Panel V

Building a Solar PV Roadmap

Moderator:

Clark McFadden

Dewey & LeBoeuf LLP

Mr. McFadden opened the panel discussion by commenting on the controversial nature of a solar PV roadmap. Although the concept seemed straightforward, he said, it was commonly misunderstood and even resisted by some participants. He welcomed the presence of a “knowledgeable and experienced†panel to examine the function of roadmapping, and whether it can be useful for the PV industry.

Ken Zweibel

George Washington University

Professor Zweibel said that the purposes of building a roadmap for the photovoltaic industry had been well stated: to accelerate PV progress to meet critical national needs, do so in a cost-effective manner, and reduce deployment risks. “If we’re going to be deploying terawatts of renewable energy,†he said, “including terawatts of solar energy, we want to do that as robustly and cost-effectively as possible.†And a roadmap capable of guiding robust deployment, he said, would need to address both technology push and market pull.

The Challenge of Setting Goals

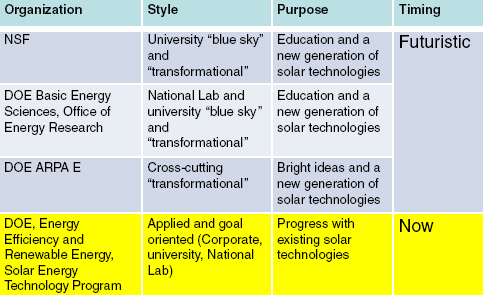

Professor Zweibel began with what he saw as a misunderstanding about setting goals for PV research. Within the federal government, he said, much of the PV R&D is “futuristic,†in the sense that it is focused on the next generation of technologies. The organizations supporting this “blue-sky†and “transformationalâ€

research include the National Science Foundation, and the Department of Energy’s Basic Energy Sciences and Office of Energy Research, and DoE’s ARPA-e. The DoE’s EERE program, by contrast, had long supported the technical work in PV that is not futuristic, work that has led to a multibillion-dollar industry in the U.S. and to world leadership in some technologies.

Here, he said, is a disconnect. “Some people are still fighting the last war,†he said, “answering the questions from 5, 10, and 15 years ago. To them, PV is an industry that is not cost-effective. They are not seeing that the goals in their minds, like a dollar a watt cost per module, have already been achieved. We’re in a world where things have changed. Some of us are making choices to focus on futuristic things when they should be enthusiastic about the out-of-the-box successes of existing technologies.†He said that one reason for this disconnect is that PV is such a fast-moving field; the technology has progressed even as people have worried about it.

Toward a Stair-Stepped Program

Professor Zweibel also saw a danger in placing too much emphasis on the “magic†of start-ups. “We’re still in the belief phase, where start-up work is so wonderful and it’s all going to work overnight,†he said. “That just hasn’t been true historically.†The lesson of 25 or 30 years of work in this field, he said, and in other fields of technology, is that even well-funded start-ups seldom have immediate commercial results. “We should be doing a stair-stepped program, where we have faith in today’s technologies, good understanding of their potential, and room for other technologies as they mature. We should not abandon key technologies just because they are commercial, because they still retain huge knowledge shortfalls. We are just getting on the first step of the stairs with leading PV options like CdTe, CIS, and even crystalline silicon.â€

He suggested, therefore, that the first solar roadmap be designed to help the Congress, DoE, and the new administration understand the immediacy of the solar opportunity in existing technologies. These technologies have already proven they can reduce costs steadily to levels appropriate for cost-competitive electricity. “If we’re going to be doing futuristic work,†he said, “we should acknowledge that those ideas will take another 20 years, and we should plan accordingly. We should not act as if all these good ideas of the last 30 years didn’t occur and are not important.â€

Costs Really Are Coming Down

Turning to actual costs, Professor Zweibel reminded participants that “generation one and two†technologies—silicon and thin films—were going into large systems at $4 a watt. A few years ago, they cost $6 a watt, and a few years before that, $10 a watt. “Those are phenomenal cost reductions,†he said, “and the goal

FIGURE 16 Government R&D 2009.

SOURCE: Ken Zweibel, Presentation at July 29, 2009, National Academies Symposium

on “State and Regional Innovation Initiatives—Partnering for Photovoltaics Manufacturing

in the United States.â€

of $2 a watt seems certain. I want to bite my tongue when I say that, but enough people have said it that it seems to be coming for a big installed system.†He mentioned advertisements by solar installers already offering $3 a watt at installations of megawatt size, and said that progress to $1.50 or even $1.25 a watt seems possible with existing technologies.

“I want to say that 30 years ago, when we at NREL started developing these cost analyses, we were regarded as stupid and naïve when we said that $1 a watt systems did seem possible. I want to tell you that we were just naïve (due to the time and money it would take to get there). The fact that we might be getting close to $1 almost stops my heart, it really does. But it seems like it can really be stated now, after 30 years.â€

Generation two, he went on, would include both thin films and concentrators,13 both of which are at or near commercial status. Generation three, he said, should be regarded as tools that eventually cut costs in half again. “We should think about systems at 50 cents a watt and below; we should make it a hard goal, not a duplicate of the goal that is already happening. Also, new technologies can be integrated into existing systems. We already do this with nanoparticle inks and

____________________

13Concentrating solar power (CSP) systems use lenses or mirrors and tracking systems to focus a large area of sunlight into a small beam.

we have for 15 years. We can do special nano absorbers in these materials to raise their efficiencies. But expecting that some kind of weird thing is going to come out of the blue and make everything different—that’s naïve again, for the same reason—time and money.†Deployment of third-generation technologies could be 25 to 40 years away, he said, though it will happen. But more importantly, “we do not need them for PV to become cost-competitive.â€

A PV Roadmap with Two Levels

With these considerations, Professor Zweibel suggested a PV roadmap with two levels. The main funding would go to the first level, and would include existing EERE-supported commercial technologies with proven potential to make low-cost goals. These include crystalline silicon PV, cadmium telluride, copper-indium-selenide (CIS) alloys, gallium arsenide multijunctions for concentrators, and thin-film silicon. The second level, with much less funding, would be a smaller category of post-proof-of-concept cell results for third-generation options like plastic cells whose progress has been sufficient to attract initial private support. The content of this category would be outside the EERE portfolio and would change steadily, which he called “important for program evolution.†But this support should not outweigh the applied R&D support of the leading commercial technologies, because these are just starting their cost reduction phase, where such funding would be highly leveraged. “Society expects us to succeed with these technologies, not dither away the opportunity.â€

He suggested several points as a “technical roadmap philosophy.†Cost goals, typically in cents per kilowatt-hour, had always focused first on module development, because modules and their efficiency account for most of the system cost. This goal is currently about five cents/kWh. Below the module, he said, was the secondary cost goal of about a few pennies per kWh for the inverter and BOS designs, grid integration, sustainability, ESH, and other less-technical sectors. A significant nontechnical goal, he said, was to reduce the procedural delays prior to actually putting PV in the ground. It can take 18 months or so in immature markets like the U.S. for the permitting process, he said.

In addition to addressing cost objectives, he said, goals should be “high-level and light-handed.†They should include efficiency, cost per unit area, and reliability, and reaching them should “allow creativity just below the top-level goals. Don’t tell people how to do things, ask for their best ideas. Be aware of the breadth and patience needed to achieve them, not the immediacy of the expectations of less-experienced evaluators.†He said that a roadmap process should include the element of continuous improvement and criticism. There should be open meetings, he said, where “people could throw brickbats at the current roadmap. Instead of defending ourselves against new ideas, we should enjoy and incorporate them. This could prevent the roadmap from becoming onerous, because there would always be opportunities to change it.â€

Identifying Pinch Points Along the Critical Path

Any good roadmap should identify not only the critical path, Professor Zweibel said, but also key “pinch points,†whether for a module technology, a BOS, or permitting procedures. These can represent a consensus within the technologies. For example, for cell efficiency, pinch points might be voltage, doping, and contacting, as in CdTe PV. For a module, they might be interconnection resistance and maximum active area. Once the roadmap is laid out, the funding organization can develop an RFP by understanding both the pinch points and capabilities necessary to meet them. The RFP would go nationwide to universities, national labs, and companies.

In conclusion, he said that the first—and most important—high-level roadmap should be one that the DoE, the Obama administration, and congressional committees would be able to understand, “especially in regard to the message that we do not need to start from scratch with revolutionary technologies. We can succeed through incremental progress on the technologies we have now. That is the crucial question to get clear, because right now we are spending a lot of time and effort on other things.â€

The second roadmap would be a high-level technical roadmap, he said, which will be continuously improved. Its purpose is to give guidance to groups that want to respond to critical problems and pinch points. This roadmap, or something like it, is needed to reenergize near- and mid-term government-funded research. “I think that many of us who do this research think the government really just wants far-out ideas. If you go talk to 100 PV scientists who helped make this industry what it is today,†he concluded, “they will say this: that the government just wants far-out ideas. I believe that is because the key decision makers are not sophisticated in PV and have not been provided with the most critical insights about past successes.â€

OBSERVATIONS ON BUILDING A PV ROADMAP PANEL

Doug Rose

SunPower

Dr. Rose offered an overview of the points he would make:

• First, he agreed with Professor Zweibel’s message that PV is poised to become a significant source of cost-effective renewable energy without needing “some far-out, next-generation technology.â€

• Second, he believed that a SEMI-like equipment technology roadmap would not be appropriate for PV.

• Third, there are many ways the DoE and federal government have and can continue to accelerate the growth of the PV industry and thereby help the United States in both the near and long term.

He began with the observation that the PV industry now is about where the semiconductor industry was in the mid-1980s in annual sales. “That was when a lot of the roadmapping was done to move the industry ahead,†he said. “But some of that analogy falls apart. One difference is that PV is already a much more manufacturing-intensive industry than integrated circuits (ICs).†More than a year ago, he said, the crystalline silicon (c-Si) PV sector used more silicon than the entire IC industry, and it has grown rapidly since then.

A Shared Ability to Lower Costs

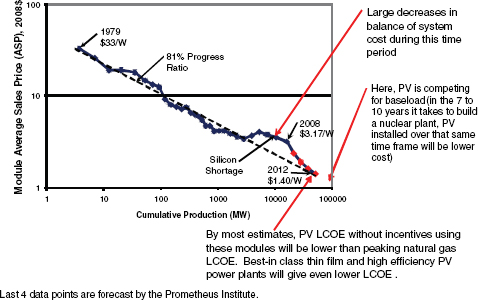

Semiconductors and PV, however, have shared an ability to drive costs down. Dr. Rose showed a graph of c-Si cost beginning in 1979, when it was $33 a watt for a module. After declining steadily, cost increased briefly around 2007-2008 because worldwide demand rose faster than the output of the polysilicon industry. A healthy consequence, however, was that it caused the industry to be more efficient with silicon use and be innovative and drive down cost in the balance-of-system portion. Now that the cost of polysilicon is dropping again, the industry is ahead of even recent price projections (it was $3.17/W in 2008 and is expected to reach the $1.40/W price well before the projected time of 2012). “At current prices for c-Si,†he said, “we can drive the levelized

FIGURE 17 c-Si PV industry back on cost learning curve.

SOURCE: Doug Rose, Presentation at July 29, 2009, National Academies Symposium on

“State and Regional Innovation Initiatives—Partnering for Photovoltaics Manufacturing

in the United States.â€

cost of electricity lower than peaking natural gas plants and then be competitive with even base load plants.â€

Turning to technology and equipment roadmaps, he acknowledged that there is much for the PV industry to learn from the successes of the IC roadmaps, but he was cautious about applying lessons directly. Among some “very big differences†between the PV industry and IC industry, he said, was that the IC industry had a natural split of intellectual property between processing and chip design, and there was a shared interest between those two groups of companies in geometry shrinks and other advances that came on a predictable schedule. “There is no analog to that in PV.â€

Second, he said, most of the PV value chain has less in common with the IC industry than it does with construction, building materials, automotive, and consumer electronics. He agreed that PV might benefit by communicating a very high-level roadmap to the rest of the industry, or Congress, on such major features as costs and volumes.

Next, porting over some of the IC-industry-derived standards could increase costs because they were developed in an industry with different characteristics. In PV, equipment costs must be kept low in order to grow cash-flow positive at greater than 40 percent per year.

The next warning is that some approaches to a roadmap could undercut the existing collaborative infrastructure in PV or undercut guidance from organizations that are more familiar with PV. And it could delay the needed U.S. market development if it results in waiting to take action until the roadmap is in place.

Avoiding Detailed Prescriptions

Dr. Rose also listed many examples of why a roadmap needs to avoid detailed technological prescriptions. That is, the PV industry is highly diverse, and that diversity is needed. Within each of the major categories, multiple companies are using different technology approaches, and roadmaps that tried to normalize these would discourage competition and innovation. In c-Si, for example, some companies are using variations on the legacy cell architecture and others are using disruptive approaches such as all-back-contact or hetero-junctions. Some of these cell architectures have the lowest cost with five-inch (flat-to-flat) wafers, while others architectures have the lowest cost with six-inch or eight-inch wafers. Some approaches use polycrystalline silicon; others use monocrystalline silicon. The biggest risk would be that standardizing on one architecture would pull resources away from the innovations that are possible and reduce the diversity that will allow systems to be optimized for different applications.

For CIS technology, there is wide diversity in deposition: sputtering, co-evaporation, electrodeposition, nanoparticle ink printing, the FASST reaction process, and ion-beam assisted. He also expressed the general concern that a roadmap could pull resources away from potentially valuable opportunities,

because module development is moving so rapidly. For example, modules might be cylinders for roof mounts, or a flexible material applied directly to roofs, or large modules for lower-cost ground mounting. He made the same points regarding CdTe, amorphous Si, and high-concentration PV technologies.

He then pointed out that the diversity that he had covered was just the semiconductor portion. For traditional c-Si, the semiconductor portion that is similar to IC processing is only about 11 percent of the value chain, and there are a lot of innovations in the rest of value chain. Then he described multiple and fast-changing approaches, such as how to optimize efficiency and module size for different applications, and how to cut wafers—by improvement of wire saws or a new cleave processes with no material loss. “The point is that diversity is actually needed for maximum success of the industry. The competition, innovation, and private funding for these different approaches drives cost reduction and optimization for different applications. The success of multiple approaches will also give faster total growth because the different approaches will have different constraints in their value chains. Just as we don’t have one type of consumer electronics, we won’t have one type of PV module.â€

The Diversity of PV Offerings

Dr. Rose described some of the diversity of systems developed and deployed by SunPower itself. He said that while SunPower does have number one market share in the United States in both residential and commercial segments, and number one or two in power plants, it is still remarkable to see the diversity from just one company using one cell architecture. Solutions in the residential market varied from (1) integrated systems for new homes to (2) systems applied to existing structures to (3) various innovations that decrease the cost of installation or add value for the customer, such as smart-mount systems and monitoring packages. For the commercial market, the company offered the original nonpenetrating horizontal mount as well as new assembled systems with tilt, and more recently a solution where the module, frame, and mounting are all integrated. The latest product was developed under the DoE TPP that SunPower leads. There are also products such as solar carports that add value to the customer beyond the energy produced.

In power plants, modules with at least medium and preferably high efficiency enable cost effective tracking, and the cost of tracking has dropped by more than 50 percent in the last few years. Tracked systems have advantages beyond their reduction of the levelized cost of energy because they increase the delivery of energy at the times that the utilities most want it. A SunPower single-axis horizontal tracker in Las Vegas has a capacity factor of about 39 percent in summer, with good delivery in the late afternoon. Utilities are becoming aware that PV has a better match to their seasonal and time-of-day peak loads compared to other sources of energy.

A Need for Public-Private Partnerships

Dr. Rose ended his presentation by describing the importance of public-private partnerships in moving the PV manufacturing industry forward. Market development will have the biggest impact. Local markets with multiyear demand drive local module manufacturing and installation, and those areas have the majority of the jobs in the value chain. It also builds downstream infrastructure, with the low cost of installation in Germany an excellent example of the near-term benefit of that. That infrastructure also has lasting benefits, allowing for faster, more cost-effective deployment of future technologies. Long-term policies, commitments for PV purchase, and carbon taxes all can contribute to market development. The greenbank, and other efforts to improve end-project-financing, which is a key constraint now, is another area that would have a big impact. Finally, bringing down some of the barriers for PV penetration, such as slow permitting, grid access, and local ordinances, is important.

Programs that directly encourage development and manufacturing are also needed. This has been one of the big areas of success for the DoE program. Funding for PV programs at federal labs and universities, as well as development support for small and large businesses, manufacturing tax credits, and technology partnerships in select areas, all can have a big impact.

Other areas such as development of a module energy rating and developing a high level roadmap which will communicate expected volumes and costs could also be useful.

DISCUSSION

The Scope and Purpose of the Roadmap

Mr. McFadden said he agreed that a roadmap imposing standardization should be resisted, and that in fact a roadmap should reflect the healthy diversity of industry activities. But he also said that many of the roadmap criticisms made by Dr. Rose were not necessarily endemic to the concept of roadmapping. For example, he said, the semiconductor roadmap had been a success largely because it reflected the input of all the knowledgeable players in that industry, and had a major impact because it was a “realistic reflection of that particular landscape.†Thus it informed people who were focused on one or two areas about the broader opportunities, obstacles, and gaps in technology generally. Beyond these broad guidelines, companies were “left on their own to figure out the most imaginative ways to approach problems, decide what else to focus on, and choose where is their specific effort and the broader industry effort would best be placed.†He acknowledged that the semiconductor industry had “a lot of advantages, such as Moore’s Law and a more predictable kind of momentum,†but he said that the roadmap process itself seemed to be illuminating for virtually all the players in the industry.

Dr. Rose replied that those were “great observations for the IC industry. The process and success there shows it can be done for that industry. It was not easy there; the success was a testament to the intelligence and dedication of the people working on it. But if you look at differences between the industries, it falls apart. The IC industry was driven by the people who shared in the benefits of standardization. Everyone I’ve talked to in the PV industry has given the input; we don’t want this type of roadmap.â€

Professor Zweibel said that “we might be confusing two things. First, there’s certainly value in supporting development of existing technology at companies and advancement in their manufacturing. And second, there’s certainly value in doing university research and foundational research to understand the fundamentals of how these things work, and building a science and technology base. Beyond those two, there’s certainly value in bringing universities and NREL together with industry as well as possible and protecting IP. We welcome participation of the federal government and various political constituencies who want to support that, and we will make sure that the money will be as well spent as possible.â€

Early PV Roadmaps

Discussants noted that the topic of a PV industry roadmap was not new; an early version was generated in 2002. Dr. Guha noted that “many of us participated in it vigorously.†He said that a subsequent roadmap was also generated, describing goals and objectives of the industry, which he called a success story. He said that one goal was to reach an installed cost point of $4.50/kWh by 2010, a point that had already been passed. “Certain things the industry did collectively are working,†he said. “We don’t need to try to fix that when it is not broken.â€

Dr. Guha continued in deploring “this fascination with doing something totally out of the box. I’ve been there. I’ve done innovation. I’ve done commercialization. And it is not trivial what we have done. Every day we meet challenges and we do innovation. And suddenly thinking I am going to do something new which is going to fix everything, is utopia.â€

Dr. Rose said he agreed with Dr. Guha’s points, and that he wanted to clarify what he had said. “My negative comments about roadmaps,†he said, “were not meant to be a general statement, but to refer only to a semiconductor-modeled technology/equipment roadmap. We participated in that 2002 industry roadmap, and it was a tremendous document that had a lot of benefit for the industry. Continuation of that kind of exercise and the ones Professor Zweibel mentioned would have a lot of value.â€

Dr. Stanbery of HelioVolt said he was also familiar with the earlier roadmap, and that some of that roadmap became a constraint to some activities. In particular, he said, it tended to channel development toward some of its major conclusions. For example, he said, after the roadmap described supply chain weaknesses

in thin-film manufacturing equipment, thin films were not included in the DoE’s subsequent funding plans.

Avoiding Too Much Detail in a Roadmap

Dr. Eaglesham agreed that “we’re not smart enough build a roadmap that specifies the technology direction you should take. The constraint you have in the system is that technology that fails to intersect the cost roadmaps of the incumbents will die. I would strongly discourage us from an exercise that goes into too much detail, and gets into picking winners, which I think we’re not ready to do.â€

Mr. McFadden reiterated that his sense of the semiconductor roadmap was that it was not intended to pick winners. “It was designed to provide a realistic view of the technology challenges.â€

Dr. Eaglesham replied that “a winner had already been selected. At that point CMOS had won. All the other technologies collapsed into a very simple 200mm roadmap. It was a different world from where we are today. It’s not clear that in an industry of this scope there’s going to be single solution.â€

Professor Zweibel said that what he had learned from roadmaps was how to listen to others, how to work together, how to deal with IP, and how to get around intransigent organizational problems, “which are lessons we all need. We don’t need this exact kind of roadmap model, but we need to learn. The point is that we can make cost-effective PV. We’ve had great results up to now, both in industry and the government programs, and yes, we welcome the renewed vigor in political support for solar energy.â€

Elaine Ulrich of the House Committee on Science and Technology, who worked with Congresswoman Gifford, said that her committee would like some further guidance from the participants. She asked for feedback on where the solar industry was, and what the industry’s primary needs were. “We need guidelines,†she said. “We need to have something to turn to. If you have investments from the government, what should guide those investments? I would like to have the input from the actual members of industry. What kinds of discussions need to happen to effectively support this industry?â€

A Need for Long-Term Consistency in Government Policy

Dr. Gay of Applied Materials said that one response to that offer was to say that “we need long-term consistency, and we need predictability in government policy.†He said that, for example, PV could contribute a certain percentage to the energy base by a given year as long as there is predictability, and if a roadmap helps us quantify the value of distributed generation, time of day opportunities, and other industry targets. With a solid business case and continuity of policy, he said, banks will finance PV. The banking community needs to have confidence, he said, that when a company enters into a power purchase agreement, the policy

stability will allow the agreement to hold up for a certain period. That framework would lead to R&D, manufacturing, and commercialization.

The Central Importance of Market Pull

Dr. Gay added that while the discussion had focused on the technology roadmap, the central issue for the PV industry was really market pull. This was demonstrated in Germany, when in 1990 a small rooftop program in Aachen became, under the influence of Hermann Sheer,14 a countrywide goal, driven by the feed-in tariff. “The policy said that for 20 years the electricity from those arrays would provide a cash flow, which was a more solid return on investment than most financial instruments.†The policy also created 100,000 jobs, he said, greater than the number in the famous automobile sector. It also created a manufacturing base, many R&D centers, the Fraunhofer Gesellschaft, and a steady stream of educated people.

“At the end of the day,†he concluded, “this is all about jobs. Those jobs begin with the universities, the pipeline of know-how, and they end up in the marketplace. I think it would best serve us to start our roadmap with that market pull.â€

____________________

14Dr. Scheer, an early supporter of Germany’s feed-in tariffs, is a world leader in the development of the photovoltaic industry.