Capital Formation and Economic Growth

Michael J. Boskin and Lawrence J. Lau

Enhanced capital, labor, and technical progress are the three principal sources of the economic growth of nations. Since the rate of growth of labor is constrained by the rate of growth of population, it is seldom, especially for industrialized countries, higher than two percent per annum, even with international migration. Consequently, the rate of growth of capital (physical and human) and technical progress have been found to account for a significant proportion of economic growth by a long line of distinguished economists: Abramovitz (1956), Denison (1962a,b; 1967), Griliches and Jorgenson,1 Kendrick (1961, 1973), Kuznets (1965, 1966, 1971, 1973) and Solow (1957), to name only a few. For example, Jorgenson, Gollop, and Fraumeni (1987, p. 21) found that between 1948 and 1979, capital formation accounted for 46 percent of the economic growth of the United States, labor growth accounted for 31 percent, and technical progress accounted for 24 percent.

Most studies of the sources of economic growth, or growth accounting, are based on the concept of an aggregate production function:

(1)

where Yt'Kt' and Lt are the quantities of real aggregate output, capital and labor respectively at time t and t is an index of chronological time.2 The purpose of growth accounting is to determine from the empirical data how much of the change in real output between say t = 0 and t = 1 can be attributed to changes in the inputs, capital and labor, and technology, respectively. Taking natural logarithms of both sides

of equation (1) and differentiating it totally with respect to t, we obtain:

(2)

where ![]() and

and ![]() are the instantaneous proportional rates of change of the quantities of real output, capital and labor respectively at time t;

are the instantaneous proportional rates of change of the quantities of real output, capital and labor respectively at time t; ![]() and

and ![]() are the elasticities of real output with respect to capital and labor respectively at time t and

are the elasticities of real output with respect to capital and labor respectively at time t and ![]() is the instantaneous rate of technical progress, or equivalently, the rate of growth of output holding the inputs constant.

is the instantaneous rate of technical progress, or equivalently, the rate of growth of output holding the inputs constant.

The first term on the right-hand side of equation (2) thus represents the contribution of the growth of capital to the growth of real output. Note that the contribution of capital depends on both the production elasticity of capital and the rate of growth of capital. If the rate of growth of capital is low, then the contribution of capital will be low even with a high production elasticity of capital. Similarly, the second term represents the contribution of the growth of labor and the third term represents the contribution of technical progress. Together, the three terms add up to the rate of growth of real aggregate output.

However, not every variable on the right-hand side of equation (2) can be directly observed. Only the rates of growth of real aggregate output, capital and labor can be observed. The elasticities of output with respect to capital and labor must be separately estimated, often requiring additional assumptions. Moreover, note that the instantaneous rate of technical progress, ![]() depends on Kt and Lt as well as t. To the extent that Kt and Lt change over time, the rate of technical progress over many periods cannot be simply cumulated from one period to the next, unless technical progress is neutral, in which case the instantaneous rate of technical progress,

depends on Kt and Lt as well as t. To the extent that Kt and Lt change over time, the rate of technical progress over many periods cannot be simply cumulated from one period to the next, unless technical progress is neutral, in which case the instantaneous rate of technical progress, ![]() is independent of capital and labor.

is independent of capital and labor.

Thus, in general, in order to use equation (2) to measure technical progress over time, three basic hypotheses are maintained: constant returns to scale, neutrality of technical progress, and profit maximization with competitive output and factor markets.3 Profit maximization with competitive markets allows the identification of the elasticities of output with respect to labor with the share of labor cost in total output. Constant returns to scale in production implies that the sum of the elasticities of output with respect to capital and labor is exactly unity, so that the elasticity of capital can be readily estimated as one minus the elasticity of labor when the latter is known. Neutrality of technical progress justifies the cumulation of successive estimates of technical progress over time.

In a recent study, we attempt to identify and estimate the degree and bias of scale economies, the rate and bias of technical progress, and the elasticities of output with respect to capital and labor for five industrialized countries—France, West Germany, Japan, the United Kingdom and the United States—without making any restrictive assumptions about the nature of the technology, the behavior of the firms, or the competitiveness of the markets (Boskin and Lau, 1990). We were able to do so by pooling the time-series data of five industrialized countries4 and making the assumptions that (1) all countries have access to the same technology, that is, they have the same underlying production function, sometimes referred to as a meta-production function; 5 (2) there are differences in the technical efficiencies of production and in the qualities and definitions of measured inputs across countries; and (3) the inputs of the different countries may be converted into "efficiency"-equivalent, or standardized, units of inputs by multiplicative country-and input-specific time-varying augmentation factors.

For example,

where ![]() and

and ![]() are the "efficiency"-equivalent quantities of capital and labor respectively of the ith country at time t; AiK(t) and AiL (t) are the capital-and labor-augmentation factors respectively for the ith country; and Kit and Lit are the measured quantities of capital and labor of the ith country at time t. The meta-or common production function is valid for all countries in terms of "efficiency"-equivalent quantities of outputs and inputs.6

are the "efficiency"-equivalent quantities of capital and labor respectively of the ith country at time t; AiK(t) and AiL (t) are the capital-and labor-augmentation factors respectively for the ith country; and Kit and Lit are the measured quantities of capital and labor of the ith country at time t. The meta-or common production function is valid for all countries in terms of "efficiency"-equivalent quantities of outputs and inputs.6

These assumptions require some explanation. Essentially it is assumed that the aggregate production function is the same everywhere in terms of "efficiency"-equivalent or standardized units of inputs. For example, one unit of capital in country A may be equivalent to two

units of capital in country B; and one unit of labor in country A may be equivalent to one-third of a unit of labor in country B. In terms of the measured quantities of inputs, the production functions of the two countries are not likely to be the same. However, in terms of "efficiency"-equivalent or standardized units, the assumption of a common production function across countries is far more plausible.

The question inevitably arises: How can one estimate these augmentation or conversion factors? How can one standardize the measured inputs? It turns out that these augmentation factors can in fact be estimated simultaneously with the parameters of the aggregate production function from data on the quantities of measured outputs and inputs, subject to a normalization. Thus, it is actually possible to answer the question of how many units of labor in country B is equivalent-to 1 unit of labor in country A at some given time t empirically.

Using this approach, we are able to estimate the rates and patterns of scale economies and technical progress, as well as the relative contributions of the inputs to economic growth, without making the three conventional assumptions, mentioned above, maintained in growth accounting.

TESTING OF HYPOTHESES

An aggregate production function of the transcendental logarithmic form with exponential augmentation factors is specified and estimated using the instrumental variables method.8 For each country and input, the augmentation factor is assumed to take the form ![]() where

where ![]() is the (unobserved) "efficiency"-equivalent quantity of the jth input in the ith country at time t, Aij is the augmentation level parameter, cij is the augmentation rate parameter, and Xijt is the measured quantity of the jth input in the ith country at time t.

is the (unobserved) "efficiency"-equivalent quantity of the jth input in the ith country at time t, Aij is the augmentation level parameter, cij is the augmentation rate parameter, and Xijt is the measured quantity of the jth input in the ith country at time t.

A series of hypotheses are tested. The first hypothesis that is tested is that of identical production functions across countries in terms of "efficiency"-equivalent units of inputs. Is the assumption that all of the countries in the sample operate on the same production function a valid one? This hypothesis cannot be rejected at any reasonable level of significance. The second hypothesis that is tested is whether technical progress can be represented in the output and input-augmentation form with exponential augmentation factors. Once again, the hypothesis cannot be rejected. We conclude that our maintained hypothesis of a meta-production function of the commodity-augmenting translog form with exponential commodity-augmentation factors cannot be rejected.

Next, we test the maintained hypotheses of conventional growth

accounting: constant returns to scale, neutrality of technical progress and profit maximization. All three hypotheses, as well as the hypothesis of homogeneity of the production function, which is implied by constant returns to scale, can be rejected at the 1 percent level of significance.

Having established the validity of our approach and the lack of validity of the conventional assumptions, we proceed to examine the structure of the technology. We test and cannot reject the hypothesis that the augmentation level parameters for capital and labor are the same across all countries. In other words, in the base period (1970), the "efficiency" levels of capital and labor were not significantly different across countries. We test and cannot reject the hypothesis that technical progress can be adequately represented by two augmentation rate parameters rather than three (output, capital and labor) for each country. We also test and cannot reject the hypothesis that technical progress can be adequately represented by a single augmentation rate parameter for each country. The one single augmentation rate turns out to be that of capital.

We therefore conclude that technical progress can be represented as capital-augmenting, which means, in particular, that technical progress is biased. Capital-augmenting technical progress implies that capital and technical progress are complementary: the benefits of technical progress are greater the larger the capital stock, other things being equal.

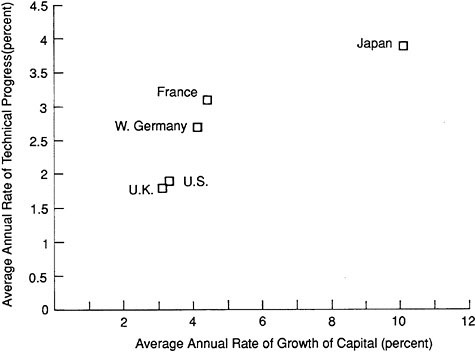

We also find that the estimated labor elasticities are generally comparable in magnitude to the actual shares of labor cost in total output (even though the hypothesis of profit maximization with respect to labor is actually rejected). However, the estimated capital elasticities are much lower in magnitude than were customarily found or assumed. (Recall that the hypothesis of constant returns to scale is not maintained in our approach.) The low capital elasticities result in estimates of significant decreasing returns to scale in capital and labor within the observed range of the inputs. (Bear in mind that the translog production function is not necessarily homogeneous and therefore does not exhibit fixed returns to scale.) Finally, the implied average annual rates of technical progress, that is, the rate of growth of output holding inputs constant, rank the different countries in the order of Japan (3.9 percent), France (3.1 percent), West Germany (2.7 percent), the United States (1.9 percent), and the United Kingdom (1.8 percent). It is interesting to note that these rates bear a direct relationship to the rates of growth of the capital stock of these countries over the sample period, illustrating the capital-technology complementarity implied by capital-augmenting technical progress (see Figure 1).

FIGURE 1 Relation between technical progress and growth of capital stock.

ACCOUNTING FOR GROWTH

What do these results imply about the relative contributions of the three sources of economic growth: capital, labor, and technical progress? They indicate that technical progress is by far the most important direct source of economic growth for the industrialized countries in our sample, accounting for more than 50 percent of the growth in real aggregate output (more than 80 percent for the European countries), followed by capital (with the exception of the United States), with labor a distant third. Moreover, capital and technical progress combined account directly for more than 95 percent of the economic growth of the industrialized countries except the United States. In the United States, where labor grew much more rapidly than in the other countries during this period, capital formation and technical progress still account directly for approximately 75 percent of economic growth.

Our results may be contrasted with those of growth accounting exercises using more conventional methods. The conventional approach which assumes constant returns to scale, attributes a much higher proportion of economic growth to capital and a correspond-

ingly lower proportion to technical progress. However, it would be wrong to interpret our finding to mean that capital is not an important source of economic growth. The effect of technical progress is found to depend directly on the size of the capital stock. It is interesting to note that the combined effects of capital and technical progress are virtually the same under both approaches as are the effects due to the growth of labor.

Our identification of technical progress as the most important source of economic growth is reminiscent of the findings of a large unexplained "residual" in early studies of economic growth. Such superficial similarities may, however, be misleading. Our finding is distinct from the earlier ones on at least two counts. First, we do not assume constant returns to scale, neutrality of technical progress and profit maximization with competitive markets. Second, we find empirically, and we believe for the first time, capital and technical progress to be complementary, so that the effect of technical progress on real output depends on the size of the capital stock. The implications of this capital-augmenting type of technical progress are quite different from those of the conventionally assumed neutral variety, the effect of which does not depend on the size of the capital stock.

CONCLUDING REMARKS

We have discussed briefly our method for analyzing important characteristics of the nature of economic growth, such as the rates and pattern of technical progress and scale economies, simultaneously, using pooled time-series data from several industrialized countries. We have found that the empirical data are inconsistent with the hypothesis of constant returns to scale at the aggregate national level. In fact, we have found significant decreasing returns to scale. Moreover, we have found that technical progress is far from neutral. In fact, it is capital-augmenting. In addition, we have also found that the empirical data are inconsistent with the assumption of profit maximization with respect to labor under competitive conditions.

What are the implications of capital-augmenting technical progress? 9 At the aggregate level, one implication of capital-augmenting technical progress is the importance of capital to long-term economic growth. The benefits of technical progress to the economy are directly proportional to the size of the capital stock. A country with a low level of capital stock relative to labor will not benefit as much from technical progress as a country with a high level of capital stock relative to labor. Capital and technical progress are, in a word, complementary. A second implication is that technical progress is more likely to be

capital-saving, in the sense that the desired capital-labor ratio for given prices of capital and labor and the quantity of output declines with technical progress, rather than labor-saving. Capital-augmenting technical is thus less likely to cause long-run structural unemployment through the displacement of workers.

We have treated technical progress as exogenous in this study, in the sense that the rates of factor augmentation are assumed to be determined exogenously. The actual technical progress realized, in the sense of the rate of growth of real output, holding inputs constant, is in fact endogenous, as it depends on capital and labor in addition to time. It is, however, remarkable that the rate of augmentation of capital turns out to be almost identical for France, West Germany, and Japan, indicating that the three countries have nearly the same access to advances in technology. It would be of interest to investigate the determinants of the differences in the rates of capital augmentation across countries. Can they be explained by education, R&D expenditures, rate of capital accumulation, or other factors?

The preliminary results presented here are interesting, but much additional work remains. Promising potential areas include accounting for omitted factors such as land (Lau and Yotopoulos, 1989), human capital, public capital (Boskin et al., 1989), R&D and environmental capital (which may explain the significantly decreasing returns to scale to capital and labor observed in the sample); possible vintage effects; and embodiment of technical progress.

ACKNOWLEDGMENT

This brief review reports on some of the results of a major study of postwar economic growth in the five largest industrial economies, conducted at Stanford University in 1987 and 1988. The full, completed study is Boskin and Lau (1990). The authors wish to thank the Ford Foundation, the John M. Olin Foundation, the Pine Tree Charitable Trust, and the Technology and Economic Growth Program of the Center for Economic Policy Research, Stanford University, for financial support. They are grateful to Paul David, Bert Hickman, Lawrence Klein, and Ralph Landau for helpful discussions. The views expressed herein are the authors' and do not necessarily reflect those of the institutions with which they are affiliated.

NOTES

REFERENCES

Abramovitz, M. 1956. Resource and output trends in the United States since 1870. American Economic Review 46:5-23.

Boskin, M. J. 1988. Tax policy and economic growth: Lessons from the 1980s. Journal of Economic Perspectives 2:71-97.

Boskin, M. J., and L. J. Lau. 1990. Post-War Economic Growth in the Group-of-Five Countries: A New Analysis. Working Paper. Department of Economics, Stanford University.

Boskin, M. J., M. S. Robinson, and A. M. Huber. 1989. Government saving, capital formation and wealth in the United States, 1947-1985. Pp. 287-356 in R. E. Lipsey and H. S. Tice, The Measurement of Saving, Investment, and Wealth. Chicago: University of Chicago Press.

Christensen, L. R., D. W. Jorgenson, and L. J. Lau. 1973. Transcendental logarithmic production frontiers. Review of Economics and Statistics 55:28-45.

Denison, E. F. 1962a. The sources of economic growth in the United States and the alternatives before us. New York: Committee on Economic Development. Supplementary Paper No. 13. 297 pages.

Denison, E. F. 1962b. United States economic growth. Journal of Business 35:109-121.

Denison, E. F. 1967. Why Growth Rates Differ: Post-War Experience in Nine Western Countries. Washington, D.C.: Brookings Institution.

Gallant, A. R., and D. W. Jorgenson. 1979. Statistical inference for a system of simultaneous, nonlinear, implicit equations in the context of instrumental variables estimation. Journal of Econometrics 113:272-302.

Griliches, Z., and D. W. Jorgenson. 1966. Sources of measured productivity change: Capital input. American Economic Review 56:50-61.

Hayami, Y., and V. W. Ruttan. 1970. Agricultural productivity differences among countries. American Economic Review 60:895-911.

Hayami, Y., and V. W. Ruttan. 1985. Agricultural Development: An International Perspective, revised and expanded ed. Baltimore, Md.: Johns Hopkins University Press.

Jorgenson, D. W., and Z. Griliches. 1967. The explanation of productivity change. Review of Economic Studies 34:249-283.

Jorgenson, D. W., F. M. Gollop, and B. M. Fraumeni. 1987. Productivity and U.S. Economic Growth. Cambridge, Mass.: Harvard University Press.

Kendrick, J. W. 1961. Productivity Trends in the United States. Princeton, N.J.: Princeton University Press.

Kendrick, J. W. 1973. Postwar Productivity Trends in the United States, 1948-1969. New York: Columbia University Press.

Kuznets, S. S. 1965. Economic Growth and Structure. New York: Norton.

Kuznets, S. S. 1966. Modern Economic Growth: Rate, Structure and Spread. New Haven, Conn.: Yale University Press.

Kuznets, S. S. 1971. Economic Growth of Nations. Cambridge, Mass.: Harvard University Press.

Kuznets, S. S. 1973. Population, Capital and Growth. New York: Norton.

Lau, L. J., and P. A. Yotopoulos. 1989. The meta-production function approach to technological change in world agriculture. Journal of Development Economics 31:241-269.

Lau, L. J., and P. A. Yotopoulos. 1990. Intercountry differences in agricultural productivity: An application of the meta-production function. Department of Economics, Stanford University. Photocopy.

Lindbeck, A. 1983. The recent slowdown of productivity growth. Economic Journal 93:13-34.

Solow, R. M. 1956. A contribution to the theory of economic growth. Quarterly Journal of Economics 70:65-94.

Solow, R. M. 1957. Technical change and the aggregate production function. Review of Economics and Statistics 39:312-320.

|

|

MICHAEL J. BOSKIN, an economist and educator, is currently chairman, President's Council of Economic Advisers. He is on leave from Stanford University, where he is the Wohlford Professor of Economics, chairman of the Center for Economic Policy at Stanford University, and research associate, National Bureau of Economic Research. He is the author of 2 books and approximately 50 articles and editor of 6 volumes of essays on taxation, fiscal policy, capital formation, labor markets, social security, and related subjects. The recipient of numerous honors and awards, Dr. Boskin received his B.A., M.A., and Ph.D. degrees from the University of California, Berkeley. |

|

|

LAWRENCE J. LAU is professor of economics at Stanford University. Since joining the Stanford faculty in 1966, he has been a visiting assistant research economist at the University of California, Berkeley, and a visiting professor of economics at Harvard University. He graduated from Stanford University in 1964 with a Bachelor of Science degree with Great Distinction in physics and economics. He later received both master's and doctorate degrees in economics at the University of California, Berkeley. He is the author of several books and approximately 100 articles in economics. |