CHAPTER 2

THE CONTEMPORARY MATERIALS SCENE

THE NATURE OF MATERIALS

This report is concerned primarily with industrial materials that are used to make things—products like machines, devices and structures. Such materials are ubiquitous, so pervasive we often take them for granted. Yet they play a central role in much of our daily lives, in practically all manufacturing industries, and in much research and development in the physical and engineering sciences. Materials have a generality comparable to that of energy and information, and the three together comprise virtually all technology.

Materials are basic to manufacturing and service technologies, to national security, and to national and international economies. The housewife has seen her kitchen transformed by progress in materials: vinyl polymers in flooring; stainless steel in sinks; Pyroceram and Teflon in cookware. The ordinary telephone contains in its not-so-ordinary components 42 of the 92 naturally-occurring elements. Polyethylene, an outstanding insulator for radar equipment, is but one of myriad materials vital to national defense. By one of several possible reckonings, production and forming of materials account for some 20% of the nation’s Gross National Product, but the number is deceptive; without materials we would have no Gross National Product.

Man tends to be conscious of products and what he can do with them, but to take the materials in those products for granted. Nylon is known far better in stockings than as the polyamide engineering material used to make small parts for automobiles. The transistor is known far better as an electronic device, or as a pocket-size radio, than is the semiconducting material used in the device and its many relatives.

Some materials produce effects far out of proportion to their cost or extent of use in a given application. Synthetic fibers, in the form of easy-care clothing, have worked startling changes in the lives of housewives. Certain phosphor crystals, products of years of research on materials that emit light when bombarded by electrons, provide color-television pictures at a cost of less than 0.5% of the manufacturing cost of the set.

The properties of specific materials often determine whether a product will work or not. In manned space flight, ablative materials of modest cost are essential to the performance of the heat shield on atmospheric reentry vehicles. New or sharply improved materials are critical to progress in

energy generation and distribution. At the other extreme are home-building materials, whose properties, though important, need not be markedly improved to meet society’s goals in housing.

Materials commonly serve a range of technologies and tend to be less proprietary than are the products made of them. Materials, as a result, are likely to offer more fruitful ground for research and development, including cooperative research and development, than are specific products. One example is fiberglass, which can be used for making pleasure boats, housing construction, and automobile bodies. Another example is certain “textured” materials, polycrystalline structures in which the alignment of neighboring crystals is determined by the processing steps employed. The ability thus to control crystal orientation grew out of research by physicists, metallurgists, and even mathematicians. The resulting improvements in properties are proving useful in a widening spectrum of applications. They include soft magnetic alloys for memory devices, oriented steels for transformers, high-elasticity phosphor bronze for electrical connectors, and steel sheet for automobile fenders, appliance housings and other parts formed by deep drawing.

THE NATURE OF MATERIALS SCIENCE AND ENGINEERING

Materials science and engineering is a multidisciplinary activity that has emerged in recognizable form only during the past two decades. More specifically:

Materials science and engineering is concerned with the generation and application of knowledge relating the composition, structure, and processing of materials to their properties and uses.

The multidisciplinary character of materials science and engineering is evident in the educational backgrounds of the half-million scientists and engineers who, to varying extents, are working in the field. Only about 50,000 of them hold materials-designated degrees*; the rest are largely chemists, physicists, and nonmaterials-designated engineers. Many of these professionals still identify with their original disciplines rather than with the materials community. They are served by some 35 national societies and often must belong to several to cover their professional and technical needs. This situation is changing, if slowly. One recent indication was the formation of the Federation of Materials Societies in 1972. Of the 17 broadly-based societies invited to join, nine had done so by October, 1973.

Materials are exceptionally diverse. Correspondingly, the scope of materials science and engineering spans metals, ceramics, semiconductors, dielectrics, glasses, polymers, and natural substances like wood, fibers,

sand, and stone. For COSMAT purposes, we exclude certain substances that in other contexts might be called “materials.” Typical of these are food, drugs, water, and fossil fuels. Materials as we define them have come increasingly to be classified by their function as well as by their nature; hence biomedical materials, electronic materials, structural materials. This blurring of the traditional classifications reflects in part our growing if imperfect ability to custom-make materials for the specific functions required of them.

MATERIALS IN THE U.S. ECONOMY

The United States, with about 6 percent of the world’s population, consumes from 25 to 50 percent of the world’s output of resources. The American people have become accustomed to a great variety and quantity of material goods from a resource base which may be diminishing. Private industry, our society’s instrument for providing these material goods, has evolved a remarkably successful producing system to keep pace with ever growing product demand. World trade and improved technology are both parts of this system. Our country must export products to pay for the raw materials imports. And it is through continued scientific and technological progress to improve the efficiency of materials use that we compete successfully in world product markets.

About 20 percent of our Gross National Product originates in the extraction, refining, processing, and forming of materials into finished goods other than food and fuel. All materials pass through a number of stages in their economic utilization. At each stage, value is added and cost is incurred to pay for energy, production and research, manpower, administration, and finally disposal and recycling costs. The primary instrument generally used in our society for implementing this utilization of materials is private industry. Competing in the market place under ground rules established by society through its governmental bodies, private industry attempts to minimize the cost of materials utilization in order to produce quality goods that satisfy its customers, and to provide a reasonable return on investment to its owners.

The consumption of basic materials in the U.S. has been growing steadily (Table 2.1), along with the population and standard of living. Another measure of the impact of materials on the economy is manufacturing employment related to materials, which was just over 16 million in 1970, or about 21% of total employment.

A third measure of the importance of materials in the nation is their contribution to the National Income or to the Gross National Product1. Table 2.2 indicates the main industrial categories contributing to the former and

TABLE 2.1 Consumption of Selecteda Basic Materials in the U.S. (Millions of Tons)

|

|

1950b |

1971b |

|

1950b |

1971b |

|

Aluminum |

1.3 |

5.5 |

Clays |

39.5 |

55.1 |

|

Calcium |

N.A. |

90.3 |

Gypsum |

11.4 |

15.7 |

|

Copper |

2.0 |

2.4 |

Pumice |

0.7 |

3.5 |

|

Iron |

94.5 |

122.2 |

Sand and gravel |

370.9 |

987.7 |

|

Lead |

1.4 |

1.3 |

Stone, crushed |

N.A. |

823.0 |

|

Magnesium |

N.A. |

1.1 |

Stone, dimension |

N.A. |

1.8 |

|

Manganese |

1.1 |

1.2 |

Talc |

0.6 |

1.1 |

|

Phosphorus |

1.7 |

5.1 |

… |

|

|

|

Potassium |

1.2 |

4.5 |

Agricultural fibers |

N.A. |

2.1 |

|

Sodium |

N.A. |

19.0 |

Forest products |

N.A. |

237.0 |

|

Sulfur |

6.8 |

12.4 |

Plastics |

1.0 |

10.0 |

|

Zinc |

1.1 |

1.2 |

|

||

|

aCommodities used in excess of 1 million tons in 1971. Totals include government stockpiling, industry stocks, and exports. Foods and fuels are not included. b1950 actual; 1971 estimated. Source: First Annual Report of the Secretary of the Interior under the Mining and Minerals Policy Act of 1970, March 1972. Figures for agricultural fibers, forest products, and plastics compiled by COSMAT from various sources. |

|||||

TABLE 2.2 Distribution of National Incomea of the United States by Industry Category–1965

their distribution in 1965. The two categories of Mining and Manufacturing relate primarily to materials, and it can be seen that they contribute some 31.6% to the National Income. An additional amount arises from the 3.76% represented by Agriculture, Forestry,and Fisheries. The specific contribution of materials in the above categories is strongly concentrated in particular subcategories. Table 2.3 and the corresponding Table 2.4 for GNP in 1971 show the distribution among the principal subcategories; those relating primarily to materials are metal-mining, mining and quarrying of nonmetallic materials, paper and allied products, rubber and miscellaneous plastic products, leather and leather products, lumber and wood products, stone, clay and glass products, primary metal industries, and fabricated metal products. These operations on materials account for perhaps one-tenth of the nation’s consumption of fuels.

While the above groups alone constitute a significant portion—some 9%–of the National Income, there are additional and major materials contributions in most of the other manufacturing subcategories which cannot be separated in terms of their share of the National Income. The difficulty stems from the nature of this measure of economic activity, which is the aggregate earnings of labor and property that arise in the current production of goods and services by the nation’s economy, i.e. the total factor costs of the goods and services produced by the economy.

An alternative economic approach that might be adapted to give better insight into the contributions of materials is the modeling of the structure of an economic system by “input-output” or “inter-industry” analysis originated by W.W.Leontief of Harvard University. The technique describes the production process in a given industry in terms of a detailed accounting of its purchases from other industries, i.e. its inputs of raw and semifinished materials, components, and services. The complete record of inter-industry transactions described in this way within the entire economy is displayed as a square-matrix or input-output table. This method has been used to identify the primary materials component of the economy in the sense discussed above, but only partially separates materials in the various manufacturing areas. In any case, the analysis is still concerned with economic value, whereas many of the questions and problems associated with materials flow are concerned with mass or volume rather than value alone.

Despite these limitations for the present purpose, some results of particular interest concerning materials have arisen from the application of the technique carried out by Carter2 in which structural changes in the U.S. economy arising from changes in technology were analyzed by comparing input-output tables prepared for two different years–1947 and 1958. The results show strikingly the relative increase over this period in “nonmaterial” or “general” inputs (these include energy, communications, trade, packaging, maintenance construction, real estate, finance, insurance and other services, printing and publishing, business machines and information technologies) that are largely balanced by relative decreases in the input of

TABLE 2.3 Distribution of National Income of the United States within Selected Industry Categories–1965

|

A. |

MINING CATEGORY ($6,432 million=1.15% National Income) |

|||

|

|

SUBCATEGORY |

SHARE OF CATEGORY (PERCENTAGE) |

||

|

|

Metal Mining |

15.93 (0.18)a |

|

|

|

|

Coal Mining |

21.16 (0.24) |

|

|

|

|

Crude Petroleum and Natural Gas |

43.14 (0.50) |

|

|

|

|

Mining and Quarrying of Nonmetallic Materials |

19.76 (0.23) |

|

|

|

|

100.0 |

|

||

|

B. |

MANUFACTURING CATEGORY ($170,408 million=30.48% National Income) |

|||

|

|

SUBCATEGORY |

SHARE OF CATEGORY (PERCENTAGE) |

||

|

|

Nondurable Goods: |

|||

|

|

|

Food and Kindred Products |

8.50 (2.59) |

|

|

|

|

Tobacco Manufacturers |

0.70 (0.21) |

|

|

|

|

Textile Mill Products |

3.44 (1.05) |

|

|

|

|

Apparel and Other Fabricated Textile Products |

3.85 (1.17) |

|

|

|

|

Paper and Allied Products |

3.36 (1.02) |

|

|

|

|

Printing, Publishing, and Allied Industries |

5.06 (1.54) |

|

|

|

|

Chemicals and Allied Products |

7.24 (2.20) |

|

|

|

|

Petroleum Refining and Related Industries |

2.97 (0.71) |

|

|

|

|

Rubber and Miscellaneous Plastic Products |

2.34 (0.71) |

|

|

|

|

Leather and Leather Products |

1.07 (0.33) |

|

|

|

38.53 (11.74) |

|||

|

|

Durable Goods: |

|||

|

|

|

Lumber and Wood Products, except Furniture |

2.42 (0.74) |

|

|

|

|

Furniture and Fixtures |

1.67 (0.51) |

|

|

|

|

Stone, Clay, and Glass Products |

3.40 (1.04) |

|

|

|

|

Primary Metal Industries |

8.65 (2.64) |

|

|

|

|

Fabricated Metal Products |

6.65 (2.03) |

|

|

|

|

Machinery, except Electrical |

10.77 (3.82) |

|

|

|

|

Electrical Machinery |

8.34 (2.54) |

|

|

|

|

Transportation Equipment and Ordnance, except Motor Vehicles |

6.78 (2.07) |

|

|

|

|

Motor Vehicles and Motor Vehicle Equipment |

8.53 (2.60) |

|

|

|

|

Instruments |

2.58 (0.78) |

|

|

|

|

Miscellaneous Manufacturing Industries |

1.68 (0.51) |

|

|

|

61.47 (18.74) |

|||

|

|

100.0 |

|||

|

a Figures in parentheses indicate the subcategory share as a percentage of the total National Income. |

||||

TABLE 2.4 Selected Industry Components of the Gross National Product (1971) (1971 GNP=$1,050,356 million)

|

|

Millions |

% of GNP |

|

Metal Mining |

$ 1,290 |

0.12 |

|

Mining and Quarrying of Nonmetallic Metals |

1,654 |

0.16 |

|

Stone, Clay, and Glass Products |

8,710 |

0.83 |

|

Primary Metal Industries |

18,923 |

1.80 |

|

Fabricated Metal Products |

16,427 |

1.56 |

|

Machinery, except Electrical |

26,066 |

2.48 |

|

Electrical Machinery |

22,388 |

2.13 |

|

Transportation Equipment, except Motor Vehicles |

14,582 |

1.39 |

|

Motor Vehicles and Motor Vehicle Equipment |

22,824 |

2.17 |

|

Instruments |

6,456 |

0.61 |

|

Miscellaneous Manufacturing Industries |

4,144 |

0.39 |

|

Chemicals and Allied Products |

20,387 |

1.94 |

|

Rubber and Miscellaneous Plastic Products |

7,371 |

0.70 |

|

Lumber and Wood Products, except Furniture |

6,395 |

0.61 |

|

Furniture and Fixtures |

3,984 |

0.38 |

|

Paper and Allied Products |

9,357 |

0.89 |

|

Textile Mill Products |

8,234 |

0.78 |

|

Apparel and Other Fabricated Textile Products |

9,293 |

0.88 |

|

Leather and Leather Products |

2,219 |

0.21 |

|

|

$210,704 |

20.03 |

|

Source: U.S. Department of Commerce |

||

materials and semifinished goods. Thus, the iron and steel sectors declined relatively some 27% (despite substantial growth in absolute terms), reflecting substitution by aluminum and plastics together with design changes to reduce the total amount of metal used by taking advantage of the improvements developed in steel properties and performance. A relative decline of 23% in nonferrous metals is the balance resulting from increased use of aluminum and the decreased use of other nonferrous metals. In addition to the relative decline of the materials inputs (which basically represents a more efficient use of materials), Carter shows that

“the classical dominance of single kinds of material—metals, stone, clay and glass, wood, natural fibers, rubber, leather, plastics and so on—in each kind of production has given way by 1958 to increasing diversification of the bill of materials consumed by each industry. This development comes from interplay between keenly competitive refinement in the qualities of material and design backward from end-use specifications.”

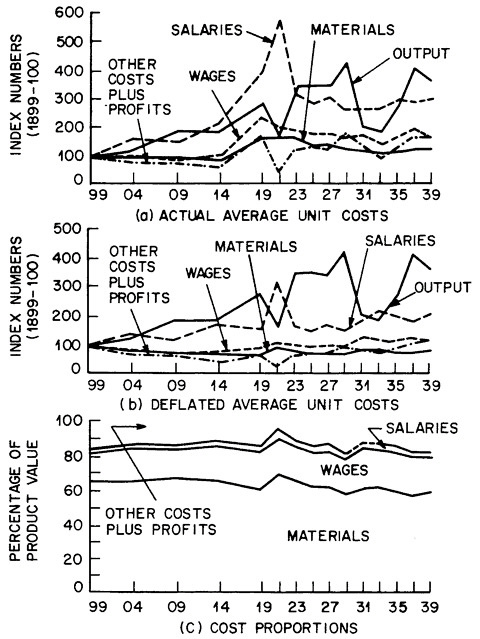

These interpretations of the influence of technological change appear to be in keeping with the results of a different type of economic analysis involving materials flows reported recently for an earlier period by Gold.3 For a variety of manufacturing industries, the influence of technological innovation over the 40-year period through 1939 was found not to be directly detectable in the proportioning among deflated unit costs (materials, wages, and salaries, and other costs plus profits) over this long-time series. The horizontal trend exhibited by the data (for steel-mill products in Figure 2.1) shows that the proportions of the cost components have remained approximately constant, despite the introduction of specific technological advances at known points in time. These observations do not mean an absence of benefits from technological progress, but rather that such progress was so pervasive in the economy at large that advances in a given industry simply maintained its competitive position with other industries. On this basis, the innovations have directly benefited consumers of a given industry’s products (in effect, much of the economic gain has been passed on to them), but have not provided much competitive advantage beyond that of effective survival in a given market.

The preceding discussion has indicated some of the principal economic measures and models for materials flows. An important contribution in relating these economic factors to the associated bulk flows is provided by the U.S. Bureau of Mines in an Analysis of the supply-demand relationships for mineral resources and commodities. In their 1970 report4 which covers

88 commodities, the emphasis of the analysis was broadened from an essentially “supply” orientation to include intermediate forms and end-uses. This change is especially important for the problem of predicting the evolution of future demand—such as is done in the analyses to the year 2000–but is also critical for the monitoring of materials flows at the present time. It, and the subsequent reports from the Secretary of U.S. Interior, provide specific information on a large group of resources that supplement still broader discussions of resource adequacy, such as those presented by Landsberg5 and the National Academy of Sciences study, Resources and Man6.

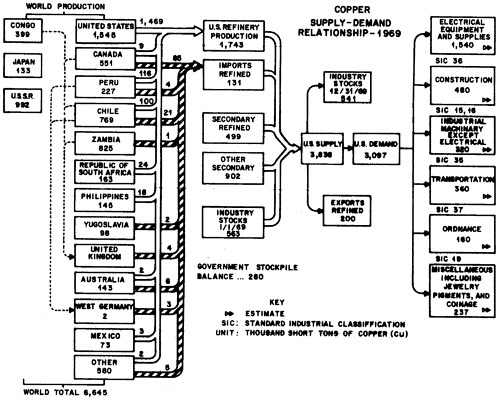

An example of the supply-demand data is shown for copper in Figure 2.2. The significant features of the data are that (a) the flow at any stage is expressed in terms of the mass of elemental metal, whether or not the commodity exists in that form at that stage, (b) the world sources of the metal that contribute to the total U.S. supply are delineated by country of origin, and (c) the resulting U.S. supply is broken down into industry stocks and exports as well as into the proportions going into specific industries (identified in terms of the Standard Industrial Classification developed by the U.S. Department of Commerce).

Data of the type provided by the Bureau of Mines analyses should permit the setting up of a bulk-flow model involving the 88 different commodities as elemental materials, although the present information does not appear to be sufficiently comprehensive with respect to the industrial classifications used. Thus, a square-matrix analog of the inter-industry type would be less complete and interpretable than for the economic model developed by Leontief. Furthermore, it is important to be able to identify the actual bulk flow at various stages rather than simply the elemental flow, and knowledge is also needed relative to the residuals developed at all stages as well as the extent of recycling and final disposal. Reliable statistical information on residuals in the form of both new scrap material (resulting during manufacture and processing stages) and old scrap (from the discarded unit or component after use by the consumer) is now becoming available through the efforts of various federal agencies and interested trade associations. However, such data are still incomplete, especially with respect to old scrap and its long-term accumulation from past activity. Furthermore, information on nonsolid discharges is particularly limited.

In the preceding discussions, the question of competition between variants of the same material (e.g. different alloys) and between different materials (e.g., plastics and metals) is visible as a significant factor in determining changes in materials flow with time. Such competition is one

aspect of the broader concept of substitution, which has emerged from an earlier restricted connotation of the use of an inferior material in a given application for a superior one that is limited in availability or higher in cost. Previously-used derogatory terms such as “cheap plastic” or “tinny” are indicative of that earlier meaning. However, perhaps one of the most important aspects of the revolution in the diversity of available technological materials is that the improved understanding of the science and technology of materials now offers a better basis for developing options in providing materials for specific needs, i.e. for providing substitutes that match or improve upon the performance of other materials. The continuing demand for materials in the future and the decreasing availability of specific materials as nonrenewable resources are consumed or become uneconomic, together with the restrictions imposed by the need to control environmental quality, will require a vigorous extension of this understanding of substitutions in the future. It may be even more useful to take into account the broadest interpretation of substitution. Thus, one should consider not only the materials-flow implications of substituting one material for another in the same class (e.g. aluminum for copper in electrical conductors) or for one in another class (e.g. fiberglass for ceramics in sewer pipes), but also of substituting an entire technology (e.g. transport by automobile rather than by horse or by aircraft rather than ship, electric power from nuclear fission or fusion rather than from fossil fuel).

Despite the shortcomings in the range of quantitative data available on materials flows in the United States, it appears that there is already sufficient information on past and present flows to merit assembling into an initial framework. A desirable first step in this direction has already been taken by the U.S. Bureau of Mines in the development of a computer-storage system for information on resource reserves. The expansion of such inventories to include the supply-demand data of the type in Figure 2.2, together with associated information on residuals and recycling, would be an appropriate next step. However, such inventories are essentially static models and the nature of the problems associated with our dynamic society require at least the exploration of possible dynamic models that would highlight the consequences of the complex interactions involved in materials flows on a national or international scale. One such approach would be to simplify the problem by restricting it to a consideration of mass flows between industrial sectors in an analog of the Leontief system. Here, the influence of changing technical or market opportunities or social demands would be inserted indirectly through changes in the output requirements of specific industries. This technique would permit the exploration of mathematical models for technological forecasting relating to future materials demands, such as that suggested by Fisher and Pry7. Also, with the development of appropriate input data, this method should be adaptable to accommodate more completely the full variety of flows operative in the total materials cycle.

An alternative approach is the even more ambitious and controversial systems-dynamics analysis developed by Meadows et al8 on the basis of the global model suggested by J.Forrester. Here, materials enter the model principally as natural resources and a component of pollution—which are two of the five basic factors (the other three being population, agricultural production, and industrial production) that are interacted and are considered in this model to place limits on ultimate growth on the planet. A major issue in the debate as to the validity of the conclusions reached from this global model—whether one considers the model predictive or, as the authors propose, only indicative of behavior modes to be expected if present trends continue—has been the reliability of the data-base available at the present time. Despite such controversy over the current use of the model, the approach itself does appear to offer an important new research tool for examining the interaction of major factors at play in continuing national or global development. The further exploration of this technique to study the dynamics of natural resource utilization, as has already been initiated, merits careful attention in order to improve man’s understanding of the changing characteristics of materials flows.

THE MATERIALS CYCLE AND THE ROLE OF MATERIALS SCIENCE AND ENGINEERING

All materials move in a “total materials cycle” (Frontispiece) which in this report we will simply call the “materials cycle.” From the earth and its atmosphere, man takes ores, hydrocarbons, wood, oxygen, and other substances in crude form and extracts, refines, purifies, and converts them into simple metals, chemicals, and other basic raw materials. He modifies these raw materials to alloys, ceramics, electronic materials, polymers, composites, and other compositions to meet performance requirements; from the modified materials he makes shapes or parts for assembly into products. The product, when its useful life is ended, returns to the earth or the atmosphere as waste. Or it may be dismantled to recover basic materials that reenter the cycle.

The materials cycle is a global system whose operation includes strong three-way interactions among materials, the environment, and energy supply and demand. The condition of the environment depends in large degree on how carefully man moves materials through the cycle, at each stage of which impacts occur. Materials traversing the cycle may represent an investment of energy in the sense that the energy expended to extract a metal from ore, for example, need not be expended again if the metal is recycled. Thus, a pound of usable iron can be recovered from scrap at about 20% of the “energy cost” of extracting a pound or iron from ore. For copper the figure is about 5%, for magnesium about 1.5%.

Materials scientists and engineers work most commonly in that part of the materials cycle which extends from raw materials through dismantling

and recycling of basic materials. Events in this (or any other) area typically will have repercussions elsewhere in the cycle or system. Research and development, therefore, can open new and sometimes surprising paths around the cycle with concomitant effects on energy and the environment. The development of a magnetically-levitated transportation system could increase considerably the demand for the metals that might be used in the necessary superconducting or magnetic alloys. Widespread use of nuclear power could alter sharply the consumption patterns of fossil fuels and the related pressures on transportation systems.

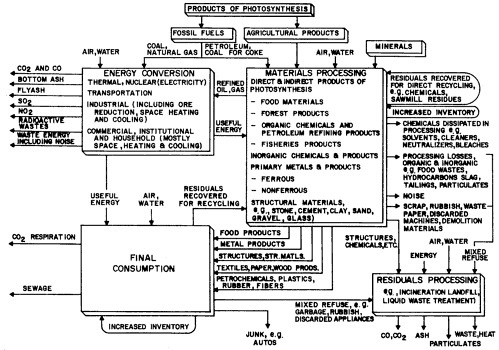

The materials cycle can be perturbed in addition by external factors such as legislation. The Clean Air Act of 1970, for example, created a strong new demand for platinum for use in automotive exhaust-cleanup catalysts. The demand may be temporary, since catalysis has been questioned as the best long-term solution to the problem, but whatever platinum is required will have to be imported, in large measure, in the face of a serious trade deficit. Environmental legislation also will require extensive recovery of sulfur from fuels and from smelter and stack gases; by the end of the century, the tonnage recovered annually could be twice the domestic demand. Such repercussions leave little doubt of the need to approach the materials cycle systematically and with caution. Some of the general characteristics of materials flows and interactions that would have to be taken into account in a model of the materials cycle are indicated in Figure 2.3 which was developed as a qualitative concept by Ayres and Kneese for dealing with the problem of residuals and recycling in relation to environmental quality.

It is readily apparent from an examination of Figure 2.3 that the currently limited knowledge concerning the materials flows operating on a world scale make it impractical to apply any comprehensive quantitative model except extremely crudely. However, on the scale of a single country, especially one such as the United States for which rather extensive statistical records of commodity flows are maintained, there is a greater likelihood that a satisfactory quantitative model for the overall materials cycle might be developed. The delineation of the critical information needed as inputs to provide a working quantitative description of the materials fluxes would be helpful not only for improving the model for highly industrialized countries, but also for indicating the minimum information needed from developing countries in order to develop more global models.

A quantitative model of the flux (rate of flow expressed in terms of mass per unit of time) of materials in the United States should be capable of giving valuable information for:

-

assessing the importance of materials in the national economy and their changes with time;

-

assessing the consequences of changes in the availability or demand for specific resources in the future;

-

examining the impact of changes in the materials flow in various sectors resulting from substitution of specific materials (whether for competitive, international, or environmental reasons) on the demand for materials in other sectors; and

-

estimating the changes in type and quantity of residuals that may result from changes in the materials used for given applications or from changes in the technology adopted for preparing and processing the materials.

INNOVATION IN THE MATERIALS FIELD

The Materials Revolution

Man historically has employed materials more or less readily available from nature. For centuries he has converted many of them, first by accident and then empirically, to papyrus, glasses, alloys, and other functional states. But in the few decades since about 1900, he has learned increasingly to create radically new materials. Progress in organic polymers for plastics and rubbers, in semiconductors for electronics devices, in strong, lightweight alloys for structural use has bred entire industries and accelerated the growth of others. Engineers and designers have grown steadily more confident that new materials somehow can be developed, or old ones modified, to meet unusual requirements. Such expectations in the main have been justified, but there are important exceptions. It is by no means certain, for example, that materials can be devised to withstand the intense heat and radiation that would be involved in a power plant based on the thermonuclear fusion, although the fusion reaction itself is not primarily a materials problem.

This expanding ability to create radically new materials stems largely from the explosive growth that has occurred during this century in our scientific understanding of matter. Advances in knowledge also have contributed much to the unifying ideas of materials science and engineering—wave mechanics, phase transitions, structure/property relationships, dislocation theory, and other concepts that apply to many classes of traditionally “different” materials. Certain semiconductor materials are perhaps the archetypal example of the conversion of fundamental knowledge to materials that meet exacting specifications. Our basic understanding of most materials, however, falls short of the level required to design for new uses and environments without considerable experimental effort. Hence, it is important to keep adding to the store of fundamental knowledge through research, although much empirical optimization will probably always be needed to deal with the complex substances of commerce.

An example of the latter is graphite which recently has solved important problems in missiles for rocket nozzles and as structural components in nuclear—power reactors. Yet, the necessary development was achieved by an enlightened empirical approach in a company which was very much material-source oriented. Graphite is a most complex material whose physical properties depend on the nature and processing of raw materials, on the quality of the initial carbon-containing material, on binder pyrolysis, and on a variety of processing variables. The most practical approach to development of a special graphite to withstand high temperature and pressure was a systematic study, therefore, of the dependence of properties on processing parameters. The starting point was an initial observation that hot pressing of normal-density carbon yields a body of high density and high strength. Science was able to provide only a very general framework for the planning

and execution of this program. This case history also illustrates a governing feature of the traditional approach to materials development. Without a complete science framework and lacking even a few broad unifying concepts, the practitioner in graphite development necessarily needed to know a very large collection of facts based on past experience in graphite. For that reason, he was material-source oriented and tended to be more affiliated with the material-supplier than with the material-consumer.

In recent decades, however, the interest in materials properties has been broadening from that of the supplier to include that of the consumer. In some programs, such as aerospace and solid-state electronics, the material user has not been able to meet all his objectives with presently existing materials. This, in turn, has often caused the user to become involved in the discovery and development of completely new materials. It has also resulted in a closer working relationship between the material developer and the material user. Further, the programs which have run into materials limitations of the kind that determine success or failure tend, in general, to be those which are straining for the utmost out of sophisticated science and technology throughout the program.

The Systems Approach

Thorough systems analysis has been used to a moderate extent in materials science and engineering, but it must become basic to the field in view of the complexity of modern materials problems and of the fact that the materials cycle itself is a vast system. The need for the systems approach is apparent in the ramifications of replacing copper wire with aluminum in many communications used where the substitution would not have worked well until a few years ago. The move was triggered by changing relative prices and supply conditions of the metals. A research and development program produced aluminum alloys with the optimum combination of mechanical and electrical properties. The aluminum wire still had to be somewhat larger in diameter than copper wire, however. Thus, wire-drawing machines had to be redesigned, in part to avoid residual strain in the aluminum wire. Thicker wire, in addition, requires larger conduits, which take more space. And new joining techniques were necessary to avoid corrosion mechanisms peculiar to the aluminum wire.

Products like nuclear reactors, jet engines, and integrated circuits are systems of highly interdependent materials, each carefully adapted to its role in the total structure. The reaction of such a system to a breakdown at one point is evident in the intended use of a promising graphite-epoxy composite for the compressor blades of a British engine for an American jet airliner. The material was not developed on schedule, to the required degree of service reliability. The repercussions reached well beyond the resulting redesign of the engine. The respective governments were compelled to extricate both companies involved from financial crises, in an atmosphere of sharp debate over domestic and foreign policy.

Science-Intensive and Experience-Based Technologies

Science-intensive technology is used to designate those activities in which specific performance is at a premium and in which the generation of new fundamental understanding of materials is necessary before the desired performance can be achieved. Hence, the descriptor, science-intensive technology or sometimes high technology, usually denotes an emerging area where knowledge and practice are changing rapidly and where a widely based fund of experience and practical knowledge has not yet accumulated.

A familiar example illustrating high technology is the space program where it is mandatory that a component should function in the desired manner at the proper time. Because the entire success of an expensive mission may depend upon the proper functioning of this component, it is natural to expend whatever research and development is required to assure success. The actual cost of the materials making up the component becomes a secondary consideration. Another example is found in nuclear-power reactors. Fuel cladding must be of sufficient integrity to guarantee against hazardous release of radioactive by-products. In the design and fabrication of the fuel cladding, substantial effort at a sophisticated scientific and engineering level is justified to achieve reliability. In the solid-state electronics industry, we have an example in which highly sophisticated and costly effort on materials is warranted in terms of the overall product value; both the processing of semiconductor material and the assembly into discrete devices or integrated circuits require a degree of control which would be incredulous in most industrial situations.

Experienced-based technology, or low technology, refers to programs which are not science intensive—in other words, which rely on more empirical approaches or which may be relatively forgiving of manufacturing processing variations. Typically, large material quantities are involved so that unit material costs are important. Examples are the manufacturing of dishes and structural steels; many tires are assembled in traditional ways involving much hand work; long-standing approaches prevail in the construction of roads and highways where unit cost is of great importance; and the paper industry continues to use empirically-derived processes.

Pace of Innovation

There is a familiar pattern in the growth, development, and diffusion of a technology. At the birth and in the early stages of a technology, such as solid-state electronics or nuclear-power reactors, the pace of invention is high and the innovating company or nation may well achieve a commanding position in the market for its new technology. In this pre-marketing stage, cost is of secondary importance, or rather, is an administrative decision related to some perception of the eventual pay-off. Later, the inventive pace begins to slacken while, at the same time, other companies or nations with necessary educational level and technical competence are acquiring the knowledge and skills so that they may catch up. The formerly-commanding position of the original innovator is gradually eroded as the relevant technological capability diffuses nationally and internationally. In this

stage, where the technology is termed as becoming mature, commercial advantage is kept by, or passes to, that company or nation which can most effectively minimize production and marketing costs while safeguarding the integrity of the product. Process innovation can then assume more importance than further product innovation.

The early stage of a technology, when the inventive pace is high, is often science-intensive. It seems that the high technologies in which the U.S. has been in the forefront, e.g. aerospace, computers, and nuclear reactors, have also been generally associated with international trade surpluses for the U.S. In the more mature stages, the science content of further developments in the technology is usually lessened, and the technology can be referred to as experience-intensive. Such technologies are more readily assimilated than high technologies by developing countries and are more likely to be associated with trade deficits for the U.S. inasmuch as the developing countries tend to enjoy lower costs, primarily through lower labor rates. When a technology reaches this phase, the U.S. runs the risk of becoming quite dependent for further developments in that technology on foreign enterprise. This may be acceptable for some technologies but not for others critical to national economic and military security. The primary metals industries are prime examples of such experience-based technologies facing severe foreign competition. Other industries in which technological leadership may have been lost by the U.S. are tires, and various consumer goods such as shoes and bicycles. Still other technologies, some of which are regarded as high technologies, are moving in the same direction, e.g., automobiles, consumer electronics, and certain aircraft products.

The implications for materials technology in the U.S. in order to meet foreign competition and maintain viable domestic industries are that high inventive pace must be created or maintained in certain fields so as to generate new high technologies and safeguard existing ones, and that the technological level must be raised and production costs lowered in selected, critical, mature industries. This must be done within the structure of U.S. industry which can be roughly classified, for our purposes, into the materials-producing and the materials-consuming industries. The former tend to be in the low-technology category, and the latter in the high-technology category. The high-technology industries, if their commercial bases are sufficiently large, are more accustomed to maintaining a balanced, but product-oriented, R and D effort than are the low-technology industries.

Disciplinary to Interdisciplinary

In the materials field, university departments have typically evolved along disciplinary lines—physics, chemistry, metallurgy, ceramics, polymers, with each discipline tending to specialize (as its name often indicates) in a particular class of materials or in a special approach to materials. Similar segmentation is apparent in the industrial sphere, with some industries specializing in metals, others in ceramics, in glass, in chemicals, or in crystalline materials for electronics. In addition, there has tended to be some separation in another direction, between materials science on the one hand, embracing the traditional scientific disciplines, and materials

engineering on the other, embracing those parts of the engineering disciplines concerned with the processing and application of materials.

Such segregation is feasible only when the technical objectives, scientific or engineering, are relatively straightforward. For example, metallurgists may have all the requisite knowledge, both of the engineering requirements as well as the scientific and materials aspects, to cope with the problem of developing improved alloys for use as electrical conductors. In such a case, the customary, disciplinary approach can be quite adequate for pursuing a problem from the research phase to the production phase. But nowadays the trend in technology is towards ever more complex performance requirements, product and device designs, and dependence on more sophisticated knowledge of the physical phenomena that can be produced in an increasing diversity of materials. The areas of knowledge required to develop, say, an integrated circuit or a biomedical material are not at all coincident with the traditional disciplinary boundaries. It is obvious that many complex technologies call for knowledge and skills that cut across several disciplines, including science and engineering. Thus, we see an increasing need for interdisciplinary approaches in order to achieve technical objectives.

But the interdisciplinary approach is by no means limited to applied research and development programs. The same is happening in basic research in materials. The very core of materials science, the relation of properties to structure and composition, implies a need for the combined efforts of physicists, metallurgists, chemists, etc. In the past, the physicist has too often made unrealistic assumptions about the composition, purity, and quality of his research materials; the metallurgist has too often not understood sufficiently how the physical phenomena exhibited by a solid relate to its structure and composition.

Materials research provides a natural meeting-ground for professionals from the various scientific and engineering disciplines, from basic research to applied research, development and engineering. Clearly, the pressure for such interdisciplinary collaboration can only grow in the future.

MATERIALS IN A CHANGING CONTEXT

Materials and the associated science and engineering exist in a social and economic context that has changed markedly during the past decade. A pertinent indicator is the National Colloquy on Materials Science and Engineering held in April 1969: the proceedings9 took virtually no notice of the field’s close ties to the environment, an omission that could hardly occur today. Materials are involved also in other kinds of change: the energy crisis, the nation’s problems with the balance of trade, federal efforts to stimulate and to assess technology; changing patterns in spending on basic and applied research and between civilian-oriented and defense- or space-oriented research and development; and the growing federal awareness of the importance of materials.

Two fundamental parameters in these matters are population growth and higher incomes. Between 1900 and 1970, the population of the U.S. rose 270%, to just under 205 million. For the year 2000 the Bureau of the Census projects a minimum population of 251 million and a maximum of 300 million. Percapita Gross National Product in constant 1958 dollars, meanwhile, has risen steadily, from $1351 in 1909 to $3572 in 1971. Both population and percapita GNP are expected to continue to grow, making ever more urgent the solution of materials-related problems.

Changing National Priorities

The materials system was shaped during World War II by diverse groups of commodity-oriented industries, educational disciplines, and technical societies, in response to the defense requirements for materials-limited hardware. This system was sharpened in the postwar era. It took the form of industrial faith in the profitability of materials research and development, an anticipated shortage of professionals in the materials field, and the materials needs of national programs for nuclear, aerospace, and defense hardware. During this period, commercial jet-powered air transportation, nuclear-power plants, space trips to the moon, and military operations in Korea and Viet Nam placed further emphasis on materials requirements.

Newly emerging national goals related to social needs, the state of the economy, and a de-emphasis of space, nuclear, and defense priorities led to a retrenchment in industrial research and development, a surplus of technical manpower in certain sectors, and the authorization of government-financed programs on housing, health and safety, energy, environmental control, transportation, recreation, and urban renewal.

Industries which were once commodity-oriented then diversified into market-oriented or integrated conglomerates; uncertainties arose as to whether or not materials science and engineering might be a technology or an educational discipline; governmental agencies became interested in technologies which were limited more by economics than by materials; and technical societies sought to re-group in response to the needs of interdisciplinary fields such as construction, pollution control, health and safety, etc. Since materials were available for hardware related to these requirements (except electronics), attention was focussed on the costs of housing, pollution control, health and safety, etc.—with emphasis on the processing of materials into the necessary hardware and its performance.

Operational research evaluating the costs of goods and services in comparison with their values as judged by the beneficiary led to reductions in industrial research in certain corporations concerned with steel, polymers, automobiles, electronics, exotic materials for aerospace, and also in free inquiry with expected but undefined rewards. The government began to focus on science and technology oriented toward national leadership in world economic competition and toward societal problems in education, energy, health, transportation, housing, and pollution abatement. The federal role stressed the need for additional mission-oriented industrial RD & E, and federal participation tended to be limited to projects of large national impact where the required resources were too large or too risky for

corporate undertaking. This participation might take the form of direct support of joint ventures, or incentives resulting from changes in taxation and regulatory restraints.

Federal, state, and local support for education is also undergoing careful scrutiny under a new set of value-judgments and an apparent lack of professionals who are knowledgeable in emerging civilian technologies. The role of technical societies as communication media for professionals vis-a-vis their effectiveness in these societal technologies is likewise being reexamined.

Materials Resources

Society is concerned with the cost, performance, and functional value of the end-product, and is only incidentally conscious of the materials being used. Walter R.Hibbard, past director of the U.S. Bureau of Mines, has said that most Americans “have no appreciation of the scientific and engineering accomplishments that have enabled them to keep receiving these benefits over the years at relatively constant costs”10.

Because of future prospects regarding decreasing supplies of traditional materials and the increasing promise of newer materials such as aluminum, plastics, semiconductors and nuclear fuels, it is more important than ever that people become familiar with the potential role of the science and engineering of materials. This evolving approach to materials, eventually affecting almost all of the goods and services with which we are familiar, will inevitably have a great influence on this nation’s economic, aesthetic, and social well-being.

Striking changes are well under way in the balance between materials needs and world trade. Qualified sources report that the United States has “rapidly deteriorating, and by now very large,” deficits in trade with minerals and raw materials, and with manufactured materials such as steel, textiles, and nonferrous metals11. But exports of finished products, which could help to offset these deficiencies, also are in a deteriorating position.

We are faced with the same question whether we are concerned with the depletion of the world-wide reserves or the deficiency of natural materials in the U.S. How can technology use our more available materials and less of scarce materials, to make improved products economically, and in quantities to keep pace with growing demand?

By 1980, our national need of materials is expected to be 40% greater than it is today, and today we require a greater supply of materials than at any previous time in our history. The U.S. already depends on foreign

supplies for most of its tungsten, chromium, manganese, platinum, mica, bauxite, cobalt, nickel, asbestos, and about a dozen other mineral commodities. Also, current engineering applications of zinc, nickel, copper, cobalt, lead, tin, and the precious metals are feared to be rapidly depleting these resources.

William J.Harris, Jr., a past executive director of the Materials Advisory Board, calls attention to the countervailing trend, however, that during the last three decades “there have been more significant advances in a wider range of materials than in any comparable period in the history of the world.”12

As an instance of how new technology has generally enabled industry to keep pace with growing demand, Hibbard13 gives the example that “output from our mines has risen almost as steadily as the mineral values in the extracted ores have diminished.” In particular, at the turn of the century, typical ore grades from copper mines were about 5% copper. The average grade of copper deposits mined today in the U.S. is less than 1% copper—about 14 pounds per ton. And new technology may make it practical to mine down to 4 pounds per ton. Although our copper grades have decreased, technology still allows us to produce copper at a reasonable price.

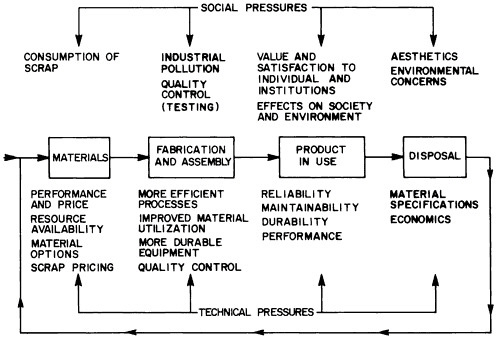

While improved extraction technology may ease our dependence on foreign sources of raw materials, improved technology in the other stages of the materials cycle will also greatly enhance our materials utilization. Figure 2.4 illustrates some of the social and technical pressures important at various stages of the economic utilization of materials. Clearly, a strong materials technology is required for industry to be responsive to these pressures in the production of goods at reasonable costs.

Besides the direct application of materials science and engineering to technology, innovation in the field can have important consequences for materials demand and consumption patterns, the consumption of energy, and the quality of the environment. Materials science and engineering can play a vital role in meeting man’s needs for better transportation equipment, prosthetic devices, and new energy generation, transmission and storage methods. By wreaking these technological changes, it can often change drastically the consumption patterns for materials and energy. New materials made from more abundant raw materials can often be developed as substitutes for old ones made from scarcer or ecologically less desirable raw materials; new ways can often be found for performing needed technological functions, e.g. transistors have replaced vacuum-tube triodes as basic amplifying elements in electronic circuits,and integrated circuits have replaced boxes of complex electronic equipment assembled from discrete components. Looking ahead with another example, present work in certain forms of levitated ground transport, if successful, could lead to greatly increased demands for new magnetic or superconducting alloys. Or again, development of suitable catalysts based on relatively abundant materials could significantly reduce the demand for platinum catalysts in treating automobile exhaust gases.

Energy, Environment

Materials, energy, and the environment are closely interrelated. The emergence of energy as a national problem of the first rank was reflected in mid-1973 in the President’s establishment of a White House Energy Policy Office and his call for drastically increased federal spending on energy R & D. At the same time the President asked Congress to authorize a Cabinet-level Department of Energy and Natural Resources and the splitting of the Atomic Energy Commission into an Energy Research and Development Administration and a Nuclear Energy Commission. The energy problem also is reflected in the formation of the Electric Power Research Institute (EPRI) by public and private utilities that account for about 80% of the nation’s generating capacity. This Institute will supervise research and development for the electric utility industry and plans to spend some $100 million in 1974, its first year of full operation. EPRI will be funded by self-assessment of member companies and will also seek to work with the federal government and equipment manufacturers.

Materials science and engineering has much to contribute in virtually all phases of the energy field; making new forms of generation possible, e.g. by finding solutions to the problem of material swelling under radiation damage in nuclear reactors; enabling new systems of electrical power distribution, e.g. through superconducting or cryogenic transmission lines; finding more efficient ways to store energy, e.g. through solid-electrolytic batteries or fuel cells; and developing more effective ways of using and conserving energy, e.g. through optimized materials processing and manufacturing operations.

National concern for the environment has been recognized in the past few years by extensive federal legislation as well as by the creation of the Environmental Protection Agency and the Council on Environmental Quality. Environmental matters also achieved international status with the Stockholm Conference on the Human Environment, held in mid-1972 under the aegis of the United Nations General Assembly. This concern was formalized in December 1972 when the General Assembly established a new unit, the U.N. Environmental Programme.

In the field of environmental quality, materials science and engineering has much to offer in the development of cleaner materials processes, effective uses for waste materials, materials and designs more adaptable to recycling, and in instrumentation to monitor and control pollution.

The U.S. Trade Balance

Materials are important factors in this country’s balance of trade. The National Commission on Materials Policy has stated that, in 1972, the U.S. imported $14 billion worth of minerals (including petroleum) and exported $8 billion worth, for a net deficit of $6 billion. If the trends of the past 20 years persist according to the Commission, the deficit could top $100 billion annually by the year 2000. In 1970, the U.S. imported all of its primary supplies of chromite, columbium, mica, rutile, tantalum, and tin; more than 90% of its aluminum, antimony, cobalt, manganese, and platinum;

more than half of its asbestos, beryl, cadmium, fluorspar, nickel, and zinc; and more than a third of its iron ore, lead, and mercury. Certain science-intensive materials, on the other hand, including organic chemicals and plastics and resins, have produced, consistently, a positive balance of trade (Table 2.5).

The country’s balance of trade has suffered from growing imports of manufactured products. This has happened particularly with low-technology (experience-intensive) goods and, to a lesser extent, with high-technology (science-intensive) goods (even allowing for a degree of controversy over which is which). It appears, in fact, that the U.S. has lost its technological leadership in some product areas, although cause-and-effect relationships among research and development budgets, technological initiative, and foreign trade are difficult to establish clearly (and lie, in any case, beyond the purpose of COSMAT).

The federal government has initiated modest efforts to stimulate civilian research, development, and innovation, so as to help recover technological initiative (which may have been lost, for example, in steel and titanium). The goal is to make U.S. products more competitive at home and abroad, and much of the emphasis will be on manufacturing technology, including materials shaping, forming, assembly, and finishing. The federal efforts include the Experimental Technology Incentives Program of the National Bureau of Standards in the Department of Commerce and the Experimental R&D Incentives Program of the National Science Foundation.

Technology Assessment

Technology assessment has long been practiced, in varying degree, in both industry and government, but a formal federal apparatus was established only recently, by the Technology Assessment Act of 1972. The Office of Technology Assessment and other mechanisms created by the Act are designed to give the Congress a stronger in-house grasp of the relative merits and side effects of alternative technologies. The Act did not establish a formal technology assessment function in the Executive Branch. The birth of the Office of Technology Assessment appears nevertheless to be stimulating similar efforts in parts of the Executive Branch.

The increasing diversity and complexity of technological products and the materials, often unfamiliar, from which they are made have posed increasingly severe burdens on the average consumer. As a result, consumers have become more concerned with the reliability, durability, safety, flammability, and toxicity of products. These pressures, in turn, translate into new challenges to materials science and engineering, introducing additional performance specifications alongside the more traditional ones.

The Federal Approach to Materials

The federal government has not yet developed a comprehensive national policy on materials. Materials-related responsibilities are diffused among a variety of formal and ad hoc committees and advisory groups, such as the

TABLE 2.5 U.S. Trade Balances in Illustrative Product Categories

|

|

1960 |

1965 |

1970 |

|

Aircraft and Parts |

$1187 |

$1226 |

$2771 |

|

Electronic Computers and Parts |

44 |

219 |

1044 |

|

Organic Chemicals |

228 |

509 |

715 |

|

Plastic Materials and Resins |

304 |

384 |

530 |

|

Scientific Instruments and Parts |

109 |

245 |

407 |

|

Air Conditioning and Refrigeration Equipment |

135 |

207 |

374 |

|

Medical and Pharmaceutical Products |

191 |

198 |

333 |

|

Rubber Manufacture |

108 |

119 |

–28 |

|

Textile Machinery |

104 |

54 |

–37 |

|

Copper Metal |

–62 |

–132 |

–171 |

|

Phonographs and Sound Reproduction |

15 |

–36 |

–301 |

|

Paper and Paper Products |

–501 |

–481 |

–464 |

|

Footwear |

–138 |

–151 |

–619 |

|

TV’s and Radios |

–66 |

–163 |

–717 |

|

Iron and Steel |

163 |

–605 |

–762 |

|

Petroleum Products |

–120 |

–464 |

–852 |

|

Textiles and Apparel |

–392 |

–757 |

–1542 |

|

Automotive Products |

642 |

972 |

–2039 |

|

Source: U.S. Department of Commerce |

|||

Interagency Council for Materials. The Government is assisted also by groups like the National Materials Advisory Board and the Committee on Solid State Sciences in the National Research Council. The gradual emergence of a more coherent federal approach to materials questions, however, would appear to be implicit in certain developments of the past few years.

The Resource Recovery Act of 1970 created a National Commission on Materials Policy, whose charge was “to enhance environmental quality and conserve materials by developing a national materials policy to utilize present resources and technology more efficiently, to anticipate the future materials requirements of the nation and the world, and to make recommendations on the supply, use, recovery, and disposal of materials.” The Commission reported to the President and to the Congress in June 1973.

The Mining and Minerals Policy Act of 1970 requires the Department of the Interior to make annual reports and recommendations for action in relation to a national minerals policy. The Second Annual Report under this Act was published in June 1973.

The creation of a Materials Research Division in the National Science Foundation brought into clearer focus the existence of a multidisciplinary materials-research community.

Recent years have also seen considerable interest in the idea that the earth’s finite content of resources for industrial materials (including fuels) restricts severely the industrial growth that traditionally has been considered the basis of economic and societal health14. This concept of “limits to growth,” and the related idea of a “steady-state society,” are not within the scope of this study. They are, however, further indications of the changing context in which materials science and engineering exists and in which, we believe, the field has vital contributions to make.

NATIONAL AND INSTITUTIONAL CAPABILITY

Materials activities are clearly sizable in this country, where 6 percent of the world’s population accounts for somewhere between a quarter and a half of the world’s annual consumption of natural resources. The U.S. is very strong in materials science and engineering, but certain weaknesses, if unattended to, could progressively erode the nation’s capability to meet the materials needs of its people. These weaknesses are due in part to the diffusion of responsibility for materials plans and programs at the federal level. To a considerable degree, the same diffusion of responsibility is found in the universities, in both education and research. Contributing also to weaknesses in materials are shortcomings in the generation and application of basic knowledge.

National capability in materials science and engineering relies on the trained manpower and basic knowledge produced by the universities and on the application of basic knowledge by industry and other mission-oriented institutions. An organization is better able to assess and exploit new knowledge

generated elsewhere when it is able itself to generate new knowledge. Thus, knowledge moves more readily from the universities to industry when companies do an appropriate amount of well-chosen basic research. It moves more efficiently also when universities conduct an appropriate amount of applied research. Current difficulties on both scores are pointed out later in this chapter under Universities and Industrial Research and Development.

The importance of materials suggests that materials science and engineering should be a prolific producer of knowledge. That this is so is indicated by the literature as abstracted in Chemical Abstracts. In 1970, 276,674 papers and patents were abstracted, of which 45 percent were in materials science and engineering. Over the past two decades, the world-wide literature in materials science and engineering has maintained an annual growth rate of 9 percent, whereas the annual growth rate for Chemical Abstracts as a whole has dropped from 8.8 percent in 1950–60 to 6.7 percent in 1960–70. Materials literature originating in the U.S. has been growing in recent years at 11 percent annually as compared with 13 percent for the U.S.S.R. The latter country overtook the U.S. in materials publications as far back as 1957. The U.S. produced about 25 percent of the materials papers in 1970; the U.S.S.R. 33 percent; and Japan 5.8 percent. In the U.S., educational institutions were the chief source (50%) of the materials literature, followed by industry (25%),and government (15%). The U.S. Accounted for 40 percent of the patents in 1970, and Japan 12.9 percent.

Manpower

Existing data on scientific and engineering manpower generally are not categorized along the multidisciplinary lines of materials science and engineering. We have used a list of specialties characterizing the field, therefore, to extract manpower data from prime sources. On this basis, it appears that materials science and engineering involves some 500,000 of the 1.8 million scientists and engineers in the U.S. We estimate (Table 2.6) that there is a full-time equivalent of 315,000 scientists and engineers in the field, including about 115,000 full-time practitioners. Within the latter group are approximately 50,000 professionals holding materials-designated degrees. Engineers, even without counting the materials-designated professionals, constitute the largest manpower group in materials science and engineering; they number 400,000 individuals, and correspond to a full-time equivalent of some 200,000. The situation with respect to women and minority groups in the materials field appears to be no different from that in science and engineering generally.

The current state of manpower data for materials science and engineering, and our knowledge of the relevant patterns of manpower flow, are such that nothing exceptional can be said of the field in comparison with the traditional disciplines, provided that external factors remain essentially unchanged. However, as the role of materials science and engineering in meeting societal needs becomes more widely understood, particularly in connection with energy and environmental problems, it is quite likely that there will be an increasing demand for scientists and engineers in the materials field.

TABLE 2.6 Estimates of Manpower in Principal Disciplinary Sectors of Materials Science and Engineering

|

|

Full-Time Equivalent |

||

|

Discipline |

Total Manpower |

MSE Manpower |

|

|

|

Total |

Doctorates |

|

|

Chemists |

150,000 |

50,000 (16%) |

19,000 (51%) |

|

Physicists |

45,000 |

15,000 (5%) |

8,000 (22%) |

|

Metallurgists |

40,000 |

40,000 (13%) |

5,000 (13%) |

|

Ceramists |

10,000 |

10,000 (3%) |

1,000 (3%) |

|

Other Engineers |

1,200,000 |

200,000b (63%) |

4,000 (11%) |

|

|

1,445,000a |

315,000 (100%) |

37,000 (100%) |

|

Note: A detailed profile of scientists and engineers in the field of materials is presented in Appendix 2A of this chapter (pp. 2–58 to 2–93). a The total number of scientists and engineers in the U.S. is about 1.8 million b Approximately 400,000 engineers are involved significantly in materials science and engineering. We estimate, conservatively, that they divide their efforts equally between materials and other engineering activities and thus are equivalent to 200,000 engineers working full time in materials. |

|||

It should be emphasized that the boundaries of materials science and engineering are blurred and continually evolving. The central disciplines and subdisciplines include solid-state physics and chemistry, polymer physics and chemistry, metallurgy, ceramics, and portions of many engineering disciplines. In a broad sense, the field also includes segments of mechanics; of organic, physical, analytical, and inorganic chemistry; and of chemical, mechanical, electrical, electronic, civil, environmental, aeronautical, nuclear, and industrial engineering (Table 2.7).

Trends in Basic and Applied Research

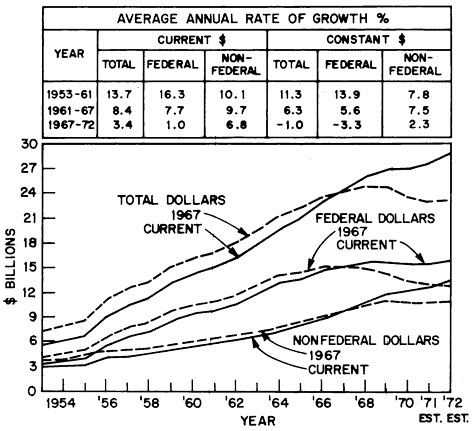

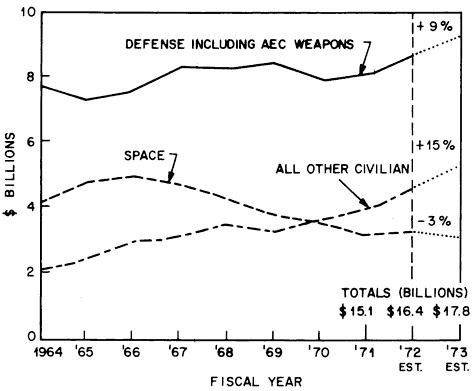

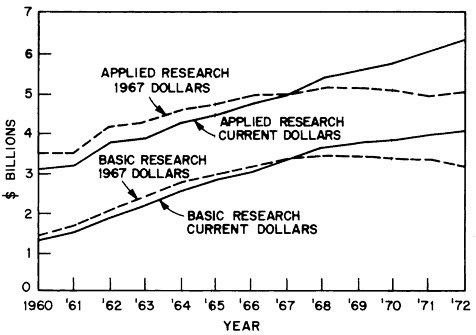

The relative economic austerity of the past few years has been felt in basic and applied research in both industry and government. Nonfederal spending on research and development has virtually leveled off (in constant dollars), while federal spending has been declining (Figure 2.5). In current dollars, total federal spending on research and development has been rising slowly since 1970, but the emphasis has been shifting away from defense and space toward civilian-oriented areas (Figure 2.6). Expenditures on space have been falling, while spending on domestic programs has been rising slightly faster than on defense research and development (although starting from a much smaller base). In constant dollars, federal spending on both basic and applied research leveled off in the late 1960’s; more recently, spending on basic research has declined slightly, while that on applied research has risen slightly (Figure 2.7).

Government Support of Materials Science and Engineering

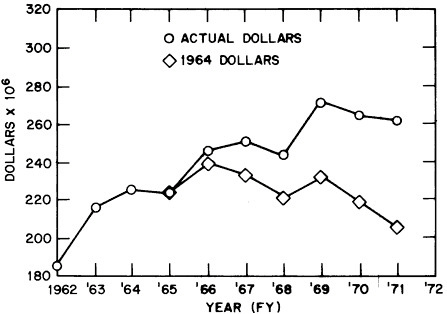

Materials science and engineering has been shaped in a major way during the past two decades by federal research and development programs that evolved in response to national needs and goals. Direct federal funding of materials R&D (which amounted to 1.7 percent of the total federal R&D budget) totaled some $260 million* in fiscal 1971, according to the Interagency Council for Materials; in constant dollars this figure is about equivalent to the $185 million spent in fiscal 1962 (Figure 2.8). (Indirect federal funding of materials R&D through hardware contracts is conservatively estimated to equal direct funding, giving a total of some $0.5 billion in federal materials R&D in 1971. A breakdown of how the federal funding of materials R&D has changed from 1967 to 1971 is given in Tables 2.8 to 2.12.

More detailed data on how the federal support of materials R&D by Agency, Type of Research, and Performer are given in Table 2.13, and by Agency and Class of Materials in Table 2.14. Only one agency, the National Science Foundation, has an identified mandate to support science and technology

TABLE 2.7 Distribution of Materials Scientists and Engineers by Category of Activity

|

Category |

% of Professionals in Category Who Are in MSE |

% of Total MSEa |

|

|

FROM THE SCIENCE REGISTER |

|

||

|

Polymer and Organic Chemistry |

51 |

6.7 |

|

|

Physical Chemistry |

76 |

3.4 |

|

|

Analytical Chemistry |

60 |

2.6 |

|

|

Solid-State Physics |

93 |

2.0 |

|

|

Inorganic Chemistry |

85 |

1.8 |

|

|

Other Physics |

17 |

1.6 |

|

|

Other Chemistry |

15 |

1.5 |

|

|

Atomic and Molecular Physics |

96 |

0.7 |

|

|

Optics |

38 |

0.5 |

|

|

Earth Sciences |

2 |

0.2 |

|

|

|

21% |

||

|

FROM THE ENGINEERS REGISTER |

|

||

|

Structural Engineering |

42 |

12.6 |

|

|

Metallurgical Engineering |

100 |

11.0 |

|

|

Electromagnetic Engineering |

42 |

10.2 |

|

|

Chemical Engineering |

92 |

9.5 |

|

|

Work Management and Evaluation |

18 |

8.8 |

|

|

Dynamics and Mechanics |

40 |

7.7 |

|

|

Engineering Processes |

60 |

5.4 |

|

|

Heat, Light, and Applied Physics |

75 |

5.4 |

|

|

Automation & Control Instrumentation |

45 |

4.7 |

|

|

Ceramic Engineering |

100 |

1.9 |

|

|

Information and Mathematics |

20 |

1.8 |

|

|

Other Engineering |

30 |

0.1 |

|

|

|

79% |

||

|

|

100% |

||

|

a The distributions between the science and engineering portions of this listing have been adjusted to 21% and 79% respectively, in accordance with the physics plus chemistry percentages shown in Table 2.6. Source: 1968 National Register of Scientific and Technical Personnel (National Science Foundation) and 1969 National Engineers Register (Engineering Manpower Commission) . |

|||

TABLE 2.8 Distribution of Federal Materials R&D Effort by Class of Materials

|

|

Percentage Effort |

|

|

Material |

1967 |

1971 |

|

Metallic |

39.3 |

37.5 |

|

Inorganic nonmetallic |

23.6 |

23.8 |

|

Organic |

20.3 |

20.6 |

|

Composite |

8.5 |

9.9 |

|

Fuels, lubricants, fluids |

2.4 |

2.0 |

|

Other |

5.9 |

6.1 |

|

|

100. |

100. |

|

|

($248.05M) |

($260.2M) |

TABLE 2.9 Distribution of Federal Materials R&D Effort by Research Activity

|

|

Percentage Effort |

|

|

Activity |

1967 |

1971 |

|

Basic Research |

41.0 |

37.5 ($ 97.6M) |

|

Applied Research |

54.7 |

53.8 ($140.0M) |

|

Experimental Development |

4.3 |

8.7 ($ 22.6M) |

|

|

100. |

100. ($260.2M) |