The Evolution of Private Health Insurance: Past Issues, Future Challenges

Stanley B. Jones

Health insurance coverage is one of those topics that makes everybody in the country angry. I learned a long time ago not to tell the person next to me on an airplane that I am involved in private health insurance because everyone is angry about health insurance coverage. Patients feel it is too costly, it does not pay for the services they need, and it involves too much red tape. Employers feel it is too expensive and are worried about its availability. Clinicians are troubled by concerns about how private health insurance shapes medical care; they think of private health insurance as a sort of procrustean bed that has the effect of distorting care. They see it as a form of harassment that determines what they do and how they think about medical problems, as well as who gets paid and how much they get paid. And they are worried about its influence on teaching institutions and the resulting great power it holds over the future of medicine and the training of young professionals.

These days the economists in Washington and assorted health policy theorists have their own gripe: it is with an attitude toward insurance that doctors and patients seem to share. This attitude may be paraphrased as, “Don't worry, insurance will pay for it!” In other words, insurance takes concern with costs out of the transaction between provider and patient.

These gripes arise from deep frustration. The reason for the frustration may be that all of us, despite our sophistication in the insurance industry or in clinical medicine, have an unstated idea about what coverage really should be. And it goes something like this: Insurance should pay for whatever you need to keep well if you are healthy, get well if you are sick, or stay as healthy as possible if you are chronically ill.

Once in a while I do mention on the airplane that I am involved in insurance, and someone will surely say at the end of a discussion of insurance, “Do you remember the days when, when you left the hospital, insurance paid for everything but the television set?” Times are not like that any more. People are troubled about insurance, about what it pays for, and about the extent to which it does not live up to that standard.

WHAT INSURANCE COVERS AND DOES NOT COVER

When people talk about insurance coverage, they really are interested in what insurance pays for. The following is a sample benefit package (it is drawn from the Health Maintenance Organization Act, so it is a particularly liberal benefit package, giving particularly liberal coverage):

-

Physician services, including consultant and referral services by a physician;

-

Preventive services, including regular checkups, pediatric examinations, immunizations, well-child care, family planning, and infertility treatments;

-

Inpatient and outpatient hospital services;

-

Emergency health services;

-

Diagnostic laboratory and therapeutic radiologic services;

-

Home health services;

-

Facilities for intermediate and long-term care;

-

Vision care;

-

Dental services;

-

Mental health services;

-

Treatment for alcohol or drug abuse;

-

Physical medicine and rehabilitative services; and

-

Prescription drugs.

Health insurance coverage is initially defined in terms of the types of health care services for which it will pay. Coverage is further defined by criteria these services must meet, such as that those services are performed by a doctor or under the orders of a doctor. An insurance expert once defined health insurance for me by saying, “health insurance pays for what doctors do or order to have done.” We have not traveled very far from that over the past fifty years. There are some areas here and there that are changing, but by and large health insurance payment decisions are based on what doctors do. Coverage is further defined based on where, or in what specific settings, such as hospitals, emergency rooms, and outpatient offices services occur.

Finally, and most importantly, coverage is defined by restricting payment to those services that are “necessary and appropriate for prevention, diagnosis, treatment, and rehabilitation of illness or injury”—a very important phrase in the history of public and private insurance contracting. Incidentally, coverage does not include that much prevention and rehabilitation; it is much more oriented toward diagnosis and treatment of illness and injury.

Of course, some services that might otherwise meet the above definitions are specifically excluded. For example, there is a growing tendency among insurers to exclude autologous bone marrow transplants because they are finding the phrase “necessary and appropriate for diagnosis and treatment” does not protect insurers in court when they think they should be protected. So they specifically exclude certain services if they do not think they are necessary and appropriate. Also, some classes of services are treated differently than others and are excluded from coverage. One example is what insurers persist in calling “ nervous and mental conditions” (their phrase not mine). In addition, insurers may exclude preexisting conditions.

For those services that are “covered,” insurance may pay only up to certain limits. The limits may be in terms of the number of visits, the number of days in the hospital, or the total dollar amount of claims paid, for example, $10,000, or $50,000, or $100,000, or $1,000,000 for the lifetime of the policy. Some insurers only pay up to their approved fee schedule for services. So if the doctor charges more, the patient may end up paying the difference. And, of course, insurers only pay after the patient meets deductibles and after coinsurance is subtracted, unless the

patient has already met his or her maximum liability for the year, in which case insurers will pay more.

In addition to the above practices, which effectively determine coverage or what an insurer pays, there are implicit or indirect limits that may not be stated. Many older people who are eligible for Medicare have said things to me like, “I was in the hospital and I really wasn't ready to come home, but the doctor (or the hospital) told me that Medicare only covers three days.” This is not true of course, but that is often the way the Diagnostic Related Group (DRG) payment ends up getting interpreted to the patient. This perception has become a limit on coverage of hospital days.

Now, given these coverage definitions, exclusions, and limits, consider the case of someone who has been rendered partly dysfunctional by a series of strokes and is sitting in front of their physician. The physician says, “Here's what we have to do: it's going to involve tests and some expensive imaging; and it's going to involve some hospital care; and there's going to be some physical therapy, maybe long-term care, and rehabilitation services over a period of time. ” The patient naturally asks, “Does insurance pay for this, doctor?” Can you imagine trying to answer if you are the physician? Not only do the above coverage criteria make it difficult to answer, but variations exist from insurer to insurer and policy to policy. Unless they happen to work in a one-company town, physicians see a bewildering array of plans. What defines coverage in most of our minds is what insurance pays for—and that always deviates from whatever we have to have done to us to stay well or get well. In this case, neither doctor nor patient will know what is covered until the final bills are received.

INSURANCE MARKETS

Why is it like that? Why does the reality of the insurance mechanism deviate so much from our unstated desire for total coverage? Let me offer a couple of underlying reasons and suggest that if we want to change coverage we have got to get real serious about these underlying reasons. Most attempts to redefine coverages in the past have not done this. People have tried to ignore these underlying reasons— or circumvent them.

The Will of the Buyer

In fact, employers purchase most of the health insurance coverage in this country and they purchase what they want. And what they want is geared toward attracting the employees they need. They do not buy coverage because they believe in good health care. They do not buy it because they are looking after the long-term health of society. They do not even buy it because they are worried about other companies in the community. Employers worry about their own employees and what they need to offer these employees in order to get them to work for them and to keep them working for them.

Thus, what people have by way of coverage varies a lot and it varies largely by labor market. People who are in low-skill labor markets get much less comprehensive coverage than those in high-skill markets. If an employer must attract highly skilled and sought-after engineers, for example, that employer will have a much better health insurance program than the firm down the road that lives largely off of unskilled workers.

Also, employees differ in what they want. Some employee groups are not really interested in some benefits and would much prefer others. Ten years ago, before the cost crunch was as serious as it is now, typically an employer would face a platter of expansion possibilities at the end of his insurance contract year. The platter might include vision, dental, mental health, and other benefits, perhaps even substance abuse coverage. Each benefit would be priced for his employee group. The employer would have the option of picking out this, that, some of this, and some of that, and would often send the insurer back to negotiate an appropriate arrangement. What they bought depended on the biases and desires of their employee groups. If their bias was heavily against what one might call preventive services, then those were excluded. If their bias was against mental health services—and it frequently was—then the employer felt it did not need to offer them. So, the labor market determines what is covered.

The employer also makes trade-off decisions between wages and coverage. The employer can pay employees in either form—higher wages or better coverage. The packaging depends on the market in which the company is competing for employees. The employer also makes trade-offs between personnel costs and prices for goods and services. The company not only competes for employees, it competes to sell products or services in the marketplace. So the employer tries to

keep personnel costs high enough to get the needed employees, but low enough to keep prices competitive. Right now, employers are desperate for lower premiums, or, at the least, for premiums that are growing less rapidly from year to year. Right now, also, demand is great among workers for higher wages rather than expansion of other benefits.

A number of problematic insurance coverage and rating activities result from these employer and employee trade-offs and cost pressures. One such problem is experience rating, in which the employer is charged a premium based on the likely future health costs of only their own employees, based on those employees' past health costs. The employer wants to pay for his or her people, but not for anyone else. The insurance industry is getting more and more sophisticated at zeroing in on just one small group and its likely costs, so that the employer pays only for them. Varying coverages are another result. Another is exclusion of preexisting conditions of employees. The insurance industry is getting more and more sophisticated at giving the employer the lowest premium that it can. Higher employee cost-sharing is also a product of this aim, as are cuts in unmanageable benefits. The insurance industry can study the claims experience of an employer and focus on those claims that are costing the most. Mental health coverages in particular have taken a huge beating because of this. They loom large as a percentage of the employer's premium dollar and they often are considered “unmanageable.” It is hard to get control of these services, to be sure that one is only paying for what one wants to pay for.

Cost pressures on employers have also led to some good responses. Health maintenance organizations (HMOs) originally came into the employer market as a response to the need to give young families better coverage at an affordable price.

Insurance as a Limited Product

Another major factor in determining coverage, in addition to the preferences of the buyer, is what I call structural limitations in the insurance product. Insurance is a fundamentally limited product, whether it be from Medicare or public insurance programs or private insurance programs. There are many things that insurance simply cannot do. One of the reasons for this is that insurance is a transaction-based system. It is based on pieces of paper, millions and millions of bills with codes on them that represent services to subscribers. Insurers process bills, and

their entire structure is built on the flow of bills. How it got that way for most of the country could perhaps make for an interesting article. Maybe it grew out of the industry's beginnings as a financial protection institution. Insurance did not set out to provide health care, it set out to protect people against the cost of health care. In any case, because of this flow of bills, insurers have huge investments in computers, and a large proportion of an insurer's employees are wrapped up in this processing activity. The way insurers think about their role is shared by this history. The upshot of it of course is computers and software and telephones. One may also attribute the sense of harassment and distance that most clinicians feel from insurance companies to these computers and telephones.

Another major limit, and perhaps a more fundamental one, is that in order to predict costs and set a premium, insurers have to quantify the use of services that are expected from a certain coverage. They must be able to count the providers or service sites and describe discrete service units. These factors are all interrelated. Often it is difficult to describe the service unit with enough precision for someone who is reviewing a bill to be able to differentiate it from another source, be assured that it was needed, and put a reasonable price on it. If a service is hard to describe for the above purposes, insurers can sometimes resort to limiting the providers who will offer it. In other words, if the service cannot be described, then the insurer can at least make sure that a doctor provides it. If insurers say that a doctor can only provide the service in a hospital, that limits the coverage even more. One of the upshots of all of this need to describe services so as to predict how many will be covered is that insurers avoid “soft” services, those that are difficult to define.

Another limit is the need to manage care. Here the question for the insurer is whether a service is necessary and appropriate for the diagnosis and treatment of illness or injury. The treatment may be worthwhile, but nevertheless not necessary and appropriate. Now, bear in mind that this is determined through pieces of paper, at “arms length,” so to speak. In fact, there is something of a religion among insurance companies about being at arms length from the providers. This means the piece of paper has to be adequate to tell whether a service is necessary and appropriate for diagnosis and treatment. This leads to a cops and robbers game wherein the physician tries to look out for the patient and checks those boxes on the form that look most helpful to the patient, none of which exactly describe what was done, and the insurer

knows what is going on and tries to stop it and find a way to trim back costs. Each side gets tougher and tougher.

The industry uses averages and percentages of the mean in physician practice patterns in order to decide what is “necessary and appropriate ” and what to pay for. There is hope that more sophisticated protocols are being developed by clinicians as a substitute for this kind of review. Pre-admission certification is another of the ways in which the industry protects itself. In this way the insurer argues about whether the service is necessary before rather than after it is performed.

This structural limit also explains why insurers tend to start independent practice association (IPA) and preferred provider organization (PPO) panels rather than group and staff models. An IPA or PPO still handles paper, it is still an arms-length arrangement, and it is still transaction based—and an insurer can understand this. The idea of sitting down around a table with physicians and hospital administrators is a very difficult concept for people in the insurance culture.

Another of the structural limits of the insurance industry is the “moral hazard problem.” There is some moral hazard for everybody involved in the insurance process. For the insurance buyer, there is the temptation not to insure until you get sick. Young people especially fall into this category. So when they get sick and go shopping for insurance, they find the insurance company has excluded preexisting conditions, or that the insurance company declines to sell them insurance at all (to keep from insuring only sick people).

For the provider there is the moral hazard of going ahead and performing a procedure since it is covered, even if it is marginal in value, or of coding a service in a way that assures it will be paid for, in order to help the patient out a little. The insurer responds to these provider practices by requiring precertification, tighter fee schedules, and what I call current procedural terminology (CPT) code wars. In these code wars the insurer studies how CPT codes are being measured and refines payment rules. The physicians on the other side are looking for ways to use the codes, and to create new codes, that will enable them to maintain their revenues. It is astounding that these codes are still controlled by organized medicine, given the reality and costliness of this war. If other tactics fail, the insurer's last response is participation.

The patient has his own version of this moral hazard, and that is to ask for a procedure simply because it is covered. The answer to that

from the insurer is cost-sharing, putting some of the burden on the individual so that they hesitate to ask for treatment.

Finally, as if there were not already enough structural limits on insurance, the need for insurers to offer competitive premiums and products poses one more. Insurance is a business. Employers can have their pick of insurers. It is a competitive industry characterized by strong fads and trends in the market. Often too little research backs up these trends. Over a given two- or three-year period, big employers all over the country do the same things. They add certain benefits, they add certain managed care practices. Often, the similarity of practices is furthered by benefit consulting companies that advise employers. When these consulting companies are asked to show data to prove that their measures save money, it is incredible how thin their data are. Sometimes they are nonexistent. Nevertheless, belief in certain measures is widespread. Insurance is an industry that is truly racked by fads, and very little is being invested in research and development.

Also, unfortunately, in insurance one can achieve a lower premium more quickly and efficiently by sophisticated rating, underwriting, and risk selection than by managed care. It is still the case that if an insurer wants to sell a smallish employer a good policy, that insurer is most likely to win the competition by figuring out how to rate better than another insurer or underwrite in a more sophisticated way, perhaps by offering a package that excludes certain conditions or certain employees. That is still the winning approach. In fact, it is frightening that ten years from now we may look back at the 1980s and 1990s, not as the era when managed care mushroomed among insurers, but as the era when insurers became more adept at rating and underwriting.

One of the sad upshots of the limits of insurance and particularly risk selection, is that one population is particularly poorly served. People who are chronically ill may in fact find a better clinical package and better care with an HMO—even a group or staff model HMO—if they only know it is available to them. But in fact some HMOs know that if they advertise that they can take care of, for example, AIDS patients in a way that was more satisfactory to the patient and less costly, then they would end up getting all the AIDS patients. And no matter how efficient these HMOs are, they cannot be competitive as an insurer if a highly disproportionate share of sick people have chosen them. The smart thing to do is not to advertise these benefits, but to let people stay with their original insurer unless they find their way to the HMO. Then, when they

get sick, they can be congratulated on their good luck and their care can be covered. We are all losing innovation and efficiency in our system because of these structural limits of insurance.

Now, before going on, I have to say that these are generalizations. We could talk about how some insurers and, especially, how some group and staff model HMOs and some clinics, hospitals, and physician groups are doing some truly innovative and interesting things. However, we hear so much about these innovations, we might get the impression that they represent some substantial portion of the industry. Alas, they do not. They represent a small part of what is going on out there; it is a hopeful part but a very small part.

IMPROVING COVERAGE

So, given the limits detailed above, if you want to improve coverage, what can you do? If your intention is to improve coverage, what kind of government improvements might help, and what kind of government changes?

First, you have to decide whether it is better to reform, to rebuild, or to replace the employer as the payer for, and purchaser of, coverage. Those are really the three options: reform, rebuild, or replace. If you think about it, it is incredible that what is covered for an employee is so dependent on accidents of employment: whether there happens to be a union negotiating benefits, what the employee's skill level is, which employer the employees happen to go with, and all sorts of other accidents that wait out there in the job market. These accidents are what determine most coverage. In order to influence that determination, we need a more careful definition of the social good of different kinds of health services and of the quality of various kinds of health services. That is the unfinished agenda.

Ten or twelve years ago I was on a panel at the Institute of Medicine, and the subject was mental health. At the time I was frustrated because I was looking for some relevance to insurance of our discussions on mental health services. And I asked this group of able and renowned clinicians if maybe we could define a core benefit made up of those services that do good, that really work, and that help people. Now, if you are an employer, and do not have a lot of money, and are trying to decide between vision care and dental care and other items, and you could be

talked into providing some mental health coverage, which services would you start with? Or, if you were willing to spend more, is there a broader set of services you might tackle? Well, the panel could not agree. Not only could we not agree on what should be on the inexpensive list, we could not even agree on the efficaciousness of possible items for the list.

If we want to improve insurance coverage, I think the burden is on clinicians and researchers to tackle that tough problem. The discussion of outcomes research is a great framework or culture in which to be talking about this, but the burden to demonstrate its social good will finally be placed on those who feel strongly about coverage.

Next, having decided whether to reform, rebuild, or replace the employer as buyer of health insurance, we have to decide whether we want to reform, rebuild, or replace private health insurance. Those who are reform minded look at that list of limits in health insurance and see the possibility that the present system can work. They argue that the problem is that we have too much of this and too little of that and this service is not well defined and that procedure is clumsy, and so on. The burden to reformers is to come up with better definitions of services so these services can be counted, so they can be costed out, and so an actuary can decide the allowable number and cost of these services and therefore, ultimately, the premium. Definitions are also needed, for providers and service sites, of the term “necessary and appropriate” so that reviewers of claims can review them better. We also need a better definition of “experimental.” Incidentally, it does not matter whether we are talking about a public or a private system. Medicare has to reform in this way as well. So, for advocates of a single-payer system who favor the Medicare insurance model, these same questions must be answered.

Those who are rebuilders and who think we can and should move into vertically integrated plans face a truly huge change, a rebuilding of the entire insurance industry. I think it is a greater change than General Motors changing its auto lines, much greater. Advocates of rebuilding are talking about recreating and restructuring the foundations of an industry. If rebuilding is the plan, then providers must be involved. The “arms-length” issue has been destructive from both sides. Providers are safely removed from insurance and in fact have been made a lot wealthier by the existence of health insurance in this country. Rebuilding insurance in order to improve coverage means moving providers into integrated systems so that they share accountability and responsibility for managing

both clinical aspects of care and cost aspects of care. Ways must be found to do that without compromising professional ethics and values.

Some flexibility in coverage, as well as room for innovation and greater responsiveness to patient needs, may arise from this. Because, in fact, if the provider and the insurer could be jointly responsible, with payments made in terms of capitation amounts and budgets, then flexibility could be achieved in all the definitions of what services will be deemed necessary and appropriate, by what providers, and at what sites.

There are those who wish to replace private insurance with government. Many people feel this way these days, but frankly, they will end up limited by the same mistakes. They will be faced by the same structural limits, but even more so. If we want the government to be the insurer, we have to work harder at defining the services, the providers, the sites and the term “necessary and appropriate.”

Lastly and most importantly, we are not going to improve coverage until we contain the rising costs of health care. The fact that costs have gotten out of hand has stopped the growth in benefits and experimentation in the last ten years. And it has encouraged all the definition sharpening, the exclusions, and ultimately the reductions in what insurance pays for. The fact is, we are moving farther and farther from our basic goal of covering what is needed to get us well or keep us well. And the reason is costs. There are two formulae to controlling costs. One is to rebuild insurers and to restructure employment-based coverage so as to move our system to vertically integrated health plans; the other is to regulate providers directly and directly set rates. At present, we are in the midst of the debate between these approaches. Ultimately, neither will improve coverages unless they contain costs.

Nonfinancial Barriers: Implications for Health Insurance

Thomas W. Chapman

I would like to discuss some of the important factors that should be dealt with in regard to health insurance coverage. I would also like to discuss other factors apart from the health insurance benefit package, although this is a key factor as it determines the utility of insurance coverage. I have participated in quite a few meetings on this general topic recently and I see this issue routinely discussed from a perspective of very narrow interests and viewpoints, on the part of employers, the government, and various provider groups. Everyone is looking at this business of health reform through their own tunnel. It brings to mind a group of people on a sinking cruise ship who are all looking out through their own particular portholes as the ocean rushes in. To continue the analogy in terms of the health care reform debate: each passenger (be they representatives of the business, insurance, hospital, or managed care sectors) partly believes that if their porthole can be secured, somehow the ship will stay afloat. There is little if no realization that they are all in this together. When the ship finally begins to sink, however, both the people in the state room and in the boiler room will go down with the ship, no matter how much they paid to get on. Thus, it is important to gain a sense of consistency of purpose and focus on what we are trying to accomplish in health care reform. There is a great deal more that we will need to do, beyond insurance reform.

I will quickly review the data and characteristics on the people we are trying to insure. The facts reflect some of the obstacles and issues we have to face. These data show that health insurance benefits are important, that there is no question about that, but that they are only a means—and only one means—to an end.

At any time in the past four years, by a number of professional counts, somewhere between 33 and 38 million people in the United States have been uninsured; the percentage of total population uninsured has remained relatively constant over that period of time. When we begin to look at 1991, we see that about half of the nation's non-elderly poor have some sort of public coverage (primarily Medicaid), the rest do not. In 11 states, including the District of Columbia, about 20 percent of the population is uninsured. About 14.7 percent of the uninsured in 1991 were children. Some estimate higher percentages of minority and unskilled workers due to unemployment.

When we take this uninsured population and examine it a little bit closer, we begin to see that there are problematic characteristics to it. For example, the three largest industry group segments of uninsured workers aged 18-64 fall into the agriculture, construction, and retail sectors. Agriculture comprises the largest share at 41 percent. Construction comprises 31 percent and retail comprises 25 percent. These data suggest that there is probably a high degree of moderate- to low-skill workers among the uninsured, along with significant nonunion, minority, seasonal, and part-time workers, most of whom are at the low end of the wage scale and do not maintain consistent employment. In fact, the vast majority of these workers are employed in small companies, their incomes average $20,000 per year, and they are 29 years of age or younger. That is functional poverty in the American economy. It is interesting how we adjust to numbers; we keep thinking that if a person earns $20,000 he or she is above poverty, but we have to think in terms of reality in America. These are the groups for whom we wish to extend insurance and access. In particular the agricultural category of 41 percent of uninsured is the largest challenge we face to overcome access. Most of these workers move from farm sites every three to four months and have children exposed to chemicals, poor nutrition, and dangerous environments.

In March 1993, I had the opportunity to spend a week traveling across the country attending seminars sponsored by the Robert Wood Johnson Foundation and the Henry J. Kaiser Family Foundation to hear

comments from people about their major problems in accessing care. It was preliminary work to start a project called Opening Doors, a program that addresses social and cultural barriers to care. The first step was to go to four cities and meet with groups of private sector and community-based providers, consumers, and other constituencies. We spent considerable time talking to these groups about what they felt were some of the social and cultural barriers to care and why those barriers were important to deal with to achieve access.

I want to share a few of the comments from these meetings with you. People routinely mentioned the abject poverty as a cultural factor that besets groups of individuals and families in this country, the frustration it produces, and the impact that it has on the willingness or even the interest of this population to seek health care. One of the interesting things that came up in our discussions was the dominant, decision-making role that men play in many cultures (U.S. and foreign) as to who gets health care, when they get it, where they get it, and how they get it for the whole family. The lack of female health care providers was a substantial and consistent comment. This gender imbalance created access and barrier issues in most communities, particularly in cultures where orthodox, traditional and conservative belief systems exist. A number of the immigrant groups who participated expressed concern that the personal information required to access health care could be passed on to government or law enforcement agencies. That fear intimidated people and kept them from getting care early on. For many underserved groups, the complexity and organization of the U.S. health care system is a major health barrier—its eligibility rules, its paperwork, the location of services and facilities, and other government requirements. The professional staff and bureaucracy in many large health care institutions were viewed as intimidating, insensitive, and unresponsive to the sociocultural needs of patients.

Another common complaint was that the process of getting care in many places is bureaucratic and slow. For example, some said that it took multiple weeks for a prenatal visit to be set up, which discouraged people from even seeking or remembering those visits. Health facilities often maintain rigid hours, they are not flexible, they do not adjust to the needs of the population, so again people face barriers. For most single parents who have no child care available, the amount of time and energy necessary to prepare for a clinic visit or a hospital visit is enormous, a major undertaking. Many commented that once they arrive, they sit for

substantial periods of time in waiting rooms, see a physician that might spend 10 minutes with them, and then are sent on their way. Recently I saw such a person in a clinic in Richmond; she really caught my eye because she reminded me of these comments. A woman was sitting in a waiting room in a community clinic with three children all bundled up, two infants and another small child, and she was waiting for a prenatal visit. I just wonder what she went through, how much determination and effort, to get to that clinic and if the providers could understand the implications of these factors on the medical care services.

The sense of awe and powerlessness experienced by patients as they try to engage the medical establishment and the delivery system on its own professional turf also creates discomfort and barriers. The fear of medical experimentation is still alive and well in many underserved communities, especially among many ethnic and racial groups. Barriers to care created by frontline receptionists and staff, a very important factor that many of us overlook most of the time, is extremely important. Fear and embarrassment of discussing sexual issues with providers in professional settings, especially those of the opposite sex, is a major problem. Indifference or a lack of understanding or belief in the value of preventive care amongst a number of groups is another, as well as cultural incompetence in professional groups. Associating a bad clinical outcome, such as the miscarriage of a friend or relative, with what may happen to them, may deter young women from seeking prenatal care. The inability of providers to identify illiteracy in the process of treatment and in the process of care also is a major barrier.

In addition to sociocultural barriers, another factor in the utility of health insurance benefits is important. What shall we do about the current complex enrollment, eligibility and claims processes under various forms of insurance? These have worked very well to discourage people from getting public and private insurance. This issue has yet to arrive at the discussion table in health care reform. I hope it does so soon. We have not decided whether people will be enrolled automatically and have a birthright to health insurance or whether there will still be some requirements, some tests, some bureaucratic steps that people have to go through. It is important to clarify this, given our experience with Medicaid. We see the Medicaid programs in many states operating like the American Express Company in the sense that there is a marketing department that encourages everybody to get a card (they are very bullish about it). Then there is a credit department that rejects and ejects people

for a variety of reasons. In many governments, especially at the state level, there are conflicting incentives regarding Medicaid. As a result, we know that there are too many people who are eligible but not enrolled, and too many people who are not enrolled because they have tried and not been successful.

The best example that I know of is right here in the District of Columbia. It was well documented in the 1992 Report to the Committee on the District of Columbia put out by the General Accounting Office. The District has a 10-page Medicaid application. It is probably easier and quicker for you to refinance your house. Three pages of instructions go along with this 10-page application. By the way, the District is not the only state that has such a mechanism. All of this paperwork was created by that “American Express Credit Division” to make sure that people do not get anything they are not entitled to, so much so that this has created a new industry for hospitals. Hospitals now go out and pay firms, almost like bounty hunters, to enroll people in the program. We have produced another industry, and that provides an economic stimulus, but now we have all of these additional firms that go out and enroll people because the process is so complex. We should be able to learn something from that and not drag it into the next era; it will undermine the utility of health insurance benefits. This is an example of waste and inefficiency we should eliminate in a reformed system.

The last factor that I wish to discuss is one that is not only important in terms of the kind of benefits we have, but also in resolving the access problem. I believe that the availability of more primary care and the management of patients on a consistent and regular basis will determine the ultimate financial success or failure of health care reform. Catching people early on and managing their problems in a regular way is something that most of us do not think about because our health care is already managed effectively and in a regular way. But for many in our country, especially the old, the poor, and the uninsured, that is not the case. We are treating them in a very expensive and inefficient way. Often they receive care that probably could have been provided in a cheaper setting and for illnesses that could have been avoided or prevented. There have been many examples and studies of this phenomenon, particularly here in the District of Columbia. We know that we could probably empty out at least half, if not two-thirds, of America's hospitals if we just managed people effectively. An enormous amount of money could be saved and applied to better purposes. What we need to

strive for is appropriate utilization and effective management of patient care on the front end. That is where the savings are, and where they can be sustained over a period of time. If we look anywhere else, such as in fee schedules and caps or other kinds of economic gimmicks, we will be dissatisfied once again, and we will guarantee that there will be new industries of smart people who are clever enough to figure out a way to work around the system and to help the providers become much more successful than previously thought.

I would like to think that we can all keep ourselves focused on the whole picture, not just our own interests, our own porthole on the ship. We must look at the entire range of issues and try to pull things together, because I think we are on the brink of a great opportunity. Health insurance benefits are certainly one of the areas in which we can make a lot of improvement. But we must look beyond fixing health insurance if we are really serious about assuring access for all Americans, particularly those that today are most disadvantaged.

Response from a Managed Care Perspective

Simeon A. Rubenstein

I will tell you a little bit about Group Health Cooperative, then I will focus on health care benefits, and then I will summarize with some conclusions. Group Health Cooperative of Puget Sound is a 500,000-member, billion-dollar-a-year, consumer-governed organization located primarily in Washington State. It is variously called a health maintenance organization (HMO), or a managed care organization, or (one of the new terms) an accountable health plan, or, as we are soon to be called in Washington State, a certified health plan. These names are all the same. They represent entities that integrate insurance and financing on the one hand with delivery on the other. They get rid of the separation, the armslength relationship between insurance and delivery. All the components of the delivery system are integrated and they have a common information system so they can report outcomes. The goals of these organizations are health status over time, system satisfaction, and cost, not cost per service, but rather cost per enrollee over a period of time. We do not just manage cost. Our purpose is to manage health care, satisfaction, and cost. This is very different from the traditional fee-for-service indemnity system.

Health care benefits, as with many other pieces of health care reform, are a major factor determining cost. I am going to focus on

options for managing cost, and on how benefits impact cost from the perspective of what we have learned at Group Health Cooperative.

Managed competition assumes informed purchasing decisions, usually by individuals rather than businesses. And yet there are multiple variables among managed care competitors. Benefits are a variable, premium and point-of-service costs are a variable, outcomes (if reported at all) are variables (and hard to understand from the purchaser's standpoint), and choice of providers or locations are variables. The goal in informed decision making in managed competition is to standardize some of these variables, such as benefits, and report the other variables in an understandable and comparable way.

But the big issue is cost, or to echo a 1992 election theme, “It's the cost, stupid!” But what cost are we talking about? Are we talking about the premium cost? Are we talking about the premium and the point-of-service cost-sharing? Or, are we talking about the cost of the macro health care system, which involves far more than health insurance premiums and cost-sharing? From some payers' standpoint, it is just the premium. For individuals who buy their own health care, it is the premium and the point-of-service cost share. For the country, it is the macro system: the premium, the cost share, the taxes for the public health care system, the cost involved in research and development, and the cost of occupational health. Clearly, it is far more than just the premium cost; and cost management or cost control is the key to our ability to increase access.

The various funding streams for health care in this country include: (a) health insurance, the largest, whether it be liability insurance, health services contractors, or HMOs; (b) the public health sector, which includes those public health services such as water purification and air quality; data collection and dissemination; public information; disaster responses; some social services; and research and monitoring through the National Institutes of Health, the Centers for Disease Control and Prevention, the Food and Drug Administration, and a variety of other organizations; (c) occupational health, which as a business-related cost acts as a stimulus for employers to create the safest possible environment for their employees; (d) the medical industrial complex, which provides venture capital to test new drugs, new equipment, or new procedures; (e) charity, which supports health care for some unable to pay; and (f) individuals who pay a portion of their own health care.

Cost management options include: (a) price controls, which historically have not worked; (b) benefit controls, either by cost-sharing, which lowers premiums but may not lower costs, or by rationing coverage as the Oregon Health Decisions approach has proposed; and (c) health services guidelines (“If we just had better technology assessment and practice guidelines, we would be able to control all the costs in health care!”) It is my view that in the absence of any incentives to use practice guidelines or useful technology assessment, these processes will make only a limited impact on costs.; (d) personal values (“We should change our expectations for health care. If everyone's expectations changed, costs would go down.” For those of you who want to change personal values and expectations, good luck.); and (e) system restructure. As presented by Dr. Chapman and Mr. Jones, system restructure holds the greatest opportunity for us to have an impact on health care costs, including the administrative overhead of health care.

Now I want to focus on the issue of benefits. At Group Health, we are currently in the middle of a benefits review process. We have three specific questions. The first question is: What should the breadth of the benefits be, what sets of services should be included in this thing we call health insurance? The second question is: What should be the depth of coverage and how much coverage should occur within these sets of services? Should it be 100 percent, should it be something less than 100 percent, and, if so, why? The third question is: How do we make difficult decisions about very specific services: for example, smoking cessation classes versus liver transplants for alcoholic cirrhosis? Those are specific services within a set of services.

THE BREADTH OF BENEFITS

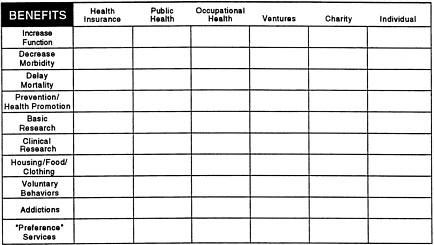

Figure 1 shows an example of how Group Health is trying to address these questions.

FIGURE 1 Funding Streams I.

Health insurance covers those health services that increase function, decrease morbidity, or prolong effective life and delay mortality (we do not really save lives, we delay death). Other services in the broad category of health care include prevention and health promotion; basic biomedical research; clinical applied research; custodial services such as housing, food, clothing (particularly relevant for long-term care); “voluntary behaviors” and addictions; and so-called preference services that include services such as cosmetic surgery and treatment for infertility. Some people link “voluntary behaviors” and addictions because debate continues on how much of certain personal activities are addictions versus controllable behaviors.

The question is not what should be covered under health insurance, it is who bears the financial responsibility for each of these services. The question is not a yes or no for health insurance, it is “where the financial responsibility lie for each of these services?” That is the way the issue should be approached. In order to do so, we must involve all the players: the health insurance industry, the public and occupational health sectors, the pharmaceutical and medical equipment industries, and consumers. Some services may have more than one source of financial responsibility. For example, in health promotion and

prevention, some services are a public health responsibility (e.g., water and air quality), some services are an individual responsibility, and some services are the responsibility of health insurance.

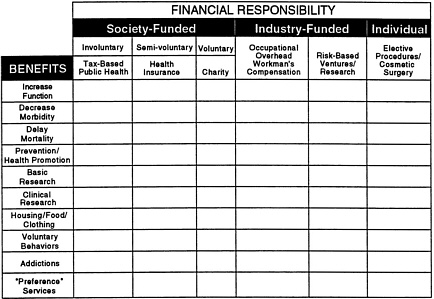

FIGURE 2 Funding Streams II.

Another approach is shown in Figure 2: The vertical column is the same as in Figure 1, but the horizontal column heading has changed. The first three horizontal rows from the heading represent how we socialize health care costs: through a tax-based system to support public goals such as public health; through health insurance and pooling of risk; or through donations, as with charities. The next two vertical columns represent the industrialization of health care costs: occupational medicine and risk-based ventures. I believe the cost of workplace injuries and disabilities should remain a business cost as an incentive to create the healthiest possible workplace. The costs of research and advances associated with new pharmaceuticals and equipment should, to a defined

degree, continue to be “industrialized” and financed by companies willing to accept the risks and rewards. The third general category is individual financial responsibility for health care costs that are “personal.”

The breadth of benefits therefore must be decided in a context that is far broader than just health insurance. We must look at all funding sources for health services and define explicit financial responsibility. Benefits should be nondiscriminatory as to type of service. Pharmaceuticals should not be excluded from coverage simply because it is a convenient administrative way to limit premiums. Mental health services should not be excluded simply because it is convenient to exclude mental health. Nor should we limit organ transplants simply because we want to keep costs down.

Benefits also should be nondiscriminatory as to provider and practice setting, to allow more innovation in the future world of organized, integrated health care systems. For example, if it is more appropriate and acceptable to deliver maternity care by a midwife rather than a physician, a health system should have that option.

DEPTH OF COVERAGE

How much coverage should be provided for any set of services? Depth of coverage is usually defined by deductibles, copayments, and coinsurance. Two questions must be addressed. The first is: Does altering the depth of coverage really change the total cost of care or does it just change the locus of responsibility for the cost of care? The second question is: Does changing the depth of coverage have a positive or negative impact on health outcomes? From both the RAND Health Insurance Study and from a study that Group Health has published on the introduction of ambulatory visit copayments, it is clear that moderate cost-sharing in an employed population appears to have no effect on health. This, however, does not necessarily apply to a poverty-level population.

Studies show that the vast majority of cost-sharing represents cost-shifting to the individual, not cost savings. For every 10 percent of cost-sharing, there is about a 9 percent cost-shift to the individual and about a 1 percent cost savings to the health care system. Our study on the introduction of ambulatory visit copayments demonstrates a 10

percent decrease in primary care visits and no change in specialty care visits.

Group Health evaluated pharmacy copayments in two separate studies. The first, conducted in the mid-1980s, compared state and federal enrollees. No difference in rates of prescriptions between these two populations was noted 12 months after the introduction of pharmacy copayments in one of the two comparable populations.

Recently we evaluated the introduction of a $5 pharmacy copayment to our Medicare beneficiaries. Previously there had been complete pharmacy coverage without cost-sharing in our Medicare supplemental policy. This modest $5 prescription cost-sharing did not alter the trend of a slight rate of rise in pharmacy prescriptions per Medicare enrollee. Our conclusion, therefore, is that Medicare cost-sharing at a $5 copayment per prescription is a 100 percent cost-shift and does nothing to the total cost of health care.

Our hospital admissions and length of stays are short by any standard. It seems unlikely that modest cost-sharing on a per diem basis will decrease these hospital days further. Hospital per diem cost-sharing will be predominantly, if not exclusively, a cost-shift to the individual.

The conclusions on the depth of coverage issues are as follows: in an employed population, modest copayments do not adversely affect health status, modest copayments have some impact in decreasing utilization and therefore decreasing total cost, and modest cost-sharing predominantly causes a cost-shift to the individual.

OTHER BENEFIT ISSUES

How do we decide about coverage of very specific health care services? The various criteria that have been proposed include: efficacy and effectiveness; cost and cost-effectiveness; and something called patient satisfaction. From a scientific standpoint, effectiveness or efficacy are the ideal criteria independent of cost. From a social standpoint, cost-effectiveness and cost benefit are the ideal criteria. From a patient standpoint, everything needed or desired should be provided, without significant additional financial responsibility. The reality is that there must be some combination of these criteria in order for us to make decisions on specific health services. A variety of secondary criteria have been discussed as well: community standards, legal risk avoidance, and

legislative mandate. I believe all are secondary to the primary criteria listed above.

The last issue is benefit implementation. I simply cannot be as eloquent as Tom Chapman about this issue because he sees this as far more of a day-to-day problem than I. Geographic issues affect how we implement benefits, social issues affect how we implement benefits, and system design issues affect how we implement benefits. Our current nonsystem of health care separates hospitals, insurance companies, physicians, and the medical industrial complex. I have friends in all four. They are trying to optimize what they do within the existing incentives that we as a society have created for them. They are not bad people. But we have to change the paradigm. It must change from everybody working to optimize their own segment of the pie to a more integrated approach where all segments work toward the goal of improved health satisfaction and cost outcomes over time.

One example of how integrated systems can work is our breast cancer screening program. In an integrated population-based system, we targeted a population of a women over age 40, stratified them by personal risk profiles, and defined an appropriate schedule of teaching, self-examination, and periodic mammography. With this program we found that Group Health enrollees had a slightly lower use of mammography than non-Group Health enrollees, but our outcomes were better. The measure of outcome was breast cancer tumors greater than three centimeters per hundred thousand women over age 50. Between 1983 and 1989, there was a consistently lower incidence of tumors greater than three centimeters in Group Health enrollees. Better outcomes were achieved using a systems approach to a population rather than an incident-based approach.

I will conclude with these recommendations.

-

Health insurance benefits must be defined within the broad funding context of health services financing, which includes all sources of funding.

-

Health insurance benefits must not discriminate based on age, gender, ethnic background, illness, or method of diagnosis or treatment. It is extremely difficult to separate bad luck from bad genes from bad behaviors.

-

Health insurance benefits should not be provider specific; providers should be able to vary by plans, by credentials, and by privileges.

-

Modest point-of-service cost-sharing is reasonable, in order to lower total costs somewhat, but should be applied with the under-standing that it will primarily shift financial responsibility to individuals rather than reduce overall costs.

-

Legislating insurance coverage for specific health services is difficult. Accurate, timely, and available information, provider-patient joint decision making, and risk sharing are far more powerful motivators to produce appropriate levels of services.

-

Benefits are not the major factor in addressing the problem of health care costs. System design and system implementation are the keys.

DISCUSSION

HAROLD LUFT: Thank you very much. Certainly my expectations have been met in terms of helping me think more clearly about some of the issues related to benefits design and what we need to consider in terms of developing a basic benefit package. I'm sure there are some questions from the floor.

QUESTION: How reasonable is it to expect that traditional insurance companies can be successful in the world of integrated health plans?

STANLEY JONES: The difficulties that an insurer faces in moving from a traditional insurance arrangement to a vertically integrated health plan are practical, but profound nevertheless. The insurance industry is made up of people who have built their reputation and accomplishment on learning complicated processing systems described to some degree in my discussion on coverage definitions: how to write coverages, how to rate them, how to run big processing organizations. People at the top have generally been in the industry for a while and have worked their way up. If you ask people at the top how their company works, they can tell you all the details. It's a lot like Medicare that way. Thank goodness for people in Medicare who can tell you where every dot is in the law and all about the regulations and how the system works. What we are now proposing is that they stop looking at all those pieces of paper, and stop writing definitions and go out and sit around a table with physicians and hospital administrators and ask how they can make

the job of keeping people healthy a joint problem. And they should ask how they can do it for a reasonable cost, using clinically sophisticated techniques and sharing the financial risks.

It's tough from the other side, too. It's tough for the providers to get used to this. I think providers have been insulated from this world of risk by insurance. But for insurers this is a huge change. I really think it's bigger than changing a product line, because it's a change in the kind of people you hire and the way you look at your company. Insurance people call on me or my colleagues as consultants and we end up telling them that what they are going to have to do is redesign their company. And they are terrible at redesigning companies. They've never done it and their whole training has not been that way. So we have an industry that, for all its good will, has a huge task ahead of it and is only starting to respond. In all fairness I have to say that the industry is starting to respond with real seriousness, but it's a big challenge for them.

QUESTION: Your comment leads to another question. Should we stick with the insurance industry or should we at least allow other groups, for example provider groups, to take the lead in this arena?

JONES: I would suggest to you that if you look at the insurance industry, you will see a lot of limits and problems, but also a lot of skills that providers will need in order to enter this marketplace. There are risks involved in entering the marketplace. And there have been some big mistakes made by providers who have gotten into packaging services and quoting prices for the next year or two or three to an insurer without having the skills that insurers have at identifying and predicting and managing financial risk. In about 10 percent of the industry, we are already seeing a lot of innovation and experimentation on the part of insurers who are linking up with providers in order to package services in a different way.

KENNETH SHINE: I would like for you to discuss the issue of guaranteeing a basic benefit package, but with an option that if people wanted to buy more benefits, they could do so. Critics of such a strategy contend that if that happens one might very well go back to a multi-tiered system in which there was the basic benefit at a relatively low level, and the population who could afford to do so would buy a higher level of benefits. I'm curious as to any of the panelist's views on this notion of

benefit levels from the point of view of balancing costs versus equity and effectiveness.

SIMEON RUBENSTEIN: Group Health has dealt with this issue for a number of years now. We asked our members what should be in the basic benefit package, and they say “everything but infertility treatments and cosmetic surgery.” Some people want a service covered because they need it, or they think they might need it, or someone in their family needs it. Others want or need a different service covered. We have to design a package (basic, standard, or comprehensive) that deals with the needs of a population of patients. Some people are going to need mental health benefits, some people are going to need treatment of diabetes, and some people are going to need more maternity benefits than others. So I believe the benefit package must be comprehensive. If there are variables, perhaps single versus double rooms in hospitals, then you can buy a slightly richer package; but almost anything other than comprehensive benefits will not work. When Oregon passed its Health Decisions program, it decided not to cover those services that do not improve health. My question was, “Why are you doing things that do not work?” The reason they are paying for services that do not work, in part, is because we live in a fee-for-service system and the patients often do not pay. There is no incentive to limit care to effective health services.

THOMAS CHAPMAN: I would agree. People are always going either to need or want more than the benefit level anyway. And I think that if we accept arbitrary levels in a benefit package, without trying to arrange for as much comprehensiveness as possible, then the question is open as to who pays the difference. We're right back into the same soup that we're in now. And it may be that there is room for creativity and diversity. Although certain services are covered by the benefit package, it may be that some services are better off provided directly. There is a limited appetite for any insurer to take risks on things that they don't know much about. It may be that we will have to arrange to provide certain services directly without insurance.

JONES: I would say there's one other consideration and that is the breadth of coverage versus the depth. Again, it depends on whether or not you have a reasonable income, but we get a sense from multiple surveys that people would rather have the breadth and give up a little bit of the depth than have deeper coverage and be at risk financially for something that falls outside the scope of benefits.

There are some other factors to consider in choosing between comprehensive and basic coverage as well. Basic coverages raise enormous problems of risk selection in competitive markets. The first problem arises if you supplement the basic coverage. If someone says I want to buy more than basic, how does that relate to the basic existing coverage, how does it get packaged, how does a regulator ensure that games aren't being played by the insurer to attract risk or discourage risk by how and when they supplement? The system right now is rife with that kind of risk selection competition.

There are a string of related issues. I would suggest to you that we are really wrestling with two questions in the country at the same time. One of them is a financial protection question. It's the traditional old insurance question, as with life insurance: how much do you want to buy? That is, how much protection do you want to buy against illness? The other question is: what is good for people in terms of health care. If we want to define how much financial injury we are going to protect everybody in this country against, it might be cleaner to separate the two questions. Instead of talking about basic services or benefits, let's talk about how much financial protection we are willing to give every American citizen and then leave them on the loose for the rest. Then, at the same time, let's talk not about health insurance, but about health care and programs that offer health care, and then let's see what we come up with. I think we get very confused conceptually between those two questions, and they lead to very different kinds of systems and industries.

LUFT: I would just add one more item. Sometimes people talk about including things like vision care or dental care, and I would argue that all of these may be good things to include in a “basic benefit package. ” However, you may want to make them separable in terms of the delivery systems. In other words, some people may use primarily vision or dental care because they are really healthy and they may not want to go into an integrated system that limits their choice of providers if they have to give up their ongoing relationship with their dentist or eye doctor. You could allow them to buy a separable dental package or enroll in a separable dental plan to avoid some of those risk selection differences. I remember early discussions of Medicare supplemental plans when people found that senior citizens with their own teeth had better physical health, consequently they offered dental coverage to attract the low-risk people. That's the sort of problem you want to avoid.

QUESTION: As a pediatrician in an inner city hospital, I'm struck by Dr. Rubenstein's careful definition of the limitations of a copay as being tested in a population that is employed. I haven't heard anyone comment, and I would like to hear your comments, about the importance of removing the financial barriers at the time the service is needed. Again I'm influenced by my belief that, for child care, no one chooses to go to the doctor for the joy of it, they go for a reason, whether it be to stay well or because someone is ill. I want to remove that financial barrier at the time the service is needed.

RUBENSTEIN: Again it gets to the depth of coverage question, and it is an important question. I do not have any hard information that addresses your question: whether or not parents actually bring in their children if there is a $3 or $5 copay.

COMMENT: I can tell you that people will not bring their children when they run out of money and they have to use it for food. At that point they do not go to see the doctor.

RUBENSTEIN: When you are talking about an impoverished group of people, there is little question in my mind that we must subsidize cost across the board for children and for adults. Charging a $5 copayment may seem almost irrelevant to me, but it has tremendous relevance to people who have no money at all. I do not know if it should be across the board for everyone below age 18 or limited to an employed or impoverished population. I do not know the answer to that.

QUESTION: I am an obstetrician/gynecologist and I would have to say something about not considering basic coverage for reproductive care. . .

RUBENSTEIN: Infertility, I said.

QUESTION: Infertility. About 7 percent of the American population is involuntarily infertile. If you accept the definition of health as physical well-being, I would really like to know how one responds to that?

RUBENSTEIN: What I can say to you is there seems to be a consensus, right or wrong, that infertility is more of a “preference service.” I realize that infertility for some people is emotionally very distressing, as are ears that stick out for children. I am not trying to equate them, I am just saying there comes a time when society makes a judgment and society has judged this to be a “preference service.” I agree with you, there are people who are very distressed by it and I don't

know what the right answer is. I am just telling you what other people are saying.

QUESTION: I am going to ask the panel to assume they are going to be setting basic benefits for the next ten years. And I am going to ask you to reflect on the technology and the cost of new technology? In a world of managed competition, are insurers and plans going to consider other factors in what is and what is not covered? And is competition going to be a factor in your decision?

JONES: Yes, to all parts of the question. It strikes me that I would be most comfortable seeing the decisions on what technology to use and how to apply it made on clinical and public health grounds rather than on insurance grounds. Frankly, I don't think ultimately it becomes a financial protection issue, but when we say “benefits” we fall back into the insurance mode. What I would really like to see us asking here is: what works? What produces useful outcomes and socially desirable goals for a society as a whole and as individuals? And can we in some way rank it or define a core product that will do good? I haven't even gotten to the question of what's a benefit yet. That logic leads me to say that I would rather see some sort of accountable health plan that includes both clinicians and people who can worry about setting prices and defining risk, and who can worry about managing resources, but who are held accountable to high standards of quality and who compete on that basis. I would rather them see them, rather than a public or private insurer, wrestling with these issues.

I would rather not see Congress discuss these questions because of the pork barrel problem. They don't want to end up in a position where people who have an idea, even a good idea about what ought to be covered, up there lobbying them and bringing all the folks who have that condition to lobby Congress. It is an impossible position to put a politician in.

QUESTION: Following up on that point … Certainly the idea of managed competition, as several of you have said, brings together clinical autonomy and financial accountability, and, in a constrained economic environment, the concept of medical necessity. In the service world, medical necessity may lead to excesses, but it probably does not put providers at great risk. Is our knowledge base on medical necessity enough to provide adequate protection for consumers and even for providers, particularly in an economically constrained environment?

JONES: Are you thinking of such technologies as outcomes research and practice guidelines?

QUESTION: I am also wondering about the ethics of physicians and nurses. Traditionally, we have relied on them to look out for what is best for the patient.

JONES: The problem of underservice is what you're raising. The only constraint in which I have confidence in that environment is not ethics, it's the marketplace. In fact, if it is possible to get away with bad quality consistently as a health care provider or insurer, then we're all in trouble. I would assume that government might play some role in holding people accountable in terms of accreditation and we will get better at measuring outcomes and improvement in health. Ultimately, however, the only test I trust is consumer's decisions on which plans they feel safer with, perhaps with some published data to help them. But even that is a risk.

The other side of the risk though is that frequently people talk about the problem of unnecessary care in the fee-for-service system and unnecessary illness that comes out of it. I think the problem is bigger than that. We are spending so much money that we are pricing the health care system out of reach of a larger and larger percentage of the population. That's more harmful to us in the long run than a lot of other things that come out of the fee-for-service system.

QUESTION: Could you give us some idea about how long it will take to build the necessary infrastructure for health care reform to succeed?

RUBENSTEIN: The infrastructure and the management talent does not exist to implement effective managed competition nationally. It is not going to happen in two to four years as originally discussed. As we have branched out into different communities in the state of Washington, it takes a minimum of two years to build an infrastructure just as an extension of our existing infrastructure. To start in totally new markets will take four to eight years. I do not think it can happen overnight.

CHAPMAN: I don't think there is one specific grand fix. In a country this complex and this dynamic, we will probably go through stages in which we implement some things, try them out and see how they work, and fine tune them and then move on to the next stage. We have been in that process for over fifty years and will probably continue.

I do not think there's any one thing that will turn everything around. Rather, a range of new and better ideas will come along.

JONES: We've waited a long time to seriously address the cost issue. We've kidded ourselves for a long time about how much good we're doing and how much we're saving. Employers have kidded themselves, insurers have kidded themselves (and advertised about nonexistent savings), and the same can be said for government. It's been in all of our interest to act like we're more successful than we are. So we've waited a long time and now we're in desperate shape in terms of costs.

On the other hand, in this country we now have a set of ideas that are really pretty unique, particularly the development of vertically integrated health systems. Whether a little bit vertical or a lot vertical, these organizations have an advantage that we sense is very important. Namely, they may allow a lot more flexibility in deciding how we are going to organize services, who is going to provide them, and all of those fine-print definitions. I have a fear that we are going to rush down the cost-containment road, and someone asked earlier if rate setting is incompatible with competition between accountable health plans. Well there are some real incompatibilities. We decide we are going to set rates and try to control volume, and then we tell an accountable health plan that the way they can really save money is to channel their patients to certain hospitals and certain physicians, but incidentally the rates for that hospital have been determined based on their getting so many patients next year. So, if you switch too many from that hospital to this one, it's going to undermine that hospital's budget. Budgeting under rate setting is based on a certain number of patients using a certain hospital. If you end up sending patients somewhere else because you get a better quality or cost deal, you end up with real incompatibilities. At some point we as a society have to make a real and difficult choice.