2

LIFE-CYCLE COST AND ITS CONTROL5

A building or other constructed facility provides shelter and service to its owners and occupants over a period of years. As this period extends to decades, portions of a building may be altered, extensively repaired, or replaced. Sometimes social, technical, or economic changes render buildings effectively obsolete, and they are abandoned, demolished, or replaced entirely. Sometimes buildings achieve particular artistic, cultural, or historic distinction that leads to their preservation when they might otherwise be retired from service.

While the number of years that a building or its component parts will be used is uncertain, building owners and designers nevertheless think in terms of a distinct economic life when making decisions about what materials and equipment to use in a new building and how much to spend on construction and the other costs of ownership. Construction costs are only a small portion of the costs of ownership, and the building owner who recognizes that he or she will bear not only these initial expenses but also the future costs of the building's operation, maintenance, and use should have some interest in controlling all of these costs. Determining how to assess, compare, select, and then control these costs so that a building will provide adequate service throughout its life is the subject of life-cycle cost analysis.

|

5 |

Appendix C briefly discusses the major principles underlying life-cycle cost analysis. |

WHY CONSIDER LIFE-CYCLE COST?

Life-cycle cost analysis is an economic evaluation process developed to assist in defining and then deciding among alternative building investments or operating strategies. Alternatives are characterized by differing patterns of costs likely to be incurred throughout a given time period, and the analysis seeks to assess these different patterns in comparable terms. Often, a single number—the present value of life-cycle cost, for example—is used to indicate a preferred choice among alternatives.

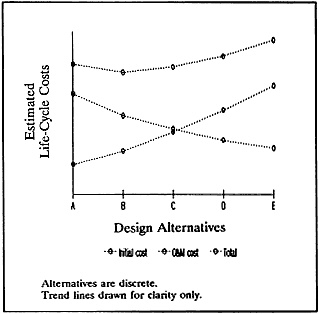

Alternatives are typically defined to illustrate in a systematic way some trade-off between first costs (e.g., for construction or equipment procurement) and future recurring costs (e.g., for maintenance or electric power consumption). The analysis is often undertaken with an expectation that an alternative can be found that will have the lowest life-cycle cost (see Figure 2-1).

Figure 2-1 Trade-offs to minimize life-cycle cost.

Finding the minimum life-cycle cost alternative generally requires good understanding of the technical factors underlying the tradeoff being considered, reasonable estimates of the various costs involved, and a certain degree of ingenuity and judgment. Designers must be familiar with how choices of materials, facility configurations, and other design variables influence initial cost and future operations and maintenance. The principles underlying life-cycle cost analysis imply that there is a continuum of alternatives, but in fact building-related options are generally quite distinct and discontinuous (e.g., only certain distinct actions and combinations are practical). The designer or manager must exercise some imagination to define a range of alternatives that illustrate realistically the trade-offs to be made and that indicate a minimum life-cycle cost.

Sometimes alternatives are simply variations of a particular design or operating strategy. Each change that yields a further reduction is in effect another alternative that is compared, in principle, to the initial design, the

''base case." The analysis stops when further significant reductions cannot be found.6 (See box next page.) Care is required to assure that performance is not compromised in the search.

This search for the minimum life-cycle cost—and the resulting efficiencies of resource utilization that a search implies—makes life-cycle cost analysis particularly appropriate for use by government agencies. These agencies build and use facilities to serve their missions, and the costs are paid with public funds. Even when one agency is responsible only for construction of a facility to be used by another agency, they all share a responsibility to use public funds as effectively as possible, now and in the future. The public should not care, in principle, whether funds are spent for construction, operations, or maintenance, today or tomorrow, so long as no more is spent than is necessary. In practice, as will be discussed in Chapters 3 and 4, the public, its elected officials, and its career civil servants may care a great deal about when and for what purposes funds are expended, and their concerns can be major obstacles to life-cycle cost control. The committee recommends that government agencies increase their use of life-cycle cost analysis as a means to overcome these obstacles.

IMPORTANT ASSUMPTIONS

The principles of life-cycle cost analysis include several assumptions that can have important consequences for design and management, particularly when the assumptions are implicit and may not be recognized by the user of the analysis results.7 Foremost among these assumptions is that all costs are measurable in monetary terms. The life-cycle cost estimate is only one of several factors that may be important to selecting among several designs or operating strategies, and the analysis is often restricted to financial costs alone—actual transfers of funds to purchase building-related goods and services.8

|

6 |

In practice, each variation may be compared only to its predecessor, in search of marginal improvements. If functional performance is explicitly considered, this process may be termed value engineering, but some value engineering studies (particularly those associated with construction contractor incentive clauses) address construction costs only. The term life-cycle value engineering is sometimes used to distinguish studies that do address life-cycle costs from those that focus on construction cost alone. |

|

7 |

Some of the computational assumptions made in analysis can significantly influence the results. These assumptions are discussed in Appendix C. |

|

8 |

Economists have developed sophisticated procedures for evaluating in monetary terms a wide range of benefits and costs, but these methods are not typically used for life-cycle cost analysis and were beyond the scope of the committee's deliberations. |

|

VA Analysis of Potential Life-Cycle Savings The Department of Veterans Affairs (VA), with more than 172 medical centers (some 2,000 buildings), owns and operates the nation's largest hospital system. The VA has developed a hospital building system designed to be economical while easing adoption of changing health care needs, simplifying bidding, and promoting fire and earthquake safety. The first demonstration of this building system was the VA hospital in Loma Linda, Calif., completed in 1973. A major force in the system's development was the effort to lower the VA's total long-term costs as owner of the facility. Detailed analyses were made of construction, operating, maintenance, and renovation costs anticipated over the 40-year economic service life typically assumed as the basis for the agency's planning and design decisions. This analysis highlighted seven major factors that could reduce the costs of ownership (the dollar estimates, based on prevailing conditions in the early 1970s, would probably higher today):

The present value of the resulting combined savings over a 40-year period, calculated using a 5 percent discount rate, was estimated to be approximately 10 percent of the life-cycle costs of ownership, with nearly three-quarters of the savings due to reductions in O&M costs. The total life-cycle costs were estimated to be approximately 8.7 times the initial costs in this calculation, so the relative saving would be less if a higher discount rate had been used. (Source: Feasibility Study—VA Hospital Building System, Research Study Report, Project No. 99-R003, prepared by the Joint Venture of Building Systems Development and Stone, Marraccini and Patterson for the Research Staff, Office of Construction, Veterans Administration, U.S. Government Printing Office, Washington, D.C., 1968) |

A second key assumption is that all alternatives considered in the analysis deliver the same performance throughout their service lives. This assumption is violated, for example, when decisions made to reduce life-cycle energy costs have resulted in indoor air quality problems. The committee noted that a growing body of evidence suggests that apparent reductions in life-cycle costs of air conditioning and lighting systems may be far exceeded by costs of lost productivity of the work force housed in a building when performance is not maintained (Woods, 1989; Brill, 1984). Analysts suggest that lost work time, insurance costs, lost revenue, and other financial consequences of poor building performance should be explicitly considered in the life-cycle cost analysis, but doing so has not become common practice. 9

"Interstitial space" in the VA hospital building system facilitate updating of mechanical system, extending the structure's potential service life. (Photo courtesy of Department of Veterans Affairs)

Finally, life-cycle cost analysis assumes there is an easy interchangeability of present and future costs, for example, spending more initially to purchase

durable materials or systems to achieve future savings in a building's maintenance costs, or choosing less costly and durable materials and systems that can be maintained at higher cost (i.e., by painting or lubrication) to yield the same service. The analysis may fail to deal explicitly with probabilities that a system or material may fail prematurely, that maintenance efforts may be ineffective, or other factors that represent uncertainties in cost estimates. These uncertainties increase as one tries to project further into the future. 10 Also, as will be discussed in Chapter 3, forces at work in the public sector may tend generally to invalidate this assumption.

LIFE-CYCLE COST MANAGEMENT

Life-cycle cost analysis is used to consider alternative future courses of action: designs for facilities yet to be built; strategies for future operations; maintenance, repair, and renewal programs. Selection of a preferred alternative implies that certain actions will be taken in the future. Effective life-cycle cost management can be achieved only if these actions are in fact taken, and failure to do so may raise the costs of ownership well above the levels anticipated in the analysis. Spending below targets set for normal maintenance, for example, may substantially increase costs of repair, replacements, and loss of use, costs that might have been avoided. (See box.) In general, inadequate operations and maintenance efforts will raise a facility's costs of ownership.

Hoping to delay normal wear and aging of a facility, managers may set future spending to exceed targets defined in the life-cycle cost analysis. However, unless the initial analysis is somehow faulty, savings resulting from extended life of building components or avoided damages are unlikely to balance fully the increases in maintenance spending. The total costs of ownership will again be raised above anticipated levels. In some cases higher life-cycle costs are warranted by the unique strategic, historical, or symbolic character of the facility. Buildings such as the U.S. Capitol, the White House, state capitol buildings, and city halls, as well as a wide variety of other landmarks, will be preserved and renovated regardless of the costs of dealing with difficult spaces and obsolete materials and operating subsystems. Costs of ownership may be

|

Costly Consequences of Neglect Subject to the dictates of Congress and the demands of their tenants, the General Services Administration (GSA) owns and manages more than 7,000 federal buildings. This inventory includes the Pentagon, still the world's largest office building, with some 6 million gross square feet of space and five decades of service. The mechanical equipment illustrates the broader problems that leave some members of Congress, quoted in the Washington Post, "appalled at the severe deterioration of the Pentagon Reservation": five coal-fired boilers linked to 1.5 miles of steam tunnels and a series of chillers drawing water from the Potomac River were installed when the Pentagon was constructed in the early 1940s. The GSA contracted in 1973 to replace the furnaces with oil-fired boilers, and the first unit was nearly completed when the oil embargo started. Replacements were canceled, and the coal-fired boilers continued to be used. For the following 15 years, shortages of funds, disputes over responsibility for maintenance, and inability to gain congressional or local government permission to proceed with plans hampered action to rehabilitate the system. In 1987 boilers were rented—at an annual cost of $1.2 million—to do the work of the equipment that is so decrepit, Pentagon officials told the Post, that it might fail or explode at any minute. The boilers are but one symptom of the Pentagon's broader deterioration that led one senator to term the building, according to the Post, "a wreck . . . about to fall in," The Defense Department's proposal to spend $1.1 billion on repairs and office upgrading encountered serious opposition in the Senate appropriations military construction subcommittee. While such comparisons have limited validity, the 1988 simple average construction cost of approximately $88 per square foot for new federal office buildings (excluding land expenses) suggests how high this price tag may be. GSA's lack of money and political strength within the administration, continuing turnover of senior management personnel (including 17 administrators since 1972, only six of whom won Senate confirmation), and weak management support systems are blamed by some observers. Others cite Congress's or the White House's indifference to property management and maintenance and the significance of GSA's role. Whatever the cause and cost, congressional conferees have come to recognize that "failure to maintain the Pentagon means that a massive renovation . . . is now needed to bring the Pentagon up to a satisfactory level." (Source. Judith Havemenn, ''Pentagon's Maintenance Woes: A Boiling Issue for GSA," Washington Post, and John Morawitz, "Analysis of Available Statistics on Comparative Construction Costs," Technical Report No. 94, Comparing the Construction Costs of Federal and Nonfederal Facilities (Summary of a Symposium), Federal Construction Council, National Academy Press, Washington, D.C., 1990). |

minimized within the context of preservation but may be higher than those for functionally comparable new construction.11

RELATIONSHIP OF PLANNING AND DESIGN CRITERIA AND LIFE-CYCLE COST

An owner or his or her agents in procuring new construction typically establishes a set of criteria that describe the characteristics the new building should have to deliver adequate performance over the course of its future lifetime. Many purchasers implicitly accept some criteria established by others, as is the case when private construction must meet the criteria stated in local building codes. 12 Architects and engineers effectively establish some of the criteria for their clients by following standard design practices or adopting specifications developed by manufacturers of materials and equipment. Some large corporations, government agencies, or other organizations that procure and manage large portfolios of buildings develop their own comprehensive statements of all of the criteria they expect designers to apply in a new building's design, but even in these cases many of the criteria are adopted from elsewhere. These criteria concentrate most on design and construction of the facility and often do not address operations and maintenance (O&M).

Regardless of their source, these criteria influence a new building's cost in complex and sometimes unforeseen ways. The number and complexity of interactions of these many criteria13 preclude generalized analysis, and it is in designing a specific building that the architect or engineer may find that local conditions, building program, and design criteria combine to require or preclude particular materials, equipment, or design details. Nevertheless, there is sufficient regularity in the relationship of criteria, designs, and costs that professionals can try to establish their general criteria such that the final design of each specific building possesses the characteristics desired.

Recognizing that certain materials or equipment cost more initially but offer O&M savings and lower life-cycle cost than other choices, owners may establish design criteria that require these materials or equipment to be used. For private sector owners and designers, these criteria may be as simple and straightforward as the specification of a particular brand-name product. However, in the interest of encouraging free competition, federal government agencies must typically avoid such direct statements and instead develop

generic criteria describing the performance required of building components. Agency professionals thus are challenged with developing generic criteria that will minimize life-cycle cost and remaining robust in the face of efforts to reduce the costs of building construction.

References

Brill, M., 1984, Using Office Design to Increase Productivity, :Work Place Design and Productivity, Inc., Buffalo, N.Y., pp. 337–352.

Glazer, A., 1989, "Politics and the choice of durability," The American Economic Review, December, pp. 1207–1213.

Woods, J. E., 1989, "Cost avoidance and productivity in owning and operating buildings," Occupational Medicine: State of the Art Reviews, vol. 4, no. 4, pp. 753–769.