3

Key Current Technologies and Evolutionary Developments

INTRODUCTION

Advanced-technology sensors, coupled with data processing and fusion and networked communications, have enabled new approaches to warfighting and have been essential for reducing combat losses, minimizing collateral damage, and allowing a smaller but more effective military force. U.S. military strategy is expected to remain dependent on maintaining technological superiority, including the development of increasingly sophisticated sensor systems and new sensor types that exploit novel threat signatures. While the possibility exists that radically new sensor technologies will be invented, there are many opportunities to customize and improve the performance of existing, and in some cases relatively mature, focal plane technologies. There is an active research community pursuing these goals on a global scale. The focus of this chapter is to describe some of the likely near-term developments to existing visible and infrared (IR) detector technologies.

The proper definition of a sensing problem drives optimization of the design features of the focal plane to lead to the best system-level performance. In many cases, new sensor systems will be enabled not just by driving closer to “physical limits” but by tailoring designs and performance to be exceptionally well matched to a specific application. Clever design architectures, adding powerful on-focal-plane processing features, lowering power dissipation, increasing detector operating temperature, and dramatically reducing costs are examples of seemingly evolutionary changes that could enable revolutionary capabilities. Innovation will likely not be driven exclusively by moving closer to the physical limits of detector performance.

A number of advances, such as putting more processing into a pixel or making a smaller pixel, depend on continued improvements in silicon complementary metal oxide semiconductor (CMOS) process technology, driven by the semiconductor industry’s push to stay on the Moore’s law scaling curve. It is worth noting that device scaling is becoming increasingly technically challenging and expensive and that physical limits are becoming real roadblocks to CMOS scaling. Many process technologies developed for 65 nm, 45 nm, or 32 nm, while excellent in terms of digital circuit performance, are less than ideal for the analog portions of a pixel. They may have high transistor leakage levels and very limited dynamic range due to smaller voltage swings, thus limiting performance. Accordingly, device scaling is likely to be exploited by adding digital functionality to pixels. As more advanced CMOS process technologies are used, the cost per transistor drops, but the cost per area of CMOS chips increases. This, in turn, carries negative implications for focal planes that require physically large areas.

Advanced processes are also costly and have large nonrecurring expenses associated with design, mask generation, and initial design and debugging, making it expensive to develop custom devices needed only in small volumes. It is also worth noting that changes in the lithography processes used at smaller feature sizes require specialty techniques, such as field stitching, to produce large-area devices that exceed the field size of modern lithography tools. In short, while CMOS scaling will dramatically shape the design options for advanced focal planes, significant learning and innovation will be required to apply these advanced technologies optimally. In many cases, visible sensor applications do not benefit from the high-volume manufacturing imperatives that both drive and allow amortization of the increasing tool cost that accompanies CMOS scaling.

A number of areas in which near-term technology advances are expected include ultralarge-format arrays; mosaic tiling technologies; pixel size reduction; smarter pixels and on-focal plane processing; improved three-dimensional (3-D) integration and hybridization; higher-operating-temperature devices; multicolor pixels; improved short-wavelength infrared (SWIR) arrays; photon counting technologies and lower readout noise; curved focal surfaces; lower-power operation; radiation hardening; cost reduction; and improved cooler technology.

KEY TECHNOLOGIES EXPECTED TO DRIVE ADVANCEMENTS IN EXISTING DETECTOR TECHNOLOGIES OVER THE NEXT 10-15 YEARS

With respect to areas in which near-term technology advances are expected, this section examines each of the advances and addresses benefits, risks or drawbacks, impact on system performance, and implications for military applications of the expected advances.

Ultralarge-format Focal Plane Arrays

Progress is expected to continue in developing increasingly large arrays for the visible, SWIR, mid-wavelength infrared (MWIR), long-wavelength infrared (LWIR), and very long wavelength (VLWIR) portions of the spectrum. While both visible and IR arrays depend on the development of larger CMOS readout integrated circuits (ROICs), IR arrays have additional challenges—for example, yielding large detector arrays in difficult material systems such as mercury cadmium telluride (MCT), availability of large substrates, and developing high-yielding and small pixel-pitch bump bonding.

Low-cost and high-performance (by some metrics) CMOS active pixel sensor (APS) multi-megapixel arrays are commercially available for the visible spectrum. Charge-coupled devices (CCDs) for scientific applications are routinely made with pixel counts exceeding 20 megapixels, and the trend to ever-larger single chips will continue. Using four-side buttable tiling, CCD focal planes of 1.4 gigapixels have been made and are in use by astronomers. In addition to monolithic silicon active-pixel sensors and CCDs, hybrid megapixel visible arrays will also become more available, providing sensitivity advantages over the traditional commercial products. Visible 50-megapixel arrays are now available with digital outputs having ROIC noise levels of less than 10 electrons and offering a sensitivity advantage over consumer products.

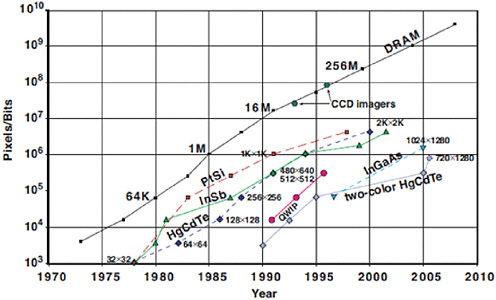

In the IR, highly sensitive, multi-megapixel infrared focal plane arrays (FPAs), up to 4 megapixels, are also widely available for the MWIR and SWIR spectrum. Recently, 16-megapixel MWIR FPAs have been demonstrated. As shown in Figure 3-1, detector array pixel count has paralleled the exponential growth of silicon dynamic random access memory (DRAM) bit capacity.1 Visible arrays with close to 100 megapixels offer the largest formats. In the IR, 16-megapixel arrays are now available.

System-level benefits of large FPAs are generally related to providing a large instantaneous field of view (FOV). As focal planes become less expensive per pixel, it increasingly makes sense to eliminate costly, power-hungry, heavy, and unreliable mechanical scanning or optical pointing systems and replace these with a fully electronic selection of the FOV by reading out a region of interest from a larger FPA. Large FPAs allow monitoring of large areas and are important for persistent surveillance applications. These FPAs enable important applications, such as high-resolution, wide-area airborne persistent surveillance and distributed aperture systems providing full spherical coverage of platforms.

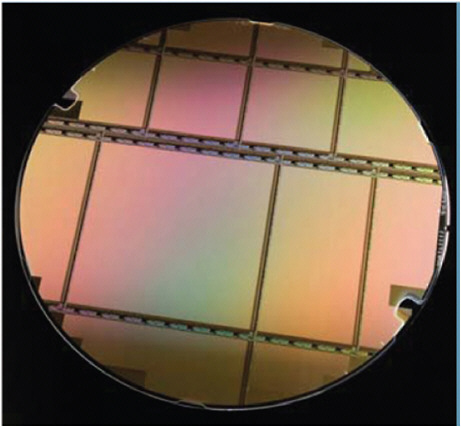

The single 8-inch ROIC wafer shown in Figure 3-2 contains 2K × 2K, 2K × 4K,

|

1 |

Paul Norton. 2006. Third-generation sensors for night vision. Opto-Electronics Review 14(1):1-10. Available at http://www.springerlink.com/content/h126r11q13747524/fulltext.pdf. Accessed March 24, 2010. |

FIGURE 3-1 Detector array pixel count has paralleled the exponential growth of silicon DRAM bit capacity. SOURCE: Paul Norton. 2006. Third-generation sensors for night vision. Infrared Photoelectronics, SPIE Proceedings Vol. 5957.

and 4K × 4K (4-, 8-, and 16-megapixel) die. Scaling up to the 16-megapixel FPA provides larger sensor FOV and improved full-Earth coverage of the ballistic missile theater. Individual larger arrays are advantageous over tiling multiple smaller FPAs and result in 100 percent coverage without the additional effort required to account for the gaps between tiled arrays.

FINDING 3-1

The evolutionary trends are semiconductor detectors characterized by increased pixel pitch and count, higher readout speed, higher operating temperature (especially MWIR), lower power consumption, and decreased sensor thickness. The need for larger fields of regard is a significant driver for larger arrays. Even beyond the diffraction limit of the optical system, oversampling can lead to slightly enhanced resolution.

Mosaic Tiling Technologies

For a number of years, visible-band CCD imagers have been built in three-side buttable and four-side buttable formats, allowing tiling of large focal planes from

FIGURE 3-2 A single 8-inch ROIC wafer from 2007 Raytheon industry research and development. SOURCE: Angelo Scotty Gilmore, Stefan Baur, and James Bangs. 2008. High-definition infrared focal plane arrays enhance and simplify space surveillance sensors. Raytheon Technology Today 1:5-8. Available at http://www.raytheon.com/newsroom/rtnwcm/groups/public/documents/content/rtn08_tech_sensing_pdf2.pdf. Accessed March 26, 2010.

smaller, higher-yielding chips, with only modest gaps between the chips. For example, the 1.4-gigapixel orthogonal transfer array CCD imager used in PanSTARRS is composed of 60 chips, each of 22 megapixels. An array of this size could not be made monolithically since it exceeds the size of the largest silicon wafers used by the IC (integrated circuit) industry. Currently, and for the better part of the next decade, silicon wafer sizes are not expected to exceed the 300 mm diameter currently in use by leading-edge semiconductor facilities, although the silicon IC industry is actively exploring a transition to 450-mm-diameter wafers. Many imaging chips are made using process technologies being run on 200-mm-diameter wafers, for both cost and technological reasons.

In many cases, the size of a silicon chip is not limited by the wafer size, but it is limited by the ability to yield working chips, which falls off rapidly with increasing chip size. Achieving high yields on large chips can be expected to be most challenging for extremely dense and complex designs using the most advanced process technologies. Tiling large arrays from smaller chips addresses the practical and economic limits of making larger monolithic chips.

While tiled arrays are already in common use in high-end scientific and military applications, there are a number of areas in which improvements can be expected. Gaps between chips can be reduced from hundreds of micrometers to as little as a few tens of micrometers, especially for monolithic technologies. Greater use of four-side buttable designs is expected. Techniques will be developed to simplify interconnections to the tiles and to lower the cost of tiled arrays. Improved manufacturability and repairability are also active areas of research.

Application areas for large-format tiled arrays with minimal seam loss are likely to include wide-FOV telescope systems with large optics and long focal lengths for such diverse applications as astronomy, space surveillance, and persistent surveillance.

Pixel Size Reduction

A general trend has been to reduce pixel sizes, and this trend is expected to continue. Several reasons exist for reducing pixel size, and the desirability of reducing pixel size is dependent on details of the application and the operating wavelength. In general, systems operating at shorter wavelengths (e.g., visible and ultraviolet) are more likely to benefit from small pixel sizes because of the smaller diffraction-limited spot size.

Diffraction-limited optics with low F-numbers (e.g., F/1) could benefit from pixels on the order of one wavelength across, as small as about 0.5 μm in the visible or about 10 μm in the LWIR. Oversampling the diffractive spot may provide some additional resolution for smaller pixels, but this saturates quickly as the pixel size is decreased.

Commercial CMOS imagers and CMOS chips have been demonstrated with pixels sized in the 1 to 2 μm range, with some examples less than 1 μm. On the silicon CMOS imager side, much of the interest in pixel size reduction has been driven by the desire to deliver a large number of megapixels to a consumer while keeping the silicon area used by the chip as small as possible to minimize cost for consumer applications, such as cell phone cameras. Interestingly, many of these cameras have low-performance optics, leading to much poorer resolution than might be expected based on the megapixel count for the imager. Visible-band small-pixel imagers are useful with small optics and can find application in unattended ground sensors as well as other systems requiring small surveillance cameras.

In the IR there remains a steady emphasis on improving uncooled microbo-

lometers that will continue to mature with smaller detector sizes and larger formats. Current products utilize a 17 μm pitch and are available in high-definition formats (640 and 1280) primarily in the LWIR band. MWIR arrays have been fabricated, but they are limited by detector noise due to the lower MWIR photon flux.

In the near future, uncooled 10-12 μm detector pitch arrays will be available in high-definition format (1920 × 1080). This reduction in pitch will enable a reduction in optics size allowing increased range capability without an increase in weight for man-portable applications.

For wide-area persistent surveillance, programs such as ARGUS-IS,2 as shown in Boxes 3-1 and 3-2, are already working on extremely large mosaics of visible FPAs to enable constant surveillance of large city areas.3 With the smaller-pitch FPAs becoming available, these types of systems should be more affordable and smaller. The technology challenge is to maintain sensitivity and reduce the thermal time constant as the pitch size is decreased. Uncooled IR technologies also will be developed that exploit piezoelectric and other temperature response mechanisms, such as bimetallic microelectromechanical systems (MEMS) structures, diode forward voltage changes, or capacitance changes.

FINDING 3-2

The global proliferation of low-cost, commodity imagers, such as cell phone cameras and automobile thermal imagers, enables adversaries to develop sensing systems at relatively low cost, reducing the barrier to achieving limited operational capabilities. As an example, the rapid proliferation of low-cost “night vision technology” is eroding the overwhelming dominance of the United States in nighttime operations, even with the superior performance of advanced systems.

FINDING 3-3

The availability of very low cost imagers developed for large consumer markets is providing opportunities to develop new sensor systems and architectures, even though the component-level imagers may not have the capabilities typical of high-performance sensors developed specifically for military applications. Additionally, the technology and manufacturing base used to make these low-cost imagers will extend the manufacturing base that can be used for fabricating customized military parts.

|

2 |

Brian Leininger, Jonathan Edwards, John Antoniades, David Chester, Dan Haas, Eric Liu, Mark Stevens, Charlie Gershfield, Mike Braun, James D. Targove, Steve Wein, Paul Brewer, Donald G. Madden, and Khurram Hassan Shafique. 2008. Autonomous Real-time Ground Ubiquitous Surveillance—Imaging System (ARGUS-IS) Defense Transformation and Net-Centric Systems. Proceedings of SPIE 6981:69810H. |

|

3 |

The data management challenges posed by a system such as ARGUS-IS are addressed in Chapter 4. |

RECOMMENDATION 3-1

The intelligence community should pay careful attention to the new capabilities inherent in both the proliferation of commodity detector technologies and their integration into novel sensor systems. ARGUS-IS and Gnuradio are examples of how available, low-cost, mature commodity visible FPA technology (cell phone camera chips) and commercial off-the-shelf (COTS) communications circuitry, through sensor integration, have enabled new, advanced, high-performance imaging capabilities.

Smarter Pixels and On-focal-plane Processing

A trend has been to take advantage of progress in electronics scaling to integrate as many functions as possible on a single chip. Visible-band CMOS active pixel sensors are particularly well developed examples of this trend. Usually the desire is to achieve cost reductions for high-volume applications by having a single-chip solution, but monolithic integration can also have other substantial benefits, such as power and noise reduction and enabling new interconnection-rich processing architectures that would not be feasible using off-chip inputs and outputs.

In the IR and high-performance visible imaging area, fully digital focal planes are just entering the market. In some cases their electro-optical (EO) performance exceeds that of traditional analog focal planes coupled to discrete electronics. High-performance IR scanners and large-area staring visible digital focal planes pixels are currently being demonstrated and show size, weight, and power (SWaP) advantages. On-ROIC digital logic enables future digital signal processing such as nonuniformity correction (NUC), image stabilization, and compression. These focal planes will enable much smaller systems (microsystems). This technology is poised to go into large-area cryogenic infrared sensors over the next few years.

Sending data off-chip requires substantial power and sending those data through communication links—for example, a radio-frequency (RF) link for an unattended ground sensor—can be even more energy intensive. There is increasing recognition of the value of trying to identify and transmit only small amounts of high-level and actionable information rather than large numbers of raw data bits. This is particularly important for systems with severe power or communication bandwidth constraints. This is leading to specialized imaging chips that have on-chip processing tuned to a specific application. Such customization can lead to dramatic improvements in system performance, but it has the drawback that longer design and fabrication cycles and large nonrecurring costs may be required to make application-specific chips.

The amount of processing that can be placed right at the pixel has generally been limited by the modest numbers of transistors that can be placed within a small pixel. Moore’s law device scaling has steadily been improving that situation, and focal planes are now being developed with reasonably small pixels and significant

|

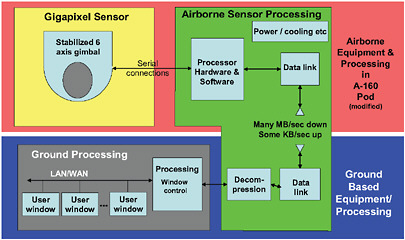

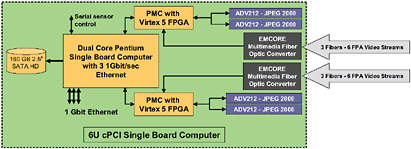

BOX 3-1 Case Study: DARPA ARGUS-IS The DARPA ARGUS-IS unmanned aerial system is designed for persistent surveillance and incorporates a 1.8-gigapixel composite visible sensor system composed of 184 FPA pairs, for a total of 368 FPAs. ARGUS-IS is demonstrating on-board real-time processing of wide-area video imagery. Figure 3-1-1 depicts the components of the system. Figure 3-1-2 outlines the specific on-board processing solution, details of which are discussed in Chapter 4, and Figure 3-1-3 provides a sample output image.  FIGURE 3-1-1 ARGUS-IS block diagram. SOURCE: Leininger, Brian, Jonathan Edwards, John Antoniades, David Chester, Dan Haas, Eric Liu, Mark Stevens, Charlie Gershfield, Mike Braun, James D. Targove, Steve Wein, Paul Brewer, Donald G. Madden, and Khurram Hassan Shafique. 2008. Autonomous Real-time Ground Ubiquitous Surveillance-Imaging System (ARGUS-IS). Proceedings of the SPIE 6981:69810H-1.  FIGURE 3-1-2 ARGUS-IS airborne processing module. SOURCE: Leininger, Brian, Jonathan Edwards, John Antoniades, David Chester, Dan Haas, Eric Liu, Mark Stevens, Charlie Gershfield, Mike Braun, James D. Targove, Steve Wein, Paul Brewer, Donald G. Madden, and Khurram Hassan Shafique. 2008. Autonomous Real-time Ground Ubiquitous Surveillance-Imaging System (ARGUS-IS). Proceedings of the SPIE 6981:69810H-1. |

|

BOX 3-2 Impact of Commodity Components One observation to highlight is the use of readily available commodity components in the ARGUS-IS system; the ARGUS-IS designers state: Though many other processing solutions exist, the rapid deployment schedule implied use of low-risk COTS [commercial off-the-shelf], or close to COTS, processing hardware. Hence, other processing elements were considered, but rejected for various reasons including: power consumption (multicore central processor units (CPUs) and graphics processor units (GPUs)), lack of configurability and development time (custom ASICs), or lack of proven integration tools or processing margin. Multicore processors and GPUs have become COTS since 2007 and enjoy certain performance and power benefits. More importantly, the observation about rapid deployment schedules using commodity components has not been lost on other design teams (e.g., at the Iran University of Science and Technology,a Xidian University,b and Nanjing University of Science and Technology).c Additional examples of commercial developments relevant to the communication architectures of remote imaging systems include the Gnuradio architecture,d with its signal processing architecture partitioned between a universal software radio peripheral with selectable daughtercards and a host processor with more or less arbitrary signal processing performance. A third example is the use of multiple-input multiple-output (MIMO)e,f in radio systems, where multiple antennas and significant signal processing are used to overcome localized radio-frequency challenges such as multipath.

|

in-pixel processing. As an example, digital FPAs with per-pixel analog-to-digital conversion, high-dynamic-range digital integration, and simple but powerful signal processing primitives have been demonstrated.

3-D Integration and Improved Hybridization Technology

Most IR and some visible technologies require hybridization of a detector array with a silicon CMOS readout IC. The detector pixels are generally connected to the per-pixel electronics through indium bump bonds. While bump-bond pitches of 14 μm or larger are relatively common, pitches of less than 8 μm offer significant challenges in terms of array yield, pixel operability, and cost. It can be expected that developments will continue to extend bump-bonding technology to smaller pixels, as well as to improve manufacturability and reduce cost at all pixel sizes.

One research area has been in the development of 3-D integration technologies providing alternatives to bump bonding. For example, oxide-to-oxide wafer bonding and silicon on insulator (SOI)-based 3-D integration have been used to demonstrate SWIR arrays integrated to CMOS with pitches down to 6 μm.

In the past, much of the processing done on a focal plane was confined to the two-dimensional real estate directly under a given pixel. Recently as many as three layers of CMOS have been stacked and vertically interconnected, offering the potential to increase the amount of processing available within a pixel footprint. 3-D integration technology has been applied to photon counting readouts for laser detection and ranging (LADAR) as well as to visible-band passive imagers. This stacked approach allows additional processing real estate in layers under the traditional sensor chip assembly.

A number of process approaches are being explored, including methods using through-wafer vias, wafer-bonded SOI electronics, and thin detector layers attached with epoxy. This technology will allow for higher-performance analog detector amplifiers and will enable on-chip and in-pixel processing of digital video and image data on large-area staring arrays.

Devices Able to Perform at Higher Temperatures

Increasing the operating temperature is of particular concern for high-performance IR detectors, since the power needed for cooling increases significantly as the operating temperature is dropped. The power savings that result from reduced cooling requirements are particularly important for space systems, for sensors used by dismounted soldiers, and for power-constrained unattended ground sensors. While high operating temperature work is generally focused on the MWIR and LWIR, even silicon visible sensors used in applications requiring long integration times must be cooled to reduce dark current, and improvements in

dark current at higher temperatures have enabled the elimination of thermoelectric coolers or a reduction in their power consumption.

High-temperature MWIR detectors will simplify future space systems by eliminating the cold FPA stage. Current space-based MWIR detectors must be cooled to temperatures in the 70 K range in order to reduce noise produced by the detectors and enable background-limited IR photodetection (BLIP). Raising the operating temperature to that of the optical bench will eliminate second-stage cryogens or mechanical coolers. Several competing technologies hold some promise in this area.

As the performance of MCT MWIR continues toward higher temperatures, new detector technologies, such as strained-layer superlattices (SLS), have some promise at high temperatures as well. The band structure of indium arsenide-gallium antimonide allows optimization of the carrier effective mass that theoretically enables detectors to have higher operating temperatures and longer cutoff wavelengths. Because the SLS detectors behave as direct bandgap devices, they avoid the quantum efficiency problems that have affected other III-V detector approaches such as quantum-well infrared photodetectors (QWIPs) and quantum-dot infrared photodetectors (QDIPs).

The literature on SLS detectors is quite active, and limiting behavior has yet to be established. The results to date are quite dependent on the epitaxial growth and processing-induced defects, much as the situation was for MCT a number of years ago. A recent review4 provided the snapshot in Table 3-1. While there is much work to be done, it appears that SLS detectors will at least provide some competition for MCT FPAs because of the more mature III-V technology and the possibilities of bandgap engineering. One example of the bandgap engineering possibilities is the nBn (or n-type/n-barrier/n-type device [and related pMp]) structure that promises to reduce generation-recombination dark currents.5 The pMp structure has shown some advantage for LWIR6 and may be extensible to the MWIR. These developments are just being reported by research groups, with varying success. This work is likely to mature in the next 10 to 15 years and, if its early promise is fulfilled, may find its way first into military systems and then to lower-cost commercial applications.

TABLE 3-1 Comparison of State-of-the-Art Type II Strained-layer Superlattice Photodiodes and nBn Photodetectors for MWIR Detection at Elevated Temperatures

|

Parameter |

Kim et al. (2008)a |

Plis et al.(2007)b |

Wei et al.(2006)c |

Razeghi et al.(2010)d |

|

Device |

nBn |

nBn |

pin SLS |

pin SLS |

|

Cutoff wavelength, μm |

4.2 |

4.5 |

4.9 |

4.2 |

|

Dark current density, A cm−2 (77 K) |

1.0 × 10−7 |

5.0 × 10−7 |

4.0 × 10−8 |

3.3 × 10−9 |

|

Dark current density, A cm−2 (high T) |

NA |

0.15 (240 K) |

0.2 (240 K) |

0.05 (240 K) |

|

Responsivity, A/W (77 K) |

1.6 |

0.7 |

1.0 |

NA |

|

D* Jones (77 K) |

6.7 × 1011 |

2.0 × 1012 |

1.5 × 1013 |

3 × 1013 |

|

D* Jones (high T) |

NA |

2.0 × 109 (240 K) |

1.0 × 109 (300 K) |

1.2 × 1010 (240 K) |

|

NOTE: NA = not available. aH.S. Kim, E. Plis, J.B. Rodriguez, G.D. Bishop, Y.D. Sharma, L.R. Dawson, S. Krishna, J. Bundas, R. Cook, D. Burrows, R. Dennis, K. Patnaude, A. Reisinger, and M. Sundaram. 2008. Mid-IR focal plane array based on type-II InAs/GaSb strain layer superlattice detector with nBn design. Applied Physics Letters 92(18):183502. bE. Plis, J.B. Rodriguez, H.S. Kim, G. Bishop, Y.D. Sharma, L.R. Dawson, and S. Krishna. 2007. Type II InAs/GaSb strain layer superlattice detectors with p-on-polarity. Applied Physics Letters 91(13):133512. cY. Wei, A. Hood, H. Yau, A. Gin, M. Razeghi, M.Z. Tidrow, and V. Nathan. 2005. Uncooled operation of type-II InAs/GaSb superlattice photodiodes in the midwavelength infrared range. Applied Physics Letters 86(23):233106. dM. Razeghi, B.M. Nguyen, P.Y. Delaunay, S.A. Pour, E.K. Huang, P. Manukar, S. Bognadov, and G. Chen. 2010. High operating temperature MWIR photon detectors based on type II InAs/GaSb superlattice. Proceedings of SPIE 7608:76081Q. |

||||

Multicolor Pixels

Multiband detectors provide independent sensing of different spectral bands within individual pixels.7 The multiband feature provides the ability to optimize detection and identification functions of the sensor system. Multiband detectors enable increased mission robustness due to their ability to provide optimum imagery over a wide range of atmospheric and battlefield scenarios. In addition, when combined with advanced signal processing and fusion algorithms, multiband FPAs provide enhanced target detection and discrimination capability.

Multiband FPAs are currently available in small and standard television formats. These will be further developed and will be available in more spectral regions.

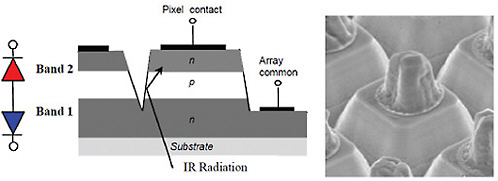

The FPAs currently operate mainly in the MWIR and LWIR bands. These will be expanded to offer SWIR and possibly visible capabilities in conjunction with MWIR and LWIR. A wider spectrum choice for multiband operation will enable new and more robust systems that provide better target recognition and identification. Figure 3-3 illustrates the architecture and morphology of single-bump, two-color detectors.

Hyperspectral detectors, separating and sensing hundreds of bands at once, will have a significant effect on materials identification, including gases and volatile materials (ranging from pollutants to explosives), and provide the ultimate passive countermeasure to camouflage.8 Hyperspectral sensors will be developed in all sizes, from handheld or wall-mounted field units to remote sensing instruments aboard aircraft or spacecraft.

While the MCT material system has been the dominant material used for dual-band MWIR and LWIR focal planes, work is going on with other materials and device types.

QWIPs generally have lower quantum efficiency (QE) and limited bandwidth, remain a niche U.S. technology, and are used more often in long-wave applications, especially for the international military market. The low QE arises as a result of the limited thickness of the multi-quantum-well absorbers and the requirement of a grating or other optical device, since the absorption requires an electric field directed across the quantum well, which is not available for normal incidence radiation. The Department of Defense (DOD) has not made significant use of this approach because of these limitations. For certain multicolor applications, narrow-bandwidth QWIPs may be appropriate. In addition, a corrugated QWIP (C-QWIP) approach has the potential to improve performance for both QE and bandwidth, if ever implemented (see additional discussion on nanophotonics in Chapter 4).

QDIPs are an alternate emerging technology that presents some promise at the research stage but remains unproved for commercial and military applications.9 The many degrees of freedom offered by a quantum dots in a well (DWELL) detec-

|

8 |

“Multispectral deals with several images at discrete and somewhat narrow bands. The “discrete and somewhat narrow” is what distinguishes multispectral in the visible from color photography. A multispectral sensor may have many bands covering the spectrum from the visible to the longwave infrared. Multispectral images do not produce the “spectrum” of an object. Landsat is an excellent example. Hyperspectral deals with imaging narrow spectral bands over a contiguous spectral range and produces the spectra of all pixels in the scene. So a sensor with only 20 bands can also be hyperspectral when it covers the range from 500 to 700 nm with 20 10 nm wide bands (while a sensor with 20 discrete bands covering the visible, near infrared, SWIR, MWIR, and LWIR would be considered multispectral). SOURCE: http://en.wikipedia.org/wiki/Hyperspectral_imaging. Last accessed on June 17, 2010. |

|

9 |

A.V. Barve, S.J. Lee, S.K. Noh, and S.K. Krishna. In press. Review of current progress in quantum dot infrared photodetectors. Laser & Photon Rev DOI 10.1002/lpor.200900031. |

FIGURE 3-3 A cross section diagram (left) and scanning electron microscope image (right) illustrate the architecture and morphology of single-bump two-color detectors. The lower junction (Band 1) responds to shorter-wavelength radiation, while the upper junction (Band 2) responds to longer wavelengths. SOURCE: King, Donald F., Jason S. Graham, Adam M. Kennedy, Richard N. Mullins, Jeffrey C. McQuitty, William A. Radford, Thomas J. Kostrzewa, Elizabeth A. Patten, Thomas F. Mc Ewan, James G. Vodicka, and John J. Wootan. 2008. 3rd-generation MW/LWIR sensor engine for advanced tactical systems. Proceedings of SPIE 6940:69402R.

tor allows multicolor operation in a single device by accessing intradot transitions (VLWIR), QD-QW transitions (LWIR), and QD-continuum transitions (MWIR). These can be accessed with different bias voltage regimes. A significant advantage of QDIPs is that, in contrast to QWIPs, they are sensitive to normal incidence radiation, but they still suffer from generally low quantum efficiency as a result of the small absorption volume. This can be mitigated with plasmonic structures, as discussed in Chapter 4. Table 3-2 provides a snapshot of the current state of development of LWIR detectors across all of the various material systems.

Visible imaging sensors often use integrated color filters to achieve red, green, blue (RGB) color model capability, though high-performance systems may use dichroic filters to make optimum use of photons. There is room for innovation in the visible sensor area to make multispectral and hyperspectral sensors, especially ones that use photons efficiently.

FINDING 3-4

Existing, mature mercury cadmium telluride, indium antimonide, indium gallium arsenide, silicon charge-coupled devices, silicon complementary metal oxide semiconductors, and avalanche photodiode focal plane technologies provide sensors with excellent performance and set a very high barrier to entry for any emerging technology. For some performance parameters, such

TABLE 3-2 Comparison of LWIR Existing State-of-the-art Device Systems for LWIR Detectors

as detectivity, mature imager technologies already are operating very close to fundamental limits. However, there is still considerable opportunity to improve other parameters such as operating temperature, power dissipation, manufacturability, and cost.

Improved SWIR Arrays

Access to the SWIR band provides the tactical advantage of being able to see in a band that has more night illumination than the visible and near-IR bands and that sees signals from all current laser designators, pointers, and range finders. The SWIR-equipped soldier can see adversaries equipped with night vision goggles without being detected, since the SWIR devices are totally passive, in contrast to image intensifiers that radiate as well as detect. A low-cost, low-power, high-resolution SWIR technology could replace the U.S. inventory of night vision

goggles and, until fielded by the competition, would provide a significant advantage under low-light conditions. Despite potential advantages, SWIR technology is still not in wide use, compared to image-intensifier-based night vision goggles. SWIR FPAs will be available with increased sensitivity, lower power, smaller pixels, and larger formats.

Currently, the 320 × 240 format is commonly available, with 640 × 480 entering the market. High-definition formats are being developed and will be available for fielding in the near future. Improvements in readout application-specific integrated circuits and detector materials have resulted in SWIR FPAs having noise levels of a few electrons. This will result in high-definition formats capable of matching light levels of image intensifiers but with extended spectral response for night glow applications and a digital interface supporting advanced processing, such as multiband fusion. Technologies that are capable of counting individual photons are currently in the early stages of development and can be expected to yield usable focal planes within 10 years. Low-power, very small cameras will transmit digital SWIR images for weeks, enabled by a combination of lower-power electronics, room-temperature detector operation, and improved batteries. The technology will also be available in 50-megapixel formats for other applications, such as airborne surveillance.

The principal game changers in SWIR will be technologies that can significantly reduce the cost of FPA fabrication, currently a material or process yield issue, facilitate finer-pitch FPAs (less than 10 μm), or exhibit dark current densities that best InGaAs at any cutoff wavelength or operating temperature.

FINDING 3-5

Short-wave infrared (SWIR), due to an atmospheric phenomenon called night glow, is emerging as a next-generation tactical imaging technology because of its covertness and the similarity between SWIR and visible imagery. As it matures, SWIR will provide an alternative to intensified visible imaging (night vision goggles).

Photon Counting Technologies and Lower Readout Noise

Three different technological paths will result in lower readout noise levels or even single-photon sensitivity:

-

For visible imagers, improvements in analog readout technology will continue, increasing the range of devices capable of sub-single-electron noise levels.

-

Innovative approaches to add modest amounts (5-100×) of linear gain to the photon detection process (such as linear-mode avalanche gain) will be pursued, to reduce the input-referred noise from the readout.

-

Significant numbers of new focal planes capable of direct photon-to-digital conversion will appear. For example, Geiger-mode detector arrays that have been developed for UV, visible, and SWIR, and are already used in active imaging systems such as direct detection LADAR, will be further developed and applied to passive photon counting imaging applications in increasingly large array sizes.

Photon counters have a number of important applications, including some low-light imaging applications, hyperspectral sensors, high-speed imaging, 3-D LADAR, and dual-mode active-passive pixels.

FINDING 3-6

Rapid progress is being made in the development of closely related single-photon and photon counting detectors and arrays. Single-photon detection and photon counting imagers are key enablers for a wide range of new secure communications, passive sensors, 3-D LADAR, and active optical sensors. Specifically, quantum cryptography relies on the distribution of entangled, single-photon qubits (keys) between the transmitter and receiver; this is inherently a single-photon process. In most cases, these applications involve physical processes in which only a small number of photons are available for detection. These detectors require high quantum efficiencies, low dark count rates, fast recovery times, and capabilities for photon number resolving.

RECOMMENDATION 3-2

The intelligence community should carefully track developments related to single-photon and photon counting detectors across the full spectrum from UV to VLWIR. Table 3-3 lists trigger events that would cause a significant shift in capability and should be carefully monitored by the intelligence community.

TABLE 3-3 Trigger Points of Technical Progress and Their Implications

Curved Focal Surfaces

Over the last decade, the ability to make cylindrically or spherically curved silicon imagers has been demonstrated, and recently a focal plane comprised of spherically curved silicon CCD imagers has been developed for a ground-based telescope. It is likely that these technologies will be refined and extended to other wavelengths (IR) and other detector materials systems. Curved focal planes can simplify the design of wide-FOV optics and allow lighter-weight solutions for high-performance imaging systems on size- and weight-constrained platforms, such as small unmanned air systems. The utility of curved focal planes becomes evident when one realizes that the human retina is curved, because this dramatically simplifies the design and complexity of the lens.

Lower Power

Moore’s law scaling of CMOS technology has led to steady reductions in the power consumed, especially for digital logic operations. Clever circuit design and architectural approaches also lead to dramatic power reductions. It is expected that further reductions in power can be achieved over the coming decade. Since many military systems operate with severe power and cooling constraints, these power reductions will result in the increased feasibility of many systems. In the case of cooled IR systems, power dissipated on the ROIC must be removed through the cooler, incurring another large power penalty, so lower-power ROIC designs are particularly desirable.

Radiation Hardening

Space systems are of critical importance for defense, and they drive the requirements for radiation-hard imagers.10 The hardness level required depends on the orbit and lifetime. Although beyond the scope of what can be discussed here, shortfalls and opportunities for improvement do exist for certain imaging technologies in certain environments, and important improvements can be expected over the coming decade. A general discussion of radiation hardness is provided in Appendix C.

Cost Reduction

Visible sensors, such as interline-transfer CCDs and CMOS active-pixel sensors, have seen dramatic cost reductions as large commercial markets, such as consumer cameras and cell phone cameras, have driven large production volumes. These parts are high performance in the sense that they represent state-of-the-art technology and are highly optimized for their intended markets. These parts may also be very low performance compared to parts optimized for a specific DOD application. While these low-cost, consumer-driven parts are not expected to replace all high-performance custom parts, they are opening up new approaches to DOD sensors because of their low cost and high performance-price ratio. One example is the recent use of large numbers of multi-megapixel cell phone CMOS imagers in wide-FOV video surveillance applications and airborne persistent surveillance systems (see above and Chapter 4 for additional information on this system). The proliferation of low-cost, visible sensors offers opportunities for DOD if it is quick to exploit this technology; however, such technologies are proliferated globally and are also accessible to current and potential adversaries.11

As discussed above, in the IR, alternatives to MCT such as InAs-GaSb SLS detectors may provide both a large decrease in cost and an increase in key performance capabilities. This detector technology will exploit the established III-V technology and manufacturing base and may also avoid some of the inherent producibility challenges associated with II-VI IR detectors. These materials can be grown by more traditional III-V molecular beam epitaxy (MBE) wafer vendors that can provide these wafers to the IR industry very much as bulk InSb wafers are supplied today. If successful, these material systems would enable an evolutionary cost reduction in sensors due to simpler technology requirements once it has been established. SLS devices are predicted theoretically12 to have lower dark currents than HgCdTe; SLS is limited by Shockley-Read generation mechanisms that produce current via point defects in the as-grown material.13,14,15 Future advancements in SLS technology will require a significant effort and investments to reduce the defect densities.

|

11 |

There is a fuller discussion of these trends in Chapter 4. The ready availability of capable, off-the-shelf imagers will have a dramatic impact on the availability of future imaging systems for friends and foes alike. |

|

12 |

M.E. Flatte and C.H. Grein. 2009. Theory and modeling of type-II strained-layer superlattice detectors. Proc. SPIE 7222:72220Q. |

|

13 |

J. Pellegrino and R. DeWames. 2009. Minority carrier lifetime characteristics in type II InAs/GaSb LWIR superlattice n+πp+ photodiodes. Proc. SPIE 7298:72981U. |

|

14 |

D.R. Rhiger, A. Gerrish, and C.J. Hill. 2008. Estimation of carrier lifetimes from I-V curve fitting for InAs/GaSb and HgCdTe LWIR diodes. Proc. MSS Parallel Meeting. |

|

15 |

M.E. Flatte and C.H. Grein. 2009. Theory and modeling of type-II strained-layer superlattice detectors. Proc. SPIE 7222:72220Q. |

Both cost reduction and the multiple open-source supplier structure of SLS detectors could have significant impacts in the widespread proliferation of large-format IR FPA technology.

FINDING 3-7

There is significant opportunity to customize image sensor architectures for specific applications that can lead to dramatic improvements in system-level performance, including size, weight, and power. Advanced architectural design, including integration of sensing and processing (in-pixel and on-chip), can have greater system-level impact than making small gains in driving detector performance incrementally closer to fundamental detectivity limits.

RECOMMENDATION 3-3

The intelligence community should evaluate and track system capabilities rather than focusing solely on component technical achievements. These include technologies that enable in-pixel and on-chip processing, lower-power operation, and higher operating temperatures, as well as technologies that improve manufacturability.

Improved Cooler Technologies

The availability of improved cooler technology can have a huge impact on the system-level performance of detector systems and may make or break whether a given focal plane technology can be considered for a given application. At least four dimensions for improvements in coolers can be identified—each dimension results in different system impacts—including the following:

-

Development of higher-coefficient-of-performance coolers: Visible and SWIR systems using thermoelectric coolers, as well as IR systems using refrigeration cycles, would benefit from more efficient coolers, because cooling power often dominates total sensor power consumption. This is particularly important for power-constrained systems, such as unattended ground sensors, and systems that are used only intermittently but must continuously be in a ready-to-operate state.

-

Reliability improvements and space qualification: A number of space systems would benefit from the availability of highly reliable and fully qualified cryogenic coolers.

-

Lower cost: For systems that must be produced in large quantities—for example, for individual soldiers—and especially for “disposable” systems, low cost is critical.

-

More compact form factor: The availability of compact and lightweight

-

coolers is a prerequisite for a number of applications. An example would include deployment of an imaging system on a micro-air vehicle.

Temperature control and stability are crucial parameters in determining the ultimate resolution, signal to noise, and other performance attributes of various IR and visible EO detectors. For this reason, detectors are often categorized as being either cooled or uncooled. Cooled detectors refer to platforms that require cryogenic temperatures in order to operate. Typical temperatures of operation for cooled sensors range from <10 to 150 K or slightly higher. Uncooled detectors, despite their title, typically incorporate some degree of temperature control near or slightly below room temperature (~250-300 K) to minimize noise, optimize resolution, and maintain stable operating conditions. The two technologies currently available for addressing the cooling requirements of IR and visible detectors are closed-cycle refrigerators and thermoelectric coolers. Closed-cycle refrigerators can achieve the cryogenic temperatures required for cooled IR sensors, while thermoelectric coolers are generally the preferred approach to temperature control for uncooled visible and IR sensors.

Although uncooled sensors offer significant advantages in terms of cost, life-time, and SWaP, cooled sensors offer significantly enhanced range, resolution, and sensitivity as a result of the reduced dark current and, therefore, lower-noise operation. For this reason, cooled IR sensors have been the technology of choice for many military operations where performance, not cost, is the prime driver. Conversely, for many commercial applications, uncooled sensors are the preferred technology because of their lower cost and higher reliability. In this section, the current status of various cooling technologies is reviewed with respect to their present and near-term applicability to IR and visible detectors.

Thermoelectric coolers and closed-cycle or mechanical refrigerators both involve the use of a working “fluid” to transfer heat from a thermal source to a thermal sink. The major difference between the thermoelectric and mechanical cryocoolers is the nature of the working fluid. A thermoelectric cooler is a solid-state device that uses charge carriers (electrons or holes) as a working fluid, whereas mechanical cryocoolers use a gas such as helium as the working fluid. While each cooling technology has its advantages and disadvantages, limitations in these cooling technologies translate directly to performance limitations in the IR and visible detectors to which they are applied. Conversely, any improvements and breakthroughs achieved in cooling technologies could provide enhancements to detector applications in SWaP metrics and in overall detector performance.

Cryocoolers

As mentioned previously, mechanical cryocoolers or refrigerators represent the only currently available technology that can reach the cryogenic temperatures

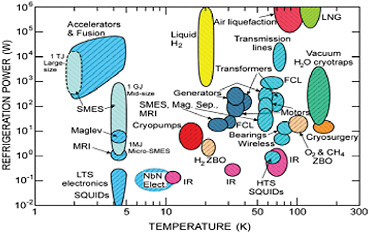

required for many IR and visible sensors. As shown in Figure 3-4, cooling of IR sensors represents one of a number of commercial and research applications for cryocoolers. The major commercial applications for mid- to large-scale cooling include cryopumps for semiconductor fabrication facilities, magnetic resonance imaging (MRI) magnet cooling, and gas separation and liquefaction. For low-power applications, IR sensors represent the largest single application for cryocoolers.

The most common types of cryocoolers can be classified as either recuperative or regenerative. In recuperative systems, gas flows in a single direction. The gas is compressed at ambient fixed temperature and pressure and allowed to expand through an orifice to the desired cryogenic fixed temperature and pressure. The Joule-Thompson and Brayton cycle refrigerators are examples of recuperative systems. In a regenerative system, the gas flow oscillates back and forth between hot and cold regions driven by a piston, diaphragm, or compressor, with the gas being compressed at the hot end and expanded on the cold end. Stirling, Gifford-McMahon, and Pulse Tube cryocoolers are the most common types of regenerative cryocooler systems.

An important parameter in measuring the performance of a cryocooler is the coefficient of performance (COP). COP is a measure of efficiency and is defined as the ratio of cooling power achieved at a particular temperature to total electrical input power to the cryocooler. Often, the COP is given as a fraction of the ideal

FIGURE 3-4 Cooling of IR sensors represents one of several commercial and research applications for cryocoolers. NOTE: FCL = freon coolant line; HTS = high-temperature superconductivity; LNG = liquid natural gas; LTS = low-temperature superconductivity; MRI = magnetic resonance imaging; SMES = superconducting magnetic energy storage; SQUID = superconducting quantum interference device; ZBO = zero boil-off. SOURCE: Radebaugh, Ray. 2009. Cryocoolers: the state of the art and recent developments. Journal of Physics: Condensed Matter 21:164219.

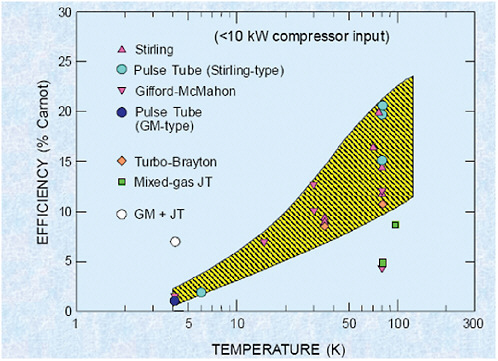

or Carnot efficiency, which is defined as the ratio of Tc/(Tc – Th), where Tc and Th refer to cold and hot temperatures, respectively, of operation. In general, recuperative systems have advantages in terms of reduced noise and vibration, whereas regenerative systems tend to obtain higher efficiencies and greater reliability at the temperatures of interest for many IR detector applications. The relative performances of the different technologies as a fraction of the limiting Carnot efficiency are shown in Figure 3-5.

Significant developments in cryocooler technologies during the past several decades have facilitated their increased use in commercial markets. One major area of improvement has been reliability. Because impurities in the working gases can freeze and either clog or damage the various internal components of a cryocooler responsible for gas flow, maintaining a high-purity gas over the lifetime of the cryocooler is a key challenge. The development of novel adsorber materials and designs, as well as improved sealing techniques for maintaining the high pressures required

FIGURE 3-5 Relative performances of the different technologies as a fraction of the limiting Carnot efficiency. SOURCE: Radebaugh, Ray. 2009. Cryocoolers: the state of the art and recent developments. Journal of Physics: Condensed Matter 21:164219.

for cryocooler operation, has significantly contributed to the improved lifetimes now achievable in many cryocooler systems (5,000-10,000 hours). Improvements in heat exchanger and recuperator designs and materials have yielded absolute COP values for cryocoolers in the range of 0.01 to 0.1 for IR detector applications. Despite these advances, the cryocooler remains a major failure point for cooled IR detectors, as well as more than doubling the weight and power requirements of the integrated IR sensor system.

While the needs of commercial and military cryocooler applications will continue to drive improvements in cost, reliability, and efficiency, it is likely that these improvements will be incremental over the next 10-15 years. Areas for improvement include the ability to operate regenerative systems at higher frequency and the ability to operate using gases at higher pressures.16,17 Operation at higher frequency enables the use of smaller, lighter-weight compressors that are often the dominant volume in regenerative cryocoolers. Similarly, increasing the gas pressure can enable larger COP by increasing the effective thermal capacitance per cycle of operation. Designs and concepts currently being considered for operation at higher frequency and pressure, as well as ongoing material and process developments, will ultimately lead to improved seals and structural performance for cryocooler components and enclosures.18 There will likely continue to be a trade-off between cost and performance as commercial and military demands for improvements in SWaP drive the technology to more demanding operating conditions where maintaining lifetimes in excess of 10,000 hours will continue to be a challenge.

Thermoelectric Coolers

Thermoelectric materials can be used to convert thermal energy to electricity or to use electricity to pump heat. In a generator configuration, thermoelectric devices exploit the Seebeck effect—the voltage created between two dissimilar conductors in the presence of a temperature difference. Thermoelectric coolers work by exploiting the Peltier effect, which refers to the creation of heat flux at the junction of two dissimilar conductors in the presence of current flow. In either configuration, the optimal performance of a given set of thermoelectric materials in a device is determined by the dimensionless figure of merit ZT = S2σ/κ, where S = Seebeck coefficient (thermopower), σ = electrical conductivity, κ = thermal conductivity, and T is the average temperature (T1 + T2)/2. Due to performance

limitations, thermoelectric generators and coolers have found only a few niche commercial applications. As generators, these applications include radioisotope thermoelectric generators (RTGs) for space applications and waste heat conversion to power small electric devices such as fans, lights, or battery chargers. Commercial applications of thermoelectric coolers include (1) climate-controlled seating for automobiles; (2) temperature control and stability for bolometric and ferroelectric detectors, laser diodes, and ink jet printers; (3) dark-current reduction in mid-wave IR detectors; and (4) noise reduction in CCD arrays.

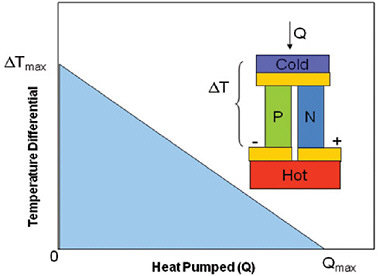

Thermoelectric coolers are essentially solid-state heat pumps where the flow of thermal energy is determined by the polarity of the applied current. The coefficient of performance for a thermoelectric cooler is a function of ZT as well as the overall temperature difference between the hot side and the cold side of the cooler. At maximum temperature difference, ∆T, the COP of a thermoelectric generator goes to zero (i.e., no heat can be removed). Conversely, at zero ∆T, a thermoelectric cooler achieves maximum heat pumping capacity. The typical load profile for a thermoelectric cooler is shown in Figure 3-6. Therefore, for most thermal management applications, including temperature stabilization for IR and visible

FIGURE 3-6 Typical load profile for a thermoelectric cooler. SOURCE: Rama Venkatasubramanian and colleagues, Research Triangle Institute, Research Triangle Park, N.C.

“uncooled” detectors, thermoelectric coolers typically operate at the minimal ∆T that provides acceptable detector performance.

Historically, the maximum achievable material ZT stood at ~1 and saw little improvement despite many decades of research starting in the 1960s through the early 2000s. However, in the early 1990s, DOD began investing significant research-and-development funding to explore the potential for achieving higher ZT values for both cooling and power generation applications. These investments paid off with the reports of breakthrough ZT values in low-dimensional thin-film thermoelectric materials. The enhancement in ZT achieved via nanostructuring in thin-film materials has prompted similar investigations in bulk materials. Recent reports have indicated that bulk thermoelectric performance in the ZT range of about 1.5 near room temperature and approaching 2.0 at higher temperatures is achievable.19

The bulk material discoveries have prompted the formation of several commercial new start companies—for example, GMZ and ZT Plus—and it is likely that these activities will transition directly to improved thermoelectric devices within the next 5-10 years. The potential impact of the thin-film materials is less certain since reproducibility, scalability, and fabrication costs remain significant challenges. For this reason, they are discussed in detail in Chapter 4. This section focuses on what is currently achievable with existing bulk commercial thermoelectric materials and what developments are likely to occur over the next 10-15 years.20

Current commercially available thermoelectric coolers are based on alloys of bismuth telluride and antimony telluride materials. These materials exhibit ZT values close to 1 unity, but in a device configuration achieve values closer to ZT = 0.7. In a single-stage device, this equates to a maximum ∆T of about 70 K as measured from an ambient temperature of ~ 293 K. An approximation of maximum achievable ∆T can be obtained using the relationship ![]() However, as previously mentioned, at maximum ∆T, a thermoelectric cooler cannot dissipate any heat. Therefore, in order to achieve ∆T of 70 K or more and still have some cooling capacity, thermoelectric coolers are stacked in “stages.” The idea is to have each stage operating at less than ∆Tmax, with its “hot” side starting at the “cold”

However, as previously mentioned, at maximum ∆T, a thermoelectric cooler cannot dissipate any heat. Therefore, in order to achieve ∆T of 70 K or more and still have some cooling capacity, thermoelectric coolers are stacked in “stages.” The idea is to have each stage operating at less than ∆Tmax, with its “hot” side starting at the “cold”

|

19 |

Poudel, Bed, Qing Hao, Yi Ma, Yucheng Lan, Austin Minnich, Bo Yu, Xiao Yan, Dezhi Wang, Andrew Muto, Daryoosh Vashaee, Xiaoyuan Chen, Junming Liu, Mildred S. Dresselhaus, Gang Chen, and Zhifeng Ren. 2008. High-thermoelectric performance of nanostructured bismuth antimony telluride bulk alloys. Zhifeng Science 320:634. |

|

20 |

A good literature summary of the current status of TE technology is found in Lon E. Bell. 2008. Cooling, heating, generating power, and recovering waste heat with thermoelectric systems. Science 321:1457-1461. Available at http://www.sciencemag.org/cgi/reprint/321/5895/1457.pdf?maxtoshow=&HITS=10&hits=10&RESULTFORMAT=&author1=bell&titleabstract=an+information-maximization+approach+to+blind+separation+and+blind+deconvolution&searchid=1&FIRSTINDEX=170&fdate=//&tdate=//&resourcetype=HWCIT. Accessed March 24, 2010. |

FIGURE 3-7 Theoretical range for maximum ∆T achievable using existing commercial materials as a function of the number of stages. SOURCE: Rowe, D.M., ed. 1995. CRC Handbook of Thermoelectrics. Boca Raton, Fla.: CRC Press, Inc.

side of the prior stage. The theoretical range for ∆Tmax achievable using existing commercial materials is plotted in Figure 3-7 as a function of the number of stages. Although the figure shows values for up to a 10-stage device, commercially available coolers typically do not go beyond 6 stages.

If recently reported ZT advances in bulk bismuth telluride can be transitioned to commercial products, it is reasonable to assume that device-level ZTs will see some modest improvements, perhaps as much as a 50 percent improvement in ∆Tmax for a single-stage device. In terms of efficiency, existing thermoelectric coolers can achieve COPs of ~1.0 (i.e., 1 W of cooling for 1 W of electrical input) at ∆T of ~30 K. If the bulk materials available for commercial coolers were to achieve ZT values closer to 1.5, then the achievable COPs would be anticipated to approach 1.5 (1.5 W of cooling for 1 W of electrical input) at similar 30 K temperature differentials. There is some evidence that modest improvements in bulk materials

are transitioning to commercial thermoelectric (TE) products.21 The reduction in material usage is attributable to anticipated improvements in material properties.

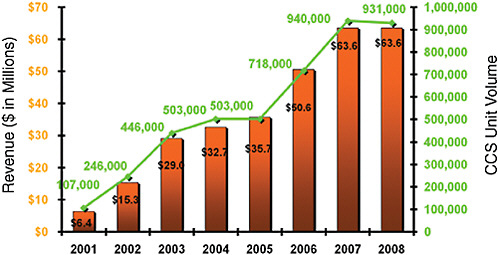

There are a number of commercial factors driving improvements in TE materials. In fact, the efforts to commercialize new, advanced bulk materials, coupled with industry efforts to improve cooler design and minimize parasitic losses, make it quite likely that these projected improvements will be realized within a 10-15 year time frame. For example, based on available data, the current market for TE coolers is relatively small, but it appears to be growing at an average rate of between 10 and 40 percent per year across a number of applications. One recent estimate puts the total TE cooler market at approximately $200,000,000.22 These estimates include TE coolers for a number of applications including climate control, EO cooling, personal coolers, and biomedical refrigeration. Figure 3-8 shows an average growth of roughly 40 percent per year between 2001 and 2008. In contrast, a Wall Street Journal 2004 article reported that Igloo products estimated the personal cooler (small coolers for refrigerating drinks and food) market at $50 million and predicted a 10 percent annual growth. Given these estimates it is reasonable to assume that a significant portion of the commercial drivers for improved TE cooler technology are coming from nondetector applications.

In summary, both cryocoolers and thermoelectric coolers are poised to achieve modest improvements in performance over the next 10-15 years in terms of efficiency. In addition, cryocooler costs and reliability at today’s performance levels are likely to improve due to commercial market drivers associated with their use in the semiconductor (cryopumps), medical (MRI, cryosurgery), and gas liquefaction industries. Reliability at today’s SWaP requirements will likely increase to exceed 10,000 hours, while costs will likely be driven lower as these markets continue to grow. For niche applications, such as high-end detectors and large staring arrays, advances in SWaP will be critical. The trend toward larger-footprint arrays is particularly challenging because it requires greater thermal stability and minimal vibration across a larger area. Although concepts for operating at higher frequency and higher pressure are likely to result in improved SWaP for cryocoolers, these advances will probably be obtained, at least initially, at the expense of reliability and cost. In addition, the higher frequency of operation may induce additional unwanted vibrational noise and susceptibility to electromagnetic interference.

FINDING 3-8

Low-cost uncooled infrared focal plane arrays are approaching the perfor-

|

21 |

Lon Bell, Amerigon, Inc., personal communication with the committee on March 3, 2010. Amerigon anticipates material usage in its products to decrease linearly over the next four years from 16 g to 11 g. |

|

22 |

Available at http://www.its.org/node/5263. Accessed March 24, 2010. |

FIGURE 3-8 Estimates of the TE cooler market. SOURCE: Courtesy of Amerigon CCS.

mance needed for applications that have traditionally relied on expensive cooled devices.

FINDING 3-9

For both cryocooler and TE cooler technologies, there are a number of commercial market drivers, separate from sensor cooling applications, that will drive evolutionary improvements in SWaP. Over the next 10-15 years, it is reasonable to expect that these improvements will achieve overall reductions in SWaP on the order of 20-30 percent.

CONCLUDING THOUGHTS

In addition to a proliferation of sensor numbers and types, new sensors must be developed to exploit unique target and background phenomenologies and be capable of processing significantly larger volumes of data. Advanced technology sensors have the potential to be used in novel sensing situations—for example, the vetting of potential enemies or the identification of combatants and noncombatants in a counterinsurgency operations. IR sensors with high-performance imaging FPAs have that capability and have long been critical to U.S. relative military superiority. Maintaining this superiority requires continual improvements in the technologies required for advanced ROICs and detector materials growth and continual awareness and incorporation of advances originating from both domestic and foreign developments.