (RES). Dr. Eaglesham noted that other governments, notably the European Union, China, India, and Australia, have all taken significant steps to encourage PV and other renewable energy development.

“It is already clear that the market will follow the manufacturing,†he said, “and the technology is going to follow the market.†Market location, in turn, is

driven by the decisions of regulatory agencies in each country. It is also driven by the cost of freight, since glass products are heavy and expensive to ship. “For this reason,†he said, “glass manufacturing is almost invariably done where it is going to be installed. I already have a barrier in importing product into Europe from Malaysia.â€

According to Dr. Eaglesham, U.S. energy policy should address the needs of three distinct phases of PV development. The first is R&D. The goal of a commercially viable technology should be supported by fundamental R&D, applied R&D, concept/pilot lines, and alpha products.

The second phase, commercialization, must support technologies of proven value. “We have to be careful here to simulate development without picking the winning technologies. This must be driven by the marketplace.â€

Finally, the stage of scale-up should focus on commercially proven technology. “The critical piece is to develop the programs that will pull from the market. We need markets to enable efficient scale up, execution capability, and growth capital. The federal role is to provide transparent and attractive market opportunities that do not favor selected technologies. They must also provide market longevity and volume, market price and program guidance, and incentives for project finance.â€

Beginning Technology Development with Market Pull

Usually, Dr. Eaglesham said, technology development is regarded sequentially; the process starts with R&D and works its way “forward†toward the market. “But for PV,†he said, “if you think about how you’re going to structure incentives, you want to work the whole thing backward. If you start with R&D and get to the end to find there is no market, all you have is a train wreck. So you begin with market creation so that the market pulls the technology from that side. A large, well-structured solar market drives investment and innovation.â€

Dr. Eaglesham offered a summary of main points:

• Current PV technologies are close to grid parity in locations of high and medium irradiance. “Our expectation is that we can drive the existing technology base to a place where it can be successful, so we want to invest in continuous-improvement pathways.â€

• The DoE can help relieve major challenges, such as slow and nonuniform permitting requirements, lack of grid-connection technology, and the need for federal renewable electricity standards. Other needs include incentives and loan guarantees at the utility level; demonstration-scale electricity storage programs; and nonblocking intellectual property provisions for basic research.

• DoE’s support for PV should be sustained from a technologically agnostic stance, implementing programs without picking winners.

• Although the PV companies are not ready to set technology-level

standards, they can benefit by collaborating on such tasks as permitting reform and system-level development.

He closed by urging universities and national labs that would like to partner with industry to be more sensitive to the question of intellectual property. “I would urge people to think about programs where industry comes to table and directs the research toward industry problems while protecting the IP,†he said. “This is a difficult conversation to have with most academic institutions right now. I only work with the ones that are prepared to work with that kind of framework.â€

DISCUSSION

Professor Zweibel continued the discussion of incrementalism, noting a substantial gap between developmental research to improve today’s technologies and reaching for “blue-sky†findings whose payoff might be 20 or 30 years away. “What we’ve heard in the presentations is that there’s a lot of momentum for very low-cost goals.†He asked whether the panelists had experienced that disconnect in terms of how R&D is done or funded.

Building on Existing Architectures

Dr. Eaglesham agreed that disruptive device architectures will be needed in the future. “But I think there’s enormous opportunity for research in materials physics and the device physics of existing architectures. In the same way, the semiconductor industry did a lot of great basic research to understand its basic materials phenomena. I would just make sure that second piece doesn’t get left out.â€

Dr. Guha recalled that in 1875 the U.S. patent commissioner recommended the abolition of the patent office because “all the inventions had already been made. We don’t want to take that path. But I also don’t want to take the path that whatever has been done cannot lead us to the goal. There has to be basic research, there has to be focused research, and I think some of the programs of DoE show that academia and industries can work together toward a common goal.â€

Dr. Eaglesham said that the “goal†for him would be to maximize the share of PV in the mix of renewable energy forms by 2020 or 2030. “If that goal was set for 2080,†he said, “it might make sense to have a larger portion of investment in finding blue-sky or radical device innovations. What makes this different for me is that we have a pressing, pragmatic near-term goal towards which we are collectively driving. I would urge people to think about how short a time that is. There is enormous value in exploring, say, the long-term nanotechnology aspects of these things, which we need, but as a country we would be making a big mistake if all we see out there is these radical third-generation things.â€

Congresswoman Giffords reiterated her concern that the solar industry was neglecting opportunities to communicate its message to members of Congress and other policy makers. She recalled the recent debates on the cap-and-trade bill, when the hallways outside committee hearing rooms were packed with lobbyists from traditional energy companies. “Where was the solar industry?†she asked. “All of us in this room have the ability to come down and advocate for this technology, but we were not there. We have a good goal, but we are up against some pretty powerful forces.â€

The Issue of Standards

Obang Yew of NIST raised the issue of setting standards for the PV industry, noting the success of SEMATECH in doing so. If the goal of industry is 70 percent annual growth,†he asked, “how do you get there without standards?â€

Dr. Eaglesham agreed that some standards do exist and that they are critical. “The PV industry is simply not mature enough to set some of them right now.†He said that the semiconductor industry had a natural collection of standards that began with wafer size and wafer-handling equipment, “and spread out from there. The standards bodies have played a huge role in helping that industry be successful. With solar, there is no standard interface for putting a steel roll into my glass-handling equipment. It’s purely a practical issue.†He added that for the same reason, there were few opportunities to work together on precommercial R&D.

Marie Mapes of the DoE followed up on Dr. Eaglesham’s mention of collaboration among various parts of the industry, asking him to elaborate. He said that some research on basic device models is common to different firms, such as optical modeling, as are areas of total cost of ownership analysis. But it is still difficult to find common themes in precommercial research, he said, “because this industry is still burgeoning many directions, which is a strength as well as a weakness.†Dr. Guha added that the industry—especially the silicon area—could take pride in the fact that partnerships among industry, academia, and national labs had been successful. “We have learned to understand each other’s language, to understand that academia can do exciting work—even though it is focused work—and that academia can help us. The main issue is respect for each other, and once you develop respect you can achieve many things.â€