History of Public Policy on lighting

The development of lighting technology, like all technologies, is influenced by the public policy framework in which the relevant innovation and commercialization occurs. This policy framework includes legislation and regulation at the federal, state, and local levels, as well as the equivalent laws in other industrialized countries. Yet, the pertinent policy framework involves more than just laws and also includes governmental research, development, and demonstration (RD&D) funding, consensus and industry standards, voluntary programs, incentive programs, building codes, and industry programs and initiatives, all operating within the context provided by market forces and consumer expectations. All of these factors play a role in the development of solid-state lighting (SSL) and are discussed below.

This chapter begins with a history of federal government policy on lighting, then covers federal legislation addressing lighting efficiency and the Department of Energy (DOE) lighting RD&D program. It then describes current federal and state programs, including federal regulations, federal voluntary programs, and state laws and regulations. Non-regulatory policy instruments affecting lighting efficiency are discussed next, including building codes, state building codes specifications for high-performance building specifications, incentive programs, and testing and measurement consensus standards. The chapter concludes with a brief summary of international regulation of lighting efficiency, followed by a case study on compact fluorescent lamps (CFLs).

History of Federal Government lighting Policy

Since the early 1970s the federal government has been involved in RD&D and policy related to more energy-efficient lighting. Four months prior to the oil embargo of 1973, President Nixon announced the formation of an Office of Energy Conservation within the Department of the Interior. One of its functions was to coordinate a 7 percent reduction of federal energy consumption (Savitz, 1986). When the oil embargo was imposed, President Nixon ordered government buildings (and requested the private sector) to reduce lighting levels to 50 footcandles (ftc) (approximately 500 lux) for office work; 30 fc (approximately 300 lux) for general lighting/hallways; and 10 ftc (approximately 100 lux) for parking lots—i.e., “50-30-10.”

Following the embargo, RD&D energy efficiency programs were initiated at DOE’s predecessor agencies: the Federal Energy Administration (FEA) and the Energy Research and Development Administration (ERDA). Most of the programs in the buildings sector were applied product research to develop more energy-efficient heating, cooling, and lighting systems. These programs were done in collaboration with industry and some of the national laboratories, predominantly the Lawrence Berkeley National Laboratory (LBNL) and Oak Ridge National Laboratory (ORNL).

When DOE was formed in 1977, the lighting program covered a wide range of energy-saving opportunities. The overall strategy consisted of three major thrusts: (1) light sources, (2) lighting applications (lighting design, fixtures and controls), and (3) lighting impacts. By 1999, light sources comprised more than half of the lighting program funding, which was $2 million to $4 million per year (NRC, 2001).

In the 1970s and 1980s, the program mainly consisted of contracts to industry, research and development (R&D) companies, and in-house research at LBNL. In spite of the relatively small amount of funding in the 1970s and 1980s, there were major successes from the DOE programs in conjunction with industry and LBNL. Two of these examples—electronic ballasts and CFLs—were case studies in a retrospective study by the National Research Council (NRC, 2001). The market share for electronic ballast increased from about 1 percent in the late 1980s to 47 percent by 2000 and 73 percent by 2005 (NRC, 2010). DOE promulgated minimum efficiency standards in 2000, effective in 2005. The National Research Council (NRC) retrospective study documented at least

$15 billion in net economic benefits for electronic ballasts as of 2000 (NRC, 2001).

The other case study was CFLs. DOE did not have a program targeted for CFLs until 1997, at which point it decided to sponsor R&D on the technology to reduce the cost and size of CFLs and accelerate their deployment. In fiscal year (FY) 1999, Congress provided funds specifically for new R&D projects, which were to be competitive solicitations that were cost-shared with industry. From FY1999 to FY2001 DOE spent $1.8 million on R&D efforts; industry cost-shared $755,000 (NRC, 2001), or roughly 40 percent. Sales increased from about 21 million units in 2000 to almost 400 million units by 2007 (NRC, 2010).

It is generally acknowledged that it is methodologically difficult to estimate the impact of energy efficiency policies on demand reductions. Changes in weather, energy prices, cultural factors, and so on, all contribute to changes in energy consumption, and disentangling those effects from the impact of policies is difficult—but also critical to support the design of effective policies.

Several studies have shown the impact of specific policies on energy consumption reductions. For example, Gillingham et al. (2004) recently reviewed literature on the cost-effectiveness and impacts of a broad range of energy efficiency policies. The authors reviewed several studies that estimated the impact of appliance standards, financial incentives, information and voluntary programs, and government energy use. They concluded that “these programs are likely to have collectively saved up to 4 quadrillion Btu1 of energy annually, with appliance standards and utility demand-side management likely making up at least half these savings” (abstract, p. i). In their analysis, the authors did not include building and professional codes, and thus these overall savings are likely to be underestimates. The authors also stated that “Energy Star,2 Climate Challenge, and 1605b voluntary emissions reductions may also contribute significantly to aggregate energy savings, but how much of these savings would have occurred absent these programs is less clear” (abstract, p. i). Another study, focusing on energy efficiency policies in California, citing reductions in per-capita emissions that could not be attributed to other sources finds that, for 2001, totaled “up to about 23 percent of the overall difference between California and the United States could be due to policy measures, the remainder being explained by various structural factors” (Sudarshan and Sweeney, 2008, p. 1). These values were 545 kilowatt-hour (kWh) per capita in the residential sector and 416 kWh and 272 kWh in the commercial and industrial sectors, respectively.

The verification of the impacts of demand-side policies is always complex, given the need to establish a counterfactual of what would have occurred without the policies. However, there is a large amount of literature on the impact of utility demand side management (DSM) and energy efficiency programs, using sophisticated econometric models. A study in 1996 from Parfomak and Lave (1996) suggested that “utilities have a clear economic incentive to overstate the impacts” of these programs. However, when empirically assessing the impact of DSM and energy efficiency programs for several utilities in the northeast and California, the authors found that the reductions claimed by the utilities and the system-level sales after accounting for economic and weather effects they estimated were in agreement.

FINDING: While it is difficult to discern the contribution of public policies on the adoption of energy efficient products, it is likely that a sizable fraction of the decrease in per capita energy consumption may be attributable to such policies, judging from a study of changes in energy consumption in California. However, the actual impact of any specific policy instrument is difficult to disentangle as is the impact on any one type of household energy use.

FINDING: Improvements in energy efficiency of lighting products have been brought about by a combination of legislation, regulation, RD&D funding, consensus standards, industry programs and initiatives, incentive programs, and market forces.

RECOMMENDATION 2-1: The Department of Energy should develop a study to quantify the relative impact of different policy interventions on the benefits of adopting efficient lighting.

Over the past quarter century, a series of federal energy statutes have mandated energy efficiency standards and labeling for lighting. These congressional enactments have been contemporaneous with a steady increase in the energy efficiency of lighting technology over this time period.

Congress has given DOE the authority to regulate the energy efficiency of some high-volume lighting products at the federal level. In 1975 the Energy Policy and Conservation Act (EPCA 75), Public Law 94-163, established a program on “energy conservation for consumer products other than automobiles” (Title III), which included major household appliances, but did not include lighting. In 1987, the National Appliance Energy Conservation Act (NAEPA 87), Public Law 100-12, included minimum efficiency standards for fluorescent lamp ballasts and incandescent reflector lamps. In 1992, the Energy Policy Act (EPACT 92), Public Law 102-486, tightened the minimum energy efficiency standards for fluorescent lamps and incandescent reflector lamps. Furthermore, DOE was granted the authority to revise and amend these standards as well as to adopt a standard for additional

________________

1 Btu stands for British thermal unit and is a measure of energy. Burning 1 gallon of gasoline would release approximately 124,000 Btu.

2 ENERGY STAR® is a voluntary program created by DOE and Environmental Protection Agency to encourage energy efficient products and buildings through labeling.

general service fluorescent lamps. In addition, EPACT (92) added standards for some types of fluorescent and incandescent reflector lamps, provided funding for voluntary testing and consumer information programs for luminaries, and created an energy efficient commercial building tax deduction program, which includes lighting. The 1992 statute also set July 1994 as the deadline for states to adopt the lighting standards developed by the American Society of Heating, Refrigerating and Air-Conditioning Engineers (ASHRAE, 90.1 standards).

The Energy Policy Act of 2005 (EPACT 05), Public Law, 109-58, included performance standards for additional lighting products (e.g., energy saving fluorescent lamp ballasts) that had not been included in any of the previous legislation. It also provided for the establishment of labeling requirements for these products and preempted state standards for the same products. EPACT (05) also officially recognized and made more transparent the ENERGY STAR® program. Finally EPACT (05) expanded the tax deduction program for commercial building energy efficiency, originally enacted in EPACT (92).

The Energy Independence and Security Act of 2007 (EISA 2007) further amended EPCA (75) to include new provisions for lighting standards. EISA 2007 includes performance-based minimum efficiency standards for general service lamps, which will become progressively more stringent over time. General service lamps are classified as screw-based incandescent and fluorescent lamps and tubes; some specialty lamps were excluded from the standard. EISA also includes minimum efficiency standards for ballasts and lighting requirements for public buildings. Title III, Subtitle B, establishes definitions, standards, and amendments for lighting efficiency, and Section 321 defines energy efficiency standards for general service lamps. Table 2.1 shows the performance standards for lamps set by EISA 2007. The standard sets a maximum number of watts that a specified lamp (e.g., the so-called “A19 shape”) can use whose luminous output falls within a specified range. General service lamps outside this range are exempt from maximum rated wattage limits.

EISA 2007 also sets up standards for federal government buildings that will provide additional incentives for energy efficient lighting. The statute directs that total energy use in federal buildings be reduced 30 percent from a 2005 baseline by 2015. Moreover, the statute directs that every federal facility be subject to a comprehensive energy and water evaluation at least once every 4 years. Finally, new federal buildings and major renovations are required to reduce their energy use, relative to a 2003 baseline, by 55 percent in 2010 and by 100 percent (i.e., zero net energy3) by 2030. There were a number of attempts in the 112th Congress to roll back the requirements from EISA 2007 for lamps shown in Table 2.1, which culminated in a FY2012 appropriations rider prohibiting DOE from spending funds to enforce the standards stated in EISA 2007 for 2012. However, manufacturers plan to implement the 2012 standards nevertheless (Howell, 2011).

TABLE 2.1 Rated Lumen Ranges, Maximum Rated Wattages, and Effective Dates for General Service Lamps Goals in EISA 2007, Section 321

| Maximum Rated Wattage | Rated Lumen Ranges | Effective Date |

| 72 | 1490-2600 | January 1, 2012 |

| 53 | 1050-1489 | January 1, 2013 |

| 43 | 750-1049 | January 1, 2014 |

| 29 | 310-749 | January 1, 2014 |

NOTE: Minimum rated lifetime will be 1,000 hours in all cases.

The SSL Multi-Year Program Plan (DOE, 2011a) notes several efforts within DOE on advancing SSL technology, products, and the underlying science. These efforts occur within the Basic Energy Sciences (BES) program; the Advanced Research Projects Agency-Energy (ARPA-E); and the Building Technologies Program (BTP), which is within the Office of Energy Efficiency and Renewable Energy (EERE). The BES program supports fundamental research to provide the foundations for new energy technologies. Such work at the electronic, atomic, and molecular levels in solidstate physics can lead to multiple applications, including for SSL technologies. One example is the support for the Solid-State Lighting Science Energy Frontier Research Center at Sandia National Laboratories. ARPA-E funds projects that are considered high risk but can potentially lead to high-payoff energy saving results if successful. Some projects funded by ARPA-E are directly related to SSL, such as the development of low-cost, bulk gallium nitride substrates and the development of advanced, energy efficient power supply technologies (DOE, 2011a).

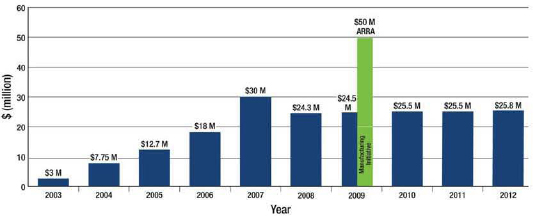

The vast majority of the work on SSL technology at DOE takes place within EERE’s BTP. The BTP oversees the Emerging Technologies subprogram, which focuses on developing cost-effective advanced technologies in such areas as lighting, windows, and space heating and cooling for residential and commercial buildings (DOE, 2010; 2011b). Research across these different areas supports the residential and commercial building goal of reducing total energy use in buildings by up to 70 percent. One budget line under Emerging Technologies is Solid-State Lighting. The funding in recent years for this activity has been about $25 million per year, as delineated in Figure 2.1, of which roughly $9 million was directed toward R&D in FY2011. Most recently, the FY2012 appropriation is $25.83 million for lighting R&D, but specifies that $12 million of that total

________________

3 A “zero net energy” building utilizes no net energy from the electrical grid through a combination of reducing overall use of energy (e.g., highly efficient lighting and HVAC technologies) and on-site production of renewable energy (e.g., wind or solar).

FIGURE 2.1 Budget authority for the Department of Energy’s lighting research and development within the Building Technologies Program (millions of dollars). SOURCE: Based on DOE (2010, 2011b) and Brodrick (2012).

must be used for R&D into manufacturing improvements for general illumination SSL. These yearly appropriations received a one-time boost with the American Recovery and Reinvestment Act (ARRA), which in 2009 resulted in about $50 million in additional funding being injected into SSL R&D activities, much of which went to jumpstart the Manufacturing Initiative.

The goal of the SSL R&D program is the following: “By 2025, develop advanced solid-state lighting technologies that, compared to conventional lighting technologies, are much more energy-efficient, longer lasting, and cost-competitive by targeting a product system efficiency of 50 percent with lighting that closely reproduces the visible portions of the sunlight spectrum” (DOE, 2011a, p. 9). Three primary interrelated thrusts are identified in the SSL multiyear program plan for which roadmaps have been developed: (1) core technology research and product development, (2) manufacturing R&D, and (3) commercialization support. The project areas outlined in the Multi-Year Program Plan cover a variety of topics split into core and product development for light-emitting diodes (LEDs) and organic LEDs (OLEDs) (DOE, 2011a).

The LED core technology focus areas are emitter materials research, down-converters (material systems designed to convert shortwavelength emitted radiation to longer wavelengths in the visible spectrum), novel emitter materials and architectures, and optical component materials. The LED product development focus areas are semiconductor materials, phosphors, emitter thermal control, luminaire thermal management techniques, electronic components research, and off-grid lighting. The core technology focus areas for OLEDs are novel device architecture, novel materials, material degradation, and electrode research. OLED product development areas include practical implementation of materials and device architectures, substrate materials, luminaire mechanical design, luminaire thermal management, large area OLED, and OLED light extraction.

The SSL Manufacturing Initiative was added to the SSL R&D portfolio in 2009 and is aimed at reducing costs of SSL sources and luminaires, improving product consistency and maintaining high-quality products, and encouraging a significant role for domestic U.S.-based manufacturing. Most of the one-time $50 million ARRA appropriation in FY2009 went into the manufacturing initiative, a fact reflected in the total obligations listed in Table 2.2. In its funding opportunity announcements, DOE expressed the goal of 50 percent cost-share for manufacturing projects and 20 percent for core technology and technology development projects. To aid in successful market adoption of SSL technology, DOE has also developed a 5-year SSL commercialization support plan to help create the conditions, specifications, standards, opportunities, and incentives that can lead to the accelerated adoption and applications of SSL products that will lead to reduced energy consumption in buildings.

TABLE 2.2 Breakdown of Current Department of Energy (DOE) Solid-State Lighting Research and Development (R&D) Obligations (from both DOE and Matching Funds) as of December 2011

| R&D Area | Funding (millions of dollars) | Percentage of Total Funding | Number of Projects |

| Core Technology | |||

| LEDs | 18.2 | 16 | 10 |

| OLEDs | 8.8 | 8 | 7 |

| Product Development | |||

| LEDs | 14.6 | 13 | 8 |

| OLEDs | 5.9 | 5 | 4 |

| Manufacturing | |||

| LEDs | 46.2 | 41 | 6 |

| OLEDs | 20.2 | 18 | 3 |

| Total | 113.9 | 100 | 38 |

SOURCE: Based on DOE (2011b) and Brodrick (2011).

TABLE 2.3 Fiscal Year 2011 Funding for Research and Development for Solid-State Lighting Program

| Pathway | Technology | EY2011 DOE Appropriationa | Applicant Cost-Sharea | Cost-Share Percentage |

| Core | LED | $3.7 | $0.9 | 19.6% |

| OLED | $0.7 | $0.09 | 11.4% | |

| Development | LED | $L5 | $0.3 | 16.7% |

| OLED | $I.4 | $0.3 | 17.6% | |

| Manufacturing | LED | $L3 | $0.2 | 13.3% |

| OLED | $0.5 | $0.2 | 28.6% | |

| TOTAL | $9.I | $1.99 | 17.9% | |

aIn millions of dollars.

SOURCE: James Brodrick, DOE.

As of December 2011 (DOE, 2011b) the DOE SSL R&D portfolio (consisting of projects awarded in current and past years that are currently being funded) included 38 projects addressing both LED and OLED technologies, with a total of approximately $114 million in government (including FY2009 ARRA-funded projects that remain ongoing) and industry investment (see Table 2.2). DOE was providing approximately $69 million ($44.6 for LEDs and $23.4 million for OLEDs ), and $45.9 million ($34.4 for LEDs and $11.5 million for OLEDs ) was provided through cost-shares by project awardees. Twenty-four projects were focused on LED technology and 14 on OLED technology. The BTP, along with ARRA funding, supported 38 projects, to which may be added 9 projects funded by the Small Business Innovation Research (SBIR) program in the Office of Science for an additional total of $4.1 million.

Table 2.3 shows the distribution of FY2011 R&D funding for core technology, product development, and manufacturing, as summarized in Table 2.2. Less than half (48.4 percent) of all R&D funding is devoted to the development of core technologies. Cost-sharing by grantees averages just under 18 percent (17.9 percent) of DOE funding and has declined in the past few years, particularly in the Product Development program, where one might expect more significant industry partnership.

The DOE Lighting R&D program also addresses issues related to commercialization, such as working with industry and other partners (e.g., Pacific Northwest National Laboratory [PNNL]4 and ORNL) to coordinate the development of standards or reduce barriers to market introduction of technologies that emerge from its efforts. It supports independent testing of SSL products, supports exploratory studies on market trends and helps to identify critical technology issues, supports workshops to foster collaboration on standards and test procedures, promotes a number of industry alliances and consortia, disseminates information, and supports a number of other initiatives (Brodrick, 2011). It also conducts technical, market, economic, and other analyses and provides incentives to the private sector to innovate.

FINDING: DOE has done an impressive job in leveraging a relatively small level of funding to play a leading role nationally and internationally in stimulating the development of SSL.

FINDING: In recent years, DOE has expanded its portfolio to include R&D into manufacturing projects, largely at the direction of Congress in the FY2009 ARRA funding and the FY2012 appropriations bill.

FINDING: The percentage of matching funds from R&D grant recipients was 18 percent for FY2011 funds. Ten years ago, for FY1999 to FY2001, it had been roughly 40 percent. It has declined in the past few years, particularly in the Product Development category.

RECOMMENDATION 2-2: The Department of Energy’s solid-state lighting program should be maintained and, if possible, increased.

RECOMMENDATION 2-3a: The Department of Energy should seek to obtain 50 percent cost-sharing for manufacturing research and development projects, as was done with the projects funded by the American Recovery and Reinvestment Act.

RECOMMENDATION 2-3b: As part of the next mandated study of the Department of Energy Solid State Lighting program in 2015, an external review should be conducted to provide recommendations on the relative proportions of funding that should be dedicated to core technology, product development, and manufacturing projects, and what the targeted level of matching funding should be in each of these three funding categories.

EPACT (05) directed DOE to establish a Next Generation Lighting Initiative (NGLI) to support the research, development, demonstration, and commercial application of

________________

4 In FY2011, $8.5 million was directed toward commercialization work at PNNL (James Brodrick, DOE, personal communication to Martin Offutt, National Research Council, February 22, 2012).

advanced SSL technologies. To that end, DOE was authorized to create an industry alliance (NGLIA) that consists of private, for-profit firms that are competitively selected to represent, as a group, U.S. SSL research, development, infrastructure, and manufacturing expertise. DOE may give preference to participants in the Industry Alliance in issuing competitive grants awards under the NGLI. DOE signed a memorandum of agreement (MOA) with NGLIA in February 2005 in which NGLIA will provide a manufacturing and commercialization emphasis for the NGLI. In order to facilitate this function, NGLIA members are provided a 1-year non-exclusive license to commercialize patented technologies resulting from the Core Technology Program. Most of the participants in the Core Technology Program are small businesses and universities who would retain the intellectual property rights in their federally funded inventions under the Bayh-Dole Act. Accordingly, DOE sought and obtained a determination of an exceptional circumstance that exempts DOE-funded SSL discoveries from the Bayh-Dole Act, as provided by 35 U.S.C. §202(a)(ii) of the statute. This determination will remain valid for 10 years, to 2015. Some of the leading researchers in the field of LED and OLED lighting have stated to the Committee that they have declined to apply for DOE funding because of this Bayh-Dole exemption.

FINDING: DOE’s waiver of Bayh-Dole for projects funded by the SSL R&D program is discouraging some universities and small companies from participating in the program.

RECOMMENDATION 2-4: The Department of Energy should consider ending its waiver of Bayh-Dole for SSL funding.

CURRENT FEDERAL AND STATE PROGRAMS

EPACT (92) gave DOE the authority to amend energy efficiency standards for covered general service fluorescent lamps and incandescent reflector lamps, and DOE later received a court order to complete the rulemaking by 2009. In July 2009, DOE published a final rule (DOE, 2009a). Its requirements came into effect starting July 14, 2012. In September 2011, DOE initiated another rulemaking on general service fluorescent lamps and incandescent reflector lamps with the aim of increasing the minimum efficacy requirements for these types of lamps by a few percent (DOE, 2011d). The final rule is projected to be published in April 2014 and become effective in April 2017. As a result of National Electrical Manufacturers Association (NEMA) comments to DOE regarding this rulemaking,5 DOE issued a report in 2011 acknowledging that in the medium term, there are projected to be shortages in the global supply of certain raw materials needed to produce such lamps as would comply with the 2009 rule (DOE, 2011f). Recently, DOE has issued waivers to manufacturers of T8 fluorescent lamps to ease the problem of these shortages, although a solution for the medium and long term is still being developed by industry even as it is developing SSL technology.

Federal voluntary programs have also played a key role in the improvement in lighting energy efficiency over the past two decades. In 1991, Environmental Protection Agency (EPA) created the Green Lights Program, a partnership to promote efficient lighting systems in commercial and industrial buildings (EPA, 2009). In this program, EPA partnered with public and private organizations to promote the use of more energy-efficient lighting. The program involved developing a plan for organizations to follow, required annual reporting of energy savings, and provided a set of free technical and marketing tools for participating organizations to help them transition to more efficient lighting.

In the mid-1990s, EPA merged the Green Lights Program into the ENERGY STAR® program. The latter program was started by EPA in 1992 as a voluntary labeling program designed to promote energy efficient appliances and other end-use products (GAO, 2010). Although ENERGY STAR® did not initially include lighting, luminaires were added in 1997, CFLs in 1999, solid-state luminaires in 2007, and integral LED lamps in 2009 (Baker, 2011). ENERGY STAR® became a collaboration between EPA and DOE in 1996 (GAO, 2010). EPA plays the primary role and has responsibility for setting performance levels, overseeing partnership agreements, product qualification determinations and listing, and monitoring and verification of the ENERGY STAR® performance criteria. DOE is responsible for the development and monitoring of test and measurement procedures, although in the lighting sector, industry has generally been proactive in developing the applicable test procedures.

ENERGY STAR® previously allowed manufacturers to self-certify compliance with ENERGY STAR® requirements, but it is now tightening the standard to require thirdparty certification of test data prior to ENERGY STAR® qualification and labeling (Baker, 2011). EPA requires that a product be tested by an EPA-recognized laboratory, which then submits the test data to an EPA-recognized, third-party certification body, which certifies that the product meets the ENERGY STAR® specifications. Once the product has been certified and displays the ENERGY STAR® label, the certification body conducts off-the-shelf verification testing (at manufacturers’ expense).

The current specifications for lamps receiving an ENERGY STAR® certification provide approximately a 75 percent savings in energy use versus a standard incandescent lamp. While the current ENERGY STAR® approach is

________________

5 Personal communication with Clark Silcox, NEMA General Counsel.

to specify different qualification criteria for specific lighting technologies, EPA has stated a goal of moving toward specification integration in which one set of technology-neutral specifications would apply to all lighting technologies. To that end, EPA has recently merged the SSL luminaire and non-SSL residential luminaire specifications into a single specification (EPA, 2011b) and has also proposed to merge the CFL and SSL lamp specifications. However, the lighting industry has expressed concern that recent EPA actions do not fully implement a technology-neutral approach. The current specification has different performance requirements for CFL and LED products with respect to many performance characteristics (life rating, color maintenance requirement, color angular uniformity requirements, lumen maintenance requirements, and power factor requirements, to mention a few) and does not appear to support the inclusion of any other technologies (such as halogen or metal halide), no matter how significant any improvements that were made in them, given that test measurement methods are typically only given for fluorescent and SSL technologies.

FINDING: A technology-neutral specification for lighting would “raise the bar” for energy efficiency without putting the government in the position of picking and choosing which technologies should be included in ENERGY STAR®.Rather, those technologies that meet the specified criteria (e.g., luminous efficacy, color temperature, color rendering) would qualify for ENERGY STAR® labeling.

RECOMMENDATION 2-5: The Environmental Protection Agency should develop technology-neutral specifications for lighting that are based on performance rather than the type of lamp to provide the most objective and even-handed standards for energy efficiency.

While ENERGY STAR® applies to more than 70 product categories, lighting is one of the few product categories in which the ENERGY STAR® qualification is dependent not only on energy efficiency, but also on lighting quality. The ENERGY STAR® lamp specification contains an extensive list of performance requirements (e.g., requirements relating to color consistency, color rendering, turn-on time, run-up time) unrelated to energy efficiency, which are intended to ensure that ENERGY STAR® lighting products have a high level of quality and are acceptable to consumers. EPA recently published a vision document in which it justifies the inclusion of non-energy related requirements in ENERGY STAR® specifications (EPA, 2012). For its part, industry has expressed concerns about the inclusion of non-energy related factors in the ENERGY STAR® lighting criteria, citing the potential for duplicative, inconsistent, or unnecessary requirements, given that other standards and regulations may include similar provisions.

The ENERGY STAR® labeling program for individual lighting products primarily applies to federal procurement and residential applications and generally not to commercial or industrial products. ENERGY STAR® applies to commercial and industrial facilities, but the standards are for overall building energy efficiency (which includes lighting) rather than efficiency of individual components such as lighting (other than those luminaires in commercial buildings subject to federal procurement). The ENERGY STAR® buildings program evolved in the 1990s out of the Green Lights Program to focus not only on technologies but also on the interaction of the various building systems. EPA awarded the first ENERGY STAR® to a building in 1999 (EPA, 2009).

Installation of more energy efficient lighting may help a commercial or industrial facility to meet the ENERGY STAR® criteria, but other energy sources must also be considered. The Design Lights Consortium, a collaboration of utility companies and regional energy efficiency organizations, is attempting to supplement the existing ENERGY STAR® approach by providing awareness of efficient lighting products for commercial buildings.6

Additionally, the Consortium for Energy Efficiency provides model incentive programs for utilities to adopt, and commercial lighting products are already included in its programs. Finally, the DOE Municipal SSL Street Light Consortium addresses the energy efficiency of street and roadway lighting and assists cities and municipalities in their energy efficiency needs. However, this program is primarily a listing of products without the certification and labeling requirements of ENERGY STAR® and is not as high-profile as ENERGY STAR®.

FINDING: The ENERGY STAR® program provides useful information to residential consumers on energy efficient lighting products. While the ENERGY STAR® program also has a commercial and industrial segment, that program focuses on overall building efficiency rather than the certification and labeling of individual products (with the exception of luminaires in commercial buildings subject to federal procurement). Many other government and industry organizations address lighting product standards for the commercial sector.

States have been active in promoting energy conservation and efficiency by adopting a variety of regulatory, policy, and incentive programs, many of which will directly or indirectly encourage more energy efficient lighting (DSIRE, 2011). In addition to these general provisions for energy efficiency, some states have adopted specific regulations for lighting. Although EPCA (75) generally preempts state energy efficiency regulations for lighting that is regulated by the federal government, EISA 2007 provides an exception for California and Nevada to adopt the EISA energy efficiency standards

________________

1 year earlier than required by the federal program. Although Nevada has declined to exercise this option, the California Energy Commission adopted regulations implementing the federal standards 1 year earlier, so the standards shown in Table 2.1 above are being implemented 1 year earlier in California, which started in January 2011.

Some states, such as Texas and South Carolina, have adopted or proposed legislation exempting any lamps manufactured entirely within that state from the federal EISA 2007 requirements.7 However, it is unlikely that any lamps and all their components are or will be manufactured entirely in a single state, and, thus, these state bills (which have also been introduced but not passed in other states) have more symbolic than practical effect.

In California, which has begun to implement the requirements 1 year in advance of the rest of the United States, no significant opposition or problems have been encountered by the initial implementation of the EISA 2007 requirements.

FINDING: The EISA 2007 requirements for phasing out inefficient lighting have sparked significant resistance by some legislators, states, and citizens in advance of the implementations of the requirements.

In addition to the regulation of the energy efficiency of individual lighting products by federal and state laws (discussed above), lighting energy use in the United States is also regulated by state-administered building codes that govern the installed power and/or energy use of lighting installations in new construction projects and major renovations that require a building permit. In particular, the American Society of Heating, Refrigeration and Air Conditioning Engineers (ASHRAE) and the International Code Council (ICC) both publish “model energy codes” for states to adopt. ASHRAE has two minimum codes applicable to new construction: Standard 90.1 for commercial and industrial buildings and Standard 90.2 for residential buildings. The ICC develops the International Energy Conservation Code (IECC) that covers both residential and non-residential requirements. In addition, some states—especially California, Oregon, and Washington—have a history of developing their own codes. At the highest level, all of these codes approach the issue in a similar way—by setting a maximum allowed installed lighting power density (LPD) and prescribing the minimum lighting controls that must be used in commercial and industrial buildings. LPD refers to the spatial average power consumption of the installed luminaires in a building or in a space and is expressed in units of watts per square feet of floor area (W/ft2). In residential buildings, the maximum LPD is not typically standardized, but the minimum efficacy of lamps is often given, in addition to prescribing some requirements for lighting controls.

The LPD cannot be arbitrarily low. The Illuminating Engineering Society (IES) defines recommended illumination levels for a large variety of visual tasks, and building codes for commercial and industrial buildings take these recommendations into account. In order to reduce energy use and costs, the trend over the past decade has been for builders to lower the LPDs to the point that the International Association of Lighting Designers (IALD) has published a statement indicating that they do not support any further lowering of the LPDs beyond ASHRAE Standard 90.1-2010 (IALD, 2011). Additional lowering of lighting power densities would only be acceptable if the illumination levels remain unchanged, which requires an increase in efficacy of the light source. The position expressed by IALD is based on the performance of currently available technology, which is commonly used as a criterion for changes in building energy codes.

FINDING: Given the currently available lighting technologies, LPD allowances for commercial buildings have reached their practical lower limits, according to lighting professionals. In the long term, SSL may permit LPD allowances in building codes to be reduced further.

Although states are required by federal law (EPACT 92) to either adopt the latest version of a model building energy code or develop one that is considered equivalent to such an energy code, there is no penalty for not complying with this requirement. As of late 2011, about half of the states have adopted a commercial building energy code corresponding to ASHRAE Standard 90.1-2007, and nearly the same number have adopted a residential model building code corresponding to 2009 IECC.8 However, the 2010 version of ASHRAE Standard 90.1 offers significant energy savings over its predecessor, as shown in determinations performed by PNNL. Large architectural engineering firms design buildings at least to the requirements of the latest standards. However many design-build contractors, who provide the bulk of the smaller buildings, typically minimize the initial cost of the building, resulting in lower performance. Furthermore, enforcement of building energy code requirements is sometimes inadequate or inconsistent at the state level. Even in California, where the energy code process is among the best in the nation, the California Energy Commission lacked enforcement authority until 2011, when the California

________________

7 Texas HB 2510, 82(R) Sess. (2011) (signed into law June 17, 2011, effective January 1, 2012); H. 3735, South Carolina General Assembly, 119th Session, 2011-2012 (introduced February 11, 2011, pending in state senate at end of session).

8 However, states are not required to meet ASHRAE Standard 90.1-2007 until July 20, 2013, 2 years after DOE issued a final determination on 90.1-2007 and the 2009 International Energy Conservation Code. They are not required to comply with 90.1-2010 until October 19, 2013.

legislature passed a law (SB 4549) granting the commission such authority.

FINDING: Minimum building energy standards and model codes are steadily improving. Nevertheless, their adoption, as well as uniform and effective enforcement of adopted energy codes, would result in significant energy savings.

PNNL has historically been tasked by DOE to perform a “determination” of the energy savings effect of a new version of building codes for commercial buildings. PNNL determined that a commercial building complying with the 2010 standard is approximately 18.2 percent more energy efficient than one complying with the same standard from 2007 (DOE, 2011e). Lighting has played a key role in achieving this result through the reduction of maximum allowed LPDs, as well as the increased mandatory requirements for lighting controls. The goal for the 2015-2016 code cycle is to improve commercial building energy efficiency by 50 percent over the 2004 standard, and the long-term DOE vision is to achieve marketable “net zero” energy commercial buildings by the year 2025 (DOE, undated). To achieve this result, buildings will have to have on site “renewable” energy generation that on average is greater than or equal to the energy consumption of the building over the course of a year.

The model residential building code requires 50 percent of the permanently installed luminaires to use “high-efficacy” lamps. High efficacy is defined in IECC10 in a way that, in practical effect, the residential building must use either CFLs or SSL products. The 2012 version of IECC increases this requirement to 75 percent of the permanently installed luminaires, and Maryland was the first state to adopt that version in December 2011. Title 24 of the California Code of Regulations requires the use of high-efficacy light sources in some rooms while giving the user a choice of high-efficacy light sources or any light sources operated on lighting controls (other than a manual switch) for other rooms.

The current approach of the model residential energy code to lighting has some important limitations. First, the codes specify the energy efficiency of installed lighting but do not address the total number of luminaires nor how the lighting is used. Moreover, the trend in IECC to require an increasing percentage of high-efficacy light sources in residential new construction may have unintended consequences in terms of the number of lamps installed or how they are used, at least in the short term when LED lamps are not yet appropriate for all residential applications. Moreover, as discussed later in this chapter, there is broad consumer dissatisfaction with CFLs.

An alternative is to follow the California example and give the home owners the option of using either high-efficacy lamps or standard lamps with appropriate lighting controls.

FINDING: Model energy codes for residential buildings only address the efficacy of light sources, not their number or their use. The approach taken by the California residential energy code may be more likely to improve energy efficiency.

Specifications for High-Performance Buildings

High-performance buildings are designed to use sustainable materials, consume less energy than other buildings, and conform to “Green Codes” or High-Performance Building Standards.11 High-performance buildings focus on reducing or eliminating the waste at the building level.

The new trend is to shift attention from LPDs to actual energy use as well as focusing on controls as a way to eliminate wasted energy. A recent, thorough assessment of the energy savings potential from lighting controls shows that the biggest opportunities for savings come from reducing lighting power use by “tuning,” or setting the illumination level appropriately for the visual task, occupancy sensing (which turns off lighting when there are no people present), and daylighting (reducing electric lighting power in response to available daylight) (Williams et al., 2012). Using all of these lighting control strategies offers an average opportunity for energy savings in the range of 25 to 40 percent.

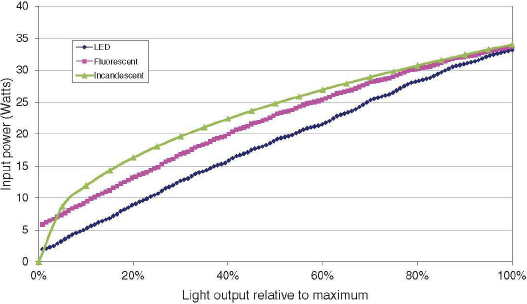

FIGURE 2.2 illustrates the relationship between light output and electrical power required to produce that light output. The quantities are shown as relative light output and relative power, and one can see that in each case, as light output is reduced, the electrical power required to produce that light output also decreases. In the case of incandescent and halogen lamps, the reduction of power is slower than with the other light sources. SSL shows the most linear response between light output and electrical power. When lighting control strategies are fully employed in a building, the installed LPDs (as represented by the right end point of the curves) become less relevant.

Some industry sources (e.g., NEMA) have concluded that regulation at the component level will not achieve net-zero energy buildings, so in order to achieve the goal set by DOE to get there by 2030, a systems approach is needed. It is noteworthy, therefore, that some residential “green codes” still express a preference for high-efficacy lighting in general, and sometimes for SSL products in particular. The approach in lighting requirements for residential buildings may need to change in view of this goal.

________________

9 See http://www.leginfo.ca.gov/pub/11-12/bill/sen/sb_0451-0500/sb_454_bill_20110216_introduced.pdf.

10 High-efficacy lamps are compact fluorescent lamps, T-8 or smaller diameter linear fluorescent lamps, or lamps with a minimum efficacy of 60 lumens per watt for lamps over 40 watts; 50 lumens per watt for lamps over 15 watts to 40 watts; and 40 lumens per watt for lamps 15 watts or less (ICC, 2012).

11 Such standards include, for example, ASHRAE 189.1: Standards for the Design of High-Performance Green Buildings Except Low-Rise Residential Buildings; and International Green Construction Code™ (IgCC) published by the International Code Council.

FIGURE 2.2 Typical power draw as a function of light output for dimmable incandescent, fluorescent, and LED luminaires with maximum rated power of approximately 34 watts.

Various incentive programs have also played an important role in encouraging the adoption of more energy efficient lighting. The most prevalent and high-profile incentive programs have been provided by electric utilities, which have actively supported the use of more energy efficient lighting as part of their DSM and energy conservation campaigns. For example, electric utilities across the nation have actively promoted CFLs with consumer incentive programs, including giveaways, direct install products, discounted prices, and rebates (Vestel, 2009). These utility incentive programs increased consumer awareness of more energy efficient products (such as CFLs) (Sandahl et al., 2006). However, the programs also encountered some limitations, including the frequent reliance on low-quality, low-price CFLs that may have reinforced negative attitudes toward this technology by consumers (Sandahl et al., 2006). In addition, providing consumers with energy efficient lamps for free or at greatly reduced prices might create unrealistic expectations about lower future costs for such lighting (Sandahl et al., 2006).

Some retailers have also implemented their own incentive programs for efficient lighting. For example, Walmart, the nation’s largest retailer, committed to selling 100 million CFLs (Barbaro, 2007). It was able to achieve this 3 months ahead of schedule because of an aggressive in-store campaign and devoted shelf space as well as partnership with DOE, Environmental Defense, and a number of other organizations to promote energy efficiency.

In addition to incentives that are available from electric utilities and retailers, the federal government has made available tax deductions to commercial building owners when they undertake energy efficiency improvements beyond minimum code requirements. EPACT (05) authorized the Energy Efficient Commercial Building Tax Deduction, creating Section 179D of the Internal Revenue Code (26 United States Code, Section 179D). According to this part of the Code, a taxpayer who owns, or is a lessee of, a commercial building that achieves reductions to 50 percent below the level set by ANSI/ASHRAE/IESNA Standard 90.1-2001 is eligible for a tax deduction of up to $1.80 per square foot, and $0.60 if lesser reductions are realized (IRS, 2012). Buildings designed to have lighting power density at least 25 percent below the baseline established by Standard 90.1-2001 are eligible for a tax deduction of $0.30 per square foot of floor space that is renovated. For public buildings, the tax deduction is available for the design teams. The original law was extended in 2008 until December 31, 2013 (GSA, 2011).

Finally, DOE has created incentives for the design and manufacture of more efficient lamps by offering a prize, called the Bright Tomorrow Lighting Prize or the “L Prize,” for the manufacturer that can design an LED lamp that meets specified performance criteria.12 As mandated by EISA 2007, DOE is offering this prize initially to manufacturers that develop and plan to manufacture at a reasonable cost energy efficient replacement technologies for “two of today’s most widely used and inefficient technologies, 60 W incandescent lamps and [parabolic aluminum reflector] (PAR) 38 halogen lamps” (DOE, 2009). It was announced in August 2011 that Philips Lighting North America had won the L Prize in the 60 W category.

________________

FINDING: Non-regulatory incentive programs may play an important role in the adoption of energy efficient lighting technologies.

RECOMMENDATION 2-6: The Department of Energy, in consultation with the Department of the Treasury, should conduct a study to determine the effectiveness and impacts of incentive program designs in fostering adoption of efficient lighting technologies.

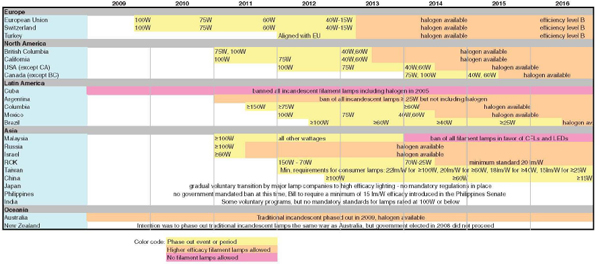

Many nations are in the process of phasing out traditional incandescent lamps in favor of more energy efficient lamps (Figure 2.3). Cuba and Australia were the first nations to phase out incandescent lamps. New Zealand joined its neighbor Australia in June 2008 by announcing that country’s intention to phase out incandescent lamps and later joined with Australia to develop a common minimum efficacy standard for these lamps, AS/NZS 4934.2(Int):2008, which was later replaced by AS/NZS 4934.2:2011. However, public opinion and a change in government in New Zealand led that country in March 2011 to repeal the ban announced in 2008. The European Union began a phase-out of incandescent lamps on September 1, 2009.

In November 2011, China announced that it will phase out incandescent lamps within 5 years. Canada also adopted a phase-out of incandescent lamps starting in January 2012, but in October 2011 the Canadian government announced that the phase-out in that country will be delayed by 2 years, expressing concerns about “the availability of compliant technologies and perceived health and mercury issues, including safe disposal for compact fluorescent lamps,” and will now begin in January 2014 (Thompson, 2011).

FINDING: Other countries are following similar regulatory pathways as the United States in phasing out incandescent lamps, although at different schedules and with some delays.

In contrast to the convergence in lighting product regulations, building regulations are less uniform around the world, and thus far there have been no internationally recognized building standards. Significantly, the International Commission on Illumination or CIE (Commission Internationale d’Eclerage) announced in 2011 that it is starting a new technical committee to develop recommendations for international building standards.

COMPACT FLUORESCENT LAMP CASE STUDY

The U.S. experience with CFLs provides a useful case study that offers some pertinent lessons for LED lighting. The CFL is much more energy efficient than the incandescent lamp, and it also lasts much longer. The incandescent lamp converts only 0.2 to 2.6 percent of electricity consumed into useful light (the rest is wasted as heat) and has a typical lifetime between several hundred and a few thousand hours (median of about 1,000 hours). The CFL, on the other hand, has an efficiency of approximately 13 percent (five-fold better than the incandescent lamp) and has a reported lifetime ranging from 3,000 to 30,000 hours (median around 10,000 hours) (Azevedo et al., 2009). The Congressional Research Service estimates that a typical 100 W incandescent lamp used $18.30 in energy per year compared to only $4.90 for an equivalent CFL lamp (Logan, 2008). The CFL thus provides great potential to save energy, money, and reduce environmental consequences, such as CO2 emissions, from generating the electricity needed to operate the light.

While fluorescent lights have been widely used in commercial and industrial applications since the 1950s, they were not appropriate for most residential applications until the advent of the CFL. The first spiral tube CFL was created in 1976, but they were not commercially available on a widespread basis until the 1990s—when they were made feasible by technological advances such as the ability to cost-effectively manufacture lamps consisting of tightly coiled gas-filled fluorescent tubes and the introduction of small electronic ballasts (Sandahl et al., 2006; Logan, 2008).

The initial consumer uptake of CFLs in the 1980s and 1990s was slow and was much lower in the United States than other industrial nations (LRC, 2003; Sandahl et al., 2006). Various utility energy efficiency programs gave away or substantially discounted CFLs in the 1990s, but these programs were generally unsuccessful in building consumer demand for CFLs. Many of the CFLs distributed in these programs were of low quality (e.g., poor CRI, unmet projected lifetime, lack of cold temperature operation, delay to full brightness, inability to dim, inability to fit in many lamp harps), reinforcing negative stereotypes of CFLs (Sandahl et al., 2006). Moreover, the free or near-free distribution of millions of CFLs created an expectation that CFLs were inexpensive, causing consumer backlash when higher quality and more realistically priced lamps were offered for sale once the giveaway programs ended (Sandahl et al., 2006).

The market share of CFLs grew rapidly in the early 2000s as utilities and other entities aggressively promoted consumer switch-over to CFLs. For example, the EPA and a large number of participating manufacturers, retailers, and utilities launched a national media campaign in 2001 promoting CFLs (Sandahl et al., 2006). Today, the majority of U.S. households have used or are currently using at least one CFL (APT, 2010). The market share for CFLs hit a peak of approximately 20 percent in 2007 but then declined in 2008 and 2009 to approximately 15 percent of the U.S. market, due in part to the recession, but also likely in part due to reduced incentive programs (Swope, 2010). This market penetration of CFLs has resulted in an expected decline in overall replacement shipments, as the CFL’s longer life has reduced the frequency in which lamps must be replaced (APT, 2010).

The ENERGY STAR® program has also helped to enhance the quality and environmental benefit perceptions of CFLs. ENERGY STAR® launched a CFL program in 1999 that set design specifications for lamps that would qualify for ENERGY STAR® labeling, which had a beneficial effect in promoting the production and sale of high-quality, energy efficient CFLs (Sandahl et al., 2006). These specifications for program-compliant CFLs have been strengthened several times since the launch of the program in 1999. Nearly 300 million ENERGY STAR®-certified CFLs were sold in the United States in 2007 (Logan, 2008).

EISA 2007 has the potential to significantly increase market demand for CFLs as the traditional incandescent lamp is gradually phased out for general service applications by the legislation. Virtually every other industrial nation has adopted similar measures to phase out incandescent lamps (see Figure 2.3; Waide, 2010). Amendments to California’s Title 24 energy code requirements in October 2005 required dedicated non-screw-based, energy efficient luminaires in most new residential applications, which again provided a regulatory boost to CFLs, although in this case for the linear pin-based CFLs with a separate ballast rather than the screwin spiral CFLs being developed to substitute for traditional incandescent lamps.

Despite this progress, the CFL has encountered a number of problems that have presented a significant obstacle to its market growth and adoption. One problem is that consumers associate negative connotations with the word “fluorescent,” likely a residue of the “unfriendly” and flickering fluorescent tube lighting used in many commercial establishments (LRC, 2003; Brodrick, 2007). Another problem, noted in the above discussion on DSM, has been the poor or inconsistent quality, reliability, and durability of some CFL lamps. For example, many of these cheaper lamps had inconsistent performance and produced low-quality light (Sandahl et al., 2006; Logan, 2008). Exaggerated product claims had a lasting detrimental impact on consumer interest and confidence in CFLs (Sandahl et al., 2006). Some cheaper CFLs even had to be recalled because they presented a fire danger (CPSC, 2010). Many consumers who were early adopters of CFLs ended up removing them from their homes because of the disappointing performance (Broderick, 2007). In many cases, CFL products were used as screw-in replacements for various types of incandescent bulbs, such as the PAR lamp, used in recessed, downlighting applications. Lacking the internal reflector, the retro-fitted, omni-directional CFL in some cases would result in lower efficacy (lumens per watt) of the luminaire. A similar problem occurred in surface-mounted downlights, where the lamp was indiscriminately matched with the luminaire’s optical components.

In addition, some CFLs have not lived up to their advertised extended lifespan. For example, one analysis of the Program for the Evaluation and Analysis of Residential lighting (PEARL) found that 2 to 13 percent (depending on brand) of CFLs failed early, and half of reflector CFLs used in recessed lighting had dimmed by at least 25 percent by halfway through their rated lifetime (Angelle, 2010). Another study performed for the California Public Utilities Commission found that the average useful life of a CFL in California was 6.3 years, considerably shorter than the projected useful life of 9.4 years (Smith, 2011). Moreover, factors such as frequently turning the light on and off can substantially degrade the longevity of a fluorescent lamp (DOE, 2011c). Given that the extended useful life of CFLs is one of their primary selling points, the early burnout of many lamps was “especially vexing” (Broderick, 2007). While substantial improvements have been made in the quality and reliability of CFLs, by engineering improvements in both the lamp and ballast design (Sandahl et al., 2006), there remains significant variation in product quality that continues to hamper consumer confidence (Logan, 2008).

Some consumers have expressed dissatisfaction with the quality of light from CFLs. These consumer concerns include the following: CFLs have a slower ramp-up to full luminous output compared to the standard incandescent lamp; most CFLs are not dimmable; and, most significantly, some consumers perceive the quality of light from CFLs as inferior to traditional lighting sources, with frequent complaints that the light is “too dim,” “harsh and unflattering,” “too blue,” or otherwise “not right” (APT, 2010; Logan, 2008; Rice, 2011; Sandahl et al., 2006; LRC, 2003; Scelfo, 2008). Although manufacturers of CFLs have invested considerable R&D effort to improve the performance of CFLs, adverse consumer perceptions can be long-lasting and hard to reverse.

Environmental and health concerns have also been an important factor in the uptake of CFLs. Each CFL contains a small amount of mercury (generally 3-5 mg per lamp), which, if accumulated in landfills or other inappropriate disposal routes, could total a significant amount of mercury released to the environment, creating both an environmental and occupational exposure risk (Aucott et al., 2003). Only 2 percent of residential users and just under 30 percent of businesses properly recycle their CFLs, even though some state laws mandate recycling of fluorescent and a number of retailers and other entities have launched free recycling programs (Bohan, 2011; Silveira and Chang, 2011). Nevertheless, EPA and others have pointed out that CFLs may still result in a net decrease in mercury releases into the environment because the mercury released from CFLs, especially if handled and disposed of properly, would be less than the amount of mercury emissions that would result from coal-fired power plants if powering all incandescent lamps (ENERGY STAR®, 2010).

Some states have adopted regulations for recycling or disposal of mercury-containing light. For example, the Massachusetts Mercury Management Act, adopted in 2006 (Chapter 109 of the Acts of 2006), prohibits the disposal of mercury-containing lamps in the trash or other unapproved sites and requires manufacturers of such lamps to implement a plan for educating users about recycling “end of life”

lamps. The Massachusetts law also establishes recycling targets for mercury-containing lamps that reached 70 percent by December 2011. Similarly, Maine requires (Chapter 850, Section 3A) any type of mercury-added lamp used in commercial, industrial, or residential applications to be treated as hazardous waste, which requires that all such lamps be treated, disposed, or recycled at an authorized destination facility. The State of Washington adopted legislation in 2010 (ESSB5543) that established a producer-financed product stewardship program for the collection, recycling, and disposal of mercury-containing lamps that must be implemented by 2013, after which no CFLs may be placed in the garbage.

Moreover, there is also concern about individual lamps breaking in residential use, and the EPA recommends special precautions in using and disposing of CFLs if they break (EPA, 2011a), which may alarm some consumers. The European Union’s Scientific Committee on Health and Environmental Risks (SCHER) calculated that ambient room exposures to mercury are in the range of or exceed the occupational exposure limit (100 μg/m3), but because that exposure limit is based on the safe level of lifetime exposure, the expert group concluded that adults would not be harmed by mercury exposures from a broken CFL lamp (SCHER, 2010). Various unconfirmed allegations in the media about other potential health impacts of CFLs, including migraine headaches, skin problems, epileptic seizures, and cancer, have further increased public anxiety about the “unfamiliar” CFLs (Ward, 2011).

Consumer confusion and uncertainty have also been impediments to CFL uptake (Sandahl et al., 2006). Some specific examples included uncertainty about whether CFLs could be used in existing luminaires, confusion caused by the use of different names to describe CFLs, the lack of ability to compare different lighting technologies in terms of watts and lumens, and the inability to communicate different color options (Sandahl et al., 2006; Broderick, 2007). Consumers were more comfortable with performance descriptions that were framed in terms of comparisons with existing, familiar products (Sandahl et al., 2006). More generally, there also is considerable inertia in the consumer demand for lighting, with many consumers displaying strong preferences for lamps that are most similar to the type they have been using previously. Thus, as the incandescent lamp is gradually phased out under the EISA 2007 timeline, many consumers will switch to halogen lamps rather than CFLs, even though CFLs generally provide a greater energy efficiency advantage.

Initial price has also been a problem for CFL uptake (LRC, 2003; Sandahl et al., 2006; APT, 2010). Even though CFLs save consumers money in the long-run because of lower energy use and longer lifespan, consumers are particularly sensitive to the higher up-front costs of CFLs, as is the case with many other energy efficient products, an effect described as the “energy paradox” of the very gradual diffusion of energy-conservation technologies (Jaffe and Stavins, 1994). The Government Accountability Office (GAO) estimates that the higher up-front cost of a CFL would be recovered in 2 to 7 months because of the higher energy efficiency and lower replacement costs of CFLs, but consumers are disproportionately influenced by the higher initial cost (Logan, 2008). Consumers apply a very high implicit discount rate—as high as 300 percent compared to the typical 2.5 to 10 percent used in most economic analyses—that deter consumer purchases of energy efficiency technologies that may cost more up-front but save money over their lifetime because of lower energy and replacement costs (Azevedo et al., 2009). This inflated consumer discount rate is attributed to a number of factors, including lack of knowledge about cost savings, disbelief about lifetime savings, and lack of expertise in addressing the time value of money (Azevedo et al., 2009).

In addition, substantial variation in CFL pricing, including the availability of inexpensive subsidized lamps, creates consumer confusion and beliefs that higher-priced CFLs are over-priced (Sandahl et al., 2006). Empirical studies indicate that many consumers are unaware of the lower operating costs of CFLs, as well as their environmental benefits (Di Maria et al., 2010; LRC, 2003). Better communication initiatives—such as clearer labels emphasizing lower lifetime costs and the trade-offs between initial and operating costs, as well as various types of consumer education campaigns, have been suggested as necessary to help consumers understand the energy saving and environmental benefits of CFLs (Di Maria et al., 2010).

Mandating technology change through legislation without any concerted effort to educate and prepare consumers, not unexpectedly, creates a political backlash, with the perceived shortcomings of the CFL serving as a key catalyst to much of the controversy and opposition. (See further discussion of this issue in Chapter 6 in the section “Role of Govern ment in Aiding Widespread Adoption.”) Some consumers are stockpiling incandescent lamps (O’Donnell and Koch, 2011), in many cases after trying and rejecting CFLs, and the public resistance to the switchover is likely to grow as more consumers become aware of the legislative consequences as they began to take effect on January 1, 2012. Some politicians have decried the “light bulb ban” and criticized the attempt to impose those “little, squiggly, pigtailed” CFLs on an unreceptive public (Rice, 2011). The EISA 2007 mandate has become a lightning rod for contested national political debates on the role of government in society and consumer freedom. Legislation has been introduced to overturn the phase-out of the incandescent lamp, but none has succeeded to date, although some have received significant and even majority support. For example, the U.S. House of Representatives passed an amendment in July 2011 that would prohibit DOE from spending any funds on implementing the lighting efficiency standards (Howell, 2011). As noted above, similar bills have been introduced in state legislatures in South Carolina and Texas (Simon, 2011).

FINDING: Disposal of mercury-containing CFL lamps and perceived health impacts are causing concern by some citizens and states. Federal legislators and other actors promoting CFL lamps failed to adequately anticipate these perceived risks and concerns.

RECOMMENDATION 2-7: Policy makers should anticipate real or perceived environmental, health, and safety issues associated with solid-state lighting technologies and prepare to address such concerns proactively.

FINDING: The experience with CFLs provides a number of lessons for SSL, including the following: (1) the quality, reliability, and price of initial products will be a critical factor in the success and consumer uptake of the product; (2) market introduction and penetration take time; (3) manufacturers and others should take care not to over promise; (4) consumer education is critical; and (5) ENERGY STAR® and other credible performance standards can play important roles in raising quality and confidence.

Angelle, A. 2010. Will LED light best your CFLs and incandescents? Popular Mechanics. August 4. Available at http://www.popularmechanics.com/science/environment/will-led-light--best-cfls-and-incandescents.

APT (Applied Proactive Technologies, Inc.). 2010. The U.S. Replacement Lamp Market, 2010-2015, and the Impact of Federal Regulation on Energy Efficiency Lighting Programs. Springfield, Mass.: APT, Inc. August. Available at http://www.appliedproactive.com/uploads/pdf/USLampMarket_and_EELightingPrograms_APT_Final.pdf.

Aucott, M., M. McLinden, and M. Winka. 2003. Release of mercury from fluorescent. Journal of the Air and Waste Management Association 53:143-151.

Azevedo, I.L., M.G. Morgan, and F. Morgan. 2009. The transition to solid-state lighting. Proceedings of the IEEE 97:481-510.

Baker, A. 2011. “ENERGY STAR® Lighting: An Update on the New Program.” Presentation to the Committee on Assessment of Solid State Lighting, Washington, D.C. July 28.

Barbaro, M. 2007. Wal-Mart puts some muscle behind power-sipping. New York Times. January 2.

Bohan, S. 2011. Mercury in unrecycled CFLs take a toll on the environment. Los Angeles Times. April 7.

Broderick, J. 2007. CFLs in America: Lessons learned on the way to the market. LD+A July:52-56.

Brodrick, J.R., U.S. Department of Energy. 2012. “Briefing on DOE Solid-State Lighting Program.” Presentation to the Committee on Assessment of Solid State Lighting, Washington, D.C. May 9, 2011; updated February 2012.

CPSC (Consumer Product Safety Commission). 2010. Trisonic Compact Fluorescent Light Recalled Due to Fire Hazard. CPSC Release #11-001. October 5. Available at http://www.cpsc.gov/cpscpub/prerel/prhtml11/11001.html.

Di Maria, C., S. Ferreira, and E. Lazarova. 2010. Shedding light on the light bulb puzzle: The role of attitudes and perceptions in the adoption of energy efficient light. Scottish Journal of Political Economy 57:48-67.

DOE (Department of Energy). Undated. Net Zero Energy Commercial Building Initiative. Available at http://apps1.eere.energy.gov/buildings/publications/pdfs/alliances/cbi_fs.pdf.

DOE. 2009. Energy Conservation Program: Energy Conservation Standards and Test Procedures for General Service Fluorescent Lamps and Incandescent Reflector Lamps. Final Rule. Federal Register 74(133):34079-34179 (July 14).

DOE. 2010. Department of Energy FY 2011 Congressional Budget Request, Volume 3. Washington, D.C.: DOE Office of the Chief Financial Officer. February. Available at http://www.cfo.doe.gov/budget/11budget/Content/Volume%203.pdf. Accessed October 25, 2011.

DOE. 2011a. Solid-State Lighting Research and Development: Multi-Year Program Plan. Washington, D.C.: Office of Energy Efficiency and Renew able Energy, Building Technologies Program. March.

DOE. 2011b. Department of Energy FY 2012 Congressional Budget Request, Volume 3. Washington, D.C.: DOE Office of the Chief Financial Officer. February. Available at http://www.cfo.doe.gov/budget/12budget/Content/Volume3.pdf. Accessed October 25, 2011.

DOE. 2011c. Energy Savers: When to Turn Off Your Lights, July 18. Available at http://www.energysavers.gov/your_home/lighting_daylighting/index.cfm/mytopic=12280.

DOE. 2011d. Energy Conservation Program: Test Procedures for General Service Fluorescent Lamps, General Service Incandescent Lamps, and Incandescent Reflector Lamps—Notice of Proposed Rulemaking. Federal Register 76:56661-56678 (September 14).

DOE. 2011e. Building Energy Standards Program: Final Determination Regarding Energy Efficiency Improvements in the Energy Standard for Buildings, Except Low-Rise Residential Buildings, ANSI/ASHRAE/IESNA Standard 90.1-2010. Federal Register 76:64904-64923 (October 11).

DOE. 2011f. Critical Materials Strategy. Washington, D.C.: U.S. Department of Energy. December.

DSIRE. 2011. Database of State Incentives for Renewables and Efficiency. Available at http://www.dsireusa.org/.

ENERGY STAR®. 2010. Frequently Asked Questions Information on Compact Fluorescent Light (CFLs) and Mercury. November. Available at http://www.energystar.gov/ia/partners/promotions/change_light/downloads/Fact_Sheet_Mercury.pdf.

EPA (U.S. Environmental Protection Agency). 2009. Celebrating a Decade of Energy Star Buildings: 1999-2009. Washington, D.C.: U.S.

EPA. Available at http://www.energystar.gov/ia/business/downloads/Decade_of_Energy_Star.pdf.

EPA. 2011a. What to Do if a Compact Fluorescent Light (CFL) Bulb or Fluorescent Tube Light Bulb Breaks in Your Home. January 25. Available at http://www.epa.gov/cfl/cflcleanup.pdf.

EPA. 2011b. ENERGY STAR Program Requirements Product Specification for Lamps. Version 1.0, Draft 1. Washington, D.C.: U.S. EPA. October.

EPA. 2012. ENERGY STAR Products Program Strategic Vision and Guiding Principles. Washington, D.C.: U.S. EPA. January.

GAO (Government Accountability Office). 2010. Energy Star Program: Covert Testing Shows the Energy Star Program Certification Process is Vulnerable to Fraud and Abuse. Washington, D.C.: U.S. Government Printing Office.

Gillingham, K., R.G. Newell, and K. Palmer. 2004. Examination of Demand-Side Energy Efficiency Policies. RFF discussion paper. Washington, D.C.: Resources for the Future.

GSA (General Services Administration). 2011. Energy Efficient Commercial Building Tax Deduction. Available at http://www.gsa.gov/portal/content/221677. Accessed May 21, 2012.

Howell, K. 2011. Despite rider, lights will stay on for standards— Advocates. Greenwire. December 16.

IALD (International Association of Lighting Designers). 2011. “Energy Codes: Moving Forward.” Memorandum dated April 12, 2011. Chicago, Ill.: IALD.

ICC (International Code Council). 2012. International Energy Conservation Code. Washington, D.C.: ICC.

IRS (Internal Revenue Service). 2012. Internal Revenue Bulletin: 2012-17. Washington, D.C.: U.S. Government Printing Office.

Jaffe, A.B., and R.N. Stavins. 1994. The energy paradox and the diffusion of conservation technology. Resource and Energy Economics 16:91-122.

Logan, J. 2008. Lighting Efficiency Standards in the Energy Independence and Security Act of 2007: Are Incandescent Light “Banned”? CRS Report RS22822. April 23.

LRC (Lighting Research Center). 2003. Increasing Market Acceptance of Compact Fluorescent Lamps (CFLs). Report prepared for the U.S. Environmental Protection Agency. September 30. Available at http://www.lrc.rpi.edu/programs/lightingTransformation/colorRoundTable/pdf/MarketAcceptanceOfCFLsFinal.pdf.

NRC (National Research Council). 2001. Energy Research at DOE: Was It Worth It? Energy Efficiency and Fossil Energy Research 1978-2000. Washington, D.C.: National Academy Press.

NRC. 2010. Real Prospects for Energy Efficiency in the United States. Washington, D.C.: The National Academies Press.

O’Donnell, J., and W. Koch. 2011. Some consumers resist ‘green’ light bulbs. USA Today. February 7.

Parfomak P., and L. Lave. 1996. How many kilowatts are in a negawatt? Verifying ex post estimates of utility conservation impacts at the regional level. The Energy Journal, International Association for Energy Economics 17(4):59-88.

Rice, A. 2011. Bulb in, bulb out. New York Times Magazine. June 3.

Sandahl, L.J., T.L. Gilbride, M.R. Ledbetter, H.E. Steward, and C. Calwell. 2006. Compact Fluorescent Lighting in America: Lessons Learned on the Way to Market. Report to DOE Prepared by Pacific Northwest National Laboratory. May. Available at http://apps1.eere.energy.gov/buildings/publications/pdfs/ssl/cfl_lessons_learned_web.pdf.

Savitz, M. 1986. The federal role in conservation research and development. Pp. 89-118 in The Politics of Energy Research and Development, Volume 3 (J. Byrne and D. Rich, eds.). Energy Policy Studies Series. New Brunswick, N.J.: Transaction, Inc.

Scelfo, J. 2008. Any other bright ideas? New York Times. January 10.

SCHER (Scientific Committee on Health and Environmental Risks). 2010. Opinion on Mercury in Certain Energy-Saving Light. Brussels, Belgium: European Union Health and Consumer Protection Directorate-General. May 18.

Silveira, G.T.R., and S.-Y. Chang. 2011. Fluorescent lamp recycling initiatives in the United States and a recycling proposal based on extended producer responsibility and product stewardship concepts. Waste Management and Research 29:656-668.

Simon, R. 2011. Texas aglow with effort to save the incandescent bulb. Los Angeles Times. July 9.

Smith, R. 2011. The new light lose a little shine. Wall Street Journal. January 19.

Sudarshan, A., and J. Sweeney, Stanford University. 2008. Deconstructing the “Rosenfeld Curve.” Working paper. Available at http://www.stanford.edu/group/peec/cgi-bin/docs/modeling/research/Deconstructing%20the%20Rosenfeld%20Curve.pdf.

Swope, T. 2010. “The Present and Possible Future CFL Market,” Presentation to the Northeast Residential Lighting Stakeholders Meeting on behalf of D&R International for U.S. DOE. March 30. Available at http://neep.org/uploads/Summit/2010%20Presentations/NEEP%20Lighting_Swope.pdf.

Thompson, E. 2011. Incandescent phase-out pushed back two years. The Vancouver Province. May 19.