1

Optics in Information Technology and Telecommunications

The information industry, including the services it provides, is growing rapidly worldwide. Its annual revenue is estimated to exceed $1 trillion, which, at an average revenue of $200,000 per employee, translates into 5 million jobs.

The demand for new information services, including data, Internet, and broadband services, has combined with the supply of innovative information technology to move us rapidly into the information age (Figure 1.1). The information age has recently been called the "tera era" because its technology demands are terabit-per-second information transport, teraoperations-per-second computer processing power, and terabyte information storage (see Box 1.1). Because of the growing importance of image and video information, there is also demand for

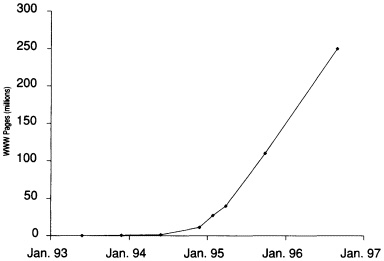

FIGURE 1.1 The growth of the Internet and the World Wide Web is among the factors driving the growth of information technology. Although not all sources agree on the exact statistics of this growth, all agree that it is a spectacular phenomenon. Optics is an important enabler for information technology. (Courtesy of P. Shumate, Bellcore.)

|

BOX 1.1 THE ''TERA ERA" VISION FOR INFORMATION TECHNOLOGY IN 10 TO 15 YEARS

The tera era is a 10- to 15-year vision for the needs of the information age, as articulated by Joel Birnbaum of Hewlett-Packard in October 1996. Projections for switching and details for storage have been added. This vision includes the need for cost-effective networks of virtually unlimited bandwidth. Note that the roadmaps of several key information technologies promise to meet the requirements of this vision: fiber transport capacity, computer processing power, and magnetic storage density are all advancing by a factor of 100 every 10 years. This implies that giga (109) performance will improve to tera (1012) performance within about 15 years. |

strong advances in display technology. Optics and electronics are partnering and complementing each other in meeting this demand for information technology and thus enabling the information age.

There are five major technology segments in which optics plays a major role or has the chance to do so in the future. One of them is information transport over long distances, through large networks under the ocean, across continents, and in the local networks of the telephone and cable television systems. For this, optical fiber transmission is already the technology of choice, with a clear edge in cost and performance over competing technologies such as coaxial cable or satellite communications. Optical processing, including switching and networking, is another segment in which worldwide R&D hopes to open up new markets. A third segment is the storage of information, where technology has to meet rapidly increasing demands for more and more storage capacity. Optical techniques are a strongly growing complement to traditional magnetic storage. A fourth segment is the display of information, for which optics is the intrinsic, unavoidable link between the human eye and the electronics of a television or computer. The fifth important segment is the interface between electronic machinery and information recorded on paper, which includes printers, scanners, and copiers. This segment is not covered in this report since most of its

R&D is conducted in industry, which—for competitive reasons—keeps these subjects quite proprietary; very little work is done in this area in university or government laboratories.

The field of information technology provides many examples of the enabling role of optical technology. Often these enablers are small in size or cost but have an impact on a grand scale in large systems and applications. A tiny semiconductor laser, for example, enables the building of an optical transmitter, which enables a transmission system, which enables the construction of a telecommunications network, which enables the delivery of information age services such as multimedia or the Internet. Another example is the optical fiber, which enables the construction of an optical cable, which enables the construction of a network, and so on. A third example is the liquid crystal, which enables the flat-panel display, without which the laptop computer could not exist. These chains of enablers make it difficult to place firm dollar values on individual component technologies; components such as lasers or fibers are relatively inexpensive, but the service revenues of telecommunications networks are in the hundreds of billions of dollars. Box 1.2 gives a more detailed illustration of the enabling devices for long-haul information transport systems.

As for optics in general, optical materials play an important enabling role. Chapter 6 gives further details of this topic (see Box 6.2, "Photonic Materials").

A few rather obvious but critical points about high-tech mass markets and low-cost manufacturing should be more widely understood and appreciated. They clearly apply to the mass markets for optical information technologies:

|

BOX 1.2 ENABLING PHOTONIC DEVICES FOR PRESENT AND FUTURE LIGHTWAVE LONG-HAUL SYSTEMS Semiconductor lasers

Semiconductor optical amplifiers

Photodetectors and OEIC receivers

Planar integrated waveguide components

Fiber-type components

(Source: T. Li, AT&T Laboratories.) |

-

When a technology creates a mass market, its products become commodity items whose production requires a capability for low-cost manufacturing.

-

Suppliers that have prepared and invested to develop competence and capability in low-cost manufacturing by the time the mass market emerges are likely to gain the largest market share.

-

The revenues generated by a large market share provide a significant source of R&D funds. This fact results in a rapid learning curve for the technology and its manufacturing, which drives costs down further and creates barriers to market entry for other suppliers.

Three established mass markets in optical information technology serve as excellent illustrations of the above points: (1) compact disk (CD)-based optical storage, (2) liquid crystal displays, and (3) cathode-ray tube displays. Each market has global revenues in excess of $20 billion per year, and in each market, offshore manufacturers planned early and were ready with timely low-cost manufacturing. As a result, more than 90% of the manufacturing of these high-tech, mass market products now occurs offshore.

At least four emerging optical information technologies—fiber to the home, optical data links, small and miniature displays, and projection displays—have an excellent chance of creating global mass markets in the not too distant future that are similar in magnitude to the three listed above. We should learn from history and make sure that U.S. industry captures a good share of the emerging mass markets.

The remainder of this chapter summarizes key trends in the four major technology segments described above, including the size of their markets and the technologies they compete with. It also outlines key challenges in this area for science, technology, education, and international competitiveness. The bulk of the chapter is based on the expert presentations and position papers listed in Appendix B.

Information Transport

Optics is now the preferred technology for the transmission of information over long distances. This technology, based on semiconductor junction lasers and optical fibers, is the technology of the information superhighways used to transmit voice, data, and video information. The major market segments include undersea transmission between continents, terrestrial long-distance telephone trunking between states and cities, local telephone exchange links between the central office and the home, and the networks of the cable television companies. Satellite-to-satellite links also offer exciting possibilities. Table 1.1 illustrates typical distance scales for these market segments.

TABLE 1.1 Typical Distance Scales for Selected Information Transport Applications

|

Application |

Distance (km) |

|

Satellite links |

50,000 |

|

Undersea transmission |

1,000-10,000 |

|

Terrestrial long-haul |

20-1,000 |

|

Cable television links |

10-20 |

|

Fiber in the local exchange |

10-20 |

The optical fiber medium offers several advantages over earlier transmission media such as coaxial cables and copper wire pairs. The most significant among these are large transmission capacity (high bandwidth), large repeater spacings, small cable size, low cable weight, and immunity from electromagnetic interference. These advantages have led to large-scale installations of optical fiber all over the world. It is estimated that more than 100 million kilometers of fiber are now installed. Figure 1.2 provides more details on U.S. installations.

Among the grand challenges that face the R&D community in this area are (1) the development of a cost-effective wavelength-division multiplexing technology for transmitting multiple signals on a single fiber, and

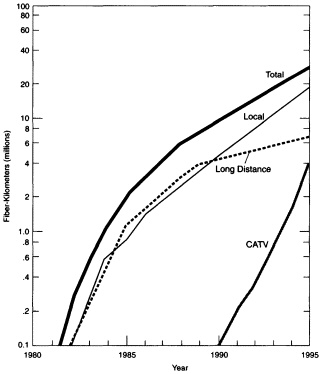

FIGURE 1.2 Nearly 40 million kilometers of fiber have now been installed in the United States, and the number is still growing strongly. As the figure shows, long-haul installations (by both long-distance and local telephone companies) started the trend around 1982. Since 1990, fiber installations by cable television (CATV) companies have grown strongly. It is anticipated that fiber-to-the-curb or fiber-to-the-home installations by local telephone companies will follow. Note that a single fiber cable typically contains 20 to 40 optical fibers. (Courtesy of T Li, AT&T Laboratories.)

(2) the development of a low-cost technology for large-scale deployment of fiber-to-the-home systems that can deliver broadband services.

An issue common to all-optical information transport technologies is the lack of systems education at U.S. universities. They offer excellent programs on the required materials, device, and component aspects of the field, but they seem not to have found a way to integrate into their programs the worldwide trend toward a greater emphasis on software and systems.

Four major application areas of optical information transport are discussed in this section: (1) long-distance transmission, (2) fiber to the home, (3) analog transmission, and (4) optical communications in space.

Long-Distance Transmission

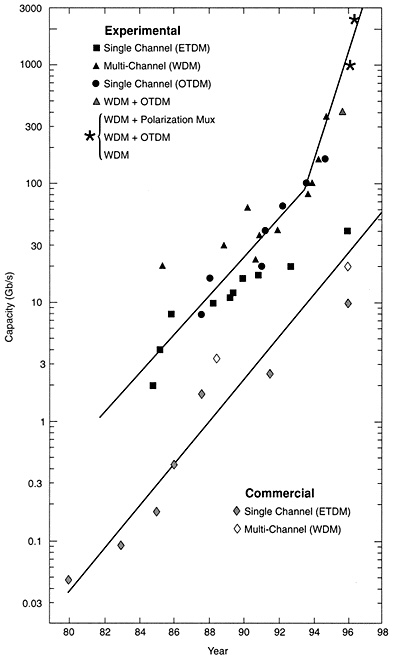

Undersea systems and terrestrial long-haul systems have been early large-scale users of optical technology. Rapid advances in both photonics and electronics are producing a wealth of new technologies that continue to significantly increase the performance of these systems. Recent progress includes the development of optical fiber amplifiers, wavelength-division multiplexing technology, photonic integrated circuits, and video compression. The vast increase in single fiber transmission capacity illustrates the rapid pace of progress and serves as a key technology roadmap for the field (see Figure 1.3). It shows exponential growth, with capacity increasing by a factor of about 100 every 10 years. Transmission at 1 terabit-per-second (Tb/s) in the research laboratory was reported in 1996. Commercial systems appear to parallel the trend of laboratory demonstrations, with a lag of 3 to 7 years.

To appreciate this staggering information capacity, recall that an optical fiber is just a thin strand of glass, about as thick as a hair. Contemplate one of your hairs and note that a terabit is a million megabits. This means that at the recently demonstrated capacity of 1 Tb/s, a hairlike fiber can transmit as many as 40 million data connections (at 28 kilobaud), 20 million conventional digital voice telephony channels, or half a million compressed digital television channels.

Undersea Transmission

Undersea fiber systems have become the major information highways between continents (see Figure 1.4). The first large system of this kind, linking the United States and Europe, was placed in service in 1988, as the successor to the transatlantic telegraph cable, which was installed in 1858, and the transatlantic telephone cable, which began operation in 1956. The old system used coaxial cables and carried information in analog form. It had a capacity of about 40 voice circuits. The new fiber systems use digital technology, which (as in computers and CDs) provides a considerable improvement in quality; at

FIGURE 1.3 A technology roadmap for lightwave systems, showing the transmission per fiber achieved in leading long-distance optical fiber systems over the past 15 years. The graph also indicates the progression of technologies developed for this accomplishment. Note the logarithmic scale for capacity on the vertical axis, which means that the straight trend line implies an exponential growth in fiber capacity. The growth rate is approximately a factor of 100 every 10 years, about the same as the rate of increase in the processing power of computers. Trend lines are shown both for demonstrations of experimental systems in research laboratories and for the first introduction of commercial systems. The time lag between the two is 3 to 7 years. The major multiplexing systems used are marked ETDM, OTDM, and WDM: ETDM systems use only electronic timedivision multiplexing to achieve high capacity by interleaving pulses of a multiplicity of signals; OTDM systems use high-speed optical techniques to accomplish the same interleaving; WDM refers to wavelength-division multiplexing, in which different TDM signals are transmitted by light of different wavelengths. The asterisks mark a set of recent experiments that demonstrate terabit capacity using combinations of the above techniques. (Courtesy of CA. Murray, Lucent Technologies.)

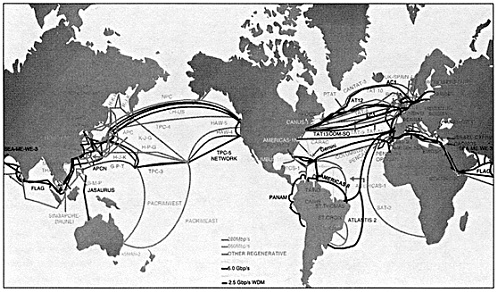

FIGURE 1.4 A map of the current global undersea optical fiber network. By the end of 1996 more than 300,000 km of optical fiber cable were installed in this network. Note that this map was totally empty before 1988, when the first large optical undersea system was deployed. Installations have been given names, such as "Columbus," or acronyms, such as TAT (for TransAtlantic Transmission), TPC (TransPacific Cable), and FLAG (Fiber Link Around the Globe). (Courtesy of P. Runge, Tyco Submarine Systems Laboratories.)

the same time, their information capacity is at least 1,000 times larger. The rapid introduction of optical fiber into global networks is illustrated by the fact that in 1991, just three years after the first optical system was introduced, fiber already carried more international digital information traffic than satellites did.

More than 300,000 km of undersea lightwave cable had been installed by the end of 1996. Typical system lengths are about 6,000 km in the Atlantic and 9,000 km in the Pacific. The rapid pace of progress is reflected in the fact that we can already distinguish three different generations of the technology, as described in Box 1.3.

The dramatic increase of undersea cable capacity, enabled by optical fiber technology, has led to an equally dramatic decrease in the cost of a voice circuit across the oceans. The key reason for this is that the cost of constructing an undersea system, particularly of laying an intercontinental undersea cable, has remained almost the same, even though a single cable now carries at least 1,000 times more voice circuits than it did 40 years ago. An example of this dramatic cost decrease is given in Figure 1.5, which shows the cost of AT&T transatlantic systems and indicates a cost reduction by more than 1,000 times over the 40-year period.

Terrestrial Systems

Optical fiber systems for long-distance transmission on land (also called "trunking") provide the links between metropolitan telephone offices, between cities, and across the continent.

|

BOX 1. 3 THREE GENERATIONS OF UNDERSEA LIGHTWAVE TECHNOLOGY The 1988 first-generation undersea technology uses conventional single-mode fiber operating at a wavelength of 1.3 μm. The system uses optoelectronic regenerators with semiconductor lasers and p-i-n photodetectors both made of InGaAsP. The bit rate of the optical signal stream in each fiber is 280 megabits per second (Mb/s), and the typical regenerator spacing is 70 km. A second generation of technology was used in the 1991 installations. It too employs conventional fibers, but with the operating wavelength moved to 1.55 μm to benefit from lower fiber losses. Single-frequency distributed-feedback lasers are used in optoelectronic regenerators, together with avalanche photodetectors. The bit rate per fiber is doubled to 560 Mb/s, and the typical repeater spacing is 150 km. The third-generation technology was prepared for installation in 1995. It uses optical repeaters with optical amplifiers. The systems operate at 1.55 μm and use dispersion-shifted fiber to provide near-zero dispersion in the operating range. The design bit rate per fiber is 5 gigabits per second (Gb/s).

The above table shows the information-carrying capacity of these three lightwave systems (FIBER 1-3) along with that of the preceding four generations of coaxial systems (COAX 1-4). Note that the data shown are for cable capacity without voice processing. Current undersea systems use digital voice processing to take advantage of silent periods in speech. This increases effective capacity by another factor of 5, enabling the third-generation lightwave system to carry more than 500,000 voice channels. |

Early metropolitan applications, such as those in the San Francisco Bay area, highlighted optical transmission's advantages. The Bay Area system, introduced in 1980, provided digital transmission at 45 megabits per second (Mb/s) with a repeater spacing of 7 km. This spacing was already sufficient to allow links between telephone offices to be direct, with no need for electronics outside the buildings. The ptical system also helped to save space in metropolitan cable ducts since a single fiber replaced the earlier T1 carrier's 28 pairs of copper wires, with a capacity of 1.5 Mb/s per pair.

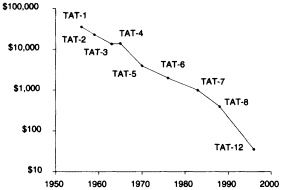

FIGURE 1.5 The falling cost per circuit of transatlantic telephone (TAT) systems. (Note the logarithmic vertical scale.)

The first major lightwave installation in the United States was the Northeast Corridor system, which linked Washington with New York in 1983 and New York with Boston in 1984, a total length of 747 miles. Its technology carried 90 Mb/s per fiber, the equivalent of 1,344 digital voice channels. This system confirmed the inherently higher quality of digital technology, but it also brought out another point: the excellent technical and economic synergy between the digital lightwave system and the digital telephone switches along the route. No analog-to-digital conversion was needed to interconnect the fiber system to the 23 existing digital electronic switching systems along the route, which resulted in considerable cost savings.

The Northeast Corridor was soon followed by more large-scale fiber installations, using rapidly advancing technology. More than 100 million kilometers of fiber had been installed around the world by the end of 1996, about one-third of the total being in the United States (see Figure 3.2).

Terrestrial fiber systems, like undersea systems, have evolved through several technology generations. (See Figure 1.3 for more detail on this rapid progress.) Advanced systems now employ optical amplifiers and wavelength-division multiplexing (WDM). WDM is a multiwavelength technique that increases the number of digital information channels that can be sent over a fiber simultaneously by transmitting each channel on its own distinct optical wavelength, as described in the section "Optical Networking and Switching" below. Terrestrial long-haul networks will benefit significantly from amplified multiwavelength transmission systems designed to access the large inherent bandwidth in the installed fiber. Capacity will increase by a factor of 10 to 50, not only providing for ample and graceful growth, but also allowing flexibility in network architecture design and in the management of network restoration in case of a failure (e.g., a cable cut). The new networking flexibility will be exploited to enable novel routing of traffic. WDM system experiments involving more than 100 channels already have demonstrated ultrahigh-capacity transmission over long distances, and large-scale experimental projects are under way to explore the potential of WDM technology for high-capacity networking. Amplified 16-channel WDM systems at 2.5 gigabits per second (Gb/s) per channel

TABLE 1.2 Estimated Global Markets for Long-Distance and Interoffice Lightwave Systems (U.S. dollars)

|

|

1995 |

1996 |

|

|

Undersea |

|

$2 billion |

$2.5 billion |

|

|

· Cable and deployment: ~70% |

|

|

|

|

· Lightwave equipment: ~30% |

|

|

|

Terrestrial |

|

$2 billion |

$4 billion |

|

|

· SONET (OC-48) and SDH (STM-16) |

|

|

|

|

· Transmission equipment only |

|

|

|

|

· Lightwave: ~20% |

|

|

|

|

· Electronics: ~80% |

|

|

|

NOTE: SONET = Synchronous Optical Network, SDH = Synchronous Digital Hierarchy. (Source: T. Li, AT&T Laboratories.) |

|||

have been developed and are being manufactured for massive deployment in the embedded terrestrial network. These revolutionary system solutions will meet the demand of envisioned broadband services for many years to come and thus make lightwave communications the principal component of the global information services infrastructure.

Table 1.2 gives estimates of the global markets for undersea and terrestrial lightwave systems. There are strong systems vendors in Europe, Japan, and North America. Because of the early large-scale deployment of WDM systems in the United States, North American vendors have gained an early market lead in WDM systems.

Fiber to the Home

Although most experts agree that in the future, fiber will be installed all the way from the telephone company central office to the home, opinions vary widely as to when this will happen. Developments in the United States and elsewhere are beginning to suggest that it may happen sooner than commonly thought.

The technical benefits of fiber to the home (FTTH) include its well-known capacity for transmitting incredibly high bandwidths at relatively negligible losses. This "future-proofs" the resulting network against demands for rising bandwidths, which history shows will indeed be necessary. Since fiber lasts 30 years or more, labor-intensive installation of cable and passive components has to be done only once because no electronics are installed in the outside plant between office and home. Upgrades take place on the premises of the service provider and the customer. Nearer-term benefits of fiber include its small size and weight compared with metallic cable, especially coaxial cable; its total immunity to both inward and outward leakage of electromagnetic

interference; and its resistance to corrosion. Systems with active components at only the ends of the network ensure high reliability. As important and practical as these advantages are, more practical benefits may help drive fiber to the home now. These include solving the high costs of drop-cable maintenance and electrical powering.

The advantages of completely replacing metallic telephone and cable television cables with fiber were recognized in the 1970s. Numerous trials in Japan, Europe, Canada, and the United States, in both the telephone and the cable television industries, established the technical feasibility, but the costs for either replacement or new construction were prohibitive. To move ahead with fiber, the telephone and cable industries refocused on less expensive fiber-to-the-curb and hybrid fiber-coax solutions, both of which realize many of fiber's advantages while sharing costs among many customers. However, these systems still complete the final connection to the customer with metallic cables (see Figure 1.6), which requires the supply of power in the outside plant on the way from the telephone office to the home.

Recent advances in key FTTH technologies have driven costs down and removed technical barriers. These advances include low-cost lasers, solutions for delivering video, and network topologies that share costs. Equally important, there are a growing number of bandwidth-thirsty services that make the high-bandwidth capability of FTTH more compelling. These include high-speed Internet access, telecommuting, home offices, and high customer satisfaction with digital video; an all-fiber network can satisfy these needs simultaneously. Perhaps most important, there is now a much clearer understanding of the cost savings that result from bringing fiber to the home. The time appears right for seriously reconsidering FTTH, at least for operators whose initial focus is on providing telecommunications services.

The most recent and perhaps most significant steps toward reducing FTTH costs are in the areas of lasers and laser packaging. New strained-layer, multi-quantum-well lasers have been developed recently that operate reliably at high-power levels throughout the required wide range of temperatures (-40°C to +85°C). Some of the most recent structures also integrate a beam expander to simplify coupling to the output fiber and laser packaging.

Electrical powering has always been a major issue and has often been referred to as the Achilles' heel of FTTH. In the United States, telephone service is nearly always available during power outages, and the public expects uninterrupted ''lifeline" service. Since fiber does not conduct electrical current as copper wires do, lifeline service has been an issue for all fiber-based networks. The challenge is to provide inexpensive, high-reliability power from the customer's premises. (Wireless technologies have the same requirement.)

Most of the recent progress in FTTH has been achieved in Japan and Europe. Manufacturers have developed equipment for NTT in Japan and for trials in England, Belgium, Germany, and Denmark. A promising development is a recent international initiative among ten network operators, including two from the United States, to define complete specifications for "full-service" access networks, including FTTH, all

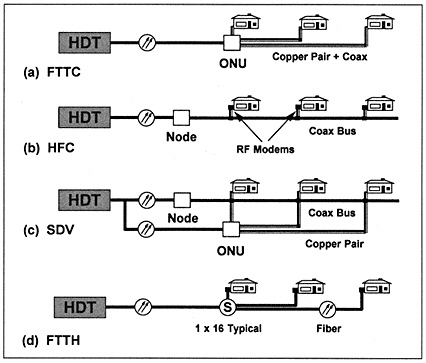

FIGURE 1.6 Four leading architectures for broadband information transport to the home from the telephone central office or a remote host digital terminal (HDT). A typical central office serves about 10,000 homes. Typical distances are 10 km from the HDT to the node or the optical network unit (ONU) and less than 1 km from these to the home. Fibers are marked by the symbol ![]() .

.

-

In the fiber-to-the-curb (FTTC) architecture, the fiber is terminated at an ONU on a street curb in a neighborhood or at a large building, and transmission continues via copper wire or coaxial cable. This technology has been used for the large-scale OPAL installation in Germany.

-

The hybrid fiber-coax (HFC) architecture uses coaxial cable from the node to the home. It carries broadcast analog television channels, as well as digital telephony and data channels, and is very similar to the technology used by the cable television industry.

-

The switched digital video (SDV) architecture is a combination of (a) and (b) that carries digital and analog services separately. It links to very few (4 to 24) homes per ONU, which allows the provision of switched digital video services.

-

The fiber-to-the-home (FTTH) architecture uses a passive optical splitter (marked

to share the long stretch of fiber from the telephone office to the neighborhood among 16 to 32 homes, which reduces the cost per home. Note that FTTH is the only one of these four technologies that requires no power supply in the outside plant between the telephone office and the home. (Courtesy of P. Shumate, Bellcore.)

to share the long stretch of fiber from the telephone office to the neighborhood among 16 to 32 homes, which reduces the cost per home. Note that FTTH is the only one of these four technologies that requires no power supply in the outside plant between the telephone office and the home. (Courtesy of P. Shumate, Bellcore.)

of which can easily evolve to FTTH. Their efforts should result in new FTTH products becoming available in 1998. Cost is still cited as the major barrier to wider early deployment, but recent analyses show that in rural areas and for some high-end suburban cable television situations, FTTH can meet first-cost objectives now. Imaginatively reducing costs even further, however, is a major challenge for the optical R&D community, in both industry and academia.

The rapid emergence of broadband telecommunications networks and broadband information services will have an enormously stimulating impact on commerce, industry, and defense worldwide. Congress should challenge industry and its regulatory agencies to ensure the rapid development and deployment of a cost-effective broadband fiber-to-the-home information infrastructure. Only by beginning this task now can the United States position itself to be the world leader in both the broadband technology itself and its use in the service of society.

Analog Lightwave Transmission

The lightwave systems discussed above are digital systems, in which information is transmitted as pulses of light. In the analog systems that are the subject of this section, a waveform such as a radar signal or an analog television signal is modulated directly onto a laser beam. This avoids costly digital-to-analog conversion at the receiver but generally limits the transmission distance to about 20 km.

Cable Television

By far the most widespread application of analog lightwave systems has been in the cable television industry. Analog lightwave systems in cable television architectures link the cable headend office to a fiber node, where a receiver extracts the radio frequency (RF) signal and transmits it to between 500 and 2,000 households using a tree-and-branch coaxial cable plant [see Figure 1.6(b)]. Fiber's success in the cable television industry arises from the fact that a single analog lightwave system with only two active components—a transmitter and a receiver—can replace a trunk coaxial cable with 12 to 30 active trunk amplifiers while providing better end-of-line performance. Virtually absent in the early 1980s, fiber now exists in more than 25% of cable systems, and fiber deployment by cable television operators accounted for 34% of all fiber deployed in North America in 1994.

A cable television signal consists of 40 to 80 analog video channels, each of which requires a 45-decibel (dB) signal-to-noise ratio at the subscriber's television set. Because of the subsequent coaxial cable plant, the signal-to-noise ratio of the lightwave system must be even higher than this 45 dB, so the linearity and noise requirements on the enabling lightwave components are very demanding. The first successful

lightwave transmitter of multiple video channels was a directly modulated 1300-nm semiconductor distributed feedback (DFB) laser. This technology, introduced in the late 1980s, remains a workhorse of the cable television industry, and advances in DFB lasers have increased both the average output power and the allowable channel load (from 40 to 100 channels). Additional enabling technologies now under development, aimed at further performance improvements, include 1550-nm DFB lasers, external modulators, and optical amplifiers.

The market for analog lightwave systems for cable television-like signals is expected to remain strong. Cable television operators, feeling the threat of competition from wireless cable and direct broadcast satellite (DBS) systems, are looking to upgrade their plants to improve both the quantity and the quality of their services. This typically means more fiber-rich architectures, in which each fiber node serves fewer homes. As cable television operators look to enter the telephony and data network market, they are installing fiber ring architectures that improve the reliability of their networks. The arrival of digital television channels, such as those used by the DBS providers, breathes added life into the analog lightwave industry. These digital channels are coded onto sub-carrier frequencies, which casts them into a format readily carried by an analog lightwave system.

Remote Antennas

The second most common application of analog lightwave systems is in links to remote antennas. The signals carried are for mobile radio, such as cellular telephones or personal communication services (PCS), or for microwave or millimeter-wave applications.

Mobile radio is the largest potential market for antenna remoting. The explosive growth of the cellular telephone market has led to a need for more frequency reuse of the radio spectrum. As cells shrink to microcells, the economic case weakens for putting a complete base station at each antenna, requiring analog lightwave backhaul from multiple mobile radio antennas. Mobile radio signals are higher frequency than cable television signals (900 MHz for cellular and 2 GHz for the new U.S. PCS licenses) and occupy less bandwidth, but they require very high dynamic range because of the "near-far" problem. In other words, the signal-to-noise ratio must be maintained for all mobile users, whether near the antenna or far from it, even though the RF power received by the antenna depends significantly on the distance to the user. Required breakthrough technology includes much cheaper laser transmitters and more compact (perhaps integrated) laser-modulator packages.

In the future, analog lightwave links may be used for antenna remoting of stationary microwave or millimeter-wave radio systems.

At microwave frequencies, direct modulation of semiconductor lasers or modulators is possible. At millimeter-wave frequencies (30 to 100 GHz), more sophisticated techniques are needed. In some respects, optical fiber is the only medium that can transport millimeter waves over any appreciable distance, because the attenuation of free space for millimeter waves is very large compared with the attenuation of fiber.

Competing technologies for antenna remoting include signal processing at the remote antenna so that a digital link can be used, line-of-sight microwave links, and coaxial cable. The choice will be based on both performance and economics.

Optical Space Communications

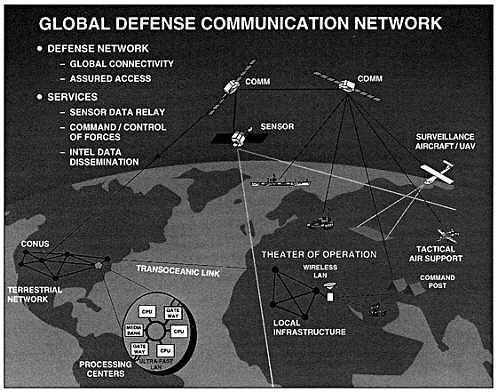

In the past decade, satellite communications have developed into a booming commercial market, global in nature but dominated by the United States. Currently valued at about $15 billion per year, this market is expected to grow to at least $30 billion per year in the next decade, or even more if mobile satellite communication services are deployed successfully. Fixed satellite services are relatively mature; their projected growth is a modest 10% per year. Direct broadcast satellites will see more rapid growth of at least 50% per year. Governments have long used satellites for a variety of communications missions (Figure 1.7), and the Department of Defense (DOD), National Aeronautics and Space Administration (NASA), and other government agencies will continue to launch and maintain dedicated satellite links, but they are expected to use commercial links more and more to save costs.

Most current satellite communications systems use simple, single-satellite relays between ground terminals. If it is necessary to span a longer distance, two relays may operate in series through a relay ground station. An alternative—direct cross-links between satellites—eliminates a relay ground station. Though not now commonly employed, this approach could be important in future satellite networks, especially for mobile communications. In addition, the utilization efficiencies of sensor satellites in low Earth orbit can be improved significantly by the use of a readout cross-link to a relay satellite in high Earth orbit. The capacity of the French SPOT-4 satellite, for example, will increase six-fold with its planned optical readout link to the geosynchronous relay satellite ARTEMIS. Furthermore, reading out low-Earth-orbit Earth resources satellites such as LANDSAT via cross-links to high-Earth-orbit relay satellites can increase sensor coverage, improve access times, and eliminate expensive global tracking networks.

Cross-links have already been operated, such as NASA's data relay satellite TDRSS (Tracking and Data Relay Satellite System), but their use is not routine. The networking choice and the particular cross-link hardware have to meet stringent cost-risk requirements for a new system design.

FIGURE 1.7 A schematic sketch of the global defense communication network. An essential element is the network in the sky consisting of interlinked communication satellites and sensor satellites. Extensive satellite networks are also planned for commercial mobile telephone and data service applications. The text discusses the capacity advantage of optical cross-links between the satellites of the network. (Courtesy of V Chan, MIT Lincoln Laboratory.)

Intersatellite cross-links can be either optical or radio frequency. The shorter wavelength of optical systems allows modest telescope sizes and transmission at a high data rate. Significant weight, power, and size advantages are realized over RF systems of similar performance, especially at very high data rates. However, optical space communications is still an emerging technology, with a checkered history. Many tough technical issues are yet to be resolved, and their solutions must be demonstrated before the technology is mature enough for deployment. Among these critical technology and system issues are transmitter and receiver technology; spatial acquisition and tracking of very narrow beams; optical-mechanical-thermal engineering of high-precision optical systems for space use; and a good understanding of system architectures and techniques for design, fabrication, integration, quality assurance, and risk mitigation. These are mainly engineering issues.

The United States has a history of major disappointments in this field. More than $1 billion has been spent, without yet producing a working optical link in space. The failed attempts can be traced to unsuccessful technology development, poor understanding of system

engineering, lack of satellite payload integration experience, and lack of creativity of the technical teams assigned to the programs. The know-how needed to successfully deploy optical communications in space does exist in U.S. universities and federally funded laboratories, but an effective mechanism must be devised to transfer the technology to the U.S. aerospace industry. Specifically, U.S. satellite communications companies, although they collectively possess many of the critical technical ingredients, seem unwilling to make the major investment necessary to aggressively pursue the development of an optical cross-link payload comparable in quality and lifetime with RF links. Most U.S. companies are studying optical links, but their strategies stress RF.

As technology advances, optical cross-links look more attractive, but detailed analyses of costs, benefits, and risks require the development of actual space-qualified optical communications payloads that are competitive with RF cross-links. As the Federal Communications Commission encourages the construction of global satellite networks, the requirement for several cross-link terminals per satellite, which is difficult for large RF antennae, is expected to become a strong motivation for optical cross-links. So far, however, neither industry nor government has made the financial commitment necessary to fund such an effort in the United States. As a result, if the market develops, the United States is likely to enter it late.

European and Japanese companies are not as reluctant as U.S. companies to proceed with a commercial payload. In Europe and Japan, government and industry have joined forces in long-term R&D in this area for the past 6 to 7 years. Notably, the European Space Agency's Semiconductor Intersatellite Laser Experiment (SILEX) represents a payload investment of approximately $250 million, to be launched soon. Japan is planning to launch the Optical Intersatellite Communication Engineering Test Satellite (OICETS) to link with Europe's ARTEMIS in 1998 and later with Japan's own geosynchronous relay COMET. The commercial low-Earth-orbit satellite constellations for mobile phone and small-terminal data services will be a lucrative outlet for such technology.

Information Processing

Of the four major application areas discussed in this chapter-optical transmission, storage, display, and processing of information-the first three have succeeded in large commercial markets. In these applications, light performs functions that cannot be done by electronics. By contrast, for most applications in information processing, electronic technology is excellent and sets a high standard of performance. Thus,

the use of optics in information processing remains a research topic, still seeking a clear competitive advantage.

In this report, the definition of optical information processing is taken to include the use of optics in data links, telecommunications switching, both analog and digital computing, and image processing. In essentially all of these applications, silicon-based electronics is presently the technology of choice. However, as cheaper and more practical optical and optoelectronic devices become available that can be used in suitable systems, optics will play an increasingly important role. This section describes optical information processing technologies from the most advanced to the most speculative.

Optical Data Links

Optical fibers are an excellent transmission medium and, as seen in the first section of this chapter, they reign undisputed in long-distance transmission links. At short distances, in local area networks (LANs) that link computer workstations around a campus or from desk to desk within a building, the opportunities for optics are growing rapidly, as costs come down and bandwidth needs continue to grow. Optical data links will be important, however, only as they become sufficiently inexpensive to compete with electronics, particularly in low-end applications such as connecting desktop computers. Optical data links also require extraordinary reliability, since they transmit computer data and images.

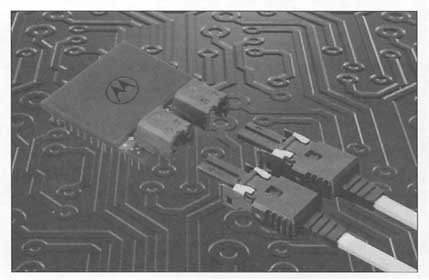

In many datacom applications, the cost per channel is reduced by using a high degree of parallelism, that is, by using arrays of lasers and detectors, connected by fiber ribbons (see Figure 1.8 and Table 1.3). Parallel optical links not only lower costs, but also reduce cable congestion, board area, and bandwidth demands on sources, detectors,

FIGURE 1.8 Motorola's Optobus system. Motorola's optical data link package contains a 10-fiber ribbon up to 100 m long, driven by arrays of lasers and detectors. The lasers are short-wavelength vertical cavity surface emitting, connected to an optical interface unit, which is a molded waveguide with direct chip attached to the optoelectronic array and to the fiber ribbon. Other parallel optical data links have been developed by HewlettPackard and Hitachi, among others. By 2005, typical prices are projected to drop to $10$15 per duplex channel at 622 Mb/s. (Courtesy of R. Nelson, Motorola.)

TABLE 1. 3 Features of Some Selected Optical Communication Application Segments

|

Target |

Distance |

Data Rate |

Modem Cost Target |

|

Telecom |

|||

|

Long-distance |

5-100 km |

0.6-2.5 Gb/s |

$10,000 |

|

Short distance |

1-10 km |

50-622 Mb/s |

1,000 |

|

Datacom |

|||

|

high-performance |

|

|

|

|

Campus |

300-2,000 m |

200-1,000 Mb/s |

100 |

|

Interbuilding |

|

|

|

|

Telecom switches |

|

|

|

|

Low cost |

|

|

|

|

Desktop |

< 100m |

< 200 Mb/s |

10 |

|

Backbone |

100-500 m |

< 200 Mb/s |

|

|

(Source: R. Nelson, Motorola.) |

|||

electronics, and fiber. They also allow many alignments in one assembly operation and eliminate the high cost of electronic multiplexing. The result is a lower packaging cost per channel and the elimination of delays caused by electronic signal processing.

In computer applications, data links are present in the local area network that connects workstations within the computing cluster, as well as to and from file servers, data communication adapters (telecom and satellite), display and printer adapters, and data storage systems. Optical data links have shown modest market penetration, with copper wiring usually being cheaper at present. Success in penetrating the market will require leverage of the enabling optical technologies. The technology driver is primarily cost; obstacles to progress include the costs of connectors and cables, packaging, and installation and alignment. Improved molding or plastic packaging as well as modeling and simulation tools for high-frequency, low-cost packages are needed.

Figure 1.9 indicates the large future markets for optical data links, as found by several market studies. The United States is in a strong position to capitalize on these markets. Companies will invest in the necessary R&D, but industry needs good standards and improved manufacturing. University research can help by working on advanced devices and low-cost fiber technologies.

The United States is competitive in high-performance datacom, but cost reductions are needed. In low-performance datacom, the United States is strong. The challenge is to enable research in the new R&D environment, in which low-cost, high-volume global markets mean low marginal profits.

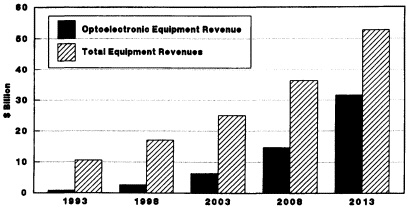

FIGURE 1.9 The Optoelectronics Industry Development Association (OIDA) predicts $25 billion in total data communications equipment revenues by 2003, of which $7 billion will be in optoelectronics. The total market should double by 2013, of which $30 billion will be optoelectronics. OIDA has produced a detailed roadmap that lays out those technologies that will be inserted in the marketplace for specific applications. Restricting the consideration to the worldwide market in parallel optical links, ElectroniCast predicted in July 1995 that the market will be $1 billion by 2000 and $3.3 billion by 2005, roughly half in computers and half in telecommunications, with 10% military.

(Courtesy of OIDA.)

Optical Networking and Switching

High-bandwidth optical telecommunication systems are digital and transmit many simultaneous telephone calls or data channels with their digits interleaved in a process called multiplexing. Today's systems perform this multiplexing electronically, beginning at the local exchanges and increasing the bandwidth and number of simultaneous channels as the signals approach the long-distance nodes (of which AT&T, for example, has 250 around the country). Commercial telecommunication systems currently do all their routing electronically. At switching nodes, receivers convert optical signals from the fibers into electrical signals, which are switched and routed to the appropriate output fiber so that each phone call gets where it is intended.

In an all-optical network, light signals would remain light signals throughout, and the switching would be optical. The architecture of the system determines the approach and specifies both the hardware and the software used for multiplexing and switching. The key technological task is to identify the capabilities of optics that enable it to play crucial roles in the assembly, management, and distribution of large numbers of signals that do not all start and end at the same two distinct points.

Switching

With the reduction in the cost of information transmission, switching is becoming an ever larger fraction of communications costs (see Figure 1.10). Switching is therefore both a large challenge and a large market; today, just one fiber can saturate the switching capability of the largest switch ever made. Since transmission cost is falling exponentially, the primary system cost will be in switching and networking, unless network architectures change to use longer spans of fiber between switches.

The current practice is electronic switching, in which a transceiver detects optical signals and electronic logic sends them where they

belong, conditions them, retimes them, and then modulates a laser that transmits them down the appropriate fiber. Electronic switches use logic functions to route the signal spatially from one channel to another. This is in contrast to switches that physically change the routing, such as the patch cords used by the first telephone operators.

The WDM systems (see Box 1.4) currently under development are all optical. They take advantage of the fact that the transmitted information is in the form of light, physically routing it via optical cross-connects. This keeps signals optical throughout switching and routing, and it avoids expensive optical-electronic conversions. In essence, it provides ''transparent pipes" that enable transmission of any bit rate, any packet length, any transport format, and any modulation format including SONET (Synchronous Optical Network) and ATM (asynchronous transfer mode).

Another approach is to replace only selected electronic components with optical ones, where the optical components have a distinct advantage. For example, taking advantage of the interconnection ability of optics can enable very high-capacity switching machines, such as might be needed for terabit-per-second ATM switches. Such devices have commonality with the advanced optical technologies developed for image processing (see below). Their use of optics solves most of the physical problems inherent in high-density electrical interconnections: Optics has no frequency-dependent loss or cross talk and is intrinsically a very high-bandwidth medium; there is no distance-dependent loss or degradation; and photons allow for electrical isolation and immunity to electromagnetic interference. Meanwhile, the logic in such systems remains electronic, where it is most efficient.

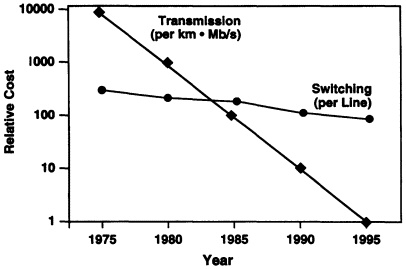

FIGURE 1.10 Transmission costs per bit have seen dramatic reduction, driven in large part by the ever-improving optical fiber transmission technology. Switching technology has not kept pace; the information sent on one fiber is more than enough to saturate the largest telecommunications switch in existence. Switching cost is likely to be an increasing fraction of the cost of telecommunications. This shows up in telephone calls costing the same whether the destination is in the same state or across the country. (Courtesy of P.E. White, Bellcore.)

|

BOX 1.4 MULTIPLEXING: SPACE, TIME, WAVELENGTH Multiplexing, or placing many simultaneous calls on a single line, may occur by dividing up the signals in time, space, or wavelength. When signals are multiplexed, they can travel either through fixed circuits or in separately addressed packets. The system architecture determines when and how much the signals in different channels are multiplexed. In time-division multiplexing, pulses corresponding to bits from different signals are placed in different time slots. The format that has become standard in long-distance telephone systems is called SONET. SONET consists of digital frames that are sent at a bit rate of 155 MHz and each contain an address that sends them in the proper direction. In space-division multiplexing, different signals travel on different fibers. Each fiber can be routed in a different direction, connected to the various nodes of the system. This approach reduces the need for switching. Wavelength-division multiplexing (WDM) is the newest approach. In WDM, each channel is transmitted in a slightly different color of light. Color-sensitive switches or receivers determine the routing and which call is received at which station. For mixed-format multimedia signals, in the time-division-multiplexed mode a new standard is being developed, called the asynchronous transfer mode. In ATM, short packets of data (typically 53 bytes) are used for all kinds of traffic, including voice, video, data, and multimedia. Each packet has a header that carries the address, and each packet is transmitted independently of every other one. ATM requires high-speed switches with fine granularity that can switch rather small packets automatically. |

WDM Networks

In a WDM network, the use of many wavelengths permits huge network capacity, and the technology is scalable, modular, evolvable, and reconfigurable. WDM is economically viable because successful optical fiber amplifiers have been developed that can simultaneously amplify a large number of channels of different wavelengths without cross talk or interference with one another.

To build up a reconfigurable WDM network, wavelength-dependent cross-connects are needed. The ideal cross-connect would allow any wavelength on any input fiber to be connected to any wavelength on any output fiber. This requires wavelength converters, a technology that has not yet proven feasible for commercial exploitation, but cross-connects without wavelength conversion could be sufficient for a significant segment of the market.

Box 1.5 provides some background information on the considerable number of R&D projects on WDM networking now under way worldwide. These projects are providing a growing consensus: Point-to-point WDM is happening now at 8, 16, and perhaps 32 wavelengths, separated by 200, 100, or 50 GHz each, respectively. Applications are in long-distance transmission and in exhausted regional routes. WDM

sources, wavelength-selective switches, and WDM amplifiers have all proven feasible. Layered WDM network architectures provide graceful evolution with increasing demand. If commercial feasibility is to be evaluated realistically, network management and control systems have to be included in these study projects.

The enabling technologies for all-optical networks are optical amplifiers, waveguide switches, pump lasers, and fiber. The emerging technologies are WDM passive components, wavelength add-drop components, multiple-wavelength lasers, photonic integrated circuits, and cross-connects. Technologies that are not here yet and are speculative include low-cost, single-mode waveguide device packaging and wavelength converters. Finally, mode-locked ultrafast laser sources may push WDM capabilities even farther than in present systems studies.

European researchers have made tremendous progress with RACE (Research Advanced Communications, Europe) and ACTS (Advanced Communications Technologies and Services) and are well coordinated,

|

BOX 1. 5 WORLDWIDE PROGRAMS ON WDM NETWORKING There are several major optical networking programs under way worldwide. An early WDM networking demonstration was by British Telecom in 1991, which ringed London with five nodes connecting 89 km route lengths at 622 Mb/s, using erbium-doped fiber amplifiers and WDM routing. RACE (Research Advanced Communications, Europe) had a joint research project among eight companies and two universities that developed a Multi-wavelength Transport Network. The demonstration in Stockholm in 1994-1995 investigated optical network layering, transparency, evolutionary paths, standards, and economic modeling. The program following this in Europe is ACTS (Advanced Communications Technologies and Services). Its first project is to develop METON (Metropolitan Optical Network), designed with an ATM optical transport layer to be cost-effective in a metro area net and a local access network. It uses optical cross-connects and optical add-drop, using fiber grating, silica-on-silicon, InP, and optoelectronic integrated circuits. The ACTS program has several projects under way similar to METON, utilizing collaboration among industry, government, and universities from a number of countries in Europe. This project includes all major European industrial interests, all major telecom network operators, leading broadcasters and cable television operators, and key European equipment manufacturers. It is the largest set of linked trials and demonstrations of new telecommunications services in the world. It will provide a trans-European Information Infrastructure, with fiber, cables, radio, and satellite links. There will be up to 10,000 businesses and 1 million individual participants in service trials. The Photonic Transport Network Project under way at NTT in Japan is also aimed at a WDM network demonstrator. In the United States, the Defense Advanced Research Projects Agency has funded several projects on WDM networking: |

with a hard push toward commercialization and local access application. The Japanese program is in its early phases but has a highly developed WDM technology base and rapid progress is expected. In China, university laboratories are in unusually close contact with industry, which increases their access to technical and business ideas and helps to guide university research. The U.S. programs are roughly comparable in scope and quality to European and Japanese programs. WDM standards are being pushed hard in Europe and are needed for commercial progress.

High-Density Optical Switching

Physical cross-connects can route entire optical channels transparently, independent of the bit rate or the transmission format. They need not switch at the bit rate (i.e., reroute the signal at each signal pulse), but since the control (electrical) and signal (optical) are not in the same form, such switches cannot control the network or retime,

|

buffer, or regenerate the signal. Logical digital switches are typically better able to handle sophisticated control functions and can perform buffering, regeneration, and retiming of signals. In the logical switch, the control and signal do have the same form, but this switch must run at the bit rate and is not transparent to upgrades in capacity or format. Nonetheless, the change to sophisticated transmission formats that can carry mixed traffic types and to packetized traffic such as ATM requires even more logical complexity in the switching systems, making logical switching increasingly necessary. ATM switching will require switches at nodes that can handle terabits per second of information. The largest ATM switches commercially available today have a throughput of about 20 Gb/s.

High-density optical interconnects allow the electronics to do the logic and the optics to do the interconnect function (see Figure 1.11 for more details). Considerable research progress has been made in two-dimensional array interconnects and the associated smart pixel technology. These technologies appear capable of tracking the growth in switching capacity of large switches over the next 15 years, and they may be crucial in making possible such large logical switching machines. These technologies may also become important in high-performance computing.

Note that the size of the digital switching market makes it a significant challenge for optics to contribute to the technology. In 1995 the U.S. market for conventional central office switching equipment was $6.3 billion; worldwide, it was $24 billion and growing at 6% per year. This total does not include the markets for ATM, digital, cross-connects, and other broadband switching, some of which are growing much faster (20% to 60% per year) although still relatively small. It is too early to project photonics markets in switching since technology insertion is not fully in place.

Current results are encouraging, but to achieve optical interconnect insertion into logical switches, continued R&D is necessary on high-yield integration of optoelectronic and electronic devices and in general on the merger of optoelectronics and electronics technologies. All forms of photonic switching require continued development of devices and packaging to reduce costs and establish reliability.

All-Optical Switching

Will there be an architecture that relies on all-optical switching? It will be difficult to compete with silicon-based electronic logic. Electronic technology, including packaging, is mature and inexpensive. Issues that cause difficulties for all-optical switching systems are synchronization and clock recovery, buffering and memory, and logic. In addition, ultrafast optical switching devices require too much power,

are too simple logically, and are not yet practical for large-scale use. Although some research systems at universities have demonstrated all-optical switching, a number of issues must be resolved before they can become practical. The future of ultrafast optical switching is not yet clear, and more research is needed. Because devices and concepts are in an early stage of development, there are still major opportunities for invention and innovation in optical devices and materials. Nonlinear materials, fibers, and switches are excellent topics for university research. In the future, telecommunication systems may experience a graceful transition to all-optical switching as more and more of the electronics functions are taken over by optics.

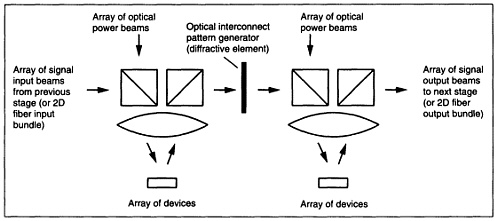

FIGURE 1.11 High-density optical interconnects that link electronic logic arrays solve a number of problems of very large digital switches. At the chip level, using optics provides protection from electrostatic discharge on the inputs and from simultaneous switching noise, reduces the area of off-chip drivers and pads, and reduces the power dissipation of off-chip line drivers. Chip-to-board interconnects use optics to overcome pin inductance on chips and chip carriers, the limited number of pins, and the use of a large number of power and ground pins because of off-chip driver current requirements. On-board and board-to-backplane interconnects use optics to overcome the limited number of pins on board connectors, connector inductance, impedance matching, wave reflections, line termination, electrical isolation, cross talk between lines, and bandwidth limits of lines. These optically interconnected systems require integrated receivers, receiver arrays, and smart pixels.

The existing technologies for high-density optical interconnects are in the form of optical data links, with multimode vertical cavity surface emitting lasers (VCSELs) or arrays. Technology for two-dimensional (2D) arrays is emerging: smart pixels, modulators, VCSELs, dense integration of modulators and detectors with silicon electronics, array optomechanics, and laser power sources.

Two-dimensional array interconnects are being researched now; experimental systems using "smart pixel" technology, for example, are demonstrating thousands of high-speed optical interconnects directly off the surface of silicon chips using free-space optics or fiber bundles.

An example of the use of 2D-array interconnects in an experimental free-space photonic switch is sketched above. In the smart-pixel version of such a system, electronics performs the logic functions and optics performs the interconnections.

(Courtesy of D.A.B. Miller, Lucent Technologies.)

Optical Image Processing and Computing

Historically, coherent optical information processing was analog, driven initially (30 years ago) by interest in synthetic aperture radar and image analysis, for which lasers and optics could provide correlations and spatial filtering. A separate stream of research developed from the invention of holography, which provided technology to enable optical associative memories and matched filters. More recently, reflection holograms have been proposed for interconnects between integrated circuits and for neurocomputers.

In the 1970s, researchers looked into using optics to perform computationally intensive operations such as vector-matrix and matrix-matrix multiplications. Special-purpose discrete optical processors were designed and demonstrated, using film as a mask for processing the input data set. The spatial light modulator (SLM), with transmission or reflection that varies across a plane, grew out of the need for a real-time programmable mask. Electrically activated liquid crystal SLMs operate at kilohertz frame rates and can accommodate more than 65,000 parallel channels. These remained expensive speciality items until the liquid crystal television, introduced in 1985, afforded researchers a low-cost alternative. However, their performance was poor.

Research on analog optical processing flourished during the 1980s, with the emphasis being on optical signal processing and neural networks for pattern recognition and image processing. Motivated by the introduction of optical bistable devices (optical transistors) in the late 1970s, researchers in the United States, Europe, and Japan also began investigating the use of optics in digital computing.

Both analog and digital technologies have been under development to replace (or enhance) electronic computers and specialty signal processors. As the optics research has been under way, however, the performance of electronic computers has continued to improve dramatically, presenting a formidable competitive challenge for optics. As a result, optical computing appears to be useful only in specialty applications in which there is a high degree of parallelism.

The generic geometry of an analog optical image processor begins with a two-dimensional coherent image, created in real-time by reflecting laser light off (or transmitting it through) an SLM. For this step, traditional liquid crystal SLMs are seeing competition from magneto-optic and electro-optic semiconductor SLMs, which can be faster. Next, in an analog processor, the coherent light is sent through optical components (lenses, holograms, prisms, pinholes, gratings, or a programmable SLM) that do the optical processing. Finally, the processed signal is read out visually or on a CCD (charge-coupled device) array. In a digital processor, the programmable SLM is replaced by a two-dimensional smart pixel array or an array of

nonlinear optical devices; digital optical processing uses logic gates and thresholding.

The applications envisioned for these technologies have typically been correlators or niche applications, but in many historical cases, these optical systems have lost their niche to high-speed silicon. Nonetheless, optical image recognition can be commercial; there is a fingerprint recognition product from Canada, for example (see Table 1.4).

The future of optical computing lies in exploiting the synergies between electronics and optics to approach problems that are difficult or impossible for all-electronic processors. Potential image processing applications lie particularly in rare-event problems, which electronic computers find difficult, such as fingerprint identification or recognition of a face in a crowd. Examples include electro-optic SLMs and smart-pixel arrays (based on semiconductor multiple quantum wells, liquid crystals, or magneto-optics) for use in microdisplays. Recently, quantum-well 600 x 600 arrays bump-bonded to silicon driver chips have been demonstrated that operate at megahertz frame rates.

Future applications of optical processing and computing lie in processing, storing, and displaying large space bandwidth product data. The need to perform these functions efficiently will grow rapidly in the information age of the next millennium. Furthermore, these functions exploit a primary advantage of optics (parallelism) in applications that have an optics-only solution (image display). It is in these computer peripherals, and in the interconnects between computers and peripheral devices, that optics fits best into computing. The size of the market is not yet defined, however, since the technologies are still under development.

For these optical technologies to have a future, they must be applied to practical problems. As for optical data links, processing information optically puts a premium on low cost. The action remains in developing practical hardware, which requires close cooperation between device and systems researchers. Devices developed without an understanding of the system are no more valuable than systems developed without an understanding of the devices. The technologies that will succeed are those that satisfy both systems and device needs.

TABLE 1.4 Examples of Optical Inspection and Machine Vision Systems That May Use Optical Processing

|

Security |

Transportation |

Manufacturing |

Medicine and Health |

Environment |

|

Novelty filtering |

Vehicle avoidance |

Part recognition |

Diagnostic cytology |

Spectral imaging |

|

Face recognition |

Sign recognition |

Integrated circuits |

Cancer detection |

Photogrammetry |

|

Fingerprint identification |

Augmented vision |

Produce inspection |

Flow cytometry |

Monitoring change |

Overall Issues

Because the competing technologies are electronics based, optical systems compete with a rapidly moving target as silicon chips become faster and faster and as parallel computing becomes more standard. Unlike other areas of information technology, in information processing, optics plays no unique role—so it must always be held to the electronics standard.

Several key technical issues remain open. Will optical computing find a niche where it is practical? Will optical image processing find a niche where it is practical? Will optical switching in telecommunication systems be centralized or distributed? What will optical cross-connects look like? The challenge is to continue the design of cost-effective devices that can be manufactured and packaged cost-effectively.

There are also important issues for optical information processing in university education and research. As noted in several places in this report, university programs rarely have a systems perspective. Because the advantages of optics for information processing lie in areas that require knowledge of both hardware and software, university education is rarely very relevant to successful engineering in this area. Similarly, in research, optical devices for information processing cannot be considered in isolation since the use of optics is determined by the system design, which is still a matter of debate. Because systems-related work in universities is relatively weak, companies involved in optical information processing typically train their employees on the job. If industry provided more state-of-the-art devices to universities, more useful systems studies could be carried out in academia. Intellectual property concerns may currently be a barrier to this in the United States.

Optical information processing faces some grand challenges: cost reduction of optical and optoelectronic components, packaged subsystems, and full systems; seamless merging of optics and electronics; optoelectronic device development driven by systems needs and system design driven by device realities; and full exploitation of wavelength, space, and time with optics.

Optical Storage

Market Size and Current Trends

The data storage market, fueled by an insatiable appetite for generating, collecting, and storing information, is growing exponentially. Multimedia applications such as video on demand, interactive games, advertising and home shopping, desktop video editing, video and data servers, document and medical imaging, and engineering and architectural drawings have made storage the fastest-growing segment of the

computer hardware industry today. Increased storage requirements are distributed throughout the hierarchy, from high-end libraries to desktop personal computers in the office or home. Typical capacity requirements and the way they are distributed are shown in Table 1.5.

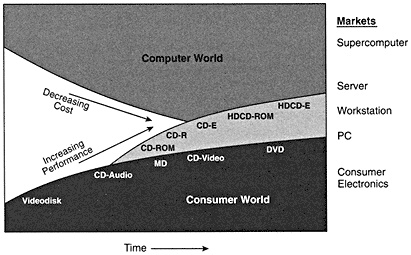

The amount of information stored electronically is already enormous (see Figure 1.12). Extrapolating the growth rate in recorded information over the past 50 years suggests that by the year 2000 the total will be 1020 bits, or 12 exabytes. This information will be stored on a combination of magnetic disks and tape, optical disks and tape, and a variety of optical formats (Table 1.6) based on the compact disk and the digital versatile disk (DVD).

CD- and DVD-based technology has accelerated the convergence of consumer and computer systems—a convergence that will put pressure on non-CD-format optical storage. This powerful impact of the compact optical disk is illustrated in Figures 1.13 and 1.14. The estimated worldwide market for data storage hardware in the year 2000 is expected to be in excess of $120 billion.

Trends in Storage Technologies

The storage industry is extremely cost-competitive, with price per megabyte being a key metric. Consumers want more capacity, cheaper systems, higher data rates, and products packaged in smaller form factors (i.e., more, cheaper, faster, smaller). Magnetic disk storage, the cornerstone of the industry, is characterized by its storage density. Packing more and more information onto each square inch of disk surface increases storage capacity, decreases the cost per megabyte, and increases the data rate because the linear density increases. At the same time, equal or greater capacity can be packaged in a smaller form factor. Since the first magnetic disk storage system was introduced in 1957, storage density has increased at a 30% compound annual growth rate. Everyone has predicted that such a growth rate can never be sustained, and they are correct: Since 1990 the annual increase has been 60%!

TABLE 1. 5 Typical Storage Capacity Requirements for Selected Applications

|

|

Medical X Rays |

Movies on Demand |

Document Imaging |

|

Main server |

Medical center |

Regional distributor |

Insurance company headquarters |

|

10,000 GB |

70,000 GB |

5,000 GB |

|

|

Local server |

Hospital department |

Local vendor |

Regional office |

|

20 GB |

350 GB |

100 GB |

|

|

Client storage |

Doctor's workstation |

Television set-top box |

Claims administrator |

|

2 GB |

0.1 MB |

2 GB |

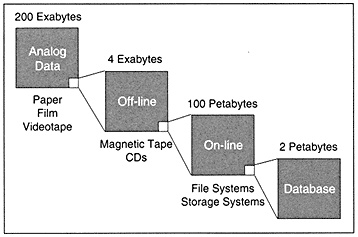

FIGURE 1.12 A pictorial overview of the data stored in the world in 1995. The variety of storage methods is indicated, from computer RAM to paper. An exabyte (EB) is 1018, or a billion billion, bytes. The 4 EB of electronic storage in 1995 is expected to increase to 12 EB by 2000. (Courtesy of A. Chandra, IBM Research.)

It is estimated that by the year 2000, magnetic storage density will be 10 gigabits per square inch (Gb/in.²). The fundamental limit is believed to be determined by the size of the smallest magnetized region that remains stable against thermal demagnetization—estimated by the most optimistic researchers to be between 100 and 1,000 Gb/in.². At these density levels, gigabyte capacity drives can be packaged like semiconductor processors and plugged into boards as storage modules. The cost is projected to be 1 cent per megabyte in 2000 and less than ¼ cent per megabyte in 2005. With the addition of removability, once the distinguishing feature only of tape and optical storage systems, magnetic storage will continue to be the dominant high-end storage technology for the foreseeable future.

Optical storage became an important part of the low-end storage market in 1982, with the introduction of the compact disk. The first success of CD technology was a consumer product capable of storing 75 minutes of high-quality music in digital form. The next application was the CD-ROM (read-only memory) used to store data for low-end computers such as PCs and workstations. This marked the beginning of the convergence of storage technologies for the entertainment and computer markets. Today, CD-ROMs have already replaced floppy disks as the preferred medium for mass distribution of programs, video games,

FIGURE 1.13 Dramatic cost reductions and performance improvements continue to bring the world of computers and the world of consumer electronics closer and closer. The optical compact disk has had a powerful impact on the merger of these two worlds. (Courtesy of A. Bell, IBM.)

FIGURE 1.14 Compact optical disks. They may not be aware of it, but hundreds of millions of people have lasers in their homes. Lasers are hidden inside their compact disk players and computer CD-ROM (read-only memory) drives, which they use to read the information stored on compact disks such as the one shown here. These disks are made of injection-molded plastic. The information is stored digitally in the form of a pattern of pits pressed in the plastic. It is recovered by sensing changes in the reflection of a focused laser beam. Digital storage ensures highquality reproduction of sound or data, and because the readout beam passes through the substrate, reproduction is insensitive to dust or scratches on the plastic surface. In addition, noncontact readout with a laser beam does not degrade the stored information in the way that passing a needle across a gramophone record did.

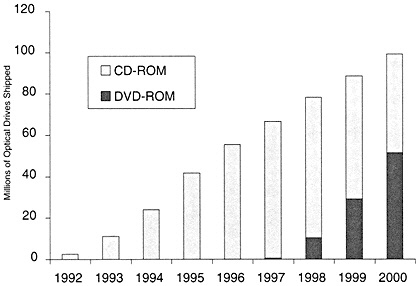

and reference material. CD-ROM installations are growing rapidly, as indicated in Figure 1.15. Low-end CD-based technologies are propelling optical storage sales toward a figure in excess of $70 billion in the year 2000, including $20 billion for CD-based drives and $40 billion for CD-based media (including content).

The original CD technology offers permanent, nonrewritable storage that can be removed easily from the drive and can be mass produced for less than 0.1 cent per megabyte. Another advantage is that optical readout using laser light does not cause deterioration of the stored information, such as that caused by a needle in a gramophone pickup. A successor CD technology with higher capacity is already in production. Digital versatile disks with capacities ranging from 4.7 to 17 gigabytes (GB) will soon allow storage of a full-length movie on a single disk. Agreement has already been reached on a DVD standard by which a four-layer DVD-ROM will hold 17 GB on a double-sided disk (see Table 1.6).