6

Economic and Policy Factors Affecting Bivalve Mariculture

Numerous economic and regulatory factors have a direct bearing on the viability of bivalve mariculture. Mariculture producers must compete in product markets with wild-harvest molluscs and with imports, many of which come from high-volume and low-cost mariculture operations in countries with lower labor costs and, often, less stringent regulatory regimes than the United States. The regulatory regime for nearshore mariculture varies from state to state and sometimes from town to town (Duff et al., 2003). An extensive literature documents cases where uninformed, outdated, or inappropriate regulatory regimes impede mariculture development (National Research Council, 1978; Kennedy and Breisch, 1983; DeVoe and Mount, 1989; Bye, 1990; Rychlak and Peel, 1993; Ewart et al., 1995; Massachusetts Coastal Zone Management, 1995; National Oceanic and Atmospheric Administration, 1999). In some instances, inconsistencies in the law produce an uncertain legal environment for mariculture operations, and regulators may be in the conflicted position of both promoting the development of the industry and preventing conflicts with other uses of the land and water (National Research Council, 1992; DeVoe, 1999).

A number of studies have reviewed policies that both facilitate and constrain aquaculture and mariculture (Kane, 1970; Wildsmith, 1982; Eichenberg and Vestal, 1992; Rychlak and Peel, 1993; Barr, 1997; Hopkins et al., 1997; Rieser, 1997; Brennan, 1999; Rieser and Bunsick, 1999; McCoy, 2000). In this chapter, the committee reviews the major policy and economic factors that affect the size and location of bivalve mariculture industry development around the United States. While some laws and

regulations may constrain mariculture development, others can serve to advance its growth. Some states have developed effective practices for interagency coordination, technical assistance, sponsorship of research and development efforts, marketing assistance, and other forms of industry promotion (Jarvinen, 2000; Jarvinen and Magnusson, 2000).

REGULATION AND PERMITTING

As traditionally practiced in the United States, bivalve mariculture relies heavily on nearshore waters that are under state or town jurisdiction. These nearshore locations may be particularly conducive to bivalve growth because of high-planktonic food levels and suitable temperature, and they provide ready access—often without the need for a boat—for stock management and harvesting. They also expose the mariculture operations to extensive use conflicts because the nearshore waters of the United States are heavily used for recreational and aesthetic purposes. The legal regime governing U.S. coastal waters gives jurisdiction over these areas to individual states, with complex and sometimes inconsistent results.

Following Duff et al. (2003), the committee summarizes the main types of policies and regulations that govern bivalve mariculture, focusing on the following areas:

-

leasing and tenure policies

-

jurisdictional complexity

-

land use, zoning, and tax policies

-

interstate transport policies

-

offshore mariculture policy

Leasing and Tenure Policies

Nearshore mariculture operations usually are sited on or in “public trust” resources (i.e., state intertidal and subtidal lands and state waters). Under the public trust doctrine, certain tidelands, coastal waters, and other public lands are held in trust by the government (in this case, the state) for the benefit of the state’s citizens for purposes that include fishing, navigation, and commerce (Duff et al., 2003). In some instances, public trust purposes also include ecological functions or public recreation (Eichenberg and Vestal, 1992). Public trusts under this doctrine operate much like private trusts, with defined property, trustee(s), and beneficiaries. Under the public trust doctrine and common law, the state as trustee is generally proscribed from divesting the property permanently. As a result, mariculture operations generally cannot purchase permanent rights to a marine

or estuarine site and must enter into lease or tenure arrangements. Since, in some instances, these are limited in term and subject to conditions and challenges, it can be difficult for mariculture operations to demonstrate long-term security of tenure (e.g., for the purpose of securing financing for farming operations and equipment).

The public trust doctrine applies to submerged lands and overlying waters under the jurisdiction of the states, but its application varies by state. For example, in Massachusetts, Maine, Pennsylvania, Rhode Island, and Virginia, the intertidal lands (between mean-high and mean-low water) may be held as private property (Underwood, 1997), but private owners must accommodate the public’s right to “fish, fowl, and navigate” in or over them.1 In Massachusetts, mariculture is not considered one of the public trust purposes that must be accommodated (Duff et al., 2003), but in Washington State, the right of oyster farmers to purchase and own tideland areas for the purpose of mollusc cultivation extends back to the 1800s (Woelke, 1969). Some states pass along responsibility for managing nearshore waters, including assignment of mariculture leases, to local town government.

To the extent that bivalve mariculture also requires federal permits, it may be subject to the “federal consistency” requirements of the Coastal Zone Management Act (16 USC 1451 et seq.), which may require a determination of the extent to which the mariculture operation is consistent with a state’s coastal management plan. One federal permit that is commonly required for mariculture is the Section 10 (Rivers and Harbors Act) permit issued by the U.S. Army Corps of Engineers (USACE), which governs the installation of mariculture gear that may pose an obstruction to navigation in navigable waters. Application for a Section 10 permit in turn can trigger USACE’s “public interest review process,” which can involve the assessment of environmental impacts and the development of an environmental impact statement. In the course of evaluating Section 10 permit applications, USACE typically seeks comments from the National Marine Fisheries Service’s Protected Resources Division, which determines the likelihood of any impacts to endangered or threatened species or marine mammals and from other federal (e.g., Environmental Protection Agency, U.S. Coast Guard, U.S. Fish and Wildlife Service) and relevant state agencies (Duff et al., 2003).

For existing commercial shellfish aquaculture operations, USACE has issued a “Nationwide Permit” (Federal Register, 2007) that “authorizes the installation of structures necessary for the continued operation” as well as “discharges of dredged or fill material necessary for shellfish seed-

ing, rearing, cultivating, transplanting, and harvesting activities.” The Nationwide Permit does not apply to new operations or expansions; to the cultivation of additional species; to the construction of structures, such as docks and piers; or to the deposition of shell material into the water as waste (Federal Register, 2007). This Nationwide Permit simplifies continued operation of existing shellfish mariculture projects in some regions. However, state and local authorities may place additional constraints that require a separate certification or waiver for authorization of continued operations.

Jurisdictional Complexity

In 1981, a comprehensive review of aquaculture regulations across the nation (the “Aspen Report” sponsored by the U.S. Fish and Wild-life Service; Aspen Research and Information Center, 1981) identified at least 120 federal laws that either directly (50 laws) or indirectly (70 laws) affected aquaculture, along with more than 1,200 state statutes regulating aquaculture in 32 states. The Aspen Report concluded that many aquaculture businesses must obtain at least 30 permits2 to site and operate their businesses.

Regulatory jurisdiction over bivalve mariculture typically falls under the auspices of multiple local, state, and federal agencies. Many states recognize mariculture as a form of agriculture and give regulatory control to the state agriculture department, but these departments usually do not have jurisdiction over the public lands where mariculture takes place. Public land management typically falls under the authority of the state department responsible for environmental protection. Regulatory complexity is further increased when towns or counties are given jurisdiction over local waters. From the shellfish growers’ point of view, the effect of this regulatory complexity in many cases has been an expensive, time-consuming, and sometimes unsuccessful process for obtaining permits (Duff et al., 2003).

In response to concerns over real or perceived regulatory complexity, many states have designated a particular state agency as the “lead” and starting point for mariculture permit applications. Many coastal states also have created interagency coordinating committees or task forces to facilitate the mariculture permit process. Some states produce written guidance to help permit applicants understand the set of permits required for different mariculture operations and the process and sequence for obtaining them. For example, Connecticut has established an Interagency

Aquaculture Coordinating Committee comprising the departments of agriculture, environmental protection, consumer protection, and economic development to provide for the development and enhancement of mariculture in that state.3 Similarly, Pennsylvania established the Aquaculture Advisory Committee4 to encourage long-term investment by reducing the number of agencies involved (by transferring most authority to the state’s Department of Agriculture) and including mariculture in promotional and economic developmental programs that are available to other industry sectors.5

Land Use, Zoning, and Tax Policies

Some states effectively subsidize mariculture operations by exempting them from sales or use taxes.6 States also may promote mariculture production via zoning designation or waterfront revitalization programs.7 In some cases, regulations have been promulgated for the express purposes of preventing competition between fishermen and mariculturists. New Jersey, Massachusetts, and North Carolina, for example, limit bivalve cultivation to bottom areas where bivalves do not grow naturally. These regulations have caused problems in New Jersey, where mariculture industry participants have pointed out that lease areas suitable for bivalve grow-out are unavailable (Duff et al., 2003).

Interstate Transport Policies

State rules concerning the importation of fish eggs, fingerlings, and bivalve seed from other states are non-uniform. Confusion, misinformation, and non-compliance have contributed to the introduction of nonnative species and increased incidence of disease, harming some bivalve mariculture businesses and changing the nature of local or regional ecosystems (e.g., Simberloff, 2005). Although some states have restricted transport to a few trusted companies, other states do not follow a strict protocol or possess testing facilities or regulations for the transport of live fish, eggs, or seed. The existence of inconsistent policies for interstate shipment of these mariculture products has hampered the ability to develop a comprehensive interstate transport capability. When limited

supplies of bivalve seed are available, market prices tend to rise because of the lack of supply or competition (Duff et al., 2003).

A related constraint facing some mariculture operations concerns the export of their product to states where commercial fishery rules define the characteristics of the product. For example, a three-inch size restriction on the commercial harvest of oysters in Massachusetts prevents the sale or even the transport through the state of smaller oysters grown on farms in Connecticut or Rhode Island (Duff et al., 2003).

Offshore Mariculture Policy

Regulatory complexity, use conflicts, and (in some cases) water- quality issues8 in nearshore waters have led to greater interest in offshore or open-ocean mariculture. The technical and economic feasibility of open-ocean bivalve mariculture has been demonstrated to some degree (e.g., mussels in the northeastern United States; Langan and Horton, 2002; Kite-Powell et al., 2003).

The regulation of offshore mariculture in the United States remains unsettled. At present, there is no federal policy pertaining specifically to the permitting of mariculture in waters under federal jurisdiction, typically 3–200 nautical miles offshore, known as the exclusive economic zone. At a minimum, a Section 10 permit is required from USACE, and in some cases, approval from fisheries management councils may be required. In the absence of a settled and transparent regulatory framework, not only is expansion of the existing industry hampered, but potential future growth and research in this area is discouraged (Barr, 1997; Brennan, 1999; National Oceanic and Atmospheric Administration, 1999). Legal rules that establish and enforce private property rights and use privileges (e.g., though leasing) are critical to the development of the industry both onshore and offshore (Hoagland et al., 2003; 2007).

A bill defining federal policy and permit processes for mariculture in the exclusive economic zone, the National Offshore Aquaculture Act has been introduced several times, most recently in 2007 as H.R. 2010 and S. 1609 in the 111th Congress (National Oceanic and Atmospheric Administration, 2008a). The 2007 bill would address the current gaps in U.S. offshore mariculture regulation by:

-

authorizing the Secretary of Commerce to issue offshore mariculture permits

-

requiring the Secretary of Commerce to establish environmental requirements for offshore mariculture

-

requiring the Secretary of Commerce to work with other federal agencies to develop and implement a coordinated permitting process for offshore mariculture

-

exempting permitted offshore mariculture from fishing regulations that restrict size, season, and harvest methods

-

authorizing a research and development program for all types of mariculture

The National Offshore Aquaculture Act has not been passed by Congress to date, in part because of controversies over the adequacy of environmental regulations in the bill and because of the role of states in regulating offshore mariculture.

MARKETS, PRICES, AND TRADE

The extent and locations of bivalve mariculture activities around the United States are influenced by market and trade conditions. This section describes in broad terms some recent trends in the U.S. markets for oysters, clams, and mussels and points out implications for U.S. bivalve mariculture.

For finfish and crustaceans, aquaculture activities are easy to distinguish from wild-capture fisheries. For molluscs, the distinction is sometimes less clear. Natural oyster beds, for example, may be leased to private individuals who harvest and maintain them, relying on natural spat settlement but seeking to maximize yield by providing an ideal substrate. Wild clam beds may be seeded with juveniles raised in hatcheries (e.g., Peterson et al., 1995), either by clam farmers who have exclusive rights to harvest there or by towns or states seeking to enhance the clam stock for the general public (which may include small-scale commercial harvesters). (For the purposes of origin labeling [P.L. 107-171] of seafood sold in the United States, seafood is considered “farm-raised” if it originated in a hatchery.) In part because the line between wild-stock fisheries and mariculture of bivalve molluscs can be hard to define, the National Oceanic and Atmospheric Administration (NOAA) reports the commercial landings of oysters, clams, and mussels as a single quantity, regardless of whether the source is wild stock or mariculture (National Oceanic and Atmospheric Administration, 2009b). This makes it difficult to distinguish trends in mariculture and wild-harvest production using the NOAA data. NOAA reports separate mariculture production statistics as part of its annual “Fisheries of the United States” report (National Oceanic and

Atmospheric Administration, 2009c), but the accuracy of these numbers has been called into question by culturists (see below).

A second complication with the bivalve landings is that NOAA reports the landings and prices for oysters, clams, and mussels in units of meat weight (National Oceanic and Atmospheric Administration, 2009b), whereas other units of weight or volume are typically used for bivalves by growers and merchants (e.g., shell-on live weight, bushels, baskets, bags, individuals). There is no standard reporting process for bivalve landings held in common across all U.S. states. Also, the same species of bivalves may be sold into two different markets with different customary units of measurement that are deeply engrained in the tradition of the business. For example, oysters may be sold to the live half-shell market by the piece or by the bushel, or they may be sold in processed form (removed from the shell and cooked or smoked) by meat weight. NOAA converts reported landings from many markets into a single meat-weight equivalent. Some growers are skeptical about the accuracy of the conversion process and of the resulting data (Robert Rheault, personal communication).

Oysters

Global oyster production is reported by the Food and Agriculture Organization of the United Nations (2009) to have reached 4.9 million metric tons (live weight, the nominal weight at the time of harvest) in 2004. The culture of oysters dates back to Roman times (Clark, 1964). Hatchery production of seed was pioneered in the 1980s (Chew, 1984). Mariculture today accounts for about 94% of global oyster production (Food and Agriculture Organization of the United Nations, 2009). The Pacific oyster, Crassostrea gigas, accounts for 99% of cultured oyster production; it is the world’s most commonly cultured bivalve species. More than 93% of oyster mariculture production takes place in Asia and the Pacific.

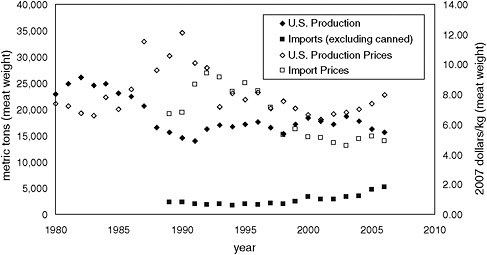

U.S. oyster production (Figure 6.1) is reported by NOAA to have accounted for about 10,000 metric tons (meat weight) on the east coast and in the Gulf of Mexico (Crassostrea virginica) and about 6,000 metric tons (meat weight) on the west coast (Crassostrea gigas) in 2006. About two-thirds of this is considered by NOAA to be mariculture production. Present U.S. total production levels are well below historic highs. Before the Chesapeake Bay wild oyster population further declined in the 1980s (National Research Council, 2004), C. virginica production exceeded 20,000 metric tons per year; historically, U.S. oyster production peaked in the late 1800s at more than 80,000 metric tons (meat weight) per year.

U.S. imports of oysters (Figure 6.1) declined from 1989 to 1996 but have been gradually rising since then to 11,000 metric tons per year

FIGURE 6.1 U.S. oyster production, including wild harvest and mariculture, (1980–2006) and imports (1989–2006) and prices in constant 2007 dollars. SOURCE: National Oceanic and Atmospheric Administration (2007; 2009b, d).

(meat weight). Most imports come from cultured oyster production in China and South Korea. The United States exports about 3,000 metric tons per year, about 19% of the total domestic oyster production. U.S. production accounts for about 4% of global oyster production, and the U.S. market (consumption) accounts for approximately 6% of global consumption (in volume terms). China accounts for about 82% of global oyster production (Food and Agriculture Organization of the United Nations, 2009).

According to NOAA data, average U.S. oyster prices have been declining in real terms since 1990 (Figure 6.1). This broad trend in average prices masks significant differences across product markets (half-shell versus canned) and production regions. For example, a half-shell oyster in New England may sell for three times the value of a half-shell oyster on the Gulf of Mexico (Robert Rheault, personal communication).

Clams

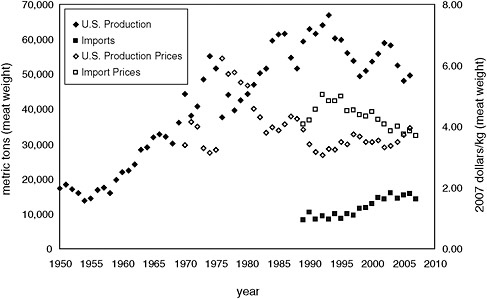

Global mariculture production of clams (including cockles and others) is reported by the Food and Agriculture Organization of the United Nations (2009) to have reached 4.1 million metric tons (live weight) in 2004. Clams are the fastest growing component of global mollusc production, with output rising at 9.1% per year. NOAA reported U.S. production

FIGURE 6.2 U.S. clam production, including wild harvest and mariculture, (1950–2006) and imports (1989–2007) and prices in constant 2007 dollars. Production data include quahogs, surf clams, Manila clams, soft-shell clams, and geoducks. SOURCE: National Oceanic and Atmospheric Administration (2007; 2009b, d).

of clams (Figure 6.2) at about 50,000 metric tons (meat weight) in 2006, with about 10% of the harvest coming from mariculture.

Imports provide another 15,000 metric tons per year (meat weight) and come primarily from China, Thailand, and Vietnam (processed) and from Canada (fresh and processed). U.S. mariculture and import volumes have been growing slowly; total U.S. consumption has been stable since the 1980s. Consumption in the U.S. market accounts for an estimated 6% of global clam production. Average U.S. prices of clams have been generally stable since the mid-1990s (Figure 6.2), but prices of imports have declined by more than 20% in real terms, likely reflecting increased supply due to strong growth in global clam mariculture.

Mussels

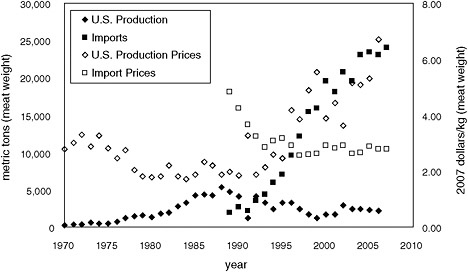

Global mariculture production of mussels is reported by the Food and Agriculture Organization of the United Nations (2009) to have reached 1.9 million metric tons (live weight) in 2004. Global mussel production is rising at 4.5% per year. U.S. production of mussels (Figure 6.3) is reported by NOAA to have peaked around 5,000 metric tons (meat weight) in 1988 and has been generally declining since then. There is very little maricul

ture production of mussels in the United States. The Pacific Coast Shellfish Growers Association (2005) reports production of 1,600 metric tons (live weight) on the U.S. west coast, primarily in Washington and California, in 2005.

Imports of mussels rose from negligible amounts in the late 1980s to nearly 25,000 metric tons per year in 2007 and account for 95% of mussels consumed in the United States. This surge in U.S. imports coincided with strong growth of export-oriented mussel mariculture in Canada and New Zealand and more recently in Chile. Canada (fresh product, mainly Mytilus edulis) and New Zealand (processed, mainly Perna canaliculus) account for 41% and 49% of U.S. imports, respectively, by weight. Consumption in the U.S. market accounts for less than 3% of global mussel production. Per person consumption in the United States grew significantly over the past 15 years but still remains a small fraction of per person consumption in Western Europe. For example, per person consumption of mussels in the United States is on the order of 0.25 pounds per year, compared to more than 6 pounds per year in the Netherlands and more than 10 pounds per year in Spain (Food and Agriculture Organization of the United Nations, 2008b).

Figure 6.3 shows U.S. average price trends for fresh mussels, based on NOAA data, on a meat-weight basis. Average import prices dropped quickly as import volumes rose from 1990 to 1995 and have since stabi-

FIGURE 6.3 U.S. mussel production, including wild harvest and mariculture, (1970–2006) and imports (1989–2007) and prices in constant 2007 dollars. SOURCE: National Oceanic and Atmospheric Administration (2007; 2009b, d).

lized. Strong marketing campaigns accompanying imports contributed to growth in the U.S. market for mussels, both live and processed. U.S. producers have responded to low-price foreign competition by focusing on higher-priced, higher-grade live and fresh products destined for the local and regional niche market segments.

From the point of view of U.S. mariculture producers, the markets for the three major bivalve groups present both commonalities and stark differences. In all three markets, the United States is a small player in a large and growing global market for both fresh and processed product. Most U.S. production is consumed domestically and accounts for the majority of sales of oysters and clams in the United States. With small fractions of the domestic product destined for export, the United States is a net importer in all three markets, and U.S. mariculture producers generally face competition from low-cost imports of similar products. Domestic mariculture production is most significant in the oyster market, where it is roughly on par with wild-capture production and imports. Domestic mariculture is relatively weaker in the clam market, which is still dominated by wild-capture supply; it is weakest in the mussel market, which is dominated by imports.

Because it is difficult for U.S. growers to compete on price in the lowcost, processed bivalve segments of the global market, most U.S. bivalve mariculture producers today seek to serve local or regional niche markets for high-priced fresh or value-added products (Duff et al., 2003). In the past, U.S. northeast bivalve producers have complained about damages from “dumping” (fresh mussels from Canada) and from mislabeling of imported or non-local bivalves (cultured clams grown originally outside the northeast labeled improperly as local product) (Duff et al., 2003). In 2003, Congress enacted a “Country of Origin” provision (P.L. 107-171), requiring the labeling of seafood sold in the United States to indicate the country of origin and whether the product is wild or farm-raised. The labeling requirement went into effect for seafood in 2005; it has since been extended to other foods as well. This should make it easier for U.S. producers to distinguish domestic product from imports in the eyes of the consumer.

U.S. Seafood Supply and Trade Balance

Some advocates for aquaculture (including finfish, crustaceans, and molluscs) suggest that the United States should promote increased domestic production of seafood, in part because this would reduce the nation’s reliance on foreign imports (National Oceanic and Atmospheric Administration, 1999). Although there are risks associated with heavy reliance on imported seafood, there are significant economic benefits associated

with international seafood trade—it is a source of export earnings for many (sometimes less developed) nations, and U.S. consumers benefit from readily available and low-cost imported seafood products. The net benefits to the U.S. economy of reducing the nation’s seafood trade deficit by increasing domestic production are uncertain. A broad effort to boost aquaculture in the United States could in theory achieve this goal, but increasing bivalve mariculture alone is unlikely to make a significant difference in the nation’s overall seafood trade balance.

The United States imported 2.37 million metric tons of edible seafood products (including all types of finfish and shellfish) in 2008 and exported 1.16 million metric tons (National Oceanic and Atmospheric Administration, 2008b). The 2008 imports were valued at about $14.2 billion and exports at about $4 billion, creating an edible-seafood trade deficit of $10.2 billion (National Oceanic and Atmospheric Administration, 2008b). (Non-edible seafood9 product imports in 2008 were valued at $14.3 billion and exports at $16.8 billion, so the United States is a net exporter, in value terms, of non-edible seafood products.)

NOAA (2009a) estimates that in round weight (live, whole fish) terms, U.S. domestic production from fisheries and aquaculture accounted for about 3.5 million metric tons in 2008; clams, oysters, and mussels accounted for approximately 1.5% of the total by weight and about 7.5% by value. Imports contributed the equivalent of 4.74 million metric tons, and exports accounted for 2.38 million metric tons, for net domestic consumption of 5.37 million metric tons of edible seafood. This supported an average U.S. seafood consumption of 16 pounds of edible seafood products per person (National Oceanic and Atmospheric Administration, 2009a).

The U.S. seafood trade deficit thus is due to large net imports of edible products. The majority of the edible fishery-product trade deficit consists of five species groups: shrimp, crabs, tunas, salmon, and lobsters. Since 1997, shrimp has been the largest single-species group contributor to the edible-seafood trade deficit. Groundfish, salmon, and lobster are the largest contributors by value to U.S. seafood exports. Reflecting the large global trade in seafood products, U.S. seafood imports come from a diverse set of exporting nations. Canada, China, and Thailand are the most significant sources of U.S. seafood imports (National Oceanic and Atmospheric Administration, 2005).

Two risks associated with imported seafood are health issues and the possibility of limited supply at some point in the future. While seafood consumption is generally considered to have significant health benefits, it can also contribute to health problems when seafood is contaminated

via pollution in the water, in prey or feed, or through the application of antibiotics and when it is processed incorrectly (Kite-Powell et al., 2008). In the United States, seafood is implicated in a significant number of food-borne illnesses, and many observers have been critical of seafood inspection, particularly for imports (Ralston and Kite-Powell, in review). However, there is little evidence to suggest that imported seafood is responsible for a disproportionate degree of health risk.

Several studies have considered likely future trends in U.S. seafood consumption, production, and trade (Delgado et al., 2003; Nash, 2004; Hoagland et al., 2007). While it is possible that better management of certain U.S. fish stocks (e.g., cod) and hatchery enhancement of wild stocks could increase wild-capture landings in the future, there is little reason to expect aggregate landings to increase dramatically. If the U.S. population continues to grow, as it has recently (i.e., by about 1% per year), and assuming (conservatively) that per-person consumption of seafood remains roughly at present levels (16 pounds of edible meat per person per year10), U.S. seafood consumption will rise by 20% to about 6.2 million metric tons per year by 2025. If U.S. capture landings and existing aquaculture production remain at present levels, this leaves a projected short-fall in 2025 of 2.7 million metric tons per year (round weight) to be filled by some combination of additional U.S. aquaculture and net imports.

Nash (2004) and others suggest that U.S. aquaculture production could be increased significantly, with a concerted effort, from its present level of less than 500,000 metric tons per year. U.S. aquaculture production has grown by an average of 6% per year (in volume terms) since 1983, although this growth has been slower during the past decade, and both imports and exports of seafood products have grown at an average rate of about 2% per year for the past 15 years (Hoagland et al., 2007). Unless the balance of U.S. aquaculture production shifts toward species, such as shrimp, tuna, and salmon, or consumer tastes change dramatically, it is unlikely that domestic production can significantly reduce imports in the near future. Nash (2004) suggests that the United States could triple domestic production of bivalves to more than 300,000 metric tons per year (live weight) by 2025; in volume terms, this could displace all current bivalve imports. However, in bivalves as in other species, U.S. mariculture production is likely to focus on high-value niche markets for fresh product and may not compete directly with low-cost processed imports. Even if U.S. aquaculture production growth can be increased by easing constraints and encouraging investment, it is likely that low-cost imports

will remain attractive and continue to supply a significant fraction of U.S. seafood in the coming decades.

LOCAL TRADITIONS AND NOT-IN-MY-BACKYARD (NIMBY) ISSUES

Local traditions and use conflicts in the nearshore waters represent both a constraint and, in some instances, an opportunity for bivalve mariculture. In communities or settings where mariculture has not been part of the established or traditional waterfront, recreational-use patterns (boating, fishing, swimming) and aesthetic considerations (ocean and bay views from waterfront homes) may lead to public objections to permitting and siting mariculture operations (Vestal, 1999). In places where there is a history of bivalve culture or an established shellfish fishing industry, the public may be more receptive to devoting additional nearshore areas to new mariculture proposals. The inclination to support mariculture may be weakened if there is a large influx of residents who do not share the community’s cultural fishing traditions. Even in some traditional fishing communities, strong objections to mariculture can arise based on loss of public-trust bottom that historically served to support extractive fishing operations. Shellfish growers can increase the social carrying capacity and reduce political opposition to mariculture leases by engaging constructively with the local community, for example, by supporting local charitable causes and designing their operations to minimize visual and physical conflicts with established uses.

Bivalve mariculture proposals that require some portion of nearshore waters or tidelands to be “off limits” to foot or boat traffic may run afoul of public rights of use and access. For example, bivalve mariculture operations that utilize gear (e.g., cages, bags, racks, longlines) on the bottom or in the water column may interfere with other uses of the coastal zone, such as recreational and commercial fishing, shipping, and boating. In several northeast states, mariculture is given lower priority than navigation, fishing, and most other uses of the coastal zone. The subordination of mariculture and other “non-traditional” uses of coastal areas is evident in a number of state constitutions.11 This has constrained some operations (Duff et al., 2003).

Some states accord a preference for certain uses of submerged lands to owners of upland property adjacent to navigable waters (riparian rights). The most important preference is a right of access by dredging, filling, or wharfing. Mariculture may be constrained by riparian rights to the extent that these activities displace mariculture operations or put shellfish

farmers who are non-riparian owners at a competitive disadvantage. The application of riparian rights varies by state (Duff et al., 2003).

In coastal settings where excess nutrient inputs are causing ecological problems or where historic natural bivalve stocks have been depleted, prospects for permitting of bivalve mariculture can sometimes be improved by educating the local community about the ecological benefits (e.g., water filtration, nutrient removal, habitat enhancement for finfish and crabs) of bivalve mariculture. Numerous towns around the United States have successfully developed marine water-resource management plans that balance recreational and aesthetic considerations with bivalve mariculture; see for example the recently developed plan for Duxbury Bay in Massachusetts (Duxbury Bay Management Commission, 2009).

FINDINGS AND RECOMMENDATIONS

Finding: The United States is a net importer of bivalve products, and this represents an opportunity for the expansion of bivalve mariculture production within the United States.

Finding: While some laws and regulations may constrain bivalve mariculture development, others can serve to advance its growth. Local traditions and use conflicts can have this dual effect as well.

Recommendation: States should streamline the permitting process for bivalve mariculture in state waters and identify areas within state waters where such activities are encouraged. Shellfish growers should engage the local community and design their operations to minimize conflicts.

Finding: Inconsistencies in the law produce an uncertain legal environment for mariculture operations. Confusion, misinformation, and non-compliance of interstate transportation policies have contributed to the introduction of nonnative species and the increase in incidence of disease. The existence of inconsistent policies for interstate shipment of these mariculture products has hampered the ability to develop a comprehensive interstate transport program.

Recommendation: States should collaborate on the development and implementation of consistent bivalve mariculture and transportation policies.