Summary

The federal government is currently spending far more than it collects in revenues, and if current policies are continued, will do so for the foreseeable future. Over the long term, three major programs—Medicare, Medicaid, and Social Security—account for the projected faster growth in federal spending relative to revenues. No reasonably foreseeable rate of economic growth would overcome this structural deficit. Thus, any efforts to rein in future deficits must entail either large increases in taxes to support these programs or major restraints on their growth—or some combination of the two. The good news is that the nation now has many options to change course and put the federal budget on a different path. Taking steps soon to stabilize the nation’s fiscal future will be less costly and difficult than acting later.

The Committee on the Fiscal Future of the United States was established under the auspices of the National Academy of Sciences and the National Academy of Public Administration, supported by the John D. and Catherine T. MacArthur Foundation, to carry out a comprehensive study leading to a set of plausible scenarios for the federal budget, to put it on a path toward a stable fiscal future. Members of the committee have quite varied backgrounds and perspectives on the budget. We disagree on many policy matters; but we are unanimous that forceful, even painful, action must be taken soon to alter the nation’s fiscal course.

Without such action, the long-term mismatch between expected revenues and the estimated costs of government policies and programs will continue to require the government to borrow heavily. If remedial action is postponed for even a few years, a large and increasing federal debt

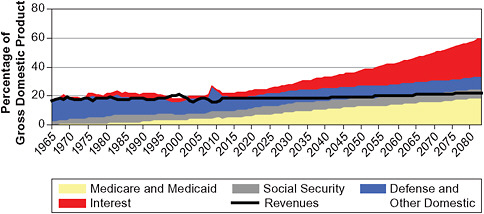

FIGURE S-1 The long-run budget outlook.

will inevitably limit the nation’s future wealth by reducing the growth of capital stock and of the economy. It will also increase the nation’s liabilities to investors abroad, who currently hold about one-half of the federal government’s debt. If policies do not change, a large and increasing debt will expand the portion of the budget required to pay interest on the debt, especially if interest rates rise, and thereby reduce the resources available for all other government activities. Increasing debt also may contribute to a loss of international and domestic investor confidence in the nation’s economy, which would, in turn, lead to even higher interest rates, lower domestic investment, and a falling dollar.

As shown in Figure S-1, the current trajectory of the federal budget cannot be sustained. Without a course change, the nation faces the risk of a disruptive fiscal crisis, a risk that increases each year that action to address the growing structural deficit is delayed. With delay, the available options become more extreme and therefore more difficult, and even more pain is shifted to future generations.

In the next year or two, large deficits and more borrowing are unavoidable given the severity of the economic downturn. However, action ought to begin soon thereafter—the committee believes that fiscal 2012 (which begins October 1, 2011) is a reasonable time to start—to first slow the rapid increase of the federal debt relative to the economy and then, over several years, reduce it to a more desirable level.

A first step toward dealing with the country’s fiscal challenge is to specify a concrete test that can help to assess whether any budget is moving toward sustainability in a prudent manner. There are a variety of ways to measure fiscal prudence and numerous targets and time paths that could be connected to various measures. In order to design plausible scenarios to

illustrate the implications of future policy choices, the committee selected a widely used metric as a reasonable (albeit not the only possible) indicator of fiscal prudence: the size of the government’s debt as a percentage of the nation’s gross domestic product (GDP). The key concern undergirding the committee’s analysis is that under a continuation of current policies this ratio would continue to rise in the years ahead, with potentially harmful effects on current and future generations.

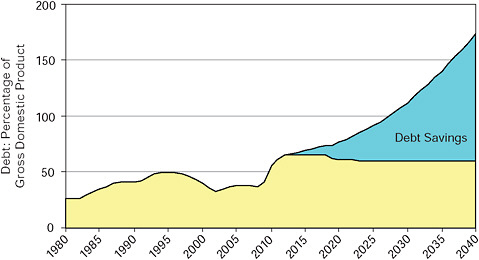

There is no magic number for the ratio of government debt to GDP; a smaller debt is always more manageable and gives a nation more ability to absorb unexpected shocks. A higher debt limits its choices and flexibility. The committee believes that the debt that will result if the United States continues with current tax and spending policies will be at a level that poses too great a risk to the economic welfare of the current generation and would impose an unfair and crushing burden on future generations. (The debt, which was about 40 percent of GDP just 2 years ago, is now above 50 percent and rising rapidly.) This is a judgment based on the committee’s deliberations over the best available data, literature, understanding of economic policy and history, and analysis of possible scenarios. Given the additional risk of carrying a higher debt burden, the committee believes that the growth in this ratio must soon be limited, as shown in Figure S-2.

More specifically, the committee believes that some combination of revenue increases and spending restraints should be implemented soon to constrain the growth of federal debt as a percentage of GDP within a decade to a level that provides an appropriate balance between the risks as-

FIGURE S-2 Debt savings from stabilizing the debt-to-GDP ratio in 12 years.

sociated with a higher ratio and the additional difficulties of implementing policies that would be consistent with a lower ratio. The committee judged that a debt of 60 percent of GDP reflects an appropriate balance and is an achievable target within a decade—and is therefore useful to guide policy choices that will ultimately be made by elected leaders. This is a different ratio than the committee would have likely proposed under different circumstances. Indeed, it will surely be seen by some as too high and by others as too low. But the committee believes it is the lowest ratio that is practical given the fiscal outlook. A higher debt burden would leave the nation less able to cope with unforeseeable but inevitable shocks—such as international crises or natural disasters—requiring a vigorous federal response. It would put the nation closer to a point from which no politically credible path to sustainability could be constructed. Moreover, stabilizing the debt at a higher ratio implies a higher deficit, a greater draw on the nation’s saving or more foreign borrowing, which will have a negative impact on future living standards. On the other side, a lower ratio would imply even more painful changes in tax and spending policies.

The rapid growth of federal spending for health care is the largest contributor to the nation’s long-term fiscal challenge. Any reasonable path to fiscal sustainability will have to include reforms to reduce the growth rates of Medicare and Medicaid. The challenge posed by Social Security is far less problematic, but still substantial. Options for putting it on a sound fiscal footing range from sizable reductions in currently projected benefit growth to sizable increases in payroll taxes, with many possible intermediate combinations. Spending growth in many other areas of federal activity can be moderated, in part by curtailing or reforming less effective programs. Options that raise taxes substantially include significant reforms to make the tax system fairer and more efficient and include the introduction of new taxes on consumption.

These and other policy changes can be combined to produce a wide range of budget paths or scenarios that would bring revenues and spending into close alignment over the long term and to stabilize the nation’s debt burden. The committee’s different scenarios are intended as an illustrative, but by no means definitive or exhaustive, set of trajectories toward a sustainable fiscal future. The committee offers four representative scenarios that illustrate a wide range of available policy choices. Any of these paths would yield growing debt savings relative to current policies and stabilize the debt at 60 percent of GDP. To achieve this, the budget does not have to be balanced or in surplus. In fact, once the target debt ratio is reached, average deficits could be as high as 2 to 3 percent of GDP without debt growing faster than GDP.

The four illustrative paths show that many policy choices are available if action is taken soon. However, none of them is easy. If the choice is to

continue all government programs at a level consistent with current policies, both spending and revenues would have to rise dramatically to prevent an ever-rising debt in relation to GDP. Given the inefficiency of the present tax structure, it would almost certainly also be necessary to change how revenue is collected. If, instead, the choice is to keep the federal government’s share of the economy close to the level of the past several decades, the government would have to scale back what it does, and extremely difficult choices would have to be made about what social goals to pursue less vigorously and what programs to end.

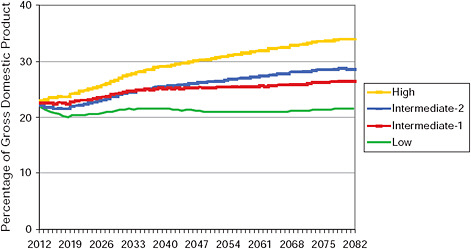

Figure S-3 compares the committee’s four illustrative paths.

-

Low spending and revenue: revenues are held near their recent average level of 18 to 19 percent of GDP, and spending is 2 to 3 percentage points higher than revenues. This path would require sharp reductions in projected growth rates for health and retirement programs, as well as reductions in the proportion of the economy’s resources available for all other federal responsibilities.

-

High spending and revenue: spending and revenues are increased substantially, with spending eventually reaching one-third of GDP. Because this spending level is still less than under a continuation of current policies, it would require an eventual reduction in the rate of growth of health spending. It would, however, accommodate the spending needed to maintain currently scheduled Social Security benefits. And it would allow spending on all other federal programs to be higher than the level implied by current policies.

FIGURE S-3 Projected federal spending under the committee’s four scenarios.

-

Intermediate path 1: spending and revenues rise gradually to about one-fourth of GDP and spending on the elderly population would be constrained to support only modest expansion of other federal spending. The growth rates for Social Security, Medicare, and Medicaid would be slower than under current policies. This path reflects the view that the federal government should make selective new public investments to promote economic growth, preserve the environment, and build for the future.

-

Intermediate path 2: spending and revenues would eventually rise to a little more than one-fourth of GDP. Spending growth for health and retirement benefits for the elderly population would be slowed but less constrained than in the intermediate-1 path. Spending for other federal responsibilities would be reduced. This path reflects the view that the government’s implicit promises for the elderly are a higher priority than other spending.

The scenarios demonstrate that it is indeed possible to reduce the risk of financial disruption and put the budget on a sustainable course using the illustrative debt target of 60 percent of GDP and timeline to reach it. The choice of the starting date and timeline, as with the level of the target, will ultimately be a decision of elected leaders, taking into account the best information available to them when they must make budget choices.

The committee recognizes that this task is extremely difficult: the pain, whether cutting the growth of spending, increasing taxes, or both, must begin very soon, while the gain of avoiding a fiscal train wreck and its consequences is in the future and of uncertain magnitude. Although it may be natural to want to delay action, the committee has concluded that doing so would be costly and possibly perilous. With delay, revenues would have to be raised even higher or spending reduced even more to bring the debt to a prudent level while also incurring higher interest payments. With delay, also, the risk grows that the nation’s creditors—especially, those abroad—will conclude that the United States has no plan to restore fiscal stability and will therefore demand higher interest rates or make other tough economic demands. The margin for error then would be smaller, and the options for corrective action even more painful than they are today.

The committee recognizes that fiscal sustainability cannot be achieved without major near-term policy changes, particularly forceful actions to slow the growth of spending in Medicare and Medicaid. Because of the difficulty of such changes, the committee proposes that elected leaders annually assess the country’s progress and develop concrete proposals to

place the budget on a sustainable path. To do so, the committee offers a framework that everyone can use to evaluate any proposed federal budget. Our framework of six tests can be used to hold leaders accountable for their proposed budgets:

-

Does the proposed budget include policy actions that start to reduce the deficit in the near future in order to reduce short-term borrowing and long-term interest costs?

-

Does the proposed budget put the government on a path to reduce the federal debt within a decade to a sustainable percentage of GDP? Given the fiscal outlook and the committee’s analysis of the many factors that affect economic outcomes, the committee believes that the lowest ratio that is economically manageable within a decade, as well as practically and politically feasible, is 60 percent.

-

Does the proposed budget align revenues and spending closely over the long term?

-

Does the proposed budget restrain health care cost growth and introduce changes now in the major entitlement programs and in other spending and tax policies that will have cumulative beneficial fiscal effects over time?

-

Does the budget include spending and revenue policies that are cost-effective and promote more efficient use of resources in both the public and private sectors?

-

Does the federal budget reflect a realistic assessment of the fiscal problems facing state and local governments?

The President and Congress share accountability for putting and keeping the federal budget on a sustainable path. The Office of Management and Budget and the Congressional Budget Office—as well as private organizations—can make major contributions to the needed reassessment of the nation’s fiscal course by regularly publishing projections of the long-term effects of the President’s budget and of major alternatives. Those projections can be used to assess the extent to which proposals are sustainable by the tests above.

The current federal budget process does not favor forward-looking assessment and management of the nation’s fiscal position. The committee finds that the present process gives too much weight to the interests of the current generation and too little weight to the interests of future generations. If the process is an obstacle to prompt correct action, then the first step in dealing with the fiscal challenge is to reform it.

The committee favors reforming the budget process to make it more far

sighted and to establish a new regime of responsible budget stewardship. Under this new regime, leaders will be better prepared to take the political actions necessary to fairly represent the interests of the nation’s children and grandchildren and to avoid the potentially serious consequences of continuing on the present path.

If action is taken soon, the country has a wide choice of options to help achieve fiscal sustainability. All are difficult; but if action is postponed, the options will be fewer and the choices will be even more difficult. With delay, the risk of a disruptive fiscal crisis will grow, and the standard of living experienced by everyone’s grandchildren is likely to be lower than it is for people today.

The challenges are formidable, but not impossible. If the nation accepts sacrifices in the short run, it will be much stronger, safer, and more prosperous in the long run.