1

Requirements and Drivers

BACKGROUND

The Aviation Safety Research Act of 1988 (P.L. 100-591) directed the Federal Aviation Administration (FAA) to conduct research to develop technology to assess and improve aircraft safety. The law stipulates that the FAA spend at least 15 percent of its research budget on long-term investigations. In response to the Act, the FAA has initiated a comprehensive research program concerned with all aspects of civil aircraft safety. The overall objective of the FAA program is to anticipate the technological advances that will likely affect future aircraft and to evaluate their implications for aircraft safety.

One very important concern regarding aircraft safety is the degradation of structural materials as aircraft operate beyond their original design life, bringing to the forefront issues of materials stability, corrosion resistance, fatigue behavior, and maintenance procedures. Industry and government, led by the FAA, are actively addressing aging of the existing commercial aircraft fleet. Clearly, it will be important to exploit and disseminate the lessons learned from the experience of the existing fleet.

New aircraft (i.e., aircraft that, in the context of this report, will enter service in the next 15–20 years) will incorporate new materials, fabrication processes, and structural concepts to realize the cost and performance benefits of lighter-weight, more-efficient structures. Use of new structural materials, such as reinforced polymeric composites and advanced light-weight metallic alloys, is increasing as performance requirements become more demanding and service environments more severe.

Evaluation of new materials and structures for commercial aircraft application requires an assessment of performance and operating costs over the entire life cycle of the aircraft, from fabrication to maintenance. Also, a thorough understanding of the long-term material properties and anticipated failure mechanisms is required to adequately develop inspection and maintenance procedures that assure safety over the service life of the aircraft.

The major objective of this study was to identify issues and potential research and technology development opportunities related to the introduction of new materials on the next generation of commercial transports and the expected effect on the life-cycle durability. The committee investigated the likely new materials and structural concepts for next-generation commercial aircraft and the key factors influencing application decisions. Based on these predictions, the committee identified and analyzed the design, characterization, monitoring, and maintenance issues that appeared to be most critical for the introduction of advanced materials and structural concepts. The committee then developed recommendations for needed research aimed at addressing knowledge gaps. Methods by which the FAA could leverage its research efforts with related research in industrial, academic, and other governmental laboratories are also suggested. Evaluation of the FAA's established role in the certification of commercial aircraft was not within the scope of this study, however the recommended research should provide the FAA with an improved understanding of new materials and structures technology to aid in future certification activities.

This study focuses primarily on airframe structures of large subsonic commercial aircraft. However, many of the issues identified will also apply to smaller, general aviation planes (both fixed and rotary wing). The emphasis of this study is, for the most part, restricted to primary and secondary airframe structures.1 While beyond the scope of this study, new materials technology could also significantly benefit major aircraft subsystems, including engines, brakes, auxiliary power units, and environmental control units.

INDUSTRY OVERVIEW AND IMPORTANT TRENDS

To identify likely application of new materials and structures in future commercial aircraft, it is critical to understand the factors that influence materials selection and design decisions. New materials and structures applications depend on the types of aircraft that will be built in the future and the performance requirements for those aircraft. The current economic health of the airline industry and future market analyses will dictate the criteria for new aircraft.

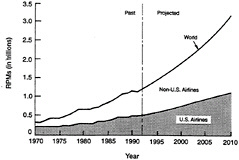

FIGURE 1-1 Past and projected trends in world air travel in revenue-passenger miles (RPM). Source: Janicki (1994).

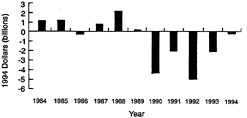

Air travel, in terms of revenue-passenger miles (RPM),2 has steadily increased over the past 20 years (figure 1-1). This trend is expected to continue well into the next century. More passengers are expected to travel more miles, with routes in the Pacific Rim seeing the greatest increase (ATA, 1993). Recently however, increased travel has not translated into greater profits for the airlines. The world's airlines lost more money (approximately $9 billion) in the years 1990–1993 than they had made since the end of World War II (ATA, 1993, 1995). Figure 1-2 shows the variability during the past decade in annual profits and losses for the airline industry.3 Even with the steady increase in the number of people traveling, the costs associated with aircraft purchase, operation, and maintenance, coupled with a worldwide economic recession and fierce competition resulting from the deregulation of the U.S. airline industry, the viability of many of the largest airlines is threatened.

As a result of the airline industry's financial troubles, the market for new aircraft has been weak. The cost of acquisition of new advanced aircraft and relatively low fuel prices have been driving carriers to either retain their aircraft for a longer period of time than originally planned or to purchase (or lease) older or refurbished aircraft from other carriers. Therefore, one of the primary sources of competition for manufacturers of new aircraft are existing or refurbished aircraft. While the basic performance (e.g., number of seats and range) of a new airplane is of considerable importance, the most important airline market factor is the purchase and operating costs incurred by the airlines (Smith, 1994b; Janicki, 1994).

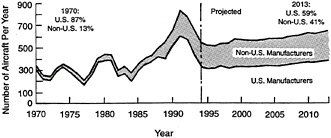

As shown in figure 1-3, aircraft manufacturers forecast a sizable market for new aircraft, based on the projections of substantial growth in passenger travel requirements and the replacement of aging aircraft in the current fleet. While the airline industry has been showing signs of recovering from the economic difficulties of the past five years (ATA, 1995), the recent trends described above will have a profound effect on the design and production of next-generation commercial aircraft.

NEXT-GENERATION AIRCRAFT

The major aircraft manufacturers have recently introduced new aircraft, including the Airbus A340, the McDonnell Douglas MD-11, and most recently, the Boeing 777. New aircraft models range from derivative models that are modifications of existing aircraft designs (e.g., fuselage extensions for increased capacity) to major redesigns with new wings, engines, and empennage. Derivative models have the advantage of similarity to an existing model, leading to reduced design and certification costs. Another benefit is that the similarity of operation and maintenance of derivative models to the existing fleet leads to greater acceptance by the airlines.

Due to the current poor market conditions for any new aircraft, coupled with the high costs and business risks involved with developing new aircraft models, the introduction of additional all-new aircraft in the near term (before the turn of the century) is unlikely. However, derivative aircraft production will continue, and these aircraft frequently exploit the benefits of new materials.

Aircraft manufacturers are currently investigating the feasibility and market for a very large commercial transport (VLCT). The current VLCT configurations under study have double-deck passenger cabins with a 500–800 seating capacity and a range of approximately 6,000–8,000 miles (AWST, 1994a,b,c). The large diameter fuselage, the large material stock sizes required, and the weight limitations imposed by runway loading restrictions in the development of such an

FIGURE 1-2 After-tax profits and losses (based on 1994 dollars) for U.S. scheduled airlines. Data Source: ATA (1995).

FIGURE 1-3 Past and projected manufacturing of commercial transports. Source: Janicki (1994).

aircraft would require significant development in technology and manufacturing capability.

APPLICATION OF NEW MATERIALS

Drivers and Barriers

The potential for the application of new materials exists on all new aircraft, including current production, derivatives, and new models. Drivers in the development and application of new materials traditionally have included performance (e.g., weight and range), durability, and regulatory compliance (e.g., environmental issues). Recently, the cost of acquisition and maintenance has become an overriding concern to the airlines. The result is that all new materials must demonstrate acceptable cost and sufficient performance improvements to justify or "pay their way" into production application.

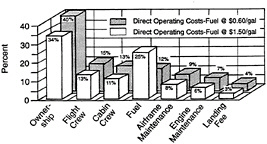

Airframe life-cycle costs, including ownership costs (airplane price and financing expenses) and operating costs (fuel and maintenance), are a significant part of the total cost

FIGURE 1-4 Breakdown of direct operating costs for two fuel-price estimates.

Source: Janicki (1994).

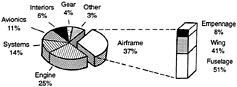

of an aircraft to an airline. Figure 1-4 shows a breakdown of direct operating costs based on extremes in fuel prices. The largest contributor to airline costs is the cost of ownership. As shown in figure 1-5 the airframe represents a significant fraction (37 percent) of the total cost of the aircraft. Regardless of aviation fuel prices, the costs related to airframe materials and structures are significant components of the total costs. The trends in environmental regulations worldwide will make end-of-life disposal or recycling of components more important factors in life-cycle costs.

Another concern indirectly related to the application of new materials is the health of the advanced materials industry itself. The economic viability of a large sector of the advanced materials industry is threatened because of significant reductions in the military markets, the economic decline in commercial aerospace, unrealistic market forecasts, and increased international competition (Seagle, 1994). In the current business environment, it is difficult for materials suppliers to commit to expensive design, development, and qualification efforts needed to evaluate and fabricate a new material for commercial aircraft applications. The necessary long lead times, significant resource commitments, and perceived high

FIGURE 1-5 Breakdown of total aircraft cost. Source: Janicki (1994).

technical risks involved in competing for applications represent major barriers for materials suppliers.

In the past, the commercial aircraft industry has taken advantage of materials that were developed and characterized as part of military programs. Significant progress, most noticeably in the development and understanding of structural composites and significant production capability in advanced materials, has come through military research and development and hardware development efforts. As a result of recent reductions in U.S. Department of Defense acquisition programs, the benefit to the commercial industry from military programs will be largely curtailed. Nevertheless, the materials and aircraft industry must seek ways to continue to develop improved materials and innovative processes.

For current-production aircraft, the incentives to introduce new materials include improved maintenance and reliability, conformance with new environmental regulations, and manufacturing cost reduction. With the possible exception of environmental compliance, material substitutions on current aircraft will only be made if there is minimal impact on designs or tooling. The high cost of material qualification, changes to engineering drawings and data sets, and component certification are significant barriers to materials substitutions.

For derivative or new aircraft, the incentive to introduce new materials include reduced airline maintenance and operating costs, reduced production and rework costs, reduced manufacturing cycle time, and compliance with environmental regulations. Although qualification costs can inhibit the introduction of new materials and structural concepts on derivative models, the consideration of incentives described above are evolving production toward short development cycles, cost reductions, and customer-preferred options. Weight savings can also be a significant factor on new or derivative designs, especially for long-range aircraft. As a design matures, the issue of weight can become increasingly important in order to meet performance commitments. Barriers to new materials applications on new and derivative aircraft include the cost of developing an engineering and processing database and manufacturing capability and the general reluctance of airlines to accept the higher potential cost and risk in the operation and maintenance of airplanes due to new materials and structural concepts.

Aircraft safety remains a central concern of the aircraft industry and the fundamental basis for structural design criteria. Because of the excellent safety record held by commercial aviation, the public is less willing to accept aircraft accidents as inevitable (AWST, 1995).

Airlines and manufacturers are conservative about implementing new technologies because they are less willing to accept business risks (including liability) introduced by the technological risks associated with new technologies. The implementation of new materials always represents a technological risk that must be weighed against the performance benefits and the confidence in design and evaluation procedures.

Projected Evolutionary Advances

As in the past, new materials and structural concepts will inevitably but gradually be introduced into commercial aircraft. During the next 20 years, the projected technological readiness of new materials will result in their utilization in primary structures that include:

-

advanced metallic fuselage,

-

structural composite wing, and

-

composite fuselage components.

The specific timing of these advances is very difficult to project because of the turbulent business climate and the dynamic nature of the factors influencing aircraft design.

Aircraft manufacturers have recently employed design teams and concurrent engineering approaches to implement new materials and structures technologies (Smith, 1994a). By involving all of the major stakeholders—including airline customers and design engineering, manufacturing, and supplier organizations—in the early design stages, their requirements can be addressed early in the development of component design. For example, airline concerns over operational and maintenance costs influence initial design criteria, component producibility becomes a key criterion, supplier-provided materials characteristics can be effectively tailored to needs, and known materials limitations can be accommodated during the first component design. This approach has significantly increased the production application of new developmental materials. For example, on the Boeing 777, approximately 60 percent of the program's materials development efforts that were underway when the decision was made to produce the airplane led to production applications (Smith, 1994a), an impressive achievement from a developmental viewpoint.