4

Economic Impact of the Oil Pollution Act of 1990 on the International Tanker Fleet

The purpose of this chapter is to assess the economic impact of the Oil Pollution Act of 1990 (OPA 90), Section 4115 and MARPOL Regulations I/13F and I/13G (MARPOL 13F and 13G) on the operations of the international tanker fleet. The committee concluded that the likely economic impact of these regulations will consist mainly of increased costs arising from (1) increased capital expenditures to replace retired tankers with double-hull tankers; (2) increased operating expenses of double-hull tankers; and (3) costs associated with the timing of the replacement of single-hull vessels.

The replacement of existing tankers with double-hull instead of single-hull tankers will be the costliest of these items. As existing tankers are phased out. supply will eventually fall below actual (and perceived) demand. The resulting gap between supply and demand will be filled by the construction of new tankers or the conversion of existing ones. Beginning January 1, 1994, new and converted tankers must have double hulls. The committee has used two approaches toward assessing the evolution of tanker demand and supply to ascertain the likely characteristics of the new double-hull tanker fleet: (1) a computer model using certain assumptions to isolate the impacts of Section 4115 and MARPOL 13F and 13G and (2) an analysis of how ''real-world" events may differ from the computer model. The international market is characterized by the highly competitive structure and conduct of the participants.1 Accordingly, demand, supply,

new construction, and scrapping are determined mainly by freight rates, although investment in new tankers may be driven by market sentiment rather than by strict economics.

Tanker Supply and Demand

At year-end 1995, the world tanker fleet consisted of about 3,000 tankers with a total capacity of 255 million deadweight tons (DWT). In addition, combined carriers designed to carry ore, dry bulk, or oil as cargo, totaling 25 million DWT, raised the potential capacity to 280 million DWT.2 To determine the size and makeup of the new double-hull tanker fleet arising from the implementation of OPA 90 and MARPOL, it was necessary to determine the number of tankers that will be needed to carry oil in the future, as well as the current and prospective supply of tankers. Estimates of future tanker demand should include both the new construction necessary to replace the existing fleet as it ages or is forced to retire and the new construction needed to carry any increase in demand for oil.

Tanker Supply

The differing impacts of Section 4115 and MARPOL 13F and 13G on the wide range of vessels used in the maritime oil transportation industry required the committee to develop a methodology for determining the effective supply of tankers over the next 20 years. (The methodology, developed in conjunction with industry experts, is defined in Appendix F.)

Vessels in the international fleet were assigned to one of four categories: double-hull vessels, double-side or double-bottom vessels, and single-hull vessels, either pre-MARPOL or MARPOL (see Figure 4-1).

Because both Section 4115 and 13F and 13G use vessel age as a criterion, the age profile of the fleet will be a significant determinant of how these regulations change the composition of the fleet. The age of the current fleet continues to reflect the impact of the shipbuilding boom of the mid-1970s. Peak capacity is found in vessels between 16 and 20 years of age, as can be seen in Figure 4-2.

The future impact of Section 4115 on the size of the international tanker fleet able to call at U.S. ports is shown in Figure 4-3. The sharp decline in 2015 marks the end of the deepwater port and lightering zone exemption that allows single-hull tankers (assumed to be tankers exceeding 120,000 DWT) to continue trading to the United States until that year.

Section 4115 does not force tankers to retire but bans them from trade to the United States. Tanker retirement, however, will be forced by the phaseout

FIGURE 4-1 Capacity of international tanker fleet by hull type as of October 1995.

Source: Navigistics, 1996.

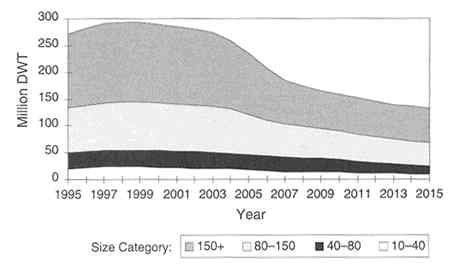

schedule of 13G.3 The retirement by year of international tankers as a consequence of 13G is shown in Figure 4-4, where it is compared to the impact of Section 4115.4 Regulation 13G will have the greatest impact during the period 2004 to 2008, when vessels constructed during the shipbuilding boom of the mid-1970s will reach the 30-year age limit. To the extent that 13G affects trading to the United States, some tankers will be retired earlier than they might have been under the OPA 90 lightering zone exemption. The figure does show, however, that Section 4115 will have a stronger impact because of its 25-year age limit, as opposed to the 30-year limit of 13G.

Figure 4-4 assumes that pre-MARPOL tankers will continue trading to 30 years using hydrostatically balanced loading (HBL), rather than being retired at 25 years—in other words, HBL will extend the retirement age of tankers built during the boom of the mid-1970s by five years, beginning in 1999. Thus, a tanker that reaches age 25 in 1999 is assumed to operate until 2004. This impact will largely be eliminated by 2008. Figure 4-5 shows the impact on the

FIGURE 4-6 Impact of MARPOL 13G on the international tanker fleet by size category through 2015.

international fleet if no vessels utilize HBL and compares this result to the impacts if all vessels implement HBL. Figure 4-6 shows the projected fleet, as affected by 13G, by size category (including orders for new construction as of October 1995) from 1995 to 2015.

International Tanker Demand

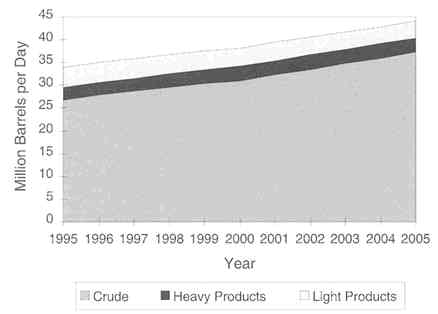

The analysis of demand for tankers is restricted to the 1995 to 2005 period because the committee determined that estimates of oil demand after 2005 are too unreliable for coherent analysis. Projections of oil demand were provided by PIRA Energy Group (1995) and compared with similar projections by Marine Strategies International (1996a) and the U.S. Department of Energy (EIA, 1996). Figure 4-7 shows projected crude and petroleum products oil flows to 2005. Crude oil movements, which account for about 80 percent of the tanker trades, grow at an annual rate of 3.3 percent, whereas oil products continue relatively flat.

The projected pattern depicted in Figure 4-7 masks important changes in the underlying trades that will have a considerable impact on tanker markets (PIRA, 1996). In the U.S. trade, short-haul imports from Latin America are projected to double, offsetting a decline in long-haul shipments from the Middle East and Africa. In Western Europe, crude imports decline by 10 percent between 1995 and 2000, followed by 38 percent growth to 2005. Imports of Middle East crude to Western Europe decline by 16 percent by 2000 but reverse with a 44 percent

increase by 2005. The projected declines between 1995 and 2000 are offset by sharply increasing crude imports from the former Soviet Union (FSU), which more than double by 2005. China, Southeast Asia, and Japan continue as markets of rapid growth through 2005, accounting for more than 60 percent (compared to 40 percent currently) of Middle East crude exports and resulting in a substantial reduction in longer-haul shipments. The shift from long to shorter hauls—notably in trade to the United States, China, Southeast Asia, and Japan—indicates that for the next few years, the increasing oil flows traced by Figure 4-7 will not be translated into corresponding increases in tanker demand because individual tankers traveling over shorter distances will be able to carry more oil per year.

Although the committee relied on the PIRA base case forecast to calculate tanker requirements, there are other credible scenarios of tanker demand. Hence, the future demand for tankers cannot be predicted with confidence (Stopford. 1996). For instance, PIRA assumes an early resumption of Iraqi oil exports that will displace 7 million DWT of very large crude carriers (VLCCs) and a rapid rate of FSU exports that will displace another 10 million DWT because both Iraqi and FSU oil exports will utilize pipelines for all or part of their transportation. If any of these assumptions fail to materialize, tanker demand will be significantly altered; the examples cited would change tanker demand by 17 million DWT. In the committee's judgment, the PIRA analysis is the most realistic.

FIGURE 4-7 International tanker oil flows, 1995-2005. Source: PIRA. 1995.

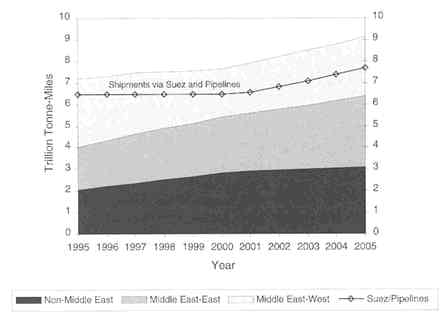

FIGURE 4-8 Interregional crude oil exports by region, 1995-2005. Source: PIRA, 1995.

Crude oil exports by region of origin between 1995 and 2005 are summarized in Figure 4-8. This figure illustrates the relative importance of Middle East exports of crude and the vigorous pace of such exports to eastern destinations. Also shown is the impact attributed to pipelines and the Suez Canal, which shorten voyage distances and reduce tanker requirements. The extent and timing of any resumption of Iraqi oil exports will have a significant impact on near-term demand. Figure 4-9 translates projected oil flows into tanker requirements for the transport of crude oil and products. Tanker demand in the projection remains stagnant to the end of the 1990s and resumes growth in the next century.

Supply-Demand Balance

Impact of HBL Requirements for New Construction

Tanker supply is defined here as the existing fleet of international tankers and combined carriers, augmented only by newbuildings on order as of October 1995 and diminished only by the mandatory phaseout provisions of OPA 90 and MARPOL. This definition is designed to isolate the impacts of Section 4115 and 13G.

FIGURE 4-9 Tanker requirements for the transportation of crude oil and petroleum products, 1994-2005. Source: PIRA, 1995.

Under competitive conditions, when current demand approaches current supply, freight rates rise (see Appendix G). If future freight rates are perceived as generating a profit, newbuildings are ordered. The operation of a competitive market, therefore, is self-adjusting in that any deficiency in tanker supply induces the construction of new tonnage.

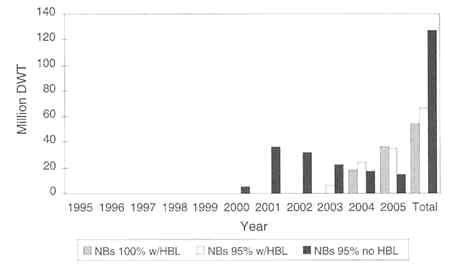

By subtracting demand from potential supply, the tanker surplus (or deficiency) can be derived and should be equal to the minimum tanker capacity (ordered after October 1995) necessary to offset the deficiency. In the following analysis, three scenarios are used to estimate newbuilding requirements: owners take delivery of new vessels (1) only when demand equals 100 percent of maximum supply, including HBL and all oil-bulk-ore vessels (OBOs); (2) when demand reaches 95 percent of maximum supply; and (3) when demand reaches 95 percent of supply without HBL. The results are shown in Figure 4-10.

The first two scenarios are designed to isolate the impacts of OPA 90 and MARPOL. The first scenario estimates that newbuilding deliveries start in 2004 and total about 55 million DWT by 2005. The second scenario estimates that newbuilding deliveries start in 2003 and will amount to about 66 million DWT by 2005. Under the third scenario, retention of existing capacity does not occur; newbuilding requirements begin in 2000; and by 2005, new deliveries total about

FIGURE 4-10 Aggregate supply-demand tanker balance with and without HBL, 1995-2005. Note: Max = maximum; Sup = supply.

127 million DWT. The newbuilding requirements under the three scenarios are summarized in Figure 4-11.

Hence, the key item in determining the required level of newbuildings will be the extent to which the HBL option is utilized by shipowners during the next few years. Clearly, the HBL alternative, if fully utilized, would provide a huge amount of equivalent tonnage. At its peak in 2003, the HBL option provides close to 90 million DWT, or one-third of the current tanker fleet (Table 4-1).

The extent to which shipowners adopt HBL will be determined by the condition of each tanker, the costs of life extension, and prevailing freight rates (MSI, 1996a). So far, no VLCCs have operated beyond age 25, and the average age of VLCCs scrapped in the last five years was much lower (see MSI, 1996a, and Figures 3-3 and 3-4). Some owners may forgo the HBL alternative and scrap their tankers earlier to avoid paying the high price of the special surveys required for a shortened period of service in a market increasingly favoring modern tankers. The self-adjusting market mechanism notwithstanding, the unsynchronized decisions of owners planning newbuildings and those facing scrapping of old ships

FIGURE 4-11 Tanker newbuildings required under MARPOL 13G for 1995-2005 with and without HBL. Note: NBs = newbuildings; w = with.

(who may be different people) could lead to periods of temporary imbalance with a significant short-term impact on freight rates. Moreover, seasonal spurts in demand (see Appendix H) could temporarily put pressure on capacity and cause freight rates to rise, inducing some shipowners to place early orders for newbuildings.

For these reasons, analysts are predicting a gradual tightening of tanker tonnage balances and increasing orders for new tankers in the next few years. Both

TABLE 4-1 Additional Fleet Capacity in Million DWT after Adoption of HBL

|

Year |

Additional DWT |

|

1995 |

1.6 |

|

1996 |

3.7 |

|

1997 |

4.9 |

|

1998 |

9.0 |

|

1999 |

21.2 |

|

2000 |

41.7 |

|

2001 |

65.1 |

|

2002 |

82.8 |

|

2003 |

88.8 |

|

2004 |

81.3 |

|

2005 |

61.0 |

Marine Strategies International (MSI) and Clarkson predict that double-hull tanker deliveries will average 20 million DWT annually between 1998 and 2000 and continue at a high level through 2004 (Stopford, 1996). PIRA forecasts that by the end of the 1990s, ''tanker order books are likely to be at the highest level in over 20 years" (PIRA, 1996).

Regardless of the timing of deliveries of new double-hull vessels, it is very likely that the market will tighten over the next two to three years because of the aging of the many tankers built in the 1970s, an accelerated rate of scrapping induced by OPA and MARPOL, and the current low level of tanker orders, which is the lowest in eight years.

Supply-Demand Balance by Vessel Size

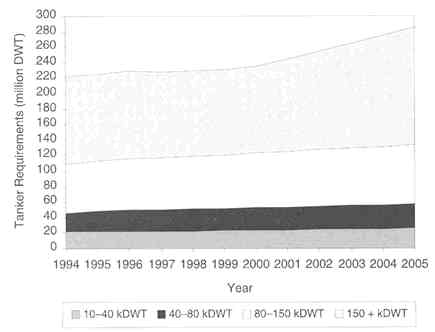

Projections of demand for the international tanker fleet as a whole are shown in Figure 4-12; projections of supply and demand by vessel size are shown in Figure 4-13. In the early years a tighter balance is indicated for smaller tankers, whereas a significant longer-lived surplus is suggested for the larger ships, particularly VLCCs. In Figure 4-13, the apparent shortage in tanker capacity from

FIGURE 4-12 International tanker requirements for all size segments, 1995-2005. Note: kDWT = 10 3 DWT.

1995 to 1998 for the 10,000 to 40,000 DWT segment arises from the exclusion of the sizable fleet of chemical tankers, many of which also carry oil.

Requirements for larger tankers of more than 150,000 DWT shown in Figure 4-13 are based on the different forecasts of PIRA and MSI. Because this segment is the most vulnerable to HBL penetration, it tends to dominate the supply-demand balance in the entire market. Additionally, the deepwater port and lightering exemption of OPA 90 will enhance the appeal of using HBL for larger vessels.

Factors Influencing Supply and Demand

The previous discussion suggests an orderly pattern of scrappings and new construction determined by the interaction of supply and demand, albeit with uncertainty regarding the use of HBL. However, a strictly rational approach must be modified by other factors, including freight rates that are at this time substantially lower than those required to support newbuilding, the apparent absence of a two-tier market that would reward double-hull tankers, the continuing change in the tanker market structure, and the present dearth of orders for new construction.

Required Freight Rate

The charts in Figure 4-14 compare the required freight rate (RFR) of typical tankers with actual rates in 1992 through 1995 and the first half of 1996. RFR is defined as the rate required to cover tanker operating expenses and realize a desired return on capital, assumed in this case to be 10 percent. The charts show that actual freight rates during the period averaged around 60 percent of the RFR, with VLCCs averaging about 57 percent, Suezmax tankers 65 percent, and the others in between. Actual rates improved during the first half of 1996 but were still less than 70 percent of the RFR for all vessel classes.

The overall picture reflects the depressed state of the international tanker market from 1992 to 1995. Average market rates for a one-year time charter for modern tankers have been less than two-thirds of the RFR. The depressed freight rates of 1992 to 1995 are typical of the last 20 years. For 16 out of those 20 years, modern tankers have been chartered below cost (Stopford, 1996). Overall, the return on net assets in the tanker business during 1990 to 1994 period was about 1.4 percent for product carriers, 3.8 percent for Aframax tankers, and zero for tankers of more than 100,000 DWT. Many tankers showed a negative return. Freight rates are now higher, but they must rise even further if they are to induce the construction of enough double-hull tankers to replace retiring single-hull ships, unless shipbuilding capacity is so high that tankers can be delivered below cost, which seems unlikely.

FIGURE 4-14 RFR by market segment, 1992-1996. Data for first six months of 1996: (a) VLCCs; (b) Suezmax tankers; (c) Aframax tankers; (d) handy-size product tankers.

Note: T/C = time charter. Source: MSI, Freight Forecaster, 1996b.

Two-Tier Freight Rate Market

Shortly after enactment of OPA 90, it was anticipated that modern tankers in general, and double-hull tankers in particular, would charge a higher freight rate to compensate for their higher quality and to help cover their higher cost of construction. The committee has obtained information from several experts and has reviewed available data to determine if any such rate premium was paid for newer

ships, for double-hull construction, or for trading to the United States. In general, ship brokers and other experts declined to affirm the existence of a rate differential for tankers in these categories (Jones, 1995; Loucas, 1995; Shawyer, 1995). They did believe, however, that given equal rates, quality tankers would be preferred. These views were summarized in a letter to the committee from the London Tanker Brokers' Panel (see Appendix I).

Others present a different view. A rigorous statistical analysis has been

TABLE 4-2 Two-Tier Markets after OPA 90

performed to determine whether a quantifiable premium was paid for modern, double-hull tankers in general and for tankers trading to the United States in particular (Tamvakis, 1995). The study examined 14,000 crude oil spot fixtures covering 1,600 crude oil tankers of 60,000 DWT or more from January 1, 1989, to June 30, 1993. The data were grouped into tanker size segments and time periods before and after the enactment of OPA 90. With respect to the post-OPA 90 period, tankers bound for the United States (regardless of size) received higher rates than tankers bound for other destinations (see Table 4-2).

The Tamvakis (1995) study may chiefly reflect the impact on U.S. rates of the liability features of OPA 90 rather than its double-hull requirement. The greater risks and costs embodied in guarantees of financial responsibility and higher protection and indemnity (P&I) premiums5 have, in effect, imposed a

penalty on shippers delivering cargo to the United States. In non-U.S. trade, VLCCs were the only group of double-hull tankers that appeared—on the basis of limited statistical evidence—to earn premium rates. This finding may reflect the efforts of some nations, notably Japan and Finland, to attract vessels of superior design and below-average age. In any event, the differential rate that has prevailed falls short of what is needed to compensate for the capital cost of new construction.

Change in Market Structure

In the last 20 years, the market for tankers has witnessed a gradual but significant change. As the cost of oil transport fell to a small fraction of the delivered price, some oil companies began to retreat from the tanker business. Increasingly, the responsibility for transport has shifted from oil companies to oil traders (Stopford, 1996).

Although the size of the tanker fleet as a whole increased by more than 50 percent between 1973 and 1994, seven major oil companies6 cut their company fleets in half, a decline from 43 million DWT (599 ships) to 22 million DWT (184 ships). This represented a 49 percent reduction in tonnage and a 69 percent reduction in ships. The oil companies' share of the international fleet trading to the United States fell from 23 percent of the tonnage employed in 1990 to 17 percent in 1994.

Chartering has also changed considerably. The proportion of the independent fleet on time charter (long-term contracts) to oil companies decreased from 80 percent in 1973 to 20 percent in 1988, whereas independent tankers hired on short-term contracts increased from 20 to 80 percent over the same period. In 1995, 2,098 tankers completed 14,409 spot market fixtures (Stopford, 1996).

Reduction in Tanker Construction Orders.

Prevailing freight rates and changes in market structure have contributed to a significant reduction in orders for new tankers. Construction orders as of July 1, 1996, are shown in Table 4-3. Only about 16 million DWT of crude and product tankers were on order in June 1996, and only 27 crude and product tankers, amounting to 3.2 million DWT (2.2 percent of the existing fleet on an annualized basis), were ordered during the first half of 1996. In 1991, orders reached 6 percent of the tanker fleet. In 1997, scheduled deliveries will fall to 2 percent of the tanker fleet (Clarkson, 1996a).

This decline is not attributable to OPA and MARPOL, because mandatory phaseouts would ordinarily have encouraged new construction. The sluggishness in orders for new tankers is apparently the result of an oil transportation market

TABLE 4-3 Tanker Fleet and Orderbook as of July 1, 1996

|

|

|

|

Orderbook (106 DWT) |

||||||

|

Vessel |

Segment (103 DWT) |

Fleet (106 DWT) |

1996 |

1997 |

1998+ |

Total |

|||

|

VLCC |

200+ |

125.3 |

4.0 |

1.8 |

1.2 |

7.0 |

|||

|

Suezmax |

120-200 |

39.8 |

1.1 |

1.7 |

0.3 |

3.1 |

|||

|

Aframax |

80-120 |

41.7 |

1.0 |

2.0 |

1.3 |

4.3 |

|||

|

Panamax |

60-80 |

14.6 |

0.1 |

0.0 |

0.0 |

0. 1 |

|||

|

Small |

10-60 |

40.5 |

1.5 |

0.2 |

0.0 |

1.7 |

|||

|

Total |

|

261.9 |

7.7 |

5.7 |

2.8 |

16.2 |

|||

|

Source: Clarkson Research, 1996a. |

|||||||||

that is strong enough to be profitable for older single-hull tankers (hence, a low scrapping rate) but not strong enough to pay the costs of new double-hull tankers (PIRA, 1996). Considering the higher freight rate required to cover the cost of a new tanker, the absence of an adequate two-tier market, and the dominance of spot market fixtures over period charters, independent owners (who hold 65 percent of the fleet) are reluctant to order new tonnage. Despite the certainty of mandatory scrapping of vessels and favorable shipbuilding prices, tanker orders are currently at their lowest level in more than eight years.

If tanker orders do not resume, the market is likely to enter a temporary period of sharp freight rate volatility. Pressures to build would then rise, and a rush to build might cause a temporary glut of orders, but shipbuilding capacity appears adequate to accommodate any increased level of construction. The market will discourage any pronounced long-term bunching of orders. If freight rates are low, resulting in few orders, the price of construction will go down so that shipyards can be better utilized. Alternatively, if freight rates increase and many orders are placed, prices will rise, thereby discouraging further orders.

Adequacy of World Shipbuilding Capacity and Financing

Estimates of Shipbuilding Capacity and Demand

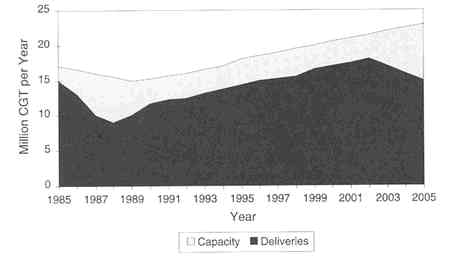

Recent reports from Europe and Japan conclude that worldwide shipbuilding capacity over the next several years will exceed demand. A European report (de Albornoz, 1996) states that capacity fell during the 1980s to a low of approximately 15 million compensated gross tons (CGT)7 by 1990 but that it has been

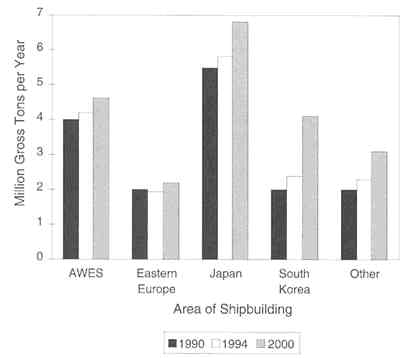

FIGURE 4-15 Increase in shipbuilding capacity by geographic area, 1990-2000. Note: AWES = Association of West European Shipbuilders. Source: de Albornoz, 1996. Reprinted with permission of the Society of Naval Architects and Marine Engineers (SNAME).

increasing since then. Figure 4-15 shows the actual increase in capacity over the period 1990 to 1994 by geographical area and projections to the year 2000.

The expansion of capacity is attributed to several factors, including regular increases in productivity in Western Europe, Japan, and Korea; the creation of several large new yards and additional dry docks in South Korea; and the reentry of Eastern European, former Soviet Union (FSU), and U.S. shipyards into the merchant shipbuilding market. Predictions are that building capacity will exceed demand through 2005 but that excess capacity will fall to a minimum around the year 2000 (see Figure 4-16).

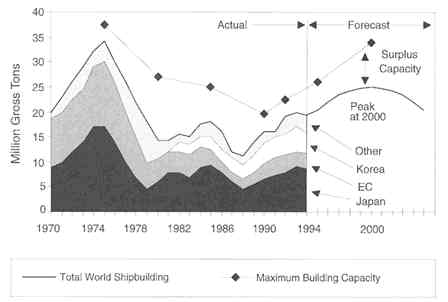

A recent Japanese report (JAMRI, 1995) took a slightly different approach by ascertaining the number of shipbuilding berths and using gross tons rather than compensated gross tons as a measure. Table 4-4 shows the number of building berths or docks for new ships exceeding 40,000 DWT. Most of the new berths or docks are for vessels exceeding 250,000 DWT. Figure 4-17 presents a comparison of shipbuilding supply and demand in gross tons.

FIGURE 4-16 Comparison of shipbuilding capacity and forecast newbuildings—European estimate. Source: de Albornoz, 1996. Reprinted with permission of SNAME.

Although the recent European and Japanese surveys vary in monetary numbers and dates of peaking, their conclusions are similar: there will be a surplus of newbuilding capacity even when demand peaks at the end of the 1990s.

Availability of Capital

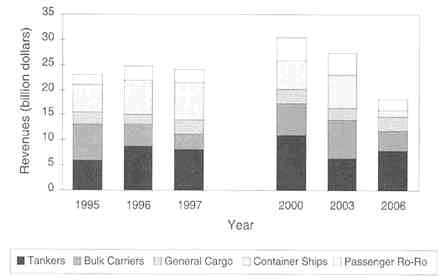

The availability of capital to finance tanker construction will depend on total shipbuilding demand, given that purchasers of all types of vessels compete for capital. Figure 4-18 presents the estimated future capital requirements for new

TABLE 4-4 Number of Shipbuilding Berths or Docks for Vessels Exceeding 40,000 DWT

ship construction for selected years to 2006. It is estimated that about $35 billion to $47 billion8 will be needed to finance the new double-hull tankers to be constructed between 1995 and 2000, compared to the $23 billion to $30 billion spent from 1990 to 1995.

Although the demand for financing is expected to peak in the year 2000, the yearly average between 1995 and 2000 will be on the order of $8 billion. Although the demand for capital will be significantly higher than in the first half of the 1990s, the financial community believes that sufficient capital will be available at reasonable interest rates (Newbold and Grubbs, 1995). Reductions in interest rates during the first quarter of 1997 and oversubscription of shipping investment schemes appear to confirm this view.

Economic Costs of OPA 90 and Marpol

Incremental Capital Costs

On the basis of a review of industry literature, presentations by various shipbuilders, and questionnaire responses (see Chapter 6), the committee developed a shipbuilding price differential between double-hull and single-hull tankers that is shown in Table 4-5. The increase in cost per DWT for double-hull vessels is estimated at between 9 and 17 percent.

The estimated increase in the cost of building a double-hull fleet of the same size and composition as the tanker fleet in existence on April 1, 1996, is on the order of $12 billion, as shown in Table 4-6. Given a renewal period of 20 years, the annual increase would average about $0.6 billion per year.

Incremental Operating Costs

In comparing the operating costs of double-hull and single-hull tankers of similar size and age, the committee found that maintenance and repair (M&R) and hull and machinery (H&M) insurance premium costs were the only costs that showed marked differences.9

Maintenance and Repairs

The only difference between double-hull and single-hull cost in the M&R category is in the cost of maintaining and repairing the protective coatings in the tanks of double-hull vessels. Because such costs are not normally incurred until

|

8 |

Estimates of capital requirements are in 1996 dollars with no inflation imputed. |

|

9 |

Insufficient data were available for the committee to quantify potential cost offsets associated with double-hull tanker operations. According to operators surveyed by the committee, double-hull tankers offer reduced times for discharge of cargo and cleaning of cargo tanks (see Chapter 6). |

TABLE 4-5 Tanker Newbuilding Prices as of April 1, 1996

|

|

Double Hull |

Single Hull |

Cost Increase |

||||

|

Vessel DWT |

Tanker Type |

($ million) |

($/DWT) |

($ million) |

($/DWT) |

($/DWT) |

(%) |

|

47,000 |

Product |

33.5 |

713 |

30.5 |

649 |

64.0 |

9.9 |

|

67,000 |

Product |

40.0 |

597 |

36.0 |

537 |

60.0 |

11.1 |

|

105,000 |

Aframax |

42.0 |

400 |

36.0 |

343 |

57.0 |

16.7 |

|

153,000 |

Suezmax |

51.5 |

337 |

44.0 |

288 |

49.0 |

17.0 |

|

300,000 |

VLCC |

80.5 |

268 |

70.0 |

233 |

35.0 |

15.0 |

later in the life of a tanker, the costs discussed here are total M&R costs for the first 15 years of life. The committee's estimates of M&R costs for double-hull and single-hull VLCC, Suezmax, and Aframax tankers are shown in Table 4-7. The costs for double-hull tankers exceed those for single-hull tankers by 11 to 37 percent, depending on vessel type.

It should be noted here that the committee's estimates of the M&R costs of the two types of vessels depend on the assumption that the added cost associated with double-hull coatings is proportional to the increase in coating area. An earlier NRC study (NRC, 1991) estimated the incremental M&R costs of double-hull tankers to be considerably higher than those estimated here. A more recent study (Whiteside, 1996) asserted that increased vigilance in checking coatings and internal spaces in double-hull tankers would result in the early discovery of problem areas and hence no additional costs for double-hull M&R over the long run.

Insurance Premiums

It is estimated that the costs of marine H&M and war risk insurance per gross ton (GT) for a double-hull VLCC or Aframax tanker are about 6 percent higher

TABLE 4-6 Increased Cost of Building the Double-Hull Fleet

|

|

|

|

|

|

Cost Increase |

|||||||

|

Vessel Type |

Size Range (kDWT) |

Total Million DWT |

Double Hull ($/DWT) |

Single Hull ($/DWT) |

($/DWT) |

(%) |

Total ($ billion) |

|||||

|

Small |

10-60 |

40.5 |

713 |

649 |

64.0 |

9.0 |

2.60 |

|||||

|

Aframax |

60-100 |

48.6 |

400 |

343 |

57.0 |

16.7 |

2.80 |

|||||

|

Suezmax |

100-200 |

46.9 |

337 |

288 |

49.0 |

17.0 |

2.30 |

|||||

|

VLCC |

200+ |

125.4 |

268 |

233 |

35.0 |

15.0 |

4.40 |

|||||

|

Total |

|

261.4 |

|

46.3 |

|

|

12.10 |

|||||

|

Source: Fleet distribution from Clarkson Research, 1996; cost per DWT from previous table. |

||||||||||||

TABLE 4-7 Comparison of Maintenance and Repair Costs ($/DWT/year) for a Double-Hull and Single-Hull Tankers by Vessel Type

|

Vessel Typea |

Double Hull |

Single Hull |

Cost Increase (% increase) |

|

VLCC |

4.89 |

4.41 |

0.48 (11) |

|

Suezmax |

7.62 |

5.95 |

1.67 (28) |

|

Aframax |

7.78 |

5.69 |

2.07 (37) |

|

aM&R differential for small tankers could not be ascertained owing to lack of data. |

|||

than for a single-hull tanker of comparable size and age. This difference arises solely from the higher purchase cost of a double-hull vessel.

Discounts in P&I insurance rates are given to all vessels with segregated ballast tanks and vary according to the tanker's age. Token P&I insurance rate discounts given between double-hull tankers in the years 1992 to 1995 were terminated in February 1996. Thus, there are currently no significant differences in P&I insurance costs between double-hull and single-hull tankers. Increases in total insurance costs for various types of double-hull tankers are on the order of 1 percent for VLCCs, 3 percent for Suezmax tankers, and 4 percent for Aframax tankers.

Total Operating Costs

When the increased cost percentages shown above are added to the operating costs for single-hull tankers reported by Drewry (1994), the increase in operating costs attributable to double-hull tankers is estimated at 5 to 13 percent, as shown in Table 4-8. The annual incremental operating cost of a double-hull fleet comparable to the existing fleet is estimated to be on the order of $900 million.

TABLE 4-8 Increase in Operating Costs for Double-Hull Tankers

|

|

Operating Costs ($ thousand/year) |

|

Increases Attributable to Double Hull |

|

|

|

|

|

Single Hull |

Double Hull |

(%) |

($/DWT/year) |

DWT of Segment (106 DWT) |

Cost Increase ($ million) |

|

Product |

3,035 |

3.430 |

13 |

9.86 |

40.5 |

309 |

|

Aframax |

3,584 |

4,050 |

13 |

5.18 |

48.6 |

252 |

|

Suezmax |

4.212 |

4,675 |

11 |

3.31 |

46.9 |

155 |

|

VLCC |

5,845 |

6,137 |

5 |

1.04 |

125.4 |

131 |

|

Total |

|

|

|

|

261.4 |

937 |

TABLE 4-9 Incremental Costs of Double-Hull Fleet

|

|

Annualized ($ billion) |

20 Year Cycle ($ billion) |

|

Incremental capital cost |

0.6 |

12.1 |

|

Incremental operating cost |

0.9 |

18.7 |

|

Total incremental cost |

1.5 |

30.8 |

Table 4-9 summarizes the incremental cost of both constructing and operating a double-hull fleet comparable in size and composition to the existing fleet. The committee estimates the incremental cost to be on the order of $1,500 million per year, or about 10 cents per barrel of oil transported. The 10-cent increment was obtained by dividing the annual incremental cost by ocean trade flows of crude oil and products, which are about 15,700 million barrels (MSI, 1996a). This rough estimate is at the lower end of estimates reviewed by the committee. The NRC study (1991), using the higher prices and costs prevailing at the time, reported an incremental cost of 16 cents per barrel for oil shipments to the United States by double-hull tankers. A more recent study (Brown and Savage, 1996) estimates the incremental cost for U.S. trade to be 14 cents per barrel. That study assumes a loss of cargo capacity resulting from the double-hull structure, which in the opinion of the authors ''dictates an increase in fleet size of 2.43 percent." In the committee's judgment, any loss of cargo capacity would be largely offset by effective double-hull designs and would occur only under special circumstances.

Tanker Replacement

The committee conducted an analysis to determine if the phaseout schedules of OPA 90 and MARPOL would result in any changes in the normal ship replacement cycle. The analytical approach used is described in Appendix J. Highlights are presented below.

As a ship gets older, the owner must decide between continued operation of an old, less efficient vessel that may be in need of some repair or replacement by a new, efficient vessel with a high acquisition cost. For the purposes of this analysis, sale of a ship to another owner to operate is not considered;10 the owner's only options are to operate or to scrap. Therefore, the owner will replace the ship only if (1) the ship is not seaworthy, (2) the tanker cannot be operated economically, or (3) regulations require scrapping. In general, the scrapping age follows a normal (bell-shaped) distribution (Figure 4-19).

FIGURE 4-19 Generalized distribution of scrapping.

The question is whether Section 4115 will cause some tankers to be scrapped and replaced earlier than the owner would otherwise desire. A vertical line drawn at a particular age on the normal distribution curve illustrates the effect of early scrapping. If ship operation is not allowed (or is too expensive) after this age, the curve is truncated at this point. The tail of the curve to the right of the vertical line indicates the impact of early scrapping.

A number of factors would maximize the impact of early scrapping due to Section 4115:

- Current tankers are in good condition, and the owners wish to operate them longer than the regulatory age restrictions allow.

- There are no non-International Maritime Organization (IMO) trades suitable for such tankers, and they must be scrapped.11

- New tankers are much more expensive than they would be without Section 4115.

- New tankers have no operating efficiencies over old tankers.

TABLE 4-10 Break-Even Special Survey Costs ($ million) for Pre-MARPOL Tankers in International Trade

|

|

Capacity Reduction |

|

|

|

Tanker Size (DWT) |

0 percent |

5 percent |

8 percent |

|

40,000 |

12.7 |

11.4 |

10.6 |

|

60,000 |

13.9 |

12.5 |

11.7 |

|

160,000 |

21.1 |

19.2 |

18.1 |

|

280,000 |

34.2 |

31.3 |

29.6 |

-

- Section 4115 leads to a shipbuilding boom and the development of new construction facilities.

Factors that would result in little or no impact of early scrapping as a result of Section 4115 include the following:

- Ship-owners scrap tankers before they reach the regulatory age restriction. The importance of this factor depends on how many tankers successfully complete their fourth and fifth special surveys.

- Major investments are needed to keep older tankers operating beyond their regulatory age limit, and they are expensive to run.

- Ship-owners wishing to extend the life of their tankers beyond the limit defined by Section 4115 find non-IMO trades for them.

- No shipbuilding boom occurs, or if it does occur, enough building capacity exists to keep prices from rising significantly.

- New tankers are much more efficient than old tankers.

- Strict surveys and inspections make it very expensive to operate older tankers.

Table 4-10 shows the break-even cost of special surveys for pre-MARPOL tankers facing their fifth special survey for various losses of capacity due to HBL (using the methods explained in Appendix J). If the special survey is expected to cost more than this break-even amount, the ship-owner will scrap the vessel rather than undergo the special survey. Given the high values of these break-even costs, the ship-owner is likely to pay for the special survey if the market over the next five years is expected to be favorable.

Most large tankers, a shortage of which might cause a shipbuilding boom, do not survive beyond their fifth special survey (i.e., 25 years).12 Consequently, it appears that the poor condition of many tankers, combined with poor market

rates, has had a greater impact on tanker replacement than Section 4115. Section 4115 will have little or no impact on the replacement of large tankers that utilize HBL and are suitable for unloading within U.S. lightering zones or at the deepwater port. If the tanker is in reasonable condition it will pass the fifth special survey, and if future freight rates appear favorable, it will be operated for another five years. The higher the freight rate, the greater is the inducement to extend the tanker's life with HBL.

The situation is different for tankers of less than 120,000 DWT. At least some of these could have passed their fifth special survey and operated economically for another five years with HBL. However, because Section 4115 does not include a life extension for vessels using HBL—in contrast to 13G—these vessels will be effectively banned from U.S. trade13 and will be either forced into early scrapping or restricted to non-U.S. trade.

Findings

Finding 1. The additional construction and operating costs of replacing single-hull tankers by double-hull tankers are expected to total about $30 billion worldwide over a 20-year period. The construction costs of double hulls are expected to run between 9 and 17 percent higher than the construction costs of new single hulls, whereas operating costs are expected to be 5 to 13 percent higher.

Finding 2. Regulations mandating a transition to double-hull vessels are unlikely to result in the withdrawal from service of single-hull vessels in international trade before the end of their economic life, for the following reasons in particular:

- Pre-MARPOL tankers can extend their lives in international trade by up to five years—although not in trade to the United States—without capital investment by using HBL.

- By using the Louisiana Offshore Oil Port (LOOP) or a designated lightering area, single-hull tankers in international trade can continue to operate to the United States until 2015. For economic reasons, only tankers in excess of 150,000 DWT are likely to use this option.

- On the basis of historical trends, many tankers are likely to be scrapped before their statutory retirement dates. However, the historical scrapping pattern reflects an extended period of oversupply and depressed markets; these conditions are likely to change between 2000 and 2005.

Finding 3. The world's shipbuilding capacity has expanded in the past several years and will be sufficient to meet the demand for construction of new double-hull tankers. However, a possible short-term bunching of orders would increase

the construction prices of all new ships and not just tankers. If such a situation were to arise, the economic impacts of Section 4115 and MARPOL would be greater than those estimated in this chapter.

Finding 4. Although sufficient capital is available to finance the replacement of single-hull by double-hull tankers, present market conditions have not stimulated such newbuilding because (1) prevailing freight rates are inadequate to provide the resources needed for new double-hull vessel construction; (2) there is no significant rate premium for double-hull vessels; and (3) a preponderance of spot (short-term) fixtures and a corresponding dearth of time (long-term) charters has made many shipowners less willing to invest in new tonnage. However, tanker ordering is often driven by market sentiment rather than by purely economic factors, and investment in new tankers is intrinsically unpredictable in its timing.

References

Brown, R. Scott, and Ian Savage. 1996. The economics of double-hulled tankers. Maritime Policy and Management 23(2): 171.

Clarkson Research, Ltd. 1995. Tanker Register. London: Clarkson Research.

Clarkson Research, Ltd. 1996a. Shipping Intelligence Weekly July 5.

de Albornoz, Carlos. 1996. The international shipbuilding market. Proceedings of the Society of Naval Architects and Marine Engineers (SNAME) 1996 Ship Production Symposium. San Diego, Calif., February 14, pp. 5-13. New York: SNAME.

Drewry Shipping Consultants. 1994. The International Oil Tanker Market: Supply, Demand and Profitability to 2000. London: Drewry Shipping Consultants.

Drewry Shipping Consultants. 1996. The Shipbuilding Market Analysis and Forecast of World Shipbuilding Demand, 1995-2010. London: Drewry Shipping Consultants .

Energy Information Administration (EIA). 1996. Annual Energy Outlook 1996. Washington, D.C.: U.S. Department of Energy.

Japanese Maritime Research Institute (JAMRI). 1995. Recent Trends of China's Shipping and Shipbuilding. Tokyo: Japan Maritime Research Institute.

Jones, Samuel. 1995. Presentation to the Committee on Oil Pollution Act of 1990 (Section 4115) Implementation Review. Irvine, California, June 12.

Loucas, John. 1995. Presentation to the Committee on Oil Pollution Act of 1990 (Section 4115) Implementation Review. Irvine, California, June 12.

Marine Strategies International (MSI). 1996a. Oil & Tanker Market Update: New Lease on Life. London: Marine Strategies International.

MSI. 1996b. Freight Forecaster. July 1996. London: Marine Strategies International.

National Research Council (NRC). 1991. Tanker Spills: Prevention by Design. Marine Board, Washington, D.C.: National Academy Press.

Navigistics Consulting. 1996. Tanker Supply and Demand Analysis, Task I and Task 2. Study prepared for the Committee on Oil Pollution Act of 1990 (Section 4115) Implementation Review. Washington, D.C., June.

Newbold, John L., and James L. Grubbs. 1995. Presentation to the Committee on Oil Pollution Act of 1990 (Section 4115) Implementation Review. Washington, D.C., October 9.

PIRA Energy Group. 1995. Forecast of Oil Demand. Prepared for the Committee on Oil Pollution Act of 1990 (Section 4115) Implementation Review. New York: PIRA Energy Group.

PIRA Energy Group. 1996. Energy Briefing. Presentation to Mr. Ran Hettena. New York. June 18.

Shawyer, Eric F. 1995. Presentation to the Committee on Oil Pollution Act of 1990 (Section 4115) Implementation Review. Washington, D.C., October 9.

Stopford, Martin. 1996. The Oil Tanker Industry, The Last 25 Years in Review. London: Clarkson Research.

Tamvakis, Michael N. 1995. An investigation into the existence of a two-tier spot freight market for crude oil carriers. Maritime Policies and Management 22(1): 81-90.

Whiteside, Richard. 1996. Presentation to the Committee on Oil Pollution Act of 1990 (Section 4115) Implementation Review. Irvine, California, February 1.

Bibliography

Cambridge Energy Research Associates. 1995. World Oil Trends. Cambridge, Mass.: Cambridge Energy Research Associates.

———. 1995. Refined Products Watch. Cambridge, Mass.: Cambridge Energy Research Associates.

———. 1996. World Oil Trends. Cambridge, Mass.: Cambridge Energy Research Associates.

———. 1996. Refined Products Watch. Cambridge, Mass.: Cambridge Energy Research Associates.

Energy Security Analysis, Inc. 1995. Pacific Basin Stockwatch Market View. Washington, D.C.: Energy Security Analysis, Inc.

———. 1996. Pacific Basin Stockwatch Market View. Washington, D.C.: Energy Security Analysis, Inc.

Japanese Maritime Research Institute. 1992. Trends of the World Shipping and Shipbuilding in 1991 and Prospects for the Same in the Near Future. JAMRI report No. 43. Tokyo: Japan Maritime Research Institute.

———. 1994. Recent Changes in the South Korean Shipbuilding Industry and Its future Prospects. JAMRI Report No. 49. Tokyo: Japan Maritime Research Institute.

Morgan, J.P. 1995. Overview of the financing outlook for the tanker industry. Prepared under the direction of James Hamilton (J.P. Morgan, Inc.) and distributed to the Committee on Oil Pollution Act of 1990 (Section 4115) Implementation Review at third committee meeting, Washington, D.C., October 9.

Stopford, Martin. 1990. The supply, demand, and freight rates in the bulk shipping market. Presented at Shipping 90 Conference. Stamford, Connecticut. March 19.