10

Wealth and Racial Stratification

Melvin L.Oliver and Thomas M.Shapiro

Income is what the average American family uses to reproduce daily existence in the form of shelter, food, clothing, and other necessities. In contrast, wealth is a storehouse of resources, it’s what families own and use to produce income. Wealth signifies a control of financial resources that, when combined with income, provides the means and the opportunity to secure the “good life” in whatever form is needed—education, business, training, justice, health, material comfort, and so on. In this sense, wealth is a special form of money not usually used to purchase milk and shoes or other life necessities; rather it is used to create opportunities, secure a desired stature and standard of living, and pass class status along to one’s children.

Wealth has been a neglected dimension of social science’s concern with the economic and social status of Americans in general and racial minorities in particular. Social scientists have been much more comfortable describing and analyzing occupational, educational, and income distributions than examining the economic bedrock of a capitalist society— “private property.” During the past decade, sociologists and economists have begun to pay more attention to the issue of wealth. The growing concentration of wealth at the top, and the growing racial wealth gap, have become important public-policy issues that undergird many political debates but, unfortunately, not many policy discussions. Our work takes up this challenge. This paper begins with a summary of the social science findings on race and wealth. The data are strongest regarding

Black-White differences, but reference is made to findings and data that refer to Hispanics, Asians, and American Indians as well.

This paper focuses on three key contributions. First, an indispensable contribution to the current understanding of racial stratification is an examination of wealth, distinct from labor-market indicators, which this paper offers. Second, the paper makes an evidentiary contribution to the theory that current racial trends in inequality result, to a significant extent, from past racial policies and practices; and that the racial inequality of today, if left unattended, will contribute to continued racial stratification for the next generation. Third, by looking at new evidence concerning wealth and racial stratification, this paper contributes an impetus to push forward the research and policy agenda concerned with America’s racial wealth gap. Thus, a wealth perspective provides a fresh way to examine the “playing field.” Consequently, a standard part of the American credo—that similar accomplishments result in roughly equal rewards—may need reexamination.

RACIAL STRATIFICATION AND THE ASSET PERSPECTIVE

Understanding racial inequality, with respect to the distribution of power, economic resources, and life chances, is a prime concern of the social sciences. Most empirical research on racial inequality has focused on the economic dimension, which is not surprising considering the centrality of this component for life chances and well-being in an industrial society. The concerted emphasis of this economic component has been labor-market processes and their outcomes, especially earnings, occupational prestige, and social mobility. Until recently, the social sciences and the policy arena neglected wealth, intergenerational transfers, and policy processes that result in differential life chances based on racial criteria. Our ongoing work attempts to redress this severe imbalance.

The data and the social science understanding are strongest for income inequality in relation to race. For most, income is a quintessential labor-market outcome indicator. It refers to a flow of resources over time, representing the value of labor in the contemporary labor market and the value of social assistance and pensions. As such, income is a tidy and valuable gauge of the state of present economic inequality. Indeed, a strong case can be made that reducing racial discrimination in the labor market has resulted in increasing the income of racial minorities and, thus, narrowing the hourly wage gap between minorities and Whites. The command of resources that wealth entails, however, is more encompassing than income or education, and closer in meaning and theoretical significance to the traditional connotation of economic well-being and access

to life chances as depicted in the classic conceptualizations of Marx, Weber, Simmel, and Tawney.1

As important is the fact that wealth taps not only contemporary resources, but also material assets that have historic origins and future implications. Private wealth thus captures inequality that is the product of the past, often passed down from generation to generation. Conceptualizing racial inequality through wealth revolutionizes the concept of the nature and magnitude of inequality, and of whether it is decreasing or increasing. Although most recent analyses have concluded that contemporary class-based factors are most important in understanding the sources of continuing racial inequality, a focus on wealth sheds light on both the historical and the contemporary impacts not only of class but also of race. Income is an important indicator of racial inequality; wealth allows an examination of racial stratification.

A wealth perspective contends that continued neglect of wealth as a dimension of racial stratification will result in a seriously underestimated racial inequality. Tragically, policies based solely on narrow differences in labor-market factors will fail to close that breach. Taken together, however, asset-building and labor-market approaches open new windows of opportunity.

HISTORICAL TRENDS AND CONTEXT OF WEALTH DISTRIBUTION IN THE UNITED STATES

Wealth inequality is today, and always has been, more extreme than income inequality. Wealth inequality is more lopsided in the United States than in Europe. Recent trends in asset ownership do not alleviate inequality concerns or issues. In general, inequality in asset ownership in the United States between the bottom and top of the distribution domain has been growing. Wealth inequality was at a 60-year high in 1989, with the top 1 percent of U.S. citizens controlling 39 percent of total U.S. household wealth. The richest 1 percent owned 48 percent of the total. These themes have been amply described in the work of Wolff (1994, 1996a, 1996b). Household wealth inequality increased sharply between 1983 and 1989. There was a modest attenuation in 1992, but the level of wealth concentration was still greater in 1992 than in 1983.

Until recently, few analyses looked at racial differences in wealth

holding. Recent work, however, suggests that inequality is as pronounced—or more pronounced—between racial and ethnic groups in the dimension of wealth than income. The case of Blacks is paradigmatic of this inequality. Eller and Fraser (1995) report that Blacks had only 9.7 percent of the median net worth (all assets minus liabilities) of Whites in 1993 ($4,418 compared to $45,740); in contrast, their comparable figure for median family income was 62 percent of White income. Using 1988 data from the same source, Oliver and Shapiro (1995a) established that these differences are not the result of social-class factors. Even among the Black middle class, levels of net worth and net financial assets (all assets minus liabilities excluding home and vehicle equity) are drastically lower than for Whites. The comparable ratio of net worth for college-educated Blacks is only 0.24; even for two-income Black couples, the ratio is just 0.37. Clearly there are factors other than what we understand as “class” that led to these low levels of asset accumulation.

Black Wealth/White Wealth (Oliver and Shapiro, 1995a) decomposed the results of a regression analysis to give Blacks and Whites the same level of income, human capital, demographic, family, and other characteristics. The rationale for this was to examine the extent to which the huge racial wealth gap was a product of other differences between Whites and Blacks. Given the skewness of the wealth distribution, researchers agree that median figures best represent a typical American family; however, it should be noted, that regressions conventionally use means. A potent $43,143 difference in mean net worth remains, with 71 percent of the difference left unexplained. Only about 25 percent of the difference in net financial assets is explained. Taking the average Black household and endowing it with the same income, age, occupational, educational, and other attributes as the average White household still leaves a $25,794 racial gap in mean net financial assets. These residual gaps should not be cast wholly to racial dynamics; nonetheless, the regression analyses offer a powerful argument to directly link race in the American experience to the wealth-creation process.

As important is the finding that more than two-thirds of Blacks have no net financial assets, compared to less than one-third of Whites. This near absence of assets has extreme consequences for the economic and social well-being of the Black community, and of the ability of families to plan for future social mobility. If the average Black household were to lose an income stream, the family would not be able to support itself without access to public support. At their current levels of net financial assets, nearly 80 percent of Black families would not be able to survive at poverty-level consumption for three months. Comparable figures for Whites—although large in their own right—are one-half that of Blacks. Thinking about the social welfare of children, these figures take on more

urgency. Nine out of ten Black children live in households that have less than three months of poverty-level net financial assets; nearly two-thirds live in households with zero or negative net financial assets (Oliver and Shapiro, 1989, 1990, 1995a, 1995b).

Because home ownership plays such a large role in the wealth portfolios of American families, it is a prime source of the differences between Black and White net worth. Home ownership rates for Blacks are 20 percent lower than rates for Whites; hence, Blacks possess less of this important source of equity. Discrimination in the process of securing home ownership plays a significant role in how assets are generated and accumulated. The reality of residential segregation also plays an important role in the way home ownership figures in the wealth portfolio of Blacks. Because Blacks live, for the most part, in segregated areas, the value of their homes is less, demand for them is less, and thus their equity is less (Oliver and Shapiro, 1995b; Massey and Denton, 1994). (Because the area of home ownership is so central to the wealth accumulation process, the most current data will be analyzed in a later section of this paper.)

Similar findings on gross differences between Hispanics and Whites also have been uncovered (Eller and Fraser, 1995; Flippen and Tienda, 1997; OToole, 1998; Grant, 2000). Hispanics have slightly higher, but not statistically different, net worth figures than Blacks, based on the 1993 Survey of Income and Program Participation (SIPP); however, these findings are not sufficiently nuanced to capture the diversity of the Hispanic population. Data from the Los Angeles Survey of Urban Inequality show substantial differences in assets and net financial assets between recent immigrants who are primarily from Mexico and Central America and U.S.-born Hispanics (Grant, 2000).

Likewise, place of birth and regional differences among Hispanic groups also complicate a straightforward interpretation of this national-level finding. For example, Cuban Americans, we would hypothesize, have net worth figures comparable to Whites because of their dominance in an ethnic economy in which they own small and medium-sized businesses (Portes and Rumbaut, 1990). They have a far different set of economic life chances than Blacks and other recent Hispanic immigrants by way of their more significant wealth accumulation. For recent Hispanic immigrants, these figures suggest real vulnerability for the economic security of their households and children.

Finally, it is important to point out findings by Flippen and Tienda (1997) that attempt to explain the Black-White and Hispanic-White gap in wealth. Substituting White means for all the variables in a complex Tobit model, Flippen and Tienda found that the model “reduces asset inequality more for Hispanics than for Blacks.” This is particularly the case for housing equity; for Hispanics, mean substitution reduced the gap by 80

percent, compared to only 62 percent for Blacks. As Flippen and Tienda note, “This suggests the importance of residential segregation and discrimination in the housing and lending market in hindering the accumulation of housing assets for Black households” (1997:18). Although their findings for Hispanics may be true for “White Hispanics,” they may not apply to Black Puerto Ricans, who share social space with non-Hispanic Blacks and, therefore, may also be targeted for institutionalized racism in housing markets and financial institutions. Preliminary data from the Greater Boston Social Survey suggest that Hispanics in that region, the majority of whom are Puerto Rican, have even lower levels of net worth and financial assets than Blacks (OToole, 1998).

The case of Asians is quite similar to that for Hispanics, in that it is necessary to be mindful of their diversity, in terms of both national origin and immigrant status. Changes in immigration rules have favored those who bring assets into the country over those without assets; as a consequence, recent immigrants, from Korea, for example, are primarily individuals and families with assets, and once they arrive, they convert these assets into other asset-producing activities—e.g., small businesses. Bates’ (1998) analysis of SIPP points out that Koreans who started businesses had significant assets and were able to use those assets to secure loans for business startups. Data from Los Angeles again underscore the importance of immigrant status and place of birth. U.S.-born Asians have both net worth and net financial assets approaching those of White Los Angelenos; foreign-born Asians, however, report lower wealth than U.S.-born Asians but higher wealth than all other ethnic and racial groups (Grant, 2000).

American Indians form a unique case when it comes to assets. They are asset rich but control little of these assets. Most Indian assets are held in tribal or individual Indian trust (Office of Trust Responsibilities, 1995). Thus, any accounting of the assets of individual Indian households is nearly impossible to calculate, given their small population and these “hidden” assets.

The dearth of studies of wealth in the United States has hampered efforts to develop both wealth theory and information. For more than 100 years, the prime sources concerning wealth status came from estate tax records, biographies of the super rich, various listings of the wealthiest, and like sources. In other words, something was known about those who possessed abundant amounts of wealth, but virtually nothing was known about the wealth status of average American families. During the 1980s, several data sources were developed based on field surveys of the American population. Most notable are SIPP, the Panel Study of Income Dynamics (PSID), the Federal Reserve Board’s Survey of Consumer Finances (SCF), and the Health and Retirement Study (HRS). Thus, it is only rela-

tively recently that any data at all were available to characterize the asset well-being of American families.

RACE, INCOME, AND WEALTH

The empirical presentation begins with a fundamental examination of the most current income and wealth data for Whites, Blacks, Hispanics, and Asians. The data displayed in Table 10–1 are taken from the 1993 SIPP, Wave 7. Drawing attention first to income comparisons, the household income ratio of Blacks, compared to Whites, is 0.61:1, and the Hispanic ratio, 0.67:1. Asians fare considerably better in this comparison, earning close to 125 percent of White income. (It is important, here, to mind the caution from the literature review: the Hispanic and Asian data are aggregated, subsuming important dimensions of country of origin and immigrant status.) These income comparisons closely match other national data and provide an effective indicator of current racial and ethnic material inequality. Changing the lens of analysis to wealth dramatically shifts the perspective. Black families possess only 14 cents for every dollar of wealth (median net worth) held by White families. The issue is no longer how to think about closing the gap from 0.61 but how to think about going from 14 cents on the dollar to something approaching parity. Nearly half of all Black families do not possess any net financial assets, compared to $7,400 for the average White family. These figures represent some asset accumulation for both Whites and Blacks between 1988 and 1994; nonetheless, the wealth perspective reveals an economic fragility for the entire American population, as it demonstrates the continuing racial wealth gap.

TABLE 10–1 Income, Wealth, Race, and Ethnicity: 1994

|

|

Median Income |

Median NWa |

Mean NW |

Median NFAb |

Mean NFA |

|

White |

$33,600 |

$52,944 |

$109,511 |

$7,400 |

$56,199 |

|

Black |

$20,508 |

$6,127 |

$28,643 |

$100 |

$7,611 |

|

Ratio to White |

0.61 |

0.12 |

0.26 |

0.01 |

0.14 |

|

Hispanic |

$22,644 |

$6,723 |

$40,033 |

$300 |

$15,709 |

|

Ratio to White |

0.67 |

0.13 |

0.37 |

0.03 |

0.27 |

|

Asian |

$40,998 |

$39,846 |

$117,916 |

$4,898 |

$57,782 |

|

Ratio to White |

1.22 |

0.67 |

1.02 |

0.51 |

0.98 |

|

aNet worth bNet financial assets. SOURCE: 1993 SIPP, Wave 7. |

|||||

The data for Hispanics resemble the Black-White comparisons in one important respect and diverge in another. The median figures for both net worth and net financial assets reveal similar gaps in comparison with Whites, but the mean figures for net worth and net financial assets bump Hispanics “ahead” of Blacks. This apparent peculiarity most likely illustrates differences in experiences, country of origin, and immigrant status referred to earlier.

Mindful that the Asian data also are grouped, the figures for Asian wealth show an even more exaggerated pattern. The median-wealth figures indicate that Asians possess about three-quarters of the net worth and two-thirds of the net financial assets that Whites own. Commentators could seize on this piece of the story, noting that Asian family income is greater than Whites’, and wonder why the wealth gap exists. An examination of mean wealth figures proves this exercise unnecessary—indeed, the data indicate parity in wealth between White and Asian families. Like the Hispanic data, but to an even greater extent, the Asian aggregate data mask different historical immigrant experiences, country of origin, and immigration status. The divergence between median and mean figures also most likely indicates that a sizable portion of the Asian community is relatively well off alongside a sizable portion of the community whose asset resources are far less than the average White family’s. In other words, in parts of the Asian community, the wealth resources more closely resemble Black and Hispanic wealth profiles, while some segments of the Asian community virtually mirror the White profile.

These data provide a baseline of information regarding racial and ethnic differences in income and wealth resources. Not only do they update previous analyses in a simple way, they also bolster the previous findings. More important, the wealth data consistently indicate a far greater chasm in and pattern of racial and ethnic inequality than when income alone is examined.

INCOME AND WEALTH

A starting point for building on the basic analysis is a further examination of the connection between income and wealth. One leading economic perspective contends that the racial wealth gap predominantly results from income inequality. Do differences in income explain nearly all the racial differences in wealth? If so, then policies need to continue a primarily labor-market orientation that further narrows income inequality. If not, however, then social policy must address dynamics outside the labor market as well as income-generating, labor-market dynamics. Thus, it is critically important to address whether the wealth of Blacks is similar to Whites with similar incomes.

The strong income-wealth relationship is recognized in previous analysis of the 1984 SIPP data. Black Wealth/White Wealth (Oliver and Shapiro, 1995a) identified income as a significant variable determining wealth accumulation, next only to age in the wealth regressions. Looking at wealth by income ranges, however, showed that a powerful racial wealth gap remained. A regression analysis similarly indicated a highly significant differential wealth return to Whites and Blacks from income. The idea that wealth is quite similar when controlling for income, nonetheless, still holds some currency; so a direct empirical examination that uses the most recently available data should provide some evidence of, and resolution of, this issue. An empirical examination can be done in two ways.

The first way to address this issue can be demonstrated by using the data in Table 10–2, which show median measured net worth and net financial assets by income quintile, race, and Hispanic origin. White households in every income quintile had significantly higher levels of median wealth than Black and Hispanic households in the same income quintiles. In the lowest quintile, the median net worth for White households was $17,066, while that of Black and Hispanic households was $2,500 and $1,298, respectively. For the highest quintile households, median net worth for White households was $133,607; significantly lower was the median for Black households, $43,806. The median net financial assets data are just as revealing. At the middle quintile, for example, the median net financial assets for White households were $6,800, which was markedly higher than for Black ($800) and Hispanic ($1,000) households.

It is important to observe that controlling for income in this manner does, indeed, significantly lessen the Black-White/Hispanic-White wealth ratios. The overall median Black-White net worth ratio was 0.14:1, but this narrows when comparing White and Black households in similar income quintiles. The gap, as expressed in ratios, stays about the same for the two lowest income quintiles but narrows to 0.3:1, 0.45:1, and 0.33:1 for the next three income quintiles. In brief, as shown by this comparative procedure, controlling for income narrows the gap; but a significantly large gap persists, even when incomes are roughly equal. This evidence does not support the proposition that Whites and Blacks at similar income levels possess similar wealth.

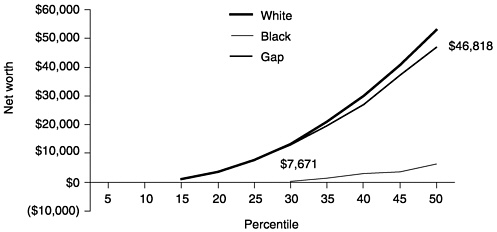

Another way to address the income and wealth connection is to examine wealth at precisely similar income points for Whites and Blacks. Net worth for Whites and Blacks is examined first at distribution percentiles—i.e., leaving income uncontrolled. Figures 10–1 and 10–2, drawn from 1994 SIPP data, show that median White wealth totaled $7,671 and Black wealth totaled $0 at the 25th percentile of each distribution. At the 50th percentile, White net worth was $52,944, compared with $6,126 for Blacks.

TABLE 10–2 Wealth by Race and Hispanic Origin and Income Quintiles: 1994

|

|

Total |

White |

Black |

Hispanic |

||||

|

|

NWa |

NFAb |

NW |

NFA |

NW |

NFA |

NW |

NFA |

|

All households |

||||||||

|

Median |

$40,172 |

|

$52,944 |

$7,400 |

$7,400 |

$100 |

$ 6,723 |

$ 300 |

|

Ratio to white: |

|

0.14 |

|

0.13 |

|

|||

|

Lowest income quintile |

||||||||

|

Median |

8,032 |

185 |

17,066 |

551 |

2,500 |

|

1,298 |

0 |

|

Ratio to white: |

0.15 |

|

0.08 |

|

||||

|

Second income quintile |

||||||||

|

Median |

27,638 |

1,848 |

39,908 |

3,599 |

6,879 |

249 |

5,250 |

250 |

|

Ratio to white: |

0.17 |

0.07 |

0.13 |

0.07 |

||||

|

Third income quintile |

||||||||

|

Median |

40,665 |

4,599 |

50,350 |

6,800 |

14,902 |

800 |

12,555 |

1,000 |

|

Ratio to white: |

0.30 |

0.12 |

0.25 |

0.15 |

||||

|

Fourth income quintile |

||||||||

|

Median |

59,599 |

10,339 |

65,998 |

13,362 |

29,851 |

2,699 |

26,328 |

2,125 |

|

Ratio to white: |

0.45 |

0.20 |

0.4 |

0.16 |

||||

|

Highest income quintile |

||||||||

|

Median |

126,923 |

36,851 |

133,607 |

40,465 |

43,806 |

7,448 |

91,102 |

11,485 |

|

Ratio to white: |

0.33 |

0.18 |

0.68 |

0.28 |

||||

|

aNet worth. bNet financial assets. SOURCE: 1993 SIPP, Wave 7. |

||||||||

FIGURE 10–1 Wealth gap in 1994 with no control of income: $0–$60,000.

SOURCE: 1993 SIPP, Wave 7.

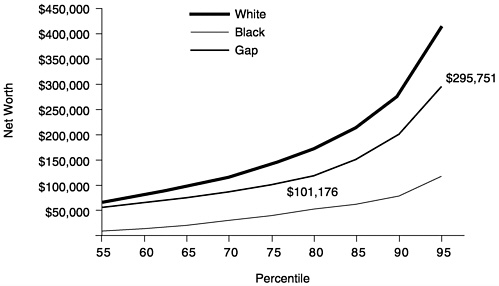

FIGURE 10–2 Wealth gap in 1994 with no control of income: $0–$450,000.

SOURCE: 1993 SIPP, Wave 7.

At the 75th percentile, White net worth was $141,491 versus $40,315 for Blacks. How much of this gap is closed by controlling for income? Will Black-White wealth become actually quite similar, or will substantial, dramatic racial wealth inequality persist? At stake here is a test of two contending claims—(1) wealth inequality fundamentally derives from income

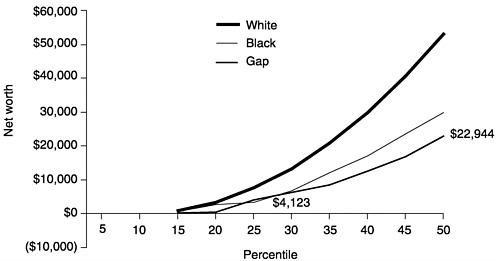

inequality versus (2) wealth inequality derives from accumulations within historically and racially structured contexts. The claim is that Black wealth would be near parity with Whites’ if incomes were equal; therefore, the logic is to compare net worth while controlling for income. Calibrating the White-to-Black income distributions means, for example, comparing the 25th percentile of the White wealth data to the 45th percentile of the Black distribution, the 50th White to the 70th Black, and the 75th White to the 88th Black.

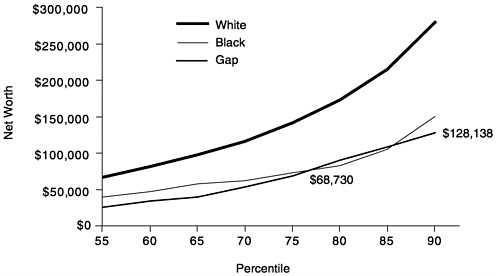

Figures 10–3 and 10–4 graph this income-wealth relationship. A summary that captures some major data points should guide any interpretation. At the 25th percentile for Whites, median net worth is $7,671; controlling for income, the Black net worth adjusts upward to $3,548. At the 50th percentile for Whites, net worth is $52,944, compared to $30,000 for Blacks earning equivalent incomes. At the 75th percentile for Whites, wealth stands at $141,491 versus $72,761 for Blacks.

At the 50th percentile, then, the original uncontrolled gap weighs in at $46,817 with a ratio of 0.12:1. Controlling for income reduces this gap to $22,944. The Black/White wealth ratio closes as well to 0.57. Let us be clear: controlling for income significantly reduces the wealth gap; at the same time, however, even if incomes are equal, a consequential racial wealth gap remains. Indeed, after controlling for income, it is prudent to note that the remaining wealth gap is about as large as the racial income inequality gap. So if this exercise is correct, something akin to the original racial income gap remains unexplained after equalizing incomes.

FIGURE 10–3 Wealth gap in 1994 controlled for income: $0–$60,000. SOURCE: 1993 SIPP, Wave 7.

FIGURE 10–4 Wealth gap in 1994 controlled for income: $0–$300,000. SOURCE: 1993 SIPP, Wave 7.

RACIAL STRATIFICATION BY AGE COHORTS

The social science analysis of wealth is still, at this point, in its beginning stages. Particularly hampering progress, thus far, is the general lack of longitudinal analysis, which is critically important in examining the dynamics of family wealth accumulation over time. We know, for example, that Blacks start far behind Whites in accumulation of asset resources, but does this gap close or widen throughout the life course? Does it reflect the pattern of income, or does it provide evidence of a social process that is more independent of income and savings? We know from cross-sectional analyses, for example, that the racial wealth gap is increasing; but we do not yet know what is happening for the same cohort of families over long periods of time. PSID allows for longitudinal tracking of a family’s economic resources across the life course; however, PSID has only been collecting detailed data on family asset and liabilities since 1984. Every five years this information is brought up to date; 1994 is the latest year these data were gathered. Thus, PSID opens a 10-year longitudinal window for tracking family asset resources.

Following family income and wealth by age cohorts from 1984 to 1994 produces some engaging results. As shown in Table 10–3, the Black-White income gap increases for the two younger age cohorts and decreases for the two older ones. Among Whites, retirement from the labor force, and the resulting decrease in income, is a likely contributor to the sizeable gap decrease during the last five-year period in the oldest cohorts. For all

TABLE 10–3 Income Gap and Age Cohorts

|

|

Income Gap (adjusted, 1994=100) |

||

|

Age cohort 1 |

|||

|

20–29 in 1984 |

$14,468 |

base |

|

|

25–34 in 1989 |

$21,072 |

increase |

$6,604 |

|

30–39 in 1994 |

$18,850 |

decrease |

($2,222) |

|

1984–1994 gap |

|

increase |

$4,382 |

|

Age cohort 2 |

|||

|

30–39 in 1984 |

$20,253 |

base |

|

|

35–44 in 1989 |

$24,131 |

increase |

$3,878 |

|

40–49 in 1994 |

$21,207 |

decrease |

($2,924) |

|

1984–1994 gap |

|

increase |

$954 |

|

Age cohort 3 |

|||

|

40–49 in 1984 |

$21,634 |

base |

|

|

45–54 in 1989 |

$30,692 |

increase |

$9,058 |

|

50–59 in 1994 |

$20,433 |

decrease |

($10,259) |

|

1984–1994 gap |

|

decrease |

($1,201) |

|

Age cohort 4 |

|||

|

50–59 in 1984 |

$25,894 |

base |

|

|

55–64 in 1989 |

$24,202 |

decrease |

($1,692) |

|

60–69 in 1994 |

$13,129 |

decrease |

($11,073) |

|

1984–1994 gap |

|

decrease |

($12,765) |

|

SOURCE: PSID. |

|||

cohorts, the income gap narrowed between 1989 and 1994. If the oldest cohort is excluded, the changes are quite moderate and no distinguishable pattern emerges. The income gap for the youngest age cohort, those 20 to 29 years old in 1984, widens by $4,382, starting at a base inequality of $14,468 and increasing to $18,850 by the time they reach 30 to 39 years old. The racial income gap increased slightly, $954, for the next oldest cohort; and the gap decreased by $1,201 for the next cohort. The income action is hardly startling.

The racial wealth gap is another story. In Table 10–4, the racial wealth gap increases at every marker for all age cohorts; and it does so systematically and spectacularly. The net worth gap for the youngest age cohort begins at $8,733 and increases $23,926 in the 10-year period. Among those age 40 to 49 in 1984, the base net worth wealth gap is a hefty $70,290 and increases to $107,000 in just 10 years. In the 10-year period, then, the income gap for this age cohort actually narrows by $1,201, although the wealth gap widens by more than $36,710. The decrease in the income gap

TABLE 10–4 Net Worth Gap and Age Cohorts

|

|

Net Worth Gap (adjusted 1994=100) |

||

|

Age cohort 1 |

|||

|

20–29 in 1984 |

$8,733 |

base |

|

|

25–34 in 1989 |

$18,585 |

increase |

$9,852 |

|

30–39 in 1994 |

$31,900 |

increase |

$13,315 |

|

1984–1994 gap |

|

increase |

$23,167 |

|

Age cohort 2 |

|||

|

30–39 in 1984 |

$42,174 |

base |

|

|

35–44 in 1989 |

$61,095 |

increase |

$18,921 |

|

40–49 in 1994 |

$63,360 |

increase |

$2,265 |

|

1984–1994 gap |

|

increase |

$21,186 |

|

Age cohort 3 |

|||

|

40–49 in 1984 |

$70,290 |

base |

|

|

45–54 in 1989 |

$78,677 |

increase |

$8,387 |

|

50–59 in 1994 |

$107,000 |

increase |

$28,323 |

|

1984–1994 gap |

|

increase |

$36,710 |

|

Age cohort 4 |

|||

|

50–59 in 1984 |

$100,501 |

base |

|

|

55–64 in 1989 |

$127,381 |

increase |

$26,880 |

|

60–69 in 1994 |

$126,005 |

decrease |

($1,376) |

|

1984–1994 gap |

|

increase |

$25,504 |

|

SOURCE: PSID. |

|||

is notable in its own right, but the magnitude of the increasing wealth gap is cause for concern.

The net financial assets data in Table 10–5 are just as revealing; they show the financial asset gap increasing at least twofold for three of the age cohorts. The gap for the oldest age cohort increases “only” by $17,532 between 1984 and 1994. For the younger cohorts, the irony is that in absolute terms the Black wealth data reveal steady but modest improvement in absolute life chances against a background of dramatically ratcheted-up Black-White wealth inequality. In this sense, life chances improve modestly, while inequality grows rapidly. A notable exception in even the humble improvement in life chances is seen in decreasing liquid assets for the oldest Black cohort. In sum, tracking resource data by age cohorts across a 10-year window provides more empirical evidence that important parts of the wealth-accumulation process are not governed by income dynamics. As White and Black families traverse the American life course, the differential opportunities afforded by increasingly dispar-

TABLE 10–5 Net Financial Assets and Age Cohorts

|

|

Net Financial Assets (adjusted, 1994=100) |

||

|

Age cohort 1 |

|||

|

20–29 in 1984 |

$6,068 |

base |

|

|

25–34 in 1989 |

$9,556 |

increase |

$3,488 |

|

30–39 in 1994 |

$14,000 |

increase |

$4,444 |

|

1984–1994 gap |

|

increase |

$7,932 |

|

Age cohort 2 |

|||

|

30–39 in 1984 |

$13,064 |

base |

|

|

35–44 in 1989 |

$23,895 |

increase |

$10,831 |

|

40–49 in 1994 |

$29,750 |

increase |

$5,855 |

|

1984–1994 gap |

|

increase |

$16,686 |

|

Age cohort 3 |

|||

|

40–49 in 1984 |

$25,205 |

base |

|

|

45–54 in 1989 |

$41,890 |

increase |

$16,685 |

|

50–59 in 1994 |

$58,000 |

increase |

$16,110 |

|

1984–1994 gap |

|

increase |

$32,795 |

|

Age cohort 4 |

|||

|

50–59 in 1984 |

$39,618 |

base |

|

|

55–64 in 1989 |

$61,522 |

increase |

$21,904 |

|

60–69 in 1994 |

$57,150 |

decrease |

($4,372) |

|

1984–1994 gap |

|

increase |

$17,532 |

|

SOURCE: PSID. |

|||

ate financial resources continue to compound racial inequality. This process is a good illustration of the sedimentation of inequality.

UNDERSTANDING THE TRENDS

A review of the literature, and the findings thus far, point to several important considerations. First, racial differences are important in terms of wealth. In the case of Blacks, for whom there is the most clear-cut data, it is obvious that racial factors are implicit in these findings. Second, national origin and immigration status may explain a great deal of the differences among Hispanic and Asian groups; but this is a key area of research that needs to be explored further. Third, American Indians pose a different set of challenges for understanding wealth accumulation because the Indian community has significant wealth in terms of land and

assets, but those assets are under federal government control. The public policies needed to address economic inequality for American Indians would require a legal solution.

The analytical power derived from examining racial stratification through the lens of wealth is most obvious in the case of Blacks. How do we explain the sources of the enormous racial wealth disparity? By focusing on a sociology of wealth that situates the social context in which wealth generation occurs, it is clear that a significant part of this difference is explained by the unique and diverse social circumstances that Blacks and Whites face. Blacks and Whites face different structures of investment opportunity, which have been affected historically and contemporaneously by both class and race. Three concepts can be used to provide a sociologically grounded approach to understanding racial differences in wealth accumulation. These concepts highlight the ways in which this opportunity structure has disadvantaged Blacks and helped contribute to massive wealth inequalities between the races in America.

The first concept, “racialization of state policy,” refers to how state policy has impaired the ability of many Blacks to accumulate wealth— and discouraged them from doing so—from the beginning of slavery throughout American history. From the first codified decision to enslave Blacks, to the local ordinances that barred Blacks from certain occupations, to the welfare-state policies of the recent past that discouraged wealth accumulation, the state has erected major barriers to Black economic self-sufficiency. In particular, state policy has structured the context within which it has been possible to acquire land, build community, and generate wealth. Historically, policies and actions of the U.S. government have promoted homesteading (Oubre, 1978), land acquisition, home ownership (Jackson, 1985), retirement, pensions (Quadagno, 1994), education (National Research Council, 1989), and asset accumulation (Oliver and Shapiro, 1995a; Sherraden, 1991) for some sectors of the population and not for others. Poor people—Blacks in particular—generally have been excluded from participation in state-sponsored opportunities. In this way, the distinctive relationship between Whites and Blacks has been woven into the fabric of state actions. The modern welfare state has racialized citizenship, social organization, and economic status, while consigning Blacks to a relentlessly impoverished and subordinated position within it (Mink, 1990).

One of the key policies of the federal government that encourages home ownership is the deductibility of mortgage interest on homes (a companion is the deferral of capital gains on the sale of principal residences). The state subsidizes home ownership by allowing the marginal tax rate to be deducted from a family’s income taxes. Housing policies that encourage ownership are a part of the “hidden” welfare state that

cost the federal government about $94 billion in fiscal expenditures (Howard, 1997). Home ownership may very well be sound social policy, but it is an uneven process that clearly benefits some groups over others (Jackman and Jackman, 1980; Ong and Grigsby, 1988). Howard (1997) calculates that 88 percent of this “hidden” welfare goes to families earning more than $50,000, with 44 percent accruing to those earning more than $100,000. This class bias has clear racial ramifications as well. Only 1.2 percent of Black families earn enough to qualify for 44 percent of the mortgage interest deduction benefits, compared to 6.6 percent of White families.

The second concept, the “economic detour,” helps explain the relatively low level of entrepreneurship among, and the small scale of the businesses owned by, Black Americans. Although Blacks have traditionally sought out opportunities for self-employment, they have faced an environment, especially from the postbellum period to the middle of the twentieth century, in which they were restricted by law from participation in business as free economic agents (Butler, 1991). These policies had a devastating impact on the ability of Blacks to build and maintain successful enterprises—the kind that anchor communities and spur economic development. Not only were Blacks limited to a restricted Black market, to which others also had easy access, but they were unable to tap the more lucrative and expansive mainstream White market. When businesses were developed that competed in size and scope with White businesses, intimidation and, in many cases, violence were used to curtail their expansion or destroy them altogether. The lack of major assets and indigenous community economic development has thus played a crucial role in limiting the wealth-accumulating ability of Blacks.

The past certainly casts a long shadow on the economic status of Blacks, but discrimination is not limited to the past. Recent studies of housing discrimination (Yinger, 1995, 1998), consumer markets (Yinger 1998), employment practices (Darity and Mason, 1998), and mortgage lending (Ladd, 1998) indicate pervasive and persistent discrimination— individual and institutional—in the last years of the twentieth century; in fact, the “economic detour” concept still operates in the most important way typical American families accumulate assets—home equity, as will be discussed in the next section.

The third concept, the “sedimentation of racial inequality” is synthetic in nature. The idea is that, in pivotal ways, the cumulative effects of the past have ostensibly cemented Blacks to the bottom of society’s economic hierarchy. A history of low wages (Leiberson, 1980), poor schooling, and segregation affected not one generation of Blacks but practically all Blacks well into the twentieth century. The best indicator of this is wealth—or lack thereof. Wealth is one indicator of material disparity that

captures the historical legacy of low wages, personal and organizational discrimination, and institutionalized racism. The low level of wealth accumulation evidenced by current generations of Blacks best represents the economic status of Blacks in the American social structure. In contrast, Whites in general—but well-off Whites in particular—had far greater structured opportunities to amass assets and use their secure financial status to pass their wealth and its benefits from generation to generation. What is often not acknowledged is that the same social system that fosters the accumulation of private wealth for many Whites denies it to Blacks, thus forging an intimate connection between White wealth accumulation and Black poverty. Just as Blacks have had “cumulative disadvantages,” many Whites have had “cumulative advantages.” Because wealth builds over a lifetime and is then passed along to kin, it is an essential indicator of Black economic well-being.

An understanding of the trends focuses attention on how past racial inequality in policy and practices translates into current racial stratification in the form of vastly different wealth resources for Black and White families, even among those with roughly equal accomplishments. Social injustice is not just an artifact of the past; contemporary institutional discrimination contributes to generating and maintaining the racial wealth gap. One key area is housing, perhaps the most important institutional sphere in which this inequality is passed along.

GENERATING CONTEMPORARY RACIAL STRATIFICATION: THE INSTITUTIONAL CONTEXT OF HOUSING, REAL ESTATE, AND FINANCIAL MARKETS

Home ownership is without a doubt the single most important means of accumulating assets for the typical American family. Home equity constitutes the largest share of net worth, accounting for about 44 percent of total measured net worth (Eller and Fraser, 1995). Federal housing, tax, and transportation policies have traditionally reinforced racial residential segregation. Continuing segregation has had an enduring impact on Blacks’ quest for asset accumulation; and continuing institutional and policy discrimination serve to intensify that impact. Three areas in which discrimination is known to be a factor are obtaining credit, assignment of interest rates, and assessment of property values. The first, access to credit, is important because whom banks deem to be creditworthy determines who owns homes, and institutional racial bias in the process of securing home ownership has had, and will have, lasting consequences. The second area of potential discrimination concerns the interest rates attached to loans for those approved for buying homes. Blacks are generally slotted for higher rates. Third, as is well known, housing values climbed

TABLE 10–6 Homeownership, Mortgages, Home Equity, and Race: 1994

|

|

Home Equity |

|||

|

|

Homeowner |

Mortgage Rate |

Mean |

Median |

|

White |

61.5% |

8.12% |

$74,859 |

$58,000 |

|

Black |

41.4% |

8.44% |

$46,254 |

$40,000 |

|

Difference |

20.1% |

0.32% |

$28,605 |

$18,000 |

|

SOURCE: 1993 SIPP, Wave 7. |

||||

steeply during the 1970s and 1980s, far outstripping inflation, and created a large pool of assets for those who already owned homes. Did all homeowners share equally in the appreciation of housing values, or is housing inflation color-coded?

Table 10–6 shows that the home ownership rate in 1994 for Blacks was about 20 percent lower than rates for Whites. Oliver and Shapiro, in Black Wealth/White Wealth (1995a), contended that this difference was not merely the result of income differences, but, rather, was a product of the historical legacy of residential segregation, redlining, Federal Housing Authority and Veterans’ Administration (FHA/VA) policy, and discrimination in real estate and lending markets (Yinger, 1995; Massey and Denton, 1994). How does this historical legacy and contemporary state of affairs contribute to the racial gap in wealth resources?

In order to purchase a home, families must pass the first stage— qualification for a home mortgage. Several Federal Reserve Board studies, based on the outcome of all loan applications (the release of which is mandated by federal legislation), show that even when applicants are equally qualified—i.e., “creditworthy” —Black families are still rejected for home loans 60 percent more often than equally qualified White families (Oliver and Shapiro, 1995a; Ladd, 1998). Thus, as egregious as past discrimination may have been in this sector, the intensity of covert continuation of racial discrimination is no less alive in the financial mortgage markets.

The second stage, for those fortunate enough to be approved for a home loan, is determining a mortgage rate. Oliver and Shapiro, in Black Wealth/White Wealth (1995a), showed that there is a mortgage rate difference for Blacks compared to Whites that is not determined by where the home is located, the purchase price, or when the home was bought. On average, Black families pay about 0.33 percent, or a third of a percent, more in mortgage interest rates than White families. Consider that the median home purchase price is about $120,000 with, say, $12,000 down payment, leaving a mortgage of $108,000. One-third of 1 percent may not sound like much, but on a typical 30-year loan this amounts to a $25-a-

month difference—for 360 months. Thus, over the loan period, a typical Black homebuyer will pay $9,000 more in interest to financial institutions than the average White homebuyer.

Bankers contend that they do not discriminate in setting mortgage interest rates on home loans. Instead, they say, it is more typical for Whites than Blacks to use larger down payments and financial “gifts” from family members to secure lower mortgage rates.2 But many people, Blacks particularly, cannot afford large down payments or do not have access to in vivo transfers; and based on accumulated evidence, we are firmly convinced that this process reveals a key to understanding how past inequality is linked to the present, and how present inequalities will project into the next generation. Essentially, past injustice provides a disadvantage for most Blacks and an advantage for many Whites in how home purchases are financed. Because similar home mortgages cost Black families $9,000 more, Blacks pay more to finance their homes and end up with less home equity in the future.

The third stage brings home equity into the analysis. The 1994 SIPP data on home equity show that buying a home seems to increase the wealth assets for all able to afford one; however, the valuing of homes and home equity is color-coded. (This analysis includes only those currently still paying off home mortgages and, thus, provides a very conservative estimate of the dynamics.) As seen in Table 10–6, the mean value of homes owned by White families increased $28,605 more than the value of homes owned by Black families. Again, Oliver and Shapiro (1995a) found that region, length of ownership, purchase price, when the home was purchased, and so on, did not explain the racial differential in home equity. The explanation lies in how the dynamics of residential segregation impact housing markets—a contemporary illustration of the economic detour Blacks confront.

A White family attempting to sell its house in a relatively homogeneous White community is limited only by market forces, that is, economic affordability. A similar Black family attempting to sell its home in

a community that is more than 20 percent non-White faces normal market limits plus effects of racial dynamics: the pool of potential buyers is no longer 100 percent of the market because most potential White buyers are not interested in mixed neighborhoods (Yinger, 1995; Massey and Denton, 1994); thus the pool of potential buyers has evaporated to mainly other Blacks who can afford the home, and possibly other minorities. The economic detour idea shows how the path to home equity can shift for Black home owners. A diminished pool of potential buyers composed of buyers with more limited financial assets also helps explain why housing values do not rise nearly as quickly or as high in Black communities or in those with more than 20 percent non-White residents.

TRANSLATING INEQUALITY INTO STRATIFICATION 1: PASSING IT ALONG

The role of intergenerational transfers in asset accumulation is certainly one of the most significant and controversial areas regarding wealth. How important are intergenerational transfers in the accumulation of assets? This question is important because if significant portions of assets are acquired as gifts from others, then a large part of the reason some people do not have assets can be traced to phenomena outside their control; and if this is the case, it could provide a strong basis for the normative argument for spreading asset ownership opportunities based on a principle of equal opportunity. For many years, the consensus viewpoint was that people save to smooth out undesirable consumption fluctuations and, in large part, to maintain comfortable living standards during the postretirement years (Modigliana and Brumberg, 1954). Financial inheritance has been dismissed as a source of the racial wealth gap on the theory that inheritance is quantitatively unimportant because the vast majority of households do not receive financial inheritances. Further, some claim that racial wealth disparities would be almost the same if wealth derived from past financial inheritances were subtracted out of current wealth.

Some economists, however, have challenged this view (e.g., Koltikoff and Sommers, 1981), concluding that intergenerational transfers were responsible for between 52 and 80 percent of accumulated wealth. Gale and Scholz (1994) calculate that 21 percent of wealth comes from in vivo gifts and 31 percent from bequests. McNamee and Miller (1998:200) conclude that “meritocracy is superimposed on inheritance rather than the other way around.” Wilhelm (1998) reviewed this literature and concluded that a great deal of wealth—at least one-half but likely more—is inherited. The bulk of these intergenerational transfers go to Whites who are well educated and work as professionals and managers. Disagreements remain,

but our reading of the evidence suggests that intergenerational transfers account for a very substantial share of total wealth; just how substantial remains to be determined empirically. In this spirit, we contribute some modest and preliminary findings.

White and Black families have a fairly realistic grasp of their economic circumstances and fortunes. It is interesting to note the expectations and hopes these families have regarding receiving and giving financial help and inheritances. In 1994, PSID families were asked about the likelihood that they would give financial assistance totaling $5,000 or more to their children, relatives, or friends over the next 10 years. This taps a double expectation—that they will be in a position to give help to people who need it and will be willing to do so. The figures, in Table 10– 7, show high expectations for both groups—52 percent for Whites and 44 percent for Blacks. Table 10–7 also contains data regarding families’ beliefs about their chances of leaving inheritances totaling $10,000 or more and $100,000 or more. The study questions probe, among other things, assumptions about present asset circumstances and optimism about future wealth accumulation. The data reveal some rather dramatic racial differences. Just about 25 percent of White families say they plan to leave an inheritance of $10,000 or more; 13.4 percent say they will bequeath more than $100,000 to their heirs. The grasp of present circumstances and optimism about future wealth among Black families is considerably more circumspect; less than 10 percent of Black families expect to leave an inheritance of $10,000 or more, and only 3.1 percent say their financial bequest will be $100,000 or more.

As noted, the above data reflect attitudes, expectations, and perhaps hopes. Actual receipt of inheritances is an interesting complement to these beliefs and expectations. Table 10–8 shows actual inheritances of $10,000

TABLE 10–7 Bequests and Race

|

|

Likelihood of Leaving Moneya |

|||

|

|

Get >$5,000 |

Give >$5,000 |

Leave >$10,000 |

Leave >$100,000 |

|

Sample |

18.9% |

49.1% |

19.1% |

9.7% |

|

White |

17.2% |

52.1% |

24.5% |

13.4% |

|

Black |

22.9% |

43.7% |

9.5% |

3.1% |

|

aChances are better than 50 percent. SOURCE: 1994 PSID. |

||||

TABLE 10–8 Inheritance and Race

|

|

Inheritance |

Value of Inheritance |

|

|

|

Past 5 Years |

Mean |

Median |

|

Sample |

3.8% |

$68,999 |

$30,000 |

|

White |

5.30% |

$74,219 |

$30,000 |

|

Black |

1.6% |

$33,363 |

$25,000 |

|

Difference |

3.7% |

$40,856 |

$5,000 |

|

SOURCE: 1994 PSID. |

|||

or more bequeathed from 1989 to 1994. Note that the amount is larger than the median net financial assets of American families (see Table 10–2). These data give a glimpse into a primary method by which wealth is passed along. Among White families, 5.3 percent were the beneficiaries of inheritances, compared to just 1.6 percent of the Black families. Thus, in the limited time period shown, Whites are more than three times as likely as Blacks to benefit from a substantial inheritance. Among Whites who received them, the mean inheritance amounted to nearly $75,000 compared to $33,400 among Blacks. Not only then are Whites much more likely to inherit, but the amounts are considerably larger, by $40,856. The difference between the mean and median inheritance among Whites indicates the extreme top heaviness of this distribution. This is not the case among the few Blacks that inherited, as the mean and median figures are comparatively close.

Wilhelm (1998) makes an important contribution to this discussion. Using PSID data, he adds further evidence of the importance of inheritance, especially when “inheritance” includes broader forms of intergenerational transfers. His summary evidence from 1984 and 1989 PSIDs shows that 22 percent already had inherited substantial amounts, with the average heir receiving $140,000. Those in the top quintile are more likely to inherit than those in the bottom quintile (26 to 15 percent); and it is not surprising that heirs in the top quintiles received considerably larger amounts, $289,000 to $60,000. He also looks at in vivo gifts from the 1988 PSID. About one in five families received such gifts in the previous year, averaging $2,540. Wilhelm’s data also show that inheritances and in vivo gifts occur among poor families to a much larger extent than previously acknowledged; and it is projected that the annual flow of transfers through inheritance will grow eightfold as the parents of baby-boomers pass on (Avery and Rendell, 1993).

TRANSLATING INEQUALITY INTO STRATIFICATION 2: THE FUTURE OF THE CHILDREN

Shapiro is presently conducting a research project examining how assets are used to pass racial stratification along, in the context of how families choose communities and select schooling for their children. This project is collecting nearly 250 in-depth interviews with families with young children in three cities. Based on preliminary insights and emerging trends from this early phase of the research, it is clear that there are those whose assets give them a multitude of options and opportunities, and those who have very limited options from which to choose. More remarkable is how families consciously use or plan to use assets to solidify their class status and racial identification, and, at the same time, consciously plan to improve the life chances of their children.

White, upper-middle class respondents with significant wealth are generally the ones “making choices.” Some of them have “prime choice”; in other words, they can live pretty much anywhere they choose, and they often choose stable, solidly middle-class neighborhoods. One mother explained her move from an integrated middle-class community to a better-off, virtually all-White suburb: “We always wanted to live on a street like this, with a big lot and all brick, two car garage, Sappington zip code 63128.” The zip code was attractive but she was moving because “I’m afraid of them. I am afraid of them. I want to shelter my kids until they’re older and they can handle it better…. I don’t want them being exposed to that type of situation…. those poor inner city kids whose parents are on crack…and have drugs and guns laying around for them to bring to school.”

One single White mother used her assets, inherited from her family, to move to a better community. This way she does not “have to worry about [my child] being abducted…I don’t have to worry so much about drive-by shooting…[that]something terrible is going to happen to him just because he was out in the street.”

At the other end of the spectrum are those who are “making do” with very limited choices, usually working class Blacks. Many describe how they are “doing the best they can,” living in a “bad, but not so bad” neighborhood. They would prefer to live elsewhere, but are glad they are not in the “worst” neighborhood. Others just feel “stuck.”

The interview analysis thus far clearly shows that families are putting a lot of thought, time, and energy into “navigating the school system.” The strategies they are able to use and the options available to them are clearly wealth-related, in that more money buys “better” schools or, at least, schools perceived as better. Whether those better schools are private, or public schools in expensive, prestigious neighborhoods, having assets allows some to elude the most troublesome aspects of America’s

urban ills. A Black mother is considering moving “because if I can’t afford to pay for private school, then I may think in terms of selling the house and moving to a community…[where] the school system is a little bit better.” She is illustrative of families who move or want to move to a community specifically for its school system, clearly planning to use family assets to increase the life chances of their children.

Often people plan to move from a community or send their children to private school once their children reach middle or junior high school age; people’s perceptions of public junior high schools revolve around gangs, drugs, negative peer influence, and so on. In our sample, families have fled, or plan to flee, urban public school systems much earlier—i.e., when their children reach fifth or sixth grade. Many adults in our sample who attended private schools as children are adamant in their desire to send their own children to private schools, stating repeatedly that “public school wasn’t an option” and often going to great lengths to ensure that their children attend private schools. Of course, for most of these families, their assets make this choice possible; but for these families and those with more limited choices, these interviews are highly suggestive of how families use assets to pass advantages along to their children.

BREAKING WITH THE PAST

A wealth perspective shows how past and contemporary institutional discrimination casts a long shadow on the economic status of Blacks. The challenge now is to explore how a wealth perspective might inform social policy. Bold and creative initiatives are needed to link the opportunity structure to policies that promote asset formation and begin to close the wealth gap. We can all help to build this agenda. Two approaches are needed. First, we must directly address both the historically generated and the current institutional disadvantages that limit the ability of Blacks and other racial groups to accumulate wealth resources. Second, we must resolutely promote asset acquisition among those at the bottom of the social structure who have been locked out of the wealth-accumulation process. Legislation at the federal level and in many of the states has been enacted to frame Individual Asset Accounts (IDAs) (Sherraden, 1991). These accounts offer a high set of structured incentives, in the form of matching payments, for poor families to save money for specific purposes, like buying a home, home repairs, starting a business, or education, health, and retirement.

Discussions promoting asset accumulation and IDA policy discussion were presented at the NRC Racial Trends Conference in October 1998. Since then, legislation has been considered and passed that structures this policy option. In addition, President Clinton, in his 1999 State of

the Union Address, incorporated this recommendation into his proposal for Universal Savings Accounts (USA; see Corporation for Enterprise development, 1996). As of this writing, the idea of promoting asset development is on the policy agenda. It should also be noted, however, that the ability of the social sciences to contribute evidence to this discussion or to shape policy design lags far behind the policy discussions and legislation.

Another positive step would be to democratize the 84 percent of welfare expenditures (Sherraden, 1991) that are targeted for the nonpoor and promote asset accumulation for the middle and upper classes—e.g., mortgage interest deduction and capital gains taxes. Making the “hidden” welfare state (Howard, 1997) subject to the democratic process puts social policy in an entirely different resource and policy context. These efforts would benefit minorities as well as many White Americans who are asset poor, making them potential allies in the fight for economic and racial justice.

Finally, the pronounced rise in wealth inequality during the 1980s is another source of policy urgency. Virtually all the growth in wealth between 1983 and 1989 accrued to the top 20 percent of households (Wolff, 1994).

RESEARCH ISSUES

Interest in wealth studies is growing rapidly; the field is young and the promise is great. A key challenge is to provide institutional incentives for this field to develop and attract top researchers. The task is twofold: technical and substantive. Technically we must ensure that the current databases continue to produce high-quality information about household asset formation and expenditures, and that other databases receive strong encouragement to include modules on assets and liabilities. As more data are collected and examined by researchers and policy makers, the information and knowledge base improves, thus measures and methodologies for change can also improve. Private foundations and the federal government should be encouraged to provide support for efforts in this direction. Longitudinal data will be especially useful for examining many of the complex issues regarding wealth accumulation and inequality, some of which have been identified in this paper. In terms of racial stratification, we offer a modest beginning by offering framework questions:

-

What accounts for the wealth gap over time?

-

How do families use assets to plan for social mobility?

-

In what way does acquiring assets affect behaviors, social psychology, future orientation, family violence, and ambitions?

-

What do more nuanced data analysis for Hispanics, Asians, and other minorities reveal about the American experience?

-

What is the role of savings in accumulating assets?

-

What is the relationship between home ownership and civic participation?

-

Will poor families save? Under what conditions?

-

What are the claims of different family members on family assets? Gender differences? Gender preferences?

-

How do families use assets to reproduce class standing for themselves and their children?

-

How important are intergenerational transfers in wealth accumulation?

-

How important are intergenerational transfers in perpetuating the racial wealth gap?

Other possible explanations of racial differences in wealth should be fully explored.

REFERENCES

Avery, R., and M.Rendell 1993 Estimating the size and distribution of the baby boomers’ prospective inheritances. Pp. 11–19 in American Statistical Association: 1993 Proceedings of the Social Science Section. Alexandria, Va.: American Statistical Association.

Bates, T. 1998 Race, Self-Employment, and Upward Mobility: An Illusive American Dream. Baltimore: Johns Hopkins University Press.

Butler, J. 1991 Entrepreneurship and Self-Help Among Black Americans: A Reconsideration of Race and Economics. Albany, N.Y.: State University of New York Press.

Corporation for Enterprise Development 1996 Universal Savings Accounts—USAs: A Route to National Economic Growth and Family Economic Security. Washington, D.C.: Corporation for Enterprise Development.

Darity, W., Jr., and P.Mason 1998 Evidence on discrimination in employment: Codes of color, codes of gender. Journal of Economic Perspectives 12(2):63–90.

Eller, T., and W.Fraser 1995 Asset Ownership of Households: 1993. U.S. Bureau of the Census. Current Population Reports, P70–47. Washington, D.C.: U.S. Government Printing Office.

Flippen, C., and M.Tienda 1997 Racial and Ethnic Differences in Wealth Among the Elderly. Paper presented at the 1997 Annual Meeting of the Population Association of America , Washington, D.C.

Gale, W., and J.Scholz 1994 Intergenerational transfers and the accumulation of wealth. Journal of Economic Perspectives 8(4):145–160.

Grant, D. 2000 A demographic portrait of Los Angeles, 1970–1990. In Prismatic Metropolis: Analyzing Inequality in Los Angeles, L.Bobo, M.Oliver, J.Johnson Jr., and A. Valenzuela, eds. New York: Russell Sage Foundation.

Howard, C. 1997 The Hidden Welfare State: Tax Expenditures and Social Policy in the United States. Princeton: Princeton University Press.

Jackman, M., and R.Jackman 1980 Racial inequalities in home ownership. Social Forces 58:1221–1233.

Jackson, K. 1985 Crabgrass Frontier: The Suburbanization of the United States. New York: Oxford University Press.

Koltikoff, L., and L.Sommers 1981 The role of intergenerational transfers in aggregate capital accumulation. Journal of Political Economy 89:706–732.

Ladd, H. 1998 Evidence on discrimination in mortgage lending. Journal of Economic Perspectives 12(2):41–62.

Leiberson, S. 1980 A Piece of the Pie. Berkeley: University of California Press.

Massey, D., and N.Denton 1994 American Apartheid: Segregation and the Making of the Underclass. Cambridge: Harvard University Press.

McNamee, S., and R.Miller, Jr. 1998 Inheritance and stratification. In Inheritance and Wealth in America, R.Miller, Jr., and S.McNamee, eds. New York: Plenum Press.

Mink, G. 1990 The lady and the tramp: Gender, race, and the origins of the American welfare state. Pp. 92–122 in Women, the State, and Welfare, L.Gordon, ed. Madison: University of Wisconsin Press.

Modigliana, F., and R.Brumberg 1954 Utility analysis and the consumption function: An interpretation of cross-section data. In Post-Keynesian Economics, K.Kurihara, ed. New Brunswick: Rutgers University Press.

National Research Council 1989 A Common Destiny: Blacks and American Society, G.Jaynes and R.Williams, eds. Washington, D.C.: National Academy Press.

O’Toole, B. 1998 Family net asset levels in the greater Boston region. Paper presented at the Greater Boston Social Survey Community Conference, John F.Kennedy Library, Boston, Mass., November.

Office of Trust Responsibilities 1995 Annual Report of Indian Lands. Washington, D.C.: U.S. Department of the Interior.

Oliver, M., and T.Shapiro 1989 Race and wealth. Review of Black Political Economy 17:5–25.

1990 Wealth of a nation: At least one-third of households are asset poor. American Journal of Economics and Sociology 49:129–151.

1995a Black Wealth/White Wealth: A New Perspective on Racial Inequality. New York: Routledge.

1995b Them that’s got shall get. In Research in Politics and Society, M.Oliver, R.Ratcliff, and T.Shapiro, eds. Greenwich, Conn.: JAI Press Vol. 5.

Ong, P. and E.Grigsby 1988 Race and life cycle effects on home ownership in Los Angeles, 1970 to 1980. Urban Affairs Quarterly 23:601–615.

Oubre, C. 1978 Forty Acres and a Mule: The Freedman’s Bureau and Black Land Ownership. Baton Rouge: Louisiana State University Press.

Portes, A., and Rumbaut, R. 1990 Immigrant America. Berkeley: University of California Press.

Quadagno, J. 1994 The Color of Welfare. New York: Oxford University Press.

Sherraden, M. 1991 Assets and the Poor: A New American Welfare Policy. New York: Sharpe.

Wilhelm, M. 1998 The role of intergenerational transfers in spreading asset ownership. Prepared for Ford Foundation Conference on The Benefits and Mechanisms for Spreading Assets, New York, December 10–12.

Wolff, E. 1994 Trends in household wealth in the United States, 1962–1983 and 1983–1989. Review of Income and Wealth 40:143–174.

1996a Top Heavy: A Study of Increasing Inequality of Wealth in America. Updated and expanded edition. New York: Free Press.

1996b International comparisons of wealth inequality. Review of Income and Wealth 42:433–451.

Yinger, J. 1995 Closed Doors, Opportunities Lost: The Continuing Costs of Housing Discrimination. New York: Russell Sage Foundation.

1998 Evidence on discrimination in consumer markets. Journal of Economic Perspectives 12(2):23–40.