6

Health Care Costs: More Questions than Answers

Optimum "stress" results when the carrot is just a little way ahead of the donkey—when aspirations exceed achievement by a small amount.

James March and Herbert Simon, 1958

Given the gap between aspirations and achievements in controlling health care costs, Americans clearly are experiencing more than optimum stress—and have been for some time. Surveys of employers and the population at large consistently show that high costs are the number one health care concern. For example, in the EBRI-IOM poll conducted by the Gallup organization in late 1991, half the respondents cited cost as the biggest health care concern facing families (see Appendix A). Four-fifths cited cost as the biggest health care concern for society as a whole. Surveys also indicate that people tend to greatly underestimate national health care spending and to greatly overestimate the portion of total spending accounted for by their out-of-pocket spending rather than by direct government or business financing (Immerwahr, 1992).

Among small employers, costs are often a determining factor in decisions about whether to offer health benefits. Among large employers, the increasing share of employee compensation and after-tax income consumed by health care costs has stimulated a shift from relatively passive monitoring to more active involvement in health benefit management.

For more than two decades, concerns about high and escalating medical care expenditures and strategies to control those costs have been a major focus of health policy. The continuation of the former and the ineffectiveness of the latter not only have made it more difficult to extend health coverage to those now uninsured and underinsured but also have been partly responsible for the growth of this pool. Further, inexorably rising costs threaten—it is claimed—the solvency of federal, state, and local govern-

ments, the competitiveness of U.S. industry, the productivity and health of the U.S. work force, and the health and financial security of tens of millions of Americans. In one analysis or another, all parties—government, employers, insurers, health care providers, and consumers—have been held responsible in varying degrees for creating "the cost problem" and have been assigned some role in solving—or, more realistically—mitigating it. The structure of health care financing and delivery and its consequences now rank among the most examined aspects of U.S. social policy.

Although two decades of public and private cost containment initiatives have produced considerable institutional, administrative, and regulatory innovation and some successes, the rapid growth persists in real expenditures for medical care relative to spending for most other goods and services. Both public and private decisionmakers have viewed this result with intense frustration and a shaken faith in medical professionals and nonprofit providers of health care and health benefits as reliable agents to keep costs at "reasonable" levels. Judgments now abound that health care costs are out of control.

It must be remembered, however, that concern about rising health care costs is shared by countries with quite different health care financing and delivery systems. This suggests that the forces behind increased spending may be less related to institutional structures than to other factors such as advances in biomedical science and medical technology and changing perceptions about what medical care is appropriate.

This chapter analyzes key trend data, examines the rather different cost containment paths taken by the public and private sectors, reflects on the nature of markets in health care and health insurance, and presents a reformulation of the questions that should be asked about health care costs. This reformulation recognizes that the health and well-being of the population is the yardstick against which the cost and provision of medical care must be assessed. The key issue is the value received for health care spending compared with the value that could be expected from other investments in population well-being.

Fortunately, U.S. employers, government decisionmakers, clinicians, and others have become more interested in the question of value and are supporting efforts to improve its measurement. Unfortunately, there are at this time insufficient data to reach clear conclusions about the overall value associated with this country's high level of spending or the value added by current increases in health care spending. Many efforts to evaluate the impact of various cost containment strategies focus on dollars, not health outcomes. Some data suggest that certain strategies may reduce particular kinds of spending, in particular, spending for hospital care. Evidence is, however, sparse about successful methods to cut overall spending or control the rate of increase in health care spending. There are also inadequate data

to support straightforward judgments about the relative effects on costs and value of granting or precluding a major role for employers or of emphasizing regulation or competition to control costs.

HEALTH CARE SPENDING: TRENDS AND EXPLANATIONS

Americans are reminded almost daily that total health care expenditures are high and increasing. In 1991, total health care spending exceeded $666 billion and made up over 12 percent of the gross national product, up from 9.2 percent in 1980 and double the level of the 1960s. No other nation devotes such a large fraction of its resources to health care.

For the past three decades, personal health care spending has exhibited double-digit rates of annual growth in the United States, as it has in many other economically advanced nations (see Table 1.3 in Chapter 1). In real terms (adjusted for economywide inflation), U.S. spending grew at a rate of 4.4 percent during the 1980s, compared with 5.4 percent in the 1970s and 6.9 percent in the 1960s (Levit et al., 1991). Adjusted for inflation, personal health care spending has risen 143 percent in the last two decades, while real disposable income rose only 74 percent (Economic Report of the President, 1992). Inpatient hospital spending grew at a somewhat slower rate than overall spending, whereas spending for outpatient hospital services and physician services grew more quickly (CBO, 1992d).

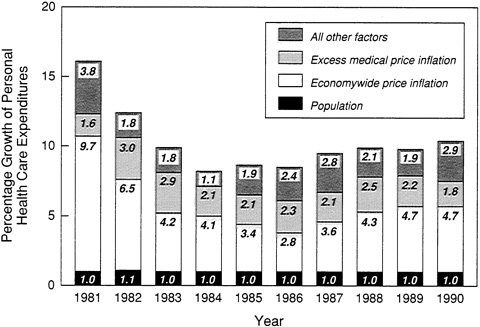

The standard analyses of health care spending identify three broad sources of increased expenditures—population growth, economywide price inflation, and excess medical price inflation—plus a fourth residual category that includes changes in such factors as the intensity and volume of medical services (Jencks and Schieber, 1991; Levit et al., 1991; ProPAC, 1992; Thorpe, 1992a). Figure 6.1 breaks down spending increases for each of the last 10 years using these categories. Overall, about 45 percent of growth in personal health care spending over the last decade is accounted for by general price inflation. Another 10 percent of the increase reflects population growth. Over one-fifth of the growth is attributed to increases in medical care prices in excess of general inflation, and the residual fifth is attributed to increases in the volume and intensity of services and other unidentified variables.

Unfortunately, measurement problems make it difficult to distinguish the effects of increased medical care prices and increased medical care quality on increased total spending and to judge trends in productivity appropriately (Cleeton et al., 1992; CBO, 1992a; Newhouse, 1992). The primary measure of medical care prices, the medical care component of the consumer price index, suffers from several weaknesses. First, it does not adjust for changes in the quality of the medical care product, such as when

FIGURE 6.1 Reasons for growth in personal health care expenditures, 1981 to 1990. SOURCE: ProPAC, 1992. Based on data from Health Care Financing Administration, Office of the Actuary.

a new drug, test, or procedure has fewer adverse side effects than its predecessor. Second, the medical care price index focuses on hospital days and physician visits rather than the episode of treatment for a medical problem. Thus, a new surgical strategy that allows quicker hospital discharges and reduced total costs may be perversely registered as increasing costs on a per diem basis (because the early days of a surgical stay are usually the most expensive). Third, the components of the index (i.e., hospital, physician, dental, and drug prices) are weighted on the basis of out-of-pocket rather than total (including insured) expenditures; this means the index is probably not a good deflator for overall national health care spending. Fourth, the index uses providers' charges for services rather than what purchasers actually pay, which is often less—especially in today's world of discounted, negotiated, and per case payments. Given these problems, it might be more appropriate to combine Figure 6.1's medical price inflation category with the residual category.

Only a modest portion of increased health care spending has been attributed to the aging of the population, increased insurance, or rising administrative costs (Fuchs, 1990; CBO, 1992a,d; Newhouse, 1992). On the other hand, most observers assume that new, advanced medical technologies—

from organ transplants to magnetic resonance imaging—have contributed significantly to health care cost escalation, although this assumption is difficult to document explicitly (Altman and Wallack, 1979; Garrison, 1991; Weisbrod, 1991; CBO, 1992a; Newhouse, 1992). In most analyses of the factors contributing to cost increases, changes in technology are not examined directly. Rather, they tend to be both intermingled with price effects (e.g., when an expensive CAT scan substitutes for an X-ray) and treated as part of a residual category to the extent that they add to the volume of medical procedures and services (e.g., when both an expensive CAT scan and an expensive MRI are substituted for or added to a less costly and generally less useful X-ray). Nevertheless, several recent analyses suggest that the development and use of new technologies—more than the increasing use of existing technologies—constitute a major source of cost increases (Schwartz, 1987; Weisbrod, 1991; Berenson and Holahan, 1992; CBO, 1992a; Newhouse, 1992).

Public and private financing and management practices are also cited as major contributors to the ''cost problem," although these factors may more easily explain high levels of health care spending than the recent escalation in the rate of health care expenditures. The practices commonly mentioned in this regard include provider payment systems that do not encourage the efficient use of resources (e.g., open-ended retrospective third-party reimbursement), insurance coverage and tax subsidies that may encourage excessive consumption, increasing malpractice litigation, excess capacity in hospital beds and in certain medical specialties, nonprice competition among providers, the ability of practitioners and providers to generate demand for an even broader set of medical services, and the difficulty of conditioning the spread of new technologies on demonstration of their cost-effectiveness. The public views such explanations of high costs as implying greed and waste on the part of physicians, drug companies, and insurers, and this viewpoint tends to limit the public's support for cost-cutting strategies that focus on any other target (Immerwahr, 1992).

PUBLIC AND PRIVATE RESPONSES TO ESCALATING HEALTH CARE COSTS

The current policy preoccupation with medical care costs is primarily a product of the last quarter century.1 Before the late 1960s, both public and private sector decisionmakers concentrated on expanding the supply of medical services (both physicians and hospitals) and widening access to these ser-

|

1 |

Much of the discussion in this section follows that presented in IOM (1989). Chapter 2 of this report describes early strategies to contain health benefit costs. |

vices. Concerns about rising health care costs were relatively muted, perhaps because everyone was satisfied with the results: more readily available services, more effective treatments for many specific medical problems, and better protection against medical care expenses. A rapidly growing economy also helped by providing new resources for a wide range of private and social needs.

As noted above, all this has changed dramatically. At least three major developments differentiate the periods before and after 1965. The first is the entry of government as a powerful force for both cost escalation and cost control following the adoption of Medicare and Medicaid in 1965. Federal and state spending for health care services and supplies rose from just under 25 percent of total public and private spending on health care in 1960 to over 40 percent by 1990 (Levit et al., 1991). The nation's governments, which also provide health benefits for their own employees and direct medical services to various special populations (e.g., veterans), have become the largest purchasers of medical care. An understanding of government cost control activities has become especially important because governments have a central role both as purchasers in their own right and as regulators of social transactions. Intentionally or not, their policies and programs can have positive or negative effects on private purchasers. The most widely cited example of a negative effect is so-called provider cost shifting, which is discussed below. A positive example is the development of tools or models for cost containment that private payers can use, for example, research on the effectiveness of alternative ways of treating specific health problems.

The second development was the beginning of serious efforts by private employers to control their expenditures for employee health benefits. Excluding public employers' premiums for employee health benefits and private employers' contributions to Medicare, private employers accounted for about one-quarter of total spending for health care services and supplies in 1990.

A third development was that forceful arguments began to be made that market competition—not government or community-oriented private programs—should be the primary vehicle for making health care effective, efficient, and affordable (see IOM, 1975, for several early formulations of the regulation versus competition debate). Community and regulatory strategies have by no means disappeared, but they have undoubtedly lost ground in recent years. On the other hand, proponents of market-based strategies generally argue that their approaches have been the subject of much talk but little real action.

The following sections examine a broad array government and employment-based initiatives to contain health care costs. Researchers' conclusions about the impacts of these programs are briefly summarized.

Government Initiatives

In the words of one historian, "Medicare gave hospitals a license to spend" (Stevens, 1989, p. 284). Government efforts to limit that license have proceeded along various fronts with mixed results.

Attempts to Control the Use, Price, and Supply of Medical Services

The preamble to the Medicare legislation prohibited federal "supervision or control over the practice of medicine or the manner in which medical services are provided" (P.L. 89-97). Consistent with this preamble, the government required and initially relied on hospitals and extended care facilities to operate utilization review committees to ensure the medical necessity and quality of care "without involving government in day-to-day hospital operations" (Mills, 1968). Rather quickly, however, policymakers came to view delegated utilization review as ineffective, "more form than substance," and moved to require Medicare's fiscal agents to undertake utilization review (U.S. Senate, 1970; Law, 1974; Blum et al., 1977). Medical and consumer groups were soon complaining, however, because this latter review process sometimes resulted in denial of payment after care had been rendered.

Before these complaints about utilization and quality review were addressed, the government acted on another front: medical care prices. August 1971 saw the start of the Economic Stabilization Program (ESP), a three-month federal freeze on all prices and wages. In the health sector, ESP controls applied in one form or another until April 1974, affecting provider charges to private as well as public payers. The end result of wage-price controls, in one evaluator's assessment, was considerable effectiveness in "reducing rates of increase in hospital employees' wages but [little impact] . . . on hospital costs" (Ginsburg, 1978). Although wage-price controls were a distinctively governmental strategy imposed on the private sector, they still left private health care providers and health insurers with substantial discretion about what services would be provided and covered.

In the middle of the wage-price control program, Congress enacted the Social Security Amendments of 1972 (P.L. 92-603), a multipronged effort at health care cost containment (U.S. Department of Health, Education and Welfare, 1976). The legislation included provisions for

-

regulation of capital expenditures through Section 1122, which provided that health care facilities would not be reimbursed by Medicare for certain expenses associated with capital expenditures that were inconsistent with state or community health planning criteria,

-

state initiatives under Section 222 to establish hospital rate-setting programs,

-

community-rather than hospital-based utilization and quality review mechanisms to be applied by Professional Standards Review Organizations (PSROs) to care received by Medicare beneficiaries, and

-

a Medicare economic index designed to limit the rate of increase in Medicare payments for physician services.

The capital expenditure provisions of the 1972 act were reenforced by the Health Planning and Resources Development Act of 1974 (P.L. 93-641), which attempted to strengthen state and community capacity to plan and control major capital investments in health care (Cain and Darling, 1979; IOM, 1981; Bice, 1988). This law viewed health care rather like a public utility or at least a service vested with a special community interest. The community, with the involvement and support of employers, insurers, unions, providers, and other local interests, would agree on the basic shape of the health care system and would influence the flow of available resources into areas of need, using its authority to grant certificates of need (CON) for certain major capital investments. Employers, employees, and the community generally—not just government as a purchaser—would benefit by better distribution of resources and restraint on the contribution of increased supply of resources to increased demand for services.

In the late 1970s and early 1980s, faith waned that this type of community-based planning and capital control—given its limited authority and the economic and other community incentives for resource expansion—could ever constrain costs (Salkever and Bice, 1978; Steinwald and Sloan, 1981). Much of the federal and state legal framework for health planning was abandoned as incompatible with newly popular market-oriented proposals for cost control. Nonetheless, about three-quarters of states still have some kind of CON legislation (Garrison, 1991). One recent analysis suggests that CON laws did affect the spending for inpatient hospital care and had mixed effects on the proliferation of certain advanced technologies (Lewin/ICF and Alpha Center, 1991).

Like health planning and wage-price controls, the Section 222 rate-setting provisions were, to a considerable degree, aimed at communitywide cost containment. They helped prompt more than 30 states to adopt some kind of hospital rate-setting program (Anderson, 1991a). Only a few of these programs were mandatory, and fewer still received waivers from HCFA to operate programs that applied to all payers within the state, including Medicare and Medicaid. Only one of the all-payer programs, that in Maryland, remains in place. Several studies have concluded that mandatory rate-setting programs can limit hospital cost increases, although program results are less consistent across states when the measure is the rate of increase in hospital costs per

capita rather than per admission or per day (see Rosko, 1989; Anderson, 1991a; and Garrison, 1991, for summaries and citations of the research literature). The 1980s emphasis on Medicare prospective payment for hospitals (and on competition as the preferred vehicle for communitywide cost containment) reduced federal government support for state rate-setting programs.

At about the same time that the above regulatory strategies were being formulated, what was to become a dominant federal argument for market-oriented strategies began to manifest itself in the promotion of health maintenance organizations (HMOs). The term HMO was coined in 1970 when Paul Ellwood argued—with great impact—that prepaid comprehensive health care could restructure incentives to reward health care practitioners for keeping people from getting ill or returning them to health as quickly as possible (Ellwood et al., 1971; Ellwood, 1975; Starr, 1982). It was an alternative to existing fee-for-service medicine and a way of avoiding a government-based health plan. The government first encouraged HMO enrollment options for Medicare beneficiaries, then, in 1973, it established administrative, financial, coverage, and other requirements that organizations had to meet to become federally qualified and it provided grants, loans, and training programs to encourage the growth of HMOs. More important, the government required that employers with more than 25 employees offer an HMO option if the employer was approached by a local, federally qualified HMO (a requirement that under more recent legislation will expire in 1995). It also acted to supersede state laws that had limited the growth of prepaid group health plans.

For a variety of reasons, employees have proved to be a more amenable target for enrollment in HMOs than have Medicare beneficiaries. In 1991, only about 7 percent of Medicare beneficiaries were enrolled in an HMO or other coordinated care plan (to use the currently preferred term), compared with over 15 percent of the entire population and perhaps 30 percent of employees (GHAA, 1991; Hoy et al., 1991; Wilensky and Rossiter, 1991). Overall, government regulations and other activities have almost certainly been a major factor behind the growth in employment-based enrollment in HMOs and other network health plans. Evidence about the impact of these plans on costs is discussed in the next section of this chapter.

In 1982, Congress, once again dissatisfied with the track record of Medicare utilization review programs, replaced PSROs with statewide "utilization and quality control peer review organizations," PROs for short (P.L. 97-248) (IOM, 1976; Congressional Budget Office, 1979, 1981; Gosfield, 1989). These new organizations built in many ways on the PSROs, which had refined many of the data collection and analysis techniques used later by both public and private purchasers (Gosfield, 1975; Blum et al., 1977; Nelson, 1984; Ermann, 1988; IOM, 1990b). As their full title suggests, PROs have an explicit quality assurance mission as well as a cost contain-

ment role. Although PROs do sell services to private employers (and Medicaid), they generally are not major actors in this arena. In contrast to the private sector utilization review programs described below, PROs have been subject to little evaluation of their effectiveness.

The Move to Prospective Payment

Quality and utilization review by PROs was intended to supplement and monitor another legislative reform of 1982 that most observers viewed as much more important: the initial shift away from cost-based reimbursement of hospitals toward prospective payment. A year later in 1983, P.L. 98-21 established a prospective per case payment system (PPS) for hospitals that became fully effective in 1986. Limited data suggest that perhaps one-third of private network health plans make some use of a diagnosis-related group (DRG)-based payment method (ProPAC, 1992).

In addition, in 1989, Congress adopted a new physician payment methodology for Medicare (P.L. 101-239), a fee schedule set according to a resource-based relative value scale (RBRVS) with certain geographic and other adjustments (PPRC, 1990). It became effective in 1992.

Although the physician payment changes are too recent to be evaluated, several evaluations of the hospital payment system are available (Russell, 1989; Coulam and Gaumer, 1991; ProPac, 1992). One recent summary of these evaluations concluded that PPS "appears to have been successful in controlling its own benefit costs, without shifting the burden to beneficiaries" but to have had "little ultimate success in controlling the overall growth in U.S. health care expenditures" (Coulam and Gaumer, 1991, p. 62). Similar but less consistent findings are reported for the hospital rate-setting programs established by states before the adoption of PPS. A limited amount of research related to Medicare prospective payment suggests it might help constrain selected cost-adding technologies (e.g., cochlear implants, for which HCFA declined to provide a device-specific DRG) and encourage certain cost-cutting technologies (e.g., reusing disposable medical supplies) (OTA, 1984; Kane and Manoukian, 1989; IOM, 1991; Weisbrod, 1991).

Payment Adequacy and Cost Shifting

As noted in Chapter 5, some observers worry that the hospital prospective payment system does not adequately consider differences in patient severity within DRG payment categories. The result may be underpayments to institutions that care for disproportionate numbers of these patients and associated hospital efforts to avoid or dump such patients. A related concern about government programs has been that they are generally reducing payments to health care providers below cost and inducing providers to

shift some of the cost burden to other employer and individual purchasers of health care.

A recent analysis for the Prospective Payment Assessment Commission (ProPAC, 1992) indicated some of the dimensions of the so-called cost shifting problem. It showed that Medicare covered only about 90 percent of Medicare patients' hospital costs, whereas Medicaid covered only 80 percent of its patients' hospital costs. Across the various state Medicaid programs, the same analysis showed wide discrepancies. Medicaid payments covered 56 percent of Medicaid patients' hospital costs in Illinois and 59 percent in Oregon but 104 and 102 percent in Maryland and New Jersey, respectively. Moreover, the study indicated that most hospitals with a greater need to shift costs to (that is, to secure additional revenues from) other payers were more able to do so than those with less need, but about 8 percent of hospitals with a moderate or great need to shift costs were unable to do so successfully. How long hospitals will be able to shift the cost burden to others is an open question. In any case, the ability of health care providers to get other purchasers of medical care to "make up" the losses they may experience from treating public program beneficiaries reflects—once again—the particular characteristics of the U.S. health care financing and delivery system.

Private Purchasers

The continued rise in health care spending by employers gradually led them to become more prudent and aggressive buyers of health benefits for their employees. Indicative of the low profile of employers in the 1960s was a National Conference on Medical Costs, convened at the request of President Johnson to consider the general problem of rising costs. This 1967 conference had no corporate members on its advisory committee from outside the health industry, listed no business associations among the groups that were consulted, and included only one corporate representative on its agenda (U.S. Department of Health, Education and Welfare, 1968). As one employee benefits manager put it later: "In the past, many of us in the business community . . . unknowingly . . . contributed to the continuation of many abuses in the medical care system by simply signing the check and looking the other way" (Chinsky, 1986).

The oil embargo in 1973 and subsequent jumps in oil prices, rising interest rates, stiffer foreign competition, and other economic shocks combined with even sharper increases in health benefit costs to overcome employer passivity. The extended wage-price controls in the health sector and other public sector actions also focused attention on alternative cost containment strategies. As described in Chapters 2 and 3, the passage of the Employee Retirement Income Security Act of 1974 (ERISA) increased em-

ployer interest in self-insurance and more direct involvement in benefit cost management.

The surge in employer actions intended to limit the rate of increase in their health benefit costs dates primarily from the 1980s. Some initiatives have been collectively bargained and developed with labor union participation, whereas others have been unilaterally adopted by employers. Some communities have seen collective efforts by employers and others to tackle various cost problems. Like governments, employers may limit their own costs without necessarily affecting costs overall, particularly if their efforts merely shift the cost burden to others.

Strategies

The portfolio of employer cost containment strategies includes six major kinds of approaches, some of which represent an intensification of older methods and some of which are largely new. These approaches, which have been described in more general terms in Chapter 3, include

-

increased employee cost sharing and limits on some covered services, such as mental health care, although the range of covered services has also expanded in several areas such as outpatient, home, hospice, and preventive care;2

-

utilization management programs intended to limit the volume of health care services through case-by-case review of their appropriateness;

-

network health plans that typically combine various kinds of direct utilization management tools with provider payment and selective contracting methods intended to control the volume of services or the price of services or both;

-

health promotion, which is often seen as a contributor to good employee relations and employee productivity as well as a possible means to lower health care costs through better health practices;

-

flexible benefits, which has as one objective the capping of the employer contribution to health benefits so that employees absorb an increasing share of increasing health care costs, either directly or through sacrifice of other benefits; and

-

self-insurance, which is aimed in part at avoiding the cost of state-mandated benefits and in part at cutting premium taxes and other costs associated with the purchase of insurance.

Tables 6.1 and 6.2 provide summary information on some employer activities in this arena. As with most other aspects of employment-based

TABLE 6.1 Percentage of Surveyed Employers Reporting Selected Utilization Management Features, 1987 to 1991

|

Type of Program |

1987 |

1988 |

1989 |

1990 |

1991 |

|

Preadmission certification |

61 |

68 |

73 |

81 |

81 |

|

Concurrent review |

49 |

49 |

52 |

65 |

65 |

|

Catastrophic case management |

51 |

50 |

55 |

65 |

67 |

|

Second surgical opinion |

__a |

73 |

__a |

__a |

__a |

|

Mandatoryb |

__a |

__a |

59 |

55 |

49 |

|

Voluntaryc |

__a |

__a |

30 |

33 |

33 |

|

NOTE: The scope of the survey varies with the different years represented here. The range is from 1,600 employers covering more than 10 million employees to 2,016 employers covering 13 million employees from all 50 states and including all sizes and types of industry. aData not available. bFor specific procedures. cFor all procedures. SOURCE: A. Foster Higgins & Co., Inc., 1992, as summarized in EBRI, 1992a. |

|||||

health benefits, employers' practices vary substantially, both in the kinds of cost containment strategies they pursue and in the intensity of their involvement. Most larger businesses can take advantage of the approaches described above. Small businesses, however, often lack the resources and interest needed to evaluate options and implement many of these cost containment strategies and even to participate in community coalitions. In addition, insurers, utilization management firms, network health plans, and other organizations have aimed their products at large employers and have been less interested in marketing to small groups. As noted in Chapter 3, small employers are less likely to offer HMOs.3 Many small employers see cutting or eliminating health benefits as their key cost containment option. Another option used by large as well as small employers is to hire greater proportions of part-time and contract workers who are not eligible for company health benefits.

Because many individual employers—even large ones—in big cities

lack leverage on their own, business coalitions in a number of communities are attempting to combine employer purchasing power. Data from the American Hospital Association's database on 130 coalitions indicated that their overwhelming emphasis is on member education and information collection. About one-quarter, however, describe themselves as actively involved in some kind of health care purchasing activity (Business and Health, 1991). The experience of one of the most active of these coalitions, Cleveland's Council of Smaller Enterprises, was described in Chapter 4, which also described a quite different, communitywide strategy promoted by employers in Rochester, New York.

Not only do employers differ in their ability to experiment with cost containment strategies, they also vary greatly with respect to the level and nature of their concern about health care costs. Understandably, most employers, especially if they self-insure, identify the health care cost issue with their own firm's experience. This experience, however, differs for employers, depending on their geographic location, industry, employee characteristics (e.g., proportions of older and younger workers, full-time and part-time, and active and retired), and sense that they can affect health care costs. As a result, although employers in some areas have formed coalitions and other vehicles for collective action, both the motivation to act collectively and the degree of consensus on specific strategies are often limited.

TABLE 6.2 Percentage of Full-time Participants in Employment-Based Fee-for-Service Health Plans Subject to Selected Cost Containment Features

|

|

Small Establishments, 1990 |

Medium and Large Establishments, 1989 |

|

Incentive for use of generic prescription drugs |

15 |

15 |

|

Mail-order drug program |

6 |

10 |

|

No or limited reimbursement for nonemergency weekend admission to hospital |

14 |

14 |

|

Prehospital admission certification Requirement |

59 |

50 |

|

Incentive to use birthing centers for delivery |

21 |

22 |

|

Incentive for participants to audit hospital statement |

7 |

7 |

|

SOURCES: Adapted from Department of Labor, 1990, Table 52 and 1991, Table 51. |

||

Some large employers are directly involved in administering cost management programs, for example, negotiating reductions in ''excessive" provider charges. Many, however, rely on insurers, third-party administrators, or others to negotiate and contract with providers, develop and administer payment methodologies, design and operate utilization review programs, and otherwise implement selected strategies. In this latter situation, individual employers may still demand programs tailored to their preferences or circumstances and thus may influence third-party strategies.

Impact of Private Cost Containment Strategies

Most proposals for health care reform that mandate employer-provided coverage (including those that allow the option of employer payments for public program coverage) and otherwise retain a significant role for employers envision expanded use of the cost containment strategies described above. In particular, they rely on utilization management and regulated competition among network health plans (as described in Chapter 5). Some proposals, however, would also reinvigorate government rate-setting and capital investment controls, discussed earlier in this chapter, and some would try to superimpose some kind of global budgeting mechanism (not just rate-setting) on the private sector. The evidence that any of the designated strategies would actually limit the rate of increase in health care costs temporarily or over the long term is, at best, quite modest, although certain techniques appear to have reduced some unnecessary or inappropriate spending and some have shifted a portion of the cost burden from employers to employees. (Some of the suggested strategies have not really been implemented either in the United States or elsewhere.) Chapter 4 noted that the proliferation of employer cost containment initiatives has increased the administrative and psychological burdens on employers, employees, and health care providers.

Many researchers have tried to assess the impact of private sector cost containment programs over the last two decades (for overviews, see Luft et al., 1985; Eisenberg, 1986; Russell, 1986, 1990; Merrill and McLaughlin, 1986; Luft, 1987; Scheffler et al., 1988; Warner et al., 1988; Hadley and Swartz, 1989; IOM, 1989; Brown and McLaughlin, 1990; Merlis, 1990; Warner, 1990; Wickizer, 1990; Anderson, 1991a; Bailit and Sennett, 1991; EBRI, 1991c; Fielding, 1991a,b; Jencks and Schieber, 1991; Scheffler et al., 1991; CBO, 1992b; Newhouse, 1992; Pauly, 1992; Steinwachs, 1992; Thorpe, 1992a). Such assessments necessarily face three serious problems: the insufficient availability and quality of relevant data; the lack of statistical or physical control over environmental or other variables that might affect results; and the difficulty of disentangling the impact of multiple interven-

tions that overlap both chronologically and geographically and that may have so-called lagged or delayed effects.4

The literature emphasizes possible effects on costs rather than effects on quality of care, access, or patient and provider satisfaction. Most analyses do not examine effects on communitywide costs, although some initiatives might be expected to have spillover effects if broadly enough implemented. The only techniques discussed here that depend particularly on employment-based health benefits as they are structured in the United States are self-insurance and flexible benefits.5 The following six points are summarized from the literature and reflect the emphasis on effects on costs.

First, employee cost sharing does reduce employer costs both by transferring some costs to employees and by reducing episodes of care, but it does not appear to reduce costs per episode of care nor the underlying rate of increase in costs. Reductions in care do not appear to be restricted to care judged unnecessary or ineffective but also extend to effective services (Lohr et al., 1986). Depending on the measures used (i.e., overall use of hospital or other services versus use of specific services such as Pap smears), cost sharing may or may not reduce utilization more for lower-than for higher-income groups (Newhouse et al., 1981; Lohr et al., 1986). Some negative outcomes associated with cost sharing have been reported for poor children, but the impact of being uninsured altogether appears to have far more serious effects (Brook et al., 1984; Lurie et al., 1984).

Second, private sector utilization management appears to have reduced utilization of inpatient hospital care and to have constrained spending for firms adopting these programs, but some, perhaps most, of this reduction has been offset by increases in out-of-hospital care. Reductions are more likely for firms with high baseline utilization rates and tend to level off over time as easy targets are exhausted. The effect of utilization management programs on access to care or communitywide costs has not been systematically studied. Like cost sharing, utilization management appears not to have a long-term effect on the rate of increase in health care costs.

Third, the ability of network health plans to achieve cost savings for

employers—compared with conventional health insurance plans—is related to plan characteristics and is complicated by difficulties in identifying and controlling for biased risk selection. The evidence of cost savings is clearest for staff model HMOs, weaker for IPAs, limited and mixed for PPOs, and essentially nonexistent for newer "open-ended" or point-of-service plans. Unfortunately, for areas not now served by staff model HMOs, these plans are the most time-consuming to establish and may not be feasible for many smaller metropolitan and nonurban areas. Lower levels of hospital use have accounted for most of the differences in costs for network versus conventional health plans. Limited evidence suggests that the rate of increase in costs for HMOs is comparable with that of conventional plans and that higher HMO market shares do not have much effect on communitywide health care costs.

Fourth, systematic evaluations of workplace health promotion programs are few in number, and some analyses suggest that net cost savings are limited and frequently overstated. However, evidence indicates that some health promotion efforts may still be relatively more cost-effective than many of the medical treatments commonly paid for by company health plans.

Fifth, although self-insurance and flexible benefits appear to offer some financial benefits to larger employers, there is no documentation that either reduces the longer-term rate of increase in health care costs. Whether flexible benefit programs-will over the long term allow employers to cap the overall rate of increase in employee benefit costs (regardless of what happens to employer-and employee-paid health care costs) remains to be seen.

Sixth, real "one-time" reductions in costs—particularly if they involve gains or at least little or no sacrifice in access, equity, or outcomes—should not be downplayed. In particular, continued public-private efforts to identify and eliminate care that is not clinically appropriate and to limit the introduction of expensive technologies of limited benefit are warranted on grounds of both quality of care and cost.

To summarize, continued innovation by employers and third-party carriers in benefit plan design may help some employers lower the level of their health benefit costs and may, in-some cases, encourage more effective utilization of health care services. It is, however, discouraging to find little evidence that private sector cost containment strategies affect the long-term rate of increase in health care costs and virtually no evidence that suggests whether employer efforts to contain costs have positive, neutral, or negative communitywide or societal impacts.

If any community may be viewed as an exception to this last generalization, it is Rochester, New York. It has a distinctive history of active, long-term employer support for community rating and other programs by the community's dominant insurer (a Blue Cross and Blue Shield plan),

communitywide health planning, HMO development, and restraint in hospital pricing. Without this support, it is doubtful that the area would have such low health insurance costs for both individual and employer group coverage (Taylor, 1987; Freudenheim, 1992b; Taylor et al., 1992). In 1991, per enrollee health benefit costs for Blue Cross in Rochester were $2,378, compared with the overall national figure of $3,605 reported in Chapter 3. Only 6 percent of the adult population reported they were uninsured, less than half the national rate. In addition, major Rochester employers, such as Eastman Kodak, have chosen not to self-insure, believing that any short-term savings would be outweighed by higher longer-term costs from the destruction of their cooperative strategy for health care financing and delivery.

Hawaii, which has among the nation's lowest costs for health care despite its pattern of higher prices for most services and goods, might also be cited as a place where employers have made a difference in overall health care costs (GAO, 1992a; Kent, 1992b; Priest, 1992). 6 It is not clear, however, whether their role has been one of direct involvement in cost containment strategies or one of more passive support for state-and insurer-initiated programs. The state is unusual in having won the only ERISA waiver to date, for its 1974 Prepaid Health Care Act.7 This legislation requires employers to provide, and employees to accept, coverage unless coverage is provided under another plan, sets a maximum level of employee contribution, and defines a required benefit package. Most employers voluntarily cover dependents even though they are not required to do so. Reports on cost control strategies in Hawaii focus not on employers but on the state, the Hawaii Medical Service Association (a Blue Shield plan that covers 53 percent of the population), and the Kaiser Foundation Health Plan, which covers 20 percent. These plans voluntarily use a modified form of community rating for employers with fewer than 100 employees.

By and large, private sector innovation in cost containment has been designed to attract large employers rather than small employers or individual purchasers. If market reforms essentially removed the large employer from the purchasing role in favor of the individual, the cost containment strategies adopted by health plans might change. The nature of any such changes would be affected by the extent to which reforms also required basic benefits, standardized utilization review, regulated payments to

hospitals and physicians, and otherwise constrained private initiative. Health plan strategies would also be affected by the degree to which reforms strengthened or weakened traditional insurance regulations to discourage competition based on risk selection, assure financial solvency, and generally police the market for deceptive practices.

FUNCTIONING OF THE HEALTH CARE MARKET

In an economy such as that of the United States, questions about the appropriateness and effectiveness of various price signals and resource allocations are often most easily settled by reference to the workings of well-functioning markets. In many circumstances, markets can be expected to generate highly effective price signals that help ensure the efficient use of resources. Unfortunately, the market for health care services—as it is currently structured—cannot make such claims. Leading issues in the debate over health care reform are whether major changes in public policy can create an effectively functioning market, whether the employer should have a major role in a market-oriented approach, and whether, on balance, the projected effects of one or another kind of reformed market would be better or worse than the major alternatives. The major alternatives are incremental changes in the current system, mandatory employer coverage (similar to the Hawaii plan or with a public plan option), and a uniform, universal public plan.

To understand the debate over market reforms, it is useful to review what economists described as the basic requirements for an effectively functioning, competitive market (see, for example, Fuchs, 1988; Aaron, 1991; Weisbrod, 1991; CBO, 1992a). These requirements include easy entry into the market by buyers and sellers; freedom from government supply or price regulation and from buyer or seller collusion to fix prices or supplies; absence of dominant buyers or sellers; buyers and sellers with reasonable and relatively equal information about price and quality; and no subsidies that distort prices and price consciousness.

In health care, however, one finds large government and private payers; organized groups of providers; some regulation of prices and substantial regulation of market entry, particularly through licensing and accreditation requirements for health care practitioners and providers; considerable doubts about the independence of supply and demand; substantial imbalances in provider and consumer information but lack of significant information about outcomes—even on the part of providers; and market agents insulated by third-party insurance practices from full price sensitivity or cost minimization pressures. In many cases, the physician, not the patient, effectively decides what quantity and quality of care will be provided, and the incentives affecting physician choices, thus, need to be understood. As noted in

Chapters 1 and 5, although the tendency of insured individuals to use (and have provided for them) more services than uninsured individuals is a partly intended and partly unwanted consequence of health insurance, such a "utilization effect" is not a desirable feature of competitive markets.

Aaron (1991) notes that "health insurance and health care pose special problems [for economic analysis because] health insurance typically is purchased by healthy people, while most health care is consumed by sick people. Society normally has little interest when people gamble and lose. But when the gamble concerns events that change basic preferences and that affect the life and health of oneself and one's family, it is not clear why past consumer decisions deserve priority over new preferences" (p. 17). Moreover, many of the most expensive decisions involve individuals whose ability to weigh expected benefits and risks of treatment alternatives are stressed by pain and fear, time pressures, and lack of information and technical understanding of specific options and the possible consequences. The more drastic the consequences of the choices people make about health care, the more compelling are the questions and arguments about the role of government in intensifying or limiting market-based incentives for individual choice and responsibility. Similar issues arise in debates over the need for government constraints on the use and interpretation of living wills and advance directives about the use of life support in cases of terminal illness or injury.

Markets that are characterized by poorly informed consumers are unlikely to yield appropriate prices and quantities. Although the information imbalance between providers and employer purchasers may be less than for the individual patient, the complexity of the medical care product and the difficulty of assessing outcomes remain obstacles to informed purchasing. (Employer interest in outcome assessment is discussed shortly.) In addition, biased risk selection can encourage competitors to focus on competition for good risks rather than on competition based on effective and efficient management of health care.

High and rising costs, gaps in coverage, and unequal access to health coverage and health care are not surprising consequences of the current structure and operation of health care markets. The committee's view is that this structure encourages the proliferation of medical technologies and services without evidence of effectiveness and that neither the producer nor the consumer side of the health care transaction faces sufficiently the real costs of its actions. Because the current incentive and market structure is widely viewed as inefficient, cost containment has become a central objective of decisionmakers even though it is not inevitably a sensible goal if high costs are producing appropriately high value. A major question for decisionmakers is whether the health care market can and should be reformed or whether the nation would be better off with a single national health plan.

Those who believe that policy changes can make market forces an effective constraint on health care use and prices propose several specific steps. They include capping the tax exclusion for employer-paid health benefits; increasing the employee's contributions for health benefit premiums; requiring multiple-choice of health plans; limiting or financially rewarding individual choice of certain kinds of health plans; capitating provider payment; standardizing benefit packages; and developing better performance monitoring techniques.

Some argue that market forces would work better if the individual, not the employer, were the key decisionmaker in health insurance purchases. They would adapt the proposals just mentioned to eliminate employer discretion in the design, selection, or operation of health plans (Garamendi, 1992). Most but not all proposed market strategies would be supported by a fairly extensive regulatory structure, regardless of whether these approaches envision any role for the employer beyond certain nondiscretionary financing and administrative tasks.

Proposals for market reform generally would shift more of the direct burden for health care spending—at the margin—away from the government or employer to the individual. They would then mitigate—to varying degrees—the burden of this shift through income-related subsidies intended to make health insurance more affordable for low-income individuals. Proposed changes in federal tax and other policies to make the choice of certain health plans more costly to individuals might also work to produce more one-time reductions in the level of health care expenditures. Whether such market strategies would selectively affect inappropriate spending, slow the development and introduction of expensive medical technologies, or reduce the underlying rate of growth in health care costs is unclear. Most of the formal economic analyses of markets and health insurance focus on efficiency and spending at a particular time rather than on effects across time (Newhouse, 1992).

Tax, regulatory, and other reforms that introduce more market like mechanisms of one type or another into health care delivery and financing probably can mobilize health care resources more efficiently in some areas. Given, however, the current distribution of income and the desired distribution of health care services and improved health outcomes (to note only one particular concern), such reforms, unaided by significant public subsidies for the purchase of insurance and improved mechanisms for monitoring health plan performance, are unlikely to generate appropriate responses.

Some aspects of managed competition or market reform proposals have been considered in Chapter 5. This discussion noted the uncertainties surrounding the methods and principles for defining basic benefits, controlling or adjusting for risk selection, monitoring health plan practices for abuses, and ensuring accountability on the part of whatever oversight entity is cre-

ated. Some of these issues are raised as topics for continued research in Chapter 7. Many of the basic assumptions of market reform models have never been tested, whereas real examples of single national health plans exist as a basis for analyzing the pluses and minuses of such a strategy and evaluating its relevance to the United States.

THE QUESTION OF VALUE

Whether or not the real expenditures on health care in the United States negatively affect the country's standard of living depends more critically on the return on this investment rather than on its level. If health care expenditures were viewed as productive enough in terms of their impact on work force quality, morale, and performance (e.g., through reduced levels of injury, absenteeism, or behavior impaired by chronic illness), perhaps concern about overall resource commitments would diminish. In short, the dividends would be worth the investment. If, however, health care expenditures divert resources from more productive expenditures or if health expenditure increases cannot, in the short-term, be offset by reductions in wages or other components of total compensation, then some specific companies and industries may suffer a competitive disadvantage.

Clearly, concern is widespread that the high level of resources devoted to the U.S. health sector is not being matched by a sufficiently high return in overall health status and individual well-being. This conclusion is controversial but is kindled by (1) studies showing that the per capita use of many medical practices varies greatly depending on geographic location, insurance status, supply of health resources, and other factors,8 (2) evidence that a significant amount of care is not medically appropriate or effective, and (3) the lack of an obvious health status advantage for the United States compared with other advanced nations that commit fewer resources to health care and yet still cover virtually of their populations (Wennberg, 1984, 1990, 1991; Brook et al., 1986; Chassin et al., 1987; Eddy and Billings, 1988; Starfield, 1991; Schieber and Poullier, 1991; Fuchs, 1992).

Increased health care expenditures have, nonetheless, coincided with some improvements in overall health status as measured, for example, by infant mortality, average life expectancy, and age-adjusted death rates from heart disease and stroke (U.S. Department of Health and Human Services, 1991). Although changed behaviors in diet, exercise, and smoking probably have played a role in these developments, there is little question that new

drugs, new types of surgery, and other medical advances have also made important contributions. Significant differentials remain, however, between more and less advantaged segments of the population. For example, the infant mortality rate for African Americans is twice that of whites in the United States. Even for infants born to college-educated women, a notable gap between the races remains (Schoendorf et al., 1992). The reasons for such differentials are not well understood but almost certainly include a mix of socioeconomic and biological factors that increased health care spending by itself could leave largely unaffected (Davidson and Fukushima, 1992; Kempe et al., 1992).

Recent decades have seen spectacular developments in biomedical science, medical technology, and medical education that hold considerable promise for future improvements in health status. In general, the American health care system produces an enormous amount of innovation; at its best, medical care in this country has no rival. Moreover, much of the innovation and trained personnel produced by or for the U.S. health care sector is available to people in many other countries, so others, too, have a stake in the innovative and educational developments induced by the complex set of existing arrangements in the U.S. health care sector. Policymakers assessing options for reform should think carefully about the impact of new policies on the country's continued capacity for innovation and education and the expected impact of this capacity on health status and well-being.

From a public policy viewpoint, it would be highly desirable to understand to what extent the high and rapidly rising health care costs stem from cultural and scientific influences (e.g., higher standards of living, higher expectations, and advances in basic science) and to what extent they derive from the way the health care system is currently organized and financed (e.g., relying heavily on employment-based health benefits rather than a single public program or an individual insurance market). Similarly, it would be highly desirable for policymakers to know whether the spending gap between this country and others is caused by greater availability and consumption of effective health services (a good idea), the greater use of ineffective health services (a bad idea), unnecessarily high payments to providers (a bad idea), or simply the slower growth of the U.S. economy (an unfortunate development)?

Policymakers can also ask more specific questions. For example, if medical training and payment were substantially reoriented to increase the proportion of generalists relative to specialists (as many recommend), would the health care system become more effective overall in reducing ill health and poor functioning? If some resources were shifted away from certain kinds of high-technology care for adults toward primary and preventive care for children and pregnant women, especially in poor and minority communities, could gains in health and well-being for the latter group be achieved,

and what would be the effect on the former group? If physician fees were decreased or increased by 20 percent, would this have any significant impact on the supply of quality medical services in the short or long run? If pharmaceutical prices were cut or increased by 20 percent, would this have any appreciable bearing on the level of introduction of useful new medical compounds? Is the administrative overhead associated with the current multipayer system matched by appropriate benefits related to the diversity of purchaser circumstances?

Answers to the above questions are not easy to pin down because the variables cited are interdependent, and the data are incomplete and sometimes misleading. The measurement problems associated with medical care prices (discussed earlier) are matched by problems in measuring medical care outputs, that is, their effect on health and well-being in the aggregate and for specific population subgroups. Aggregate measures of health are still relatively crude; most analyses rely on mortality statistics with occasional use of other measures such as proportion of infants with low birth weights (Schieber et al., 1991).

On the other hand, some important advances in measuring health status and well-being at the individual level are being achieved using both generic and disease-or problem-specific measures of functioning and of health-related quality of life that go well beyond traditional measures of mortality and morbidity (Lohr, 1989, 1992). These advances have not yet had much utility for general comparisons of population health status over time and across geographic units. This is in part because these measurement tools are not well known outside certain research settings and in part because they require information reported by individuals that is not routinely and widely enough available from such sources as birth and death records, health insurance claims, national health surveys, and disease reporting systems.

With varying degrees of sensitivity to the complexities involved, policymakers, providers, employers, unions, and consumers have begun to focus increasingly on the question of value and to demand comparisons of the cost-effectiveness of individual practitioners, providers, and both new and existing medical services (Roper et al., 1988; Lohr, 1989, 1992; Eddy, 1990a,b,c, 1991a,b; IOM, 1990a,b; Couch, 1991; Fox and Leichter, 1991; Buck, 1992; Mulley, 1992). The results may be used (and possibly misused) to help determine what services health plans should cover, set payments for medical care, select providers for network health plans, and develop clinical practice guidelines for practitioners, payers, and patients (IOM, 1985, 1991, 1992a,b; ProPAC, 1986, 1992; PPRC, 1988, 1989; Rettig, 1991).

Most efforts to assess the effectiveness of medical services and technologies, especially new technologies, are publicly supported, although some private organizations, such as the Blue Cross and Blue Shield Association, have become involved in technology assessment. Initiatives by private

payers, however, are limited partly because of the expense and complexity of technology assessment and partly because they cannot fully capture the benefit of their work, the results of which can be used by their competitors (the ''free rider" problem). Reflecting the growing perception that the federal government needed to bolster its involvement in effectiveness research, Congress created the Agency for Health Care Policy and Research in the Department of Health and Human Services in 1989 and gave it broad responsibilities to develop practice guidelines and conduct research on the effectiveness of alternative forms of care for specific clinical conditions.

Although much of the interest in health status and outcome measures has come from either national policymakers or clinicians, employers and unions in a number of communities are becoming involved in pragmatic efforts to apply these measures, often with the support of private groups such as the John A. Hartford and Robert Wood Johnson foundations. Employers and unions are working with researchers, providers, and public officials to find practical ways to gather better data on outcomes and then use this information to improve the quality and efficiency of care (Borbas et al., 1990; Geigel and Jones, 1990; Madlin, 1991a; Stern, 1991; Buck, 1992; Mulley, 1992). Such efforts are under way in communities in Iowa, Minnesota, Ohio, Tennessee, and elsewhere.

The United States is clearly a leader in the arena of effectiveness research and technology assessment. Whether employers are, at the margin, providing any extra stimulus to effectiveness research and methodology development (beyond what government, private foundations, and some insurers would provide) is hard to say. Undoubtedly, many employers focus on costs and little else. Arguably, however, some large employers and employer coalitions may be encouraging a speedier movement from the research to the application stage for effectiveness assessments. Furthermore, a greater level of interest in local, communitywide assessments of provider performance may exist now than would be the case were employers uninvolved in health benefits.

Nonetheless, the challenges in devising good measures of outcomes and effectiveness, collecting accurate data, making fair comparisons, and doing it all at a cost perceived as reasonable are enormous. Given the complexity of medical care processes and the problem of controlling for the impact of economic, ethnic, and other variables on health, difficulties will surely continue for efforts to link many health care services—and expenditures—to specific outcomes. In addition, better measurement of health care outcomes and performance and programs to judge and improve the appropriate use of new or existing technologies may add to the cost—broadly defined—of administering health benefits. Like any other costs, these should be judged by whether and how much they help improve the value of health spending,

for example, by reducing spending for inappropriate care or achieving better outcomes for the same amount of spending.

Overall, policymakers, researchers, employers, unions, and health care providers must be committed for the long term to asking the right questions and seeking their answers. Whether initiatives such as those described above will produce information and responses that are convincing and timely enough to persuade purchasers—including government purchasers—to look beyond the unit price of services, the "premium" for an insured or self-insured health plan, or the appeal of cost shifting remains to be seen.

CONCLUSION

Startling as they may be, high levels and rates of increase in health care spending may by themselves provide little reason for anxiety. The crucial issue for policymakers is not whether the ratio of health care spending to GNP is high and rising, but whether the level, distribution, and rate of increase in health care spending produce appropriate value compared with alternative kinds of spending within the constraint of available resources. In times of economic difficulties, when many important needs may not be satisfied, concerns about the relative value perceived for health care spending may intensify.

Although individuals and employers in the United States can and must make resource-related trade-offs about spending for health care versus spending for other purposes, it is at the level of national policy that the most complex balancing must occur. It is there that competing interests, short-term and longer-term objectives, and calls for major restructuring of the health care system are most explicitly weighed.

Should policymakers expect that incremental changes in existing institutional arrangements and public policies can improve the distribution and deployment of resources in the medical sector to achieve acceptable health outcomes at a reasonable cost? Most of the committee members believe the answer to this question is no. Without major restructuring of the current system of voluntary employment-based health benefits, certain problems, such as cost shifting, inadequate access to appropriate care for many of the uninsured, competition based on risk selection, and rapid diffusion of new technologies without evidence of cost-effectiveness, are unlikely to diminish.

In its quest for a more cost-effective health care system, would the nation be better off removing the employer from any active decisionmaking role and leaving the field mainly to government policies and programs or mainly to the operation of some reconfigured individual market for health care services or—more likely—some combination of the two? The committee could not agree on an answer to this question. Although committee members agreed that employers' capacities and incentives to manage health

benefit programs effectively are quite uneven and narrowly focused on their own employee groups, they disagreed about the theoretical and empirical case for different strategies for controlling health care costs and the philosophies underlying these strategies. The next chapter, however, outlines some areas in which the committee did generally agree on steps that could improve the performance of the current system of voluntary employment-based health benefits.