Panel III

Small and Medium-Sized Enterprises and High-Value Manufacturing

Mr. Brown noted that members of Congress were especially interested in learning how programs like MEP can maximize their effectiveness in the current budget environment. The meeting so far, he said, had proven valuable in describing how the MEP program can leverage both expertise and funding across agencies. The MEP does an excellent job, he said, of disseminating new technologies and processes to SMMs.

Support for small firms and manufacturers create jobs and new products. Their greater flexibility and greater tolerances for risk allow them to innovate successfully. But, he said, many people think that innovation and efficiency displaces jobs. In fact, studies have shown that over time, innovation creates more jobs that are more productive and higher-paying. “I think that message is often lost,” he said, “and I think it’s imperative for supporters of advanced manufacturing innovation to get that message out.”

The fact that innovation creates higher-paying and more productive jobs, he said, has important implications for federal funding policy. A related point, made by an earlier speaker, is that innovation suffers when manufacturing moves offshore and removes the “side result of continuous learning.” He introduced the next speaker, Dr. Gregory Tassey, as an economist one who has studied these issues and would summarize some of the benefits of keeping manufacturing jobs in the United States.

Gregory Tassey

Economic Analysis Office

National Institute of Standards and Technology

Dr. Tassey began his presentation by observing that while most people agree that manufacturing is essential to the U.S. economy, no such agreement exists in explaining why this may be true. He said also that many economists saw no special importance in what products are manufactured; he repeated the quip that it does not matter whether we’re manufacturing potato chips or semiconductor chips, “as long as we’re manufacturing something.” Still other economists, he said, argue against producing a product in the United States if the relative prices of the world economy favor production offshore. To dispute such arguments, and the inference that the United States would do equally well as a service-based economy, he said he would propose four major rationales in favor of a strong onshore manufacturing base.22

Rationales for Strong Onshore Manufacturing

The first was diversification, which was seldom discussed in the debates over manufacturing. The United States is a large economy, and “putting too many eggs in one basket is a risky strategy. Manufacturing contributes $1.6 trillion to GDP, and employs 11 million workers. If you’re going to replace all of them with service jobs,” Dr. Tassey said, “you have to make some very convincing arguments that services can drive this economy at the rates that we want.” He said that many economists believe that services are not tradable, which is an argument that pertains to a time when a typical service was very labor intensive and needed to be produced on site. In other words, one would not send the laundry to China every Monday morning to benefit from lower wages. In fact, he said, many services are now tradable, such as customer assistance, engineering, and accounting, and some 30 countries have an explicit agenda to encourage service exports. “So if we became a service economy, we would end up having to compete just as vigorously as we are forced to do in manufacturing,” he said.

A second argument in favor of on-shore manufacturing is that it accounts for 67 percent of business and industry R&D, which represents a contribution of 11 percent of GDP. It also supports a 57 percent share of the nation’s industrial scientists and engineers. “If you remove manufacturing, you

_______________

22For a more detailed presentation of Dr. Tassey’s discussion, see Gregory Tassey, “Rationales and Mechanisms for Revitalizing U.S. R&D Manufacturing Strategies,” Journal of Technology Transfer 35: 283-333, 2010.

have decimated the research infrastructure of the private sector,” he said. This could be rebuilt over time, he said, and some services do a moderate amount of R&D internally, but that amount “pales in comparison with the amount done by the manufacturing sector.”

In addition, Dr. Tassey said, the fast-growing high-tech services sector must have close ties to its manufacturing base to fuel innovation. “There are definite co-location synergies between services and the sources of their technology,” he said. Those working in a manufacturing supply chain find increasingly important interactions with workers in related activities. “These co-location synergies,” he said, “flow between the tiers of the supply chain and ultimately the hardware and software that are used by the service industries.”

Finally, he said, the majority of the nation’s trade is in manufactured goods, but “we have not had a trade surplus in manufacturing in 35 years.” Every year of a deficit, he said, detracts from the economy’s GDP, and the projections for GDP growth in the future are “not particularly robust.”

The Impact of R&D on the Economy

Dr. Tassey returned to the impact of R&D on the economy, beginning with innovation. The innovation process begins with science, he said; the science is used to develop technology, and the technology is developed into something useful to a commercial market. “What happens after that is the key to determining economic benefits,” he said, “for manufacturing or any other sector of the economy.” That is, the product or process must be proven and scaled up to the point of reliability that meets the demands of manufacturing and the tastes of the market. “It’s only as a market expands and we in the domestic manufacturing industry capture a lion’s share of the benefits that we deliver the value-added needed by the economy.”

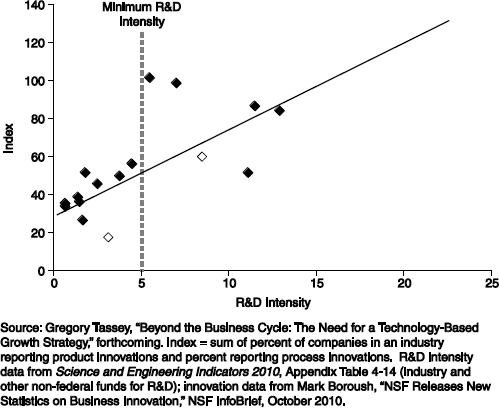

The nation has not well understood the relationship between R&D and innovation before, he said, but lately the NSF has begun to collect broad-based innovation data; the first of these data were released in the fall 2010. “So I took that data and created an index, plotted against R&D intensity,23 and there is definitely a positive correlation.”24

In addition, Dr. Tassey said, the distinction between software and hardware as products is beginning to blur, partly because software is embedded—and produced—as part of so many physical products. “So in my opinion, we’re really not talking about hardware and software, we’re talking about manufacturing.”

_______________

23In economics, R&D intensity may refer to a firm’s spending on R&D in relation to sales. In this context, Dr. Tassey is referring to R&D spending in relation to GDP.

24Gregory Tassey, “Beyond the Business Cycle: The Need for a Technology-Based Growth Strategy,” forthcoming.

FIGURE 4 Rate of innovation vs. R&D intensity.

SOURCE: Gregory Tassey, Presentation at November 14, 2011, National Academies Symposium on “Strengthening American Manufacturing: The Role of the Manufacturing Extension Partnership.”

R&D-intensive Industries

Innovation is just the first stage of commercialization, he said; economists are interested in all of its stages and the total economic impact that generates jobs, salaries, profits, and other benefits. To frame this larger picture he compared the degree of R&D intensity in manufacturing industries with real economic output for the period 1999-2007. He divided industries into two categories: R&D-intensive industries, including pharmaceuticals, semiconductors, and communications equipment, and non-R&D-intensive, including basic chemicals, machinery, and electrical equipment. He found an R&D intensity in the first group averaging 9.5, and an R&D intensity averaging only 2.5 in the second groups. He then looked at the percent change in real output between 2000 and 2007 and found a group average of 25.4 percent in the R&D-intensive industries, and a group average of just 2.9 percent in the non-

R&D intensive industries, which was attributed almost entirely to the change in output for basic chemicals.

Given the importance of R&D intensity to the economy, one might argue in favor of situating high-intensity industries in the United States, rather than offshore. In fact, the United States is in danger of losing—or has already lost—the domestic leadership it once had in high-value manufacturing sectors. Part of the cause of this loss, said Dr. Tassey, is attributable to off-shoring.

How Off-shoring Leads to Stronger Competition from Abroad

Off-shoring is a complicated process, Dr. Tassey said, which had little importance until about two decades ago, when U.S. companies were globally dominant. Then companies began to target foreign markets and to send their manufacturing abroad to be close to those markets. At first they supported just a small amount of R&D to move those products into the market. At first, this did not represent a huge loss of value added. However, as the host countries provided more of the skilled labor, they began to gain R&D experience and expanded their internal R&D infrastructures to capture synergies at the “entry” tier of the high-tech supply chain. For example, Taiwan and Korea became skilled at producing electronic components, while China excelled at assembly. In this way, those countries gradually became competitive in their own sub-markets.

The process usually begins as the country specializes in a particular tier of the high-tech supply chain. As they become successful, they begin to integrate backward along those supply chains, taking more value added from the Western economies, including the United States. This “hollowing out” of supply chains has cost the United States in value added and jobs. According to this “poor technology life-cycle management,” he said, the United States had been the “first mover” in many commercial technologies, but gradually lost virtually all market share in many of these technologies, including:

• Oxide ceramics.

• Semiconductor memory devices.

• Semiconductor production equipment, such as steppers.

• Lithium ion batteries.

• Flat-panel displays.

• Robotics.

• Solar cells.

• Advanced lighting.

At the same time, the new host economies began to integrate forward along the supply chains. One study found that 30 economies have explicit high-tech service export strategies. For example, Taiwan is integrating forward from electronic components into electronic circuits, and Korea is integrating forward

from component to electronic products. Such economies are beginning to integrate forward into services as well, so that co-location synergies are being lost by the United States and captured by others. Some observers downplay the seriousness of this hollowing out of U.S. supply chains, citing the success of the Apple model, for example, and some design-only semi-conductor firms. “I don’t consider that a viable long-term strategy,” said Dr. Tassey. “There’s nothing to stop the Asians from integrating forward into design, and they are doing it.” He cited the Android-based phone made by Samsung as a “classic example.”

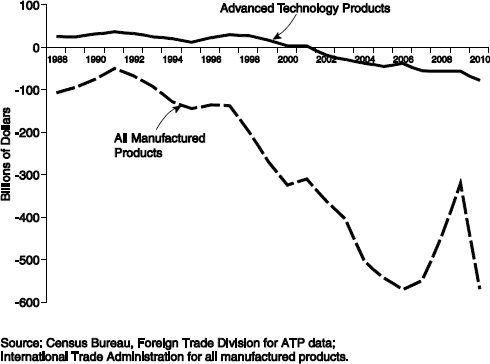

The Downturn of the High-tech Trade Balance

Historically, Dr. Tassey continued, the United States has been a world leader at innovating products for the major technology-based markets, but in subsequent market expansions it has let this leadership slip away. Within the U.S. trade balance, the figures of most interest for economic development have been those labeled by the Census Bureau as high-technology products, which amount to some 500 product codes out of 22,000 manufactured products. This

FIGURE 5 U.S. trade balances for high-tech vs. all manufactured products, 1988-2010.

SOURCE: Gregory Tassey, Presentation at November 14, 2011, National Academies Symposium on “Strengthening American Manufacturing: The Role of the Manufacturing Extension Partnership.”

high-tech trade balance was positive when the government first began tracking it in 1988, but by 2002 it had turned down. It has continued downward since then, and is now about negative $80 billion a year, with no sign of a reversal.

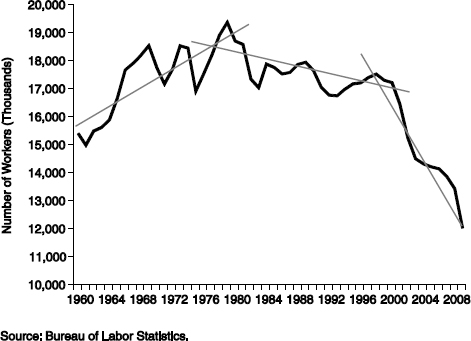

The effect of this decline shows up clearly in U.S. manufacturing employment. When the United States was dominant during the first few of decades after World War 2, U.S. manufacturing and manufacturing employment both expanded rapidly, until about 1980. For the next two decades employment lost momentum and turned downward, influenced by the economic success of Japan and then of Germany. In the last decade, the rapid growth of newly competitive economies have pushed the employment curve more sharply downward. Some people have blamed some or much of this job shrinkage on automation, he said, but automation had become a significant part of manufacturing long before the downturn began, with no noticeable effect on employment.

Dr. Tassey said he had recently participated in a seminar in Germany where he learned several interesting things. First, Germany has a trade surplus in manufacturing, in spite of having a 9 percent lower R&D intensity, a 39 percent

FIGURE 6 U.S. manufacturing employment: 1960-2009.

SOURCE: Gregory Tassey, Presentation at November 14, 2011, National Academies Symposium on “Strengthening American Manufacturing: The Role of the Manufacturing Extension Partnership.”

higher level of hourly manufacturing labor compensation, and a 12 percent higher corporate tax rate than the United States. Even so, he said, German manufacturing firms still perform far better than U.S. firms.25 “And in my opinion, the reason is they take a comprehensive, whole technology life-cycle approach to their government support of the domestic manufacturing industry. They have an extremely good educational system. I’m not just talking about college; I’m talking about high school, vocational training, and apprenticeship programs.”

Germany has also optimized its industry structure, for both large firms and SMEs, by subsidizing the transfer of skilled labor in SMEs through the Fraunhofer Institutes. “They optimized their industry structure,” he said. ”They have the highest percentage of their manufacturing value added coming from R&D-intensive industries. And this means that their competitive advantage is very likely to be more stable over the next decade or so. It doesn’t mean their strategy is perfect; I can find some holes in it. But right now they’re outperforming us.”

Trends Needing Policy Attention

Dr. Tassey then asked what policy attention those trends might inspire in the United States. First, he said, was R&D intensity, which has remained flat at 3.7 percent since the mid-1980s. This pales in comparison to truly R&D-intensive industries, whose intensities range from 5 to 22 percent. It also defies the expectation that low-R&D-intensive industries would be off-shored first, causing the overall intensity figure would rise. The need for an effective policy response to this situation, he said, is great. About $1.3 trillion are being spent globally on R&D now, he said, which is “a huge amount,” and represents even greater leverage; for every dollar of R&D and every technology produced, additional money is spent on capital formation, marketing, and other functions, raising economic growth generally. In particular, the high-tech industries account for just 7 percent of GDP, and yet that 7 percent is leveraging the other 93 percent of industries, which depend primarily on the 7 percent of high-tech industries. “So it’s incredibly important to focus on that and make it robust,” he said.

A final trend that needs policy attention, he said, is the trend of off-shoring R&D itself. U.S. manufacturing firms are off-shoring their R&D at three

_______________

25While the U.S. has one of the highest nominal corporate tax rates in the world, effective tax rates are often much lower. In this regard, a recent GAO report notes that using allowed deductions and legal loopholes, large corporations enjoyed a 12.6 percent tax rate far below the 35 percent tax that is the statutory rate imposed by the federal government on corporate profits. See U.S. Government Accountability Office, Corporate Income Tax: Effective Tax Rates Can Differ Significantly from the Statutory Rate, GAO-13-520, Washington, DC: U.S. Government Accountability Office, May 30, 2013.

times the rate of growth of domestic R&D spending. This is not a trend that can be fixed by federal intervention, he said, because government funding of manufacturing R&D increases the sector’s R&D performance intensity from 3.7 percent only to 4.1 percent.

Another important topic, he said, was the farther-on private investment that provides the necessary capital equipment, hardware, and software that leads to productive uses. This fixed private investment rose by 167.7 percent during the 1990s, due primarily to the growth in IT innovations, but during the following decade the increase dropped to 14.6 percent. “That is definitely a serious problem,” he said.

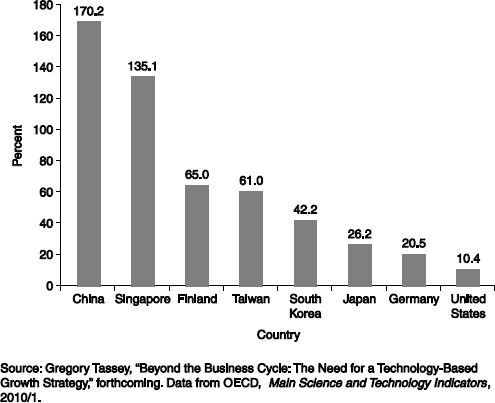

Another view of R&D intensity, Dr. Tassey continued, is its funding as a percentage of GDP. This ratio has been more or less flat since 1953. In the 1960s, there was almost no technology-based competition, whereas 50 years later the world has exploded in R&D spending to some $1.3 trillion a year, most of it in manufacturing. And yet the R&D intensity levels as a share of GDP have remained essentially the same. Industry has done its part, he said, increasing its spending steadily over that period until the last decade, when it leveled out—probably because of the off-shoring trend. “But the real villain here,” he said, “is the federal government, which has reduced its R&D funding relative to GDP for 50 years.” Globally, the United States ranks 8th in national R&D intensity. “That’s not terrible,” he said, “but it’s a trend you have to pay attention to. We were once the most R&D intensive, and now we’re slipping.”

How, he asked rhetorically, is the United States responding to this slippage? “Well,” he answered, “we’re not.” Between 1995 and 2008, the United States increased national R&D intensity by 10.4 percent, less than its major economic competitors. Much larger increases were recorded by China (170 percent), Singapore (135 percent), Finland (65 percent), Taiwan (61 percent), South Korea (42 percent), Japan (26 percent), and Germany (20.5 percent). He showed another chart comparing the manufacturing value added from R&D intensive industries. The United States ranked near the middle, exceeded by Japan, Korea, and Germany, which had the largest percentage.

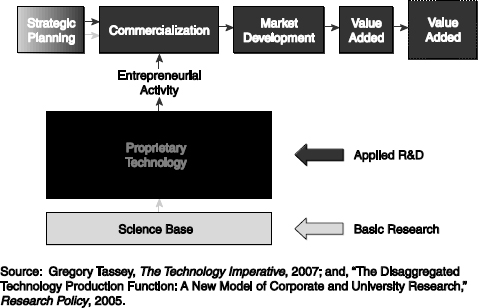

Revisiting the ‘Black Box’ Model of Innovation

The response to the underinvestment in R&D intensity, Dr. Tassey said, is commonly described in terms of technology-element growth models. The model that has been embraced by most economists and used to drive policy in this arena for decades, he said, might be called the “black box” model. It rests on a base of federal investment in science, which is considered a pure public good. This element of the model is not disputed, as the government’s responsibility for supporting basic science is generally acknowledged. However, he said, conservative economists tend not to recognize the economic importance

FIGURE 7 Changes in national R&D intensity, 1995-2008.

SOURCE: Gregory Tassey, Presentation at November 14, 2011, National Academies Symposium on “Strengthening American Manufacturing: The Role of the Manufacturing Extension Partnership.”

of this investment. Instead, they limit the source of economic growth to the “black box” of proprietary technology—such as patents—that become the raw material whereby companies, venture capitalists, entrepreneurs, and other actors commercialize a technology and add value to it. Because the proprietary technology in the black box belongs to the private sector, and the value added represents the payments to labor and the payments to corporations as profit, the model affords few leverage points for public policy.

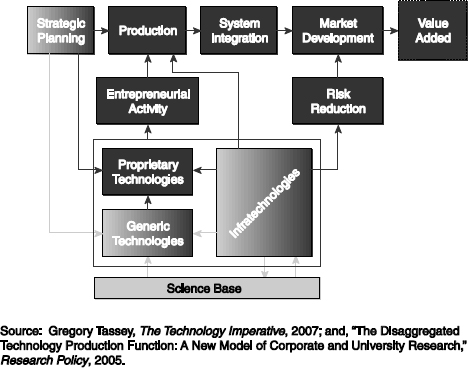

In place of this black box model Dr. Tassey proposed a model that “breaks the black box apart” into three elements, each of which responds to different needs and investment incentives. One is the same proprietary technology that dominated the original black box model. A second element is generic technologies, often known as platform technologies. These are

FIGURE 8 ‘Black Box’ model of a technology-based industry.

SOURCE: Gregory Tassey, Presentation at November 14, 2011, National Academies Symposium on “Strengthening American Manufacturing: The Role of the Manufacturing Extension Partnership.”

significant but not proprietary kinds of R&D that are usually co-funded and co-developed by public and private interests and hence considered to be quasi-public goods. The third element, called infra-technologies, includes tools that are essential in making the innovation process efficient. They include such complex elements as test methods, databases, modeling, and standards, many of which are critical for small companies but beyond their technological or financial reach.

As an example, he showed how this technology-element model would be applied in biotechnology. He showed lists of activities in each of five categories, only the first and last of which—science base and commercial products—were present in the original black box model. The three middle categories—infra-technologies, generic product technologies, and generic process technologies—were not present. “Yet in reality,” he said, “they do exist, and a simple list of these categories demonstrates how important it is for policy to recognize them and this complexity.” He also characterized this model in terms of public-technology goods, mixed technology goods, and private technology goods.

FIGURE 9 Economic model of a technology-based industry.

SOURCE: Gregory Tassey, Presentation at November 14, 2011, National Academies Symposium on “Strengthening American Manufacturing: The Role of the Manufacturing Extension Partnership.”

Underinvestment in Longer-term Technologies

The last indicator of underinvestment, Dr. Tassey said, was a shift in the composition of R&D toward shorter-term activities. The real growth has been in industry’s net investment in next-generation technologies that provide the short-term products for the domestic supply chain. This shift has been accompanied by a fall in R&D investments in technologies that might be expected to bring longer-term returns.

In planning policy, he said, it is essential to keep in mind that most federal R&D funding is directed toward agency mission objectives, including defense, space, health care, energy, and environment. National defense and health together account for 81 percent of the federal R&D budget, while only about 2 percent of the budget supports projects whose primary focus is economic growth. “While economic activity is stimulated by this skewed funding strategy,” he said, “the federal portfolio is not close to being optimized for economic growth.” An example is the category of federally funded “generic” or proof-of-concept technology research. Of the total amount, some $3.1 billion

goes to defense, $400 million to energy (ARPA-e), and only $60 million to “general economic growth” in programs that translate technologies into actual, marketable products.

In summary, he said, three important targets for manufacturing R&D policy are (1) amount of R&D, (2) composition of R&D, and (3) efficiency of R&D. The third target was increasingly important in the face of global competition. “You can’t take all day to move through a technology life cycle or you’ll find out that someone else in another country has beaten you to the market and seized the first-mover advantage.”

In closing, Dr. Tassey said that technology clusters are important “because they greatly improve the efficiency of R&D.” Clusters are most effective, he said, when they are part of a policy that is planned and sustained over the long term. “We spent a lot of years figuring out how to do this,” he said. “In the case of technology investment, it’s only through the long term that your strategy can really work. You have to come up with metrics in the short and medium terms to show decision makers that you’re making progress of benefit to participants. But only over the longer term will you get beyond benefits to participants to benefits for the national economy as a whole.”

THE DVIRC PERSPECTIVE ON THE SUPPLY CHAIN

Joseph J. Houldin

Delaware Valley Industrial Resource Center

Joseph Houldin began by clarifying that he represented the Delaware Valley Industrial Resource Center (DVIRC), the MEP of the Philadelphia area, and had never worked for an OEM or an SME. Nonetheless, he said, his goal was to discuss the relationship between OEMs and SMEs in terms of supply chains. The DVIRC had only recently become actively involved in supply chains, beginning with a partnership with the Catalyst Connection, a “sister MEP” described earlier by Petra Mitchell.

He had worked with the MEP since 1988, and said that like his colleagues, he loved the job. “I feel we’re doing something very important for the country,” he said. In light of the presentation by Dr. Tassey, he said, it was clear that the job on the ground could be done more effectively under a clearer and more comprehensive set of federal policies. “So here is a request from one of the troops in the field,” he said. “To the degree we can get a little more structure and direction from the federal level, it would be greatly appreciated.” He did say his organization received good support from the federal MEP, “which is greatly appreciated.”

Toward Collaboration Between Levels of the Supply Chain

Mr. Houldin said that he had been watching and reading about supply chains for 20 years, beginning earlier in his career when he was involved in site

location issues for economic development. Much of the discussion about industrial structure was then academic in nature, he said, but economic development people listened in to learn about the competitive advantages of certain locations. Also, other MEP organizations had looked at the supply chain as a channel through which to bring services to SMEs. They tried to do this, in theory, by encouraging larger companies to reach farther down their supply chain requirements to coordinate for certain business practices; the MEP would help support that when possible.

But there was little collaboration between levels, he said. “What we saw 15 or 20 years ago was that if the OEM was at the top of the chain and the SME was at the bottom, they were separated by many tiers.” Not only were there tiers, he said, but tentacles off the tiers, which acted as barriers to improved performance and economic growth. Today there are fewer tiers, and the SME is better able to add value to the chain through better business practices.

From the perspective of the private sector, Mr. Houldin said, the functions of the supply chain used to be limited to purchasing, cost reduction, and productivity improvement. In recent years, these functions are increasingly seen in terms of partnerships between smaller and larger companies in the form of supply chain networks and supply chain managers. This change, which is coming slowly but surely, he said, includes much more discussion of not only price, but the effect on price of logistics. “Hopefully that holds promise for the dynamic changes between larger and smaller companies.”

Pushing New Functions Down to SMEs

In addition to the challenges of price and cost reductions, other trends within which the supply chain lives, Mr. Houldin said, include how best to outsource “non-core” functions once housed within the company itself. Such actions, of course, require decisions about which functions should be considered non-core. Outsourcing does create opportunities for SMEs and reallocation of value within the chain. But it also means that many new functions are pushed down the value chain to the SMEs, including more R&D, logistics work, and just-in-time production. The SMEs may see these requirements either as part of a larger opportunity to develop new customers or as a web of challenges too complicated to deal with. The MEP, he said, can help a company work its way through such questions.

When an SME has a large customer whose priorities are not set only by price, it can receive many benefits. These include not only certifications, but also significant productivity improvements which are then owned by the SME. These improvements represent not just an exchange of dollars, but a value added to that company. Among them may be new software or IT systems, on-time delivery methods, lead-time reductions, improved design or engineering, and value added elements that are shifted down the chain or distributed through the

network. These improvements can allow the SME to create new capabilities and develop new OEM customers.

Both the nature of companies and the challenges for MEP are influenced by geography, he said. The business environment in southeastern Pennsylvania differs from that of the Midwest, for example, where OEMs tend to be large companies. In the Philadelphia/ South Jersey area, few large supply chains are driven by a single company, and fewer are driven by a single industry. About 15 years ago, a third of the firms there were small OEMs, and 2/3 were considered job shops. A job shop typically handles relatively small orders for SMEs, and may move to a new customer as each job is concluded, but they are technically considered to be a manufacturer by selling a manufacturing service.

A Trend Toward Job Shop-OEM ‘Hybrids’

The number of job shop customers in the region had recently dropped, Mr. Houldin said, as many of them had moved up to become hybrid job shop-OEM organizations. The DVIRC found through surveys that these small manufacturers usually moved up in terms not of product but of service, which is generally related to engineering. As a hybrid, he said, they are now selling problem solving abilities to larger companies; they are also selling delivery time, and charging a premium for speed. Today, he said, only about one-third of manufacturers are job shops, and one-third have moved up to become hybrids. Another third are $20 million companies that have their own proprietary product and take it to the market, domestically and globally. It is uncertain whether they can be considered an OEM, although they do sell to the end market. “There are public million-dollar companies that are doing that too,” he said, “so I think there’s something going on that makes the old industrial structure discussion more complicated than it was before.”

The good news, he said, is that many American small companies are reinventing themselves and learning how to respond to a changed marketplace where they are pushed and pulled by customers of many kinds. “We need to help change the thinking in SMEs to value providers, value receivers, and value creators.”

Linking SMEs with More Customers

Recently, the DVIRC has been included in a regional grant program to expand its work from talking with the SMEs to talking with their customers. The specific purpose of the program is to work with the building industry to determine how best to retrofit existing buildings with new technologies. The program, which began 11 months ago, is funded by the Small Business Administration, the Economic Development Agency, DoE, and MEP, and will be led by Penn State University, other universities, and large companies. Because the DVIRC works with many partners, he said, it is learning a great

deal, “which is a terrific thing for us and is going to help our clients.” Another positive feature of the program, he said, is that the thrust of the program is not to develop new systems or technologies, but to connect existing systems and technologies with manufacturers so as to bring them to market quickly. “I think that has helped move MEP into the discussion in a more aggressive way,” he said. As a result, the DVIRC is meeting with United Technologies Corp., IBM, Applied Materials, and other large firms about using technologies they already have or partnering with SMEs to help develop these or other technologies.

Mr. Houldin concluded with the suggestion that OEMs commit to “re-shoring” 10 percent of their offshore work for domestic markets whenever the business case permits. A major advantage, he said, would be to renew the connections between manufacturing and innovation capabilities, as described by Mr. Tassey earlier. He encouraged the federal government to support this suggestion with its own “Buy America” initiatives, especially those involving purchasing power and contracts for more domestic manufacturers.

BUILDING A COMPETITIVE MANUFACTURING SECTOR: HOW MEP COULD HELP

Susan Helper

Case Western Reserve University

Dr. Helper said she would present some of her own data about manufacturing, which illustrated the large number of different manufacturers that need to be served differently by MEP. “I think in general we need to talk about a different model,” she said, which can be illustrated by two futures she called “low road and high road.” These would illustrate why it is difficult for small manufacturers to succeed, she said, and what the MEP and others can do to help.

She reiterated the importance of supply chains. Because of outsourcing, many large manufacturers now depend on SMEs. For example, about a third of U.S. automobile supply employment is in firms of less than 500 employees. This accounts for about a million of the 12 million total U.S. manufacturing jobs. Another million or so people are employed in supply chains in agricultural equipment, aerospace, and other industries.

Dr. Helper’s study, the Case Western Auto Supply Chain Study, lists two primary sources of information. One was interviews with 30 firms during the summer and fall of 2010. These include first- and second-tier suppliers employing 50 to 50,000 workers. Its customers included the Detroit 3, Honda, Nissan, Toyota, and BMW. The second source was a just-completed confidential survey, funded by the Department of Labor, of auto suppliers in the United States. These included all tiers of the supply chain, as well as foreign-owned firms. The survey received 1400 responses, representing about 25 percent of total firms, and 30 percent of firms with fewer than 500 employees. These smaller firms account for about a third of employment in the auto supply chain.

“I wanted to focus not on the huge companies, like Timken or Magna,” she said, “but on the smaller suppliers of the larger companies.”

Taking the High Road: Productivity and Continuous Improvement

Of the two possible “futures” for each company in her study, she began with the “high-road” future. This “win-win-win” future was one of well-paid workers making cost-effective and sustainable products for consumers and generating profits for owners. This future embodied “sort of a theory about the nature of knowledge” in which high-road techniques harness everyone’s knowledge—not just top executives’—to achieve innovation, quality, and variety. This might be called “agile production,” she said, by which firms design, set up, debug, and produce a variety of products quickly—just in time. It no longer relies on a fixed division of labor because the product mix changes constantly; it employs people who can do more than one job, because no one knows what the next job is going to demand. She mentioned a manufacturer in Ohio that used agile manufacturing techniques that could produce and deliver a wind turbine within 24 hours for most of the United States.

The low-road strategy, by contrast, was one in which each company in the supply chain tries to profit by squeezing those who are below. This, she said, is cost-shifting—trying to have somebody else bear the costs—rather than maximize the value of the chain. “We heard this constantly in our interviews,” Dr. Helper said. “We also heard, ‘Our hands are tied,’ ‘We’d like to help but we can’t afford to pay anybody,’ and so on.”

With respect to these two strategies, she said, her data showed wide variability within industries. She said that according to data gathered by her colleague Daniel Luria, these different strategies, even within narrowly-defined industries, had different implications for innovation and the nation’s standard of living. Within the narrow industry of automotive stampers, she calculated the value added per employee. After subtracting purchase inputs, this is money that is used to pay the workforce, invest in new capital, and deliver profits to the owners. The lowest-performing 20 percent of firms in her survey in terms of value added indicated that this remaining money per worker is about $30,000. “You can’t pay minimum wage with that,” she said, “let alone re-invest.” On the high end, by contrast, firms were generating about $120,000 of value added per worker. This was used to invest in worker training, new product design, and state-of-the-art equipment. One such company paid for college for any employee, and even paid for advanced degrees for people on the shop floor who wanted to move up into management. “This indicates a viable business,” she said. Similarly, her data showed that hourly wages reflected the same breakdown. The lower-end firms were paying about $9 an hour, the higher-end firms $17. “That’s a difference between a living wage and really a poverty wage.”

Evidence that High-road Firms Succeed

Dr. Helper then examined how well the high-end companies succeeded. A key top-line strategy for them was to design their own products; the high-end group was designing about 70 percent of them, while the lower-end group designed nothing, doing only contract production. This pattern was common to many industries, she said.

She examined the innovation benefits derived from shop-floor skills (“lean” behaviors) and divided them into two aspects. The first was resource reduction, especially waste reduction and inventory reduction, both of which free up capacity. The second aspect was continuous improvement, or “kaizen,” often defined in terms of quality circles. “How to debug your products is really important to this innovation strategy that we’re all talking about,” she said.

Dr. Helper illustrated this point with data from the Michigan Manufacturing Technology Center. It showed that from 2007 to 2010, companies with consistent quality (quality + stability) generated higher productivity as measured by the percentage of products that were “good first time,” versus products that had to be discarded or debugged. In the stamping sector, for example, the lowest-productivity group of companies had a “good first time” rate of 97 percent, while the highest-productivity group had a rate of 99.97 percent. This seemingly small difference was reflected by a large difference in productivity. The value added per full-time equivalent in the first group was $55,000, while the value added in the second group was $125,000. Likewise, employee turnover was 32 percent in the first group and 0 percent in the second. She showed the same pattern in other sectors, including molding, machined parts, dies/molds/prototypes, machine tools, and electricals/electronics.

This second aspect of lean, the continuous improvement, appeared to accomplish at least two objectives. First, it provided distributed knowledge to speed de-bugging. And second, firms with quality circles, suggestion systems, and preventive maintenance were able to design a higher percentage of their products, do more R&D, and improve processes faster. Firms where employees attended quality circle meetings, for example, grew 6.4 percent in sales between 2007 and 2010, while firms where employees did not attend quality circle meetings lost 26.9 percent in sales. Firms that performed preventive maintenance grew 17.1 percent in sales over the same period, while firms that did not perform preventive maintenance lost 10.4 percent in sales.

“How do firms achieve such high productivity and high wages?” asked Dr. Helper. One point, she said, is that direct labor accounts for only 5 to 15 percent of firms’ outlays. And higher-wage workers have many ways they can reduce costs and increase revenue. The more people on the shop floor understand the purpose what they are doing, the better they understand the importance of debugging, for example. They also know how expensive a mistake can be, when shutting down an assembly line can cost $10,000 per minute. Despite these clear advantages, however, most firms reported that do not

adopt high-road policies. For example, fewer than 50 percent have quality circles or consistent preventive maintenance. Clearly, substantial barriers exist.

Barriers to the High Road: Complementarities and Externalities

One barrier to the adoption of the high road, she said, is a lack of awareness of the importance of complementarities. That is, one investment in productivity is unlikely to pay off without other, complementary investments. The ability to have an agile production system requires near-simultaneous investments in equipment, marketing, IT, and human resources. For example, the installation of advanced equipment is unlikely to pay off without the information technology that links it with all users. She offered the case of the shop foreman who is in charge of the latest IT equipment but continues to carry the schedule for the shop floor in his shirt pocket. Similarly, a company that makes the same product every day can get by with only fixed automation; today, however, when a company needs the ability to design, schedule, and produce many different products quickly, it probably needs a computerized numerical control system, and it has to train people to use it. “This is really hard for a small firm to pull off,” she said.

Another barrier to the high road is lack of awareness of externalities, such as education.26 In the old U.S. model of skill development, large companies invested in their own training and apprenticeship programs. Today the restructuring of U.S. manufacturing has weakened this custom. Large companies rely for skills instead on SMEs and shared supply chains. With each supplier selling to several automakers, automakers are tempted to “free-ride” on their rivals’ investments in training for suppliers. “If I’m GM,” Dr. Helper said, “I’m reluctant to help my supplier get better because Ford’s going to benefit.” A result is that large companies seek the best suppliers they can find anywhere, including abroad. “It’s much easier, particularly if you are constrained for cash, to just complain about who is going to invest in training, and then nobody invests.”

Training Systems for SMEs Abroad

Abroad, she said, the situation is different, where governments have invested in their suppliers and in training at all levels. “It’s not that shared supply chains here are bad,” she said, “it’s that they need to be governed differently than the way we’ve governed them in the past.” She cited Germany’s Fraunhofer Institutes as an example of a training system where even small firms

_______________

26An externality is” a cost or benefit, not transmitted through prices, incurred by a party who did not agree to the action causing the cost or the benefit.” Source: Wikipedia.org. For example, a firm may pay for a training program at a community college in hopes that graduates will come to work at the firm. This external expense may benefit another firm if a graduate chooses to work there instead.

can learn from people with deep knowledge and learn to make long-term strategies.

The MEP, said Dr. Helper, responds to these problems in several ways. One is to help firms understand complementarities by providing a comprehensive diagnosis of supply chain or other issues. Unlike many federal programs that offer only training, the MEP helps with solutions to problems it diagnoses. In particular, it directly provides lean training; she urged more emphasis on continuous improvement coaching as well. The MEP also brokers some solutions. It offers links to information about what works, such as help in translating new technology or a new management practice to make it useable by SMEs. It may also provide information sharing within clusters and help with funding.

She made a few suggestions for improvement at MEP. One was a reminder that the MEP cannot be all things to all clients. “MEP will have to solve these problems not by itself, but as part of the whole system,” she said. She cautioned that the decentralization of manufacturing makes more kinds of demands on the MEP, but urged the program to remember the priority of upgrading their clients’ skills and resources. She also commented that the MEP could make better use of data—not just the data that it collects about the success of particular projects, but about which practices actually work.

Finally, Dr. Helper also urged the MEP to deepen its relationships with universities. An obvious benefit can be to gain current knowledge about new technologies. Universities can also train field agents to translate the technologies to clients once they understand them. In addition, academic partners can help grapple with management issues, such as risk analysis and total cost of ownership. As labor costs go up, companies of all sizes face many costs of different kinds that are difficult to measure. Finally, she said, universities can lead discussions with MEP about leadership development within firms—the skills required of management to not only make positive changes, but sustain them.

THE MAGNET STORY:

FROM LEAN MANUFACTURING TO PARTNERSHIPS FOR INNOVATION

James Griffith

MAGNET

and Timken Company

Mr. Griffith, who is the CEO of the Timken Company, a century-old global manufacturing firm, said that the company had undergone a “radical transformation” over the past decade. At the turn of the century, it was an automotive supplier of bearings and other specialty steel products struggling to adapt to hard economic times. Today, Timken is a far more diverse and

profitable firm that derives less than 20 percent of its revenues from autos. During that decade it has doubled in size with the same number of employees.

The renewed success of Timken, said Mr. Griffith, difficult though it was, convinced him and other leaders that more could be done to revive the rust belt economy of northeast Ohio in which he lived. About five years ago a group of Cleveland foundations raised $30 million to invest in economic development for the region. Building on one of the nation’s first MEP organizations, the Cleveland Advanced Manufacturing Program (CAMP), they recognized that technology should be an emphasis and launched a number of initiatives. Nortech was created to bring more technology-based firms to the area. Jumpstart was designed to promote entrepreneurism. BioEnterprise took advantage of the leadership of the Cleveland Clinic to foster the growth of new biomedical firms. And all were partners with the Ohio Third Frontier, which has made high-tech investments in the state totaling at least $1 billion.

The existing manufacturers, Mr. Griffith went on, responded to this activity by wanting to clarify their own role in economic development. In response, Mr. Griffith and others led a review of the most promising opportunities. They discovered that companies that had survived and thrived as global leaders, such as Timken, Eaton, and Parker Hannifin, were now tied to global supply chains, not those of northeast Ohio. And at the SME level, they found two different kinds of companies—older suppliers struggling to determine which markets to pursue, and new, emergent bio-enterprise companies building on 21st-century technologies.

The Need for a Manufacturing Advocacy and Growth Network

The group decided to change and expand the mission of CAMP, and in 2007 renamed it MAGNET, the Manufacturing Advocacy and Growth Network. It remains an MEP, with the fundamental goal of helping manufacturers “to become more competitive and to grow.” Mr. Griffith was named Chairman, guiding the development of an organization of a staff of about 36 full-time employees and $10 million in funding from a combination of federal, state, and industry sources. It is also one of 13 Ohio Edison Technology Incubators, and a leader of the northeast Ohio economic development system. About $2 million were added to its budget from foundations, government grants (many of them cooperative with the other technology organizations), and corporations. The corporations wanted not so much to build their own supply chains as to strengthen the entire regional economy that included their headquarter cities and home terrain. The $2 million, in particular, was spent on advocating for manufacturing. This, he said, began with convincing government leaders and “hard-headed CEOs” that there was already an advanced manufacturing presence in northeast Ohio, and that an organization like MEP could increase the value and power of that presence.

Second, the funding went to strengthen the educational community, including community colleges, technical high schools, four-year colleges, and

private institutions. During the corporations’ study, Mr. Griffiths and his colleagues had examined the curricula of the 17 universities in the region and could not find the word manufacturing in any of them—“even though we were the largest piece of the economy.” The group set out to change that by encouraging educational institutions to build curricula that serve manufacturers, raise the level of workforce expertise, and promote career opportunities in manufacturing.

Moving from Lean-only to Innovation and Export Strategies

Finally, MAGNET sought to bring leading management skills together to promote not only lean practices—the early focus of MEP—but also innovation and export strategies. It has lead responsibility for serving the automotive sector. Recent steps include adding a new green enterprise development training capability through Purdue University and a new product development management service to help smaller manufacturers. Its Edison Incubator has 22 tenants, and is working to link them more closely with product engineering capabilities.

Mr. Griffith described the impact of MAGNET for FY2011: 57 events attended by 1,601 people from 791 companies; the sale of 99 fee-for-service projects; services to 551 manufacturing companies; and an economic impact including $296 million in increase/retained sales, $17 million in cost savings, $50 million in investments, and 1,382 jobs created/retained. “Five years down the path,” he said, “this thing is beginning to work.”

A Different Look from the ‘Normal’ MEP

The effort has focused on bringing a different approach than “the normal MEP,” with a different look. “And we’re now recognizing that many of these companies don’t even know what they need in the way of innovation,” said Mr. Griffith. As a result, the group was designing a new program called PRISM, the Partnership for Regional Innovation Services to Manufacturers. This is to be a “boot camp” of marketing and innovation for small companies. The first four companies are now going through a “beta test phase,” with an objective of 50 clients. It is also negotiating with two large educational institutions about how to build a new economic model for the region. This would position MAGNET as a “neural network” that connects the universities to the SMMs. The goals would be to help SMMs understand what resources are available and build within the universities the specific engineering, innovation, local, and global marketing skills needed by the manufacturers.

Scaling the MEP to the size required to drive the growth of SMEs, Mr. Griffith concluded, would take an estimated $20 million annually. “This gives some perspective on how one region is now looking at MEP,” he said, “within the larger portfolio of what is needed to transform a regional economy.”

DISCUSSION

Robin Gaster asked Dr. Helper whether the auto stamping companies she studied were hiring more workers as a result of their high-road practices. She said that this was probably happening over time, but that the main positive outcome was that they were more likely to stay in business. She added that two kinds of companies were most likely to survive the recent recession. One kind was the “really, really good companies.” However, she said that some companies proudly told her they survived because they had no fixed costs: they owned their building and their land, and they laid off their workers to await better times. Among companies that failed, on the other hand, some were well managed but caught by circumstances, such as the purchase of expensive equipment just before the recession.

Advantages of Kaizen

She added that she did have evidence about the link between kaizen—continuous improvement—and innovation. It is only a correlation, she said, but it does suggest that companies with quality circles and preventive maintenance are more likely to do R&D, to design a greater percentage of their products, and to generate a greater percentage of innovative products. “So there’s a statistical link, as well as the case studies.”

Dr. Wessner asked Mr. Griffith what he needed to make MAGNET work better “Do you have scale issues? Are you getting enough funding?” He suggested that some organizations are obsessed with “that great new company with the latest super-high-tech that will take forever to get to market, rather than supporting companies that just employ people and produce and export.” Mr. Griffith said that the board at MAGNET struggles with finding a sustainable funding model. Another struggle, he said, was that the current MAGNET metrics “are built around propagating lean.” He noted that several speakers had discussed jobs retained, but few had described jobs created. “Investments in innovation take time,” he said. “My view is that it will take a long time to rebuild the economy in northeast Ohio. We spent 50 years building an infrastructure that is bureaucratic and is now in the way of the new technology companies. We have a strategy that works if we can figure out how to put the pieces together, sustain the funding, and accurately measure the progress.”

Searching for a Sustainable Model

Dr. Wessner asked if there was enough foundation support for MAGNET. Mr. Griffiths said that “foundation support, unfortunately, is very much like government support. You get it on an annual basis. That’s not really a sustainable model.” He said the organization had just hired a person to help design such a model, and to advise on which pieces should come from government, which from foundations, and which from MAGNET itself in its

fee-for-service work. He said that Minnesota’s work in funding surveys and other work through sponsorships is an interesting model.

Dr. Wessner noted the similarities between what northeast Ohio is going through and what the U.S. semiconductor manufacturers went through in the 1980s. The semiconductor firms attracted $100 million from DARPA, which they matched in creating the consortium SEMATECH. They also received trade adjustments to stop dumping, along with signals from the government that they wouldn’t be allowed to go out of business. Those CEOs that designed SEMATECH eventually adjusted their model to go ahead without the government funding.

Mr. Griffith mentioned also the model of the steel industry, which he represented. It went through a “massive restructuring” in the late 1990s without outside help. Because it made hard decisions, exited markets where it couldn’t compete, and closed noncompetitive facilities, the steel industry in the United States is operating profitably today. “So there are lots of different ways to work your way through this. But the future of the northeast Ohio economy will be a grow-your-own kind of economy. There are some success stories of companies that have figured it out with the help of the MEP, the foundations, and some good entrepreneurial business people. It will be interesting in 20 years to come back and see what makes up this economy.”