___________

At times, provisions in the Patient Protection and Affordable Care Act (ACA) send conflicting signals, requiring the committee members to come to a common understanding about what these provisions should mean for the essential health benefits (EHB). Specifically, the committee reached the following conclusions before offering recommendations in subsequent chapters: (1) the EHB package should first be constructed as a basic plan that meets statutory requirements before additions, and any addition should be subject to the same evaluative process the committee recommends; (2) every service or item that might be classified within the 10 categories or a typical employer plan is not essential; (3) due to data limitations on offered benefits, the scope of typical employer benefits needs to be thought of as equivalent to a typical premium and the EHB package should be built up to fit within such a predefined premium target; (4) initial secretarial definition of the benefits should be as detailed as data permit; (5) typical employer should be defined as small firms, and the constraints they face taken into account; (6) state mandates should not receive special treatment but should be subject to the same inclusion criteria as any other service or item; and (7) benefits should be focused on medical ones.

Through an array of statutory provisions involving the 10 categories of care, the typical employer plan, consideration of state mandates, and various other requirements, the ACA provides legislative guidance for the contents of the EHB. Yet the committee’s review of this language revealed some conflicting and ambiguous direction with respect to the definition of the EHB. Furthermore, presentations during the committee’s public workshops and responses to its public comment form revealed a spectrum of views on foundational issues that needed resolution.

The foundational areas explored in this chapter involve the following questions:

• Does essential mean a basic or very expansive package?

• Are the 10 categories of care covered in typical employer plans?

• Is everything within the 10 categories of care or a typical employer plan essential?

• Within what boundaries, if any, are the covered benefits meant to be defined?

• How specific should the Secretary be when defining the package?

• What is a typical employer in the context of the ACA?

• How should state mandates be considered?

• Should medical and nonmedical services be distinguished in the context of the EHB?

Thus, the committee thought it wise to step back from the details of the statutory language to consider elaborating on the underpinnings of the approach that the Department of Health and Human Services (HHS) should take in determining what, in fact, is an essential benefit. After all, this is the package of benefits that many individuals will be required to purchase, and the meaning of essential can take on different connotations and result in benefit packages of diverse degrees of comprehensiveness and affordability.

FINDING THE MEANING OF ESSENTIAL

To many, essential in common parlance means basic, a minimum “floor” of benefits, yet others differ, seeing the intent of the ACA for the EHB package to be to provide a robust and comprehensive coverage. To complicate matters, the word essential was often used interchangeably by people providing comments to the committee, but to mean different things.

For example, at the committee’s first workshop, presentations by a bipartisan panel of former and current Senate staff members expressed some disagreement about what the ultimate package would look like—whether the desire was to create a “robust” benefit package vs. a “minimum” benefit package. Mr. David Schwartz said that Congress intended the EHB package to be “meaningful” and comprehensive and thus linked it to the benefits of a typical large employer plan as did Dr. David Bowen (Bowen, 2011; Schwartz, 2011). In contrast, Mr. Mark Hayes pointed out that the ACA uses the term essential because the legislature intended these to be basic, not comprehensive benefits, affordable for small employers (Hayes, 2011). Although the ACA lays out a more comprehensive set of benefits than does the Federal Employees Health Benefits Program (FEHBP) statute, Ms. Katy Spangler emphasized that the committee should “look at the least robust version of the benefit package as meeting” the standard of minimum essential coverage; otherwise, she said, fewer people will be able to afford coverage, thus defeating the purpose of the ACA to expand coverage to those who cannot now afford it (Spangler, 2011). Other presenters and commentators similarly presented diverse visions of the EHB package.1

Previous mandatory coverage requirements have similarly been couched in terms such as “minimum” or “basic,” and these provided floors that could be supplemented at the individual, employer, or plan option. For example, the 1973 Health Maintenance Organization (HMO) Act required “a comprehensive package of basic benefits, including essential preventive services, along with a list of supplemental benefits for which the enrollees would make an extra payment” (The American Presidency Project, 2011; Bergthold, 2010). In 1990, the American Medical Association (AMA) put forward a proposal for a minimum health care benefit package that would have required employers to offer insurance coverage that included a limited set of covered benefits (for example, including no more than a specific number of doctor visits per year), the result of making what the AMA described as difficult choices to provide a degree of benefits to those who previously had no coverage.2 In 1993 with the objective of providing small employers access to affordable health insurance and thus be better able to compete with larger employers, the State of Maryland set standards for all insurance carriers participating in the small employer market, establishing a “floor”—actuarial equivalency to the minimum benefits required to be offered by federally qualified HMOs—and a “ceiling”—the average premium for the standard benefit plan could not exceed 12 percent of Maryland’s average annual wage. Subsequently, this amount was reduced to 10 percent. Approximately 98 percent of those participating in that market add benefits, “buying up” from the basic plan (MHCC, 2007; Sammis, 2011; Wicks, 2002).3 Utah NetCare, which is Utah’s “version of an EHB package,” was designed to be a third less expensive than the average employer-based premium in that market. Although the basic benefit package is currently available and being purchased, “most people purchase benefit packages in excess of the basic requirements.”4 Others pointed to the basic mandatory vs. optional services under Medicaid as an example of

1 See the committee’s workshop publication for further discussion, Perspectives on Essential Health Benefits.

2 This benefit package idea was rescinded as AMA policy in 2005.

3 The Maryland Insurance Association also surveyed the largest carriers in 2008 regarding the top five benefit plans sold to small employers. These results were not published.

4 According to Utah’s largest commercial insurer with about 50 percent of the market, the enrollment or uptake of the minimum NetCare package among their members represents about 0.005 percent of the overall market. Personal communication with James Dunnigan, Utah State Legislature, May 4, 2011.

differentiating between levels of basic and enriched service choices in benefit packages. Section 1302 of the ACA specifically allows health plans to add benefits beyond whatever is defined as the essential health benefit package; however, individuals accessing coverage by virtue of exchange subsidies may not be able to afford supplementary coverage beyond what is offered in the exchange plan.

Having as many benefits incorporated in a plan as possible provides consumers protection for unforeseen expenditures, but it does so at the risk of raising the overall premium substantially, constituting an initial barrier to obtaining coverage for many and raising the total amount of federal subsidization. On the other hand, if the benefit package is not comprehensive enough or deductibles and co-payments are too high, patients may be underinsured. The major issue confronting the committee was how to balance the expansiveness of the benefit package with its affordability, while preserving the intent of the ACA to expand coverage to millions.

10 CATEGORIES OF CARE VS. TYPICAL

The 10 categories of care designated in Section 1302 for inclusion in the EHB package are a mix of condition-specific care (maternity and newborn care), types of services (laboratory services), facility-based care (hospitalization), and age-based services (pediatric services).5 Consequently, some categories overlap; for example, if maternity care was not a separate category, those services could be classified among the others. Section 1302 requires that the EHB include “at least” the following:

• Ambulatory patient services

• Emergency services

• Hospitalization

• Laboratory services

• Maternity and newborn care

• Mental health and substance use disorder services, including behavioral health treatment

• Pediatric services, including oral and vision care

• Preventive and wellness services and chronic disease management

• Prescription drugs

• Rehabilitative and habilitative services and devices

Congress sought to remediate what it saw as shortcomings in current coverage by pulling out certain categories to ensure that they were covered, such as maternity services, mental health and substance abuse disorder services, and habilitative services. Coverage of maternity care has frequently not been a standard offering in the individual market; instead, until the ACA requirement goes into effect, it often must be purchased as an additional policy rider that is frequently “expensive and limited in scope” (NWLC, 2008). Habilitative services are distinct from rehabilitation, in that they are designed to help a person first attain a particular function vs. restoring a function. As was remarked during one of the committee’s workshops, a separate listing of mental health and substance abuse disorder services would not be required if parity had truly been achieved.

The EHB are to reflect typical employer plans, and the U.S. Department of Labor (DOL) conducted a review of plan documents in fulfillment of the ACA’s requirement for a survey of employer-sponsored coverage to determine the benefits typically covered by employers. The results of the “survey” can best be characterized as a survey of plan documents and their degree of specificity, which does not fully reflect whether plans actually offer a specific benefit. For example, the DOL reports 67 percent of workers have plans that list coverage of durable medical equipment, while one Mercer survey (2011) suggests that 97 percent of employers actually cover this benefit to some degree.

Although most of the broader categories of the ACA are in typical plans, it is less clear whether habilitation, wellness and chronic disease management programs, and pediatric oral and vision are, and even if they are, what services are affected. The committee asked three insurers to report on whether they covered these and other categories and services in the small group market (Appendix C, Tables C-2 to C-4).

5 The ACA as amended expressly prohibits listing abortion as an essential health benefit (§ 1303(b)(1)(A)(i)).

• Habilitation was not covered by two of the three insurers reporting, with the third including habilitation in most plans but with coverage criteria determined by state mandates; early intervention services were not covered by one plan but were by the others in response to state mandates.

• Case management and diabetes care management,6 possible components of wellness and chronic disease management, were “available” from two insurers with the other responding that these were not covered benefits.

• Full pediatric oral and vision care have not been standard benefits, but are typically available as riders.7

• Depending on the particular mental health and substance abuse disorder service, coverage was indicated as almost universal, although some services such as inpatient or outpatient substance abuse detoxification was less frequently covered. Coverage may have been in response to state mandates or had specific policy limitations.8

The plans offered by large employers are considered the most inclusive of benefits, yet even in these plans, services such as wellness services and pediatric oral and vision services may only be available as supplements to a standard medical plan and habilitation is not specifically designated as a covered benefit (Kang, 2011; Mercer, 2011). How these categories, and the services within them, are defined may change insurer response about whether they are currently covered services or not. Nonetheless, it appears the typical employer plan will have to be expanded to accommodate the 10 categories of care.

The statute permits the Secretary to add more categories, by saying the EHB package must include “at least” the 10 broad categories of care. It was beyond the committee’s charge to specify the addition of specific categories and services, but the committee wanted to conceptually explore how to think about inclusions as the Secretary would have to do. As Congress did in drafting the legislation, the committee examined legislative guidance for other health insurance programs (e.g., FEHBP, Medicare, Medicaid, private plans) to see what other categories are required under those programs. For example, hospice and home health care are separately designated services for inclusion under Medicare Part A.9 Home care is “mandatory” under Medicaid (Appendix D). But neither is specifically drawn out in the FEHBP statute, or the Massachusetts creditable coverage requirements, although they are required in Maryland’s small business products (MHCC, 2011). Next, the committee explored whether they might be considered typical benefits. For hospice care, the DOL’s Bureau of Labor Statistics’ National Compensation Survey found it to be available to 67 percent of workers enrolled in plans (BLS, 2009), Mercer reported 91 percent of employers were offering this benefit, and the three insurers polled by the committee indicated it was covered. For home health care, the DOL found that 73 percent of workers have plans that mention coverage, Mercer found that 93 percent of employers offer such coverage, and the three polled insurers indicated that it was covered (Appendix C). For both services, coverage was subject to certain criteria and limits. Thus, the typical employer plan is likely to have to add additional services to meet the statutorily required 10 categories as well as likely already to have some categories or services that might be considered beyond those 10 categories.

Conclusion: The committee concludes that the contents of the EHB package should first be constructed as a basic plan that will meet the statutory requirements of typical employer plan and its expansion to the 10 categories before considering any other additions. Adding more benefits would necessitate raising premiums and/or further modifying benefit design and administration factors, such as network design and medical management criteria and programs. As a result, the committee does not recommend specific additions to the 10 categories of care at the outset but would require any additions to be considered within the broader

6 The DOL report indicated that diabetes care management was listed in 27 percent of workers’ plan documents reviewed, but 73 percent do not have plans that mention coverage (see Appendix C).

7 Mercer reported that 46 percent of all employers offer plans that provide pediatric dental and 44 percent provide pediatric vision coverage (see Appendix C).

8 The DOL report found less frequent mention of some services in plan documents with respect to substance abuse services. The services reported on in the IOM committee’s request to the insurers were primarily limited to those listed in the DOL survey. (See Appendix C.)

9 Social Security Act, Title XVIII § 1812 [42 U.S.C. 1395(d)].

evaluative process outlined in this report’s Recommendation 1 for defining essential health benefits (see Recommendation 1 in Chapter 5).

The decision about what is essential or nonessential is likely more complex than a binary one of determining whether a benefit is essential or not, but of being more or less essential, thus requiring an element of prioritization in the definition of essential benefits. Employers and insurers already deem some things excluded from coverage based solely on the impact on premiums or because offering such coverage would expose the insurer to the risk of adverse selection. Other times a decision is made according to a “social insurance test”: is it reasonable to ask others in the risk pool to subsidize the cost of providing the benefit (Levine, 2011)? Section 1302 states that the EHB shall include the 10 general categories and “the items and services covered within the categories.” However, within these 10 general categories, as well as in typical employer plans, there are services and items that should be excluded or limited in coverage because they can be deemed less effective and thereby less essential. Additionally, there may be services that have been excluded in the past that should be reconsidered.

Conclusion: The committee concludes that the Section 1302 language that says “the items and services covered within the categories” should not be construed to mean that every service that is within 1 of the 10 categories or is covered by a typical employer plan should automatically be included in the definition of the EHB.

The ACA provides further guidance that suggests that the EHB cannot be approached with an open wallet, but must fall within a cost range that is affordable for likely purchasers and sustainable by the government. The exchange products are to be based on a typical employer model. Employers buy insurance products on behalf of their employees and under budgetary constraints, and they are acutely aware of the fact that each dollar spent on health insurance premiums is a dollar that cannot be allocated to wages or other benefits (Emanuel and Fuchs, 2008). Therefore, operating under a budget and considering tradeoffs among inclusion and exclusion of benefits as well as benefit design options is typical among employers.

Before passage of the ACA, the Congressional Budget Office (CBO) scored the impact of the bill’s provisions on the federal budget and on premiums for individuals and small employers, using as a starting point the average employer premium from the Medical Expenditure Panel Survey (MEPS) but with subsequent adjustment based on consideration of the Kaiser Family Foundation (KFF)/Health Research & Educational Trust (HRET) employer benefit survey and consultation with benefit consultants on premium trends. The scope of benefits was considered to be reflected in the scope of the average employer plan premium (with the average weighted by enrollment). Thus, the average employer premium was factored into the calculations used in assessing the ultimate cost impact of health reform on individuals, small business, and the federal government (CBO, 2009a,b).10 Finally, the ACA requires a report to Congress on updating the EHB, which is to specifically assess the impact of any additions to benefits that might increase costs and identify corresponding reductions to meet the actuarial limitation of the scope of a typical employer plan.

The legislative language can be interpreted to mean that the EHB will not be more costly than “typical” employer-based insurance, and this provides a fiscal restraint on the expansiveness of the EHB package and its cost,11 and by extension, the federal subsidy amount paid over time. The lack of specificity in available data about benefit inclusions also argues for the scope of the benefit package to be thought about in dollar terms reflecting

10 Personal communication with Phil Ellis, Congressional Budget Office, February 11, 2011.

11 Former legislative staff conveyed to the IOM committee that the typical employer language in Section 1302 was considered to be a reasonable restraint on the expansiveness of benefits. Personal communication with Yvette Fontenot, formerly with the Senate Committee on Finance, December 6, 2010.

what a plan subscriber is typically paying. The reference to “scope of benefits” in Section 1302 may, therefore, have to be interpreted as equivalent to what can be obtained by a typical premium amount.

Conclusion: The committee concludes that scope of benefits of a typical employer plan needs to be thought of not only as the listing of benefits but also as what is paid by the subscriber for those benefits. Without some constraint on the size of the EHB package, the premium prices faced by individuals seeking to obtain coverage both inside and outside of the exchanges in the individual and small business market may prove unaffordable to the target population and diminish access to health insurance coverage. The committee concludes that the EHB should be defined as a package that will fall under a predefined cost target rather than building a package and then finding out what it would cost.

UNDERSTANDING TYPICAL SPECIFICITY IN SCOPE OF BENEFITS

The study sponsor asked the Institute of Medicine how best to reconcile a federal standard for benefits coverage under the EHB package with state and regional variations in practices and benefits coverage patterns (Glied, 2011). The statute guides EHB definition to include at least 10 broad benefit categories of care and be equal in scope to the benefits provided under a typical employer plan. The committee considered how much variance could be permissible across the country with regard to the defining and implementation of the EHB—and consequently how specific secretarial guidance should be to states and insurers.

Specificity of Inclusions in Existing Documents

Several reports have sought to identify covered benefit inclusions to describe the scope of a typical employer plan, each one variously reporting by the portion of workers covered, the portion of employers providing coverage, or whether the benefits are standard or not. National data remain limited in specificity regardless of source.

Insurance policies vary in the degree of specificity with which they describe covered benefits; some health plan documents are very general while others are more highly detailed. The DOL, for its legislatively required “survey” of employer-sponsored coverage, examined 3,200 plan documents and found it difficult to describe with much precision the benefits of typical employer plans. Attempts were made to abstract 19 types of services or items from plans—finding, depending on the service, that from 9 to 73 percent of workers’ plans do not mention whether the service is included; for example, 9 percent of workers’ plans do not specifically list coverage of emergency room visits, while 73 percent of workers’ plans do not specifically list coverage of kidney dialysis or diabetes care management (DOL, 2011). Thus, the usefulness of plan documents, as the DOL and the IOM committee in similar exercises found, is limited in informing about whether a benefit is covered as a typical benefit (Appendix C, Table C-1, column 2). It is unusual for every possible service to be explicitly listed as included; Oregon’s prioritized list for Medicaid, including each of the condition-treatment pairs that are covered, was the most specific list encountered (Oregon Health Services Commission, 2011).

Conclusion: As a result of the finding of lack of specificity, the committee believes that if a requested medical service can reasonably be construed to fall within 1 of the 10 covered benefit categories12 and is not expressly excluded, then it should be considered eligible for coverage as long as it is judged medically necessary for a particular patient.

For example, radiation therapy for cancer treatment might not be listed explicitly as a covered service but could reasonably be considered to fall within the general category of ambulatory patient services and, therefore, covered if judged medically necessary. The medical necessity of a particular treatment would be based on the specific type and state of the patient’s cancer, as well as previous treatments applied to the individual’s diagnosis.

12 This conclusion references the 10 categories because they are identified by the law; the conclusion could be extended to benefit categories once identified by the Secretary as part of the EHB.

However, greater specificity within plan documents listing which classes of services are covered (e.g., listing of radiation therapy) would provide greater clarity and consistency across plan documents.

Balancing Flexibility and Specificity in Guidance

The committee considered whether only using the 10 broad categories of care in Section 1302 would be sufficient for secretarial guidance for the inclusion content of the EHB or if the 10 categories alone would result in too much state-by-state variation in what is considered essential. If more specificity is desired, then how detailed should the benefits list be? With increasing specificity comes greater uniformity in the EHB, and with this the advantages of standardization: clarification of price differences among plan options, for greater consumer confidence in picking plans with lower costs; minimization of adverse selection; ease in risk adjustment; and help in ensuring the adequacy of the lowest-cost plan (Bergthold, 1993). It might also be implied from HHS’ request to the DOL to examine specific services that HHS expects to include some additional specificity beyond the 10 required categories.

If specificity has these advantages, what degree of regional or local variation in EHB definition should be allowable? In testimony to the committee, the director of the California Department of Managed Health Care cautioned, based on experience with state requirements for managed care, that very broad categories in the authorizing Knox-Keene Act left too much undetermined and thus resulted in many state mandates to clarify intent (DMHC, 2011). Conversely, the National Governors Association, among other proponents of secretarial guidance promoting a high degree of flexibility, felt that generality would better enable market competition and innovation (Salo, 2011).

The committee examined the legislative guidance for a number of programs and the plan documentation that resulted in those programs (e.g., FEHBP, the Massachusetts and Utah exchanges, managed health care in California, the Maryland plan for the small group market). The committee finds that the legislative guidance for these programs at least outlines broad general categories of care as does the ACA but may go beyond general categories to list more discrete services (e.g., coverage for transplants in Maryland’s requirements for its small business Comprehensive Standard Health Benefit Plan) (Appendix D). Regardless of statutory descriptions, resulting plans, as reflected in evidence of coverage documents that consumers receive, generally go on to specify services in greater detail. However, plans even under the same legislative authority can vary in their degree of specificity within the same state. Moreover, in each of these programs (whether a state-specific program or the FEHBP), there is one entity providing oversight, while the EHB package will be administered across the 50 states by many different bodies. Individual states are opting for differing structures (i.e., quasi-governmental structure, nonprofit corporation, state government operated) and modes of contracting; some states will be active purchasers and will selectively decide which plans may participate in the exchange, while others will take a clearinghouse approach, accepting all comers (KFF, 2011). This multi-jurisdictional approach increases the likelihood that use of broad categories by the Secretary would result in variation even within local markets, compromising consumer protections unless there was increased specification beyond the 10 categories of care in the ACA.

Conclusion: To ensure better national comparability, the committee concludes that initial secretarial guidance should include as much specificity as can be developed from current best practices in plan documentation. More specificity is needed than the 10 categories outlined in the ACA because implementation of the EHB program will be disseminated across multiple jurisdictions, each with its own individual state-based oversight bodies.

TYPICAL EMPLOYER: SMALL VS. LARGE

Several questions arise with respect to typical employer. First, how should typical employer be defined? Sherry Glied, Assistant Secretary for Planning and Evaluation, indicated that she would welcome the committee’s advice on the meaning of typical (Glied, 2011). As noted above, there were different perspectives on whether the benefit plan should reflect that of the small-or large-sized employer. Consequently, the committee wanted to review the landscape of employer sponsorship of insurance and examine different attributes of plans offered by small and large employers:

• What is a typical employer in general and in the context of the ACA?

• What are the typical cost of premiums, amount of employee cost sharing, and trends in plan type by employers of different sizes?

• What benefit differences are there for employers of different sizes?

What Is a Typical Employer?

Several approaches can be taken to defining typical employer, and they may lead to different results in terms of benefit coverage and design. If based on the number of firms or employers, then a typical employer looks more like a small employer (98 percent of all employer firms in the United States are classified as small) (U.S. Census Bureau, 2008),13 and if based on the number of covered employees, a typical employer looks more like a large employer (65 percent of all employees in the country) (U.S. Census Bureau, 2008). Beyond this simple distinction are more nuanced differences in the degree to which employers offer health insurance coverage, whether the EHB package will apply to the plans offered by firms of different sizes, and the degree of uninsurance among their employees, all of which can be important to defining typical in the context of health insurance expansion under the ACA.

In 2011, just 60 percent of employers nationwide offered health insurance, including 99 percent of large firms (with 200 or more employees) and 59 percent of small firms (with 3 to 199 employees). Smaller firms, particularly those with less than 10 workers (48 percent offered in 2011) and those with 10-24 workers (71 percent), are less likely to offer health insurance coverage (KFF and HRET, 2011) (see Table 4-1). Thus, the workers of these smaller firms are a target of health reform coverage.

Employers might obtain insurance through insurance brokers, directly from insurers, or decide to self-insure; understanding the extent of self-insurance in small and large firms is of interest because self-insured plans are not required to incorporate the EHB. Self-insured means that the employer acts as its own insurer and accepts the associated risk; “fully insured” arrangements means the employer and employee pay a per capita premium to an insurance company that accepts the risk. In 2010, 16 percent of workers in smaller firms (3-199 employees) were in self-insured arrangements;14 there is also a type of insurance that is a blend of insurance and self-insurance, in which some small employers choose insurance plans that have very high deductibles, such as $5,000, and the employer might self-fund the deductible amount. In contrast to the significantly lower percentage of small firms that are currently self-insured, 58 percent of workers in firms with 200-999 workers are self-insured, 80 percent in firms with 1,000-4,900 workers, and 93 percent in firms with more than 5,000 workers (KFF and HRET, 2010a). Thus, workers in smaller firms are more likely to obtain health insurance that would include the EHB package, whether they access it through the exchange or not. The insurance landscape, however, is in flux, with more small employers considering whether to self-insure to avoid requirements to provide an EHB package if it is more expansive than they desire or, alternately, provide employees with a fixed dollar contribution to have them purchase plans as individuals (Eibner et al., 2011).

TABLE 4-1 Percentage of Firms Offering Health Benefits, by Firm Size, 1999-2011

| Firm Size | 1999 | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 |

| 3-9 Workers | 55 | 57 | 58 | 58 | 55 | 52 | 47 | 49 | 45 | 50 | 47 | 59a | 48a |

| 10-24 Workers | 74 | 80 | 77 | 70a | 76a | 74 | 72 | 73 | 76 | 78 | 72 | 76 | 71 |

| 25-49 Workers | 88 | 91 | 90 | 87 | 84 | 87 | 87 | 87 | 83 | 90a | 87 | 92 | 85a |

| 50-199 Workers | 97 | 97 | 96 | 95 | 95 | 92 | 93 | 92 | 94 | 94 | 95 | 95 | 93 |

| All small firms | |||||||||||||

| (3-199 Workers) | 65 | 68 | 67 | 65 | 65 | 62 | 59 | 60 | 59 | 62 | 59 | 68a | 59a |

| All large firms | |||||||||||||

| (200 or More Workers) | 99 | 99 | 99 | 98 | 97 | 98 | 97 | 98 | 99 | 99 | 98 | 99 | 99 |

| All firms | 66 | 68 | 68 | 66 | 66 | 63 | 60 | 61 | 59 | 63 | 59 | 69 | 60 |

NOTE: These results are from the Kaiser-HRET Survey of Employer-Sponsored Health Benefits, 1999-2011. Results based on sample of both firms that completed the entire survey and those that answered just one question regarding whether they offered health insurance.

a Estimate is statistically different from estimate for the previous year shown (p <. 05).

SOURCE: KFF and HRET, 2011. Reprinted with permission by Gary Claxton, Vice President and Director of the Health Care Marketplace Project, Kaiser Family Foundation.

13 Note: The number of nonemployer firms (21,351,320) is much greater than employer firms (5,930,132); nonemployer firms have no payroll.

14 The KFF and HRET survey uses the terms self-funded and fully funded rather than self-insured and fully insured.

Uninsured workers are a prime target for insurance expansion; substantial numbers of workers are uninsured and need affordable insurance. Among the 29.3 million uninsured workers in 2009, 48 percent worked in firms with fewer than 100 employees and an additional 13 percent were self-employed (KFF, 2009).15 Furthermore, the rates of small firms offering insurance are much lower for worker populations at or below the 25th percentile in hourly wages compared with small firms having higher wage workforce (Blumberg and McMorrow, 2009). Others emphasize that the portion of uninsured or “underinsured” in small firms of fewer than 50 workers is greater than in larger firms—that is, more than half of those at small firms vs. about a quarter of those in large firms (Collins et al., 2010). Although often employed by large firms, these uninsured low-income workers would need an affordable benefit package, and their needs are likely more similar to employees in small firms.

What Are Typical Premiums, Deductibles, and Plan Types?

The main reasons given for smaller firms not offering insurance are primarily economic: the employer cannot afford it, the employee share would be too high, employees prefer the monetary benefit in terms of wages, and the benefit is not needed to retain employees. In the 2010 KFF and HRET Annual Employer Health Benefits Annual Survey, more than half of the respondents cited cost of health insurance being too high as the reason for not offering it (Holve et al., 2003; KFF and HRET, 2010a). Because employers are making purchasing decisions on behalf of their employees and health benefits offered by employers represent a tradeoff between benefits and wages for employees, employees too have an interest in the level of expenditures. Increases in health insurance premiums, in general, have been implicated in decreased coverage rates (Chernew et al., 2005). The committee explored whether there were differences in premiums, deductibles, and plan types between small and large employers.

Premiums

It is useful to understand similarities and differences in the premiums paid by employers and workers in small and large firms, particularly if premium equivalence is used in defining a scope of benefits because of a lack of definitiveness in plan documents. Unadjusted premium data show little difference by employer size; however, an often-cited article indicates that in 2002, small employers paid 18 percent more, on average, for the same benefits as those offered by the largest firms (Gabel et al., 2006; Miller, 2011).16 The amount was 25 percent higher for indemnity plans and 18 percent higher for preferred provider organization (PPO) arrangements. Assuming similar health status and demographics between the small and large employers studied, higher premiums for smaller firms vs. larger ones could be attributed to higher insurance broker commissions, a smaller population base over which to spread administrative costs, insurer profit/risk charges, and weaker market power of individual and small group purchasing on their own (Executive Office of the President Council of Economic Advisors, 2009; Gabel et al., 2006). More up-to-date adjusted figures were not available to the committee, but the ACA medical loss ratio (MLR) provisions should help address some of these issues. The MLR informs consumers and regulators about the percentage of the premium being spent on fees, administration, and profits.17

15 About one-third of the uninsured are in firms with fewer than 100 workers.

16 Gabel et al. (2006) find this difference when comparing the smallest firm size of 1 to 9 workers compared with firms with 1,000 or more workers.

17 Small group must meet a medical loss ratio of at least 80 percent and large group must meet a loss ratio of at least 85 percent, or rebates must be paid (§ 2718 of the Public Health Service Act) [42 U.S.C. 300gg–18]. “These requirements, effective on January 1, 2011, are designed to make sure that 85 cents on the dollar is spent on claims costs, while the remaining 15 cents are allocated to administrative expenses in the large group market. In the small group and individual markets, 80 cents on the dollar are spent on claims cost, while the remaining 20 cents are allocated to administrative expenses. If a carrier fails to meet this benchmark, a portion of the premium must be refunded to subscribers” (McGraw Wentworth, 2011, p. 1).

A consistent relationship of firm size to premium price is not apparent across single and family coverage. MEP-IC (MEPS-insurance component) data define a small firm as one with 50 employee full-time equivalents (FTEs); starting in 2014, the ACA requires state exchanges to serve businesses with 50 or fewer employees, leaving it to the state to decide whether to open the exchange market to employers of 100 or fewer individuals. Data on 2009 private sector premiums do not show much difference in premiums for individual policies ($4,652 for small firms under 50 vs. $4,674 for larger firms), and for a family of four, larger firms pay more ($12,041 for small firms vs. $13,210 for large) (Branscome and Davis, 2011; Davis and Branscome, 2011). Older MEPS data for 2006 show that private sector small firms paid 4.5 percent more than larger firms for single coverage policies, but 3.0 percent less for family policies (Branscome, 2008).18 Premiums for “plus 1” policies in 2009 show a higher premium for small firms ($9,124 for small vs. $9,042 for large) (Crimmel, 2010).

Employers have to determine what portion of the premium the employer and the employee will contribute. Some employers do not require employees to contribute (AHRQ, 2009a). On average, employee contributions in the private sector are 20.5 percent of individual policy premiums and 26.7 percent for family policies, with 2009 MEPS-IC data showing that employees of small firms contributed a lower percentage than those of larger firms for individual policies, but the reverse relationship for family policies (Branscome and Davis, 2011; Crimmel, 2011; Davis and Branscome, 2011). Although employer contributions have an apparent impact on the premium cost seen by an individual employee, in fact, the entire cost of health insurance premiums—like all other employee benefits—are ultimately taken from employee wages. Thus, both employers and employees have a strong interest in ensuring restrained premium growth.

Deductibles

Differentials in deductible levels suggest that benefits purchased by employees of small firms already require greater out-of-pocket payment for deductibles, raising the question of how much more emphasis could be placed on the benefit design factor of deductibles vs. other approaches to balance the breadth of EHB coverage with an affordable premium. For example, the 2009 total average deductible for an employee-only policy in a larger firm is $822 compared with $1,283 for firms of fewer than 50 employees, and for families the difference is $1,610 vs. $2,652, respectively (AHRQ, 2009b,c). Workers in small firms have seen deductibles increase much faster than workers in large firms. The average deductible for employee-only PPO coverage increased from $469 to $1,146 between 2005 and 2010 among workers in firms with 3-199 workers, compared to $254 to $460 among larger firms (KFF and HRET, 2005, 2010). Moreover, 46 percent of covered workers in small firms had deductibles of $1,000 or more compared with 17 percent of covered workers in large firms for single coverage (KFF and HRET, 2010a). Little variation by firm size is now observed in the percentage of workers enrolled in a plan with a deductible, with an average for all plans of 73.8 percent (AHRQ, 2009a). This is in contrast to the practice in 2002 when larger firms were less likely to have a deductible.

Plan Types

The majority of firms offer only one type of plan, with only 15 percent of small firms and 44 percent of large ones offering more choice (KFF and HRET, 2010a).19 Gabel’s study found that benefits were less comprehensive for small firms, regardless of their enrollment in indemnity or PPO plans (Gabel et al., 2006).

Different plan types have more or less stringent medical management to administer benefits, and regardless of firm size there has been tendency over time for an increasing degree of medical management as shown by data about plan types (KFF and HRET, 2010b). At opposite ends of the spectrum are the traditional fee-for-service indemnity plan, with no managed care elements, and the staff model HMO, with the most. Between these two extremes lie PPOs, HMOs that permit greater choice of physicians, and point-of-service (POS) plans that combine

18 For premium per enrolled employee, $4,260 for small firms (less than 50 employees) and $4,077 for large. For employee plus one, $8,105 and $7,969, respectively, and for family coverage, $11,095 and $11,438, respectively.

19 Note: This survey defines small as 3-199 workers and large as 200 or more.

elements of the HMO and PPO in an attempt to balance freedom of choice for the employee and financial control for the employer. Indemnity plans have virtually disappeared, while there is growth in PPO arrangements and different forms of managed care. Consumer-driven health plans or high-deductible health plans with a savings account option (HDHP/SO) have been introduced to better engage individuals in their own health care choices. These plans are typically offered through a PPO, but enrollment data are often shown separately because of the distinct nature of the cost-sharing arrangement.

DOL data only report on percentage use of fee-for-service (FFS) and HMO arrangements, and recent data do not show a difference by firm size (BLS, 2011), but this may be attributed in part to the fact that DOL FFS data include both PPO and POS data. KFF and HRET (2010a) data suggest a gradient of less participation in PPO FFS arrangements from larger firms to small but increasing participation in POS plans (a type of managed care arrangement); there is a less clear pattern for choice of a high-deductible health plan, although workers in very large firms are electing these at the highest rate of all groupings.

What Benefits Are Offered by the Typical Employer?

Attempts to distinguish differences in benefits by employer size met data limitations beyond that experienced by the DOL’s survey of plan documents, but what data are available show little difference in the scope of benefits by firm size; instead benefit design factors play a larger role. The DOL Bureau of Labor Statistics’ National Compensation Survey, collected from a sample of 3,900 employers, was able to yield data on coverage of 10 different services by employer size—outpatient and inpatient surgery, physician office visits, hospital room and board, chiropractic, home health care, skilled nursing facility, hospice care, biofeedback, and homeopathy (BLS, 2009); in most instances, the frequency with which the employer pool offers each of these benefits is very similar regardless of the size of the employer (Appendix C, Table C-1 columns 3 and 4). For example, outpatient surgery is offered to 97 and 98 percent of large and small employers workers, respectively, and hospice is offered by 66 and 69 percent, respectively. Other data from the 2009 Mercer National Survey of Employer-Sponsored Health Plans are not reported by the most relevant firm size in the context of the ACA (Mercer, 2009) but show that employers with fewer than 500 workers are less likely to cover some specific services such as alternative medicine therapies (e.g., acupuncture, chiropractic) and infertility services (Table C-1 columns 5 and 6).

Because of the limitations of the DOL survey of plan documents in revealing the contents of employer plans to inform a typical profile of benefits, the committee obtained data from three major health insurers—CIGNA, UnitedHealthcare, and WellPoint—on the benefits that they offer in the small employer and individual markets (see earlier discussion of the likely benefit enhancements that small employer plans will have to make to meet the 10 category requirement in the ACA). The profile of services covered by all of their standard plans, covered by some due to state mandates, or excluded is very similar for the small group market across these insurers (Appendixes C and F). The committee does not have a basis to assert that these plans are “typical” of all insurers, but finds that they are potentially informative to HHS for developing a preliminary list of services and actuarial estimates to consider when defining the EHB in accordance with the steps in the committee’s Recommendation 1 (Chapter 5).

Both WellPoint and UnitedHealthcare report that little of the variation in customizing coverage in either the large and small group market is due to differences in covered benefits as opposed to benefit design options. Employers and insurers told the committee that tighter provider networks and tighter medical management are a feature of products selected in the smaller firm market (Calega, 2011; Turpin, 2011). WellPoint conveyed that its small group market is very standardized, and even in the large group market, only 5 percent of customization requests relate to adding coverage and 2 percent to removing coverage (e.g., when an employer becomes self-insured and does not want to include a state mandate), with the remainder of customization requests pertaining to adjusting cost sharing or limit setting (Appendix E). WellPoint reported in detail on the benefits covered by 99.7 percent of its small group products through Anthem Blue Standard Coverage Plans (small group = 1 or 2 to 50 employees); only a very small percentage of plans (0.3 percent) excluded specific services such as allergy testing and injections, cardiac and pulmonary rehabilitation, and durable medical equipment (Appendix E).

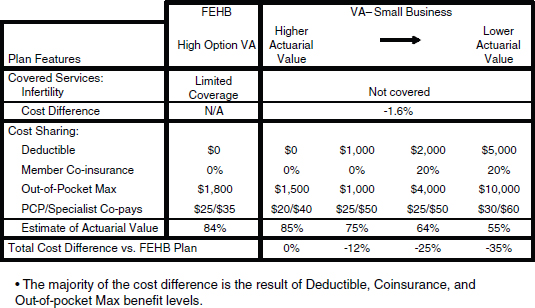

To further illustrate the influence of benefit design as opposed to differences in covered benefits, UnitedHealthcare offered a comparison of covered benefits in the large and small firm markets, using plans offered in

Virginia—a low-mandate state—as an example (Figure 4-1). The single covered benefit difference is that FEHBP has limited coverage of infertility services, while none of the small business products include infertility services. The resulting cost difference based on that service alone is a 1.6 percent lower price in the small group market. However, the major differential in pricing comes from benefit design choices, including the level of deductible, cost sharing, and out-of-pocket maximums desired—a 12 to 35 percent lower price—not differences in covered services.

NOTE: N/A = not applicable; PCP = primary care provider.

SOURCE: Sam Ho, UnitedHealthcare. Figure 4-1 New 11/16/11

Benefit profiles are also very similar between the small group and individual markets according to these three insurers; the primary differences, reported by CIGNA, UnitedHealthcare, and WellPoint, have been: (1) maternity care has not been a feature of the individual plans unless purchased as a rider or mandated by the state, but the ACA requires its inclusion, (2) coverage for mental health and substance abuse services in individual plans has varied more than the small group market plans, with coverage being more limited and sometimes excluded unless required by state mandates (Appendix C, Tables C-2 to C-4).

In summary, health insurance premiums are determined by a number of factors including the population covered by a plan, the expansiveness of coverage, the benefit design, and underlying medical and insurance prices depending on the competitiveness of the local market. Based on available data, small and large employers offering insurance, on average, are paying similar premiums, yet small employers appear to have more cost-sharing limits on coverage. For example, employees of smaller firms are paying higher deductibles. Thus, benefit design considerations have been an important factor in what coverage is available to small firms and at what price. An advantage of exchange participation is that it will bring the purchasing power of larger groups to the marketplace and, ideally, offer more comprehensive coverage for what small employers are now paying, and through subsidies, allow additional persons to obtain coverage that they could not afford previously. Notably, when the state-based health insurance exchanges begin operations in 2014, the focus will be on serving individual purchasers and firms with fewer than 100 employees. Beginning in 2017, states can choose to allow those in the large group market (100+ employees) to purchase coverage in the exchanges.20

20 § 1312(f)(2)(B).

Conclusion: Available data suggest the profile of covered benefits among large and small employers and the average premium paid is often not great; benefit design choices play a greater role. Given the ACA’s focus on providing access to health insurance for workers of small firms and individuals in the opening years of the health insurance exchanges, the committee concludes that the initial focus of the EHB definition should be one that would be typical in the small employer market. Thus, when there is sufficient information to inform a choice between the scope of benefits between small and large employers (whether specified in service type, premium amount, or limits on services), the emphasis should be on the choice that would reflect the typical small employer market as long as that is consistent with meeting the statutory requirements (e.g., 10 categories).

An extension of thinking about what is essential is consideration of the disposition of state mandates and how they fit within an EHB package. The term “state-mandated health benefits” (also referred to simply as “mandates,” “state mandates,” or “mandated benefit laws”) refers to state laws that require health insurance contracts to cover specific treatments or services or medically necessary care provided by a specific type of provider.21 Prior to the passage of the ACA, states were the primary regulators of the content of health insurance policies. The committee was asked to consider what role, if any, existing state mandates should play in defining essential health benefits. The ACA obligates each state to subsidize the benefits it mandates above and beyond EHB requirements.22

Applicability of State Mandates

Although all states have some mandates in place, they differ dramatically with respect to the total number in each state. Estimates of the number of existing mandates vary significantly, in part because they vary in terms of what they define as a “mandate” and also whether they count multiple laws requiring the same type of coverage in different market segments as distinct mandates. The Council for Affordable Health Insurance (CAHI) found an average of 42 mandates per state, with a high of 69 in Rhode Island and a low of 13 in Idaho (Bunce and Wieske, 2010). These numbers include, however, not only treatment and provider mandates, but also “population” mandates (requirements to cover specific populations such as newborns or grandchildren) and “offer” mandates (requirements simply to offer certain coverage for purchase). Other studies have found much lower numbers. For example, a 2007 study found an average of 18 mandates per state, with a high of 35 in California and a low of 2 in Idaho. These numbers do not include offer mandates, but do include population mandates (Monahan, 2007). Analysis of the number and type of state mandates by the BlueCross BlueShield Association tends to find fewer mandates than the CAHI numbers (Cauchi, 2011; Laudicino et al., 2010). Mandates proliferated particularly during the past 10-20 years (Bellows et al., 2006). Certain types of mandates are very common. For example in 2010, 50 states require coverage for mammography screening, 47 states currently have mandates requiring coverage for diabetes-related supplies, 45 require coverage for treatment in an emergency room, and 36 require coverage for off-label drug use (Bunce and Wieske, 2010); some are less frequent: congenital defect (1 state), early intervention services (7), and hospice care (12). With respect to provider mandates, 44 states require coverage for the services of chiropractors, 44 require coverage for the services of psychologists, and 41 require coverage for the services of optometrists, while 19 states mandate speech/hearing therapists, 12 mandate acupuncturists, and 7 mandate drug abuse counselors (Bunce and Wieske, 2010).

State mandates do not apply to every type of health insurance arrangement or type of market product. For example, the General Accountability Office (GAO) found the median number of mandates that were commonly applicable to the large employer, small employer, and individual market in 2002 to be 17 (GAO, 2003).23 Importantly,

21 Some states also have laws requiring health insurers to offer coverage for certain types of benefits or providers. Those laws are omitted from this discussion.

22 § 1311(d)(3)(B).

23 The GAO report reviewed benefit requirements in eight states (Alabama, Colorado, Georgia, Idaho, Illinois, Maryland, Nevada, and Vermont) (GAO, 2003).

they do not apply to any employer-provided health plans that are self-insured by the employer. Given the high rates of self-insurance among larger employers, the result is that more than half (59 percent) of the individuals with employer-provided coverage are covered by plans that are not subject to state regulation, including state mandates (KFF and HRET, 2010a) and the proportion is higher among very large firms (MacDonald, 2009). Whether mandates apply to state Medicaid programs, or other state programs designed to provide coverage to low-income individuals, depends on the particular statute enacting the mandate. Legislatures may include such programs within a mandate, but often they do not (Hyman, 2000). Typically the greatest impact of mandates is on privately financed health insurance sold through the individual and small group markets within a state. Additionally, the FEHBP national fee-for-service plans do not have to incorporate state mandates, but can pick up state mandates as a negotiated benefit.

Debate Over State Mandates

State mandates have been a controversial element of health insurance regulation. Proponents of mandates argue that there are situations in which market intervention, in the form of mandates, is necessary to meet various health policy goals or to correct market failure. For example, mandates can be used to make coverage available that insurance companies would not voluntarily offer because of concerns about adverse selection. Additionally, mandates can be used to increase utilization of effective medical services, thereby improving population health. Mandates can also be used to enforce principles of justice or fairness by requiring the risk of loss due to certain medical conditions be shared within an insured community.

Critics of mandates tend to focus on two distinct issues. The first is the restraint that mandates place on the ability of two willing parties to contract freely. The objection based on freedom to contract is a normative argument based on the position that individuals should have the right to choose which risks they want to insure against and which they do not, and that it is unfair to require individuals to purchase coverage they do not value or desire.

The second primary critique of mandated benefit laws is that they increase the cost of health insurance and therefore lead to fewer individuals being able to afford insurance. Essentially, the argument is that it is unjust to increase the cost of coverage by requiring coverage for a broad range of services when it results in some individuals being unable to afford and purchase basic insurance coverage. There is, however, no consensus regarding the price impact of mandates or the effect that any price increase has on coverage rates.

Finally, concerns have been expressed that mandates are not evidence-based and do not always reflect clinical best practices. Thirty-two states have authorized some type of benefit review procedure to be put in place, and 27 states have in place some “systematic approach” to evaluating financial impact (CHBRP, 2009). However, very few of these laws actually require prospective, expert analysis of evidence for a mandate before it can be voted on by the legislature. Even in states with robust review procedures, there is little evidence that the review procedure leads to evidenced-based mandates that significantly improve health outcomes. One recent study of the mandate processes in Connecticut and California concluded that “without a specific structure in place to provide legislators with appropriate data (e.g., on costs, medical effectiveness) very little evidence is provided to legislators. And even when there is a structure in place to ensure such data are available, those data appear to have only a modest impact on bill passage”; as a result, “even where there is an independent, expert commission providing robust data on proposed regulation, bills with virtually no impact on either health insurance coverage or treatment utilization are passed” (Monahan, 2012).

These concerns were echoed in comments the committee received, including numerous arguments that state mandates are not evidence-based, increase variability across states, and contribute to increasing insurance premiums (Bocchino, 2010; Darling, 2011; Malooley, 2011). Indeed, well-known examples among several mandates of questionable clinical value that have been passed prematurely include those requiring coverage for high dose chemotherapy and autologous bone marrow transplant for breast cancer and for hormone replacement therapy (Jacobson, 2008; Jacobson et al., 2007). Others were concerned that “benefit mandate choices [should be] kept outside the purview of elected officials” (Jones, 2010) and that, after passage, state mandates may crowd out the introduction of alternative services, while remaining “static” (Stoss, 2010). The consumer advocate group Health Access said that although it supports some mandates (such as mental health parity and coverage of prenatal care

in the individual market), it does not regularly endorse benefit mandates because they are often related to specific drugs, devices, or tests and do not tend to evolve as treatments change (Wright, 2011). Others argued that HHS should view state mandates “as informed judgments of what is needed by populations” (Spielman, 2011).

Options Considered by the Committee

The committee was asked to consider what role, if any, existing state mandates should play in defining essential health benefits. The committee considered several different options, discussed below.

1. Incorporate all existing state mandates into the definition of “essential health benefits” that apply to a particular state.

One option considered by the committee was to recommend that in defining the EHB the Secretary should incorporate all state mandates that were in effect on March 23, 2010, in a particular state. The advantage of this approach is that it would preserve the coverage requirements that a state had in place prior to the passage of the ACA, without requiring the state to bear any increased cost that might otherwise result from mandating a benefit not included in the definition of essential health benefits. However, doing so may be seen as being contrary to the ACA’s statutory language, which clearly contemplates requiring states to pay the increased premium cost that results from state mandates that exceed essential health benefit requirements. It would also result in drastically unequal definitions of essential health benefits among the states and would essentially require the federal government to subsidize state policy choices.

2. Incorporate mandates that exist in a majority or supermajority of states into the definition of essential health benefits that applies in all states.

Another option considered by the committee was to recommend that in defining the EHB, the Secretary include coverage for any treatments or services that are required to be covered by either a majority or a supermajority of the states. Doing so would allow for a uniform definition of essential health benefits, but would also subject minority states to the legislative actions of the majority states and would likely drive up the cost of coverage in states without many existing mandates. As above, the federal government would be forced to subsidize state policy decisions, although under this option only those decisions made by a majority of states. In addition, because very few states have legislative decision-making processes that reliably incorporate evidence, the committee was concerned that incorporating even supermajority mandates would undercut the overall approach to the EHB advocated by the committee, and as set forth in this report, by potentially including mandates that could not be justified under the committee’s framework.

3. Do not explicitly incorporate existing state mandates into the essential health benefits framework, but rather subject coverage for all types of treatments and services to the same framework, principles, criteria, and methods used to determine essential health benefits generally.

Finally, the committee considered giving no special preference to existing state mandates, but rather requiring the potential coverage of any treatment or service to be governed by the same criteria, with none receiving special consideration by virtue of its status as a state mandate. This option would result in states’ being required to pay the increased costs associated with any mandates that exceed the EHB requirements. While disadvantageous to states, the result is clearly contemplated by the statutory language of the ACA. This approach also has the significant advantage of allowing for consistency in all EHB coverage decisions and in providing federal uniformity. Given the lack of evidence that existing state mandates result from a sound evidence-based process, the committee concludes that this third option is the most desirable alternative.

Conclusion: Because state mandates are not typically subjected to a rigorous evidence-based review or cost analysis, cornerstones of the committee’s criteria, the committee does not believe that state-mandated

benefits should receive any special treatment in the definition of the EHB and should be subject to the same evaluative method (see Recommendation 1 in Chapter 5). This interpretation is consistent with the language in the ACA regarding state mandates; that is, Congress did not require their inclusion.

At the committee’s first meeting, the Assistant Secretary for Planning and Evaluation (ASPE) asked the committee to consider the corollary question of what distinguishes a medical service from a nonmedical service and how that distinction might apply in the context of defining what is essential. The propensity has been not to define what a medical service is specifically, but to say what is not covered because it is nonmedical (e.g., custodial care is not considered a medical service), is provided by a non—health care provider, or requires an assessment of whether a service is medically necessary. The committee explored various ways of defining: (1) by provider, (2) by specific services, and (3) by medical necessity determination.

Defining medical services as those delivered only by physicians, nurses, and physician assistants is more restrictive than most employer policies. A broader range of health services provided by other types of health professionals (e.g., physical therapy, speech therapy, occupational therapy) is often included in employer policies. Some plans both in the United States and elsewhere, however, limit the providers they include as covered—for example, requiring a supplementary policy be purchased to have access to physical therapy services rather than as part of a basic policy (British Columbia Ministry of Health, 2011). The inclusion of rehabilitation and habilitation in the l0 required categories suggests that such health professionals would provide “medical” services relevant to the EHB (Ford, 2011; Thomas, 2011). Acupuncturists and naturopaths are frequently excluded provider categories in standard insurance policies, on the basis that their practice falls into a “nonmedical” category, except in states where there is state-mandated coverage inclusion. The ACA prohibits insurers from discriminating on the basis of type of provider as long as the provider is operating within its scope of practice; however, this is a separate issue from defining specific types of services as being part of the EHB package.24

Insurers make distinctions about whether services or specific items are nonmedical and whether that alone is a sufficient reason for exclusion. For example, while interventions such as the teaching of Braille and American Sign Language can improve functioning and productivity in persons who are blind or hearing impaired, they have been classified as primarily educational and not part of health care delivery. Similarly, exercise-related services and items (e.g., exercycles, gym memberships, personal trainers) are beneficial to health, but insurers reach different conclusions about whether to support such services (e.g., certain Medicare Advantage plans support gym memberships, while Kaiser Permanente does not) (Empire Blue Cross Blue Shield, 2011; Levine, 2011). However, some educational services such as diabetes or asthma self-management training are covered services by insurers because they are directly related to a medical condition and improve clinical outcomes, plus they are time limited. The introduction of habilitation as a category for the EHB raises questions about where to draw the line between habilitation and social/educational services that is not easily resolvable.

Other presenters and online questionnaire respondents advocated for inclusion of the full spectrum of Early and Periodic Screening, Diagnosis, and Treatment (EPSDT) program services, such as the Medicaid optional service of primary care case management and any treatments needed to address conditions found as a result of the preventive services covered (Booth, 2011; Courselle, 2011; Jezek, 2010; KFF, 2005; Maves, 2010), or given the large turnover factor from Medicaid to the exchanges, for inclusion of other types of support services offered in federally qualified health centers to ensure patient access to care (some of these services are included by insurers as part of medical management, but others such as transportation may not be). For tax purposes, the Internal Revenue Service (IRS) takes a broad view of expenditures that could be included as allowable deductible medical expenses (Harmon, 2011; Pratt, 2004),25 but this seems less applicable to the context of defining the EHB given that the IRS definition goes well beyond the kinds of expenses that are typically covered by any type of private health insurance plan.

24 § 1201, amending § 2706(a) of the Public Health Service Act [42 U.S.C. 300gg–5].

25 26 U.S.C. § 213 defines the allowable deductible expenses under the tax code.

As one of its criteria for the EHB, the committee concludes that inclusions in the EHB be based on being a medical service, not serving primarily a social or educational function. Because the boundaries of what is medical and nonmedical are not always distinct, the committee acknowledges that the decision of what is medical and nonmedical will for the time being need to rest at the health plan level with oversight by state regulators and HHS to document what services are offered or excluded, particularly in the area of habilitation. Many insurers are engaging in innovative programs to improve care practices and the appropriateness of services for individuals, and these might include some components that might be considered nonmedical yet they better help patients achieve medical goals, often in a less costly way. Thus, they may serve other committee criteria to be cost-effective and to support innovation. In Chapter 5, the committee reviews components of medical necessity definitions.

Conclusion: As one of its criteria for the EHB, the committee concludes that included benefits should be a medical service or item, not serving primarily a social or educational function. This conclusion does not preclude coverage of some educational or support services with that and the other committee criteria in mind (e.g., supported by a sufficient evidence base of effectiveness and promoting a health gain to justify the cost). However, like other services and items to be included as an essential health benefit, such service must meet the test of Recommendation 1 (see Chapter 5).

The next chapter outlines a process for defining the initial EHB set that builds on the conclusions reached in this chapter.

AHRQ (Agency for Healthcare Research and Quality). 2009a. Table 1.F.1 (2009) percent of private sector employees enrolled in a health insurance plan that had a deductible by firm size and selected characteristics: United States, 2009. http://meps.ahrq.gov/mepsweb/data_stats/summ_tables/insr/national/series_1/2009/tif1.htm (accessed July 11, 2011).

______. 2009b. Table 1.F.2 (2009). Average individual deductible (in dollars) per employee enrolled with single coverage in a health insurance plan that had a deductible at private-sector establishment by firm size and selected characteristics: United States, 2009. http://meps.ahrq.gov/mepsweb/data_stats/summ_tables/insr/national/series_1/2009/tif2.htm (accessed July 11, 2011).

______. 2009c. Table 1.F.3. Average family deductible (in dollars) per employee enrolled with family coverage in a health insurance plan that had a deductible at private-sector establishments by firm size and selected characteristics: United States, 2009. http://meps.ahrq.gov/mepsweb/data_stats/summ_tables/insr/national/series_1/2009/tif3.htm (accessed July 11, 2011).

The American Presidency Project. 2011. 376—statement on signing the Health Maintenance Organization Act of 1973: December 29, 1973. http://www.presidency.ucsb.edu/ws/index.php?pid=4092#axzz1S653ScBM (accessed June 28, 2011).

Bellows, N. M., H. A. Halpin, and S. B. McMenamin. 2006. State-mandated benefit review laws. Health Services Research 41(3 Pt 2):1104-1123.

Bergthold, L. 1993. Benefit design choices under managed competition. Health Affairs 12:99-109.

______. 2010. What is an “essential benefit”? http://healthaffairs.org/blog/2010/10/29/what-is-an-essential-benefit/ (accessed November 1, 2010).

BLS (Bureau of Labor Statistics). 2009. Table 14. Medical care benefits: Coverage for selected services, private industry workers, National Compensation Survey, 2008. In National Compensation Survey: Health plan provisions in private industry in the United States, 2008. Washington, DC: U.S. Bureau of Labor Statistics.

______. 2011. Table 1. Hospital room and board: Type of coverage, private industry workers, National Compensation Survey. http://www.bls.gov/ncs/ebs/sp/selmedbensreport.pdf (accessed July 11, 2011).

Blumberg, L. J., and S. McMorrow. 2009. What would health reform mean for small employers and their workers. http://www.urban.org/url.cfm?ID=411997 (accessed July 6, 2011).

Bocchino, C. 2010. Online questionnaire responses submitted by Carmella Bocchino, Executive Vice President, America’s Health Insurance Plans to the IOM Committee on the Determination of Essential Health Benefits, December 6.

Booth, M. 2011. Testimony to the IOM Committee on the Determination of Essential Health Benefits by Meg Booth, Deputy Director, Children’s Dental Health Project, Washington, DC, January 14.

Bowen, D. 2011. Testimony to the IOM Committee on the Determination of Essential Health Benefits by David Bowen, Deputy Director for Global Health Policy and Advocacy, Gates Foundation, Washington, DC, January 13.

Branscome, J. M. 2008. Statistical brief #207: Employer-sponsored single, employee-plus-one, and family health insurance coverage: Selection and cost, 2006. http://www.meps.ahrq.gov/mepsweb/data_files/publications/st207/stat207.shtml (accessed July 7, 2011).

Branscome, J. M., and K. E. Davis. 2011. Statistical brief #321: Employer-sponsored health insurance for small employers in the private sector, by industry classification, 2009. http://www.meps.ahrq.gov/mepsweb/data_files/publications/st321/stat321.shtml (accessed July 6, 2011).

British Columbia Ministry of Health. 2011. Medical and health care benefits. http://www.health.gov.bc.ca/msp/infoben/benefits.html (accessed June 30, 2011).

Bunce, V. C., and J. P. Wieske. 2010. Health insurance mandates in the states 2010. http://www.cahi.org/cahi_contents/resources/pdf/MandatesintheStates2010.pdf (accessed May 4, 2011).

Calega, V. 2011. Comments to the IOM Committee on the Determination of Essential Health Benefits by Virginia Calega, Vice President, Medical Management and Policy, Highmark Blue Cross Blue Shield, Washington, DC, January 13.

Cauchi, R. 2011. State health insurance mandates and the ACA* essential benefits provisions. http://www.ncsl.org/default.aspx?tabid=14227 (accessed November 8, 2011).

CBO (Congressional Budget Office). 2009a. Letter to the Honorable Evan Bayh, U.S. Senate from Douglas W. Elmendorf, Director, Congressional Budget Office, November 30, 2009.

______. 2009b. Letter to the Honorable Harry Reid, Senate Majority Leader from Douglas W. Elmendorf, Director, Congressional Budget Office, December 19, 2009.

CHBRP (California Health Benefits Review Program). 2009. Appendix 22: Other states’ health benefit review programs, 2009. Oakland, CA: California Health Benefits Review Program.

Chernew, M., D. M. Cutler, and P. S. Keenan. 2005. Increasing health insurance costs and the decline in insurance coverage. Health Services Research 40(4):1021-1039.

Collins, S. R., K. Davis, J. L. Nicholson, and K. Stremikis. 2010. Realizing health reform’s potential: Small businesses and the Affordable Care Act of 2010. New York, NY: The Commonwealth Fund.

Courselle, A. 2011. Online questionnaire responses submitted by Abigail Coursolle, Greenberg Traurig Equal Justice Works Staff Attorney, Western Center on Law & Poverty to the IOM Committee on the Determination of Essential Health Benefits, March 11.

Crimmel, B. L. 2010. Statistical brief #285: Employer-sponsored single, employee-plus-one, and family health insurance coverage: Selection and cost, 2009. http://www.meps.ahrq.gov/mepsweb/data_files/publications/st285/stat285.pdf (accessed November 8, 2011).

______. 2011. Statistical brief #325: Changes in premiums and employee contributions for employer-sponsored health insurance, Private industry, 2001-2009. http://www.meps.ahrq.gov/mepsweb/data_files/publications/st325/stat325.shtml (accessed November 8, 2011).

Darling, H. 2011. Recommendations on criteria and methods for defining and updating individual mandates and packages: Purchaser perspectives. PowerPoint Presentation to the IOM Committee on the Determination of Essential Health Benefits by Helen Darling, President and CEO, National Business Group on Health, Washington, DC, January 13.

Davis, K., and J. M. Branscome. 2011. Statistical brief #322: Employer-sponsored health insurance for large employers in the private sector, by industry classification, 2009. http://www.meps.ahrq.gov/mepsweb/data_files/publications/st322/stat322.shtml (accessed July 6, 2011).

DMHC (California Department of Managed Health Care). 2011. Independent state review processes. PowerPoint Presentation to the IOM Committee on the Determination of Essential Health Benefits by Cindy Ehnes, Director, Maureen McKennan, Acting Deputy Director for Plan and Provider Relations, and Andrew George, Assistant Deputy Director, Help Center, Department of Managed Health Care, Costa Mesa, CA, March 2.

DOL (Department of Labor). 2011. Selected medical benefits: A report from the Department of Labor to the Department of Health and Human Services. http://www.bls.gov/ncs/ebs/sp/selmedbensreport.pdf (accessed June 13, 2011).