This chapter describes criteria for eligibility and the process for application, certification, verification, participation, meal counting, and reimbursement in the National School Lunch Program (NSLP) and the School Breakfast Program (SBP), as well as the limitations of the current administrative process. It is essential to understand all elements of the school meals programs before considering alternative procedures that could reduce administrative burden and make it possible to provide nutritious meals to a greater number of the nation’s schoolchildren.1

ADMINISTRATIVE PROCESS OF THE SCHOOL MEALS PROGRAMS

This section describes the overall flow of the administration of the school meals programs and then provides detail on eligibility; certification; verification; participation; and counting, claiming, and reimbursement.

Process Flow

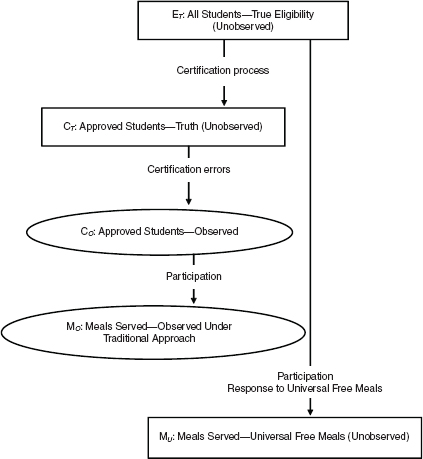

Figure 2-1 illustrates the flow of the school meals process, from determining the eligibility of students to serving them nutritionally qualified meals, noting that the distributions of students and meals

____________

1 This chapter draws heavily on Chapter 2 of the panel’s interim report (National Research Council, 2010).

FIGURE 2-1 School meals process and distributions of enrolled students and meals served across free, reduced-price, and full-price categories: Traditional approach and universal free meals.

SOURCE: Prepared by the panel.

served across the free, reduced-price, and full-price meal categories at each point differ. The first two boxes and the first oval in the figure reflect distributions based on all enrolled students; the second oval and last box relate to average daily meals served. For simplicity, we have assumed that the process depicted in the figure occurs instantaneously

and have ignored how the distributions and the relationships among them change over time.2

The top box in the figure, labeled “ET: All Students—True Eligibility (Unobserved),” represents the distribution of all enrolled students by their true eligibility status, including those who are eligible for free meals using program rules described below; those who are eligible for reduced-price meals using those rules; and all other students, who are eligible only for full-price meals. As noted, this distribution is not observed. The process by which students are identified and approved as being eligible for free or reduced-price meals is known as certification.3 Students who are found to be eligible through the certification process become approved students.

The second box in the figure, labeled “CT: Approved Students—Truth (Unobserved),” represents the distribution of all enrolled students according to a certification process with no errors. Some students who are eligible for free or reduced-price meals decline to participate in the certification process. All students who either do not apply or are not directly certified for free meals are eligible only for full-price meals, as are those students who apply but are found to be ineligible for free or reduced-price meals. The distribution, CT, is not observed. The number of students in the free category of CT will be less than or equal to the number in the free category of ET by the number of students who were not directly certified and who did not apply for benefits. Enrolled students who were not directly certified and did not apply for benefits will be in the full-price category of CT. Likewise, students in the reduced-price category of ET who did not apply will be in the full-price category of CT.

The first oval (and third item) in the figure, labeled “CO: Approved Students—Observed,” represents the distribution of enrolled students into categories of approved for free meals, approved for reduced-price meals, and eligible for full-price meals, in which the categories of approved for free or reduced-price meals are as determined by the actual operation of the certification process and maintained in school records. The certification process is described below. The difference between CT and CO is due to misclassification of students (errors) during the certification process. For example, some students who are eligible for free meals may have been approved for reduced-price meals.

____________

2 As discussed below, a student paying full price at the beginning of the school year can be approved for free meals later in the year if, for example, the family’s income falls. Once approved, the student can continue to receive free meals for the remainder of the year (and up to 30 days into the next year until a new eligibility determination is made), even if the family’s income rises above the eligibility threshold for free meals.

3 The certification process encompasses both direct certification by comparison of student enrollment lists with state and local lists of participants in several means-tested programs and the solicitation, submission, and review of applications.

On any given day, a student may bring a meal from home or purchase a meal that does not qualify for reimbursement because it does not satisfy the nutritional requirements of the school meals programs. Hence, schools must count the total number of reimbursable meals served each day and note whether each student taking a meal is approved for a free or reduced-price meal or must pay full price. The last two distributions in Figure 2-1 reflect the distribution of average daily reimbursable meals served across the three categories.

The second oval (and fourth item) in the figure, “MO: Meals Served— Observed Under Traditional Approach,” represents the distribution of meals served across the free, reduced-price, and full-price categories in a school that uses the traditional procedures for certifying students and claiming reimbursement. While some students never participate (take meals) or participate on only some days, others participate every day. When students line up in the cafeteria with their trays, a cashier determines whether each meal served qualifies as reimbursable under the school meals programs according to such criteria as food group composition and serving size. The cashier determines whether the student is approved for a free or reduced-price meal in a way that ensures there will be no overt identification of the student’s eligibility category.4 This process provides the meal counts maintained in school records that are used to determine federal reimbursements in the school meals programs.

The third box (and fifth item) in the figure, “MU: Meals Served— Universal Free Meals (Unobserved),” represents the participation distribution when meals are provided free to all students. The distribution is unobserved because meals are not counted by category when they are provided free under a special operating provision such as Provisions 2 or 3 or the American Community Survey (ACS) Eligibility Option (AEO). The available evidence suggests that if meals are provided at no cost, more students participate. This distribution is important in assessing the costs and benefits of a new provision, and a primary objective of the panel was to determine whether there is a reliable and operationally feasible method for estimating this distribution for a school, group of schools, or school district using available data.

____________

4 The Richard B. Russell National School Lunch Act (Section 9B(10):3-22) states

(10) No physical segregation of or other discrimination against any child eligible for a free lunch or a reduced-price lunch under this subsection shall be made by the school nor shall there be any overt identification of any child by special tokens or tickets, announced or published list of names, or by other means.

Available: http://www.fns.usda.gov/cnd/governance/Legislation/NSLA_12-13-10.pdf.

Eligibility

Students are eligible for free school meals if their family’s “current” income is at or below 130 percent of the poverty guideline for their family size. Current income requested on the application form “may be for the current month, the amount projected for the first month the application is made for, or for the month prior to application” (U.S. Department of Agriculture/Food and Nutrition Service, 2011b). Students are “categorically eligible” for free meals if someone in the family participates in certain other means-tested public assistance programs targeting the low-income population. Specifically, students are categorically eligible for free meals if their families receive assistance from the Supplemental Nutrition Assistance Program (SNAP, formerly the Food Stamp Program), Temporary Assistance to Needy Families (TANF), or the Food Distribution Program on Indian Reservations (FDPIR). A student also is categorically eligible if he/she is enrolled in a Head Start or Even Start program or is (1) a homeless child as determined by the school district’s homeless liaison or by the director of a homeless shelter, (2) a migrant child as determined by the state or local Migrant Education Program coordinator, or (3) a runaway child who is receiving assistance from a program under the Runaway and Homeless Youth Act and is identified by the local educational liaison. With the passage of the Healthy, Hunger-Free Kids Act of 2010, foster children also are categorically eligible for free meals.

Students who are not eligible for free meals are eligible for reduced-price meals if their family’s “current” income is greater than 130 percent of the poverty guideline and at or below 185 percent of the poverty guideline. All other students are eligible only for full-price meals (U.S. Department of Agriculture/Food and Nutrition Service, 2011b).

Certification

Certification is the process by which students are approved as being eligible for free or reduced-price meals. There are two types of certification: direct certification and the solicitation, submission, and review of applications. School districts, often through their state education agency, directly certify “categorically eligible” students based primarily on their participation in SNAP, TANF, or FDPIR. The 2004 Child Nutrition and WIC Reauthorization Act required that all school districts establish a system of direct certification of students from households that receive SNAP benefits by school year (SY) 2008-2009. Some states or districts also make use of TANF or other program data as part of direct certification. For direct certification, states or districts match lists of students (including names, addresses, and so on) with the administrative data concerning indi viduals participating in SNAP or other assistance programs. Students

matched in this way are “directly certified” as being eligible for free school meals. Parents are notified that their children are eligible and do not need to file an application. Matching for direct certification is done at least once a year, and beginning in 2011-2012 will be done three times a year.5 Some states and districts conduct direct certification more frequently to identify newly eligible students. For example, Washington State conducts direct certification monthly. In 2009-2010, an estimated 72 percent of students from SNAP-participant households nationwide were certified for free school meals through direct certification without applications.6 In 2010-2011, this number increased to 78 percent.7 As a result of errors in record matching or participation in a program for which a state does not perform direct certification, however, some categorically eligible students are not directly certified. Families of such students can establish their categorical eligibility by providing a SNAP, TANF, or FDPIR case number on their application for school meals.8

The application process begins just prior to and at the start of a school year (normally mid-July through early September), when school districts send a letter to the parents of their students describing the school meals programs, inviting them to apply, and providing an application form.9 The application requests information about participation in SNAP or other assistance programs, family composition, and family income. School or district officials review the applications and make a determination as to whether the students listed on the application should be approved for free or reduced-price meals. If an application lists a legitimate case number for SNAP or another approved program, the students are certified as being categorically eligible for free meals.

While most applications are submitted at the beginning of the school year, applications and eligibility are in effect from the date of approval through the entire school year and up to 30 operating days into the subsequent school year until a new eligibility determination is made. A family may submit an application at any time during the year, and it may do so later in the year if, for example, its income has fallen or it has started

____________

5 A 2011 interim rule issued by the U.S. Department of Agriculture (USDA) requires direct certification using SNAP records at least three times a year, beginning in 2011-2012.

6 State-level direct certification rates for SNAP (excluding Alaska, with a direct certification rate over 100 percent) ranged from 47 percent to 91 percent. A SNAP direct certification rate may be overstated if the state also directly certifies using TANF or FDPIR records (U.S. Department of Agriculture/Food and Nutrition Service, 2010:14).

7 In 2010-2011, state-level direct certification rates ranged from 51 percent to 97 percent (excluding Alaska) (U.S. Department of Agriculture/Food and Nutrition Service, 2011a:14).

8 If the family provides a valid SNAP, TANF, or FDPIR case number on the application, they do not need to provide further information about family income.

9 Some districts are moving to electronic applications.

|

|

|||

| Fiscal Year | Approved for Free Meals (%) |

Approved for Reduced-Price Meals (%) |

Must Pay Full Pricefor Meals (%) |

|

|

|||

| 2010 | 42.5 | 8.4 | 49.1 |

| 2009 | 40.1 | 8.6 | 51.3 |

| 2008 | 37.9 | 8.6 | 53.5 |

| 2007 | 37.1 | 8.3 | 54.6 |

| 2006 | 37.8 | 8.4 | 53.8 |

| 2005 | 37.1 | 8.1 | 54.8 |

|

|

|||

| NOTE: Approval status for the school meals programs includes both the National School Lunch Program (NSLP) and the School Breakfast Program (SBP). SOURCE: Tabulation from the Food and Nutrition Service (FNS) National Data Bank pro-vided to the panel, July 5, 2011. |

|||

participating in SNAP or TANF, qualifying it for greater benefits under the school meals programs.

The distribution of approved students by category for the school meals programs in fiscal years (FY) 2005 through 2010 is shown in Table 2-1. This is the CO distribution in Figure 2-1.

It should be noted that not all families with students who are eligible for free or reduced-priced meals submit applications. In 1994, the Food and Nutrition Service (FNS) reported that “available data indicate that between 16 percent and 25 percent of potentially eligible families do not apply for school meals benefits” (U.S. Department of Agriculture/Food and Nutrition Service, 1994a:1-5). Although this may no longer be true in light of incentives (such as the allocation of funds in other programs using the school lunch eligibility percentage) and processes (such as direct certification) for certifying as many eligible students as possible for free meals, more recent estimates are not available.

An FNS study enabled a comparison of the distributions of eligible and certified students (U.S. Department of Agriculture/Food and Nutrition Service, 1999). It used data from the Current Population Survey (CPS) to estimate the percentage of students who were income-eligible for free and reduced-price meals, providing a survey-based estimate for ET (see Figure 2-1), with eligibility based on annual income data. These estimates were compared with the numbers of students approved as eligible for free or reduced-price meals, CO. Table 2-2, taken from that report, indicates that the number of students certified was growing from 1993 through 1998, whereas the number eligible according to annual income was flat or declining. By 1998, the number of students approved for free meals was 127 percent of the number of students who were estimated to be income-eligible for free meals, and the number of students approved for free or

|

|

||||||

|

Free Meals |

Free and Reduced-Price Meals |

|||||

|

Year |

CPS Income-Eligible |

NSLP-Certified |

Certified/Eligible(%) |

CPS Income-Eligible |

NSLP-Certified |

Certified/Eligible(%) |

|

|

||||||

| 1999 | 12,464 | 15,876 | 127 | 18,928 | 19,260 | 102 |

| 1998 | 13,128 | 15,965 | 122 | 19,190 | 19,067 | 99 |

| 1997 | 13,461 | 15,799 | 117 | 19,416 | 18,762 | 97 |

| 1996 | 13,382 | 15,415 | 115 | 19,727 | 18,273 | 93 |

| 1995 | 13,655 | 14,920 | 109 | 20,030 | 17,577 | 88 |

| 1994 | 13,718 | 14,396 | 105 | 19,609 | 16,952 | 86 |

| 1993 | 13,924 | 13,792 | 99 | 19,750 | 16,273 | 82 |

|

|

||||||

SOURCE: U.S. Department of Agriculture/Food and Nutrition Service (1999:3, 5).

reduced-price meals was 102 percent of the number of students who were estimated to be income-eligible for free or reduced-price meals, indicating the possibility of over certification in the school meals programs. As noted in a study by the National Research Council of the National Academy of Sciences, “results like this contributed to the Improper Payments Act of 2002, which requires that various federal agencies identify and reduce erroneous payments in their programs” (National Research Council, 2009:14).10 Subsequent research found that at least some of the difference between income eligibility estimated from the CPS and approval status under the school meals programs could be due to how income relative to poverty is measured (annual or monthly) and to changes in monthly income from the time of application to the time of verification (U.S. Department of Agriculture/Economic Research Service, 2006b).

In response to the Improper Payments Act, FNS funded the Access, Participation, Eligibility, and Certification (APEC) Study in 2004 to obtain national estimates of the amounts and rates of erroneous payments in the NSLP and SBP (U.S. Department of Agriculture/Food and Nutrition Service, 2007b). Erroneous payments may be due to certification errors attributable to household misreporting or administrative mistakes or to

____________

10 As discussed in Chapters 3 and 5 of the 2009 National Research Council report, estimates of eligibility based on annual income are likely to be too low, given that families may have 1 or more months of low income that would qualify them for free or reduced-price meals even when their annual income exceeded the income eligibility limits.

noncertification errors in counting and claiming payment for reimbursable meals. The study used a complex sample design to survey school districts, schools, and students.

The APEC study provided baseline estimates of erroneous payments for the 2005-2006 school year. It also provided parameters for estimation models to allow FNS staff to update estimates of erroneous payments. The study found that 77.5 percent of all certified students and denied applicants were correctly certified or denied meal benefits, whereas 22.5 percent were certified in error or erroneously denied benefits. The study also found that overcertification was more common than undercertification: the percentage of students certified for a higher level of benefits than that for which they were eligible (the overcertification rate) was 15 percent; the percentage of students either certified for a lower level of benefits than that for which they were eligible or erroneously denied benefits (the undercertification rate) was 7.5 percent. More detailed results from the APEC study are discussed later in this chapter.

Verification

In addition to special studies, such as the APEC study, the accuracy of the certification process is examined through a requirement for school districts to verify a sample of NSLP applications annually. Typically, a school district is required to conduct an annual verification of 3 percent or 3,000 (whichever is smaller) of the applications approved and on file as of October 1 of the current school year.11 Verification is to be completed by November 15 of the current school year. Samples are to be selected from “error prone” applications, those from families whose reported monthly income is within $100 of a school meals eligibility threshold (130 percent or 185 percent of the applicable poverty guideline). The households that submitted the applications selected for verification are required to submit documentation of income for any point in time between the month prior to application and the time of verification. School districts make at least one follow-up attempt with households that fail to respond. Students in households that fail to provide the required documentation are removed from eligibility. Results of verification studies are reported annually on form FNS-742. Data for each school district are reported through state agencies to FNS regional offices, which upload the data to FNS headquarters, where they are maintained.

____________

11 In some states, the state agency conducts the verification.

|

|

||||

|

Percentage of |

||||

|

Fiscal Year |

NSLP |

Free |

Reduced |

Full |

|

|

||||

| 2010 | 31,746,374 | 55.4 | 9.5 | 35.1 |

| 2009 | 31,311,515 | 52.0 | 10.1 | 37.9 |

| 2008 | 31,015,551 | 49.6 | 10.1 | 40.3 |

| 2007 | 30,629,762 | 48.9 | 10.0 | 41.2 |

| 2006 | 30,128,292 | 49.0 | 9.8 | 41.2 |

| 2005 | 29,645,759 | 49.2 | 9.7 | 41.1 |

|

|

||||

| SOURCE: Tabulation from the Food and Nutrition Service (FNS) National Data Bank provided to the panel, July 5, 2011. | ||||

Participation

Any student attending a school that participates in the school meals programs may obtain a meal for free or at the reduced price, if so approved, or by paying the full price for the meal. As noted earlier, cashiers assess which meals meet the nutritional requirements of the NSLP and SBP and, for qualifying meals, record each student’s approval status (free, reduced price, full price) in a way that does not overtly identify the student’s status. Meal counts by category are aggregated for each month for the school, the school district, and the state. This process provides the meal counts maintained in school records, which are also reported at the state level to FNS via form FNS-10.

FNS defines participation to be the 9-month (September-May) average of each month’s average daily meals served, divided by an attendance factor of .927 to account for absenteeism. This yields an estimate of the expected number of meals that would be served if students were never absent. Table 2-3 is from a special tabulation from the FNS National Data Bank that was provided to the panel in 2011. It shows participation in the NSLP by year and the percentage of meals served that were free, reduced-price, or full-price. The percentage distribution is MO in Figure 2-1.12

Another way of analyzing participation is to calculate a rate for each meal category (see Table 2-4). Dividing participation (average daily number of meals served divided by .927) in a category by the total number

____________

12 The factor .927 is used by FNS to estimate what participation would be if students were never absent. FNS derives participation estimates by applying the assumption that all students, including those who are eligible for free and reduced-price meals, attend school at the same rate of .927. The panel did not use this factor in any of its analyses.

|

|

|||

|

Participation Rate (Percentage) |

|||

| Fiscal Year | Free Approved | Reduced Price Approved |

Full Price |

|

|

|||

| 2010 | 81.9 | 73.1 | 43.7 |

| 2009 | 80.5 | 72.8 | 45.9 |

| 2008 | 80.7 | 72.2 | 46.4 |

| 2007 | 80.8 | 73.5 | 46.2 |

| 2006 | 78.5 | 70.8 | 46.3 |

| 2005 | 79.1 | 71.5 | 44.9 |

|

|

|||

NOTE: The participation rate is computed as average daily meals served in category dividedby the product of .927 and the number of students certified in that category. The factor .927is intended to account for the fact that not all enrolled students are at school every day.

SOURCE: Tabulation from the Food and Nutrition Service (FNS) National Data Bank pro-vided to the panel, July 5, 2011.

of enrolled students approved in that category shows consistently higher participation by students approved for free meals (81.9 percent in 2009-2010), followed by students approved for reduced-price meals (73.1 percent in 2009-2010). Students having to pay full price participate at lower rates (43.7 percent in 2009-2010).

Additional information on participation is available from the School Nutrition Dietary Assessment Study-III (SNDA-III) (U.S. Department of Agriculture/Food and Nutrition Service, 2007a). The main focus of the study was on assessing the nutritional content of school meals and identifying students’ and parents’ reasons for participation or non participation. The study used the following two definitions of participation: (1) the percentage of enrolled students who took a meal that qualified under the school meals programs on a target day and (2) the percentage who “usually” took such a meal, with “usually” being defined as 3 or more days per week.

On a typical day in the 2004-2005 school year, about 62 percent of all students participated in the NSLP and about 18 percent in the SBP according to SNDA-III. Nearly three-quarters of students reported participating in the NSLP on 3 or more days per week, and one-quarter reported participating in the SBP on 3 or more days per week. Parents of students who did not participate in the NSLP reported some of the same reasons for this decision as those given by students—for example, that their child did not like the cafeteria food (68 percent) or preferred to bring a lunch from home (65 percent).

Table 2-5, based on SNDA-III, shows the percentage of enrolled students who participated in the NSLP on a target day in 2004-2005 sepa-

|

|

||||

|

Income/Meal Category |

Elementary (%) |

Middle (%) |

High (%) |

All |

|

|

||||

|

Income relative to poverty guideline: |

||||

|

Less than or equal to 130 percent |

86.9 |

71.7 |

55.5 |

75.7 |

|

Between 130 and 185 percent |

86.5 |

63.5 |

64.1 |

75.5 |

|

More than 185 percent |

62.1 |

54.6 |

36.3 |

52.6 |

|

Receipt of meals (parent report): |

||||

|

Receives free or reduced-price meals |

86.5 |

70.7 |

66.4 |

78.8 |

|

Does not receive free or reduced-price meals |

60.1 |

51.9 |

34.3 |

49.6 |

|

|

||||

SOURCE: U.S. Department of Agriculture/Food and Nutrition Service (2007a:36, vol. II).

rately for elementary, middle, and high school students by income level and reported receipt of free or reduced-price meals (official approval status was not determined). The table shows that about 87 percent of all elementary school students with family income less than or equal to 185 percent of the poverty guideline (that is, students income- eligible for either a free or a reduced-price meal) and 62 percent of all elementary school students with family income more than 185 percent of the poverty guideline participated in the NSLP on the target day. For middle school students, participation rates were lower than those for elementary school students in all three income categories; participation by those income-eligible for a reduced-price meal fell between participation by those eligible for a free meal and those not eligible for either a free or a reduced-price meal. For high school students, participation rates were lowest of all among those income-eligible for free meals and those income-eligible only for full-price meals.

One of the panel’s objectives was to recommend a method for estimating the unobserved distribution in Figure 2-1 labeled “MU: Meals Served—Universal Free Meals (Unobserved).” This distribution reflects what would happen in the future if a district adopted free meals for all students through a new approach that used available data, such as those from the ACS, to establish claiming percentages13 for reimbursement from

____________

13 Claiming percentages are used in determining a school district’s reimbursement for the school meals programs. In the traditional approach in the contiguous states in the 2011-2012 school year, a school district with less than 60 percent of students eligible for free or reduced-price meals in the 2009-2010 school year was reimbursed $2.77 for every free lunch served, $2.37 for every reduced-

the U.S. Department of Agriculture (USDA), the AEO option. A student who was approved for a reduced-price meal would save $.40 per meal with universal free meals, and a student who would otherwise pay the full price for a meal would save the entire amount that was charged by the school district. Consequently, one might expect that the increased participation due to providing free meals to all students would be greatest among students who formerly had to pay full price for their meals, followed by those who paid a reduced price. As described in Chapter 3, however, one participant in the panel’s workshop with selected school nutrition directors noted that, based on his experience, providing free meals to all students also increases participation among students who have always been eligible for free meals because the stigma associated with the program has been removed.

Counting, Claiming, and Reimbursement

The meal-counting process begins when the cashier determines whether a student’s meal qualifies as reimbursable (by satisfying the programs’ nutritional requirements) and whether the student is approved for a free meal or a reduced-price meal or must pay full price. As noted above, a student’s approval status cannot be overtly identified by this process. Thus, for example, all students taking a reimbursable school meal must go through the same cashier line, regardless of eligibility status. According to the APEC report (U.S. Department of Agriculture/Food and Nutrition Service, 2007b:16, vol. I):

To obtain meal reimbursements, school personnel must accurately count, record, and claim the number of reimbursable program meals actually served to students by category—free, reduced-price, and paid (except for schools using Provision 2 or Provision 3 in non-base years). To do this, school districts must put in place a system that issues benefits, records meal counts at the school’s point of service, and reports them to the central district office. The district must receive reports of meal counts from the schools, consolidate them, and submit claims for reimbursement to its state agency.

price lunch served, and $0.26 for every full-price lunch served as part of the NSLP. A district with 60 percent or more of students eligible for free or reduced-price meals in the 2009-2010 school year received an additional $.02 per lunch. There are separate reimbursement rates for breakfast. The claiming percentages are the percentage of total meals (separate for lunch and breakfast) that are served to students eligible for free meals, the percentage served to students eligible for reduced-price meals, and the percentage served to students who must pay full price.

TABLE 2-6 Federal Reimbursement Rates for 2010-2011 School Meals Programs by Eligibility Category

|

|

||

| Eligibility Category | Lunch Rate | Breakfast Rate |

|

|

||

| Free | $2.72 ($2.74) | $1.48 ($1.76) |

| Reduced Price | $2.32 ($2.34) | $1.18 ($1.46) |

| Full Price | $0.26 ($0.28) | $0.26 ($0.26) |

|

|

||

| NOTE: Dollar amounts in parentheses are reimbursement increments for schools serving large proportions of free and reduced-price meals (see text). SOURCE: See http://www.fns.usda.gov/cnd/Governance/notices/naps/NAPs10-11.pdf. |

||

States report monthly aggregates to FNS on form FNS-10. FNS uses these data to determine reimbursements due to the states, which distribute the reimbursements to the school districts.

Most of the support USDA provides to schools in the NSLP and SBP comes in the form of a monthly cash reimbursement for each meal served. Table 2-6 shows reimbursement rates by eligibility category for school year 2010-2011. (Rates may be adjusted annually.) Schools that served more than 60 percent free and reduced-price lunches 2 years earlier are eligible for $.02 more per category for the NSLP (shown in parentheses in the table); schools that served more than 40 percent free and reduced-price lunches are eligible for higher severe-needs rates for the SBP (shown in parentheses in the table). Higher reimbursement rates also are in effect for Alaska and Hawaii.

SPECIAL PROVISIONS AND OPTIONS FOR OPERATING THE SCHOOL MEALS PROGRAMS

As discussed in Chapter 1, schools, groups of schools, or entire school districts may choose to apply for one of four special provisions or options instead of following the traditional procedures for eligibility determination and meal counting. Typically, they apply for these provisions through the state. These provisions are most appropriate for areas with high percentages of students eligible for free or reduced-price meals. Provisions 1 and 2 were included in federal regulations in 1980, while Provision 3 was included in 1995. The Community Eligibility Option (CEO) was approved under the Healthy, Hunger-Free Kids Act of 2010 and is being implemented as a pilot in Illinois, Kentucky, and Michigan for school year 2011-2012, and will be available to all states in 2014-2015. Each special provision results in some variation on the traditional method for establishing claiming percentages.14 Two other options were authorized for

____________

14 Although claiming percentages are not used explicitly to claim reimbursement under traditional operating procedures, we discuss them explicitly in this report to illustrate the differences among the traditional procedures and the various special provisions and options.

consideration by the secretary of agriculture in the Healthy, Hunger-Free Kids Act of 2010—use of a periodic socioeconomic survey and the AEO. These provisions and options are summarized in Box 2-1.

Provisions 1, 2, and 3, the Community Eligibility Option, Use of a Socioeconomic Survey, and the ACS Eligibility Option15

Provision 1 permits schools enrolling at least 80 percent of students who are eligible for free or reduced-price meals to certify students’ eligibility for free meals for 2 years instead of reestablishing eligibility every year. Provision 1 enables administrative efficiencies but does not involve providing universal free meals. There are currently very few (perhaps no) schools operating under Provision 1.

Provision 2 permits schools, groups of schools, and entire school districts to establish claiming percentages for federal reimbursement in accordance with information collected during a base period and to serve all meals at no charge for a 4-year period. The first year is the base year, during which the school provides all meals for free but collects applications, makes eligibility determinations, conducts verifications, and takes meal counts by type.16 During the next 3 years, the school performs no new eligibility determinations or verification checks and counts only the total number of reimbursable meals served each day.17 Reimbursement during these years is determined by multiplying the total count of reimbursable meals for a claiming month by the percentages of free, reduced-price, and full-price meals served during the corresponding month of the base year to estimate the number of meals served in each category. The base year is included as part of the 4 years. At the end of each 4-year period, the district may apply to the state agency for a 4-year extension if the income level of the school’s population has remained stable, declined, or improved only negligibly since the base year.18 If an extension is not appropriate, the district may return to the traditional method or apply to conduct another Provision 2 base year, use a streamlined base year, or convert to Provision 3 (either

____________

15 FNS provides information about all provisions at http://www.fns.usda.gov/cnd/Governance/prov-1-2-3/provision1_2_3.htm.

16 Note that with the operation of a base year with universal free meals and the collection and processing of applications, the reimbursement for a district is based on data that reflect the impact of changes in participation resulting from the provision of free meals.

17 Under Provision 2, the count of the total number of meals served need not be broken down by eligibility category.

18 The income level of the school’s population meets this definition if it has not improved by more than 5 percent, after adjusting for inflation, between the base year and the comparison year. Income is measured by the source of socioeconomic data the district used in its approved application for provision status to the state. Available: http://www.fns.usda.gov/cnd/Governance/prov-1-2-3/Prov2Guidance.pdf.

| Provision 1 | Authorized in 1980. Must have 80 percent or more free- or reduced-price-eligible. Applications every 2 years. |

| Provision 2 | Authorized in 1980. Universal free. Base year with universal free. New base year every 4 years unless extended. Reimbursement: blended reimbursement rate (BRR) using percentage of meals served by category in base year month times meals served in current month. |

| Provision 3 | Authorized in 1995. Universal free. Base year not necessarily with universal free. New base year every 4 years unless extended. Reimbursement: BRR using percentage of meals served by category in base-year month times meals served in base-year month times adjustment. |

| Community Eligibility Option | Authorized in 2010. Universal free. Implemented in three states in 2011, available to all states in 2014-2015. No applications; uses direct certification and local lists. Reimbursement: BRR based on adjusted fraction identified for free meals, zero for reduced price, and for full price—1 minus the adjusted fraction for free times meals served in current month. Direct certification to be performed at least every 4 years. |

| ACS Eligibility Option | Authorized for secretary of agriculture’s consideration in 2010. Universal free. Base year with universal free. No new base year required. Reimbursement: BRR based on benchmarked ACS estimates of eligibility rates by category and base-year participation rates by category, times meals served in current month. |

| Socioeconomic Survey Option | Authorized for secretary of agriculture’s consideration in 2010 for implementation in not more than three districts. Universal free. Periodic socio-economic survey to estimate eligibility rates. Reimbursement: BRR based on estimated eligibility rates times meals served in current month. |

| SOURCE: Prepared by the panel. | |

with a Provision 3 base year or using the original Provision 2 base year). Some schools use Provision 2 only for the SBP. These schools still collect applications, make eligibility determinations, and perform verifications for households with students that participate in the NSLP.

Provision 3 permits schools, groups of schools, and school districts to receive the same level of federal cash and commodity assistance each year during a 4-year period, with some adjustments. The base year is the last year the school made eligibility determinations and counted reimbursable meals by type, and typically meals are not served free during this year (although they may be). For the subsequent 4-year period, schools must serve meals to all participating students at no charge, and do not make additional eligibility determinations or conduct additional verification checks. Reimbursement is based on current-year reimbursement rates and meals served by category during the base year, with adjustments for changes in enrollment and number of operating days. In contrast with Provision 2, the base year of Provision 3 is not included as part of the 4 years, and schools may charge students for meals during the base year. At the end of each 4-year period, the district may apply to the state for a 4-year extension if the income level of the school’s population has remained stable, declined, or improved only negligibly. If an extension is not appropriate, the district may return to the traditional method or apply to conduct another base year, conduct a streamlined base year, or convert to Provision 2 (either with a Provision 2 base year or using the original Provision 3 base year as the base year for Provision 2).

The Community Eligibility Option permits schools, groups of schools, and school districts to provide meal service to all students at no charge for 4 years if they identify 40 percent or more of enrolled students as being categorically eligible for free meals through direct certification or as certified by local officials, mainly through lists of, for example, homeless students, migrant students, runaways, or foster students. Such students are termed “identified students.” The estimated percentage of free meals is the product of the percentage of enrolled students who are identified and a specified factor (currently 1.6). This percentage is capped at 100 percent. The estimated percentage of full-price meals is 100 percent minus the estimated percentage of free meals.19 The reimbursement is the total number of meals served times the sum of the product of the percentage of free meals and the free meal reimbursement rate and the product of the percentage of full-price meals and the full-price meal reimbursement rate divided by 100. Schools or school districts are required to conduct direct certification every 4 years to reestablish eligibility and the percentage of identified students. However, they may conduct direct certifica-

____________

19 It is assumed that no reduced-price meals are served.

tion more frequently and, if the percentage is larger, may use the larger percentage to claim reimbursement. If the percentage is smaller, they are not required to use it in intermediate years.

A Socioeconomic Survey was first used in the Philadelphia Pilot Project. FNS often uses pilot projects to test alternative procedures for the school meals programs. Since 1991 in the School District of Philadelphia, about one-third of schools have been operating under the traditional procedures, and about two-thirds have been providing free meals to all students and developing claiming percentages by combining information about students in households directly certified for free meals with information from a household survey designed to determine eligibility for free and reduced-price meals (Reinvestment Fund, 2007). The application and verification processes are eliminated for the latter schools. The steps in the process for estimating claiming percentages include direct certification, followed by a survey of nondirectly certified students. The direct certification and household survey data showed that 79.6 percent of students attending schools with universal free meals were eligible for free or reduced-price meals in school year 2006-2007. As illustrated later in this section, reimbursement for the part of Philadelphia where eligibility is determined from a socioeconomic survey is based on the eligibility distribution of enrolled students rather than on participation.

In the early 2000s, FNS commissioned the U.S. Census Bureau to develop eligibility estimates for schools in the School District of Philadelphia from the 2000 census long-form sample,20 which the ACS replaces, to determine the usefulness of such estimates in place of a special survey or other method (U.S. Census Bureau, 2005). The estimates from the decennial census were compared with the counts of students approved for free and reduced-price meals from the National Center for Education Statistics’ (NCES’) Common Core of Data (CCD) for all schools in Philadelphia. The study found that on average, 61 percent of students were eligible for free or reduced-price meals based on the 2000 census, compared with 74 percent approved according to the CCD.21

The Philadelphia pilot, the only district in the country using a socio-economic survey, was scheduled to end after the 2009-2010 school year.

____________

20 Although eligibility for the school meals programs is, as noted above, based on monthly income for students who are not directly certified or otherwise categorically eligible, esti mates from the decennial census must be derived using the annual income data that are collected on the long-form questionnaire.

21 The data cited in this paragraph are for year 2000. Data cited in the preceding paragraph are for 2006-2007. The Reinvestment Fund compared 2000 census Public Use Microdata Sample (PUMS) data with ACS 2005 data and documented a drop of 5 percent in eligibility for free and reduced-price meals (not counting eligibility because of participation in SNAP and receipt of public assistance income).

However, the program was granted an extension, and now the Healthy, Hunger-Free Kids Act of 2010 authorizes the secretary of agriculture to consider an approach that uses a periodic socioeconomic survey of households of children enrolled in schools within a school food authority (SFA) in not more than three SFAs that participate in the NSLP. According to the law, use of a socioeconomic survey would also require universal free feeding and reimbursement based on eligibility as determined through the survey. The law requires further that USDA establish requirements for use of such surveys, including criteria for survey design, sample frame validity, minimum level of statistical precision, minimum survey response rate, frequency of data collection, and other criteria as deemed necessary.

The AEO is the name selected by the panel for a potential new provision relying on the ACS and other information to establish claiming percentages.22 The Healthy, Hunger-Free Kids Act of 2010 authorized the Secretary of Agriculture to consider implementing the AEO. Like Provisions 2 and 3, it would permit schools, groups of schools, and entire school districts to serve all meals at no charge. Under the procedures recommended by the panel, the AEO would, like Provisions 2 and 3, establish claiming percentages for federal reimbursement using information collected during a base period. A difference between the AEO and Provisions 2 and 3, however, is that the AEO claiming percentages would be updated annually, using estimates from the ACS, and there would be no requirement to conduct a new base year periodically. During the first year of the AEO, the participating schools in a district would provide free meals to all students but collect applications, make eligibility determinations, conduct verifications, and count meals by category. The base year data used to determine reimbursement would include the impact on participation of providing free meals. In the following years, the schools would conduct no new eligibility determinations or verification checks and count only the total number of reimbursable meals served each day. The mechanism for determining reimbursement under the AEO is discussed in general later in this chapter, with detail provided in Chapter 5.

Department of Education Requirements for Using NSLP Certification Data Under Provisions 2 and 3 and the CEO

Title 1, Part A, of the Elementary and Secondary Education Act of 1965 (ESEA), as amended, requires a local education agency (LEA) to rank schools based on the percentage of students who are economically disad-vantaged and, for accountability purposes, requires reports of progress toward achievement standards for economically disadvantaged students:

____________

22 Detail on how the AEO might work is provided in Chapter 5.

To meet this requirement an LEA must have school level data on individual economically disadvantaged students. For many LEAs information from the NSLP is likely to be the best, and perhaps the only, source of data available to identify these students. Moreover, in the case of priority for public school choice and eligibility for supplemental education services, the law specifically requires an LEA to use the same data it uses for making within-district Title I allocations; historically, most LEAs use school lunch data for that purpose.23

With Provisions 2 and 3 and the CEO, the NSLP data on which students are eligible for free and reduced-price meals are no longer available during nonbase years. The Department of Education disseminated guidance to states on this issue,24 which states that “for purposes of disaggregating assessment data by the economically disadvantaged subgroup for reporting and accountability and for identifying students as economically disadvantaged in implementing supplemental education services and priority for school choice, school officials may deem all students in a CEO school as economically disadvantaged.” The same treatment is provided for Provision 2 and 3 schools. Further, “when annually determining the eligibility of a CEO school to receive Title I funds and its Title I allocation, an LEA must assume that the percentage of economically disadvantaged students in the school is proportionate to the percentage of meals for which the CEO school is reimbursed for free meals by the USDA for the same school year.” Provision 2 and 3 schools are to use the percentage of students certified as eligible for free or reduced-price meals during the base year for this purpose. For schools operating under the traditional approach, the percentages are derived annually from the school meals certification and verification process.

Comparison of Provisions and Options

Provision 1 offers the least reduction of administrative burden among the six alternatives—Provisions 1, 2, and 3; the CEO; use of a socio-economic survey; and the AEO—because it reduces the burden of the application process by only about one-half by requiring that applications be taken once every 2 years. In the second year, applications are still needed for students new to the school district. Provision 1 has no impact on participation. All other provisions and options offer a greater reduction of administrative burden; in return, schools electing to adopt one of these provisions or options must use sources other than federal funds to pay the

____________

23 Memorandum from Carl Harris, deputy assistant secretary for education to state com missioners of education, dated May 20, 2011.

24 Ibid.

difference between the federal reimbursement and the cost of providing all meals at no charge. According to the Food Research and Action Center, “schools with high percentages of low-income students—75 percent or more in some cases—are able to use Provision 2 for both breakfast and lunch without losing money. Some schools have opted to use Provision 2 for just breakfast when the percentage of free and reduced-price students is as low as 60 percent.”25 According to the SNDA-III study, 12.9 percent of schools used Provision 2 and 1.3 percent of schools used Provision 3 to provide free lunches to all students in school year 2004-2005 (U.S. Department of Agriculture/Food and Nutrition Service, 2007b:47).

The CEO offers the greatest reduction in administrative burden because it does not require base-year applications from families to establish claiming percentages and relies only on identification of categorically eligible students through direct certification and local officials’ lists. However, it can be used only by schools or districts with more than 40 percent of enrolled students who are “identified,” and according to this criterion, only 3.5 percent of districts reporting on form FNS-742 in 2009-2010 would be eligible to participate in the CEO districtwide.

Provisions 2 and 3 and the AEO could be implemented by any district determining that doing so would be economically feasible, subject to approval. The AEO is similar to Provision 2 in terms of reduction of burden during the first 4-year period. Under the procedures recommended by the panel, however, the AEO would provide additional savings thereafter because it does not require subsequent base years. In comparison with Provisions 2 and 3, the AEO has an advantage in that it uses annual releases of ACS data to update claiming percentages each year to reflect changes in socioeconomic conditions in a district. A disadvantage is that the survey data are less timely and therefore slower to reflect changing conditions than new certification data from a new base year.

ALTERNATIVE REIMBURSEMENT FORMULAS

The reimbursement formulas discussed below may be applied for an entire school district, a group of schools, or an individual school. Should a district choose to use multiple options within the district, the reimbursement formulas are applied separately, and the sum is the reimbursement for the school district.

Under the traditional procedures for operating the school meals programs (and under Provision 1), federal financial assistance to school districts is calculated as the total number of reimbursable meals served to students approved for free, reduced-price, or full-price meals multiplied

____________

25 See http://frac.org/newsite/wp-content/uploads/2009/05/provision2.pdf.

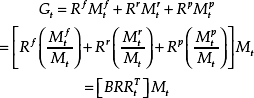

by the applicable meal reimbursement rates. Thus, the federal government’s outlays (G) for reimbursable meals under the NSLP or SBP are

where

- Gt is the federal government’s outlay for reimbursable meals in month t, in dollars;

- Rf is the reimbursement rate for free meals for this school year, in dollars (e.g., $2.77 for the NSLP in 2011-2012, if the school is not eligible for an increment);

- Rr is the reimbursement rate for reduced-price meals for this school year, in dollars;

- Rp is the reimbursement rate for full-price meals for this school year, in dollars;

- Mtf is the total number of free meals served in month t;

- Mtr is the total number of reduced-price meals served in month t;

- Mpt is the total number of full-price meals served in month t;

- Mt = Mtf + Mtr + Mpt is the total number of reimbursable meals served in month t; and

- BRRtT is the blended reimbursement rate for the traditional approach (denoted by “T”) in month t.

The second way of writing the federal government’s outlays shown above (the three terms in brackets) illustrates the use of claiming rates (if expressed as a ratio) or claiming percentages (if expressed as a percentage). The claiming percentages under traditional operating procedures are the percentage of meals served in each eligibility category (free, reduced-price, or full-price). The third way of writing the federal government’s outlays shown above illustrates the concept of the blended reimbursement rate (BRR) as a summary measure of the three claiming rates, and it is used in later chapters to illustrate the effects of using different estimates as a basis for reimbursement.

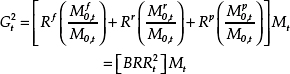

Under Provision 2, the numbers of meals served by category—Mtf, Mtr,and Mpt —are unknown because they are not counted, but the total, Mt, is known, and can be used along with counts of meals served by category during the same month of the base year to determine the

reimbursement amount. Therefore, the reimbursement formula for Provision 2 is

where

- G2t is the federal government’s outlay for reimbursable meals served in month t in Provision 2 schools, in dollars;

- Rf, Rr, and Rp are reimbursement rates as defined above;

- Mt is the total number of reimbursable meals served during month t;

- Mf0,t is the total number of free meals served in month t of the base year;

- Mr0,t is the total number of reduced-price meals served in month t of the base year;

- Mp0,t is the total number of full-price meals served in month t of the base year;

- M0,t = Mf0,t + Mr0,t + Mp0,t is the total number of reimbursable meals served during month t of the base year; and

- BRRt 2 is the blended reimbursement rate for Provision 2 in month t.

The ratios in the first version of the equation above are the Provision 2 claiming rates, based on the percentage of meals served in each category in the base year. Like the BRR for the traditional approach, the BRR for Provision 2 varies from month to month.

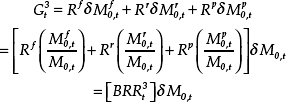

Under Provision 3, meals served by category are estimated by using meals served in the same month of the base year multiplied by a factor reflecting the change in enrollment and the number of operating days relative to the base year. Therefore, the reimbursement formula for Provision 3 is

where

- G3t is the federal government’s outlay in month t for Provision 3 schools, in dollars;

- Rf, Rr, and Rp are reimbursement rates as defined above;

- Mf0,t is the total number of free meals served in month t of the base year;

- Mr0,t is the total number of reduced-price meals served in month t of the base year;

- Mp0,t is the total number of full-price meals served in month t of the base year;

- M0,t = Mf0,t + Mr0,t + Mp0,t is the total number of meals served during month t of the base year;

- δ is a ratio adjustment (ratio of current-year to base-year value) reflecting changes in enrollment and the number of operating days (e.g., if enrollment increased by 5 percent since the base year and the number of operating days were unchanged, the factor would be 1.05); and

- BRRt 3 is the blended reimbursement rate for Provision 3 in month t.

The claiming percentages and BRR under Provision 3 are identical to the claiming percentages and BRR under Provision 2. Total reimbursements are different, however, because under Provision 2, schools count the number of meals served in each month (Mt), while under Provision 3, schools use the number of meals served in that month of the base year, adjusted only for changes in enrollment and operating days (using 5), as an estimate of the meals served in the current month.

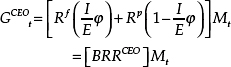

Under the Community Eligibility Option, reimbursement is based on the total number of meals served, the ratio of the number of identified students26 to the number of enrolled students in the base year (or a year since the base year),27 and a factor specified in the Healthy, Hunger-Free Kids Act of 2010. The factor was set by the act at 1.6, and can be updated by the Secretary of Agriculture beginning with the 2014-2015 school year.

____________

26 Identified students are certified as eligible for free meals based on documentation of receipt of benefits or categorical eligibility as described in section 245.6a(c)(2) of Title 7, Code of Federal Regulations. They include students who are directly certified, on the home less liaison list, income-eligible for Head Start or pre-K Even Start, in residential child care institutions, migrants, runaways, foster children certified through means other than an application, and other nonapplicants approved by local officials.

27 The base year immediately precedes a district’s implementation of the CEO. Under the CEO, districts may conduct direct certification on a yearly basis. If the most current data show an increase in the percentage of enrolled students who are identified, the district may use that percentage for determining the USDA reimbursement. If the data show a decrease, the district may continue to use the original percentage. (From a memorandum issued by the U.S. Department of Agriculture, Food and Nutrition Service, director of Child Nutrition Division, Cynthia Long, dated May 20, 2011.)

The factor is intended to estimate the additional number of eligible students who would have been certified through the traditional application process. The CEO reimbursement formula uses just two rates—free and full price—and is

where

- GCEOt is the federal government’s outlay in month t for CEO schools, in dollars;

- Rf is the reimbursement rate for free meals as defined above;

- Rp is the reimbursement rate for full-price meals as defined above;

- I/E is the ratio of the total number of identified students (I) to total enrollment (E) as of April 1 of the base year or a subsequent year;

- φ is a factor specified by the Secretary of Agriculture (currently 1.6), and the product

φ is restricted to being no greater than 100 percent; and E

φ is restricted to being no greater than 100 percent; and E - BRRCEO is the blended reimbursement rate for the CEO.

Under the CEO, the claiming rate for free meals is the ratio of identified students to enrolled students times the factor. The claiming rate for reduced-price meals is zero. The claiming rate for full-price meals is 1 minus the claiming rate for free meals.

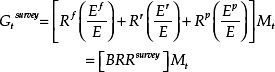

Using a socioeconomic survey (as in Philadelphia), a district combines the data from the survey with the number of directly certified students to estimate the percentage of enrolled students eligible for free, reduced-price, and full-price meals. The reimbursement formula is

where

- Gtsurvey is the federal government’s outlay established for the schools providing free meals to all students;

- Mt is the total number of reimbursable meals served in month t;

- Rf, Rr, and Rp are reimbursement rates as defined above;

- Ef is the number of enrolled students who have been directly certified or estimated as eligible for free meals based on a survey of students’ families;

- Er is the number of enrolled students who have been estimated as eligible for reduced-price meals based on a survey of students’ families;

- E is the total student enrollment;

- Ep = E - Ef - Er is the number of enrolled students who are eligible for full-price meals; and

- BRRsurvey is the blended reimbursement rate for the schools that provide free meals to all students and use data from the survey to determine reimbursements (roughly two-thirds of the schools in Philadelphia).

In this equation, the claiming percentages are the eligibility ratios Ef/E, Er/E, and Ep/E.

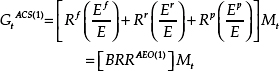

Under the AEO the panel considered two potential reimbursement equations. The first is modeled after the option that relies on a socioeconomic survey and uses claiming rates based on eligibility:

where

- GtACS(1) is the federal government’s outlay for reimbursable meals served in month t by AEO schools in dollars (the (1) denotes that this is the first version of the AEO proposed for using ACS data, and it uses eligibility estimates alone to define the claiming percentages);

- Rf, Rr, and Rp are reimbursement rates as defined above;

- Mt is the total number of reimbursable meals served in month t;

- Ef/E is the estimated fraction of enrolled students who are eligible for free meals based on the ACS and other sources;

- Er/E is the estimated fraction of enrolled students who are eligible for reduced-price meals based on the ACS and other sources;

- Ep/E = 1 - Ef/E - Er/E is the estimated fraction of enrolled students who are eligible for full-price meals based on the ACS and other sources; and

- BRRAEO(1) is the BRR under the assumption that claiming percentages are based on student eligibility fractions estimated using the ACS and other information.

The computations for BRRsurvey and BRRAEO(1) are the same, and these BRRs do not vary from month to month. However, these BRRs are based on different data. A local socioeconomic survey is used to estimate the eligibility-based claiming percentages in the former, and the ACS is used to estimate the eligibility-based claiming percentages in the latter.

In light of the differences between the distributions of students by eligibility category in Table 2-1 and the distributions of meals served by eligibility category in Table 2-3, a concern with the above “enrollment-based” reimbursement equation—that is, an equation based on the distribution of enrolled students—is that it might be unfair to districts. Specifically, as illustrated in an example presented by FNS at the panel’s first meeting,28 districts might receive smaller reimbursements than they would with a “participation-based” equation—that is, an equation based on the distribution of meals served. Therefore, the panel focused on a more general expression for the AEO reimbursement formula:29

![]()

where

- GtACS(2) is the federal government’s outlay for reimbursable meals served in month t in AEO schools in dollars, with the (2) indicating that this is the second version of the AEO considered by the panel, and it is based on estimated claiming percentages that account for both eligibility and participation;

- Rf, Rr, and Rp are reimbursement rates as defined above;

- Mt is the total number of reimbursable meals served in month t;

- Cf is the claiming rate for free meals, an estimate of the fraction of reimbursable meals served to students eligible for free meals;

____________

28 FNS gave a hypothetical example of a school with 70 percent of students eligible for free meals, 10 percent eligible for reduced-price meals, and 20 percent eligible for full-price meals. In this hypothetical school, however, 77.7 percent of meals were served to students eligible for free meals, 10 percent of meals to students eligible for reduced-price meals, and 12.3 percent of meals to students eligible for full-price meals. In this example, the average reimbursement per meal based on the eligibility distribution is $2.17, while the average reimbursement per meal based on the participation (meals served) distribution is $2.36. (In this situation, the school was eligible for the $.02 per meal increment, and the reimbursement rates for free, reduced-price, and full-price meals were $2.70, $2.30, and $.25, respectively.)

29 A special case of this formula uses the enrollment percentages from the previous formula to estimate the claiming percentages.

- Cr is the claiming rate for reduced-price meals, an estimate of the fraction of reimbursable meals served to students eligible for reduced-price meals;

- Cp = 1 - Cf - Cr is the claiming rate for full-price meals; and

- BRRAEO(2) is the BRR when claiming rates are based on both eligibility and participation.

As indicated by the formula, the BRR does not vary from month to month.

The claiming rate for a category is the estimated fraction of reimbursable meals that are served to students who are eligible for that category, although meals would be provided free to all students. The three claiming percentages are the MU distribution in Figure 2-1, and, as noted earlier, one objective of the panel was to determine whether there is a reliable and operationally feasible method for estimating this distribution.30

ERRORS IN METHODS FOR DETERMINING REIMBURSEMENTS

Both the traditional method and the special provisions and options have limitations that result in errors in determining reimbursements. The limitations associated with the traditional method are described in the following section. The limitations associated with the special provisions are described in the final section.

Traditional Method

Currently, the majority of school districts use what we call the “traditional” method of operating the school meals programs. As described earlier, at the beginning of the school year, the district initiates a process in which parents are asked to apply for free or reduced-price meals by supplying their income and the number of household members or the information required to establish categorical eligibility (e.g., a SNAP case number).31

In this process, parents of students who are not directly certified need to apply in order for their children to receive the benefits of free or reduced-price meals. If a family that is eligible for these benefits does not apply and is not identified by direct certification, the students have been denied access to free or reduced-price meals to which they are entitled.32

____________

30 As shown in Chapter 5, meals served claiming percentages can be expressed in terms of the product of eligibility percentages and participation rates.

31 An application does not need to be submitted if a student has been directly certified for free meals.

32 This is not counted as a certification error in official statistics, however.

Even if parents submit an application form for their children, they must complete it correctly. To do so, they must have an accurate understanding of the program definitions of income and membership in the household. When parents are asked to report the number of household members, for example, they need to know that the count does not include foster children living in their household33 but does include relatives such as aunts or grandparents who are part of a student’s economic unit. The parents need to know which forms of income should and should not be included and the correct dollar amounts for included forms. The application process further requires that parents apply these concepts accurately to their individual family situation.

Once an application has been submitted, school or district officials must review it and determine whether the students in the family are eligible for free or reduced-price meals (or must pay full price). Even if the application is completely accurate, errors can be made at this stage in the certification process. Although the required annual verification of a sample of applications may reduce errors in the completion and review of applications, substantial certification errors still remain, as discussed below.

Once a student has been approved for free or reduced-price meals or the application for such benefits is denied and the student must pay full price for a meal, the meal counting and claiming process begins. A school must retain daily records of the number of meals served for each eligibility status by linking a reimbursable meal served to a student and then linking that student to his or her certified eligibility status. The school’s daily records are compiled and submitted to the school district, and the school district submits them to the state. The state completes form FNS-10, providing the information that FNS uses to determine reimbursements. At each stage of this process, errors may occur.

The APEC study (U.S. Department of Agriculture/Food and Nutrition Service, 2007b), discussed earlier, found that the certification process is especially prone to error, with approximately 9 percent of total reimbursements for both the NSLP and SBP considered erroneous because of certification errors. The study reported on two sources of certification error: (1) household reporting errors and (2) administrative errors made by districts in processing applications. It established that 23.2 percent of all certified students and denied applicants had household reporting errors on their forms, while 8.3 percent were subject to administrative

____________

33 This statement was true when the panel began its work, but the policy has changed. According to U.S. Department of Agriculture/Food and Nutrition Service (2011b), foster children are now to be counted as part of the household.

error.34 (The two sources of error could occur on the same application and could have been offsetting.) Household reporting error led to over-certification for 13.5 percent of applications and undercertification for 9.7 percent of applications, while administrative error led to overcertifica-tion for 6.2 percent of applications and undercertification for 2.1 percent of applications.35 The most common type of household reporting error was misreporting of total income; this error affected 20 percent of certified students and denied applicants. Eight percent of certified students and denied applicants had errors in the number of household members listed on the form. The most common administrative error was certification of a student as eligible for free or reduced-price meals when the application was incomplete and should have been denied.

According to the APEC study (U.S. Department of Agriculture/ Food and Nutrition Service, 2007b:53, vol. 1), roughly 14 percent of those approved as eligible for free meals should have been approved for a status with fewer benefits (8 percent for reduced-price and 6 percent for full-price meals). At the other end of the distribution, 36 percent of students whose applications were denied, and thus were required to pay full price, should have been approved for free or reduced-price meals (19 and 17 percent, respectively). Given the limited income range over which a student qualifies for reduced-price meals, approvals for that category are the most error prone. Roughly one-third of students approved for reduced-price meals should have been approved for free meals, and 25 percent should have had their applications denied.

To quantify the potential effect of certification errors on the distribution of students by eligibility status when the traditional method is used, the APEC study compared the distribution of students based on the categories for which they had been approved with the distribution based on their true eligibility status, using the sample of students who had undergone the certification process and either had been certified for free or reduced-price meals or had their applications denied.36 The distribution based on approval status was 78 percent free, 17 percent reduced price, and 5 percent full price (U.S. Department of Agriculture/Food and Nutrition Service, 2007b:51), while the distribution based on true eligibility status was 74 percent free, 14 percent reduced price, and 12 percent full price (U.S. Department of Agriculture/Food and Nutrition Service,

____________

34 Denied applicants—that is, applicants who are not approved for free or reduced-price meals—can still purchase meals at full price.

35 Overcertification occurs when a student is certified for more benefits than those to which she or he is entitled. For example, a student approved for free meals is overcertified if she or he should have been approved for reduced-price or full-price meals.

36 Because estimates were not obtained for students who did not apply, these distributions do not pertain to all enrolled students.

2007b:53). It was also estimated (U.S. Department of Agriculture/Food and Nutrition Service, 2007b:97) that the gross reimbursement error resulting from certification errors in the NSLP was 9.4 percent of total reimbursements (sum of absolute values of overpayments and underpayments divided by total cash and commodity reimbursement). Underpayment due to undercertification offset some of the overpayment due to overcertifica-tion, resulting in a net overpayment of 4.8 percent of total cash and commodity reimbursements.

The APEC study also evaluated noncertification errors, classified as cashier or aggregation37 errors. The study found that the process by which cashiers assess and record whether a meal is reimbursable is a substantial source of erroneous payments, particularly in the SBP, even though most schools had fairly low levels of cashier error. The high aggregate level of cashier error arose from a few large schools having very high levels of this type of noncertification error. However, it was conjectured that automated point-of-sale technology in place in most schools would minimize this type of error.

Provisions and Options

With the traditional method, the accuracy of reimbursements depends on four factors:

- the correct certification of students as eligible for free or reduced-price meals (certification error);

- the correct determination that a meal qualifies for reimbursement (cashier error);

- the correct classification of each student taking a meal by approval category (free, reduced price, or full price) (cashier error); and

- the summation of counts of meals served over cashiers and days, transmission of the school’s meal counts by category to the school district, the state, and the federal government for reimbursement (aggregation error).

For Provisions 2 and 3 and the AEO, these same factors would contribute to errors in the base year. The APEC study found that overcertifi-cation rates are higher and erroneous payments due to certification error

____________

37 Aggregation error is the sum of three potential errors: (1) the school does not sum meal counts correctly, (2) the school does not report to the district correctly, and (3) the district does not report to the state correctly. The error rate for the first type of error was very small, while the error rates for the second and third types were about 2 percent and 1.5 percent of NSLP reimbursements, respectively. The last two error types typically resulted in an overpayment to the school.

are more common in Provision 2 and 3 schools (in their base years) than in schools using the traditional method. Erroneous payments in the NSLP were approximately 1.75 percent larger for Provision 2 and 3 schools. With these provisions, any overstatement (or understatement) of claiming percentages for the base year will persist through subsequent years of their use until a new base year is established. The APEC study did not differentiate between schools in their first base year and subsequent base years, because the sample of Provision 2 or 3 schools was too small. In subsequent base years, there is likely to be more error because after 4 years of not taking applications, parents and school district staff have become less familiar with the application and verification procedures and less skilled in carrying them out. In light of the ongoing provision of free meals, some parents may not understand why applications need to be submitted, and may not submit applications at all or take the time to complete them accurately. School food service directors participating in the workshop hosted by the panel expressed concern about such problems arising when a new base year is established. Because the AEO has only one base year at the beginning of the process, the challenges associated with subsequent base years will not obtain.