A Strategic Assessment

SYMPTOMS OF A SERIOUS NATIONAL PROBLEM

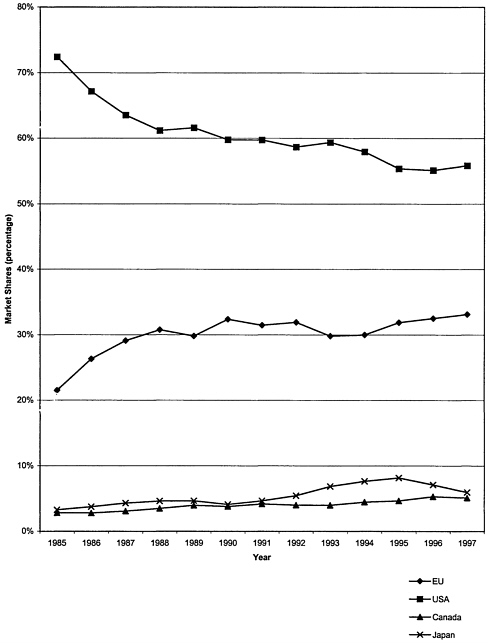

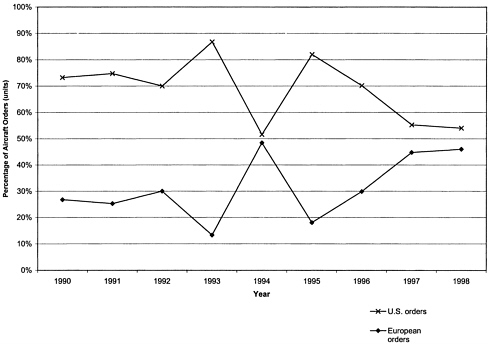

Aeronautical capabilities are important to the U.S. economy, and the committee found evidence that the aeronautics segment of the economy is becoming less competitive. As shown in Figure 1, the U.S. share of world aerospace markets fell from over 70 percent in the mid-1980s to 55 percent in 1997. Figure 2 shows that the United States is losing market share in terms of unit orders in the important category of large commercial transport aircraft to Europe, down from 73 percent in 1990 to 54 percent in 1998.1,2 The demand for smaller regional commercial jet transport aircraft is growing, but the two major suppliers of regional jets, Bombardier and Embraer, are based in foreign countries (Canada and Brazil, respectively). The consequences of the loss in overall market share are disturbing, as discussed below.

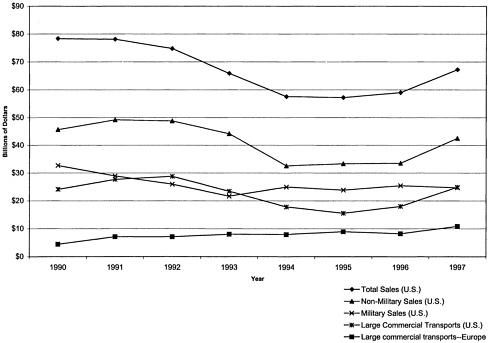

National security is also closely tied to the superiority of U.S. aeronautical capabilities. Comparing market shares in military aircraft procurements, therefore, is less meaningful because economics are, or should be, secondary to national security considerations. Also, as shown in Figure 3, the total U.S. aeronautics sales (deliveries) are largely driven by sales of large commercial transports. Still, it is noteworthy, for example, that although the French Dassault Aviation Rafale fighter aircraft is a generation between our F-15 and F-22, it has been ordered into quantity production, while congressional actions have made the F-22’s future uncertain. Similarly, the Tiger, the Eurocopter (French and German) scout-attack helicopter, can be considered a generation between the U.S. AH-64 Apache and RAH-66 Comanche helicopters; but the first procurement contract for the Tiger has already been signed,3 whereas the Comanche is still in a stretched out development. Recent history shows that military aircraft in domestic production often enjoy sales overseas, which reduces the cost of subsequent domestic procurements.

|

1 |

Competitiveness, as measured by market share, is but one indication of economic health and vitality. Changes in the absolute level of economic activity are also important—and Figure 3 confirms that the absolute level of aeronautical sales has also dropped in the United States during the 1990s. Lowering trends in market share and the absolute level of economic activity, if uncorrected, will naturally lead to the demise of aeronautics as a viable enterprise. Thus, the committee believes that maintaining a competitive industry with a significant market share is important. |

|

2 |

There is usually a lag time of about three years between orders and deliveries. |

|

3 |

Aviation Week and Space Technology. p 28. May 8, 1999. |

FIGURE 1 Market shares of international aerospace manufacturing.

Sources: For 1980 to 1995: Table 9.3, “Final Aerospace Turnover Consolidated at National Level in Current Prices,” The European Aerospace Industry—Trading Position and Figures 1997. For 1996 to 1998: European Association of Aerospace Industries.

FIGURE 3 Aeronautics sales history.

Source: Aerospace Facts and Figures published by the Aerospace Industries Association of America (based on census data adjusted to 1997 dollars) and the Airline Monitor, May 1999. Note: Total sales are for aircraft, aircraft engines, and parts and represents deliveries made. Data on European military sales is not available.

A CLEAR INFLUENCE: TRENDS IN AERONAUTICS R&T

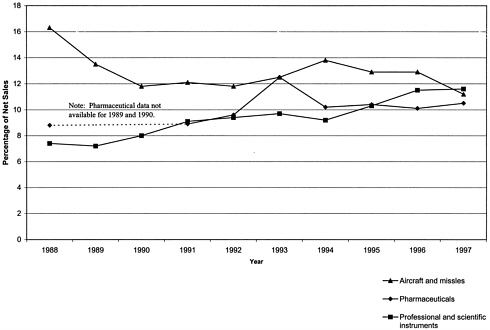

Although a strong national program of aeronautics R&T may not, by itself, ensure the competitiveness of the U.S. aviation industry, the committee agrees with earlier studies4 that without it, the United States is likely to become less competitive in aeronautics relative to countries with stronger programs. Aviation is an R&T-intensive industry. Maintaining a successful, state-of-the-art aeronautics industry has required that a higher percentage of net sales be invested in R&T than other industries associated with rapid innovation and application of scientific advances, such as pharmaceuticals and scientific instruments (Figure 4).5

Some aeronautics R&T programs have produced “breakthroughs” that are immediately usable. NASA’s low-drag cowl for radial engines and “coke-bottle fuselage” to reduce transonic drag rise are examples from the past. In the Department of Defense, more recent aeronautics breakthroughs include shaping for stealth; multi-axis thrust vectoring exhaust nozzles integrated with aircraft flight-control systems; fly-by-wire flight control technologies; high-strength, high-stiffness fiber composite structures; and tilt-wing rotorcraft technology. Many of these advances have been achieved in partnership with NASA R&T programs and are finding widespread use in both military and commercial aircraft.6

More often, aeronautics R&T advances are evolutionary, and a substantial number of years can pass before the aviation systems making use of these advances enter service. Modern aircraft are complex “systems of systems,” and advances in one discipline, such as aerodynamics, may require an advance in another discipline, such as structures, before they can be applied in a new aircraft design. Years of validation, testing, and certification are, therefore, usually required before a new aeronautics R&T development can be exploited.

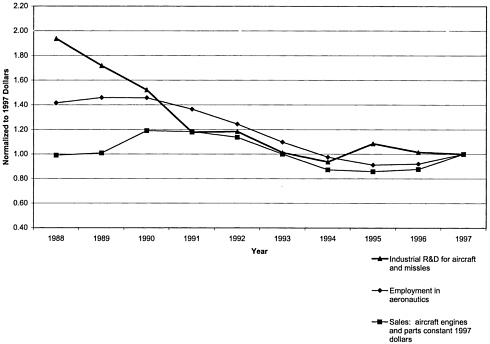

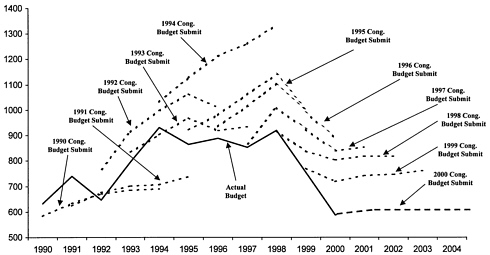

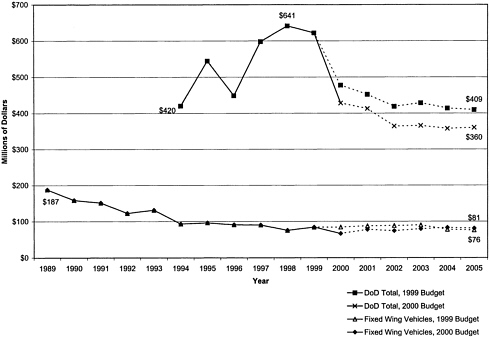

Figure 5 shows that aeronautics R&D funded by U.S. industry dropped by almost 50 percent between 1988 and 1991, followed by reductions in sales and employment. Figure 6 shows that the Administration’s funding requests for NASA aeronautics R&T have been steadily reduced each year since 1994. Figure 7 shows a similar decline in Department of Defense funding for aeronautics R&T. As the two traditional sources of support for aeronautics R&T, industry and government, have been falling in the United States, government support for aerospace R&T in the European Union has been growing (Figure 8).7 This correlates in time with Europe’s increasingly successful economic challenge to the United States in aeronautics.

|

4 |

National Research Council. 1992. Aeronautical Technologies for the 21st Century. Aeronautics and Space Engineering Board. Washington, D.C.: National Academy Press. |

|

5 |

Figure 4, as labeled, shows funding for research and development (R&D), which is quite different than R&T. This report uses R&T to denote basic and applied research and technology demonstration (e.g., “6.1” and “6.2” and “6.3” funding within the Department of Defense), whereas R&D can include all aspects of product development. The focus of this study is R&T. However, in some cases, the committee was unable to obtain data on R&T levels and trends. In those cases, the report relies on data for R&D (as in Figures 4, 5, 6, and 8). Although the R&D data depicted in these figures is not the same as R&T funding, they represent the best data available to the committee and are useful for purposes of trend analysis and comparative studies of R&D among different industries, as shown. Each chart uses one term or the other, and the charts that depict R&D funding are used only to show trends over time or to contrast levels of R&D among different organizations. |

|

6 |

The applicability of many aeronautical technologies to both military and civil aircraft illustrates the dual-use nature of aeronautics R&T, which is discussed further in Appendix A. |

|

7 |

European governments do not release data on how much aeronautics R&T they support, so the committee relied on data for aerospace R&D, which includes aeronautics R&D. |

FIGURE 5 Aeronautics industry trends, 1988–1997.

Sources: Employement and Sales—Aerospace Facts and Figures 98/99, Aerospace Industries Association , and Industiral R&D Early Release Tables, 1997, National Science Foundation.

Note: The industrial R&D data include missles. The other two categories do not. Dollar values converted to constant 1997 dollars. Data then normalized to 1997 values: Employment-1,086,000; Sales-$50.7 billion; Industrial R&D-$24.2 billion

FIGURE 7 Department of Defense aeronautics R&T funding (total and fixed wing vehicles).

Source: W.Borger, Air Force Research Laboratory. Presentation to NRC Committee on Strategic Assessment of U.S. Aeronautics. June 1999. (Data converted to constant 1997 dollars; an inflation factor of 2.3 percent was used for 1998 to 2005.)

LIKELY CONSEQUENCES IF TRENDS ARE NOT REVERSED

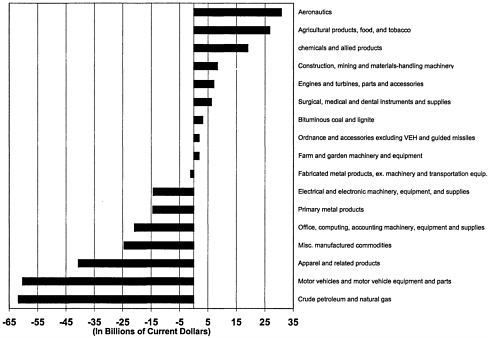

As already noted, a competitive aeronautics industry is important in terms of both national security and economic factors, such as employment and the nation’s balance of trade (Figure 9).

Militarily, a dominant aeronautics capability projects a U.S. global presence and influence as no other technology does, or will do, for the foreseeable future. No other capability allows for the rapid projection of force over long distances or is as flexible in providing combat air support for ground forces. The United States needs a strong aeronautics capability to meet its international commitments and responsibilities in an uncertain and volatile global political environment. This future capability rests solidly on today’s aeronautics R&T investment.

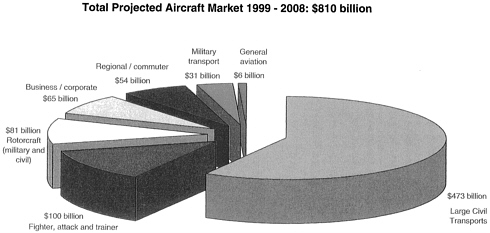

With regard to economic factors, a recent market study (summarized in Figure 10) projects a worldwide civil aircraft market of $810 billion over the period 1999 to 2008. The study showed that large civil transports account for over one-half of this market. The remainder is comprised of regional/corporate airplanes, military airplanes, and civil and military rotorcraft. In addition, $274 billion in gas turbine engine sales are projected over the same period, more than one-half for aviation uses,8 and the projected market for aircraft retrofitting and modernization is $20 billion. In total, the world market for aeronautics products is expected to exceed $1 trillion over the next 10 years, and most of it will be captured by companies (and countries) who have made and continue to make sizeable investments in aeronautics R&T.

The market study cited above provides information only on the primary economic benefits from goods and services associated with aeronautics R&T. Secondary benefits are also accrued. For example, investments in air traffic control systems worldwide are expected to range from $41 to $58 billion.9 Also, the technology to develop efficient gas turbine engines has been used to develop gas turbine engines for other uses, such as ship propulsion and emergency electrical generation in critical buildings. In fact, examples of the general applications of aeronautical technology abound. These secondary benefits not only add to the gross national product, but they also enhance national security, the economy, and the general quality of life.

Government aeronautical test facilities are another area of concern. The construction, maintenance, upgrading, and use of some of the nation’s specialized aeronautical testing facilities, typified by large-scale wind tunnels, are company or university assets, but most have been built and operated by the government—NASA or the U.S. Air Force, for example. Many facilities have been or are being closed down, the U.S. government has backed away from proposals to construct major new facilities, and U.S. aircraft companies are increasingly going overseas to perform wind-tunnel testing of new U.S. designs.10

The committee believes that aeronautics in the United States can ill afford to lose highly educated, motivated engineers and scientists. This core group is essential for advancing the state of the art and developing innovative new generations of vehicles and systems. The knowledge and understanding of aeronautical engineers who have had first-hand experience with flight hardware is lost if it is not passed on—on the job—from one generation of practicing aeronautical engineers to the next. As a result of industry consolidations and the end of the Cold War, the

number of new commercial and military development programs for military and commercial aircraft has been significantly reduced. In this environment, developing experimental aircraft is one approach for maintaining the skills of aircraft designers. Furthermore, in the experience of committee members, the cutting edge of aeronautics R&T is most attractive to young, talented engineers and scientists. Therefore, continued reductions in aeronautics R&T would damage the personnel base required to maintain a robust, competitive aeronautics industry capable of supporting U.S. national security and economic interests.

Although knowledgeable observers may differ in their assessments of the degree of the severity of the consequences, the committee wishes to point out that continued reductions in funding for aeronautics R&T may have irreversible consequences. Once the position of the United States in aeronautics is lost, it will be exceedingly difficult to regain because of the difficulty in reassembling the infrastructure, people, and investment capital.

RECOMMENDATIONS

This committee agrees with the findings of many previous studies:11

-

Aeronautics as an ongoing enterprise is important to national security, the national economy, and the quality of life in the United States.

-

Aeronautics R&T is important to the aeronautics enterprise in the United States.

The committee concluded that consolidations in the aeronautical industry, especially in the airframe development and manufacturing industry, the end of the Cold War, and the increasing globalization of the aircraft industry do not affect the general requirements for facilities and other resources essential to effective aeronautics R&T. In some instances recommendations from the earlier studies have taken on greater urgency. The continuing decline in the U.S. market share for commercial jet transport aircraft, recent regional conflicts, and the Air Force’s decision to devote more of its assets to space developments and operations in an era of declining overall budgets have made the needs for strong support for aeronautics R&T more urgent.

The committee agrees with the conclusion reached by other studies that government funding of aeronautics R&T is worthwhile.12 In particular, the committee endorses the three key goals identified by the National Science and Technology Council:13

-

Maintain the superiority of U.S. aircraft and engines.

-

Improve the safety, efficiency, and cost effectiveness of the global air transportation system.

-

Ensure the long-term environmental compatibility of the aviation system

|

11 |

For example, National Science and Technology Council (NSTC). 1995. Goals for a National Partnership in Aeronautics Research and Technology. Washington, D.C.: Office of Science and Technology Policy. Available on-line at “www.whitehouse.gov/WH/EOP/OSTP/html/aero/cv-ind.html”. |

|

12 |

Ishaq Nadiri. 1993. Innovations and Technological Spillovers. NBER Working Paper Series. Working Paper No. 4423. August, 1993. Also, Edwin Mansfield, J.Rapoport, A.Romeo, S.Wagner, and G.Beardsley. Social and Private Rages of Return from Industrial Innovations. Quarterly Journal of Economics. Vol 77, pp 221–240. 1977. |

|

13 |

NSTC, op cit. |

The committee endorses NASA’s response to these challenges, in which it defined three pillars, supported by 10 technology enabling goals (see Box 1). The second and third goals of the National Science and Technology Council can be considered as broadening the old “higher, farther, faster” pure performance objectives of the past. Where the National Advisory Council for Aeronautics (NACA, the predecessor to NASA) and the military were once the primary federal organizations involved in aeronautics R&T, now the Department of Defense, NASA, the U.S. Department of Transportation (including the Federal Aviation Administration), and the National Science Foundation all have significant R&T programs related to aviation. The focus of each program is determined by each agency’s missions, legislative charter, and annual budget appropriation. The importance of coordination among these agencies is increasingly important for at least three reasons:

-

The result of the overlapping responsibilities arising naturally from greater density of aviation operations and the growing sophistication of flight systems, which are increasingly dependent on electronics, optics, and computers.

-

The burgeoning costs to develop increasingly capable aeronautical systems under the pressure of constrained budgets.

-

The widespread acceptance in the military of “dual-use science and technology” (combining civil and military applications) and commercial-off-the-shelf equipment and systems for military applications. As stated by the National Science and Technology Council, “Nationally we have the infrastructure—government, industry and universities— to maintain leadership. We must now renew our focus on partnership to meet national challenges and accomplish national goals.”14

The committee recommends that major improvements be made in the coordination of aeronautics R&T activities among NASA, the Department of Defense, the Federal Aviation Administration, industry, and academia. An overarching organization for national aeronautics R&T is needed to speak for national values, ensure efficient use of resources, make cooperative actions more productive, and eliminate duplication where it is not an effective motivator of competition. Successful collaborative programs (e.g., AGATE, NRTC, and IHPTET15) should be examined to identify characteristics adaptable to this purpose.16

Aeronautics is an R&T-intensive enterprise. The committee is convinced that continued reductions in government support of aeronautics R&T would jeopardize (1) the ability of the United States to produce preeminent military aircraft and (2) the ability of the aeronautics sector of the U.S. economy to remain globally competitive. A rigorous proof of this conclusion requires detailed military, technical, and economic analyses that the committee was unable to complete during this brief study. However, the committee is greatly concerned that ongoing reductions in R&T, which seem to be motivated primarily by the desire to reduce expenditures in the near term, are taking place without an adequate understanding of the long-term consequences. The committee recommends that the federal government analyze the national security and economic implications of reduced aeronautics R&T funding before the nation discovers that reductions in R&T have inadvertently done severe, long-term damage to its aeronautics interests.

In addition, for the United States to succeed in the globalized world aviation market, the nation requires clearly defined national objectives for aeronautics R&T. These objectives should be established considering our national requirements and how they can best be satisfied with active participation from industry and government developers as well as the military and commercial technology users of aeronautics R&T results. Continuing inputs from these four components are crucial to the implementation of technologies needed to keep the United States militarily secure and globally competitive.

|

BOX 1 NASA’s Aeronautics Goals In March 1997, NASA’s Office of Aeronautics and Space Transportation Technology adopted 10 enabling technology goals to guide pre-competitive research in long-term, high-risk, high-payoff technologies. The goals are in three groups or “pillars”:

Source: Aeronautics and Space Transportation Technology: Three Pillars for Success, NASA Office of Aeronautics and Space Transportation Technology, Washington, D.C., March 1997. |