2

The Changing Demands on National Technology Policy and Strategy

Three important changes in the global political and economic environment have recast the central technology-related challenges facing the United States and thereby exposed major vulnerabilities in the U.S. technology enterprise. First, there have been steady and rapid changes both in industrial and corporate structure and in the nature of competition in many industries. In particular, the technical intensity of many manufacturing and service industries has increased dramatically at the same time that a revolution in production systems, both the human and the technical elements, has redefined the standard of competitive organizational and managerial performance for most companies.

Second, there has been a long-term shift in the global economic and technological position of the United States. Twenty years ago the preeminence and comparative self-sufficiency of the U.S. economy and technology enterprise could be taken for granted. Today the United States has become but one of several major economic and technological powers in a much more tightly integrated and interdependent world economy.

Third, the end of superpower military and geopolitical rivalry has placed a growing premium on economic and commercial technological strength as a source of national power and political influence worldwide. This geopolitical shift comes at a time when civilian technological advance, driven by global economic competition, is pacing technological advance in many fields critical to the national defense.1

These three changes are simultaneously creating a new set of challenges for U.S. public and private agendas for technological advance and application. They raise serious questions concerning the current scope and composition of the nation's portfolio of technological activities, including

the breadth and relative self-sufficiency of R&D effort, and the strength of technical, organizational, and managerial capabilities that complement R&D and are essential to the effective application of technology. Together these three trends challenge the utility of many of the underlying assumptions and distinguishing features of the postwar U.S. technology enterprise discussed in Chapter 1.

RISING TECHNICAL INTENSITY AND THE REVOLUTION IN PRODUCTION SYSTEMS

Global competition and rising technical competence worldwide are changing the intensity, pace, and character of technological innovation in nascent, developing, and mature industries in important ways. Historians of business and technology have described the rise of complex, private-sector managerial bureaucracies that have emerged in parallel with the development of an ever more powerful global transportation and communications infrastructure. They have documented how the complexity of products and services, the size and diversity of markets, and the economies of scale and scope in R&D, production, distribution, and sales—each of which has several technological elements—are driving changes in the nature of competition. It is beyond the scope of this report even to catalog the full range of changes in marketplace competition; a virtual flood of scholarly analysis and popular journalism explores how industries vary as a function of their history, the technologies that they embrace, the dynamics of competition among leading players, and the characteristics of buyer-supplier relationships, to name just a few.2 A couple of trends, however, seem universal, important, and undeniable, namely, the increasing technical intensity of important manufacturing and service industries and the revolution in production systems.

The Rising Technical Intensity of Industries

In many industries commercial technology is increasingly "science-based," that is, drawing to an increasing extent on codified and systematized knowledge rather than craftlike, experiential know-how (Alic et al., 1992).3 In a few cases this is largely new science, but more generally it is based on a broad mix of old science, new science, and technological know-how from many different sources.

Also, in the development of promising new industries or in the transformation of major existing industries, more engineering and technological resources are being brought to bear than ever before. The result is a quickening of the pace of commercial technology development and diffusion accompanied by shorter product life cycles. In this context it is easy to understand how, in certain high-potential, technology-intensive industries,

the capital and skill requirements for market entry and competitive survival of individual firms have risen dramatically. The financial and scientific or technological resources necessary for a firm to enter marketplace competition in, for example, bioengineered products or optoelectronic devices, regional banking or package delivery are substantial (Burrill and Lee, 1991; Kodama, 1991; Quinn, 1992; U.S. Congress, Office of Technology Assessment, 1987, 1991a).

The development and commercialization of new products and services have always been a multidisciplinary effort. The most successful practitioners in one field are likely to be those who can identify and draw upon complementary or supporting technical advances in other fields. In a new manufactured product, for example, the challenge is to determine simultaneously—at a minimum—good choices for materials, product features, manufacturing processes and technology applications, and the most promising approaches for product improvement after its introduction. In the last half century, in particular, the absolute volume of specific knowledge within technical disciplines has grown tremendously, and the resources required to attack problems with the best and newest tools of several disciplines have grown commensurately. In other words, the scope of the scientific and engineering basis for making a "good" competitive decision is often both larger and richer than it was a generation ago.

Competition among companies that have the resources and ability to manage such a demanding, rapidly evolving, multidisciplinary process is driving a higher degree of interdependence among fields in commercial applications. Technology fusion, or the marriage of disparate technologies from different industries to create new products, new services, or new systems, is becoming an increasingly important source of product and process innovation in all industrialized economies. For example, the marriage of electronic and mechanical technologies, or "mechatronics," has led to the creation of such products as numerically controlled machine tools and industrial robots. Optoelectronics, the fusion of electronics and optics technologies, has yielded major commercial products, including optical fiber communication systems. Similarly, the coevolution and combination of computerized inventory systems and universal telephone service has revitalized both the retail and the catalog sales industries.4

The implication of such technology fusion is that, in many industries, technological advance depends increasingly on the effective technical interaction and collaboration of equipment vendors, component suppliers, system assemblers, private and public research laboratories, other service providers, and consumers in complex networks or "organizational complexes" of innovation. Not only is the process of successful commercial innovation becoming much more technology-intensive and fusion-oriented, but this same phenomenon means that established industries and technological niches are

much more vulnerable to "invisible competitors," that is, new combinations of technologies once considered beyond the scope of interest and concern of a given industry (Kash and Rycroft, 1992; Kodama, 1991; Rycroft and Kash,1992).

These developments place new demands on the technological capabilities of companies and of nations. To compete effectively companies must coordinate and integrate their advanced technical activities much more fully with the rest of the production system, pushing R&D activity further downstream into design, production, and marketing, as well as factoring production and marketing considerations into the earlier phases of upstream development activities. Likewise, they must look beyond their own corporate, industry, and national borders for technology that might yield competitive advantage, and develop the capacity for rapidly assimilating and mastering it. Faced with high costs and uncertainty associated with the development and commercialization of many promising areas of technology, a growing number of companies are entering into R&D consortia, joint ventures, or alliances with other firms (domestic and foreign), with universities, and with government agencies in an effort to share risks and costs for the sake of mutual benefits (Hagedoorn and Schakenraad, 1993; Mowery, 1987; Tassey, 1992; Vonortas, 1989).

The increasing technical intensity of industries and the growing importance of technology fusion in the context of stiff international competition also place a premium on broadening a nation's overall R&D portfolio, in effect, hedging against unforeseen opportunities and challenges. These changes demand particular attention to the widening spectrum of industrial technologies whose development and diffusion are beyond the capabilities of individual firms operating in competitive markets. Governments worldwide are defining more industrial technology as "generic," or "precompetitive," and therefore a legitimate target for private-sector consortia and public-sector support.5 To strengthen their domestic generic technology base and help resident companies capture the benefits of that base, many governments are helping to cultivate linkages and collaboration across the diverse spectrum of domestic R&D institutions—corporations, universities, national laboratories, and private research laboratories. At the same time, the nature of global technology-intensive competition demands that a nation's technology enterprise become more effective at tracking and acquiring new technology from outside national borders.

The Revolution in Production Systems

The rapid growth in technical intensity of many industries coincides with a radical shift in the organization of production and innovation that is redefining the standard of competitive performance in most manufacturing

and many service industries. Characterized as a revolution in production systems, this organizational and managerial shift is captured by such concepts as just-in-time, total quality management, design for manufacturing, and concurrent engineering. Many successful producers of complex products and services are now combining aggressive R&D and technology outreach strategies with organizational changes that make possible more rapid, continuous, incremental and concurrent improvements in products and processes. While demanding more effective integration of all elements in the product-realization process—including R&D, design, engineering, production, marketing, and in-field support—this approach tends to be less disruptive in the short term and often yields large improvements in the system of manufacture or service delivery (as an integrated part of the production process) over longer periods of time (Barkan, 1991; Bowen, 1992; Dertouzos et al., 1989; Lee, 1992; Quinn, 1992).

A continuous incremental improvement strategy leads to the possibility of inserting new component and subsystem technology as it becomes available, thereby capitalizing on new technical advances more rapidly. 6 The technical resources and capabilities of suppliers and vendors, therefore, have become far more critical elements in the manufacturing firm's product and process development strategies than was true two decades ago. These closer linkages to suppliers contribute to both higher quality of products and increased performance of the production system. This gives advantage to firms with strong cooperative relations with suppliers, workers, and potential customers (Lundvall, 1992; von Hippel, 1988).

Much of the change is a result of greater appreciation of the demonstrated efficiencies of modern Japanese production methods, sometimes gathered under the rubric of ''lean production" and "flexible manufacturing." In contrast with traditional mass production, lean production refers to a constellation of new organizational relationships both inside and outside the firm, to a new way of viewing workers, customers, and suppliers, and to a different understanding of how technologies change and improve (Hill, 1991; Kline, 1991; Womack et al., 1990). The goal of lean production—in comparison with mass production—is to use less labor, materials, plant, equipment, and time at all levels in the firm to produce a greater variety of high-quality products, while continuously accommodating rapid changes in product design and performance.7

Table 2.1 sets out the most salient differences between the new "lean" or "flexibly decentralized" model of industrial production and the more traditional model of "mass" or "robust" production. As this comparison highlights, a lean production system is organized and managed to seek perfection the first time, to avoid wasted time and materials, and to understand and meet or exceed customer expectations. The lean production work force combines the multiple skills of the craft worker with the scale advantages of

TABLE 2.1 Changing Organizational Patterns in U.S. Industry

|

Old model |

New model |

|

Mass production, 1950s and 1960s |

Flexible decentralization/Lean production 1980s and beyond |

|

Overall strategy |

|

|

• Low cost through vertical integration, mass production, scale economies, long production runs. |

• Low cost with no sacrifice of quality, coupled with substantial flexibility, through partial vertical disintegration, greater reliance on purchased components and services. |

|

• Centralized corporate planning; rigid managerial hierarchies. |

• Decentralization of decision making; flatter hierarchies. |

|

• International sales primarily through exporting and direct investment. |

• Multi-mode international operations, including minority joint ventures and nonequity strategic alliances. |

|

Product design and development |

|

|

• Internal and hierarchical; in the extreme, a linear pipeline from central corporate research laboratories to development to manufacturing engineering. |

• Decentralized, with carefully managed division of responsibility among R&D and engineering groups; simultaneously product and process development where possible; greater reliance on suppliers and contract engineering firms. |

|

• Breakthrough innovation the ideal goal. |

• Incremental innovation and continuous improvement valued. |

|

Production |

|

|

• Fixed or hard automation. |

• Flexible automation. |

|

• Cost control focuses on direct labor. |

• With direct costs low, reductions of indirect cost become critical. |

|

• Outside purchases based on arm's-length, price-based competition; many suppliers. |

• Outside purchasing based on price, quality, delivery, technology; fewer suppliers. |

|

• Off-line or end-of-line quality control |

• Real-time, on-line quality control. |

|

• Fragmentation of individual tasks, each specified in detail; many job classifications. |

• Selective use of work groups; multiskilling, job rotation; few job classifications. |

|

• Shopfloor authority vested in first-line supervisors; sharp separation between labor and management. |

• Delegation, within limits, of shopfloor responsibility and authority to individual and groups; blurring of boundaries between labor and management encouraged. |

|

Old model |

New model |

|

Mass production, 1950s and 1960s |

Flexible decentralization/Lean production 1980s and beyond |

|

Hiring and human relations practices |

|

|

• Work force mostly full-time, semi-skilled. |

• Smaller core of full-time employees, supplemented with contingent (part-time, temporary, and contract) workers, who can be easily brought in or let go, as a major source of flexibility. |

|

• Minimal qualifications acceptable. |

• Careful screening of prospective employees for basic and social skills, and trainability. |

|

• Layoffs and turnover a primary source of flexibility; workers, in the extreme, viewed as a variable cost. |

• Core work force viewed as an investment; management attention to quality-of-working life as a means of reducing turnover. |

|

Job ladders |

|

|

• Internal labor market; advancement through the ranks via seniority and informal on-the-job training. |

• Limited internal labor market; entry or advancement may depend on credentials earned outside the workplace. |

|

Governing metaphors |

|

|

• Supervisors as policemen, organization as army. |

• Supervisors as coaches or trainers, organization as athletic team. (The Japanese metaphor; organization as family.) |

|

Training |

|

|

• Minimal for production workers, except for informal on-the-job training. |

• Short training sessions as needed for core work force, sometimes motivational, sometimes intended to improve quality control practices or smooth the way for new technology. |

|

• Specialized training (including apprenticeships) for gray-collar craft and technical workers. |

• Broader skills sought for both blue-and gray-collar workers. |

|

SOURCE: U.S. Congress, Office of Technology Assessment (1990b, p. 115). |

|

the mass producer. Multiskilled workers use increasingly automated and more flexible machines and tools to make a greater variety of products with the same capital equipment, for example, by software rather than hardware modifications. Inside the lean production organization, the division of labor is organized around cooperative cross-functional teams at all levels, thereby encouraging sharing of responsibility and close integration of different parts of the product realization process (Hill, 1991). Cooperative work groups on the factory floor can coordinate work more effectively and make incremental changes directly and quickly.

These techniques tend to be linked and interdependent. Therefore, it is critical that those who organize and arrange the production and delivery of goods or services understand the complexity of the production/delivery system that their decisions affect when considering improvements to that system. For instance, although just-in-time production techniques are often praised for their contribution to lowering inventory investment, these techniques have also provided powerful incentives for firms to achieve higher component quality. While elevating the importance of supplier relationships, these techniques also allow firms to reduce investment in material-handling equipment and to decrease warehouse storage requirements as well as material buffers in the assembly process. Conversely, just-in-time practices, if divorced from strong cooperative relations with suppliers, workers, and customers, are unlikely to work well, and may even be counterproductive. The new "lean" system needs to be implemented as a whole. Beyond these gains, a greatly increased flexibility of product manufacture allows rapid response to new orders (Heim and Compton, 1992; Hill, 1991; Lee, 1992).

Indeed, well-executed, lean production of products with a high piece count has enabled manufacturers to cut production costs by up to 50 percent while simultaneously yielding much higher product quality than older production processes. When a Xerox benchmarking team compared their company's performance against that of their Japanese affiliate and other Japanese photocopier manufacturers in the late 1970s and early 1980s, they were astonished by the differential between Japanese and U.S. firms. Japanese manufacturers were producing significantly higher quality products than Xerox with half the manufacturing costs (Bebb, 1990).

A similar gap between Japanese and U.S. automakers in quality and cost was documented during the mid-1980s. More recent data show that some plants of U.S. automakers have nearly caught up with Japanese in the number of labor hours required to assemble a car. Nevertheless, many other U.S. plants continue to lag far behind their Japanese counterparts in labor productivity, in some cases requiring 50 percent more labor hours to produce a comparable number of automobiles (Womack et al., 1990; Clark and Fujimoto, 1991).

In addition to the gains cited above, when management practices adhere

to the human resource principles of lean production, significant gains in worker satisfaction can also be realized. The record of the General Motors-Toyota joint venture, New United Motors Manufacturing, Inc. (NUMMI), in Fremont, California, demonstrates that significant quality and productivity improvement can be accompanied by major increases in worker satisfaction under lean production (Adler, 1993; Vierling, 1992), NUMMI was established in 1984 in the Old GM-Fremont plant, hiring 85 percent of the unionized work force that had worked in the plant under GM's traditional mass production organization. By the end of 1986, productivity at the NUMMI plant was higher than all other GM plants and twice that of its predecessor, GM-Fremont. At the same time, absenteeism at the NUMMI plant fell to a steady 3 to 4 percent, down from levels of 20 to 25 percent under the old GM-Fremont management, and the number of worker grievances filed under NUMMI management dropped to a fraction of those filed during the GM-Fremont era. By the end of 1991, over 90 percent of NUMMI employees described themselves as "satisfied" or "very satisfied" (Adler, 1993).8

Although the NUMMI experience demonstrates that the improvement of worker welfare and the other productivity and quality objectives of lean production can be mutually reinforcing, it should be noted that "lean" approaches that neglect the human component of production systems can have the opposite effect. One recent study of other Japanese auto transplants in North America concluded that these companies' commitment to conserving resources or "leanness" did not extend to their work force, citing a relatively high incidence of work-related injuries such as repetitive stress injury at a number of plants (Berggren, et al., 1991).9 Although many changes in production systems during the industrial age have led to less desirable conditions for workers in the factory, the committee notes that the opposite can be true with a shift to lean production if increased participation and enhancement of firm's most valuable asset—its work force—are central to its strategy.

In a similar manner, many of the principles of lean production can be applied to the new product development process. Several studies have shown in detail that the more systematic approach to the integrated, concurrent design and development of products and their related processes, known as "concurrent engineering," can significantly reduce product lead times and increase engineering productivity while maintaining, if not improving, product quality. It does so by the use of multifunctional teams in each phase of product development along with much-improved methods of communication and documentation. A study of production and product development performance in the photocopier industry during the late 1970s and early 1980s concluded that Xerox, the leading U.S. producer of photocopiers, took twice as long and twice as much engineering manpower to develop a new product as Fuji Xerox and other Japanese competitors (Bebb, 1990).

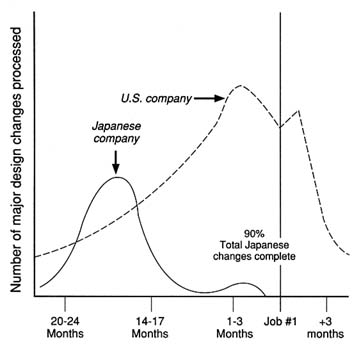

Likewise, in a comparative study of 29 major new car development projects in 20 companies (three American, eight Japanese, and nine European), Clark and Fujimoto (1991) showed that Japanese firms employing concurrent engineering techniques were able to complete a development project with, on average, one-third the engineering hours and two-thirds the lead time of their U.S. and European competitors. Similarly, Sullivan's (1987) two-company comparison of the process of developing a new model automobile showed that major design changes peaked for the Japanese firm about 35 percent of the way through the process, whereas the design changes of the U.S. firm peaked just before and after the new model's release and were much more numerous overall. 10 See Figure 2.1.

Finally, there is broad evidence that the principles of lean production and concurrent engineering have the potential for widespread application in the production and delivery of services such as accounting, banking, retail sales, package delivery, health care, insurance, and telecommunication services. Indeed, service firms can be said to have pioneered in some forms of lean production and concurrent engineering, especially in new ways of using computer and communications systems to develop and deliver new services as well as to redesign existing services to suit new forms of delivery, all while reducing the cost and raising the quality of services delivered to customers (Barkan, 1991; Drucker, 1991; Enderwick, 1990; Guile and Quinn, 1988a,b; Lee, 1992; Quinn, 1992; U.S. Congress, Office of Technology Assessment, 1987).11 As in the production of manufactured goods, lean production of services is driven by attention to the value added at each stage of the product-realization process. In both cases, the focus is on eliminating steps and activities that do not contribute sufficient value to justify the cost of their inclusion in the process.

All of these factors together make the advantages deriving from economies of scale alone much less significant than they once were in many industries. The ability to respond quickly and flexibly to changing customer demands and the importance of rapidly absorbing new technologies in both product and process design require a revolution in both the internal communications of the firm and in its relationship with customers and suppliers, as well as a new level of attention to the optimal use of human talents in the work force. To compete in this new context, companies need to embrace continuous improvement of product and production processes, integrating R&D effectively with design, production, and marketing. It is also critical that they move away from their traditional arm's-length, adversarial relationships with suppliers and customers and toward more cooperative, mutually beneficial relationships with these important "external" sources of innovation. At the same time, they should rely less on managerial hierarchy and focus instead on cooperative work teams, employee empowerment, and continuous skill building at all personnel levels.

FIGURE 2.1 Rate of issuance of design changes, patterns of U.S. and Japanese auto manufacturers. SOURCE: After Sullivan (1987, p. 39).

Many features of the Japanese production system have been successfully adapted to the U.S. workplace by a number of U.S. and Japanese-owned firms. Reinforced by public- and private-sector initiatives, such as the Malcolm Baldrige Quality Award, the National Center for Manufacturing Sciences consortium, and the dissemination of International Organization for Standardization (ISO) 9000 quality standards by a host of private-sector industrial associations and management consulting firms, many U.S.-based manufacturing and service companies have begun to embrace such concepts as total quality management and concurrent engineering.12 Nevertheless, the spread of modern production practices throughout U.S. industry, beyond a relatively small group of U.S. and foreign-owned multinational companies, has been very slow.

Average U.S. industrial performance in this regard is particularly troubling, given that Japanese manufacturers continue to advance the competitive standard by investing considerably more than their U.S. counterparts in advanced manufacturing technologies and automation (See Table 2.2).13 Moreover, the rapid spread of lean production practices and advanced manufacturing technology through multinational companies to production facilities

TABLE 2.2 Use of New Technology in Manufacturing, Japan and the United States: 1988

|

|

Technology Users as a Percentage of Small and Large Manufacturing Enterprises1 |

Large/Small Ratio |

Japan/U.S. Ratio |

|||||

|

Type of New Manufacturing Technology Japanese definition (closest U.S. definition in parentheses) |

Japan |

U.S. |

Japan |

U.S. |

Small |

Large |

||

|

(a) Small |

(b) Large |

(c) Small |

(d) Large |

(e) |

(f) |

(g) |

(h) |

|

|

Numerically controlled and customized numerically controlled machines tools (NC.CNC machine tools) |

57.4 |

79.4 |

39.6 |

69.8 |

1.4 |

1.8 |

2.0 |

1.1 |

|

Machining centers (FMS cells or systems) |

39.4 |

67.4 |

9.1 |

35.9 |

1.7 |

4.0 |

7.4 |

1.9 |

|

Computer-aided design (and computer-aided engineering) |

39.1 |

75.2 |

36.3 |

82.6 |

1.9 |

2.3 |

2.1 |

0.9 |

|

Handling robots (pick and place robots) |

22.6 |

62.2 |

5.5 |

43.3 |

2.8 |

7.8 |

11.2 |

1.4 |

|

Automatic warehouse equipment (automatic storage and retrieval) |

10.9 |

44.9 |

1.9 |

24.4 |

4.1 |

13.1 |

24.1 |

1.8 |

|

Assembly robots (other robots) |

8.3 |

41.4 |

3.9 |

35.0 |

5.0 |

8.9 |

10.6 |

1.2 |

|

NOTES: 1 The comparisons between Japan and the U.S. are approximate since differences exist in technology definitions and employment size categories. Additionally, the Japanese data are enterprise-based, while the U.S data are establishment-based. The Japanese define a small manufacturing enterprise as having less than 300 employees and large enterprise as having 300 employees or more. The U.S. government defines small enterprises as firms with 50 to 499 employees and large enterprises as firms with 500 employees or more. (e)=(b)/(a). (f)=(d)/(c). (g)=(a)/(c). (h)=(b)/(d). SOURCES: After Shapira et al. (1992, p. 5). (a),(b) Ministry of International Trade and Industry (1989). (c),(d) U.S. Department of Commerce (1989a). |

||||||||

in developing countries, where wages are anywhere from one-fifth to one-tenth those of the U.S. work force, suggests that the pressures on U.S.-based companies to modernize their organization, management and plant will intensify greatly in the coming decade.14

At the level of national technology strategy and policy, the revolution in production systems places a growing premium on the rapid and widespread diffusion of "best practices" in the management of human capital and the production process as a whole throughout a nation's economy. It also reveals the importance of building and strengthening local or regional clusters of complementary skills, human resources, and technical infrastructure (Porter, 1990; Womack et al., 1990).

TOWARD A TECHNOLOGICALLY MULTIPOLAR AND INTERDEPENDENT WORLD

In parallel with the revolution in production systems and the changing character of technology-based competition in many industries, the past two decades have witnessed pervasive changes in the global distribution and organization of technological capabilities among nations. First, there has been a major shift in the postwar technological balance of power around the world. Whereas the United States in the early postwar period was both technologically and economically preeminent in almost every field, technological and economic power is now much more evenly distributed among North America, the Pacific Rim, and an increasingly integrated European Community. Whether the measure is investments in R&D as a share of gross national product, patent shares, or successful launches of new technology-intensive products and services, it is clear that the United States no longer dominates the world in scientific and engineering prowess. This is especially true if domination is defined as organizational mastery of technology development and application in all its aspects rather than merely being first to demonstrate new technologies in the laboratory or in prototype form.

Accompanying the gradual but steady equalization in basic national technical competence has been an unprecedented trend toward internationalization of production and associated technological activities through the expansion of international trade, investment, and cross-border corporate alliances. Capital, technology, industrial management systems, people, products, and services cross the borders of industrialized countries at unprecedented rates as part of everyday commerce. As a result, the process of technological innovation itself is becoming increasingly internationalized, and the pace at which new technology diffuses throughout the advanced industrialized world is accelerating. A product sold in France, Japan, the United Kingdom, or the United States is likely to be a global product—developed

in one country, based on research or design done in another, assembled by one multinational company from components made around the world, and sold and serviced by still another multinational company that has name recognition in a particular country's market.

Converging Capabilities in Technology Creation and Commercial Use

The nature and significance of the shifting global balance of technological power are illustrated by various comparative indicators of national scientific and technological strength. Comparisons of national trends in R&D investment, R&D work force expansion, patenting, and the publication of the results of scientific and technological research show that other industrialized nations are closing the gap with the United States in the capacity to produce and absorb new scientific and technological knowledge.

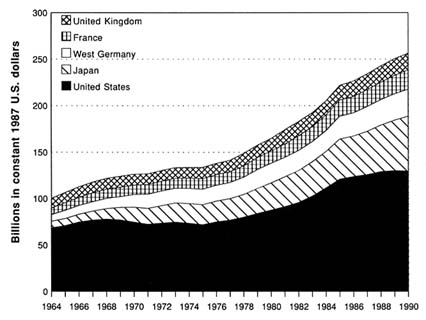

In total dollars invested in research and development, both defense and nondefense-related, the United States remains without rivals (see Figure 2.2). In 1990 the United States invested more money in research and development

FIGURE 2.2 National R&D expenditures, by country: 1964-1990.

SOURCE: National Science Board (1992, p. 73).

than Japan, Germany, France, and the United Kingdom combined. Similarly, total U.S. investments in basic research (research that advances scientific knowledge yet does not have specific commercial objectives) roughly equals the combined basic research investments of these four countries.15

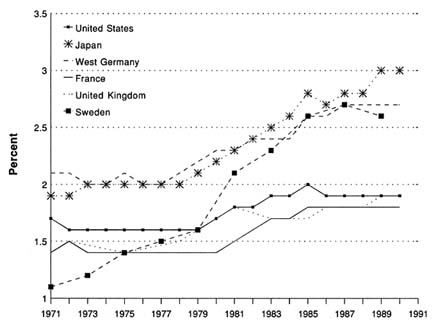

At the same time, international comparisons of trends in the ratio of total R&D investment to gross national product (GNP)—the R&D intensity of a nation's economic activity—show that Japan, Germany, and Sweden have surpassed the United States during the last decade. As of 1990 the United States invested 2.7 percent of its GNP in total R&D while Japan, Germany, and Sweden invested 3.1, 2.8, and 2.9 percent, respectively. However, since the contribution of defense-related R&D to the technology needs of the civilian economy is much more limited today than 20 years ago (see pp. 53–54 below), the more relevant measure of an economy's technical strength is its ratio of nondefense, or civilian, R&D investment to GNP. International comparisons of civilian R&D intensity document a large and widening gap between the United States and some of its major industrial competitors (see Figure 2.3).16 This ratio has remained fairly constant for the

FIGURE 2.3 Nondefense R&D expenditures as a percentage of gross national product, by country: 1971–1990. NOTE: Based on data valued in constant 1987 U.S. dollars. SOURCE: National Science Board (1992, p. 74).

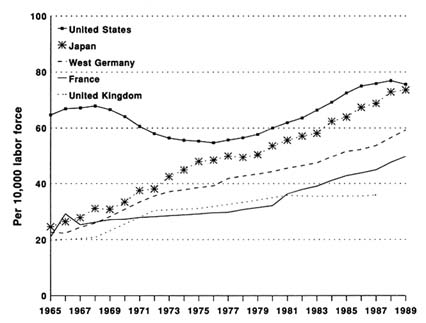

FIGURE 2.4 Trends in employment of scientists and engineers in R&D, by country: 1965–1989. NOTE: Latest available U.K. data is from 1988. SOURCE: National Science Foundation (1992, p. 67).

United States, ranging between 1.6 and 2.0 percent for the past 20 years. In contrast, over the same period, Germany, Sweden, and Japan have increased the civilian R&D intensity of their economies significantly. As of 1990 the United States invested 1.9 percent of its GNP in nondefense R&D, while Germany, Sweden, and Japan invested 2.7, 2.6, and 3.0 percent of their respective GNPs on nondefense R&D.17

Similarly international comparisons of R&D scientists and engineers as a share of the total work force of industrialized nations show that the distinctiveness of the U.S. postwar position has eroded in recent decades (see Figure 2.4). By 1989 Japan had nearly closed the gap with the United States, fielding 74 R&D scientists and engineers (most of whom were engineers.18) per 10,000 workers, compared with 76 in the United States.

In the area of production technology and associated methodologies, Japan has emerged as a world leader. As noted above, Japan has done more than any other nation to advance, codify, and disseminate a revolution in production systems captured by such concepts as just-in-time, total quality

management, design for manufacturing, and concurrent engineering. Japan's leadership in, and mastery of, these modern production methodologies have been well documented. In the automotive and photocopier industries, Japanese firms have demonstrated that they can develop new products in half to two-thirds the time with half the engineering work-hours required by their leading U.S. or European competitors (Barkan, 1991; Bebb, 1990; Clark and Fujimoto, 1991; Imai, 1990).19 As of the mid-1980s, Japanese industry already enjoyed the world's highest density of advanced manufacturing technology embodied in production equipment such as industrial robots, numerically controlled machine tools (NCMTs), and flexible manufacturing systems (FMS) (Edquist and Jacobsson, 1988; Shapira et al., 1992). see Table 2.2.

The redistribution of shares of world production and trade in high-technology manufacturing industries over the past decade is another proxy measure of the shifting balance of technological power.20 Between 1980 and 1990, world production of high-tech manufactures (calculated in 1980 dollars) more than doubled, while high-tech trade grew fourfold. The United States continues to host a larger share of world high-tech production than any other nation. However, between 1980 and 1990, its share of global shipments of high-tech manufactures fell 4 percentage points from 40 to 36 percent, while that of Japan increased from 18 to 29 percent (see Figure 2.5). Over the same period, high-tech manufacturing as a share of total U.S. manufacturing grew from 20 to 30 percent while it more than doubled in Japan from 16 to 35 percent. Between 1980 and 1988, the U.S. share of world high-tech exports fell from 27 to 23 percent, while Japan's rose from 10 to 15 percent. 21

In summary, the wide postwar gap between the United States and its major industrial competitors in both the creation and the commercial application of new technology has been closed in many areas of technology and is closing in others. Hence, the U.S.-dominated, technologically unipolar world of the 1950s and 1960s has given way to a world in which there are now multiple poles of technological power distributed throughout the globe.

Deepening Economic and Technological Interdependence

The past decade has seen an acceleration of the transition from a world of relatively discrete national technological systems toward one of globally interconnected and interdependent national technological systems. The internationalization of technology development and diffusion is following upon a profound deepening of international economic interdependence during the past 15–20 years, as evidenced by the growth of world trade, a virtual explosion of foreign direct investment, and the associated proliferation of international technical and logistical networks of firms. Nevertheless, the

FIGURE 2.5 Shares of global market for high-tech manufactures: 1980, 1987, 1990. NOTE: Based on data valued in constant 1980 U.S. dollars. SOURCE: National Science Board (1991, p. 402).

transition to a fully globalized world economy is still far from complete (Freeman and Hagedoorn, 1992; Patel and Pavitt, 1991, 1992; Pavitt, 1992).

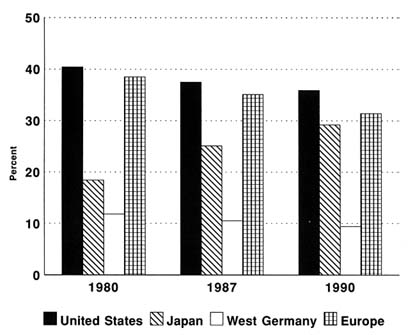

During the 1980s, trade in manufactured goods as a percentage of total manufacturing output of the 25 leading industrialized nations grew from 20 to 35 percent. Over the same period, trade in high-tech manufactures grew from 19 to 27 percent of these countries' total high-tech production. By the late 1980s, U.S.-based high-tech manufacturers were exporting more than 20 percent of their total output, while their Japanese and German counterparts were exporting 24 percent and 60 percent of their respective high-tech output.

Likewise, between 1980 and 1990, U.S. imports of high-tech products as a share of total U.S. domestic consumption of these goods nearly doubled from 8 to 14 percent (National Science Board, 1991). See Table 2.3. Over the same period, high-tech import penetration of the major European economies, already on average 3 to 4 times the U.S. level in 1980, increased

TABLE 2.3 Import Share of Domestic Market for High-Tech Manufactures, by Country: 1980, 1986, 1990

|

High-Tech Manufactures |

1980 (percent) |

1986 (percent) |

1990 (est.) (percent) |

|

United States |

8.0 |

12.1 |

13.8 |

|

Japan |

6.6 |

8.4 |

9.2 |

|

West Germany |

25.1 |

31.2 |

41.2 |

|

France |

33.2 |

45.1 |

55.2 |

|

United Kingdom |

29.1 |

38.8 |

42.1 |

|

Italy |

29.3 |

44.5 |

43.6 |

|

SOURCE: National Science Board (1991,p.405). |

|||

FIGURE 2.6 Growth in world trade, output, domestic investment, and foreign direct investment: 1975–1991. NOTE: E based on 1991 estimates. SOURCE: U.S. Department of Commerce, International Trade Administration, Office of Trade and Economic Analysis, unpublished data, 1993.

significantly to more than 40 percent in Germany, Italy, and the United Kingdom, and more than 55 percent in France. Japan, on the other hand, which began the decade with an absolute level of high-tech import penetration below that of the United States, experienced much slower growth of import penetration during the 1980s than any other major industrialized country.22 Trade data by themselves, however, grossly understate the deepening of international economic interdependence over the past decade.

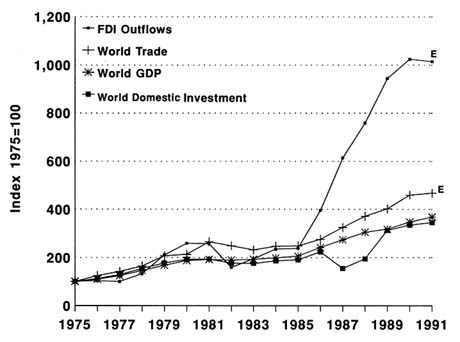

Since the mid-1970s the main driver of global economic integration has been the growth of foreign direct investment or multinational corporate enterprise.23 In the past decade alone, world flows of foreign direct investment have tripled, growing two and one-half times faster than world trade since 1983 (see Figure 2.6). More than three-fourths of the growth in world stock of foreign direct investment was accounted for by non-U.S. companies, and nearly a quarter of the growth was absorbed by the United States.

During the past decade, foreign direct investment has assumed an increasingly important role in all major industrialized economies, again, with the notable exception of Japan. As the data in Table 2.4 show, most of the United States' major trading partners except Japan were significantly more

TABLE 2.4 Foreign-Controlled Firms' Share of Total Business Enterprise R&D Expenditure, Employment, and Product Shipments in Manufacturing Enterprises in Six Countries

|

|

% Share Business Enterprise R&D Expenditure 1989 |

$ Share Employment 1989 |

% Share Product Shipments 1989 |

|

United States |

8.8 |

10.0 |

14.9 |

|

France |

12.4 |

22.1 |

26.7 |

|

United Kingdom |

17.0 |

14.8 |

23.5 |

|

Sweden |

13.6 |

14.0 |

15.1 |

|

Germany |

18.1 |

21.7 |

|

|

Canada |

52 |

34.0a |

48.6b |

|

Japan |

1.0 |

1.1 |

2.3 |

|

NOTE: The United States defines foreign-controlled firms as nationally incorporated and unincorporated business enterprises in which foreign persons have at least a 10 percent interest. Some nations define foreign-controlled firms at a higher level of equity interest. * Data not available a 1986 data b 1987 data SOURCES: Organization for Economic Cooperation and Development (1992b, Table 59 and 60, and unpublished data, 1993). |

|||

TABLE 2.5 Measures of the Proportion of Foreign Direct Investment in the U.S. Economy

|

|

Percent |

|

Foreign direct investment position in the U.S. economy as a proportion of total U.S. domestic net worth (1991) |

5.3 |

|

Total assets of U.S. affiliates in manufacturing as a proportion of total assets of all U.S. manufacturing companies (1990) |

18.6 |

|

Stockholder's equity of U.S. affiliates in manufacturing as a proportion of stock-holder's equity of all U.S. manufacturing companies (1988) |

12.9 |

|

Sales of U.S. affiliates in manufacturing as a proportion of sales of all U.S. manufacturing companies (1990) |

16.4 |

|

Employment of nonbank U.S. affiliates as a proportion of total U.S. private nonbank employment (1990) |

5.0 |

|

Employment of U.S. affiliates in manufacturing as a proportion of all U.S. manufacturing companies (1990) |

10.8 |

|

Value added of nonbank U.S. affiliates as a proportion of U.S. gross domestic product (1989) |

5.1 |

|

Value added of U S. affiliates in manufacturing as a proportion of all U.S. manufacturing companies (1989) |

13.4 |

|

SOURCES: From U.S. Department of Commerce (1991, and unpublished data, International Trade Administration, Office of Trade and Economic Analysis, 1993). |

|

dependent on foreign direct investment by the late 1980s than the United States itself. The affiliates of foreign-owned companies accounted for 21 percent or more of the total domestic sales of manufactured goods in the United Kingdom, Germany, France, and Canada, and only 15 percent of total U.S. manufacturing sales. Nevertheless, no other major industrialized nation experienced growth in its dependence of foreign direct investment during the 1980s as rapid as that of the United States.

Between 1980 and 1991, foreign direct investment in the United States expanded nearly fivefold.24 By 1990 foreign-owned companies controlled more than $1.5 trillion in assets in the United States and employed roughly 4.7 million Americans. In manufacturing alone the U.S. affiliates of foreign-owned firms accounted for approximately 19 percent of total U.S. manufacturing assets, 16 percent of U.S. manufacturing sales, 13 percent of U.S. manufacturing value added, and nearly 11 percent of U.S. manufacturing employment in 1990 (see Table 2.5). 25 Currently the subsidiaries of foreign-owned firms operating in the United States are estimated to account for more than one-third of U.S. imports and one-fifth of U.S. exports (U.S. Department of Commerce, 1991).

Likewise, the multinational presence of U.S.-owned companies has expanded greatly during the past decade both in dollars invested abroad and in

the number of U.S. companies that have gone multinational. In 1990 the assets of overseas affiliates of U.S. companies were in excess of $1.5 trillion, and more than one-third of U.S. multinationals' earnings came from overseas operations. That year, U.S.-owned operations abroad employed more than 6.7 million people, drawing heavily on local production, technical, and management talent. Already in 1986, sales by the foreign affiliates of U.S. high-tech companies were twice as large as U.S. high-tech exports, and foreign affiliate assets represented more than 40 percent of the total assets of U.S. high-tech manufacturing industries (Conference Board, 1992; Julius, 1990; National Science Board, 1989; U.S. Department of Commerce, 1992c).26

In summary, economic and technological interdependence among industrial nations is deep and likely to continue to deepen. The depth of interdependence experienced by the major industrialized nations varies considerably—from the highly ''internationalized" economies and national technology enterprises of Western Europe, to the historically more autonomous yet rapidly internationalizing U.S. economy and technology enterprise, to the relatively autonomous and more slowly internationalizing Japanese economy and technology enterprise. Although trends in the global economy suggest that these asymmetries in dependence will diminish with time, they are unlikely to disappear in the short term.

The Internationalization of Technology Development and Diffusion

The rapid expansion of foreign direct investment during the 1970s and 1980s was accompanied by major changes in the conduct and spatial organization of corporate technical activities worldwide. From the mid-1950s to the late 1970s, the development of new product and process technology was, for the most part, an exclusively "domestic" as well as "in-house" activity for U.S. companies.

Since the late 1970s, however, changes in the global competitive environment have fostered an increasingly international approach to technology development and application on the part of U.S. and foreign multinationals. While affecting different industries to different degrees, increased global competition, the advantages of collocating production and R&D in many industries, national "managed trade" or "industrial" policies of varying scope, the promise of wider markets, and the availability of cost-effective sources of new technology and specialized technical competence overseas have all played a role in shifting corporate technology strategies. Responding to the challenges and opportunities associated with this new environment, multinational companies in many industries have begun to reorganize their technical activities to optimize them on an international basis.

In 1990 U.S. companies invested more than $10 billion in R&D overseas,

nearly 14 percent of total company-financed industrial R&D in the United States that year. Leading the charge have been U.S. multinational companies in the computer, telecommunications, microelectronics, pharmaceuticals, and automotive industries, which now conduct anywhere from one-quarter to one-third of their R&D work abroad (U.S. Department of Commerce, 1992c). However, foreign multinationals, whose ranks expanded dramatically during the last two decades, have also increased their overseas R&D spending since the early 1980s. In the United States alone the U.S. subsidiaries of foreign firms accounted for more than $11 billion, or more than 15 percent of total U.S. company-financed industrial R&D in 1990. By 1990 at least 115 foreign companies had established 254 R&D facilities in the United States; 150 of these R&D facilities were established by Japanese companies, 95 by European companies, 6 by Korean companies, and 3 by Canadian companies (Dalton and Serapio, 1993).27

Multinational R&D spending alone, however, clearly understates the extent to which private-sector technology development, application, and diffusion are internationalizing. As the population of U.S. and foreign multinational companies has mushroomed, these firms have, in turn, helped cultivate increasingly dense global technical and logistical networks of companies that include a much broader population of "domestic," technically innovative suppliers, vendors, and distributors.

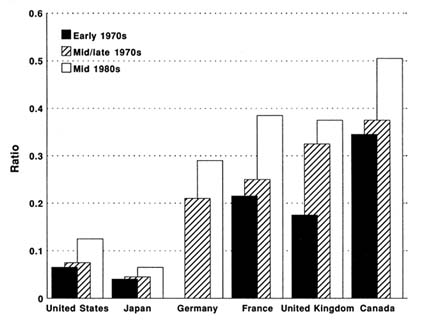

One measure of the growing importance of these global networks is the rapid growth in volume of intermediate inputs for final production obtained from international rather than domestic sources (see Figure 2.7).28 A recent study of sourcing patterns for manufactured intermediate inputs in six industrialized countries from the early 1970s to the mid-1980s has shown that the direct import of these inputs from abroad increased more rapidly than domestic sourcing in all of the countries surveyed. As a result, by the mid-1980s, foreign sourced manufactured inputs were 50 percent of domestically sourced inputs in Canada and between 30 and 40 percent of domestically sourced inputs in France, Germany, and the United Kingdom. Much lower levels of foreign sourcing were observed for the United States and Japan, although both countries experienced significant increases in foreign sourcing between the mid-1970s and the mid-1980s (Wyckoff, 1992).

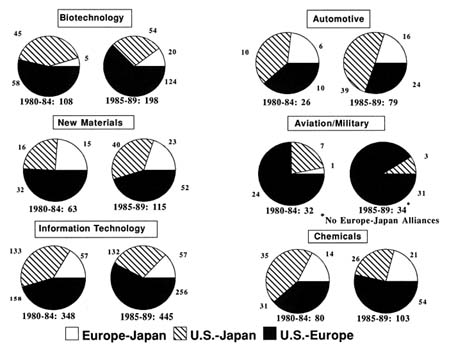

Another window on the growth of collaborative sourcing and development of technology by firms is provided by the surge in the number of corporate technical alliances (such as patent licensing and joint R&D) during the past decade. One recent survey has documented a steep rise in the number of transnational technical alliances among companies since the late 1970s (Hagedoorn and Schakenraad, 1993). While three broad industrial areas—information technology, new materials, and biotechnology—have experienced a particularly high level of alliance activity since 1980, other industries such as aerospace, automotive, and chemicals have also experienced

FIGURE 2.7 Ratio of imported to domestic sourcing of inputs, average of manufacturing goods, by country. NOTE: Early 1970s information for Germany is not available. SOURCE: Wyckoff (1992, p. 6).

growth in the number of international corporate alliances in recent years (see Figure 2.8).

Collectively the internationalization of R&D, the growth of global technical and logistical networks, and the rapid expansion of world high-technology trade define a powerful and pervasive trend toward internationalization of technology development and diffusion. While the current extent of internationalization is greater in certain industries and certain countries than in others, and should not be overstated, the trend is well established and gathering momentum. 29 In many sectors new technological knowledge is becoming a global commodity, rapidly accessible to any organization with sufficient incentive and technical sophistication to absorb it. In this new environment, U.S. prosperity, military security, and other vital national interests will depend increasingly on the ability of U.S. public- and private-sector actors to access and harness the technological output and capabilities of other nations as well as on that of global technical networks that defy national classification.

FIGURE 2.8 Number of new transnational corporate technology alliances, by industry: 1980-1989, SOURCE: Hagedoorn and Schakenraad (1993).

THE GEOPOLITICAL PREMIUM ON ECONOMIC STRENGTH

For more than four decades the military and geopolitical rivalry between the United States and the Soviet Union defined the global balance of power and served as a major driver of U.S. science and technology policy. U.S. military strategy and national security have been based on the development of U.S. superiority in military technology and on the strength of the U.S. industrial base. Throughout the 1950s and 1960s U.S. military strength and the nation's economic and commercial technological muscle were, for the most part, mutually reinforcing; public-sector investments in defense-related technologies complemented private-sector investment in commercial technological preeminence. In turn the growth of new industries and the U.S. economy overall ensured that the resources needed to maintain the nation's military strength and defense technology base were available.

During the 1960s and 1970s, even as other advanced industrialized nations closed the gap with the United States in economic prosperity and

technological competence, the United States was able to continue to leverage its military superpower status to advance U.S. economic and political interests in negotiations with its allies and trading partners. The 1980s, however, were a time of dramatic change. As recently as 1980 the Cold War was in full swing and substantial increases in U.S. government defense spending (including defense R&D) were based on arguments setting forth the Soviet threat. At the same time, the exposure of the United States to foreign trade and investment (in particular, by Japanese companies.30) was just beginning to be felt. Over the course of the 1980s, the perceived threats to U.S. prosperity and security switched positions. On the one hand, the collapse of the Soviet Union seems to have put military security within reach. On the other hand, seemingly intractable U.S. trade and fiscal deficits, intensive foreign competition both at home and abroad in many major industries, and growing U.S. dependence on foreign sources of capital and technologically advanced products and components have raised concerns about U.S. economic security.31 These changed national priorities suggest the need to reevaluate U.S. technology policy and strategy.

In this new world, leadership in military technology will remain critical to U.S. national security and U.S. influence abroad, but the level and nature of demands on the nation's defense capability have changed. Defense budgets are contracting and are likely to continue to do so for the foreseeable future. As a result, the U.S. national security missions' claims on, and contribution to, the nation's technology enterprise are likely to decrease.32

It has also become apparent that leadership in critical military technologies will be increasingly built on, and sustained by, leadership in the development and competitive commercial application of their corresponding, and often "progenitor" civilian technologies. This is because civilian technological advance—driven by global economic competition—is now pacing technological advance in many fields critical to the national defense, especially in respect to materials, components, and subsystems.

In the 1950s and 1960s, when the relative national investment in space and defense R&D was much larger than it is at present, many building-block technologies (solid-state electronics, computer technology, aeronautics and jet propulsion, and nuclear power) were in an early phase of their technological life cycle. This situation was favorable to the spin-off approach that U.S. technology policy had grown to rely on, implicitly if not explicitly, for substantial contributions to the generation of new commercial technology in the postwar period.

Beginning in the mid-1960s, many of these new technologies moved into more mature phases in which advances became more applications-specific and technologies derived from military R&D and procurement in the earlier period had already been adopted by civilian industries. Thus, in semiconductors and computers especially, the growth rate of commercially

oriented R&D supported by industry, both in the United States and worldwide, far outpaced the growth of government-funded R&D in these technologies. As this change has occurred in more and more sectors, "spin-off" has been transformed into "spin-on" in all but a few sectors that are highly specialized to military requirements (such as nuclear weapons design and fighter aircraft). Indeed, only in aerospace, gas turbines, jet engines, specialized sensors, laser applications, and techniques of systems engineering and systems integration has the military provided a significant impetus for technological advance in recent years. In most other frontier areas the primary impetus to technological advance has been provided by commercial markets and economic competition.33

Since the late 1970s four new generic areas of technological advance have opened up: optoelectronics and fiber optics, advanced engineered materials, biotechnology, and software engineering, including artificial intelligence. With the exception of health-related research in biotechnology, which has been driven largely by public support from the National Institutes of Health, advances in these technological areas have been driven primarily by commercial demand. None of these new technologies has depended to more than a limited degree on support from the nation's military and space missions.34

These new areas of technological advance have been characterized by two conditions. First, military and space investments (both R&D and procurement) by the federal government have generated much less comparative advantage for the United States in recent years than earlier generic technology investments. Second, such advances as occurred in these newer technologies have at the outset been much more market-driven than earlier advances in integrated circuits, computers, and nuclear power.

In summary, (1) the particular demands on the U.S. national defense capability are substantially changed, (2) the national security mission's claim on, and contribution to, the nation's technology enterprise are dropping, and (3) the importance of defense-specific technologies has declined while the dependence of defense technology generally on technologies developed first in the commercial sphere is rising. 35 As a result, the nation's traditional approaches to defense procurement and defense research and development need to be reexamined—the old strategies seem unlikely to yield the same national security benefits as they did in the past. The increasing dependence of U.S. military leadership on the commercial economy, and specifically on commercially driven technological advance (a growing fraction of which is occurring outside the United States), should stimulate fresh thinking about the current composition and strategy of public-sector investment in science and technology (Carnegie Commission, 1990, 1992b; Center for Strategic and International Studies, 1991; Moran, 1993).

CONCLUSION: WEAKNESSES EXPOSED

Broad changes in the global environment—the revolution in production and innovation systems, the shift in the global balance of technological power in the context of deepening economic interdependence, and the end of the Cold War—alter the context for national technology strategy and policy and require rethinking of appropriate policies.

-

First, the accelerating pace and the increasingly multidisciplinary an science-based character of technological change call for greater breadth and better balance in the R&D portfolio of companies and the nation. Ensuring competitive capability across a broad range of industrial technologies (including infrastructural and pathbreaking technologies) demands a higher degree of collaboration among firms, and between firms and other private and public R&D institutions. Tracking and acquiring new technology from outside corporate and national borders have become a necessary complement to internal technology development.

-

Second, the revolution in production systems demands that companies (supported by government policies) adopt new organizational structures that rely less on managerial hierarchy and functional compartmentalization and focus instead on improved intrafirm communication and coordination, teamwork, employee empowerment, and continuous skill building at all personnel levels. It also places a premium on public policies that support the creation and development of local or regional clusters of particular complementary skills, human resources, and technical infrastructure.

-

Third, the shift to a technologically multipolar world, increasing global competition, and the trend toward internationalization of production and innovative activity have made it imperative that individual companies and national economies (supported by government policies) work to harness global technology and high-technology markets more effectively to advance their respective interests.

-

Finally, the breakup of the Soviet Union and the changed relationship between commercial and military technologies have substantially changed the demands on the U.S. national defense capability, reduced the number of defense-specific technologies, and dramatically increased the opportunity for defense technology to come from the commercial sphere. Moreover, current and ongoing U.S. defense cuts may displace a significant fraction of the nation's advanced technical work force and thereby risk dissipating their accumulated skills and competencies. 36

Each of these broad changes in the global political and economic environment exposes serious weaknesses in the United States' current portfolio of technological activity. The revolution in production systems focuses attention on what many view as a legacy of underinvestment in, and managerial

inattention to, process technology, human resources, and the social organizational aspects of technology's introduction and use in the workplace. Ongoing defense cuts, the changing relationship between civilian and defense technology, and the changing nature of industrial innovation more generally raise serious concerns about the present size, composition, and intensity of the nation's civilian R&D effort. And the shifting balance of technological power and deepening technological interdependence expose a parochialism in U.S. private and public technology strategies and policies that could easily undermine the nation's ability to harness global technology and markets.

Collectively the challenges and opportunities presented by these changes in the global context underscore the need for the United States to make national economic development an explicit objective of federal technology policy. The following chapter examines the major strengths and weaknesses of the U.S. technology enterprise as revealed by these global trends.

NOTES

|

1. |

This is true for two reasons. First, the fields that are most unique to defense and that may be regarded as single-purpose are largely concentrated in the area of strategic systems, which are most likely to be of lower priority in the coming defense environment. Second, the coming era of "smart" conventional weapons is more dependent on "dual-use" technologies, where commercial R&D is driving the pace of advance to an increasing degree. At the same time, these technologies were in a much earlier stage of their "technological life cycle" when defense was the driving force in their development, which was much less application-specific. |

|

2. |

See, for example, Chandler (1962, 1977, 1990); Hughes (1983); Porter (1990); Rosenberg (1982); Scherer (1980). |

|

3. |

Despite the increasingly science-based quality of commercial technology, there is still a large component of tacit knowledge embodied in the actual practice of all technology. Indeed, this is even true in the laboratory practice of the purest science. Hence, it is easy to overstate the science-based nature of technological competition. |

|

4. |

For a comprehensive discussion of technology fusion as it applies to manufacturing industries, and the revolutions in mechatronics and optoelectronics, see Kodama (1991, chapter 5). For other examples of technology fusion in the service sector, consider the many service industries that have sprung from or have been radically transformed by the fusion of information technology and telecommunication. See Guile and Quinn (1988a,b) and Quinn (1992). |

|

5. |

During the past decade other industrialized nations have greatly increased their collective public- and private-sector investments and overall strength in many areas of pathbreaking and infrastructural technology. See Chapter 1, p. 17, for definition of these types of technology. U.S. public- and private-sector investment in these technologies, however, is generally seen as inadequate to the needs of U.S. industry (Tassey, 1992; U.S. Department of Commerce, 1992b). |

|

6. |

Part of the problem is the different natural cycle time of various elements in the new product development and manufacturing process. Generations of components and subsystems follow each other in much shorter succession than the overall design of a more complex piece of equipment. Thus, it is often important to configure the whole product development and manufacturing process to absorb incremental improvements of many different rates, resulting in an integrated process of "continuous improvement" rather than large individual leaps. |

|

7. |

Womack et al. (1990) and Jaikumar (1989) have shown that Japanese companies often get a lot more mileage out of flexible manufacturing systems (FMS) than U.S. companies using the same equipment. In particular, the Japanese make a much larger variety of products on the same system, thus taking much greater advantage of its flexibility feature. |

|

8. |

Interviews by several independent observers of workers who have worked under both systems at NUMMI support the statistical evidence in the sense that workers express far more satisfaction with the new system (often in very strong language). See, for example, Adler (1993) and Vierling (1992). |

|

9. |

The study by Berggren et al. (1991) also challenged the assertions of other "lean production" studies regarding the productivity and profitability of "lean" Japanese transplants. Among other things Berggren et al. suggest that the heavy focus on the productivity consequences of workplace organization has led lean production advocates to overlook the fact that Japanese transplants have invested heavily in new process technology and that many of them are world leaders in automation. Furthermore, the authors assert that the bookkeeping practices of some of these transplants raise questions regarding their claims of high profitability. |

|

10. |

Barkan (1991), Clark and Fujimoto (1991), Lee (1992), and others have documented the importance of high relative productivity of engineering services in product development and design to the superiority of the Japanese system of manufacture. They have also observed that the Japanese principles of product design are heavily derived from Japanese experience in manufacturing systems. In other words, the social system of manufacturing seems to have come first, and the lessons learned from that experience were then applied "upstream" in the design and development process. |

|

11. |

Consider, for example, the rise of Federal Express to the pinnacle of the package delivery business (Nehls, 1988, Quinn 1992), or the organizational revolutions at American Express, the General Mills Restaurant Group, and Wal-Mart. Organizational changes made possible by the effective use of information and telecommunications technology and the application of customer-focused, lean production principles have allowed these companies to deliver a wider range of better quality services to customers at lower costs (Quinn, 1992, pp. 136–145, 319–320). With regard to Wal-Mart stores, the fastest-growing, most profitable major U.S. retail chain of the past decade, Quinn notes that the retailer has "perhaps the best technology-based communications system in its field, including satellite and interactive video links to many stores. With its detailed stock management systems, it can delegate and control to the counter level. This allows its personnel to run a 'store within a store' for better personal motivation and more focus on the customer." |

|

12. |

For further discussion of these and other initiatives, see National Center for Manufacturing Sciences (1992a,b), Peach (1992), U.S. General Accounting Office (1991). |

|

13. |

See also Chapter 3, pp. 74–76. |

|

14. |

A recent U.S. Congress, Office of Technology Assessment (1992b) report on U.S.-Mexico trade found that export-oriented Mexican firms undercut U.S. wages for production workers by at least 5 to 10 percent, while in some cases achieving comparable levels of quality and productivity. The report concluded that in the future, multinational firms would have increasing latitude in locating production where labor is cheap and other conditions for modern manufacturing can be met. For a more optimistic assessment of the current and future attractiveness of the United States as a location for manufacturing activity by multinational corporations, see National Research Council (1992a). |

|

15. |

See Irvine et al. (1990) and Chapter 3, Figure 3.1. |

|

16. |

More than one-quarter of U.S. R&D investment is dedicated to national security needs—that is, researching and developing technologies of limited applicability to the civilian economy. For this reason, the committee considers the ratio of civilian or nondefense R&D to the gross national product a more meaningful measure of the relative technical intensity of national economies than the ratio of total R&D to GNP. Moreover, while it can be argued that economies of scale in R&D yield particular advantages to the United States because of its large overall investment in nondefense R&D (more than that of Japan and Germany combined), the committee does not believe that these advantages compensate for the U.S. disadvantage in civilian R&D intensity to any significant degree. For further discussion of the diminishing relevance of national security-related R&D to the nation's commercial technology base, see Chapter 2, pp 53–54. |

|

17. |

The latest year for which total and nondefense R&D data for Sweden are available is 1989. It is worth noting that those countries that invest the highest proportion of their GNP on nondefense-related R&D are also countries noted for their policy emphasis on (and relative success with) the adoption and diffusion of technology—Switzerland, Germany, Sweden, and Japan. This line of argument suggests differences in the "character" of R&D and the organization of innovative activities between these countries and the United States. For further discussion, see Edquist (1990); Ergas (1987); Kodama (1991); Nelson (1993); and Patel and Pavitt (1992). Mansfield's comparative research on the allocation and productivity of industrial R&D resources among matched sets of U.S. and Japanese firms notes that the Japanese firms devote considerably larger shares of their total R&D investment to scanning and assimilating technologies developed beyond the firm, incremental improvement of existing products and processes, and process technology in general (Mansfield, 1988a, b). Also see Chapter 3, pp. 76–83 below, for further discussion of the composition and management of the U.S. civilian R&D portfolio. |

|

18. |

Despite gray areas in definition and classification of scientists and engineers, the disparities here are so great they cannot be offset. |

|

19. |

See discussion of concurrent engineering on pp. 36–37 above. |

|

20. |

For definition of high-technology products, see Chapter 1, note 28. |

|

21. |

See National Science Board (1991, pp. 401–407. appendix tables 6-2, 6-3, 6-4, 6-7). High-tech production data for 1988–1990 are estimates. All production and trade data are figured in constant 1980 dollars. |

|

22. |

Intra-industry trade data also underline the anomalous position of Japan among advanced industrialized countries. See Lincoln (1990). It should be noted that there is considerable debate as to the magnitude and causes of these apparent differences in the level of foreign penetration of national economies, and hence, whether it is even useful or accurate to explain these differences as asymmetries of access. For a sampling of this debate, see Japan Economic Institute (1991); Krugman (1991); Lawrence (1991a,b); Lincoln (1990); Saxonhouse (1989, 1991). |

|

23. |

Foreign direct investment in the United States, as defined by the U.S. government for reporting and statistical purposes, is the ownership by a foreign person or business of 10 percent or more of the voting equity of a firm located in the United States. An equity interest of 10 percent or more is considered evidence of a long-term interest in, and a measure of influence over, the management of the company (U.S. Department of Commerce, 1992d, p. m-1). Although some nations define foreign direct investment at a somewhat higher percentage of voting equity than the United States, analysts of global foreign direct investment trends do not consider these differences to be very significant. |

|

24. |

In 1990 total foreign direct investment inflows into the United States fell dramatically from $72 billion in 1989 to $26 billion, the smallest amount since 1985. In 1991 and 1992 the downward trend continued in foreign direct investment inflows. There is some debate whether 1990 marks a fundamental turning point or an aberration in the long-term growth trend (U.S. Department of Commerce, 1992a). |

|

25. |

Foreign-owned firms' share of manufacturing value-added is for 1989 (U.S. Department of Commerce, unpublished data, 1993). |

|

26. |

According to data presented in Julius (1990), U.S. companies' foreign affiliate sales in some countries were much larger than U.S. exports to these countries (five to one in United Kingdom). In other countries, however, foreign affiliate sales were only marginally greater than U.S. exports (only about 10 percent larger in Japan). |