2

Resources for Information Technology Research

The resources needed for research include funding and human capital, which are interrelated. Increases in funding for information technology (IT) research can enable industrial and university laboratories to hire more researchers, increase the number of graduate students trained in the nation's research universities, and allow the purchase of more IT hardware, software, and services to support those people. Similarly, increasing the size of the research workforce demands additional financial resources for salaries and technical infrastructure. But numbers alone do not tell the whole story. Equally important are the types of work supported and the types of organizations that fund or undertake the research. Vendors of computing and communications products, systems integrators, and end users all have different perspectives on the IT challenges that need to be addressed, and these perspectives combine with those of government funders of research and the researchers themselves to influence the scale and scope of the research agenda.

This chapter reviews trends in the nation's overall investment in IT research. The first section provides a framework for evaluating trends by explaining the importance of diversity in research portfolios, a theme carried forward through the chapter. The next two sections examine levels of government and industry funding for IT research, concentrating on the years 1987 to 1998. Distinctions are made, when possible, among funding sources (e.g., specific federal agencies, vendors, or users of IT components) and the types of research supported (e.g., component

advances vs. system integration issues). The last section of the chapter reviews trends in academic IT research, which receives much of the government and industrial support.

A credible discussion of research resources presupposes the existence of data: unfortunately, the present discussion is limited by the nature and quality of available statistics on IT research expenditures, as well as by lags between the time conditions are measured and the time they are reported. Despite extensive efforts by the National Science Foundation (NSF) and the Bureau of the Census, federal statistics on industrial and federally funded research remain difficult to track over time because some individual firms have been reclassified into different industry sectors and survey methodologies have been revised. Private sources of information, whether corporate reports or statistics from industry associations, typically do not distinguish expenditures on basic research from those on technology development (or applied research). Further complicating matters, neither federal nor private statistics speak to IT as a whole. Rather, they refer to academic disciplines (e.g., computer science and electrical engineering) or industry classifications (e.g., office and computing equipment and computing and data processing services). Some of the categories are being updated, but it is too soon to assess the impact of those changes. As computing and communications technologies converge and IT is infused into a growing number of products and services, assessing the size and needs of IT research will become even more difficult.

Because of the limitations in the available data sets, this chapter does not attempt a definitive assessment. Instead, it presents and analyzes a mosaic of available statistics to elucidate the dominant themes in support for research. In some cases, funding for combined expenditures on research and development (R&D) is used as a proxy for research; in others, the distinctions in federal data between basic and applied research are used to gain some insight, however limited, into the overall investments in these areas.

DIVERSITY IN THE RESEARCH BASE

The payoff of any research, especially fundamental research, is inherently uncertain. Research managers cannot predict which projects will prove successful or produce the greatest benefit to their organizations, industry, or society as a whole. Accordingly, savvy research managers seek to invest in a range of diverse research programs as a strategy for ensuring that at least a fraction of the overall portfolio will pay off—preferably enough to justify the entire investment. The concept of preparing for the unpredictable by investing in diverse activities that pursue a

spread of the best possible ideas is known as “portfolio management” in financial markets, which rely on this concept to manage risk.

Diversity within a research or financial portfolio plays much the same role as does genetic diversity in a species. A living organism carries a small amount of genetic material in addition to the genes that are essential for function. In a static environment, this genetic diversity imposes a cost beyond that carried by a species whose members are genetically identical and specifically tuned to exploit the environment. However, in times of a change or competition from other species, genetic diversity enables a species to adapt to the new environment using its extra resources. Similarly, diversity in the research base ensures that a nation's innovations will continue in the face of unforeseen changes in the technical, business, or societal landscape. 1 Diverse approaches will thus be available when changing conditions require new solutions quickly.

No one can fully predict future needs. The need for high-speed packet switching could not have been predicted 25 years ago, yet it is the heart of the Internet today. The need for ultralow-power microprocessors was largely unexplored 20 years ago, whereas today it is a critical underpinning in the growing area of portable and handheld computing. The economic payoffs of specific investments are likewise difficult to predict. Coding theory and digital signal processing were important research areas 40 years ago because of their applications in telephony and military radio. There was no way to know, however, that this research would have such enormous importance for consumer cellular telephones and Internet multimedia conferencing, which have hundreds of millions of users.

Lack of diversity in the IT research base can result from several factors. First, inbreeding can dilute the effectiveness of a research area as the same small community keeps funding and peer reviewing its members' projects. Or a research area can become too focused on a single approach that in retrospect turns out to have been unproductive. This can happen in a vigorous industry when firms adopt common approaches in their products, implying to researchers that even a successful new idea could not be introduced into practice. For example, radical new ideas for microprocessor designs might seem futile, because a tiny number of designs dominate today's market and the cost of market entry is enormous. However, low-power designs, crafted for the battery-powered portable devices that are sure to increase in number, might offer an opportunity for a very different approach.

Second, there can be a lack of funding for certain types of research —resulting in an absence of understanding of some technology that might suddenly become important to the field. This can happen when innovation moves ahead of research and new products and services are developed without sufficient intellectual underpinnings. Arguably, some of

the problems inherent in large-scale systems fall into this category (as discussed further in Chapter 4).

Third, research can reflect, to too great a degree, the objectives of the funders rather than the ideas of researchers. Although narrowly defined project goals can sometimes drive research that has serendipitous outcomes, they typically undermine diversity. This prospect fueled debate within the IT research community in the 1990s, when the High Performance Computing and Communications Initiative focused attention on the nature of research program definition and its impacts. Of course, it can be difficult to quantify the opportunity cost, which, at best, may be measurable only in retrospect.

FEDERAL SUPPORT FOR INFORMATION TECHNOLOGY RESEARCH

The federal government has been a strong supporter of IT research since World War II. Some of this research is conducted in federal laboratories, such as those supported by the Department of Energy (DOE) and the Department of Defense (DOD), but the greatest impact may have come from federally funded research carried out in university and industrial laboratories (CSTB, 1999). Over the past 50 years, this research has contributed to a wide range of important developments, including interactive time-shared computing, computer graphics, artificial intelligence, relational databases, and internetworking (CSTB, 1995, 1999).2 These technologies laid the foundation for new firms and new industries that have made substantial contributions to the nation's economic and social development. The context for decisions about new IT research continues to change—the industrial context seems particularly uncertain as this report is written—but broad lessons can be extracted from history to inform future decision making.

As noted in earlier reports by the Computer Science and Telecommunications Board (CSTB, 1995, 1999), federal support for IT research has been most effective when (1) directed toward fundamental research with long-term payoffs, (2) used to support experimental prototypes that pushed the technological frontier and created communities of researchers that crossed institutional boundaries, and (3) expanded on research pursued in industry laboratories. Such investments not only generated new technical ideas and knowledge that subsequently were incorporated into new products, processes, and services, but also—especially in the case of university research—trained generations of researchers who went on to lead the IT revolution. Continued federal support for projects that complement industry-funded research in these ways will help maintain the strength of the IT sector. Federal agencies also need to continue to

look forward, supporting computing and communications research in areas that are likely to grow in importance.

The following sections examine trends in federal funding between 1990 and 1998, the relative contributions of particular agencies, the operating styles of major federal agencies, and the characteristics of some large IT research programs. That period was chosen because it constitutes the most recent period for which consistent statistics are available. Other sections draw on data for 1999 and 2000.

Trends in Federal Funding

Trends in federal support for IT research over the past decade can be gleaned from data on funds obligated for research in computer science and electrical engineering, the two academic disciplines most closely associated with IT. Computer science encompasses the study of the theory of computing; the design, development, and application of computing devices; information science and systems; programming languages; and systems analysis—all topics that are directly applicable to IT. Electrical engineering includes the study of electronic devices and communication systems, which is directly relevant to IT, as well as the study of electric power systems, which is not. The sum of research expenditures for computer science and electrical engineering is an imperfect, but reasonable, proxy for IT research. Although it overstates federal expenditures by including work on electric power, this overstatement is offset by uncounted research in other academic disciplines relevant to IT, such as mathematics and cognitive science (important for understanding human-computer interaction).

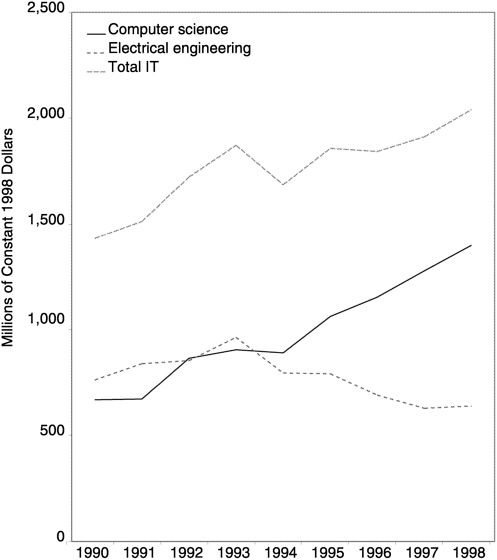

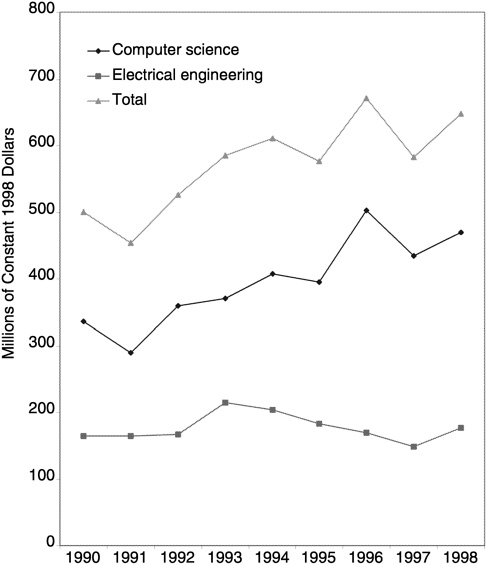

The data indicate that federal funding for IT research has, in general, been strong over the past decade. Combined federal funding for computer science and electrical engineering grew from $1.4 billion to $2 billion in constant dollars between 1990 and 1998—a 40 percent increase in real terms (Figure 2.1).3 However, federal funding for IT research remained virtually unchanged in real terms between 1993 and 1997, when the Internet and the World Wide Web began to exert a significant influence on the nation's economic and social structure, and when combined sales of IT goods and services were growing at an annual rate of more than 10 percent in real terms. 4 In other words, the explosion in IT applications throughout industry, government, and society was not matched by a commensurate increase in federal research support for the field—even as those applications began pushing beyond the knowledge limits of the underlying technology and began opening up new research opportunities.

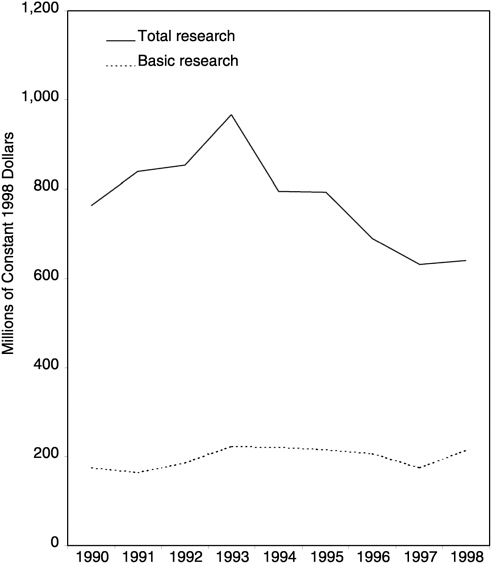

Despite the gains in funding for IT as a whole, federal support for research in electrical engineering appears to have declined between 1990

FIGURE 2.1 Federal funding for IT research, 1990 to 1998. SOURCE: National Science Foundation (2000a).

and 1998. The data suggest a 16 percent drop in real terms, from $764 million to $639 million in constant dollars (Figure 2.2). Most of the cutswere in the applied research budget, effectively boosting the share of funds devoted to basic research from 23 percent to 34 percent of total research spending in electrical engineering. However, support for basic research did not grow appreciably until

FIGURE 2.2 Federal obligations for research in electrical engineering, 1990 to 1998. SOURCE: National Science Foundation (2000a).

in electrical engineering appear to be due almost entirely to cutbacks in support from the DOD, which accounted for as much as 84 percent of the nation's total research funding for the field during this time period. This observation suggests that a significant portion of the cutbacks was directed toward those areas of electrical engineering that are directly related to IT, but sufficiently detailed data are not available to confirm

1998. Reductions in total research this statement. Nor can available statistics reveal whether apparent reductions in funding for electrical engineering resulted from the reclassification of some research from electrical engineering to computer science.

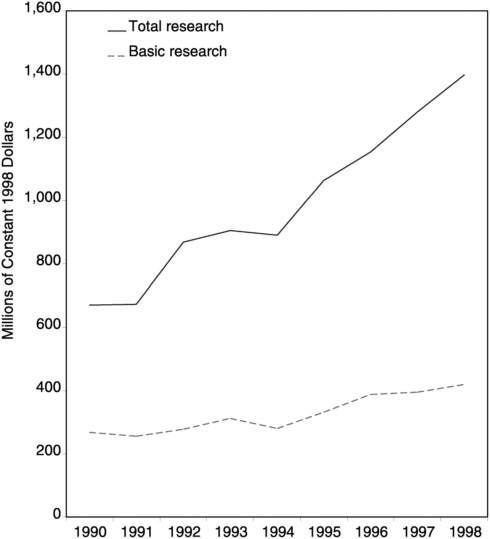

In computer science, combined federal expenditures for basic and applied research (also referred to as “total research”) more than doubled in real terms between 1990 and 1998, growing from $671 million to $1.4 billion in constant 1998 dollars (Figure 2.3). Here, however, funding for applied research grew more quickly than that for basic research. Although

FIGURE 2.3 Federal obligations for research in computer science, 1990 to 1998. SOURCE: National Science Foundation (2000a).

spending on basic research increased from $269 million to $419 million during the 8-year period, its share of total federal funding for computer science research fell from 40 percent to 30 percent. Statistics on basic versus applied research must be used with caution because distinctions between the two categories are notoriously difficult to make and may only reflect differences in accounting methods. Nevertheless, the data correlate with the testimony to this committee (and others) by IT researchers—especially university researchers—who perceive a decided shift in federal funding away from fundamental research and toward more applied projects with narrower scopes of inquiry, additional project milestones, mandatory system demonstrations, and interim deliverables. This trend has an upside and a downside: it may enhance the accountability of government agencies and help document the benefits of public investments (objectives set forth by the Government Performance and Results Act), but IT researchers report that it hampers their ability to conduct long-term research with inherently uncertain outcomes. At risk is the type of work that has been the cornerstone of federally funded IT research for decades.

Sources of Federal Support

Despite growth in the number of agencies listed as supporting IT research, federal funding remains concentrated in a handful of agencies. As recently as 1998, 88 percent of all federal funds for computer science research were distributed by just three federal agencies: the Department of Defense (DOD), the Department of Energy (DOE), and the National Science Foundation (NSF). The DOD alone contributed 40 percent of the total, with much of its funding coming from the Defense Advanced Research Projects Agency (DARPA) (see Table 2.1). A similar proportion of all funding for basic research in computer science came from the same three agencies, with the NSF alone contributing 62 percent of the total in 1998. This funding pattern continues a historical trend: as far back as 1976 (the earliest date for which consistent data are available), these three agencies contributed 91 percent of federal funding for computer science research, with the DOD alone contributing 68 percent.

Although the DOD has driven many important IT innovations in the past 50 years, the field's reliance on this one agency makes IT research support especially sensitive to fluctuations and directions in defense spending—and to repeated calls for research to be more relevant to defense missions. Defense budgets declined significantly in the post-Cold War environment, with total defense R&D declining 24 percent in real terms from its high in 1989 to 1999.5 Although DOD funding for computer science research grew 32 percent in real terms between 1990 and

TABLE 2.1 Federal Funding for Computer Science Research by Agency, 1998

|

Total Research |

Basic Research |

|||

|

Agency |

Millions of Dollars |

Percent of Total |

Millions of Dollars |

Percent of Total |

|

Department of Defense |

562 |

40 |

85 |

20 |

|

Department of Energy |

396 |

28 |

22 |

5 |

|

National Science Foundation |

267 |

19 |

258 |

62 |

|

Department of Health and Human Services |

66 |

5 |

35 |

8 |

|

Department of Commerce |

58 |

4 |

1 |

0 |

|

National Aeronautics and Space Administration |

26 |

2 |

17 |

4 |

|

Other |

25 |

2 |

1 |

0 |

|

Total |

1,399 |

100 |

419 |

100 |

SOURCE: National Science Foundation (2000a).

1998, it varied from year to year, declining in real terms in 1991, 1994, and 1996. Steep increases in spending by NSF and DOE during those years more than compensated for fluctuating military funding, but increases in computer science spending were not matched in spending for electrical engineering. The DOD funding for electrical engineering research dropped 20 percent in real terms between 1990 and 1998, driving the decline in total federal funding for the field.

The concentration of federal IT research funding within three organizations may have other limiting effects, not only on technology but also, perhaps, on the performance of government operations. Several agencies, including the Department of Health and Human Services (DHHS), the Social Security Administration, the Federal Aviation Administration, and the Internal Revenue Service, find their missions increasingly reliant on capable IT systems, which figure not only in internal processes (e.g., determinations and tracking of Social Security benefits) but also, increasingly, in the conduct of external activities for which they have some responsibility and in the very fabric of their relationships with external parties, from entities in regulated industries to individual citizens. The potential benefits to government agencies from IT are such that special federal efforts have been mounted to pursue them, including the Digital Government program described in Chapter 4. This level of attention and effort distinguishes IT from other types of infrastructure, such as transportation, on which agencies also depend.

Achieving the benefits of IT within agencies has been more difficult than articulating their promise. The difficulties these agencies have experienced with systems modernization over the past decade (see Chapter 3) suggest that adequate solutions to their IT needs are not available and cannot be developed within existing time and budget constraints. The problems are related mostly to the large scale of the systems and applications—a common issue that might have the best chance of being resolved if the agencies supported the relevant IT research. Yet the agencies are not mounting significant IT research programs, nor have they rushed to support the exploratory Digital Government program launched by the NSF to couple IT researchers to agencies with IT challenges—an initiative that could stretch the state of the art. Surely, support for IT research from federal agencies other than DOD, DOE, and NSF has increased as a percentage of total federal support since 1990, but the fraction remains small. Only 12 percent of total IT research funding and 13 percent of basic research support came from other agencies in 1998—and most of that was provided by science-based agencies such as DHHS and the National Aeronautics and Space Administration (NASA), which have long histories of attention to IT. Few other agencies have established IT research programs, and without the impetus of their resources and problem definitions, technical progress on these problems will probably be a matter of chance.

Styles of Federal Support

Federal agencies support IT research in different ways that tend to be suited to different types of problems. The most notable distinction is that between the research management styles of DARPA and the NSF. Research at DARPA has always emphasized the design and engineering aspects of IT, and building and experimenting with research prototypes are an essential aspect of that research.6 Such experimental work requires continuity—more funding per investigator and longer projects than are necessary for theoretical or paper studies (CSTB, 1994). DARPA's program managers assemble and oversee research portfolios within particular thematic areas. Researchers themselves play an indirect role in setting the objectives of the program through their interactions with program managers, and some DARPA programs specifically allow investigator-initiated proposals within the research theme of the program. Program managers are technically savvy—usually researchers on leave from university or industry—and know both the field and its researchers well. They work with research leaders and military leaders to develop long-term objectives that are both tractable for the research community and valuable to the DOD, balancing near-term military needs against longer-

term fundamental research that will advance the field. Program managers often devise ways for researchers from different organizations to work together on common problems or to bring new expertise or disciplines to bear on a problem.

The NSF, by contrast, relies much more heavily on peer review to allocate its IT research funding. Proposals are submitted by principal investigators, reviewed by several research peers, and acted on by a program manager. As a result, ideas are derived from the research community without the programmatic framework characteristic of a DARPA-funded effort. At the same time, most research proposals are for individual-investigator research. Grants are typically small, on the order of $90,000 per year, and include support for graduate research assistants. More than 10 years ago, the Computing and Information Science and Engineering (CISE) directorate within the NSF began to address experimental research with grants that could support modest-sized research teams for several years, something that had not been possible within conventional grant programs. Recently, this approach has been extended from hardware to software systems experiments. In partnership with DARPA, the DHHS's National Library of Medicine, NASA, and others, CISE supports the Digital Libraries Initiative (DLI), characterized by research themes focused more on an application vision than is typical of traditional computer-science research programs, which support subdisciplines such as programming languages, operating systems, and artificial intelligence. In keeping with a trend throughout the NSF, CISE is sponsoring more interdisciplinary work, engaging more social scientists (e.g., in support of better user interfaces or better systems to support group interaction) and researchers in the natural sciences to work in collaboration with computer scientists and engineers.

In addition, CISE sponsors a variety of efforts designed to provide IT infrastructure to support NSF's broader mission, namely, the support of scientific research. The most notable examples originated with the super-computer centers established in the mid-1980s. Now called Partnerships for Advanced Computational Infrastructure (PACI), two facilities with high-performance computers are linked nationwide to groups of academic and industrial partners to constitute a “distributed metacomputing environment,” featuring large-scale computing and visualization techniques to address scientific questions in many disciplines.7 Other efforts aim at improving networking infrastructure for the scientific community, leveraging the multiagency Next Generation Internet (NGI) initiative. These activities routinely provoke comments from IT researchers who fear that these efforts will be counted as programs that contribute to IT research, when in fact their purpose is to provide IT systems for other scientists to use in their research. They are, for the most part, infrastructure programs,

not research programs. The DLI, as well as some of the larger activities likely to emerge from the Information Technology Research initiative (see below), are different from PACI and the infrastructure component of the NGI because of their more balanced integration of application objectives with IT research.

Federal Information Technology Research Programs

The majority of recent federal funding for IT research has been provided under the umbrella of the High Performance Computing and Communications Initiative (HPCCI), which involved 10 federal agencies and offices and had a total budget of over $800 million in 1999 (Table 2.2). This initiative pursues research in several areas, primarily high-end computing and large-scale networking. High-end computing research includes work on components and architectures for high-speed computers (i.e., computers capable of 1015 operations per second); software for operating them and supporting various applications (e.g., scientific visualization, weather prediction, biomedical research); and theoretical computer

TABLE 2.2 Federal Funding for High Performance Computing and Communications by Agency, FY99 (millions of dollars)

|

Agency |

High-End Computing |

Large-Scale Networking |

Othera |

Total |

|

National Science Foundation |

224.7 |

72.0 |

4.3 |

301 |

|

DARPA |

48.0 |

82.2 |

10.4 |

141 |

|

Department of Energy |

91.9 |

33.9 |

0 |

126 |

|

National Institutes of Health |

27.1 |

67.9 |

8 |

103 |

|

National Aeronautics and Space Administration |

71.4 |

20.6 |

0.6 |

93 |

|

National Security Agency |

24.0 |

3.0 |

27 |

|

|

National Institute of Standards and Technology |

3.5 |

5.2 |

4.3 |

13 |

|

National Oceanic and Atmospheric Administration |

8.8 |

2.7 |

12 |

|

|

Agency for Health Care Policy and Research |

0 |

3.1 |

4.9 |

8 |

|

Environmental Protection Agency |

4.2 |

4 |

||

|

Total |

503.6 |

290.6 |

32.5 |

828 |

|

aThis category includes funding for high-confidence systems; human-centered systems; and education, training, and human resources. SOURCE: National Science and Technology Council (1999b). |

||||

science. Research in large-scale networking involves attempts to develop and deploy innovative technologies for high-speed networking and to experiment with applications that can take advantage of these networks. The NGI initiative falls into this category.8 Smaller amounts of funding are allocated to the development of high-confidence systems that have predictably high levels of availability and security; human-centered systems that enhance interactions between computers and users; and education, training, and human resources.

Other federal programs are aimed at more specific needs of federal agencies and contribute to the research base in different ways. For example, the DOE spent $484 million in 1999 on its Accelerated Strategic Computing Initiative (ASCI), which is intended to develop technologies that will enable the agency to simulate the performance of nuclear weapons without testing them (in compliance with the Comprehensive Test Ban Treaty). Through this program, the DOE is establishing centers of excellence at five universities to pursue high-end computing systems and simulation software and is working with the developers of these systems.9 Meanwhile, NASA pursues a more limited program of IT research to develop tools and integrated systems for the design and manufacture of flight vehicles, to manage complex flight and aviation operation systems, and to automatically generate and verify flight-crucial software. The DOD research labs support a range of fundamental and applied research programs to serve military needs.

A new multiagency initiative, proposed under the name Information Technology for the Twenty-First Century (IT2) by the NSF is intended to boost fundamental IT research, particularly in the areas of scalability and software. In its first year (FY00), the initiative provided an additional $366 million in federal funding for IT R&D to support (1) long-term research in software, human-computer interfaces and information management, scalable information infrastructure, and high-end computing; (2) the procurement and deployment of advanced computers that are 100 to 1,000 times more powerful than those available in 1999, simulation software and tools to make the computers useful in scientific and engineering applications, and teams of researchers to work on them to solve challenging problems, and (3) research on the social and economic impacts of IT that will enhance the usefulness of IT systems, limit potential misuses of such systems (such as potential violations of privacy), and lead to better understanding of the ways in which knowledge, values, and systems of society influence the spread of IT and the acceptability of IT systems in various applications (NSTC, 1999a). The long-term research component, in particular, is an attempt to recapture the past success of federal funding for IT research and “lead to fundamental breakthroughs in computing and communications, in the same way that government

investment beginning in the 1960s led to today's Internet” (PITAC, 1999). The initiative is to be coordinated jointly with the HPCC programs and the NGI initiative. The Clinton Administration proposed an additional $605 million in IT R&D funding in its FY01 budget to support research in priority areas, such as infrastructure for advanced computational modeling and simulation; storing, managing, and preserving data; security and privacy of information; ubiquitous computing and wireless networks; intelligent machines and networks of robots; more reliable software; broadband optical networks; and future generations of computers. It will also support partnerships to pursue research breakthroughs in particular application areas, such as health care and education (White House, 2000).

Six federal agencies are participating in the IT2 initiative: DOD, DOE, NASA, NIH, the National Oceanic and Atmospheric Administration (NOAA), and NSF. Each has developed new programs or expanded existing ones to meet the objectives of IT2. Some of these programs will address elements of large-scale systems and social applications of IT, but not to the full extent needed (see Chapter 3 and Chapter 4). Although it is too soon to evaluate these efforts, early indicators point to some practical challenges. The largest federal supporter of computing research, DARPA, attempted to jump-start its efforts to promote path-breaking IT research by issuing a broad agency announcement (BAA) in late 1998 (immediately after PITAC released a draft version of its report) calling for “radically new visions” of the future of information technology (Box 2.1). Anecdotal reports suggest that the results were disappointing to DARPA, perhaps because the research community was uncertain about the new effort. Nevertheless, several projects were funded as a result of this announcement, including Project Oxygen at the Massachusetts Institute of Technology (MIT) Laboratory for Computer Science;10 the Endeavor expedition at the University of California at Berkeley; 11 Portolano/ Workscape at the University of Washington;12 and another expedition at Carnegie Mellon University. Each of these is exploring different aspects of the post-PC era in which computing will be embedded into a range of information devices.13

In late 1999, NSF issued a solicitation for proposals under its agency-wide Information Technology Research (ITR) program, which called for research in eight areas related to IT: software, IT education and workforce, human-computer interfaces, information management, advanced computational science, scalable information infrastructure, social and economic implications of computing and communications, and revolutionary computing (NSF, 1999). Awards are anticipated in September 2000, but anecdotal reports on this effort point to the stresses on NSF program management caused by a large influx of researcher communications (e.g., letters of intent, preproposals, and proposals) that need to be evaluated

|

BOX 2.1 Expeditions into the Twenty-first Century “The goal of Expeditions into the 21st Century, a broad agency announcement (BAA) issued by the Defense Advanced Research Projects Agency, is to encourage vigorous and revolutionary research in information technology (IT). The funded efforts will set out to invent the future of IT by exploring alternative visions and their impact on society. The ideas pursued by expedition teams are expected to lead to unexpected results, thereby nourishing the information infrastructure and industries of the future. “The BAA solicits proposals for radically new visions that step outside of the present and anticipated models of both IT itself (i.e., hardware, software, etc.) and the domains and modes in which it is applied. There are a number of precedents for the ‘expedition' approach. A famous example is the Xerox Palo Alto Research Center, where researchers created an experimental network of computers for use by individuals doing office work. This effort pioneered many of the revolutionary technologies that led to today's personal computers—graphical user interfaces, pointing devices, laser printing, distributed file systems, and ‘what you see is what you get' word processing. This expedition was rooted in an alternative vision regarding how IT could be organized and used by individuals (i.e., distributed computing) as opposed to a more predictable goal of increasing the raw capability of then-dominant mainframe computers. “An expedition may focus on either a discipline-based theme, such as bioinformatics, or an infrastructure-based theme, such as ubiquitous computing. To establish a context, each expedition must be based on assumptions not true today; for example, one could assume the worldwide availability of near-infinite bandwidth. An expedition need not be limited to a single such assumption; however, proposals are expected to outline an approach to the exploration of a vision within the context of the assumptions. The bottom line: Think big and bold.” SOURCE: Reproduced from the Defense Advanced Research Projects Agency(1999). |

and responded to by a fixed staff already busy with ongoing responsibilities. Extraordinary efforts were made to recruit experts to participate in the necessary peer review. It will be years before the results of these recent efforts by DARPA, NSF, and other participants in the IT2 initiative can be evaluated, but current indications underscore the importance of the human infrastructure associated with the design and implementation of federal programs.

INDUSTRY SUPPORT FOR INFORMATION TECHNOLOGY RESEARCH

In the United States, industry is the leading supporter of IT R&D overall, according to available statistics—although these statistics raise as many questions as they appear to answer.14 The committee chose to analyze the available, albeit flawed, information in the belief that rough dimensions could be discerned and would be relevant to thinking about how to make progress, notably because the conduct and capacity of industry research are key to policy debates about whether and why the federal government should support more IT research. In an attempt to understand the sources of variation in reported aggregate data and to devise a more consistent set of data covering the 1990s, the committee made special arrangements with the Census Bureau to secure access to the raw data it collects on corporate R&D expenditures. In addition, committee members were able to enhance the utility of the data with quantitative and qualitative insights based on their own experiences. That said, the committee underscores the inadvisability of reading too much into specific numbers and other details.

Federal statistics indicate that companies in the six industry sectors most closely related to the manufacture and supply of IT products and provision of information services—office, computing, and accounting machines, communications equipment, electronic components, computer and data processing services, professional and commercial equipment and supplies, and communications services—invested some $52 billion in R&D in 1998. Detailed data are not available for the professional and commercial equipment and supplies industry. The five remaining sectors had combined R&D expenditures of $45 billion in 1998 (Table 2.3). This figure represents 7.3 percent of the combined annual sales revenues of the companies in these industries. More than one-quarter of these R&D expenditures, or $12.7 billion, was spent on research, with roughly 20 percent of research funding, or $2.7 billion, classified as basic research—the best approximation of fundamental research that is available using federal statistics.15

As the data in Table 2.3 indicate, there are considerable sector-to-sector differences in the support of R&D. For example, in the office, computing, and accounting equipment industry, R&D expenditures totaled more than 9 percent of sales revenues in 1998, whereas in the communications services industry (which might include companies such as AT&T, MCI, Sprint, and the regional Bell operating companies), expenditures on R&D represented less than 1 percent of sales revenues. Equally significant differences exist in support for research. Manufacturers of office, computing, and accounting machines, communications equipment, and

TABLE 2.3 Company Investment in Research and Development in Information Technology Industries, 1998 (millions of dollars)

|

Investment |

||||

|

Industry Sector |

R&D as % of Sales |

Total R&D |

Total Research |

Basic Research |

|

Office, computing, and accounting equipment |

9.2 |

8,890 |

3,441 |

276 |

|

Communications equipment |

11.2 |

10,173 |

2,296 |

1,148 |

|

Electronic components |

8.4 |

9,776 |

4,661 |

635 |

|

Communications services |

0.9 |

1,768 |

349 |

56 |

|

Computing and data processing servicesa |

12.4 |

14,297 |

1,996 |

599 |

|

Total |

7.3 |

44,904 |

12,743 |

2,714 |

|

NOTE: Does not include data for the professional and commercial equipment and supplies industry, which had estimated R&D investments of $7.2 billion in 1998. aComputing and data processing services includes prepackaged software, programming services, systems integration, and other computer-related services. SOURCE: National Science Foundation (2000b). |

||||

electronic devices (including semiconductors)—“component vendors” in the terminology developed in Chapter 1—funded more than 80 percent of the research reported by IT firms in 1998. Communications service providers—which can be considered “end users” in the terminology of Chapter 1—funded less than 6 percent of the total. The computer and data processing services industry, despite its significant R&D expenditures both in nominal terms and as a percentage of sales, also invests relatively little in research: its research expenditures accounted for just 14 percent of the IT industry total in 1998. The computer and data processing services industry encompasses firms engaged in a wide variety of activities, from the development of prepackaged software (another “component”) to custom programming and systems integration (“systems” work in the terminology of Chapter 1) to computer support and repairs. As the analysis below demonstrates, much of the R&D in this industry is attributable to software developers, such as Microsoft, implying that systems integrators themselves fund little research.

Most industry-funded IT research targets the discovery of new technical opportunities, usually within the sponsor's line of business. The time horizon is longer and the risk is higher than would be the case for product development, but the work does not pursue fundamental knowledge and it typically is completed within 3 years. Targeted research

usually is done only by larger companies with $3 billion or more in annual revenues; smaller companies do little or no explicit research. A few large companies, such as IBM Corporation, Lucent Technologies, Microsoft Corporation, and Xerox Corporation, support fundamental research conducted in their own laboratories and, to a much lesser extent, in universities. This research addresses fundamental questions not necessarily limited to the sponsor's line of business, and it has resulted in a number of major industry innovations, from the transistor to relational databases. Without exception, such work accounts for only a small fraction of the sponsor's overall research portfolio, because the emphasis is on targeted work.

The following sections examine trends in industrial research support, R&D at large companies, disincentives to corporate R&D investment, gaps in systems integration research, research by end-user organizations, and venture capital support for innovation.

Trends in Industry Support

Trends in industrial support for IT research over the past decade are difficult to discern because of limitations in data collection and inconsistencies in the available data. Over the past 20 years, the Census Bureau has expanded the three relevant Standard Industrial Classification (SIC) categories—business services, electronics, and computing equipment—on two different occasions, meaning that each one has twice been segmented into a larger number of subsectors. 16 The reclassification of IT companies cannot be tracked because the Census Bureau cannot say which companies are in which categories. (The business category declared by a company in its filings to the Securities and Exchange Commission (SEC) is not relevant because Census makes its own classification decisions based on the composition of the company's domestic payroll.) To complicate matters, a change in a firm's business focus (e.g., from telephone services to equipment manufacturing or communications business consulting) also leads to a reclassification of the firm and its research.17 There are also data gaps because the Census Bureau did not collect R&D statistics from service-sector companies (whether in telecommunications or banking) prior to 1995, nor does it break out the IT-related component of R&D expenditures by firms in other industries (i.e., end users of IT), such as the Boeing Company, General Motors Corporation, and Merrill Lynch. Furthermore, companies have different cultures and definitions for research; even within a single company it is often impossible to get an accurate estimate of spending on research that is spread thinly among divisions and researchers. Often the most important research is conducted informally by individuals without explicit corporate approval. In the past, it

was somewhat easier to estimate spending because research was concentrated in the centralized laboratories of a few large companies.

Industry support for IT research is in the midst of significant transformation, driven in large part by burgeoning demand for IT-based products and services. Large IT firms and start-ups are attempting to meet the demand by bringing new technologies to market at an increasing rate, a trend that has profound implications for research. As new competitors enter the industry, the traditional process of performing in-house research and incorporating the results into new products and services is being supplemented by some firms' attempts to, in effect, purchase research results. Some companies buy research explicitly by supporting university research, buying other companies (e.g., start-ups that have developed innovative products or technologies), or licensing technology from them, thereby obviating the need to fund their own research directed at developing similar solutions. Many companies engage in no explicit research, instead buying it indirectly through the activities of their vendors. Some assemblers of personal computers, such as Dell Computer Corporation and Gateway, Inc., for example, conduct virtually no research, choosing instead to assemble components (e.g., microprocessors, disk drives, operating systems) purchased from vendors such as Intel Corporation, Seagate Technologies, and Microsoft, which do conduct R&D. The same is true for many communications service providers, which perform limited R&D because they build networks out of communications equipment developed by vendors (although they often participate in testing equipment supplied by vendors and are actively involved in designing their own networks). Supply chains in IT industries are, therefore, important to understanding the flow of innovation, in addition to furnishing components for larger products and services. This trend has significant implications for research throughout the IT industry.

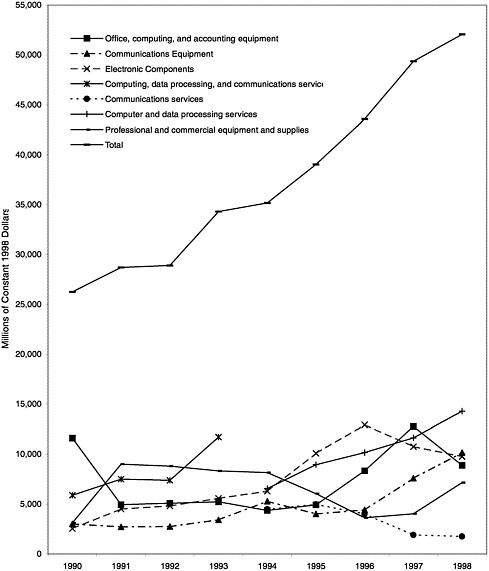

Federal statistics suggest that industry spending on IT R&D grew rapidly between 1990 and 1998 (Figure 2.4). The sheer magnitude of the swings in the reported data for individual industry sectors calls into question the reliability of the data and indicates the degree of reclassification of firms among sectors over time.18 Nevertheless, the data suggest that firms in the office, computing, and accounting industry and in the professional equipment industry reduced their R&D expenditures in the early 1990s before boosting them later in the decade. R&D in computing and data processing services appear to have grown, while R&D in communications services declined.

These trends mirror the data on R&D reported by firms in their annual filings to the Securities and Exchange Commission, although the magnitude of the changes is considerably less dramatic (Table 2.4). Among a dozen or so top IT firms whose combined R&D investments constituted

FIGURE 2.4 Reported company investments in research and development in IT industries, 1990 to 1998. Data for the professional and commercial equipment and supplies industry estimated in 1998. SOURCE: Compiled from U.S. Census Bureau statistics.

almost three-quarters of all reported IT industry R&D in 1998,19 such spending declined moderately in real terms between 1991 and 1994 and then grew rapidly between 1995 and 1999. Only three companies reported 1999 R&D investments lower than those of 1991 (in real terms). IBM's investments in R&D declined from $7.6 billion in 1991 to $4.4 billion in 1995 before rising to $5.2 billion in 1999, Digital Equipment's investments

TABLE 2.4 Research and Development Investment by Large Information Technology Companies, 1991-1999 (millions of constant 1998 dollars)

dropped from $1.9 billion in 1991 to $1 billion in 1997 before the company was purchased by Compaq Computer in 1998, and Xerox's R&D spending dropped slightly, from $1.02 billion to $966 million. Most companies posted real gains in R&D spending during the course of the decade. Microsoft's R&D spending jumped from $270 million to $2.9 billion in real terms between 1991 and 1999 and Intel's leapt from $711 million to $3.1 billion. Cisco Systems, a relative newcomer to the field, increased its R&D investment to more than $1.5 billion in 1999. People in these industries or knowledgeable about them recognize that the figures apply primarily to development or highly applied activity rather than to more fundamental research, but the figures do suggest an increase in innovative activity in the IT industry.

Despite impressive gains, company-financed R&D has not grown as quickly as have the sales of IT goods and services. Several of the companies listed in Table 2.4 saw their R&D investments decline as a percentage of net sales between 1991 and 1999 (Table 2.5), despite growing absolute R&D investments by many of them. Intel, for example, boosted its R&D spending almost fivefold between 1991 and 1999, but its R&D as a percentage of sales dropped from 13 percent to 10.5 percent. Although there were signs that many of the numbers improved in the late 1990s, the data overall indicate that R&D funding by large IT companies has declined in proportion to the IT marketplace, as noted earlier in this chapter.

Furthermore, the decline in the rate of R&D investment has been magnified by a shift toward more near-term, targeted research or development in many industry labs. Over the past decade, the share of IT R&D conducted by the 12 largest firms —those most likely to conduct long-term research—has declined by more than 10 percentage points. In addition, several large IT companies that operate central research divisions have redirected their research to track more closely areas of clear business interest. These changes have been driven by a desire to (1) better couple research activities with product development as a means of bringing new technologies to market more quickly and improving overall corporate performance, 20 (2) shift resources into computing and communications systems research, and (3) emphasize a more problem-oriented way of selecting research topics (Box 2.2). Research is coupled more closely now to the needs of the marketplace. IBM, for example, still supports the industry's largest in-house research program, but more of its work is concentrated on systems and software, the underpinnings of e-commerce, than on mathematics and physics.

Disincentives to Corporate Investment in Research and Development

Like most commercial enterprises, IT firms have strong economic reasons to refrain from investing in research, especially long-term research.

TABLE 2.5 Research and Development as a Percentage of Sales in Large Information Technology Companies, 1991 to 1999

|

BOX 2.2 Redirection of Research at Large Industrial Laboratories IBM Corporation When IBM Corporation experienced substantial operating losses in the early 1990s, IBM Research undervent significant restructuring. Skeptical of the Research Division's contributions to the company 's bottom line, IBM executives cut the company's total research and development (R&D) expenditures from $7.7 billion in 1991 to $4.4 billion in 1995, and the division's budget dropped from $550 million to $430 million. Although most of the cuts were accommodated by trimming overhead and eliminating redundant or unpromising programs, total R&D employment declined from a peak of about 3,400 to approximately 2,800 in late 1997. To deal with this situation, IBM managers attempted to couple research more closely to corporate objectives. IBM reoriented its research to focus less on physics and materials science and more on information systems, storage, software, applications, and solutions. Accordingly, the number of researchers working on networking, Internet technologies, solutions, and services grew, whereas the number of physicists and materials scientists declined. Electronic commerce emerged as a main focus of research. This research is clearly market-driven but still requires fundamental advances in computing and mathematics. It has produced innovations such as secure encrypted transactions. In recent years, IBM Research has experienced a resurgence. By 1999, IBM's R&D spending had increased 19 percent (in real terms) over its 1995 level, and the Research Division's budget reached an all-time high. Between 1995 and 1999, IBM established three new research facilities across the world: a lab in Austin, Texas (1995) that works on microprocessor technology; a lab in Beijing (1995) that focuses on speech recognition and digital library applications; and a facility in India (1998) that addresses cutting-edge customer solutions. IBM Research also has produced some much-heralded successes. Work on speech recognition contributed to the successful ViaVoice product; researchers found a way to replace aluminum with copper in microprocessors, paving the way for smaller, faster chips; and work on magnetoresistive data recording technology enabled IBM to capture 40 percent of the laptop storage market and produced the Microdrive, a 1-square-inch storage device for digital cameras and handheld computers. Paul Horn, director of research, says these technologies and others derived from the company's research contribute $25 billion a year in revenues for IBM—one-third of its total. AT&T and Lucent Technologies Since splitting off from AT&T in 1996, Lucent Technologies (which retained Bell Laboratories) committed itself to funding research at 1 percent of total revenues, which gives researchers an incentive to contribute to the company 's growth. Research expenditures have grown with the company at roughly 19 percent a year since 1996, reaching $4.5 billion in 1999. To increase the value and effectiveness of its research, Lucent established a variety of mechanisms to accelerate the commercialization of research results. It established an internal venture capital operation to fund innovative ideas that do not fit into existing business units. It has launched a dozen or so internal businesses that have their own presidents and virtual stock, as well as several independent spin-offs, such as Visual Insights, which sells software that can detect billing fraud by analyzing large amounts of |

|

data; Veridicom, Inc., which markets Bell Labs' patented fingerprint-authentication technology; Lucent Digital Radio, which is developing technology to convert analog FM radio signals to high-quality digital sound for broadcasters and greatly improve the quality of AM radio; and Persystant Technologies, which offers a software server that creates virtual environments linking networked users—whether on wired or wireless phones, laptops, or multimedia personal computers—over the public Internet or corporate intranets. Some of these ventures have moved their research results to the marketplace in just 8 months. AT&T also remains committed to funding research, but at a level not to exceed 0.3 percent of total revenues. Actual expenditures for research at AT&T have been closer to 0.2 percent of revenues since the two companies split, because the size of the staff grew more slowly than had originally been anticipated. AT&T also has allied research programs with newly defined strategic initiatives of its business units, especially those focusing on Internet-related technologies. For example, AT&T formed a subsidiary, a2b music, in November 1997 to provide secure downloading of music over the Internet. The company uses AT&T's encryption technology to protect the digital content rights of music labels and artists. Xerox Corporation Most of Xerox Corporation's computing- and communications-related research is conducted at its Palo Alto Research Center (PARC), which views itself as providing the equivalent of genetic diversity for Xerox. PARC's goals are to create surprising technological opportunities and ensure resilience against dramatic changes in the information technology industry. The center maintains small research programs in several topical areas that are expanded or contracted as technology trajectories and each program's relative importance to the company become clearer. Over time, PARC's research agenda has shifted to emphasize computing over areas such as mathematics and physics, and the center's overall level of effort has increased slightly, reflecting Xerox's commitment to research. To avoid repeating past mistakes, Xerox PARC has established mechanisms to improve its ability to capture the value of its research. Researchers are encouraged to work more closely with Xerox business units, and PARC routinely uses “spin-ins” (cases in which Xerox forms a corporation to develop a technology, takes a majority ownership position, and offers participants stock) and “spin-outs” (in which separately operating companies are formed that license the technology from Xerox) to encourage the commercialization of research results. Research problems still are chosen in a highly decentralized fashion, with researchers proposing new projects, but PARC has emphasized a problem-oriented approach to project selection. The idea is to focus on projects that are important to the company, such as how to make a totally silent copier. A challenge like this allows a range of responses, from incorporating sound-deadening devices in the copiers to facilitating the use of computer displays instead of paper copies. Such problem-oriented research often results in multidisciplinary work teams. Work on “smart matter” (the creation of materials with embedded computing capabilities), for example, involves both solid-state physicists and computer scientists. SOURCES: Buderi (1999); Carey (1999); Neil Marx, Internet DivisionFinance, IBM Software Group, personal communication, November 20,1997. |

Within their relatively small research budgets, vendors are understandably reluctant to invest in projects from which they are unlikely to reap many or all of the benefits. Economists call this the “appropriability ” problem: because good ideas diffuse rapidly and can be only partially protected by patents, individual firms cannot be assured of reaping (or appropriating) the benefits of their investments. Practical companies therefore tend to underinvest in the generation of new knowledge and technologies (see Box 2.3).

But IT firms face additional hurdles that make the problem of funding research especially acute. First, the IT industry is known for a rapid pace of innovation, which by all reports has accelerated in recent years. With product cycles as short as 6 to 9 months in many areas of IT, companies must pour resources into product development or risk being quickly left behind. The future is harder for research managers to predict than it was in the 1980s, a shift that increases the perceived risk for companies that invest too much in a particular vision of the future. IT companies that commit resources to projects that extend more than 3 years or so can find themselves abandoned by an unexpected direction of the industry. In such an environment, long-term research is risky unless broadly distributed across a portfolio —as prescribed by the diversity principle explained at the beginning of this chapter.

Other disincentives may be further reducing interest in IT research. One is the so-called network effect: the value of a networked application grows with the number of its users.21 Because of this effect, the market can lock in popular applications, which quickly become difficult to displace. The value of prototype applications in such an environment is small. For example, there is little incentive to do research on technically superior alternatives to common standards such as TCP/IP, Microsoft Windows, or the Intel microprocessor architecture; the rewards are more obvious for products that leverage these de facto standards.22 In this environment, there is less innovation in the form of fundamental improvements, which would challenge the dominant technologies; instead, innovation tends to be seen in new products and services that cleverly adapt these technologies to new market needs.23 For example, the Internet's basic protocol, IPv4, which provides only about 4.3 billion unique addresses, may not provide a large enough address space to meet future demands as the Internet grows. A replacement, IPv6, which is generally thought to not only provide a vastly larger address space but other technically superior features, was developed in anticipation of this need, but because of the high cost of getting everyone to switch protocols it has thus far failed to catch on in the marketplace. To surmount the switching problem, a variety of coexistence strategies are being pursued in the Internet community, but none have yet caught on with a large

|

BOX 2.3 The Economics of Research Funding Over the past 30 years, economists have developed a solid body of theory that demonstrates the limitations of the marketplace in supporting research, as well as the need for public support. This theory is based on the observation that knowledge—especially scientific and technical knowledge generated by research—has many of the characteristics of so-called public goods: research results are widely available to people and organizations whether or not they paid for or participated in their creation, and the discoverers of new knowledge cannot easily prevent others from making use of the knowledge without imposing additional costs on themselves and society. In economic terms, these characteristics are referred to as “nonrival use” and “costly exclusion,” respectively. These characteristics are associated especially with long-term, fundamental research. Together, they make it difficult for firms that fund research to fully capture (or appropriate) the benefits of the resulting knowledge or to keep others from doing so. Competitive markets work well when the incremental costs and benefits of using a commodity can be assigned to the user; they do not work well for the creation of scientific and technical knowledge, and firms tend to underinvest in research. Firms can try to protect new knowledge by seeking patent or copyright protection or by trying to keep it secret. Patents and copyrights provide legally enforceable means of protecting knowledge, but they require public disclosure, enabling others to learn from the work (by, for example, reverse engineering) and to find alternative means of achieving the same end. By keeping trade secrets, companies can avoid public disclosure, but this approach offers little means for legal recourse should others learn the secret (unless they use unlawful means to do so). Neither set of mechanisms, therefore, provides foolproof protection for new knowledge. Moreover, each imposes some economic inefficiencies, akin to those of a monopoly, that result from the restrictions placed on the use of the ideas. Such restrictions can result in duplicative research programs in different firms and the insufficient exploitation of new ideas. Despite appropriability problems, firms do support some fundamental research. Their motives range from monitoring progress at the frontiers of science, to identifying ideas for potential lines of innovation that may emerge from the research of others, to better positioning themselves to penetrate the secrets of rivals' technical practices. By conducting fundamental research, firms can also hope to attract top technical and scientific talent, who can contribute to research as well as development activities. Cohen and Levinthal (1990), in their theory of absorptive capacity, argue that firm-level investment in research creates an absorptive capacity in the firm that makes it better able to realize the benefits of research conducted by others. Nevertheless, funding fundamental research is a long-term strategy that is sensitive to commercial pressures to shift the research toward developing new products and services and improving existing ones. SOURCE: Condensed from Chapter 2 of Computer Science and Telecommunications Board (1999); additionaldiscussion of the appropriability problem can be found in Nelson(1959) and Arrow (1962). |

number of users. So Internet users have been forced to adopt various work-arounds, such as network address translation, that provide a quick fix for the address shortage but have significant side effects. The ultimate outcome is, as of this writing, unclear.

Further pressure to reduce expenditures on long-term research is being created by companies that successfully compete in certain segments of IT markets without incurring research expenses. As noted earlier, companies such as Dell Computer and Gateway have captured large shares of the market for PCs by offering products that incorporate standard components purchased from other vendors. Their products exploit technical advances made by supplier firms—many of which maintain extensive R&D programs.24 In effect, these assemblers buy research conducted by their component vendors and benefit from the economies of scale that the vendors enjoy by selling to numerous assemblers.

Another disincentive to fundamental innovation may be the limited capacity of users to absorb new technology.25 For example, the difficulty and risk associated with upgrading software can deter users from adopting new programs as quickly as vendors can generate them; similarly, end users may not be able to incorporate increases in processing speeds as fast as manufactures can provide them. Another limiting factor is the nature of the customer base for potential IT innovations. Because many potential users (both individuals and organizations) are less sophisticated and able than the early adopters of IT, vendors have limited incentive to invest in fundamental research unless they can hope to penetrate new markets with rapidly improving technology. Considerable energy is instead devoted to launching tactical product innovations and letting the marketplace sort out the winners from the losers. The enormous amount of activity and marketing hype should not be confused with fundamental advances in IT.

A Countertrend in Central Research Laboratories

Competitive pressures have not forced the traditional IT research labs to give up on fundamental research entirely. For example, Lucent Technologies supported a Bell Labs cosmologist who was attempting to detect hidden dark matter in the universe. Interestingly, the work contributed to a software product that detects billing fraud by analyzing patterns in large amounts of data. Other Lucent researchers are investigating neural pathways of the slug to learn how to build self-healing information networks or exploring computers based on quantum mechanics and the information processing capabilities of genetic material (Carey, 1999). Nevertheless, the breakup and divestiture of AT&T has steadily diminished the flow of fundamental IT research historically associated with the Bell Labs name (see Box 2.4).

|

BOX 2.4 Changes in Telecommunications Research The telecommunications sector provides a compelling example of the transformation from a vertically structured to a horizontally stratified industry. Before 1984, AT&T maintained a regulated monopoly over the nation's telecommunications services. As both an equipment manufacturer and a service provider, the company had strong interests in end-to-end systems issues, and its research laboratories (most notably Bell Laboratories) supported those interests. With its divestiture in 1984, AT&T's research divisions were divided between AT&T and the Bell Communications Research Corporation (Bellcore), which was formed to conduct research in support of the seven newly established local exchange service providers, the regional Bell operating companies (RBOCs). Bellcore's applied research organization started out with approximately 350 professional research staff, drawn almost entirely from the original Bell Laboratories, and grew to its target staff size of 501 within 3 years. By 1990, its budget peaked at about $135 million—nearly all of which was provided by the RBOCs.1 Then, amid increasing competition in the telecommunications sector, the RBOCs' funding for applied research at Bellcore steadily and rapidly declined, and by 1998 Bellcore's applied research staff was back down to about 350. Approximately 20 percent of Bellcore's researchers were funded by government contracts in 1998; another 50 percent were funded by Bellcore's business units to support the company's Software System and Professional Services products (e.g., technology and architectures for Internet telephony products, new types of software-based tools for efficiently finding Y2K problems, and, more generally, for testing software). Less than 30 percent of Bellcore's research budget was directed at broader industry research issues. Furthermore, Bellcore's customer base had grown substantially beyond the RBOCs, so the share of Bellcore's research supported by the RBOCs declined. Further separating Bellcore from the service providers, the RBOCs sold Bellcore (now called Telcordia Technologies) to Science Applications International Corporation in 1998, divesting themselves of their core research capability. Some of the RBOCs (e.g., NYNEX, U S WEST) supported large internal research organizations in 1990, with combined research expenditures of $75 million to $100 million. But these research programs were eliminated or dramatically scaled back during the 1990s. As a result, by 1999, the RBOCs no longer supported fundamental research (i.e., research that may net generate a return on investment until more than 3 years in the future), and even their support for more targeted research (i.e., attempts to discover innovative approaches for addressing clearly defined immediate problems) declined precipitously. The spin-off of Lucent Technologies from AT&T in 1996 reinforced the separation between equipment providers and service providers, as roughly two-thirds of AT&T's original research capacity (including Bell Labs) went to Lucent Technologies and only one-third remained within AT&T (in the form of AT&T Research). Research at Lucent continues to move toward systems and software, but with a less direct connection to the operational issues faced by telecommunications service companies. |

|

All of these changes occurred during a 15-year time period when the need to better understand how to design large, complex information networks, including their associated applications, greatly increased. 2 As a result, the majority of research supporting the nation's telecommunications industry now is conducted by equipment suppliers, such as Lucent Technologies, Nortel, and Cisco Systems, with fundamental research performed by some of the largest of these firms. These organizations, in effect, conduct research for a rapidly growing sector comprising RBOCs, long-distance carriers (such as MCI and Sprint), and Internet service providers. 2The history recounted here, and the estimates of R&D support by the RBOCs, were provided by Stewart Personick, former vice president of information networking at Bellcore, personal communication, April 26, 1999. |

Some IT companies have created new corporate research laboratories to extend their horizons. Intel, for example, established a microcomputer lab in 1996 to conduct pioneering research on microprocessors. With an original staff of 70, the group's objective was to identify technical roadblocks to improved microprocessor performance and find ways to overcome them (Takashi, 1996). In November of 1998, Motorola created a central research lab, Motorola Labs, as a way of combining and better managing the approximately 1,000 researchers who had previously worked in separate research groups focusing on wireless communications, semiconductors, and other products. At the same time, Motorola began increasing its funding for research, especially fundamental research, to bring it up to what it describes as a standard level of research funding among larger IT companies, 1 percent of the prior year's revenues.26 Research topics range from high-quality displays for cellular phones to work with genetic material aimed at finding ways of using the attraction between pairs of organic acids to lay down patterns of circuitry on integrated circuits (Hardy, 1999).

The most obvious newcomer to corporate research is Microsoft, which in 1991 established a research division that has attracted some of the top talent in IT. Microsoft Research grew to some 200 researchers by 1999, even expanding to include a facility in England, and further growth has been planned. Research groups are maintained in a dozen areas, including speech recognition, decision theory, and computer graphics. They

pursue research with long-term implications for the company that also may also feed into ongoing development projects.27 Systems to check spelling and grammar, assist users in real time, facilitate remote collaboration, and translate among languages are among the fruits of Microsoft's R&D that have been commercialized; more speculative work includes efforts to develop a tablet computer—a portable, wireless device without a keyboard that could serve a range of personal computing and communications purposes—and to develop large-scale-image databases with intuitive interfaces (Markoff, 1999; Barclay et al., 1999).

Gaps in the Research Base: Systems Integration

As noted in an earlier report by the Computer Science and Telecommunications Board (CSTB, 1992), systems integration first became an issue in the 1960s, when federal agencies began hiring contractors to design large-scale systems for data processing, communications, and aerospace and defense applications. Over the next 40 years, the emergence of distributed personal computing, local area networks, and, more recently, the Internet, drove a growing need for systems integration. The integration challenge goes beyond making incompatible machines communicate with each other; it is a problem-solving activity that harnesses and coordinates the power and capabilities of IT to meet customers' needs. The result is generally one-of-a-kind systems that increase productivity, flexibility, responsiveness, and competitive advantage. Considerable effort is expended on customized consulting—modification, interfacing, coding, and installing hardware and software—to integrate the individual components into a cohesive whole.

Systems integration is now a thriving U.S. industry that is finding new opportunities in the efforts across the economy to engage in e-commerce. Total revenues for custom integrated system design and custom programming services topped $76 billion in 1997, up from $34 billion in 1990.28 Different types of firms provide such services. Companies such as Andersen Consulting, Electronic Data Services (EDS), and Computer Sciences Corporation earn the majority of their revenues from systems integration activities. Many of the large accounting/business services firms, including PricewaterhouseCoopers, KPMG, and Ernst & Young, also have established systems integration and services practices. Large diversified computer manufacturers, such as IBM and Hewlett-Packard, have moved into systems integration and related services, creating new divisions for these activities. IBM's Global Services Division is the fastest-growing part of the company; its revenues increased almost 30 percent between 1997 and 1999 and accounted for 37 percent of the company's revenues in 1999. Also participating in the industry are a number of defense contractors,

such as Lockheed Martin and the Boeing Company, which developed their systems integration experience by designing complex weapons or command-and-control systems for the military and by operating their own substantial information and communications systems.

In general, systems integrators support limited R&D, and most of what is funded is development. Neither Andersen Consulting nor EDS—two of the largest systems integration firms—report R&D expenditures in their annual reports (Table 2.6). Andersen does have a small research division that employs about 200 computer scientists and business analysts to identify interesting technologies and build prototype applications for testing with potential customers; however, the division constitutes a small part of the company.29 Its work focuses on areas such as e-commerce, intellectual asset management, and work group productivity.30 Lockheed Martin, a diversified company with approximately $1 billion in R&D

TABLE 2.6 Research and Development Investments of Representative Systems Integrators, 1998 (millions of dollars)

|

Company |

Systems Integration Revenues |

Systems Integration R&D |

|

Services-only firmsa |

||

|

Andersen Consulting |

8,307 |

0 |

|

American Management Systems |

1,058 |

77 |

|

Computer Sciences Corporation |

7,660 |

0 |

|

Electronic Data Services |

16,891 |

0 |

|

Keane |

1,076 |

3.5 |

|

Diversified firmsb |

||

|

IBM |

28,916 |

25% of research division budget |

|

Hewlett-Packard |

6,956 |

50 |

|

Lockheed Martin |

5,212 |

36.4 |

|

aData on the services-only firms was taken from annual reports to the Securities and Exchange Commission. Andersen Consulting reports no research and development expenditures in its annual filings to the Securities and Exchange Commission, but it does operate a research group with about 200 members. bData for the diversified firms shows systems integration revenues out of total corporate revenues and systems integration R&D out of total R&D. Data on IBM provided by Irving Wladawsky-Berger, vice president of technology and strategy at IBM, personal communication, October 6, 1999. Data on Hewlett-Packard provided by Curtis Hoyle, special assistant to the director, Hewlett-Packard Laboratories, personal communication, November 2, 1999. Data on Lockheed Martin provided by B. Clovis Landry, vice president of technology, Lockheed Martin Information and Services Sector, personal communication, October 11, 1999. |

||