The Industrial Green Game: Pp. 1–34.

Washington, DC: National Academy Press.

The Industrial Green Game: Overview and Perspectives

DEANNA J. RICHARDS AND ROBERT A. FROSCH

The industrial green game involves the smart design of products, processes, systems, and organizations, and the implementation of smart management strategies that effectively harness technology and ideas to avoid environmental problems before they arise. The green game values environmental quality across the board in production and consumption activities and integrates environment as a strategic element in the design and management of economic enterprises.

The rules of the green game recognize that the entire system of production and consumption determines environmental quality. Environmental impacts are a function of the way services are provided and the way goods are produced, delivered, used, and disposed of. Production and consumption are considered together, because gains made by controlling, reducing, or minimizing pollution from production can be soon overshadowed by the impacts from concurrent increases in the scale of demand for those services and goods from a growing customer base.1 Today, the scale of production and consumption is global. Advances in transportation and communication technology underlie a rapidly increasing internationalization of production and consumption. The regular flows of commerce—movements of people, raw materials, final goods, intermediate goods, and capital—cross national boundaries in enormous volumes on a daily basis. Indeed, we no longer live in small groups interacting with local ecosystems. Now, through the industrial support systems we have built and continue to evolve, we interact with the global environmental system as a whole. Yet, most recent environmental policy has focused on pollution from the point of view of industrial production.

At the same time, advances in areas like materials and production technologies are creating new types of companies. While the world has a long history of multinational companies, there is no precedent for the large and growing number

of companies (or groups of companies) that now manage truly integrated global production systems and direct their products to an increasingly homogenous global market. In addition, the primary opportunities to reduce the adverse environmental impacts of economic activities continue to be technological. Conservation actions—such as reducing waste, or switching off lightbulbs—are important but among the simpler strategies one may adopt. Efficiency improvements—such as modernizing with more energy-efficient systems or re-engineering so that little or no waste is produced, or developing and deploying processes and systems that offer superior environmental quality—provide the greatest opportunity for improving environmental quality. These improvements often are driven by innovations in technology. Such advances, applied usually by private firms, are the means by which societies become less resource dependent and develop and deploy environmentally safer materials, processes, and systems. In this context, corporate decisions and the personal choices of consumers are important determinants of environmental quality.

The green game requires designing and manufacturing products (including facilities) and providing services by taking an environmental life cycle approach. This approach involves understanding and managing the environmental impacts of the material and energy inputs and outputs associated with the product or service from the extraction of the raw materials, through their many life stages (including reuse and recycle) to their reincarnation in new products or disposal.

The game calls for considering and managing the environmental impacts of the many activities that are reflected in the final costs of everyday goods and services. These activities include designing, developing, or making the product or creating the service; transporting, marketing, selling, maintaining or repairing the product; or even taking back the purchased product at or before the end of its useful life.

A systems approach is needed to play the game well. Industrial ecology2 represents such an approach. In the noisy market of environmental terms and buzzwords, industrial ecology has become a short phrase for many ideas related to improving environmental quality with economic concerns in mind. Industrial ecology can be thought of in much the same way ecologists view ecology, as the study of the interactions among organisms and between organisms and their physical environment (Raven et al., 1995). Ecology is the study of processes and interactions, not a scientific prescription for solutions to environmental changes. Ecological study helps reveal how natural ecosystems operate, evolve, and are affected by the actions of humankind. Ecology provides the knowledge base that is then applied in a range of activities from forestry and agriculture to designing artificial wetlands and restoring the health of ecosystems. Similarly, industrial ecology views environmental quality in terms of the interactions among and between units of production and consumption and their economic and natural environments, and it does so with a special focus on materials flows and energy use. It also provides a strong basis for integrating environmental factors at various

scales: the microlevel (industrial plant), the mesolevel (corporation or group or network of industrial activities that operate as a system for specific purposes), and the macrolevel (nation, region, world).

Industrial ecologists are interested in how industrial systems will evolve to meet environmental objectives. The industrial ecologist seeks to understand the current workings of industrial systems, how new technologies and policies may change the operation of those systems, and what impacts different industrial strategies may have on the economy and on environmental quality. This, then, forms a basis for wise decision making and good industry practices, driven by inquires such as those shown in Box 1.

This volume builds on earlier efforts of the National Academy of Engineering (NAE) in the area of technology and the environment.3 It presents ideas for improving environmental quality through better design and management in industrial-related production and consumption activities. Concerns related to the impact of human-devised systems on the biosphere are addressed in Engineering Within Ecological Constraints (Schulze, 1996). The accompanying papers we presented at a 1994 NAE International Conference on Industrial Ecology. This overview draws on the papers as well as observations from two NAE workshops addressing the impact of the services sector on the environment, held in October 1994 and July 1995.

This overview first examines the changes to the playing field on which the green game is played. The rules of the game are defined foremost by a set of continually evolving regulations. Yet flexibility is need to take advantage of new technologies, changing economics, and new modes of production that are in increasing use around the world. The green game has to be responsive to community concerns, including environmental justice. It has to respond to improved information and knowledge about environmental impacts, and their causes and potential solutions. All of this requires vigilance—to take advantage of opportunities for environmental improvement and to respond to unanticipated environmental consequences of technology and economic growth. It is ultimately driven by the costs of taking specific actions.

Next, the overview considers an old idea (Commoner, 1971) for managing materials: recycling. Many environmental impacts result from the accumulation in the biosphere of man-made and extracted raw materials. Therefore, materials management for the industrial green game can utilize systems that use waste as useful materials and substitute materials that improve environmental quality; systems for multiproduct cycles; an systems based on service or functionality.

The overview then looks at the information tools needed to guide environmental decision making within a corporation. A firm's green game is enhanced by understanding the environmental impacts inherent in the selection of materials and processes, by assessing associated environmental and health risks, and by improving the ability to track and assign responsibilities for environmental costs using effective performance measures. It is also critical to gain information about

|

BOX 1 Questions for the Industrial Ecologist

|

consumer attitudes toward the environment. This allows identified concerns to be managed, improves the reporting on a firm's environmental record, and is key for any environmental marketing a firm may do. Further, better knowledge of public understanding can be useful in communicating and managing environmental risks, and in responding to unanticipated environmental consequences of technology an economic growth, which are inevitable in the green game.

Finally, the overview examines tools that can provide clues for improving the way firms play the industrial green game. In this regard, there is an important government role in collecting and providing information that is unlikely to be gathered by private industry but which, if available, could have a large impact on improving the green game.

THE CHANGING PLAYING FIELD

The industrial green game is complicated by the fact that environmental costs are often not reflected directly in the value of products or services. If they were, products and services that impact the environment more than others would be priced accordingly. In practice, however, the cost of environmental damage is often incurred as the cost of protecting human health and the environment, and this expense is passed on essentially as overhead to the public. Subsidies further distort these costs by giving market preference to certain industries or practices.

The difficulty in determining environmental costs is illustrated by considering effluent charges. The notion of applying effluent charges is based on the seemingly logical rationale that polluters should pay for their actions. For example, a factory whose effluent impacts adversely fish populations imposes a cost on commercial fishermen without their consent. As long as the cost of the pollution is not incurred by the factory, it has no incentive to reduce the pollution. As long as factory ownership is unclear, the polluter has "free" access to the fishing hole for waste disposal. It is difficult, however, to determine the appropriate charge (or penalty) that will generate the "ideal" level of pollution, without knowing the costs of pollution damages. It is because this type of information is absent or difficult to determine that the industrial green game is so difficult to play. Some of the external costs of pollution have been internalized through environmental regulations, which often are designed to address single environmental concerns. Several U.S. regulations were enacted in response to crisis in various environmental media (for example, the Clean Water Act to address water pollution and the Clean Air Act to address air pollution) or to address specific pollution-management concerns (for instance, the Resource Conservation and Recovery Act to address solid waste management and the Comprehensive Emergency Response and Liability Act [also known as Superfund] to remediate contaminated land and groundwater).

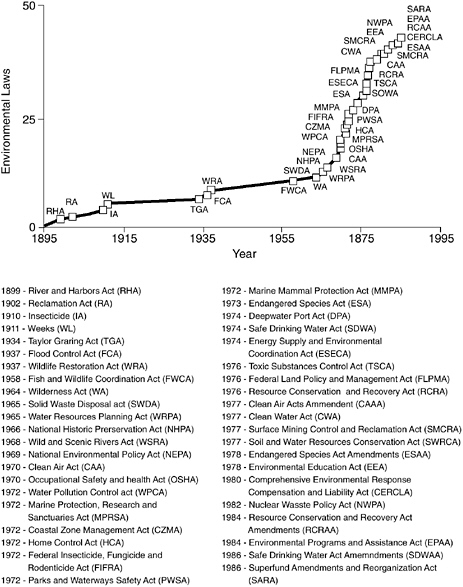

In the United States, there is a 30-year record of "command and control" environmental regulation and enforcement that has dictated how companies addressed environmental, health, and safety issues. Businesses have responded to the regulatory "stick" by complying with regulations and applying technology to control pollution. The tangle of these regulations has grown extraordinarily rapidly (Figure 1). Sometimes, they thwart more systems-based approaches to improve environmental performance. Indeed, there is growing evidence that approaches other than those proscribed by regulations can effectively meet and sometimes exceed environmental standards or goals set by the regulation. One example is the joint U.S. Environmental Protection Agency (EPA)-Amoco study of opportunities to prevent pollution at an Amoco refinery. The results of the effort revealed that, compared to traditional steps to meet regulatory requirements, similar reductions in pollution could be achieved at lower cost ($11 million instead

FIGURE 1 Growth in the Number of U.S. Environmental Laws. SOURCE: Balzhiser, 1989.

of $51 million) by taking approaches different than those required by the regulations (Schmitt et al., 1993; Solomon, 1993). The potentially stifling effect of regulation on innovation can be avoided by setting performance standards that companies may meet in whatever creative manner they devise.

More recently, incentives have been added to the ''toolset" used to improve environmental quality. In a shift from its traditional enforcement programs, the

EPA has started to allow companies to take voluntary actions in partnership with the agency (U.S. Environmental Protection Agency, 1996). The agency has established compliance assistance centers to provide technical and other help to smaller companies that wish to comply with EPA requirements without provoking enforcement actions. Among the campaigns are several that provide support for and publicly recognize companies that reduce solid waste (Waste Wise), upgrade to more energy-efficient lighting (Green Lights), reduce release of certain high-priority chemicals (33/50), and introduce more energy-efficient products to the market (Energy Star).

Bans and taxes are nonregulatory, market-based tools that are used to reduce the environmental costs associated with materials. The ban on DDT is an example of a prohibition used to eliminate a harmful chemical. Taxes have also be used to phase out the use of chemicals. For example, when it became apparent that depletion of the ozone layer was linked to chlorofluorocarbons (CFCs), a graduated tax was levied on the substances and a target date was set for their phase-out. This sped the development and introduction of substitute chemicals and innovations that eliminated the need for CFCs in many applications.

Another more recent market-based innovation in the green game is the use of tradeable permits. Under this scheme, the environmental protection authority issues a limited number of permits allowing for the discharge of a specific amount of pollutants. The number of permits determines the quality of water or air. There is no guarantee that the initial number of permits is optimal, but the system ensures a given level of control by allowing permits to be traded. For example, in one current experiment, a manufacturer may increase sulfur dioxide emissions in locations where sulfur dioxide pollution is not a problem in exchange for reducing emissions in places where sulfur dioxide emissions do pose a problem. This leads to overall efficiency improvements. If a firm that has a permit is able to reduce pollution at less cost than are other firms, it can sell the right to pollute to a firm that is unable or unwilling to reduce its emissions. Under this scenario, the firm that sells the permits reduces its pollution level an still makes a profit from the sale of the permit.

In addition to regulation and market-based initiatives, environmental costs can be further internalized by efforts to encourage recycling or reuse. In the United States, the focus has been on recycling specific materials, such as paper, plastic, and certain metals, an requiring certain products to contain recycled material. In Japan, government policy and industry efforts have converged around the notion of a "recycle society" (Gotoh, this volume). In this society, well-designed technical and economic mechanisms would encourage industry and the public to seize every opportunity to recover, recycle, and reuse materials and energy to the maximum degree that is thermodynamically feasible and economically justified. To aid the creation of the recycle society, Japan has introduced recycling laws that cover a range of constituent materials and some finished products. They have also established an ecofactory research effort to develop technologies

needed for environmentally conscious manufacturing (Japan External Trade Organization, 1993).

Germany has pursued a different tactic, requiring manufacturers to "take back" their products when they are discarded by the customer. Manufacturers are encouraged to recover useful material and energy and properly dispose of what is left. These initiatives make manufacturers responsible for the products they bring to market. The concept is often referred to as "product stewardship." Because regulations like these impact companies that compete globally, environmental concerns have become strategic. Companies have begun assessing the total environmental impacts of their products over the course of the product's full life cycle (Horkeby, this volume; Johnson, this volume; Marstander, this volume). They are also refining their financial analysis of products to identify in-house environmental costs, which previously were lumped into overhead (Ditz et al., 1995; Macve, this volume; Todd, 1994; Todd, 1997).

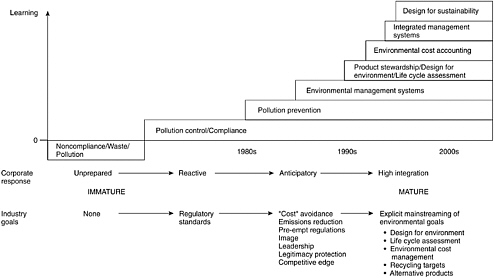

There are also other nonregulatory forces that are part of today's industrial green game. These include the emergency of voluntary international environmental standards (ISO 14000), citizen involvement, and environmental justice issues. These forces more fully explain the incentives corporations may have for evolving toward more socially oriented goals, such as environmental protection, as Allenby (this volume) speculates. Companies today can be found anywhere on the learning curve shown in Figure 2. Companies that value environmental quality—whether by force of regulation, because they see an economic opportunity in preventing pollution, or because they recognize the strategic importance of environmental factors or want to be "responsible" companies—are among those that are assessing the value of taking action beyond basic compliance that will lead to less regulation, decreased liability, and better integration of environmental concerns with business practices.

SYSTEMS WHERE WASTE IS A USEFUL INPUT

Most environmental impacts result when materials accumulate in the biosphere. The materials may be naturally occurring and extracted from the earth, or they may be man-made. The management of materials is therefore critical to the industrial green game. One way to manage materials, which aims to avoid such accumulations, is to close the materials loop of production and consumption systems. Another is a no-growth approach based on an impractical premise of not extracting or creating the materials in the first place.4

The idea of closing the materials loop is not new. It derives from the observation that in natural systems, waste is a misnomer. Materials that are not used by a particular organism generally are used by others to grow and survive. This self-sustaining characteristic has evolved over time (Ayres, 1994), and, indeed, organisms that produce waste products do so without much thought about what happens to the waste. Until recently, the evolution of technological systems has

occurred with little thought about what occurs to materials that are "wasted" from the system. From a systems point of view, there is a danger in suboptimizing residual material from industrial processes or discarded products from consumer use. Frosch (this volume) warns that optimizing a particular process or subsystem to increase the efficient use of a material may be less effective than optimizing the system as a whole. Indeed, a larger, more complex, more diverse system may offer greater opportunity to efficiently use and reuse materials.

A example of the optimization that can occur at these larger scales is illustrated by the symbiotic workings of a set of industries in Kalundborg, Denmark (Grann, this volume). Here, a power plant, an oil refinery, a plaster-board manufacturing plant, a biotechnology plant, and a fish farm and surrounding farming community benefit from joint utilization of material residues that otherwise would end up as waste. In Kalundborg, refinery wastewater is used for power plant cooling; excess refinery gas and sulfur recovered by the refinery are used to manufacture plaster board; biological sludge from the pharmaceutical plant is used by farmers; steam from the power plant is used by the pharmaceutical plant; fly ash from the power plant is use by cement manufacturers in different town; and waste heat from the power plant is used in fish farming and by the municipality as part of its heating distribution system.

The Kalundborg situation has been presented as an elegant model of what can happen when symbiotic relationships among industrial players are encouraged (National Science and Technology Council, 1995). This has spurred interest in communities to get co-located industries to examine the possibility of developing partnerships to improve use of residual material and to build ecoindustrial parks.5 These experiments will help the understanding of how materials flow at the local level and what needs to be done to better utilize them. However, there is a danger in viewing the Kalundborg model as the best way for industry to mimic nature with the goal of solving environmental problems. Most symbiotic relationships are not robust enough to handle changes in outputs such as would occur if a partner were to go out of business or find it more advantageous to not produce a waste in the first place. The small scale and limited diversity of such industrial ecosystems may make them fragile.

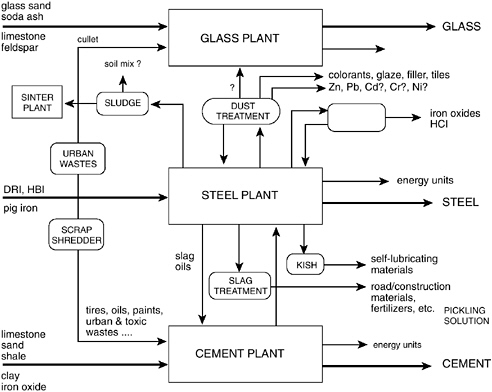

Another shortcoming of the Kalundborg model is that it presents too narrow a view of what is possible in terms of symbiotic relationships. There are other configurations that are worth considering. One involves looking at similar processes within an industrial sector. Figure 3, for example, shows the potential synergies among various material production plants, which may or may not be co-located.

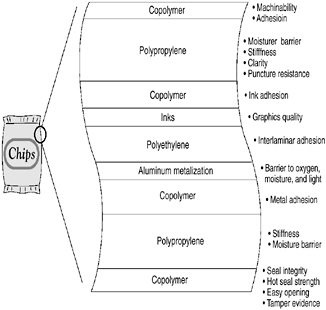

Finally, the co-location model for creating symbiosis does not consider the changing nature of materials and their production, summarized in Table 1. Today's materials are more likely to be specialty, engineered, or advanced materials such as alloys, composites, laminates, or coatings than commodity materials. A potato-chip bag, for example, is not a simple paper or plastic product but a

FIGURE 3 Potential synergies among various materials production plants. SOURCE: Szekeley, 1994.

complex material of several layers (Figure 4) that is more efficient than the packaging it replaced on a material weight per unit product basis. In fact, the trend in materials is toward complexity, variety, and efficiency (Eyring, 1994). These types of materials are drastically different from the simple materials (steam, sulfur, wastewater, sludge, and fly ash) that circulate in the Kalundborg model.

In addition, Table 1 shows that the newer materials are made not in plants dedicated to a single product, but in plants designed for flexible manufacturing where several different products may be produced, each with a very different waste stream. These plants, in turn, feed into an interdependent global economy, and their materials find their way into a diversity of products in a range of locations. This suggests a need for improved methods of assessing and managing risks associated with materials and processes used to make them. It also suggests the need for better separation technologies, if these materials are to be recovered and returned to commerce after they are discarded. Frosch (this volume) observes that even when recovery of useful material is technically feasible, it may be economically unsound, and when it is technical and economically satisfactory, a lack of information can still stymie implementation. Finally, when all else is

FIGURE 4 Cross-section of chip bag. SOURCE: U.S. Congress, Office of Technology Assessment, 1991.

satisfactory, there may be organizational problems, or the recovery effort can run counter to regulatory and legal requirements. What is needed is wise policy that removes barriers to improved movement of usable residual material and promotes the closing of materials loops at various scales.

DESIGNING SYSTEMS FOR MULTIPLE-PRODUCT CYCLES

The industrial green game requires that concerns about environmental quality include not only production and product use but also useful materials or potential energy embedded in products. In this strategy, products are used in several systems or product cycles, either as parts, materials, or embedded energy, as shown in Figure 5. Essentially, a product becomes input to several product cycles instead of merely finding its way to the trash heap after one life cycle. This simple idea, backed by regulatory pressures (e.g., German take-back legislation), has led some companies to innovate and use that innovation in marketing and advertising opportunities.

The utility of designing products for multiple product cycles depends on the product. Diversities in products and the manufacturing sectors that produce them (Table 2) have to be taken into account. An important distinction is the lifetimes of products. Some are made to function for a decade or more; others have lives

TABLE 1 The Evolving Materials Paradigm

|

Materials-As-Resource Paradigm |

Value-Added Materials Paradigm |

|

Resource-dependent materials |

Information-, technology-dependent materials |

|

Commodity materials |

Specialty, engineered, advanced materials |

|

Monolithic materials |

Alloys, composites, laminates, coatings, ceramics |

|

Structural materials |

Functional material |

|

Large-volume, continuous processes |

Small-scale, batch processes |

|

Plants dedicated to single product |

Plants designed for flexible manufacturing |

|

Price and availability as competitive basis |

Quality, performance, service as competitive basis |

|

Resource-oriented research |

Manufacturing-oriented research |

|

Environmental resources abundant |

Environmental resources limited |

|

Research performed by single principal investigators |

Research performed by multidisciplinary, collaborative research teams |

|

Self-sufficient economy, few potential vulnerabilities |

Interdependent, global economy, many potential vulnerabilities |

|

Metals dominance |

Chemicals ascendance |

|

SOURCE: Sousa, 1992. |

|

measured in months or weeks; still others are used only once. The designer and other's who bring a product into existence must adopt different design approaches to these different types of products according to their durability, materials composition, and recyclability (Graedel and Laudise, forthcoming).

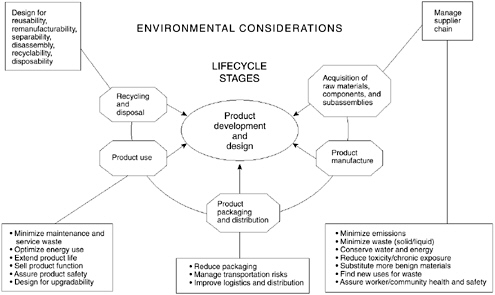

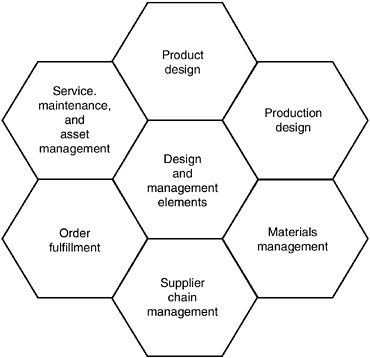

As environmental objectives are introduced in product design, manufacturers are reexamining their approaches to a wide range of concerns, such as product and packaging design, materials selection, production processes selection, energy consumption, environmental market research, environmental labeling, and marketing. From a business perspective, the introduction of environmental objectives in product design must not cause delays in bringing the product to market. Green game strategies for managing the life-cycle impacts of products are summarized in Figure 6. These strategies are implemented in a variety of business processes: product design, production design, materials management, supplier chain management, order fulfillment, as well as service, maintenance, and asset recovery (Patton, 1994) (Figure 7).

Product Design

This is the method used by manufacturers to develop products to meet customer and market requirements. It begins with the definition of the product, a critical step that determines the features which will guide the product development team. This definition is reviewed throughout the product development cycle

-

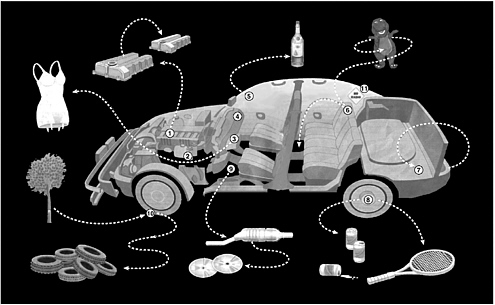

IS: Recycled plastic valve cover. (In most cars, valve covers are metal.) WAS: Plastic intake manifold (which draws air into the engine). MAY BE: Shredded and remolded into future plastic valve covers, perhaps eternally.

-

ARE: Toxic fluids — coolants, various brake, engine and transmission lubricants. WERE: Usually destined to contaminate landfills. WILL BE: Drained immediately by salvager. Coolants can be resold; as for the rest — well, they're working on it.

-

IS: Nylon air bag. WAS: Never used, fortunately. MAY BE: Women's underwear. Salvager must first deploy the bag to remove the toxic propellant. The nylon, which typically is shredded and discarded, then can be recycled and sold to various industries, automotive and otherwise.

-

IS: Padded dashboard. WAS: Assembled from a multilayer amalgam of foam, metal and various plastics. WILL BE: Hard to recycle until someone devises a dashboard made of a uniform plastic that is both durable (safety always overrides recyclability) and aesthetically pleasing (i.e., not reminiscent of a 1972 Chevy Vega). Could be a long wait.

-

IS: Windshield. WAS: In a large vat at the glass factory. MAY BE: A bottle of Scotch. (Increasingly, automotive glass is recycled by the container industry.)

-

IS: Polyurethane seat filler and vinyl seat covers (in those rare cases, when the seats aren't covered with leather). WAS: Alas, nothing — at least not until engineers devise a non-cheesy-looking recycled polyurethane. MAY BE: Shredded and used as soundproofing in car floor, or sold to stuff Barney the dinosaur.

-

IS: Luggage compartment liner made of recycled (not standard issue) polyurethane. WAS: Polyurethane bumper. MAY BE: Virtually any other part made chiefly of polyurethane. PROBABLY WON'T BE: Another bumper. In general, exterior parts, degraded by exposure to the elements, are recycled into interior parts.

-

IS: Aluminum wheel. WAS: A bauxite deposit in Arkansas. MAY BE: Shredded and remolded into future wheels; down the road, perhaps, sold to make Venetian blinds, lounge chairs, tennis rackets, staples, screws, Pabst cans.

-

IS: Catalytic converter. MAY HAVE BEEN: Another catalytic converter. MAY BE: Yet another. BMW now buys back used catalytic converters and chemically extracts the platinum, rhodium and other precious metals from the cores. These can be used to make future converters — or perhaps, Pearl Jam's next platinum disc.

-

IS: Left front tire. WAS: Rubber tree somewhere in Malaysia. MAY BE: Shredded, sold and mixed with asphalt to make pavement. But more likely, tossed on a New Jersey waste dump, there to remain for the next millennium.

-

IS: "No Radio" placard. WAS: Recycled paper pulp. WILL BE: Ignored, in all likelihood.

FIGURE 5 The ultimate used car. SOURCE: Jerome, 1993. Figure by Jaegerman. Copyright © 1993 by The New York Times Company. Reprinted with permission.

TABLE 2 Manufacturing Sectors and Their Products

|

Manufacturing Sector |

Product Examples |

Product Lifetime |

|

Electronics |

Computers, cordless telephones, video cameras, television sets, portable sound systems |

Long |

|

Vehicles |

Automobiles, aircraft, earth movers, snow blowers |

Long |

|

Consumer durable goods |

Refrigerators, washing machines, furniture, furnaces, water heaters, air conditioners, carpets |

Long |

|

Industrial durable goods |

Machine tools, motors, fans, air conditioners, conveyer belts, packaging equipment |

Long |

|

Durable medical products |

Hospital beds, MRI testing equipment, wheelchairs, washable garments |

Long |

|

Consumer nondurable goods |

Pencils, batteries, costume jewelry, plastic storage containers, toys |

Moderate |

|

Clothing |

Shoes, belts, polyester blouses, cotton pants |

Moderate |

|

Disposable medical products |

Thermometers, blood donor equipment, medicines, nonwashable garments |

Single use |

|

Disposable consumer products |

Antifreeze, paper products, plastic bags, lubricants |

Single use |

|

Food products |

Frozen dinners, canned fruit, soft drinks, dry cereal |

Single use |

|

SOURCE: Graedel and Laudise (forthcoming). |

||

The basic platform that emerges in the design process defines the initial product and its potential modifications. Products designed for easy upgrade, motivated by business opportunities for using the same platform for several products, offer substantial opportunities to reduce solid waste. This is because only some parts need to be redesigned to get the performance of a newer model. Designs that facilitate the exchange of circuit boards are examples of design for upgradability. A variation of this approach is the design of parts that may be used among several products lines or are interchangeable among different models. Design features such as these, together with product recovery and remanufacture, can result in a reduced solid waste load.

Other more direct green game objectives that should be considered in product design include using less material or more energy-efficient components. Reduced use of materials translates easily to cost savings—smaller quantities of the material have to be purchased, less energy is used in its manufacture, transportation costs related to both the input materials and finished product are lowered, and there is less material to handle when the product is returned for disposal. Similarly, attention to the fate of a product, in terms of reuse or recycling, can result in product innovation. Reuse strategies that lead to reduced material costs can build brand loyalty among customers, who may be more likely to engage in repeat purchases from the original manufacturer, and provide source material to meet recycled-content requirements.

Production Design

Often the most effective strategy for improving environmental quality is to use the latest production technologies and processes. More advanced technologies tend to be more efficient and can be cleaner. Chiaro (this volume) describes the environmental advantages of new smelting facilities that use more advanced technology compared with those used by older smelting facilities. The selection of a new process technology or new equipment is often the result of tradeoff among costs, effectiveness, and environmental impacts. The environmental quality of the new technology can be assessed by carefully screening chemicals used in the processes and those that are emitted during production. In many cases, equipment can be bought from a wide selection of vendors who compete on a variety of factors, including cost and environmental quality. Tradeoffs between environmental objectives and other business goals can be gauged by assessing competing vendor bids against environmental criteria.

Materials Management

Materials management is one of the most important aspects of managing for environmental quality. Materials selection, chemical-use evaluation, and life cycle assessments are important ways in which materials management can be improved.

Materials are generally selected because they meet certain product form and function criteria (such as strength and durability) as well as production concerns (such as manufacturability). Reuse and recyclability are increasing concerns in materials selection, and there are several examples of how materials that facilitate reuse and recycling can result in green game gains by improving environmental quality and reducing cost. In the United States, where a strong secondary market exists for refurbishable auto parts and recycled auto materials, the economic value of more than 75 percent (by weight) of a car is recovered and reused. In electronics, a high-volume industry, reusable circuit boards are being channeled to service

and repair operations (Holusha, 1996). The expense and initial difficulties of recycling plastic enclosures and other parts of electronic products have been addressed by simple strategies, like minimizing the diversity of plastics used and by clearly marking plastics in terms of several classifications of the material. When materials are carefully selected with reuse and recycling in mind, it is easier to create cost-effective (and sometimes profitable) relationships with recyclers and material vendors, to whom businesses might sell recovered materials. Such practices can also be useful in meeting government procurement requirements, which in many areas mandate the percentages of recycled materials that products should contain.

Chemical-use evaluations can be important in assuring that hazardous materials are not used in products and in identifying potential chemical-related problems early enough in design so that the product and process used for manufacture can be reengineered. Simple tools, such as checklists, can be effective in evaluating many materials. Recently, more systematic approaches such as life cycle assessments (LCA) are being used to guide materials use decisions.

LCAs are intended to evaluate the environmental impacts of products at every stage, from raw material extraction and production through distribution and disposal. They generally consist of three distinct but interrelated components:

-

Life cycle inventory, an input-output accounting that quantifies the inputs of energy and raw materials and outputs of products, air emissions, water borne effluent, solid waste, and other environmental releases associated with the entire life cycle of the product, process, or activity.

-

Life cycle impact analysis, a characterization of the effects of the environmental loadings identified in the life cycle inventory and an assessment of the loadings in terms of ecological and human health impacts.

-

Life cycle improvement analysis, a systematic evaluation of the needs and opportunities to reduce the environmental burden associated with impacts of the inputs and outputs that have been inventoried and analyzed.

There are problems with LCA (Johnson, this volume). LCA is methodologically and analytically complex; creates the false impression that it includes everything; is data- and resource-intensive; neglects qualitative and unquantifiable factors; and frequently uses inadequate ''surrogates" for environmental impacts. Furthermore, LCA has the potential for "paralysis by analysis," if the boundaries of the analysis are not well defined. In evaluating two products, it is reasonable to examine the raw materials used to make them. But, should the energy used to make the machinery used to extract the raw materials be included as well? Should the type, age, and efficiency of the machinery used to make the product be considered? And should the source of electricity be tracked back to it fossil, hydro, gas, or solar origins? LCA also is of little help for assessing the realistic impacts of pollution that often depend on time and location of occurrence. For example,

a product ending up in well-run landfill will do less environmental harm than one that is not properly disposed. How should different types of environment impacts be compared and characterized? Life cycle assessment provides no answers to these questions. The challenge is in selecting boundary conditions that make sense, clearly identifying what those boundaries are, and then communicating the results of the analysis in a sensible manner.

One striking outcome of LCA and other similar models is what they reveal about the systems being assessed. Johnson (this volume) shows how LCAs of paper (as a product) reveal the complexity of the materials and energy flows of this simple material that is also 35 distinct products. In addition, simply cataloging and revealing the volumes of releases has proved effective in prompting reductions in waste. The prime example is the U.S. Toxics Release Inventory (TRI), which was created in response to the Emergency Planning and Community Right to Know Act of 1986. Under the law, companies are required merely to report their releases of waste, but even this simple step spurred actions to reduce waste and to understand the relative effects of various chemicals.

At a minimum, inventorying materials and energy flows can establish baseline information on a system's overall resource requirements, energy consumption, and emission loadings, and it can help identify opportunities for the greatest green game improvements in environmental quality. More sophisticated systems, such as Volvo's Environmental Priority Strategies System (Horkeby, this volume), can compare system inputs and outputs in assessing the environmental quality of comparable but alternative products, processes, or activities. This, in turn, helps guide the development of environmentally superior of innovations.

Most companies using some variation of life cycle assessments do so to verify claims they make in green advertising; to fend off unwanted regulatory pressures; and to identify opportunities to reduce the pollution impacts of their products and production processes.

Supplier Chain Management

Manufacturing today occurs though complex supplier chains. Often materials, parts, and components are made by different suppliers. At one extreme, the whole manufacturing effort is outsourced to suppliers. These "virtual manufacturers" provide the knowledge behind the innovation and then market products that are made entirely through supplier chains. All manufacturers rely to some degree on supplier chains, and their competitiveness depends on managing the supplier chain well. Technology partnerships, reuse or recycling relationships, and supplier evaluation have all been used to manage supplier chains for environmental quality.

Technology partnerships can involve a parent manufacturing company developing a technology for use by suppliers on a proprietary or fee basis. When electronics companies phased out the use of ozone-depleting chlorofluorocarbons

as solvents to clean electronic circuit boards, the alternative water-based systems were developed primarily by the major manufacturers and shared with their suppliers (International Cooperative for Environmental Leadership, 1996). Plastics manufacturers, who are often part of several supplier chains, recognize that their competitiveness may well depend on their ability to create materials that can be recycled conveniently and cost-effectively. These manufacturers have developed and continue to engineer plastic resins to meet new requirements, eliminating ingredients that inhibit cost-effective recycling and establishing business relationships that will lead to the cost-effective recovery of resins in order to meet recycled-content requirements.

The importance of evaluating the environmental quality of supplier chains is critical to playing the industrial green game well, partly because of transnational differences in standards and practices. Suppliers must comply with environmental regulations in the countries in which manufacturers' products are eventually sold. Suppliers practices also must conform with any voluntary labeling a company uses to designate its product as "green." Manufacturers, therefore, have to understand their suppliers' practices and, more generally, assure environmental quality from the supplier chain by using surveys, questionnaires, audits, and third-party certifications.

Grann (this volume) shows how similar concepts are used in the building of a pipeline through a sensitive ecological area. His paper describes the use of British Standard BS 7750—Specification for Environmental Management Systems—and a forerunner of the international environmental standards ISO 140017 to manage environmental aspects of the project. A detailed environmental protection plan for the pipeline project was prepared to ensure a high level of environmental performance and strict adherence to all regulations, permits, and requirements. The plan included a set of environmental documents that were used by contractors to state their commitment to environmental protection by identifying environmentally critical operations, prescribing appropriate environmental measures, and giving detailed work instructions for proper job execution, control, and verification.

Order Fulfillment

The way in which orders are fulfilled to complete sales and deliveries can have major green game implications, particularly in packaging, inventory management, and distribution logistics. The strategy for dealing with packaging is similar to that associated with the product: Use less material, use biodegradable material, and design packaging for reuse and recycle. The less tangible aspects of fulfilling orders and of inventory management and distribution require the use of logistical information. Just-in-time manufacturing practices—matching production to market demand to eliminate storage or surplus of product—reflect how forecasting systems and inventory management can minimize the manufacture

and storage of unsold products. Poor forecasting and inventory management are not only a source of unnecessary cost to manufacturing firms, they also mask large, hidden sources of environment impacts. Products that are scrapped because of poor inventory controls are good neither for profits nor environmental quality. Improvements in inventory management can have positive impacts on both profits and environmental quality.

The logistics of distribution are also an important determinant of environmental quality, particularly in terms of the energy used for transportation. When a company controls the distribution of its products, it can make effective gains in environmental quality. Increasingly, distribution is also outsourced often to large distribution service providers. Distribution-related concerns about environmental quality are most evident in mail-order-type businesses. An order may be called into a toll-free number and relayed to a supplier, who then either manufacturers the product or packages it and gets the product to the customer by land, sea, or air through a transportation and distribution service provider, such as the U.S. Postal Service or private companies like United Parcel Service. The changing nature of production and distribution will likely raise difficult questions about such issues as location, transportation, and logistics, which impact both cost and environmental quality concerns.

Service, Maintenance, and Asset Recovery

The service and maintenance of a product (particularly a long-lived product) can result in environmental impacts that are easily overlooked. As product life cycles get shorter, many more durable products, such as printers and personal computers, typically function long after the manufacturer has stopped making them. As a result, supplying replacement parts can be expensive for the manufacturer. However, discarded products may be an excellent source for reusable and refurbishable components (Holusha, 1996). The large volume of products to be serviced, and the high profitability of doing so, can make maintenance and repair services a ready outlet for large volumes of discarded parts.

Both legal and market requirements are forcing many businesses to collect and recover their products, or assets. Whether or not recycling or disposing of packages and products is economical depends heavily on product design. As legal and market dictates change, many businesses are responding by developing recycling systems. For example, to recycle the electrophotographic cartridges used in laser printers and fax machines, Canon developed different approaches to meet the characteristics of its two major markets (Maki, 1994). In Europe, the company uses its network of dealers as collection points. In the United States, where there are diversified sales channels over a vast geographical area, Canon collects its cartridges from customers through a prepaid parcel service. As an added incentive, the company contributes $1 to an environmental group of the customer's choosing for each cartridge returned.

Costs associated with service, maintenance and asset recovery include the design and development of collection schemes and encouragement of consumer participation. Since product return/recycle requirements are likely to become much more widespread, green game strategies should include arrangements for addressing asset recovery, and requirements for recovering costs should be addressed in each product line.

DESIGNING FROM A FUNCTIONALITY BASIS

Concerns about environmental quality are commonly viewed in terms of the hardware associated with the production of the product. The product may be a consumer good (like an automobile, a personal computer, or refrigerator), or a service (such us construction of roads, airports, pipelines, power stations, telephone cables, or other infrastructure). Turning this view on its head, the green game views the design of systems according to the "software," or functionality, derived from the product. The product becomes the service derived from the hardware: pest control as opposed to pesticides; temperature control, heat, and light instead of electricity; refrigeration instead of refrigerators; computing and telecommunication instead of computers, satellites, and cellular phones.

Stahel (this volume) suggests an economy based on functionality to decelerate the flow of materials within the economy. The idea allows manufacturers and others to exert control over the product life cycle by encouraging the customer to buy the function the product provides instead of the product itself. This is not a new idea but one that expands on past practices such as the leasing of phones. The trick for business is to build in the ability to upgrade to better and more efficient products as advances in technology provide greater energy efficiency and pollute less. Stahel points to Xerox, which advertises itself as a document company, and the design innovations the company has adopted to manage, upgrade, and maintain its inventory of photocopying machines that are used in high-volume sectors of the economy. In this instance, the company is selling documentation, not its machines.

The green game strategy of providing functionality instead of hardware is not applicable to all products nor is it one that will meet the needs of all customers. One outcome of the economy's growing service sector may be increased demand for leased products, better maintenance, and better protection against liability in operating longer-lasting products. The service sector, which currently accounts for 75 percent of jobs and 75 percent of GDP in the United States, includes operations such as hospitals, hotels, restaurants, photocopying services, real estate management, transportation and distribution companies, retail outlets, entertainment parks, cinemas, rental car agencies, and airlines. These types of businesses use many different products, and the decisions they make about environmental quality are related to functionality. Such businesses are more likely to lease these products, and when they purchase equipment, they value good maintenance

that extends the life of products. United Postal Service, for example, extends the life of its truck fleet by practicing predictive maintenance—replacing parts based on their predicted life times—using sophisticated information systems that keep track of every part in every piece of equipment (Nielsen, 1995).

In discussing electricity as an energy source, England and Cope (this volume) focus on the values, or services, that electricity consumers derive from the product. The focus on end-use draws attention to the aim of the entire system to provide heat, light, temperature control, and so on. The ultimate goal is energy efficiency. In contrast, the motivations of actors upstream from end-use is to generate the maximum number of kilowatt-hours, to mine the maximum amount of coal or uranium, or to extract the maximum amount of fuel. The functionality-based approach leads to thinking about the linkages in the system and is quite different than a systems view of electricity generation. Energy efficiency becomes a critical aspect of managing the system. Moving upstream, toward generation of electricity, this approach points to other strategies for using waste heat and material produced during electricity generation.

USING INFORMATION IN THE GREEN GAME

Information and its use are critical to the industrial green game, whether one talks about using waste as useful material, handling environmental considerations in the design stage, or designing systems on the basis of functionality. The discussion above covered a wide range of information uses, from simple inventorying to establishing a baseline of material and energy inputs, product outputs, and waste emissions; helping to select materials and evaluate the use of chemicals; providing details for managing the supplier chains; improving logistics and inventory controls; and facilitating maintenance in leasing operations for a functionality economy. There are three other areas where information aids the green game: accounting for environmental costs, measuring environmental performance, and gauging consumer attitudes about the environment.

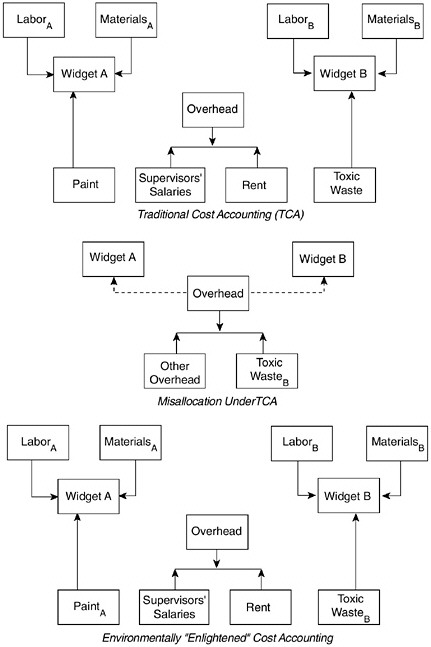

Accounting for Environmental Costs

Traditional accounting has often relegated environmental costs to overhead and hidden them from managers. A modified accounting scheme that gets at environmental costs is presented in Box 2. In this system, overhead is relegated to individual activities and responsibility is assigned to those with decision making responsibilities. Macve (this volume) addresses the challenge of getting a better feel for overhead costs in multiactivity and multiproduct firms. He points out that activity-based accounting attempts to identify the causal relationships in an operation, regardless of how remote the links may be. He argues that from an economic and decision making perspective, such allocations are basically arbitrary and irrelevant, since costs do not create value. What matters is how costs

will change as a result of each decision—whether the extra revenue or other benefits the decision will bring are worth the extra costs. The accountant's approach is to develop systems of accountability and responsibility for costs and profits that provide norms and standards of human performance. The challenge of "environmental costing," Macve concludes, is not only to increase the technical sophistication by which environmental factors are tracked through to activities, but also to construct a new accountability that is linked to real incentives. As the field of accounting develops to provide better information about firms' environmental costs, it is likely to influence environmental-quality-related business decisions (Ditz et al., 1995) and improve the industrial green game.

Measuring Environmental Performance

The measurement of environmental performance is an effective tool when accounting for environmental costs is linked to incentives for managers to play the industrial green game well. What is measured is driven by policies a company may adopt, and a range of measures may be devised to gauge achievement against a set of objectives. The measures are most commonly absolute, such as achieving waste reduction of 200,000 tons against an objective of 150,000 tons. They also may be relative and time dependent, such as achieving an energy-use reduction of 20 percent compared with the previous year's result and against an objective of 30 percent for the current year. A combination of absolute, relative, and time-dependent measures are used to track four areas of environmental performance:

-

Environmental Impacts. These are really measures of loading of materials and emissions that result in environmental impacts. They are useful in gauging the overall performance of a firm as well as for assessing the performance of individual organizational units, operations, or processes.

-

Contributory Impacts. These relate to the performance of components of a firm such as plant and equipment, and materials quality and use, and to management systems such as training that contribute to the overall impacts.

-

Risk Measures. These relate to the probability that the unexpected rare releases of a pollutant may result in potentially serious consequences. In such an instance, the risk, or probability, of such an event is a more useful measure of performance than the number of actual events.

-

External Relations Measures. These relate to the environmental performance of the firm within the community. It includes everything from the number of complaints to the level of support of environmental programs.

In developing a system of measures for the green game, several factors should be considered (Business and the Environment and KPMG Peat Marwick, 1992).

First is the purpose of the measurement. If the goal is to understand impacts or to develop information for public reporting, it may be sufficient to measure and report on impacts. However, if the purpose is to guide management action to improve performance, then specific areas contributing to that performance and associated measures will have to be identified.

The second factor is the availability of information. Information that is readily available is more likely to be used. Much of the information can be gleaned through reviews or audits (Steelman et al., this volume) and then used to provide a basis for setting quantitative objectives against which performance may be measured.

Measurability is the third factor. In the industrial green game, simple measures such as energy efficiency or material-use efficiency are easier to determine than more complex factors such as supplier performance. Because continuous improvement is a feature of the green game, information should be gathered even if obtaining a measure is difficult and especially if a particular aspect of operation is considered important.

Finally, the controllability of what is being measured should be factored into the development of performance measures. Controllability and measurability are closely linked. Some areas of environmental impacts, such as emissions or energy use, are easier to measure and control. Others, such as supplier performance, customer satisfaction, or the environmental impacts of products, are more difficult to control but may be important to measuring performance.

Steelman et al. (this volume) and Marstander (this volume) provide details of how two companies gathered information to identify opportunities for continuous improvement. The essence of measuring performance in the industrial green game requires first identifying the information to be gathered. Progress is gauged by comparing these data with baseline information, and periodic audits are then used to evaluate progress in meeting environmental quality goals as well as identify areas for improvement.

Gauging Consumer Attitudes

As purchasers of products and services, consumers are critical to playing the industrial green game well. Consumer demand for "green" products and competition from companies that play the green game well determine the value companies place on meeting that demand. Simon and Woodell (this volume) track environmental policies as well as consumer attitudes toward the environment in Europe, Japan, and the United States. They use this approach as a basis for explaining the expectations of consumers for environmentally superior goods and services, the role customers expect of companies in addressing environmental concerns, the level of consumer involvement in environmental actions, the types and levels of environmental information sought by consumers, and the impacts of "green" advertising. Simon and Woodell find increasing confusion about what

constitutes a truly green brand or company. They also find that, from a consumer's point of view, a product's environmental record ranks well below attributes such as price, quality, and past experience with the brand. However, environmental image is the only factor in brand choice, besides price, that has shown significant growth in the recent years. They also find a drop in the willingness of customers to pay a premium for environmentally preferable product. Several studies show a consistent pattern over time. In 1988, when asked if one would accept "a less good standard of living but with much less health risk," 84 percent agreed in the United States, 69 percent in Germany, and 64 percent in Japan. Two years later, in 1990, fewer accepted the same premise, with 65 percent of Americans, 59 percent of Germans, and only 31 percent of Japanese willing to sacrifice standard of living for a cleaner environment.

These trends present companies with the challenge of providing environmental quality as an added value to customers at little or no additional cost. Yet, there is growing evidence that simple waste reduction and energy-efficiency improvements can reduce costs, primarily by reducing the use of raw materials. Furthermore, environmental requirements that apply to products can have more complex financial and design trade-offs. But not making those trade-offs in good design and management can be more costly. For example, reuse or recycling can be very expensive for products that have not been designed with these requirements in mind. Collection and disassembly can be costly, and the resulting materials may have little or no recoverable value. On the one hand, products that are appropriately designed may be inexpensive to disassemble and may yield parts or materials with high recoverable value. In terms of revenue, products that are not designed with environmental requirements in mind can have disappointing sales for a variety of reasons, including that failure to address specific requirements may prevent their sale in a particular country or may preclude their consideration for specific bidding opportunities. On the other hand, products designed to meet environmental requirements may be able to increase company revenues by assuring worldwide acceptance or by taking market share away from competitors who are less able to respond to changing requirements.

Measuring Public Perception, Understanding, and Values

Understanding what the public knows and thinks about specific environmental issues is important in those instances where environmental improvements are forged through public debate, particularly when changing public policy or public behavior is necessary. Unlike surveys that are used to determine customer values, the "mental model" method (Morgan, this volume) can be used to get a better sense of what the public knows and thinks about a particular issue. The method gives participants no "clues" from which to form their responses, which is a problem with traditional surveys of public attitudes. Morgan argues that one gets a

better understanding of the public's knowledge and thoughts on a particular subject using the more rigorous and time-consuming one-on-one interview process.

In many instances, industry actions intended to improve environmental performance can be taken without public debate or an assessment of the public's understanding of complex issues. That is not the case when it comes to communicating risk and developing policy to address industrial green game concerns such as global warming, health effects of electromagnetic radiation, or the use of genetic engineering in agriculture. The development of risk communication material that is based on an understanding of what the public knows and thinks will be important in managing a range of environmental and technology risk issues that are central to a winning green game strategy.

IMPROVING THE GAME

The industrial green game, executed primarily in firms, is played within larger physical, economic, and organizational systems and associated metasystems. Rejeski (this volume) characterizes the role of government as that of a navigator providing a broader and longer-range view than that of firms or individuals. He suggests three actions government can take to move the green game to a higher level of play and thereby improve the environmental performance of production and consumption activities.

-

Mainstream environmental concerns into national accounts. This requires altering fundamentally the system of national accounts to get at the total environmental costs of the nation (and firm) by including natural capital and its depreciation and subtracting remediation costs and monetized environmental damages.

-

Track and benchmark materials and energy use. This requires analyzing and continually improving environmental quality by mapping the metabolism of materials and the use of energy to provide policymakers with better contextual and historical snapshots against which national policies and alternative strategies may be assessed. It also requires benchmarking system efficiencies against ''best-in-class" systems to identify potential improvements in the metabolism.

-

Forecast technological change and set goals. This requires mapping potential outcomes of various technological trajectories on the economy and the environment and examining the trajectories for convergence with some set of long-range, socially defined and agreed-upon goals.

These suggested actions are not prescriptive or regulatory. They relate to developing important information that can be used in the policy making and decision making of firms in pursuit of environmental quality.

CONCLUDING REMARKS

As the green game is played out in corporate boardrooms, the shop floor, in the home, and in the community, it is clear that technology and engineering will continue to play a critical role in reducing many environmental impacts of production and consumption. Neither technology nor technological know-how are in short supply. The primary opportunities come from the continued, sustained application of existing technology to identified problems. The primary need is to create the incentives and techniques for companies to use technology and knowledge to improve environmental quality. The main barrier in this regard is the corporate manager, who sees dealing with environmental impacts only in terms of its costs or as a difficult trade-off between design and management.

The papers in this book suggest that a revolution is taking place in how private firms, across all economic sectors, are dealing with the environmental impact of production and consumption. It is not unlike the revolution that made safety and quality strategic concerns of most companies. In the next decade or two, the best and most profitable companies competing globally will understand the environmental impacts of their products (or service), production process (or service delivery), and operations. And, working with consumers or in response to market pressures, these companies will play the green game better, thus improving both their competitive position and the environmental quality of the planet.

NOTES

REFERENCES

Ausubel, J. H.1992. Industrial ecology: Reflections on a colloquium. Proceedings of the National Academy of Sciences 89:879–884.

Ayres, R. U.1994. Industrial metabolism: Theory and policy. In The Greening of Industrial Ecosystems, B. R. Allenby and D. J. Richards, eds. Washington, D.C.:National Academy Press.

Balzhiser, R. E.1989. Meeting the Near-Term Challenge for Power Plants. Pp. 95–113 in Technology and Environment, J. H. Ausubel and H. E. Sladovich, eds. Washington, D.C.:National Academy Press.

Business in the Environment and KPMG Peat Marwick. 1992. A measure of commitment: Guidelines for measuring environmental performance. London: Business in the Environment.

Commoner, B.1971. The Closing Circle. New York: Bantam Books.

Ditz, D., J. Ranganathan, and R. D. Banks. 1995. Green Ledgers: Case Studies in Corporate Environmental Accounting. Washington, D.C.: World Resources Institute.

Ehrenfeld, J. 1995. Presentation at NAE Workshop on The Services Industry and the Environment, Woods Hole, Massachusetts.

Eyring, G. 1994. Trends in materials technology. Pp. 23–25 in Industrial Ecology: U.S./Japan Perspectives, D. J. Richards and A. B. Fullerton, eds. Washington, D.C.:National Academy Press.

Frosch, R. A., and N. E. Gallopoulos. 1989. Strategies for manufacturing. Scientific American 260:144–151.

Frosch, R. A., and N. E. Gallopoulos, 1992. Towards an industrial ecology. In The Treatment and Handling of Wastes, Bradshaw, et al., eds. London: Chapman and Hall.

Graedel, T. E., and B. R. Allenby. 1995. Industrial Ecology. New Jersey: Prentice Hall.

Graedel, T. E., and R. A. Laudise. (Forthcoming). Manufacturing. In The Ecology of Industry, D. Richards, ed. Washington, D.C.: National Academy of Engineering.

Holusha, J. 1996. Where old computer parts are given new lives. New York Times. June 10, D, 5:1.

International Cooperative for Environmental Leadership (ICEL) 1996. The International Cooperative for Ozone Layer Protection 1990–1995. Washington, D.C.: ICEL.

Japan External Trade Organization (JETRO). 1993. Ecofactory: Concept and R&D themes. Insert in New Technology Japan, February 1993. Tokyo: JETRO.

Jelinski, L. W., T. E. Graedel, R. A. Laudise, D. W. McCall, and C. K. N. Patel. 1992. Industrial ecology: Concepts and approaches. Proceedings of the National Academy of Sciences, 89:793–797.

Jerome, R. 1993. The ultimate used car. New York Times Magazine. October 31.

Maki, I. 1994. Canon's recycling initiative. Pp. 41–42 in Industrial Ecology: U.S./Japan Perspectives, D. J. Richards and A. B. Fullerton, eds. Washington, D.C.: National Academy Press.

National Science and Technology Council. 1995. Bridge to a Sustainable Future: National Environmental Technology Strategy. Washington, D.C.: National Science and Technology Council.

Nielsen, K.1995. United Parcel Service (UPS) and Its Environmental Strategies. Paper presented at the National Academy of Engineering on the Service Industry and the Environment.

O'Rouke, D., Connelly, L., and C. P. Koshland. 1996. Industrial ecology: A critical review. International Journal on Environment and Pollution 6(2/3)89–112.

Patton, B.1994. Design for environment: A management perspective. In Industrial Ecology and Global Change, Socolow et al., eds. Cambridge: Cambridge University Press.

Patel, C. K. N.1992. Industrial ecology. Proceedings of the National Academy of Sciences 89:798–799.

The President's Council on Sustainable Development (PCSD). 1996. Eco-Efficiency Task Force Report. Washington, D.C.: PCSD.

Raven, P. H., L. R. Berg, and G. B. Johnson. 1995. Environment, 1995 Version. Saunders College Publishing.

Richards, D. J., and R. A. Frosch. 1994. Corporate Environmental Practices: Climbing the Learning Curve. Washington, D.C.:National Academy Press.

Schulze, P. (ed). 1996. Engineering Within Ecological Constraints. Washington, D.C.: National Academy Press.

Schmitt, R. E., H. Kleee Jr., D. Sparks, and M. Podar. 1993. Forming partnerships to protect the environment. Joint Amoco-EPA pollution prevention at the Yorktown Refinery. Paper presented at the NAE Workshop on Corporate Environmental Stewardship, August, Woods Hole, Mass.

Solomon, C.1993. Clearing the air: What really pollutes? Wall Street Journal. March 29. A;1:1.

Sousa, L. J.1992. Toward a new materials paradigm. Minerals Issues, (December). U.S. Department of the Interior, Bureau of Mines.

Szekeley, J. 1994. Personal communication.

Tibbs, H. B. C.1991. Industrial Ecology: An Environmental Agenda for Industry. Boston: Arthur D. Little.

Todd, R. 1994. Zero-loss environmental accounting systems. Pp. 191–200 in The Greening of Industrial Ecosystems, B. R. Allenby and D. J. Richards, eds. Washington, D.C.: National Academy Press.

Todd, R. (Forthcoming). Environmental Measures: Developing an Environmental Decision-Support Structure. In Environmental Performance Measures and Ecosystem Condition, P. C. Schulze, ed. Washington, D.C.: National Academy Press.

U.S. Congress. Office of Technology Assessment (OTA). 1992. Green Products by Design. Washington, D.C.: U.S. Government Printing Office.

U.S. Environmental Protection Agency. 1996. Partnerships in Preventing Pollution: A Catalogue of the Agency's Partnership Programs. Washington, D.C.: U.S. Environmental Protection Agency. (Also available at http://www.epa.gov/partners.)

Watanabe, C. 1993. Energy and environmental technologies in sustainable development: A view from Japan. The Bridge 23(2):8–13.

Wever, G. 1995. Strategic Environmental Management Using TQEM and ISO 14000 for Competitive Advantage. John Wiley and Sons, Inc.: New York, NY

White, R. M. 1994. Preface. In The Greening of Industrial Ecosystems, B. R. Allenby and D. J. Richards, eds. Washington, D.C.: National Academy Press.