5

U.S.-Japan Cooperation in Dual-Use Technologies: Pursuing Opportunities and Managing Risks

SUMMARY POINTS

-

In the future the United States will need to rely more heavily on commercial technologies in developing and procuring defense systems, including technologies in which Japan has developed considerable strength. This implies a need for greater access to Japanese commercial technologies and their utilization in defense systems. Japan has developed leading edge capabilities in a number of technologies with significant and growing defense applications, which could contribute to meeting U.S. security needs.

-

Despite the large potential for mutual benefits, a focused, long-term effort will be needed to overcome barriers to beneficial cooperation. The most significant barrier is the lack of support in Japanese government and industry for facilitating the application of Japanese commercial technologies to U.S. defense needs.

-

U.S. dependence on Japan and other countries for critical technologies and high-technology products for defense systems is an important issue that will require continuous attention. Some degree of dependence is inevitable. The key will be to manage dependence in order to minimize the risks and maximize the benefits of utilizing Japanese and other foreign technologies.

-

Despite declining defense budgets, Japan is well positioned to continue to pursue commercial and industrial technology benefits from defense and security-related projects, including those involving international collaboration. This could lead to increased international competitiveness for Japanese companies, with implications for U.S. industry in areas such as aircraft and commercial space.

ACCESSING JAPANESE COMMERCIAL TECHNOLOGIES FOR U.S. DEFENSE NEEDS

As discussed in Chapter 3, Japan’s spending on defense technology development is very low relative to its total defense budget and the size of its overall R&D enterprise. Although the potential for achieving a more reciprocal U.S.-Japan defense technology relationship exists through several of the collaborative mechanisms discussed in Chapter 4, and there are areas of dedicated defense technology in which the United States would significantly benefit from greater exposure or access to developments in Japan, Japan’s dedicated defense technology capabilities are likely to remain narrower and less developed than those of the United States.

However, Japan has developed considerable strengths in a variety of dual-use technologies. This is significant because the United States is currently engaged in a broad effort to increase utilization of the commercial technology base for defense systems.1 There are two reasons for this effort. First, with ongoing defense budget cuts as a result of the end of the Cold War, there is a growing imperative to stretch and restructure weapons procurement and research and development (R&D). A greater use of commercial items and commercially derived technologies, particularly in subsystems and components, should reduce costs. The second reason for a greater U.S. Department of Defense (DoD) reliance on commercial technology is that in areas such as electronics, software, and materials, commercial technology developments are outpacing technologies developed solely for defense uses. In some cases, greater utilization of the commercial technology base would deliver benefits to U.S. weapons systems in the form of greater capability as well as lower costs.

Japanese strengths in microelectronics, advanced materials, advanced manufacturing, and other critical technologies are well known and comparable to the capability possessed collectively by our NATO allies. As noted, Japan’s defense procurement and technology development policies have emphasized utilization of commercial technologies and civil-military integration, particularly at the components level. 2 There are a number of obstacles blocking DoD access to Japan’s commercial technologies, including the fact that ownership often resides in Japanese companies that are not traditional Japanese defense suppliers; the Japan Defense Agency (JDA) and other Japanese government agencies might have little leverage.3 Also, Japanese advantages in many high-technology fields tend to take the form of manufacturing practices and techniques that may be more difficult to transfer at arms length than “hard technology, ” which can be expressed in drawings and technical instructions. Finally, some have questioned the interest of U.S. companies in Japanese technology and the willingness of Japanese companies to transfer their technology. 4

The National Research Council’s (NRC) Committee on Japan organized several workshops in which representatives of U.S. companies discussed Japanese strengths in dual-use technology areas. One workshop focused on advanced composites, and the other on optoelectronics. Table 5-1 shows selected Ministry of International Trade and Industry (MITI) R&D programs in advanced materials and optoelectronics. These are not the only areas of Japanese technological strength in which contributions to meeting U.S. defense needs might be pursued, but they are useful examples that illustrate more general issues.

|

1 |

National Economic Council, National Security Council, Office of Science and Technology Policy, Second to None: Preserving America’s Military Advantage Through Dual-Use Technology, 1995. |

|

2 |

Richard J. Samuels, Rich Nation, Strong Army: National Security and the Technological Transformation of Japan (Ithaca, N.Y.: Cornell University Press, 1994), especially Chapter 8 and Chapter 9. A succinct treatment is contained in U.S. Congress, Office of Technology Assessment, Other Approaches to Civil-Military Integration: The Chinese and Japanese Arms Industries (Washington, D.C.: U.S. Government Printing Office, 1995). |

|

3 |

A recent survey of U.S. government and industry representatives conducted by the MIT Japan Program discusses these obstacles in more detail. See Matthew Rubiner, U.S. Industry and Government Views on Defense Technology Cooperation with Japan: Findings of the MIT Japan Program Survey, 1994. |

|

4 |

Michael Green, The Japanese Defense Industry’s Views on U.S.-Japan Defense Technology Cooperation, 1994, p. 18; Rubiner, op. cit., p. 20. |

Advanced Composites

Advanced composites include areas of materials development and manufacturing as well as fabrication technologies for specific applications. The primary applications of advanced composites in the United States have been in defense systems—both missiles and military aircraft—and in commercial aerospace. Because of cuts in defense procurement, U.S. materials makers and composites fabricators have come under severe strains in recent years, and industry has cut its own R&D spending, even as U.S. government R&D support has increased.5

In a survey of U.S. companies active in this field, Japanese companies were mentioned most frequently as major foreign competitors.6 Japanese companies built their composites capabilities by focusing on sporting goods and other commercial applications but are now internationally competitive in aerospace applications as well.7 Japanese companies are focused on a number of process technology advances in composites with both commercial and military applications (see Table 5-2).

TABLE 5-1 Selected MITI R&D Programs Related to Optoelectronics and Advanced Materials

|

5 |

U.S. Department of Commerce, Office of Industrial Resources Administration, Critical Technology Assessment of the U.S. Advanced Composites Industry (Springfield, Va.: National Technical Information Service, 1993), p. i. |

|

6 |

Ibid., p. 132. |

|

7 |

This is illustrated by Toray’s supply of materials to Boeing for the vertical tail fin on the 777—the largest composite structure thus far on a commercial aircraft. See National Research Council, High-Stakes Aviation: U.S.-Japan Technology Linkages in Transport Aircraft (Washington, D.C.: National Academy Press, 1994), pp. 46-48. |

TABLE 5-2 Examples of Japanese Focus and Strength in Advanced Composites

|

Civil Engineering Applications The use of composites in civil engineering (buildings, roads, telephone poles, etc.) will become more attractive as the cost of composites goes down and environmental regulations limit the use of other materials. Large Japanese construction companies are cooperating with the Japanese government in launching demonstration projects, but U.S. materials companies do not have access to a comparable knowledge base because the U.S. construction industry does very little R&D. |

|

Pitch-Based Carbon Fiber U.S. companies have deemphasized work in this area in the face of continuing challenges to lowering manufacturing costs, but several Japanese companies remain very interested and active. |

|

Process Control for Pan-Based Carbon Fiber U.S. companies are competitive on a cost and performance basis, but it appears that Japanese companies turn out more consistent fiber. |

|

Process Control for Prepregnation Japanese manufacturers exhibit superior consistency in turning out treated fibers, particularly very thin prepregnations. |

|

Three-Dimensional Weaving, Preforms, and Tooling for Low-Cost Resin Transfer Molding (RTM) Building on the strengths of its textile processing and machinery industries, Japan has developed strengths in weaving fibers. The Japanese focus is on lowering the cost of preforms through automated weaving and flexible machines. |

|

Cocuring This is the process being used to manufacture the FS-X wing. A Japanese focus is to bring down the parts count in order to lower cost. A large part of Japan’s success in this area may be the result of work practices that may be difficult to institute in the United States. |

|

Ceramic Fiber Manufacturing Ceramic composite materials development is a key enabling technology for future high speed commercial engines. Several Japanese companies continue developing improved versions of their fibers, despite the present low level of demand. |

|

SOURCE: Compiled by Office of Japan Affairs staff. Based on discussionsat the National Research Council Workshop on Japanese Advanced CompositesTechnology, 1993. |

For example, the use of composites in civil engineering (buildings, roads, telephone poles, etc.) is likely to become more attractive as the cost of composite materials goes down and environmental regulations limit the use of other materials. Discussions at the NRC workshop indicated that, while large Japanese construction companies are cooperating with materials makers in exploring these applications, U.S. materials companies do not have access to a comparable knowledge base because the U.S. construction industry does very little R&D.8 Access to the data resulting from Japanese demonstration projects would help U.S. materials companies prepare to serve these emerging markets. DoD interest in civil engineering applications of composite materials is reflected in funding by the Advanced Research Projects Agency (ARPA) of a university-industry consortium that seeks to develop the “knowledge, tools and techniques for building bridges and elevated highways from advanced composite materials.”9

Another example of Japanese focus is three dimensional weaving, preforms, and tooling for low-cost resin transfer molding (RTM). Building on the strengths of its textile processing and machinery industries, Japan has developed strengths in weaving fibers. An ongoing MITI-sponsored project supports development of fiber weaving equipment.10 The Japanese focus is on lowering the cost of preforms through automated weaving and flexible machines. Although U.S. companies are currently strong in RTM, the Japanese are focusing a major effort in this area.

A third example of Japanese strength in composite materials is cocuring. This is the process being used to manufacture the FS-X wing. The focus is to bring down the parts count in order to lower costs, which cocuring accomplishes. Discussions at the NRC workshop and a recent report by a panel organized by the Japan Technology Evaluation Center confirm a Japanese focus on incremental improvements in manufacturing practices to reduce cost, as opposed to greater U.S. reliance on computer modeling and basic materials research.11

Another characteristic of Japanese companies working in this area is consistent, long-term R&D funding in areas that many U.S. firms have abandoned due to uncertain short-term commercial prospects. Ceramic composite materials development is a key enabling technology for future high-speed commercial engines. Some U.S. companies are capable of making advanced ceramic fibers, but demand is currently quite low. Japanese companies continue to pursue advances, in part through government-sponsored R&D activities. Future applications of these materials include engines for high-speed civil transport aircraft.

Optoelectronics

The term “optoelectronics” refers to a diverse group of technologies and applications, including displays, optical storage, fiber optics and optical interconnect, imaging sensors, and illumination systems. Optoelectronics advances are contributing to U.S. military capabilities in a number of areas, including communications, sensors, and guidance systems. Along with information systems and modeling and simulation, sensors were recently singled out as a key

|

8 |

A discussion of Japanese activities in utilizing composite materials for civil engineering applications is contained in Dick J. Wilkins, Moto Ashizawa, Jon B. DeVault, Dee R. Gill, Vistasp M. Karbhari, and Joseph S. McDermott, JTEC Panel Report on Advanced Manufacturing Technology for Polymer Composite Structures in Japan (Loyola, Md.: International Technology Research Institute, 1994), pp. 55-76. |

|

9 |

Jeffrey Mervis, “Defense Conversion Comes to Campus,” Science, March 25, 1994, p. 1676. |

|

10 |

Wilkins et al., op. cit., p. 18. |

|

11 |

Wilkins et al., op. cit., p. xix. |

strategic investment priority by the DoD.12 As a result of R&D investments made by U.S. government and industry targeting defense and information systems applications, U.S. industry has broad technological strengths in optoelectronics, with many leading-edge technologies being pushed forward by smaller companies.

Various optoelectronics technologies have also been applied in consumer and industrial equipment. Japanese companies have developed broad technological strengths largely based on their focus in these areas.13Table 5-3 lists areas of Japanese strength in optoelectronics discussed at the NRC workshop. Representative examples include compact disk players, fax machines, and hand-held video cameras. As in advanced composites, U.S. optoelectronics manufacturers surveyed by the U.S. Department of Commerce rate Japanese companies as their most capable foreign competitors.14

Many optoelectronics technologies and components have applications in both commercial and military systems. For example, large Japanese companies control a significant percentage of the consumer market for laser diodes, while a number of small U.S. companies produce expensive high-performance devices for military applications using similar basic technology. Incorporating Japanese manufacturing insights into these areas could help lower the production costs of U.S. firms. Japanese companies are also making fundamental technological breakthroughs in this field, a recent example being the development of a blue-light-emitting diode by Nichia Chemical, a small company based on the island of Shikoku.15

TABLE 5-3 Areas of Japanese Technological Strength in Optoelectronics

|

Blue and blue-green lasers and emitters CD laser technology, including arrayed CD lasers and holographic focusing High-speed external modulators Solid-state optical sensors Optical image stabilization techniques (camcorders) Illumination systems Liquid toner electrophotography and photoconductors General array technology Monolithic devices Metal semiconductor metal detectors Low-cost plastic fiber arrays |

|

SOURCE: Compiled by Office of Japan Affairs staff. Based on discussionsat the National Research Council Workshop on Japanese OptoelectronicsTechnology, 1994. |

|

12 |

Department of Defense, Director, Defense Research and Engineering, Defense Science and Technology Strategy (Washington, D.C.: Department of Defense, 1994), p. 12. |

|

13 |

Stephen Forrest, Larry A. Coldren, Sadek Esener, Donald Keck, Fred Leonberger, Gary R. Saxonhouse, and Paul W. Shumate, Optoelectronics in the United States and Japan (Loyola, Md.: Japanese Technology Evaluation Center, forthcoming). |

|

14 |

U.S. Department of Commerce, Office of Industrial Resource Administration, Critical Technology Assessment of the U.S. Optoelectronics Industry (Springfield, Va.: National Technical Information Service, 1994), p. V-2. |

|

15 |

Bob Johnstone, “True Boo-roo,” Wired, March 1995, p. 136. |

A U.S.-Japan collaborative research effort in optoelectronic devices is currently being implemented. The joint research program contemplates a user-broker system for prototyping and testing optoelectronic devices. Discussions were originally initiated by Japan under its Real World Computing program, organized by MITI. The National Institute of Standards and Technology (NIST) is the lead agency on the U.S. side.16

In addition, U.S. industry and government agencies are pursuing a number of domestic initiatives to improve U.S. capabilities, particularly in areas where Japan is strong, under the Advanced Technology Program of the Department of Commerce and the Technology Reinvestment Project administered by ARPA. Private groups involved include the National Center for Manufacturing Sciences and the Optoelectronics Industry Development Association. It may be possible to leverage these and other efforts in developing approaches to increase U.S. industry access to Japanese commercial technology for U.S. defense needs. Box 5-1 describes a promising example of a consortium of U.S. companies that is developing applications for graded-index plastic optical fiber, a technology licensed from a Japanese inventor, with support from ARPA.

Incorporating Japanese Commercial Technologies and Capabilities into U.S. Weapons Systems

As the discussion of advanced composites and optoelectronics illustrates, there are a number of important areas of dual-use technology in which Japanese strengths built through addressing commercial markets could be applied to meet U.S. defense needs. The scope for such cooperation will grow in coming years, as DoD’s reliance on commercial technologies in these and other areas grows. However, except for cases in which DoD utilization of commercial components in areas dominated by Japanese companies is so extensive that it raises concerns about dependence —a topic discussed below—there are few examples of Japanese commercial technologies applied to U.S. defense needs.

In facilitating greater U.S.-Japan cooperation in this area, the role of industry-to-industry relationships is likely to be even more important than it is in the cooperative mechanisms focusing on particular defense systems, which were discussed in Chapter 4. Particularly where the application of Japanese manufacturing techniques is sought, technology transfer will often involve extensive interaction between U.S. and Japanese industrial partners.

There are several contexts and mechanisms through which Japanese commercial technologies could be incorporated into U.S. defense systems. Collaboration could be targeted at a specific subsystem or subsystem upgrade, as discussed in Chapter 4. Joint R&D on generic enabling technologies not linked to a specific program is another possible context. Likewise, the roles of the Japanese and U.S. governments may vary depending on the context. When U.S. defense contractors or subcontractors license Japanese technology or incorporate Japanese-made components embodying a given technology, the direct government role would ideally be minimal. Where technologies need to be moved forward to address specific defense needs, the Japanese and U.S. governments could play a more direct facilitating role. For example, DoD and JDA could work jointly to modify mechanisms that Japan has already used effectively to incorporate commercial technologies into its defense systems.

|

16 |

NIST has selected the Optoelectronics Industry Development Association (OIDA) as the U.S. broker. See “U.S. Chooses Optoelectronics Broker in Cooperative Effort with Japan,” NIST press release, January 1995. |

Despite the potential for mutual benefits in dual-use collaboration, activity to date has been minimal. This indicates that there are significant barriers to this form of collaboration. One issue that was discussed extensively in Chapter 4 is Japan’s arms export policies. Second, although Japanese companies appear to be willing to incorporate their own technologies into joint projects, there is a strong perception that they are more reluctant to license their technologies for cash than are U.S. companies and that they are concerned about technologies being used against them in commercial markets.

Some analysts assert that a lack of interest in Japanese technologies on the part of U.S. companies is a major barrier. Although, clearly, U.S. defense contractors have been mainly motivated to cooperate technologically with Japanese companies due to a desire to access the Japanese market, rather than by a desire to access to Japanese technology, it is also clear that a number of U.S. companies have been rebuffed in their efforts to access Japanese technology over the years. Only if barriers to access are lowered on the Japanese side will it become clear whether lack of U.S. industry interest in Japanese technology is a serious barrier. As the optoelectronics case described in Box 5-1 illustrates, there are a range of leading edge dual-use technologies in Japan that U.S. industry is likely to pursue access to given a favorable or at least not hostile attitude on the part of Japanese government and industry.

Overcoming these obstacles is likely to require a focused, long-term effort by both countries. It will require more on the U.S. side than simply compiling lists of superior Japanese technologies. U.S. government and industry will likely need to jointly develop new approaches to building effective collaboration with Japanese counterparts. Part of this effort will involve developing new incentives for Japanese government and industry participation. Although there is a strong case to be made that expanded collaboration in this area would strengthen the U.S.-Japan alliance and Japan’s security, it does not appear that Japanese government and industry are strongly supportive of the Technology-for-Technology initiative, which is aimed at bringing this about.

New incentives could take several forms. In the collaboration between Ishikawajima-Harima Heavy Industries (IHI) and Newport News Shipbuilding, a promising example described below and in Appendix B, U.S. government funding of the MARITECH program and the changing nature of global competition in commercial shipbuilding facilitated greater willingness to share technology on the part of Japanese industry. Other useful examples come from the semiconductor industry. Since the late 1980s, the number and scope of mutually beneficial U.S.-Japan alliances in the semiconductor industry have increased dramatically, as U.S. sales in Japan have grown.17 Examples include the Motorola-Toshiba and Hitachi-Texas Instruments alliances. Although the U.S.-Japan Semiconductor Trade Agreement of 1986 (renewed in 1991), which stipulated a goal of 20 percent foreign penetration of the Japanese market, is strongly opposed by many in Japan and the United States, a strong case can be made that it has provided a framework of incentives that has contributed to the more reciprocal industry-to-industry relationships seen today. 18 Both positive and negative incentives may be necessary to facilitate collaboration in dual-use technologies that serves the long-term interests of both the United States and Japan. Specific approaches are discussed in Chapter 6.

|

17 |

See Electronic Industries Association of Japan, Semiconductor Industry International Cooperation Update (Tokyo: EIAJ, 1993). |

|

18 |

Laura D’Andrea Tyson, Who’s Bashing Whom? Trade Conflict in High-Technology Industries (Washington, D.C.: Institute for International Economics, 1993), Chapter 4. |

|

Box 5-1 Graded-Index Plastic Optical Fiber A recent, interesting example of technology transfer from Japan to the United States in optoelectronics is graded-index plastic optical fiber. The technology was licensed from a Japanese individual inventor by Boston Optical Fiber, a small start-up company.1 Currently, applications are being developed by a consortium of U.S. companies with funding from the U.S. Department of Defense Advanced Research Projects Agency (ARPA). Plastic optical fiber was first developed by Du Pont for General Motors in the late 1960s, but achieving the performance necessary for widespread commercial application proved to be difficult. Du Pont suspended its development activities and licensed the technology in the late 1970s. Japanese companies have achieved some success in incremental improvements. Plastic optical fiber is now used in signs as well as in some medical and automotive applications. There has been no U.S. manufacturer for some time. Boston Optical Fiber was launched in 1992 by Ed Berman, who anticipated a growing market for plastic fiber and was motivated to establish a U.S. source. As Berman was in the process of getting started, he learned of a breakthrough that had been made by a Japanese inventor. Interestingly, the inventor is a professor at Keio University who made the invention on his own and therefore owns all of the rights. The breakthrough, known as graded-index plastic optical fiber (GIPOF) allows plastic fiber to be used in high-band width data communications, which had previously been impossible. Berman contacted the inventor and after about ten months of persistent effort was able to negotiate a nonexclusive license. At the same time, he was discussing the potential of the technology with program managers at ARPA, who were interested in the wide applicability of GIPOF and in facilitating the growth of a U.S. manufacturing source. ARPA recently agreed to provide $4 million in support to a consortium formed to develop applications for GIPOF, which includes General Motors, Honeywell, Boeing, and Boston Optical Fiber. The industry partners are providing $2 million in matching funds. This consortium is not part of the Technology Reinvestment Project that ARPA plays a leading role in administering.

|

Government Facilitation of U.S.-Japan Private Sector Collaboration that Strengthens the U.S. Defense Industrial Base

In an environment in which defense spending has dropped substantially, U.S. defense prime contractors and suppliers are following a combination of diversification, exit, and consolidation strategies. Many of these companies possess technologies, low-cost manufacturing capacity, and other capabilities that might be of interest to potential Japanese partners suffering under the recent yen appreciation. In addition, U.S. companies that have depended on DoD support to fund basic technology development—often of a dual-use character—are looking for ways to continue to access the same level of R&D activity while DoD support declines.

|

Although slower peak speeds prevent GIPOF from replacing glass optical fiber in intercity telecommunications applications, it could replace copper wire in local area network (LAN) applications, particularly those where weight is a consideration. Several of the other members of the ARPA-supported consortium have such applications in mind. Boeing, for example, would like to replace as much copper wire as possible in its aircraft. To start, it will focus on applying GIPOF to linking entertainment systems and other noncritical areas. As more automotive subsystems incorporate computer controls, the Delphi unit of General Motors anticipates that all automotive computers will eventually be linked with a master computer through a LAN. Honeywell will be working on the electronics to support these applications developments. Boston Optical Fiber has just 15 employees at this writing, but anticipates rapid growth. The Japanese inventor of GIPOF has also licensed the technology to a group of Japanese companies that are collaborating in R&D work—Sony, NEC, Toray, and Toshiba. This case illustrates that there clearly are cutting-edge technologies in Japan that U.S. industry and DoD are interested in transferring and developing. It also illustrates that technology transfer from Japan to the United States can be relatively straightforward. The relative ease of obtaining the license could be attributable to unusual features of this case that lowered or eliminated barriers that often exist for U.S. companies seeking to acquire Japanese technologies, barriers that are discussed extensively in this report. For one thing, Boston Optical Fiber was dealing with an individual inventor. It is relatively rare for cutting-edge inventions to be controlled by individual inventors in Japan, and more common for large Japanese companies to seek cross-licensing or technology in return for technology rather than an arms-length license for their breakthrough inventions. Another relevant factor is dual-use. GIPOF is clearly a dual-use technology; LANs are pervasive in military information systems and weight savings from plastic fiber could enable a range of new military applications. However, the consortium is now focusing on clearly commercial applications. Although under Japan’s export control policies it should be possible to license GIPOF and other Japanese dual-use technologies specifically to develop defense applications, it is often difficult or impossible because of uncertainties over export control interpretation and other factors. This case illustrates how Japanese dual-use technology can be transferred to the United States to meet commercial and defense needs. In future cases where there is a basic willingness on the part of Japanese innovators to share technology, it should be possible to utilize similar mechanisms. |

One example of collaboration that is currently ongoing is the Newport News Shipbuilding-IHI relationship (see Appendix B). Newport News has been largely dependent on government contracts for nuclear-powered aircraft carriers and submarines. In recent years, however, declining military acquisitions have necessitated a rethinking of the firm’s future. A cornerstone of the shipyard’s diversification effort has been a drive to enter the liquified natural gas (LNG) tanker market. After encountering obstacles, Newport News has been able to license IHI’s SPB containment system for LNG tankers. The terms of the arrangement allow Newport News to use the SPB system on any contract, whether doing so in partnership with IHI and other shipbuilders or as an independent builder. The association with IHI has also allowed Newport News to assimilate advanced Japanese shipbuilding techniques that hold long-term potential for

improving the efficiency of its operations, better enabling it to compete in commercial shipbuilding markets.

IHI recognized several advantages in cooperating with Newport News in consortia to bid on LNG projects and in other areas. Newport News ’ large manufacturing capacity will enhance the competitive position of consortia in which it participates, particularly for large projects. IHI also perceived Newport News as having significant political influence within the U.S. government. Finally, a consortium that included a large U.S. partner would be well positioned to compete in the U.S. market, should it improve.

Since Newport News has not yet won a contract utilizing the license from IHI—either by itself or as part of a consortium with IHI and the other yards—it is impossible to assess the bottom-line benefits of the relationship at this point. Still, the case represents a promising example of how U.S. defense contractors might leverage international technological capabilities in order to diversify and address commercial markets.

The evolution in IHI’s strategy may also be a harbinger of more general shifts in the international strategic alliance approaches of Japanese firms, which have traditionally been eager to enter alliances that enhance their technological capabilities but have been reluctant to share their own technologies. The growing need for Japanese companies to reduce manufacturing costs brought about by the long-term appreciation of the yen and fierce global competition—including competition between groups of Japanese companies—might lead to more U.S.-Japan business alliances in which technology flows from Japan to the United States.

The Newport News-IHI relationship has been further strengthened by their joint involvement in the Marine Systems Technology (MARITECH) program. MARITECH was initiated in 1993 to revitalize the U.S. commercial shipbuilding industry. Administered by ARPA, MARITECH functions much like the Technology Reinvestment Project. Firms submit proposals for projects to ARPA, and ARPA supplies matching funds to those deemed best able to contribute to the advancement of relevant technologies. Funding for 1994 was $30 million, with another $190 million allocated through 1998. MARITECH seeks to improve the competitiveness of U.S. shipbuilders by fostering the creation of technologies that will help American shipyards produce commercial vessels more quickly and profitably.

MARITECH represents a significant experiment in U.S. technology policy. As an existing program in which DoD is facilitating transfer of Japanese and other foreign technologies to build the dual-use capabilities of U.S. companies, it could serve as a model for future initiatives to the extent that it succeeds.

MANAGING DEPENDENCE ON JAPAN AND OTHER FOREIGN SOURCES FOR CRITICAL TECHNOLOGIES, COMPONENTS, AND EQUIPMENT

Reliance on foreign suppliers for critical military components and technologies and the related risks have attracted attention and concern in the United States over the past decade.19

|

19 |

A number of studies and articles on this issue have been conducted in recent years, such as Institute for Defense Analysis, Dependence of U.S. Systems on Foreign Technologies, 1990; The Analytical Science Corporation (TASC), Foreign Vulnerability of Critical Industries, 1990; National Defense University, U.S. Industrial Base Dependence/Vulnerability, 1987; and Theodore Moran, “The Globalization of America’s Defense Industries: Managing the Threat of Foreign Dependence,” International Security, Summer 1990. These reports are summarized in U.S. Congress, General Accounting Office, Assessing the Risk of DOD’s Foreign Dependence (Washington, D.C.: U.S. Government Printing Office, 1994). George Gilboy, “Technology Dependence and Manufacturing Mastery,” MIT Department of Political Science unpublished paper, 1995, was also made available to the Defense Task Force for this analysis. |

Japan has been a focus for rising concerns in this area because of its strong technological-industrial capabilities. The two most significant U.S. policy initiatives relevant to this discussion have addressed areas of U.S. weakness vis-à-vis Japan, with implications for dependence on Japan or Japanese denial of critical technologies—significant DoD financial support for the SEMATECH R&D consortium and the National Flat Panel Display Initiative announced in 1994.20

Japanese and other foreign producers may be able to supply components of better quality or lower cost or may be the only available source of a specific technology. However, foreign sourcing and dependence carry potential national security liabilities. These include (1) acute short-run risks of inadequate supplies of components or equipment for surge or mobilization contingencies; (2) longer-term risks of inadequate access to foreign technologies during the development phase for new systems; and (3) risks of spillover effects and generalized industrial erosion that the absence of domestic capabilities might have on upstream and downstream industries.

In short-term contingencies the key national security imperative for any critical component or piece of equipment is to obtain adequate supplies for peacetime surges in production or general mobilization. Concerns about foreign sources revolve around the possibility that adequate supplies would be blocked or otherwise unavailable. For example, foreign production sites or transportation channels might be destroyed or disabled by military action, natural disasters, or accidents. Foreign sources might also withhold supplies from the United States for political reasons.

The overall extent of foreign dependence and foreign sourcing is generally unknown, particularly at the lower tiers of the supplier base.21 The preponderance of publicly available information indicates that foreign dependence, particularly dependence on Japanese sources at the lower tiers, is now extensive and that it increased during the 1980s.22

A good example for evaluating these concerns in the context of Japan is ceramic semiconductor packages.23 Ceramic packages are key components for microelectronics installed in virtually every military system. Although there are several domestic suppliers, imports account for about 90 percent of identifiable defense shipments.24 A single Japanese company, Kyocera, holds over half the world market, and most other significant players are Japanese, so foreign sources are few and concentrated. Kyocera is the largest domestic merchant supplier, but it

|

20 |

SEMATECH received DoD support from its inception in 1987 and recently announced that it would no longer need government support from 1997. |

|

21 |

U.S. Congress, General Accounting Office, Significance of DOD’s Foreign Dependence (Washington, D.C.: U.S. Government Printing Office, 1991), p. 1. |

|

22 |

For example, U.S. Department of Commerce, Office of Industrial Resource Administration, National Security Assessment of the Domestic and Foreign Subcontractor Base: A Study of Three U.S. Navy Weapon Systems (Washington, D.C.: U.S. Department of Commerce, 1992). |

|

23 |

U.S. Department of Commerce, Office of Industrial Resource Administration, The Effect of Imports of Ceramic Semiconductor Packages on the National Security: An Investigation Conducted Under Section 232 of the Trade Expansion Act of 1962 (Springfield, Va.: National Technical Information Service, 1993). |

|

24 |

Ibid., p. ES-5. |

imports critical materials to its U.S. facility.25 Further, Kyocera is clearly uncomfortable about the public relations aspect of supplying packages that are used in weapons systems.

Most of the criteria for evaluating the risks of acute dependence indicate that relying on Japan for ceramic packages represents a relatively high risk. U.S. merchant production of ceramic packages has declined in recent years, as several domestic producers have scaled back production or exited the business, and remaining producers have cut back investment and R&D. In early 1993 two of the remaining domestic producers petitioned the Department of Commerce to conduct an investigation under Section 232 of the Trade Expansion Act of 1962. Although the U.S. government ruled following the investigation that imported ceramic packages do not represent a threat to national security, the weakness of the domestic production base was recognized, and an action program focusing on technology development and manufacturing was instituted in 1993.

Dependence carries two types of long-term risks, both of which are technology-related. The first is that lack of U.S. capabilities in a given critical technology might delay or inhibit incorporation of that technology into new systems. For a number of reasons, foreign sources may be unwilling or unable to supply the United States with the technologies needed for modernization.

The current situation in flat panel display technology serves to illustrate this type of risk. DoD has stated that reliance on commercial technologies must increase in order to lower acquisition costs and because in areas like electronics commercial technology is outstripping advances on the military side. Today, several small specialized U.S. vendors supply DoD’s requirements for flat panel displays. Although these domestic suppliers are technologically sophisticated, U.S. display producers are not present in the high-volume markets, such as laptop computers, that are driving manufacturing technology and cost reductions. DoD officials have stated that it will be necessary to have advance access to prototypes, assured access to customized products utilizing the latest commercial technology, and the benefit of lowered cost that comes from volume production. Japanese manufacturers, the dominant players, have reportedly indicated that they are not willing to work with DoD on its specialized needs.26

In 1994 DoD announced a Flat Panel Display Initiative to help facilitate an expanded U.S. manufacturing and market presence. The initiative has several elements, including core technology funding, R&D support for companies that commit to build production facilities, aggregation of government procurement demand, and interagency monitoring. The total cost over five years is expected to be $587 million.

Some experts have criticized DoD’s approach, saying that the initiative represents a misguided foray into industrial policy that will backfire over the long term.27 The more compelling criticisms revolve around future market entry, the ultimate feasibility of establishing a profitable U.S. production base, and the utility of alternative strategies such as pressing harder on the Japanese government or working with Korean and other non-Japanese companies. The basic questions are whether U.S.-controlled mass production of displays in the United States is a

|

25 |

Ibid., p. VII-2. |

|

26 |

U.S. Department of Defense, Building U.S. Capabilities in Flat Panel Displays (Washington, D.C.: Department of Defense, 1994), p. VII-3. |

|

27 |

These objections are drawn mainly from Claude Barfield, “Flat Panel Displays: A Second Look,” Issues in Science and Technology, Winter 1994-95, pp. 21-21. |

critical enough security need to justify a significant government initiative and whether success is achievable at a reasonable cost.

Although there is insufficient information at this time to answer these questions definitively, and a specific evaluation of DoD’s display initiative is outside the scope of this study, it is possible to examine U.S. policy options toward developing advanced display capabilities in light of the dependence issue. Even if Japanese companies were willing to work with DoD, a number of the criteria for evaluating dependence risks—such as the concentration of suppliers and criticality of the technology—imply a high risk. Significant Korean entry and success would alleviate several of the dependence risk factors, but complete dependence on foreign sources for this technology may be unacceptable from a long-term national security standpoint. Although there is a danger that the DoD initiative will not be enough to ensure adequate U.S. capabilities, at about $115 million annually it is a relatively low-risk program that maintains a technological and business option to develop an industry and which may succeed in stimulating the desired critical mass of manufacturing capability. The initiative is also likely to increase DoD’s leverage with foreign producers, perhaps stimulating investment in U.S. manufacturing.

Dependence on foreign sources raises a final, more diffuse risk to national security—that capabilities lost in one segment will weaken related sectors, leading eventually to a general downgrading of U.S. technological capabilities in a broad industrial area or that broad industry weakness will adversely affect specific supplier segments that are critical to national security. According to one formulation, manufacturing and technological capability in high-value-added industries has an intrinsic worth to a dynamic economy that is greater than the value of output at a given point in time. Some argue that Japanese technology and industrial policies recognize this dynamic better than those of the United States, leading Japan to emphasize indigenization and nurturing of technological capability.28

The trends of the 1970s and 1980s certainly bear out this assertion. For example, loss of U.S. commercial competitiveness in an industry that at first glance appeared to have little security importance —consumer electronics—indeed contributed to the current lack of a U.S. presence in mass production of flat panel displays. The strength of Japanese companies in dynamic random-access memories was leveraged to gain advantages in key areas of semiconductor equipment, such as photolithography. There is some evidence that during the late 1980s individual Japanese companies and production networks utilized practices that are illegal and considered anticompetitive in the U.S. context to pursue their advantage.29 Concerns were raised about Japanese direct investments in U.S.-high technology companies—in some cases the last remaining companies in their segments. It appeared to some that broad dominance in information-related industries was within the reach of the large Japanese electronics companies.

The situation looks somewhat different in 1995. Today, it is clear that closed production networks and markets and the focus on acquisition and improvement of technology at the

|

28 |

Richard J. Samuels, Rich Nation, Strong Army: National Security and the Technological Transformation of Japan (Ithaca, N.Y.: Cornell University Press, 1994). |

|

29 |

“Officials from several government agencies told us that Japanese companies were engaged in tying practices between 1987 and 1989. One agency official stated that his office brought up the issue of tying 9 to 10 times during consultations with the Japanese government and asked the government to encourage Japanese companies to discontinue these practices. This official confirmed that U.S. companies licensed technology to Japanese companies in order to get memory chips.” U.S. Congress, General Accounting Office, International Trade—U.S. Business Access to Certain Foreign State-of-the-Art Technology (Washington, D.C.: U.S. Government Printing Office, 1991), pp. 43-44. |

expense of creating new technology have imposed costs on Japan. For example, if the Japanese computer market had been more open in the 1980s, Japanese companies might have recognized the importance of networked personal computers earlier and adjusted their strategies accordingly. Japan’s dominance in DRAMs and resulting large profits attracted new market competition from Korean firms. As U.S. semiconductor and computer companies focused on higher-value-added products and new technologies, many have been able to grow and even establish strong positions in the Japanese market.

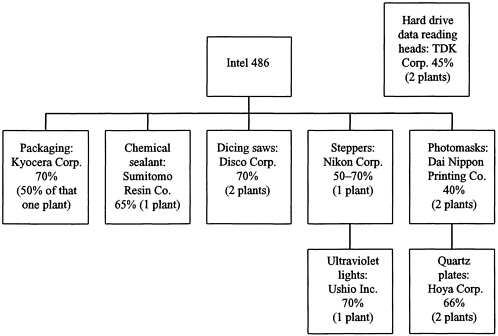

However, Japanese companies remain dominant in many areas of the semiconductor and semiconductor equipment industry (Figure 5-1). In the area of lithography equipment, which is critical for semiconductor manufacturing, U.S. producer GCA was forced to shut down in 1993 despite a successful effort to develop superior technology in partnership with SEMATECH. This case illustrates that even when technology policies are effective other policy measures might be necessary to maintain U.S. capabilities. Dependence on Japan affects U.S. space systems integrators as well. For example, NEC and Fujitsu are the only producers of gallium arsenide field effect transistors, which are critical components in space systems.

FIGURE 5-1 Typical personal computer supply chain dependencies.

SOURCE: George Gilboy, compiled from The Wall Street Journal, August 27, 1993.

Although the rapid erosion of U.S. capabilities in electronics appears to have halted and may even have been reversed in some areas, the United States remains dependent on Japan for a large range of electronics-related technologies and products. It is unreasonable to expect the United States to maintain self-sufficiency in all critical technological areas. The costs of attempting to do so would be staggering. Also, there are advantages to a certain level of interdependence—the United States is able to incorporate advanced foreign technologies into new weapons systems, it may be able to procure components at lower cost, and it can focus resources on potentially more important priorities.

Although some degree of dependence is inevitable, and Japan is likely to remain the most significant source of these dependencies, there are steps that U.S. government and industry can take to effectively manage that dependence and to reduce or eliminate it when necessary for national security purposes. DoD has taken useful steps to subsidize domestic R&D and encourage manufacturing. In the future, more extensive steps might be necessary to ensure a domestic production base in areas where dependence is unacceptable. In areas where dependence on Japan brings substantial benefits with acceptable risks, it might be necessary to pursue specific guarantees from Japanese producers and the Japanese government that U.S. military needs will be met in an emergency.

As for the continuing risk of industrial erosion, DoD’s ability to have a major impact is limited. Several of the most important factors influencing overall economic relations, such as trade policy, fall under the responsibility of other agencies. Still, DoD can actively cooperate with other agencies in preserving critical capabilities and by pursuing more reciprocal technology flows in the context of the security relationship, can contribute to creating an atmosphere of mutually beneficial interdependence.

POSSIBLE FUTURE CHALLENGES IN DUAL-USE AREAS

Through licensed production of U.S. military aircraft, Japan has built a manufacturing and technology base that facilitated participation as a key supplier in the global aircraft manufacturing industry, as discussed in Chapter 4. One important dual-use area to single out for future attention because of Japanese policies and current trends is space.

Space will continue to be an important area for development and application of a wide range of broadly applicable technologies, such as propulsion, materials, optoelectronics, energy storage, and systems integration. Space technology is a field in which the United States has consistently led Japan in nearly all dimensions and applications, and the flow of space-related technology has been exclusively from the United States to Japan. American strength in this area stems from the decades-old commitment to space exploration and exploitation.

However, the Japanese space program has gathered momentum in recent years as Japan has sought to develop commercially viable space-related industries. To that end, “Japan has followed in space the strategy that has been successful in other high-technology areas—identifying the leader in technological capability and learning as much as possible from its accomplishments, then building on that learning to develop a strong indigenous technology base.”30 Commercial licensing, technology transfer, and other cooperative projects have helped Japan develop its

|

30 |

John M. Logsdon, “U.S. - Japanese Space Relations at a Crossroads,” Science, January 17, 1992, p. 294. |

capabilities in space technologies more quickly and less expensively than would have been possible otherwise.

U.S.-Japanese collaboration in space has been extensive. In 1968 the two governments agreed that the United States would support Japan in the development of selected space-related technologies and capabilities. For example, Japan was permitted to manufacture Delta launch vehicles. As a result, it was able to acquire an important technology without making massive investments in research and development. Collaboration progressed throughout the 1970s, with Japan acquiring broadcast, meteorological, and communications satellites and assimilating related technologies through joint manufacturing activities. Japanese industry developed a very strong, internationally competitive position in ground stations for satellite tracking and communications during this period.

In 1984 Japan began to move toward privatizing its communications and broadcasting networks. Although satellite systems had been only a small component of its service networks, Japan decided that full-fledged commercial operating systems should be developed. Satellites and launch services would be required to develop such systems, and U.S. firms sought to be included in the supply of hardware and in owner-operated groups. This became a U.S.-Japan trade issue during the mid and late 1980s. With the help of the U.S. Trade Representative and the Federal Communications Commission, American firms were able to gain access to the developing market.

Today, Japan’s ongoing and planned space programs are “broad, bold and far-reaching in perspective.”31 Its space programs are overseen by the Space Activities Commission, an advisory body to the Prime Minister, coordinated by the Science and Technology Agency, and undertaken by the Institute of Space and Astronautical Science, the National Aerospace Laboratory, and the National Space Development Agency of Japan. U.S.-Japan cooperation in space programs and technologies has continued at the government-to-government level through Japanese participation in the development of the planned Space Station.

There are several issues related to space development in Japan that U.S. industry and government will need to monitor for the future. The first is the technological trajectory of Japanese and other foreign countries in satellite communications, launch capabilities, and underlying technologies. A recent panel that looked at global developments in satellite communications concluded that in this rapidly expanding field U.S. leadership is being challenged.32 Although U.S. firms are still the world leaders in most aspects of commercial space activities, Japan has well-funded, long-range research programs to develop advanced indigenous capabilities in satellites and launch systems. The H-II rocket, for example, is a promising advanced launch system, despite some delays experienced in design and testing.

A second issue is the opportunities that Japan might have in the future for developing space capabilities through addressing security needs. Although Japan currently has restrictions on military uses of space, the recent report of an advisory committee to the Prime Minister calls for Japan to develop a system of reconnaissance satellites. If such satellites are used for observation,

|

31 |

C . L. Merkle, J. R. Brown, J. P. McCarty, G. B. Northam, L. A. Povinelli, M. L. Stangeland, and E. E. Zukoski, JTEC Panel Report on Space and Transatmospheric Propulsion Technology (Loyola, Md.: Japanese Technology Evaluation Center, 1990), p. xi. |

|

32 |

Burton Edelson, Joseph Pelton, Charles W. Bostian, William T. Brandon, Vincent W. S. Chan, E. Paul Hager, Neil R. Helm, Raymond D. Jennings, Robert W. Kwan, Christoph E. Mahle, Edward D. Miller, and Lance Riley, NASA/NSF Panel Report on Satellite Communications Systems and Technology (Baltimore, Md.: International Technology Research Institute, 1993), p. 183. |

perhaps performing disaster prevention and weather functions as well as reconnaissance, and do not direct weapons, it might be possible to deploy such a system within the current Japanese policy framework. Further, Defense Task Force members observed during meetings in Japan in November 1994 that there appears to be strong and fairly broad support for such a system. Finally, in contrast to theater missile defense, where much of the Japanese procurement could go toward buying or licensing American equipment, an indigenous reconnaissance satellite system could advance Japan’s security goals while providing a bigger boost for industry. Security concerns could justify such a system being procured domestically, in contrast to NTT (Nippon Telephone and Telegraph) and other commercial satellite procurements, which now must be open to international competition as a result of U.S.-Japan trade negotiations.

DoD has singled out control of the use of space as one of five key U.S. war fighting needs for the future.33 Maintaining a strong, internationally competitive U.S. space industrial base will be necessary to meet this critical need.34 In addition to Europe, Russia, and China, Japan’s future capabilities in space and underlying technologies have the potential to affect U.S. interests in this area.

|

33 |

DoD, Defense Science and Technology Strategy, op. cit., pp. 6-7. |

|

34 |

Vice President’s Space Policy Advisory Board, The Future of the U.S. Space Industrial Base, 1992. |