Japan's Unique Capability to Innovate: Technology Fusion and its International Implications

FUMIO KODAMA

JAPAN'S UNIQUE INNOVATION CAPABILITY

In 1975, the Japanese created a new word "mechatronics" by combining the two words mechanics and electronics. Essentially it implies the following two categories of products. (1) The marriage of electronic technology to mechanical technology resulted in the birth of a more sophisticated range of technological products. Typical examples are NC (numerically controlled) machine tools and industrial robots. (2) Products in which a part, or the whole, of a standard mechanical product was superseded by electronics make up the second category. Typical examples are digital clocks and electronic calculators.

In the machine tool case, the diffusion rate of mechatronics technology can be measured by the ratio of the numerically controlled machine tools to the total production of machine tools. A marked increase in the diffusion rate, in fact, occurred in 1975. Since then, diffusion has been quite rapid in this industry.

Mechatronics: A Key to Japan's Industrial Strength in the Past

Let us try to measure the diffusion of mechatronics technology in various types of machinery. A "mechatronized machine" is defined as a machine with computer control. The diffusion rate can be measured by the ratio of the mechatronized machines to the total production of machines. Those categories of machinery in which the diffusion rate of mechatronics is above 30 percent are industrial robots, machine tools, bending machines,

TABLE 1 Mechatronics Ratio and Growth Rate

|

Category of Machinery |

Percentage of Mechatronized Machines |

Growth of Production 1983/1977 |

|

Industrial robots |

80 |

10.67 |

|

Machine tools |

60 |

2.52 |

|

Bending machinery |

30 |

7.00 |

|

Printing and bookbinding machinery |

30 |

2.44 |

|

Forging machinery |

20 |

0.76 |

|

Sewing machines |

20 |

0.99 |

|

Woodworking machinery |

10 |

1.35 |

|

Plastics machinery |

10 |

2.18 |

|

Food-processing machinery |

3 |

1.71 |

|

SOURCE: MITI, Vision for Industrial Machinery (Tokyo: 1984), p. 200. |

||

and printing and bookbinding machinery. Those categories of machines that are not yet widely mechatronized are sewing machines, woodworking machinery, plastics-processing machinery, and food-processing machines.

Moreover, we can observe a significant difference in the growth of production between these two categories of machinery, as shown in Table 1. As the table clearly shows, the group with a diffusion rate of mechatronics higher than 30 percent has a higher growth rate. On the other hand, the group with diffusion of less than 30 percent has grown more slowly. Thus there seems to be a positive correlation between the diffusion rate and growth. This indicates the possibility that the group whose growth is stagnant may regain a growth momentum with the introduction of mechatronics technology.

Optoelectronics: An Emerging Capability

In the 1980s, optoelectronics, a marriage of electronics and optics, has been yielding important commercial products such as optical fiber communications systems. It united the electron with the ephemeral photon, the particle of light, to attain greater efficiency in data processing and transmission than electronics can achieve by itself. It is drastically revolutionizing the communications system and is widely expected to form the next generation of information-based technology.

In 1986, Fortune magazine asked 10 scholars, business executives, government officials, and foundation leaders in each field to rank the state of research and development in the United States, Japan, Western Europe, and the USSR on a scale of 1 to 10. The focus of the study were the following four technological fields: (1) computers, chips, and factory automation;

TABLE 2 Results of the Fortune Scoreboard

|

Technical Field |

United States |

Japan |

West Europe |

USSR |

|

Computers, chips, factory automation |

9.9 |

7.3 |

4.4 |

1.5 |

|

Life sciences |

8.9 |

5.7 |

4.9 |

1.3 |

|

Advanced materials |

7.7 |

6.3 |

6.0 |

3.8 |

|

Optoelectronics |

7.8 |

9.5 |

5.7 |

3.6 |

|

SOURCE: Gene Bylinsky, "The High Tech Race: Who's Ahead?" Fortune, October 1986, pp. 18–36. |

||||

(2) life sciences; (3) advanced materials; and (4) optoelectronics, as shown in Table 2.

As can be seen in the Table 2, there is one field in which the United States was not rated number one: optoelectronics. The magazine reported that everyone conceded that the Japanese lead the world in this important new technology, which was originally developed in the United States. In the Fortune piece, an expert commented that the Japanese lead is very considerable, and there is little evidence that anything we are doing in this country will close the gap in the near future.

Characterization: Technology Fusion

Conventional wisdom holds that technical innovation is achieved by breaking through the boundaries of existing technology. With regard to recent innovations in new fields such as mechatronics and optoelectronics, however, it would be more appropriate to view innovation as fusing different types of technology rather than as technical breakthroughs.

Therefore, we might better say that the mechatronics revolution is generated by the fusing of mechanical technology with electronic and materials technologies, and that the optoelectronics revolution is generated by the fusing of glass technology with cable and electronic device technologies. As the names mechatronics and optoelectronics imply, "fusion" means more than the summation and combination of different technologies, and implies an arithmetic in which one plus one make more than two.

The fusion of technologies goes beyond mere combination. Fusion is more than complementarities,1 because it creates a new market and new growth opportunities for each participant in the innovation process. Fusion

goes beyond the cumulation of small improvements, because it blends incremental improvements from several (often previously separate) fields to create a product endowed with some extra ingredient not found elsewhere in the market. It also goes beyond interindustry relationships, because different innovations in different industries progressed in parallel, taking the form of joint research.

NEW OPPORTUNITIES FOR TECHNOLOGY FUSION

Expected Technological Advances

Roughly every five years, Japan's Ministry of International Trade and Industry draws up a list of major fields of technology. At the last such meeting, which I had the good fortune to chair, scientists and engineers representing seven technological fields gathered together to draft the list. This time, however, we tried a somewhat different approach.

We asked the participants from each field to list those fields, outside their own, from which they are most eagerly anticipating new advances. We asked these questions of scientists and engineers who are working in corporate R&D and planning, in terms of their expectations in the short term (0–5 years) and in the long term (5–10 years).

The seven technical fields consisted of new materials, biotechnology, electronics (hardware), information processing (software), energy, aerospace, and construction/transportation; 70 scientists and engineers were sampled for each technical field. Thus we sent the questionnaire to 490 people in 231 companies. A total of 149 responses were obtained, which represents a return ratio of 30 percent. The most active response came from information processing: its return ratio was 42 percent, followed by energy (33 percent). This reflects the fact that advances in these technical fields heavily depend upon advances in other technical fields.

Table 3 summarizes the results of our survey for the short term (0–5 years). The second row from the bottom gives each field's maximum possible number of responses (i.e., the total number of respondents minus the respondents in the field itself). Expectations are reported in two rows, the third row from the bottom recording the number of respondents in other fields who indicated high expectations for developments in that field, and the bottom row expressing this number as a percentage of the maximum possible number of respondents.

According to these scores and percentages, within the next five years the greatest expectations are held for electronics (i.e., as many as 94 respondents in other fields, or 72 percent of all possible respondents, answered that they anticipate advances in that field). This is followed by new materials (85 points) and then by information processing (72 points). However,

TABLE 3 Expectations for Development Across Technological Fields

|

|

Expectations for |

||||||

|

Expectations by |

New Materials |

Biotechnology |

Electronics |

Information |

Energy |

Aerospace |

Construction |

|

New materials |

— |

2 |

15 |

10 |

11 |

9 |

2 |

|

Biotechnology |

12 |

— |

12 |

14 |

0 |

1 |

1 |

|

Electronics |

16 |

1 |

— |

13 |

4 |

6 |

2 |

|

Information processing |

11 |

3 |

29 |

— |

2 |

2 |

1 |

|

Energy |

19 |

2 |

18 |

14 |

— |

3 |

6 |

|

Aerospace |

13 |

3 |

11 |

9 |

4 |

— |

2 |

|

Construction/ transportation |

14 |

3 |

9 |

12 |

6 |

2 |

— |

|

Total (A) |

85 |

14 |

94 |

72 |

27 |

23 |

14 |

|

No. of possible respondents (B) |

128 |

130 |

130 |

119 |

126 |

131 |

130 |

|

(A/B) (%) |

66 |

11 |

72 |

61 |

21 |

16 |

11 |

|

SOURCE: Japan Society for the Promotion of Machinery Industry, ''Survey on the Interaction Among Important Industrial Technologies" (in Japanese), Tokyo, May 1990. |

|||||||

relatively little is anticipated from the fields of biotechnology, aerospace, energy, and construction.

The high marks for electronics do not need any explanation because in the last decade we have observed radical progress in microelectronics and can expect this trend to continue. The high score for information processing reflects the fact that, like genetic engineering, it is expected to provide important tools for research and analysis. Expectations vis-à-vis biotechnology remain low, however, as this area has yet to move much beyond the conceptual stage. It also reflects the disappointment of Japanese industry in the results delivered by biotechnology thus far.

The low expectations regarding aerospace and energy, however, merit particular attention. It is widely known that state-sponsored aerospace and energy projects, many of which are military related, have produced numerous breakthroughs in new materials, electronics, and software, in the form of spin-offs. The low expectations for this field, however, seem to indicate that the development of new materials and computers is generally no longer expected to follow these conventional mechanisms. New materials and computers are now expected to be developed in direct response to specific technological needs, rather than emerging in a roundabout way from defense-related projects. In the area of software, for example, it is interesting

TABLE 4 Expectation of Advances in Each Technological Area

|

|

Possible No. of Responses |

Short Term (0–5 years) |

Long Term (5–10 years) |

||

|

|

A |

B |

B/A (%) |

C |

C/A (%) |

|

New materials |

128 |

85 |

66 |

94 |

73 |

|

Biotechnology |

130 |

14 |

11 |

62 |

48 |

|

Electronics |

130 |

94 |

72 |

78 |

60 |

|

Information |

119 |

72 |

61 |

68 |

57 |

|

Energy |

126 |

27 |

21 |

45 |

36 |

|

Aerospace |

131 |

23 |

16 |

38 |

29 |

|

Construction |

130 |

14 |

11 |

16 |

12 |

|

SOURCE: Japan Society for the Promotion of Machinery Industry, "Survey on the Interaction Among Important Industrial Technologies" (in Japanese), Tokyo, May 1990. |

|||||

to note that current work on a system to regulate the electric power supply of greater Tokyo's 30 million residents is far larger than most defense systems.

Table 4 summarizes the results for the short term (0–5 years) and the long term (5–10 years), so that the shift from the short to the long term can be seen. In the longer term, great expectations are held for new materials (i.e., 94 positive responses, or 73 percent of all possible responses). Expectations for electronics fall to second place in the longer term: 78 points, or 60 percent. This reflects the widely held view that the major breakthrough will be affected only by the development of new materials, not through the application of electronics.

It is hoped that, in the future, biological processes will come to replace physical and chemical processes in various fields of manufacturing. This is reflected in the increased expectations for biotechnology in the long-term view (5–10 years). Its score increases from 14 points (11 percent) in the short term to 62 points (48 percent) in the long term.

New Materials: Designed Materials

Discussions about high technology industries often center around electronics. As far as the importance of materials is concerned, however, a growing consensus seems to be emerging among experts in various fields from various countries.

Tadahiro Sekimoto, president of NEC Corporation, has pointed out that developments in the electronics industry depend on developments in materials research. Along the same lines, Professor Hiroshi Inose, winner of the

Marconi Award for his work in digital communications, claims that the focus of technological development once shifted from systems to devices, and now it has shifted again to materials. In the United States, Ralph E. Gomory, formerly senior vice president and chief scientist at IBM, has made the point that every single step in computing has depended on solving one materials problem after another. As these comments indicate, expectations regarding advances in materials technology are greater now than ever before. Materials have clearly played an important role throughout history. How, then, are today's expectations of materials technology different from those of the past?

Throughout the history of civilization, materials gave their names to whole epochs: the Stone Age, the Bronze Age, the Iron Age. However, until recently the materials involved have been mostly nature's gifts or simple improvements on them. But now we are standing on the threshold of a new age of man-made materials, because today scientists can tailor the basic structures and properties of materials to suit their needs. Companies that lead in inventing and producing these ingredients of tomorrow will be in a strong position to dominate many high technology industries.

It is widely believed in Japan that the country is entering the age of fourth-generation materials. The first-generation materials are stone and wood, whose use entails only transforming natural resources. The second-generation materials are copper and iron, which become usable by extracting components from naturally available materials. A typical example of third-generation materials is plastics, which are not available in nature but are made by synthesizing them artificially. Fourth-generation materials will be designed according to usage by controlling the behavior of atoms and electrons in the materials, in the same manner in which we design equipment and systems.

Increasing expectations regarding new, directly applicable materials technology reflect, at least in part, a dramatic change in the nature of technological innovation in the materials field. The terms "materials design" and "custom materials" have also recently entered the scientific lexicon. This means that molecular structures can now be artificially manipulated to produce specific materials for specific uses.

Therefore, I would argue that the essence of the new materials revolution is the technology fusion between two industries, fabrication and materials, which had never been realized before. If this is the case, it can no longer be taken for granted that the Japanese materials industries are much weaker than the fabrication industries. In fact, an early indication can be found in the results of the Fortune scoreboard in Table 2, which revealed that the ratio of Japan/U.S. scores was as close as 0.82 in advanced materials, compared to 0.74 in computers and 0.64 in life sciences.

An interesting implication derived from the findings that the new materials

revolution is a product of technology fusion might be that the pattern of this revolution will not follow the conventional pattern of a materials revolution. The main actor in this revolution will not necessarily be the materials industry, but might be the fabrication industry, the customer for materials. We can find early indications of this possibility in the recent Japanese development of optical fiber technology, in which NTT, the customer for optical fiber, developed the manufacturing technology.

Biotechnology: Rational Drug Design

The concept of "technology fusion" can be extended further beyond physical sciences and chemistry. Through the emergence of biotechnology, the trend toward technology fusion is becoming obvious even outside physical and chemical sciences. The concept that corresponds to "materials design," is known as ''rational drug design" in biotechnology. The traditional way of discovering pharmaceuticals was to screen thousands of chemicals in a hit-or-miss search. This is inefficient and wastes time.2

Instead of hit-or-miss screening, the new breed of drug designers now uses biotechnology to help them work backward from what biologists know about a disease and how the body fights it. It is essentially the long-awaited combination of biotechnology and chemistry: a technology fusion that promises to streamline and enhance drug development and reshape the biotechnology and pharmaceutical industries.

These drugs should be far more effective against disease and have fewer side effects than current drugs. Dozens of companies that are zeroing in on drugs to fight nervous system disorders have used biotechnology to unravel brain function. They will likely use chemical synthesis to create their drugs.

Although the development of biotechnology is more targeted toward producing pharmaceuticals in the United States, the Japanese think of it in a broader area of application. The concept of biochemistry had long been taken for granted in Japan, because of its long tradition of fermentation technology. The situation is best illustrated by the development of glutamic acid with microbial fermentation.

During the early period of the fermentation industry's development, the primary objective was to establish a production technology based on modern sciences. And to attain it, manufacturers and laboratories competed fiercely with each other. From this development race, it was discovered that the production of glutamic acid with microbial fermentation is facilitated by the addition of cofactor substances. The principle of such metabolic

control was later established as a general technological procedure to produce lysine or other amino acids by fermentation.

Sodium glutamate was discovered as the savory component of kombu, or seaweed, by Dr. K. Ikeda in 1908 and was subsequently commercialized as a seasoning. Efforts continued to develop production processes and applications for the chemical, and those combined efforts raised the amino acid industry to its present standing.

In the 1950s, worldwide demand for sodium glutamate grew. To overcome the accompanying shortage of new materials and the accumulation of unsold by-products, a need arose to develop new processes enabling the manufacture of chemicals at a low cost with a minimum amount of byproduct. Vigorous research resulted in the development of chemical synthetic and fermentation processes and a combination of the two.

The Ajinomoto Group pioneered the invention of a manufacturing method applying chemical synthesis and a combination of the above two processes, while the Kyowa Hakko Group took the initiative in establishing a manufacturing technology based on fermentation processes. Through a fierce development race run by private businesses around 1955, solid foundations

TABLE 5 Data for Commercially Produced Amino Acids

|

Amino Acid |

Present Source |

Potential for Application of Biotechnology |

|

Arginine |

Gelatin hydrolysis |

Fermentation |

|

Aspartic acid |

Bioconversion of fumaric acid |

Bioconversion |

|

Citrulline |

— |

Fermentation |

|

Glutamic acid |

Fermentation |

De novo synthesis |

|

Glutamine |

Extraction |

Fermentation |

|

Histidine |

— |

Fermentation |

|

Leucine |

— |

Fermentation |

|

Lysine |

Fermentation (80%) |

De novo synthesis |

|

|

chemical (20%) |

|

|

Ornithine |

— |

Fermentation |

|

Phenylalanine |

Chemical from benzaldehyde |

Fermentation |

|

Proline |

Hydrolysis of gelatin |

Fermentation |

|

Serine |

— |

Bioconversion |

|

Threonine |

— |

Fermentation |

|

Valine |

— |

Fermentation |

|

SOURCE: Massachusetts Institute of Technology, 1980. |

||

were established for extraction, chemical synthesis, and fermentation processes.

Especially noteworthy was the establishment in 1956 of an industrial fermentation process for glutamic acid production by Dr. I. Kinoshita of the Kyowa Hakko Co. It turned out to be an epoch-making invention that not only brought about a major innovation in the sodium glutamate industry and in the fermentation field at large, but also had a big impact on applied microbiology.

This success triggered rapid progress in research related to amino acid manufacturing methods using microbes. Many new processes derived from these studies, ranging from a glutamic acid fermentation that used wild strains to a direct fermentation process that is applying mutant strains, and included a precursor process developed to avoid metabolic obstruction as well as an enzymatic process that is combined with chemical synthesis. As a result, it became possible to produce almost all types of amino acids with microbes, as shown in Table 5.

Further, the developmental fever coupled with the biotechnology boom in recent years is spurring the adoption of fixation enzymes, cell fusion, and recombinant DNA processes. As these are made available industrially, the progression of amino acid manufacturing technology is accelerating further.

THE EMERGING TECHNO-PARADIGM

Categories of Paradigm Shift

Many specialists have been pointing out changes in the basic pattern of technological innovation.3 With the emergence of high technology, various changes are occurring in the whole framework of corporate strategy. These changes are significant enough to merit the label ''paradigm shift." Table 6 summarizes five categories of paradigm shift.4

First, a fundamental redefinition of the manufacturing company is taking place. The manufacturing company was traditionally a site for production, and the economist's formulation is a production function: capital plus labor make things. Yet in many Japanese manufacturing companies, R&D investment is much greater than capital investment. R&D investment surpassed capital investment quite recently and the change occurred rapidly. This signals a paradigm shift; if R&D investment begins to surpass capital

TABLE 6 Five Categories of Techno-paradigm Shift

|

1. Manufacturing companies: from PRODUCING to THINKING ORGANIZATION 2. Business dynamics: from SINGLE to MULTITECHNOLOGY BASIS 3. R&D activities: from VISIBLE to INVISIBLE ENEMIES 4. Technology development: from LINEAR to DEMAND ARTICULATION PROCESS 5. Technology diffusion: from TECHNICAL to INSTITUTIONAL INNOVATION |

|

SOURCE: F. Kodama, Analyzing Japanese High Technologies: The Techno-Paradigm Shift, (London and New York: Pinter Publishers, 1991). |

investment the corporation could be said to be shifting from being a place for production to being a place for thinking.5

Second, there are changes in business. In the past, one technology used to correspond to a given company. But now, especially in Japan, technological diversification has progressed so much that it is hard to distinguish a company's principal business from its secondary business. In many cases the principal business of a company is now overtaken by its secondary business. Today's leading Japanese firms have entered the stage where they survive by adapting to the environment, relying on consistent, dependable R&D.

Third, major changes are observed in the field of research investment decision making in industry. Investment decisions are no longer based on rates of return. It is more like the principle of surf riding: the waves of innovations come one after another and you have to invest; if you miss, you are killed.6 The pattern of competition is also changing; the competitor used to be another company within the same industrial sector, but in many cases nowadays the competitor is a company in a different industrial sector. Thus high tech companies have to monitor not only direct competitors in their own sector but also firms in other industries. In effect, this means that high tech companies must engage in R&D competition with invisible enemies.

Fourth, there are changes in the technology development process. In the high tech era, the key issue of technology strategy has become not how to break through technological bottlenecks, but how to put existing technology to the best possible use. Accordingly, a day of reckoning has come for technology strategy, that traditionally has emphasized the supply side of technology development. A need has now arisen for a technology strategy which works from the demand side. In developing new strategies to meet this need, the most important element is the process of demand articulation.7 Through this process, the need for a specific technology manifests itself and the R&D effort is targeted toward developing and perfecting it.

Fifth, the barriers to technology diffusion are shifting from technical problems to institutional inertia. According to Christopher Freeman, the widespread generalization of information technology, not only in the leading branches but also in many branches of the economy, is possible only after a period of change and adaptation of many social institutions to the potential of the new technology. Whereas technological change is often very rapid, there is usually a great deal of inertia in social institutions.8

Technology Fusion as an Underlying Trend

We can synthesize those categories of techno-paradigm shift described above around the concept of technology fusion. In other words, the shift of innovation patterns toward technology fusion is a trend underlying all the categories of techno-paradigm shift.

The relationship between technology fusion and manufacturing companies' becoming thinking organizations is observable. Technical terms are increasingly being used as catch phrases for corporate identity and for defining a corporate business domain. For example, C&C (computer and communication) is used by NEC, E&E (energy and electronics) by Toshiba, and IM&M (information movement and management) by AT&T in the United States. As those phrases imply, technology fusion is clearly envisioned, and it is reported that such phrasing has helped to shift these companies' efforts into growth areas.

Technological diversification is at least a necessary condition for technology fusion. It leads to technology fusion, because technological diversification in Japan is attained through diversification of R&D. Through the technological diversification effort already made, Japanese companies have built the fundamental basis for technology fusion.

The techo-paradigm shift in R&D activities will facilitate the realization of technology fusion. One corporate strategy for insuring against the

possibility that technical problems will be solved by companies outside a given industrial sector (and that they will profit from them rather than the corporation) is to form technical alliances with companies in other sectors. These cross-sector alliances work not only as a competitive hedge against technological surprises that might be brought about by companies in different industrial sectors, but also as a device that facilitates technology fusion.

Technology fusion is intrinsic to the process of demand articulation, because demand articulation is defined as the search and selection process among technical options. When component technologies are not available within existing technical collections, a long-term technology development effort is needed. However, when demand is well articulated, development activity can be made complementary to the other technologies being developed. In other words, technological development activities through demand articulation drive technology fusion, or sometimes force it.

So we see that the changing focus of manufacturing companies, the diversification of R&D, the changing pattern of R&D activities, and the increasing importance of demand articulation are all related to the increasing importance of technology fusion in creating technologies.

NEW PARADIGM FOR POLICYMAKING

This shift in the techno-paradigm is making obsolete the policy arguments of science and technology that have hitherto been common sense in theories of business administration and international relations. As a result of a lack of full appreciation of the paradigm shift in science and technology, there are mismatches in management practices, paradoxes in economic policy9 and international disputes are becoming more pronounced. High technology may thus change the conventional wisdom in theories of business administration and international relations.

Corporate Strategy: New Technical Alliances

The inadequacy of solutions for trade friction, based on the old paradigm of trade theory, can be best illustrated by the U.S.-Japan trade agreements in two important industrial sectors: the automobile and semiconductor industries. The dispute in the former after the oil crisis added a new term to the lexicon of international trade, the "voluntary export restraint" (VER) by Japanese manufacturers, although there had been earlier versions for color televisions and steel. In fact, this is a very subtle way to avoid an inconsistency between the ideals of "free trade" and its real practices.

In the U.S. market, Japanese cars seem to dominate the mass production segment, while European makers control the luxury niche. But due to U.S. import restrictions imposed on cars, Japanese auto makers now hope to move into the luxury market, competing with the smooth-riding Mercedes Benz models. In order to replicate the well known operating comfort of Mercedes, Japanese auto makers seem to be relying on automated precision electronics technology, rather than mechanics. In other words, mechatronics is making this transition possible. Japanese auto companies are approaching the problem through a different technological trajectory—technology fusion.

In 1986 the U.S.-Japan Semiconductor Trade Agreement was signed. It was the first U.S. trade agreement dedicated to improving market access abroad rather than restricting market access at home. Unlike previous bilateral trade agreements, it attempted to regulate trade not only in the United States and Japan but in other global markets. 10

In the new techno-paradigm, however, basic high tech problems are occasionally solved by ideas or technologies born in totally unrelated fields. Leaders in technological advances come to dominate their predecessors in an established industry; revolutionary innovation coincides with a change of leadership. The change of leadership will more and more occur across national boundaries, thus making it impossible to define international competition in technological development using conventional patterns.

As the challenge for high tech leadership comes from seemingly unrelated industries, without regard to the country of origin, international agreements among companies in the same industrial sector to avoid competitive pressure could easily be rendered meaningless. Conversely, companies could form technological alliances across national and industrial boundaries, competing for development. The technological alliances between companies, that belong to different industrial sectors, and are located in different countries, might facilitate the realization of technology fusion.

Government Policy: New Research Consortia

The new technological paradigm also presents challenges for government policies to promote innovation. The evolution of Japan's government-sponsored R&D consortia in recent years illustrates how technology fusion is increasingly taken into account in Japanese policymaking. The Japanese experience may hold some lessons for U.S. policymakers attempting to structure effective support for commercially oriented collaborative research.

In the United States, precompetitive research is usually carried out at a university under the sponsorship of several private corporations. This represents a chronological, linear concept of technological innovation, in which research begins at the scientific stage and progresses through the application and development stages. In Japan, however, precompetitive research achieved through research associations is better represented by plotting industrial linkages on a graph of coordinates, in which the goal is to create engineering infrastructure as the basis for competition.11 This is especially true when it comes to the creation of fusion-type innovations.

The VLSI (very large scale integration) research association is a model of how government policy can speed technology fusion, and represented a turning point for Japanese R&D consortia. The project included all five of Japan's IC (integrated circuit) chip manufacturers at the time. In this research association, rather than focusing on the method of production itself, research efforts emphasized developing a prototype for IC manufacturing equipment.

In other words, potential users of manufacturing equipment joined together to articulate their needs. This demand articulation clarified the technical path for semiconductor manufacturing equipment, and facilitated an information flow between the potential suppliers and the IC makers. On the basis of this information, the suppliers—largely firms new to the business of semiconductor manufacturing equipment—were able to make the long-term investments necessary to enter this new field.

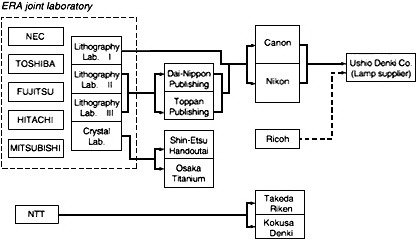

The Engineering Research Association (ERA) for VLSI existed from 1976 to 1979 and spent a total of ¥73.7 billion, of which ¥29.1 billion was paid by the government on a project funding basis. Members of the association were Fujitsu, Hitachi, Mitsubishi (Electric), NEC, and Toshiba. These five companies established a joint research laboratory within the association.

A large percentage of the research and development carried out in the joint research laboratory was subcontracted to the supplier companies, which were not members of the association. Suppliers that were heavily involved included Nikon, which developed the optical wafer stepper; JOEL, which developed electron beam lithography; printing companies, which developed lithography; and silicon crystal suppliers.

In Figure 1, major actors involved in the Japanese development of VLSI and the technical linkages among them are depicted.12 The specific activities of the association included the development of the optical stepper. The lithography research laboratory sought to reduce the electronic circuit onto the silicon base optically, not electronically. Therefore, this laboratory

Figure 1 Upstream linkages of Japanese VLSI development. Source: Fumio Kodama, Analyzing Japanese High Technologies: The Techno-Paradigm Shift, (London: Pinter, 1991), p. 89.

contracted research to camera manufacturers who owned the lens technology, and thus companies such as Nikon and Canon succeeded in developing the optical stepper.

By gathering the major chip manufacturers together, the articulation of demand for semiconductor manufacturing equipment was encouraged. In this way, technology fusion between optical and electronics technologies was realized through the efforts of demand articulation by the chip manufacturers.

The shift to technology fusion is well reflected in recent changes in the way in which research consortia are organized. The analysis of membership in research associations reveals that the average number of industrial sectors per project is increasing, while the number of participating companies per industrial sector is stable or decreasing. In other words, collective research increasingly combines firms in different industrial sectors rather than different companies within the same industrial sector.13

TABLE 7 Classification of Member Enterprises by Industrial Sector per Engineering Research Association

|

Time Period |

Number of Projects |

Number of Industrial Sectors per Project |

Number of Registered Companies per Industrial Sector |

|

1961–1964 |

3 |

3.0 |

3.2 |

|

1965–1969 |

0 |

— |

— |

|

1070–1974 |

13 |

2.2 |

3.0 |

|

1975–1979 |

14 |

3.4 |

3.4 |

|

1980–1984 |

35 |

3.9 |

3.3 |

|

1985– |

23 |

4.3 |

3.2 |

|

Total |

88 |

3.6 |

3.2 |

|

SOURCE: I. Shirai and F. Kodama, "Quantitative Analysis on the Structure of Collective R&D Programs by Private Corporations in Japan, NISTEP Report No. 5" (Tokyo: National Institute of Science and Technology Policy, August 1989). |

|||

For the entire 30-year history of the research association system, the average number of industrial sectors per project is 3.6, and the number of participating companies per project is 3.2. The research associations are divided into six cohorts based on the date of establishment. The time periods for the six cohorts are shown in Table 7. The average number of industrial sectors represented in the 13 research associations established between 1970 and 1974 is 2.2 sectors per project. This number has increased steadily since. It has risen to 4.3 sectors per project in the 23 research associations established after 1985.

On the other hand, the average number of participating companies per industrial sector has held steady at about three. This illustrates the shift in how research consortia are organized. In the past, collective research was organized mainly among companies belonging to the same industrial sectors. However, it is now being organized among companies in different sectors.

Over the past several years, the Japanese government has indicated that it intends to go further along this path. ISTEC, the International Superconductivity Technology Center established in 1988, was one of the first Japanese consortia to invite foreign participation. A wide range of industries are represented as members, including service industries such as banking. The importance of foreign participation to future collaborative research in Japan is indicated by steps the government is taking to make it easier for foreign firms to join Japan's national projects, and by the fact that the

Intelligent Manufacturing System, micromachine, and other new programs were conceived as international projects.

In terms of technology fusion, we make the following interpretation: the networking of different kinds of ''technological competence," 14 owned by different companies in different industrial sectors and different countries, is being created by government-organized research consortia. In this way, policy can play the key networking role of matching competencies and needs. The benefits of the consortia go beyond the R&D subsidy value, because networks are formed more quickly than if the initiative had been left entirely to the firms themselves. Technical and market information exchanged through these relationships will lead to faster corporate investment in innovation.

Japan's experience has relevance for U.S. policymakers. The U.S. government has increased support for collaborative research in recent years. Examples include SEMATECH, the Department of Commerce's Advanced Technology Program, and the Department of Energy's battery consortium among the Big Three automakers. If the Japanese experience is valid and if technology fusion is facilitated by wide industry membership in collaborative research, the United States might benefit from focusing on bringing a variety of competencies into consortia.

The American position on foreign participation in government-sponsored collaborative research is unclear at this point. But increasingly, technical competencies are found in firms throughout the world. Therefore, by excluding foreign nationals from government-sponsored research consortia, a country risks limiting technology fusion. It should not be assumed that a country can cover the entire spectrum of needed technological competence. The inclusion of foreign companies that have unique technical competence, therefore, might enhance the probability that global technological networking will result in heightened technology fusion in fields in which domestic organizations do not have high competence.