U.S. Manufacturing in Global Context

The National Institute of Standards and Technology (NIST) Manufacturing Extension Partnership (MEP) program was founded in 1989 as a means of supporting the manufacturing sector and in particular small manufacturers. At the time, the primary challenge was seen as coming from Japan, with its high-quality and very efficient manufacturing processes. Consequently the MEP program focused much of its effort until quite recently on helping manufacturers to implement lean production processes.

This focus is evolving as rapid changes in both the global and U.S. economies are driving manufacturing firms to adapt to new circumstances. Even if their markets are strictly domestic, they face the globalization of supply chains and competition from abroad. In particular, they face productivity and marketing challenges.

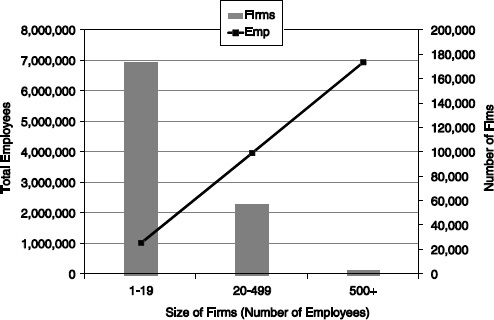

The MEP focuses most of its services on small- and medium-sized manufacturers (SMEs1). SMEs are a critical component of the U.S. economy. Recent data from the Census Bureau indicates that firms with fewer than 500 employees account for 99 percent of firms engaged in manufacturing.2 However, while small firms with fewer than 20 employees account for almost 75 percent of all manufacturing firms, they have only 9.1 percent of total manufacturing employment, compared with almost three-quarters of manufacturing employment generated by larger firms with at least 100 employees (see Figure 2-1). This has implications for MEP strategy (discussed below).

________________

1Here we have adopted the European terminology for small- and medium-sized businesses. MEP itself does not appear to utilize the associated size bands for any analytic or program purposes.

2U.S. Bureau of the Census, Statistics of U.S. Businesses,

<http://www.census.gov/epcd/susb/2008/us/US--.HTM>. Accessed July 24, 2012.

FIGURE 2-1 Total employment in U.S. manufacturing by size of firm, 2011.

SOURCE: U.S. Census: Longitudinal Business Database.

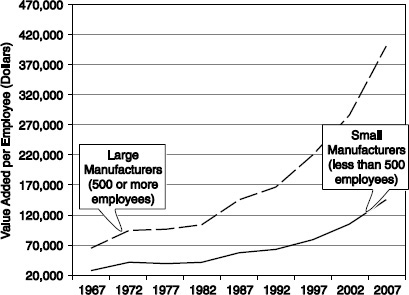

Over the past 10 years, the productivity gap between small and large manufacturers3 has been expanding. During that period, large firm productivity grew by about 300 percent (see Figure 2-2), while that of SME manufacturers has grown by 200 percent. Moreover, as large firms started from a much higher productivity baseline in 1997, the absolute gap had widened sharply and was by 2007 about $250,000 per employee.

Over the long run, as NIST MEP points out in Figure 2-2, this growing gap means that SMEs will certainly face increasing competitive pressures.4 Other changes have occurred as well. The globalization of the world economy means that even small manufacturers have the need to become more agile and better marketers as they seek a niche in lengthening supply chains. The impacts of globalization have in part driven MEP's new strategic thrust, discussed in Chapter 6, which focuses on helping companies innovate and grow rather than just cut costs (see below).

________________

3In most industries, small businesses are defined by the Small Business Administration as those with fewer than 500 total employees.

<http://www.sba.gov/content/what-sbas-definition-small-business-concern>. Accessed July 27, 2012.

4For a discussion of this divergence in manufacturing productivity, see Susan Helper, “The High Road for U.S. Manufacturing, Issues in Science and Technology, Winter 2009. She notes that higher productivity is associated with higher worker training, use of information technologies, and greater integration into high-value supply chains.

FIGURE 2-2 Value added per employee small and large manufacturers, 1967-2007.

SOURCE: MEP “Delivering Measurable Results to Manufacturing Clients,” 2009 p.3; data from U.S. Census Bureau, 2007 Economic Census: Manufacturing (November 2010), calculations by MEP. Data presented in constant dollars.

THE IMPORTANCE OF A STRONG U.S. MANUFACTURING INDUSTRY

There are a series of interrelated reasons which prompt ongoing attention to manufacturing and which set the context for understanding and probing MEP’s relevance and operation.

Manufacturing remains an important component of the U.S. economy. It contributes $1.6 trillion to gross domestic product (GDP), and employs 11 million workers, with many of the manufacturing jobs providing above average pay and benefits.5 The manufacturing sector also has powerful indirect employment effects on other sectors of the U.S. economy, supporting millions of additional supply chain jobs across the economy.

A Major Source of R&D

Manufacturing companies in the United States represent 12 percent of U.S. GDP, manufacturing and account for nearly 70 percent of private-sector

________________

5“Total hourly compensation in the manufacturing sector is, on average, 22 percent higher than that in the services sector. About 91 percent of factory workers have employer-provided benefits, compared to about 71 percent of workers across all private sector firms.” See Executive Office of the President of the United States, 2009, A Framework for Revitalizing American Manufacturing,

<http://www.whitehouse.gov/sites/default/files/microsites/20091216-manufacturing-framework.pdf>.

research and development (R&D) and 60 percent of all U.S. R&D employees.6 Reflecting this, the sector employs 57 percent of the nation’s industrial scientists and engineers.7 While some service industries do a moderate amount of R&D internally, that amount “pales in comparison with the amount done by the manufacturing sector.”8

The Largest Contributor to U.S. Exports

As an economic sector, manufacturing is the largest contributor to U.S. exports.9 In 2010, the United States exported over $1.1 trillion worth of manufactured goods, accounting for 86 percent of all U.S. goods exports and 60 percent of U.S. total exports. These exports have a direct and positive impact on job creation. “Exports contributed 46 percent to the growth of the U.S. economy between 2009 and 2011. This export surge helped create 600,000 jobs nationally in 2010, even while the rest of the economy was shedding them.”10

Linkages to Innovation

A strong manufacturing sector is also of central economic importance because of its strong linkage to innovation. Susan Helper and Howard Wial report that 22 percent of manufacturers introduce new processes to increase productivity compared to just 8 percent of non-manufacturers.11 U.S.-based manufacturing also helps to sustain an “industrial commons,” a term that describes the complex and enduring partnerships among manufacturers, universities, technical colleges, firms, research institutes, financing entities, and other links in the supply chain.12 Recognizing the importance of U.S.-based manufacturing for sustaining a robust innovation ecosystem, recent reports by the President’s Council of Advisors on Science and Technology have

________________

6See the Council of Economic Advisors, 2013 Economic Report of the President, Chapter 7, March 2013.

7National Center for Science and Engineering Statistics, Research and Development in Industry: 2006-07, Detailed Statistical Tables NSF 11–301, Arlington, VA: National Science Foundation, 2011. Available at

<http://www.nsf.gov/statistics/nsf11301/>.

8See Gregory Tassey, “The Manufacturing Imperative,” in National Research Council, Strengthening American Manufacturing: The Role of the Manufacturing Extension Partnership, C. Wessner, Rapporteur, Washington, DC: The National Academies Press, 2013.

9In order to stimulate the creation of additional jobs, President Obama’s National Export Initiative has set the ambitious goal of doubling U.S. exports by the end of 2014.

10Emilia Istrate, “Making It Here, Selling It There, and Creating U.S. Jobs,” Washington, DC: Brookings, March 8, 2012.

11Susan Helper and Howard Wial, op. cit., 2010. In general, small businesses have been found to renew the U.S. economy by introducing new products and new lower-cost ways of doing things, sometimes with substantial economic benefits. For review of the empirical evidence supporting the finding of high-innovation performance of small firms, see Zoltan J. Acs and David B. Audretsch, “Innovation in Large and Small Firms, An Empirical Analysis,” The American Economic Review, Vol. 78, No. 4, 1988, pp. 678-690.

12See Gary Pisano and Wily Shih, “Restoring American Competitiveness,” Harvard Business Review, July 2009.

Box 2-1

The Link Between Manufacturing and Innovation

Manufacturing is integral to new product development. Production lines are links in an iterative innovation chain that includes precompetitive R&D, prototyping, product refinement, early production, and full-scale production. U.S. corporations still dominate a number of industries, such as personal computers and certain semiconductors, even though end products are produced offshore. America’s logic chip-design industry, which includes companies like Qualcomm, Nvidia, and Broadcom, relies almost entirely on silicon wafers fabricated in Asian foundries, while Apple iPods, iPhones, and iPads are assembled in China by the Taiwanese firm Hon Hai Precision Industry. In such products, the greatest economic value is in software, microprocessors, and proprietary designs, while the hardware is generally comprised of standardized parts and assembled with standard production processes.

In many high-technology industries, however, design is not so easily separated from manufacturing. Production processes for advanced solar cells, lithium-ion vehicle batteries, and next-generation solid-state lighting devices are highly proprietary to the producing company and often constitute a competitive advantage. If new U.S. companies lack the domestic capability to scale up, Intel founder Andy Grove warns, “we don’t just lose jobs—we lose our hold on new technologies. Losing the ability to scale will ultimately damage our capacity to innovate.”a

aNational Research Council, Rising to the Challenge; U.S. Innovation Policy for the Global Economy, C. Wessner and A. Wolff, eds., Washington, DC: National Academies Press, 2012, p. 84.

emphasized the critical importance of advanced manufacturing in driving knowledge production and innovation in the United States.13

Linkages to Advanced Services

A robust manufacturing sector does not operate in isolation; it consumes a variety of services and relies heavily on them to operate. As a recent McKinsey report notes, “service inputs (everything from logistics to advertising) make up an increasing amount of manufacturing activity. In the United States, every dollar of manufacturing output requires 19 cents of

________________

13President’s Council of Advisors on Science and Technology, 2011, “Report to the President on Ensuring American Leadership in Advanced Manufacturing,”

<http://www.whitehouse.gov/sites/default/files/microsites/ostp/pcastadvanced-manufacturing-june2011.pdf>.

Box 2-2

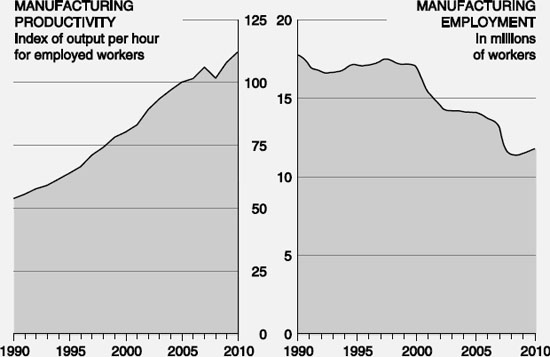

The Debate on Manufacturing Productivity Growth

Data from the Bureau of Labor Statistics show manufacturing productivity doubled between 1990 and 2010.a Over the same period, manufacturing employment fell, dropping rapidly between 2000 and 2010. Looking at these trends, many analysts concluded that U.S. manufacturing has become more efficient.

FIGURE B-2-2 Manufacturing productivity and employment 1990-2010.

SOURCE: Bureau of Labor Statistics.

Recently, some economists have disputed this view. They have sought to show that U.S. statistics may be overstating the gains in manufacturing productivity because they fail to reflect the value of imported inputs adequately in manufactured products and because they do not adequately account for the growing use of temporary factory workers.b They also note that gains in manufacturing productivity are unevenly distributed, with the significantly higher productivity in computer and electronics manufacturing masking the trends in other sectors. Foreign manufacturing and trade practices, particularly those of China in the first decade of this century, have also negatively affected U.S. manufacturing employment. Susan Houseman estimates that these measurement biases may have accounted for as much as half of the measured

growth of U.S. manufacturing output from 1997 to 2007, excluding computers and electronics manufacturing.c

aManufacturing productivity is calculated by dividing the value of U.S. manufacturing output (as adjusted for inflation and quality changes) by the number of manufacturing-worker hours.

bAccording to Susan Houseman, the integration of a variety of outsourced components in the production process makes it difficult to count U.S. manufacturing output separately. This means that price savings that U.S. factories have realized from outsourcing can show up as gains in U.S. output and productivity. Economists also note that “since the late 1980s manufacturers have increasingly used workers employed by temporary help services to work in their factories. Although they work in factories alongside manufacturers’ employees, these workers do not count as manufacturing workers in the official statistics. Yet the goods that they help produce count as manufacturing output. For this reason, some economists believe that manufacturers’ productivity is overstated when they use temporary help services.” See Susan Houseman et al., “Offshoring Bias in U.S. Manufacturing,” Journal of Economic Perspectives, 25: 111-132.

cIbid.

services. And in some manufacturing industries, more than half of all employees work in service roles, such as R&D engineers and office-support staff.” 14

Manufacturing and National Security

A strong manufacturing sector is also essential for the nation’s security; global leadership in development and production of advanced manufacturing technologies provide the basis for military superiority and preparedness. 15 However, there is growing concern that the broader deterioration of the nation’s industrial base over the last three decades (described below) has also left the United States dependent on production facilities in other nations for a variety of strategic components and systems and high-tech materials.16 Recognizing this vulnerability, the director of national intelligence has announced the preparation of a National Intelligence Estimate (NIE) on the state of American manufacturing.17

Citing these considerations, a growing number of analysts argue that maintaining a competitive onshore manufacturing sector and the associated skilled labor and technical institutions are linked and essential for long-term

________________

14McKinsey Global Institute, “Manufacturing the Future; The Next Era of Growth and Innovation,” November 2012. Access at

<http://www.mckinsey.com/insights/manufacturing/the_future_of_manufacturing>.

15See Erica R. H. Fuchs, “Innovation, Production, and Sustainable Job Creation: Reviving U.S. Prosperity,” Department of Engineering and Public Policy, Carnegie Mellon University, February 2012.

16See, for example, Richard Silberglitt, James T. Bartis, Brian G. Chow, David L. An, and Kyle Brady, Critical Materials: Present Danger to U.S. Manufacturing, Santa Monica: Rand Corporation, 2013.

17Richard McCormack, “Intelligence Director Will Look at National Security Implications of U.S. Manufacturing Decline,” Manufacturing and Technology News, February 3, 2011, Vol. 18, No. 2.

national competitiveness.18 They note that once manufacturing activity moves overseas, so do the required skills, networks, and supply chains; and once offshore they, and the learning they engender, are difficult to recover. These analysts therefore argue that it is important for U.S. policymakers to be concerned with the capabilities and composition of the economy, just as policymakers are elsewhere.19

RECENT DECLINES IN U.S. MANUFACTURING

While the United States is still the world’s largest manufacturer with a global share of about 22 percent of global output, and industrial output has risen in 2013, U.S. producers continue to face intense and growing competition from around the world. There is a growing awareness in this country that thriving manufacturers are critical to America’s economic recovery. Policymakers are increasingly emphasizing that the United States cannot completely move into a knowledge-based and services-based economy; it also has to produce tangible assets. There concerns are buttressed by a growing and authoritative concern that the erosion of America’s manufacturing and high-technology base threatens to undermine U.S. leadership in next-generation technologies.20

Sharp Declines in Manufacturing Employment

Jobs in the U.S. manufacturing sector have declined by about 8 million in the last 26 years.21 Particularly in the last decade, employment levels in manufacturing have declined steeply by about one-third. This decline, at least initially, was the result of greater competition from low-wage countries, leading to the offshoring of low-skilled jobs to lower-cost locations.22 Manufacturing

________________

18For an analysis of the linkages between manufacturing and R&D, see E. Fuchs and R. Kirchain, “Design for Location? The Impact of Manufacturing Offshore on Technology Competitiveness in the Optoelectronics Industry”, Management Science, 56(12): 2323-2349, 2010. See also Greg Tassey, “Rationales and Mechanisms for Revitalizing U.S. Manufacturing R&D Strategies,” The Journal of Technology Transfer, June 2010, Vol. 35, Issue 3, pp. 283-333; Gary P. Pisano and Willy C. Shih, “Restoring American Competitiveness,” Harvard Business Review, July-August 2009; and Ro Khanna, Entrepreneurial Nation: Why Manufacturing is Still Key to America’s Future, New York: McGraw Hill, 2012.

19For a review of current programs and policy focus around the world to support innovation-led competitiveness, see National Research Council, Rising to the Challenge: U.S. Innovation Policy for the Global Economy, C. Wessner and A. Wm. Wolff, eds., Washington, DC: The National Academies Press, 2012.

20See, for example, E. Fuchs and R. Kirchain, “Design for Location? The Impact of Manufacturing Offshore on Technology Competitiveness in the Optoelectronics Industry,” Management Science, 56(12): 2323-2349, 2010.

21This information is based on data prepared by the U.S. Census. Access at

<http://www.ces.census.gov/index.php/bds/sector_line_charts>. For additional information, see Robert D. Atkinson, 2011, “Explaining Anemic U.S. Job Growth: The Role of Faltering U.S. Competitiveness,” Information Technology and Innovation Foundation, December 2011.

22For example, one study has shown that “between one-quarter and more than one-half of the lost manufacturing jobs in the 2000s are the result of import competition from China”. See David Autor,

employment fell by 16.1 percent from 2003 to 2009, before recovering by 4.6 percent to end 2012.23

The Growing Trade Deficit

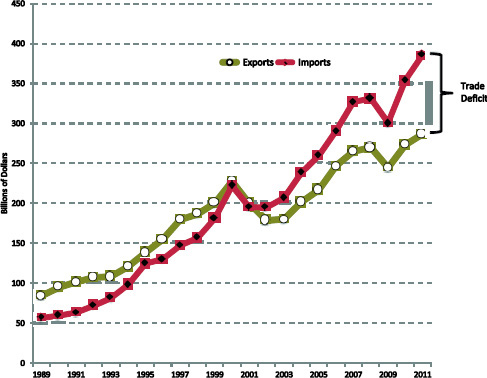

These employment and wage trends also roughly coincide with trade deficit in the U.S. manufacturing sector, which was -$585 billion in 2011.24 Americans are consuming more manufactured goods than ever, but U.S. share in production of manufactured goods is declining. Worryingly, the United States continues to lose ground in key manufacturing sectors, including those sectors that are likely to drive our economy in the future. Until 2001, the United States ran a trade surplus in “advanced technology products,” which includes biotechnology products, computers, semiconductors, and robotics. By 2010, however, the United States ran an $81 billion trade deficit in this important sector (see Figure 2-3).25 This represents a very significant shift.

The Impact of Offshoring Manufacturing

Much of the trade deficit in advanced technology is attributable to the phenomenon of progressive offshoring over the last few decades. First, U.S. manufacturers began by setting up manufacturing facilities abroad, either to be near growing markets, to make use of skilled, low-cost labor, or both. The offshore facility did a small amount of R&D in order to move products into the market. As host countries became able to provide more skilled labor, they often pressed companies to provide R&D training and expand their internal R&D infrastructures to capture synergies at the “entry” tier of the high-tech supply chain. For example, Taiwan and Korea became skilled at producing electronic components, while China excelled at assembly. In this way, those countries gradually became competitive in their own submarkets.26

________________

David Dorn, and Gordon Hansen, 2011, “The China Syndrome: The Local Labor Market Effects of Import Competition,” MIT Working Paper; econ-<http://www.mit.edu/files/6613>. Some of this decline is conventionally described as due primarily to increased efficiencies and productivity gains, though the basis for this view has been questioned by Susan Helper and Susan Houseman, among others.

23BEA. Access at

<http://data.bls.gov/timeseries/CES3000000001?data_tool=XGtable>.

24Bureau of Economic Analysis, “International Economic Accounts, Trade in Goods and Services 1992-Present,”

<http://www.bea.gov/international/index.htm>. Accessed December 2011.

25U.S. Census, Trade in Advanced Technology Products 2010,

<http://www.census.gov/foreign-trade/balance/c0007.html>.

26See Gregory Tassey, “The Manufacturing Imperative,” in National Research Council, Strengthening American Manufacturing: The Role of the Manufacturing Extension Partnership, op cit. See also Gregory Tassey, The Technology Imperative, Edward Elgar, 2009.

FIGURE 2-3 U.S. exports and imports of high-technology products in constant dollars.

SOURCE:: U.S. Census Bureau.

The Role of Foreign Applied Research Programs

Traditionally, U.S. firms have excelled in being first to acquire knowledge, thanks in large part to the steady production of good ideas through substantial and sustained federal investments in basic research. However, U.S. policy has traditionally not supported major national programs to accelerate the application of new ideas through engineering and the commercialization of new products in the market. 27

As documented in Appendix A of this report, many other countries do intervene with substantial resources and well-equipped facilities early in the product development cycle. They provide shared-use facilities, expertise garnered from working on multiple projects over long periods of time, and connections to other parts of the innovation ecosystem, be it suppliers, customers, or sources of finance, as well as a ready and low-cost source of technical support. They believe that a robust domestic industrial base, which

________________

27For a review of leading national programs to advance innovation in manufacturing in Canada, Germany, France, the United Kingdom, and Taiwan, see Appendix A of this report. For a review of foreign programs to accelerate innovation, see National Research Council, Rising to the Challenge: U.S. Innovation Policy for the Global Economy, op. cit., Ch. 6.

can produce advanced products in high volumes and the high-skilled jobs that this productive activity generates, is integral to maintaining their global competitiveness. 28

The Hollowing Out of U.S. Supply Chains

As economies specialize in a particular tier of the high-tech supply chain, they begin to integrate backward along the supply chain, taking more value added from the Western economies, including the United States. As Gregory Tassey and others maintain, this “hollowing out” of supply chains has cost the United States dearly in terms of wealth creation, high-value jobs, and technology sales. Although the United States had been the “first mover” in developing many commercial technologies, “poor technology life-cycle management,” has led to a gradual loss of market share in products such as oxide ceramics, semiconductor memory devices, semiconductor production equipment, lithium ion batteries, flat-panel displays, robotics, and advanced lighting.29

The Importance of Co-Location

There is growing recognition, based on empirical research, concerning the importance of colocation in manufacturing activity. Manufacturing in itself is desirable, playing an important role in the economy, as noted above. As noted above, while representing 12 percent of U.S. GDP, manufacturing accounts for nearly 70 percent of private-sector research and development and 60 percent of all U.S. R&D employees.30 A recent MIT institute-wide research effort reaffirms the importance of proximity to manufacturing and innovation. From extensive interviews with managers at small- and medium-sized U.S. manufacturers, the MIT researchers found that these companies “often repurpose existing technologies or techniques and apply them to make new products. And they often bundle products together with services—thus blurring the boundary between the manufacturing and service industries.” They conclude that proximity and collaboration matter in this sphere: “A key to innovation for these firms is being located in a diverse industrial ecosystem that offers many complementary resources, such as training and opportunities for collaborative research.”31

________________

28See David Cameron, Speech at the Lord Mayor’s Banquet, November 12, 2012. In his speech, Prime Minister Cameron promoted investments in innovation and manufacturing, citing their major contributions to advancing Britain’s foreign and economic policies.

29Gregory Tassey, “Rationales and Mechanisms for Revitalizing U.S. Manufacturing R&D Strategies, The Journal of Technology Transfer, January 29, 2010.

30See the CEA 2013 Economic Report of the President, Ch. 7, March 2013.

31Suzanne Berger et al., “A Preview of the Production in the Innovation Economy Report,” Cambridge: MIT Press, 2013.

For the fast-growing high-tech services sector, it is particularly important to have close ties to its manufacturing base to fuel innovation. There are co-location synergies between services and the sources of their technology. Those working in a manufacturing supply chain find increasingly important interactions with workers in related activities. “These co-location synergies flow between the tiers of the supply chain and ultimately the hardware and software that are used by the service industries.32

Moreover, as the military comes to rely more heavily on complex and advanced technology systems, retaining the capacity and knowledge necessary to manufacture these goods in the United States becomes more important.33 The ability to source critical infrastructure components, from communications equipment to power generation also affects our ability to protect against disruptions in the supply chain.34

Recent empirical research also suggests the importance of spillover benefits from manufacturing to the location and to the country in which the activity occurs. For example, a 2010 study by Greenstone, Hornbeck, and Moretti showed significant productivity gains for firms due to the development of a new manufacturing plant in the area.35 A study by Lee Branstetter in 2001 showed that spillovers tend to be intranational, captured by the country in which the activity occurs.36

The MIT Production in the Innovation Economy study cited above focuses on the interdependence between production and innovation. Their initial task force paper states that “learning takes place as engineers and technicians on the factory floor come back with their problems to the design engineers and struggle with them to find better resolutions; learning takes place as users come back with problems.” This is perhaps best illustrated by the decision of companies such as Intel or GLOBALFOUNDRIES to keep their design and some production facilities closely linked through co-location.37

________________

32See Gregory Tassey, “The Manufacturing Imperative,” in National Research Council, Strengthening American Manufacturing: The Role of the Manufacturing Extension Partnership, op cit. In its 2011 manufacturing report (op. cit. p. 11) the PCAST states: “Proximity is important in fostering innovation. When different aspects of manufacturing—from R&D to production to customer delivery—are located in the same region, they breed efficiencies in knowledge transfer that allow new technologies to develop and businesses to innovate.”

33U.S. Department of Commerce, Revitalizing Manufacturing, January 2012.

34A key goal of the Obama administration’s Advanced Manufacturing Partnership is to “jumpstart domestic manufacturing capability essential to our national security.” See Sridhar Kota, “Revitalizing American Manufacturing,” in National Research Council, Strengthening American Manufacturing: The Role of the Manufacturing Extension Partnership, op cit.

35Michael Greenstone, Richard Hornbeck, and Enrico Moretti, “Identifying Agglomeration Spillovers: Evidence from Winners and Losers of Large Plant Openings,” April 2010. Access at

<http://emlab.berkeley.edu/~moretti/mdp2.pdf>.

36Lee G. Branstetter, “Are Knowledge Spillovers International or Intranational in Scope? Microeconometric Evidence from the U.S. and Japan,” Journal of International Economics, 53, (2001), 53-79.

37For example, GLOBALFOUNDRIES $2.2 billion Technology Development Center in Malta, New York, which will be located “right next to the fab,” offers real-time advantages. This means that the same engineers that operate the fab can participate in R&D, and this proximity enables them to

Box 2-3

Losing Manufacturing and Innovation?

“The danger is that as U.S. companies shift the commercialization of their technologies abroad, their capacity for initiating future rounds of innovation will be progressively enfeebled. …The loss of companies that can make things will end up in the loss of research that can invent them.”

Suzanne Berger, Report on the MIT Taskforce on Innovation and Production, Cambridge, MA: MIT Press, 2013.

NEW OPPORTUNITIES FOR “RE-SHORING” MANUFACTURING

According to a 2012 MIT survey on re-shoring, “Manufacturing is now going through a genuine transformational period,” although the scale and permanence of this change is not certain.38 Currently, this “trend” towards re-shoring is being led by a group of relatively capital-intensive manufacturing industries including computers and electronics, machinery, fabricated metals, electrical equipment, and plastics and rubber. The MIT survey found that manufacturing firms increasingly see the benefits of offshore production being eroded by rising offshore labor costs, and shifting currency exchange rates.

At the same time, the surveyed firms cited a number of factors including lower energy costs and advances in manufacturing techniques that favor the re-shoring of manufacturing to the United States. 39 Recent years have yielded advances in hydraulic fracturing or “fracking” technology resulting in a significant increase in the supply of proven natural gas reserves and declines in natural gas prices.40 Advances in automation, additive manufacturing and nanotechnology also have the potential to shift the nature of manufacturing from

________________

“collaboratively discuss challenges—there is no substitute for right next door.” Remarks by Mike Russo, “Breaking New Ground: The New York Advantage.” Presentation at the National Academies Conference on New York’s Nanotechnology Model: Building the Innovation Economy, Troy, New York, April 4, 2013.

38MIT Forum for Supply Chain Innovation and Supply Chain Digest, “U.S. Re-Shoring: A Turning Point,” Cambridge, MA: MIT, 2012. Three hundred and forty participants completed the MIT survey, of which 198 were manufacturing-only companies. Out of those 198 companies, 156 were U.S. companies, defined as having their headquarters in the United States. “Specifically, 33.6 percent of respondents stated that they are ‘considering’ bringing manufacturing back to the United States, while only 15.3 percent of U.S. companies stated that they are ‘definitively’ planning to re-shore activities. Time-to-market and controlling costs were two main reasons for re-shoring, according to the survey.”

39TD Economics, “Onshoring, and the Rebirth of American Manufacturing,” October 15, 2012. Access at

<http://www.td.com/document/PDF/economics/special/md1012_onshoring.pdf>.

40See PWC, “Shale Gas: A Renaissance in U.S. Manufacturing?” 2011. Access at

<http://www.pwc.com/en_US/us/industrial-products/assets/pwc-shale-gas-us-manufacturing-renaissance.pdf>.

mass production of generic products towards efficient and localized production of personalized products.41

New Policy Opportunities

The MIT report on onshoring concludes that “there exists a huge opportunity for U.S. companies and policy makers to accelerate this trend and return the country to an era of manufacturing growth.”42 The federal government can help sustain this trend to re-shore through its trade, taxation, and manufacturing policies and through its investments in the nation’s research and development infrastructure.43 Major initiatives, such as the announced development of a National Network of Manufacturing Institutes (NNMI), can accelerate the adoption, refinement, and application of a variety of emerging technologies. As described below, a manufacturing strategy that includes sustained support for an improved MEP program can further contribute to the strengthening of U.S. manufacturing.

The Call for a National Manufacturing Strategy

As we have seen, a growing number of experts have called for a national strategy to support U.S.-based manufacturing. They highlight the importance of manufacturing to innovation, economic growth, and job creation, and draw attention to new opportunities to re-shore production.44 These calls are being backed by the development of new institutes to support advanced manufacturing.45 There are bipartisan bills before Congress to promote growth of the manufacturing sector, support the development of a skilled manufacturing workforce, enable innovation and investment in domestic manufacturing, and support national security.46

________________

41See the Economist, “Additive Manufacturing, Print Me a Jet Engine,” November 22, 2012.

42MIT, “U.S. Re-Shoring: A Turning Point,” Cambridge, MA: MIT, 2012.

43U.S. Department of Commerce, “Revitalizing Manufacturing,” January 2012.

44For a comprehensive review of the rationale and potential of such a program, see the prepared remarks by Daniel Eugene Sperling of the National Economic Council, “Case for a Manufacturing Renaissance,” at the Brookings Institution, July 25, 2013.

45In addition to the pilot institute for additive manufacturing headquartered in Youngstown, Ohio, competitions have been launched to create three additional manufacturing innovation institutes with a federal commitment of $200 million across five federal agencies—Defense, Energy, Commerce, NASA, and the National Science Foundation.

46On June 20, 2013, U.S. Rep. Dan Lipinski (D-IL) introduced H.R. 2447, “The American Manufacturing Competitiveness Act of 2013,” a bill that would bring together the private and public sectors to develop recommendations to revitalize American manufacturing and create good-paying, middle-class jobs here at home. U.S. Rep. Adam Kinzinger (IL-16) is the lead Republican cosponsor.

Box 2-4

The Five Pillars of the Proposed National Manufacturing Strategy

In prepared remarks at the Brookings Institution, Gene Sperling, the director of the National Economic Council described the five key thrusts of the Obama administration’s National Manufacturing Strategy.a

1. Making the United States more cost competitive for production: To make production in the United States more cost competitive, the administration has proposed tax reforms that lower the overall rates to 28 percent and 25 percent for manufacturers. Also proposed is the modernization of the nation’s infrastructure to reduce supply chain and transportation costs. The strategy also foresees seizing cost advantages from new technologies in accessing natural gas and energy resources.

2. Spurring innovation based on next-generation technologies: This includes creating a network of 15 advanced manufacturing innovation institutes to bring companies and universities, supported by federal agencies, to coinvest in world-leading technologies and capabilities. The administration also proposes to increase federal investment in advanced manufacturing R&D, as well as invest in U.S. leadership in key technologies such as bio-based products, clean energy, advanced vehicles, materials, robotics, and other platform technologies with broad benefits.

3. Strengthening skills, communities, and supply chains to attract investment: This includes investing in a skilled workforce through a proposal to create an $8 billion Community College Career Fund and initiatives to strengthen manufacturing communities through a $6 billion Manufacturing Communities Tax Credit to help regions that are suffering job losses to attract investments. In addition, the Investing in Manufacturing Communities Partnership will seek to coordinate economic development resources across the federal government to support local strategies to compete for manufacturers.

4. Access to markets: A new Interagency Trade Enforcement Center has been created to pursue trade cases more actively. The administration is also seeking new trade agreements to open foreign markets to U.S. manufactured goods.

5. Promoting investment and insourcing in the United States: This includes launching Select USA, a federal program to attract and promote investments to the United States.

aGene Sperling, “The Case for a Manufacturing Renaissance,” address at the Brookings Institution, July 25, 2013.

IN SUMMARY

There is growing and authoritative concern that the erosion of America’s manufacturing and high technology base threatens to undermine U.S. leadership in next-generation technologies and the high value-added employment gains that would follow expanded U.S. high technology production and exports. Moreover, some analysts argue that maintaining a competitive onshore manufacturing sector and the associated skilled labor and technical institutions are linked and essential for long-term national competitiveness. They note that once manufacturing activity moves overseas, so do the required skills, networks and supply chains; and once offshore they, and the learning they engender, are difficult to recover. These analysts therefore argue that it is important for U.S. policymakers to be concerned with the capabilities and composition of the economy, just as policymakers are elsewhere. At the same time, the emergence of new technologies and other favorable developments, such as shifts in energy costs, open fresh windows of opportunity for manufacturing in the United States that can to be exploited by new policies.

Given that a strong domestic manufacturing base is integral to sustaining innovation and maintaining global competitiveness in advanced technologies and critical to national security, the United States needs to augment its efforts to support U.S.-based manufacturing. The next chapters describe how the MEP contributes to this mission, and how it could be improved and expanded, based on this assessment and as well as learning from best practice lessons from leading applied research and manufacturing programs from around the world.