2

A Framework for Thinking About the Hydrogen Economy

This report concerns research and development (R&D) to advance the hydrogen economy, a transition to a national energy system envisioned to rely on hydrogen as the commercial fuel that would deliver a substantial fraction of the nation’s energy-based goods and services. While the focus of the report is on technology recommendations, the committee also recognizes that any technological change must take place within a larger economic and societal context. Therefore, this analysis begins with a perspective on the context in which the R&D programs of the Department of Energy (DOE) are embedded—a framework for thinking about a hydrogen economy.

OVERVIEW OF NATIONAL ENERGY SUPPLY AND USE

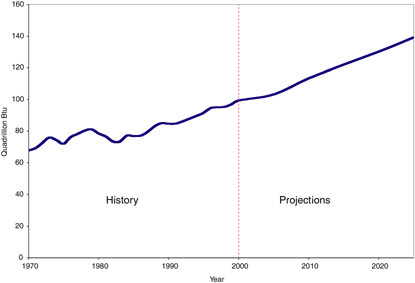

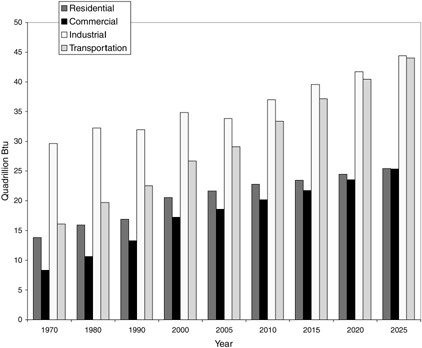

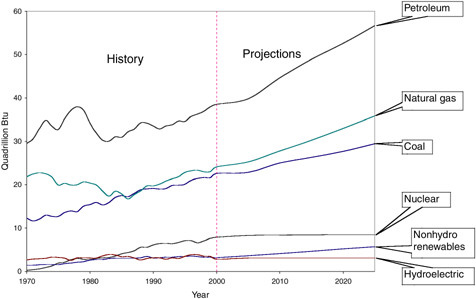

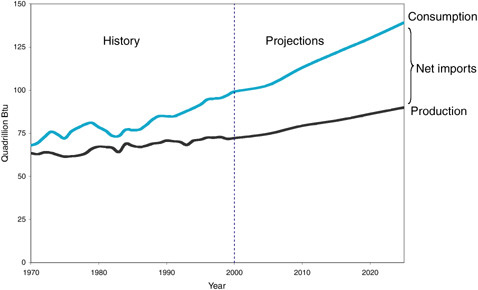

The transition to a hydrogen economy would begin in the context of a mature and reasonably efficient energy system; indeed, hydrogen technologies must compete effectively with that system if the transition is to occur at all. As shown in Figure 2-1, U.S. primary energy consumption has risen over recent decades, and is likely to continue increasing. To the consumers who contribute to this demand, energy is valuable not in its own right but rather as a source of products and services that are highly valued. In the United States, these services are customarily organized into sectors—residential, commercial, industrial, and transportation sectors—as shown in Figure 2-2. Fossil fuels overwhelmingly drive this consumption, as shown in Figure 2-3. Domestic production of energy, especially petroleum, has not kept pace with consumption (see Figure 2-4), resulting in increasing imports.

The national energy system contains great inertia, and several persistent trends will influence the energy economy well into the future. Most fundamentally, the Energy Information Administration’s Annual Energy Outlook 2003 (EIA, 2003) projects total energy consumption to increase at an annual average rate of 1.5 percent out to 2025, as shown in Figure 2-1. This increase is more rapid than projected growth in domestic energy production, leading to increasing dependence on imported fuels. For example, natural gas imports from Canada are projected by the EIA (2003) to provide 15 percent of the total U.S. natural gas supply in 2025, and liquefied natural gas (LNG) imports from overseas are expected to grow dramatically to 6 percent of the total from near zero today. While the Canadian imports can be presumed stable, the same cannot be said of the LNG imports that increasingly come from the most politically volatile regions of the globe. Import dependence for energy products is growing too. Refining capacity in the United States is projected to increase to nearly 20 million barrels per day in 2025, but this country will still depend on foreign refineries for roughly 33 percent of its petroleum products.

Over the same 2003–2025 time period, the EIA (2003) projects that CO2 emissions from energy use will rise in step with energy use, an average of 1.5 percent per year under current policies and practices. Atmospheric concentrations of CO2 are likely to increase. And though the environmental implications cannot be specified with precision, it seems reasonable to believe that as human activity continues to change the chemical content of the atmosphere, some kind of negative consequence will result.

ENERGY TRANSITIONS

The earliest transition to a modern energy system coincided with the Industrial Revolution. New ways to produce goods and services demanded large quantities of fuels with predictable burning characteristics. Fuels were tailored to the devices that burned them (steam engines, lamps, furnaces, and so forth), and these devices were designed around assumptions about fuels, a pattern that continues to the present day.

Over time, the fuels sector has undergone two kinds of transition. The first is a general trend toward greater efficiency in the use of energy to produce the goods and services desired by the world’s economy, coupled with structural

changes in developed economies away from manufacturing toward services. This tendency has been most pronounced in the United States, in which the energy intensity of the economy fell from about 70 megajoules (MJ) per constant dollar of gross domestic product (GDP) in the mid-19th century to about 20 MJ today (Schrattenholzer, 1998).

The second transition comprises a change in market share among the various commercial fuels; this change has favored fuels with lower ratios of carbon to hydrogen. In general, solid fuel has lost market share to liquid fuel, especially in transportation, where the greater energy density (energy per unit of volume) of the liquids offers significant advantages. More recently, the share of natural gas has grown steadily, though chiefly in stationary applications in which the lower energy density of natural gas presents no disadvantage. As an unintended consequence of this interfuel competition, the more carbonaceous fuels such as wood and coal have been superseded by less carbonaceous fuels such as oil and methane.

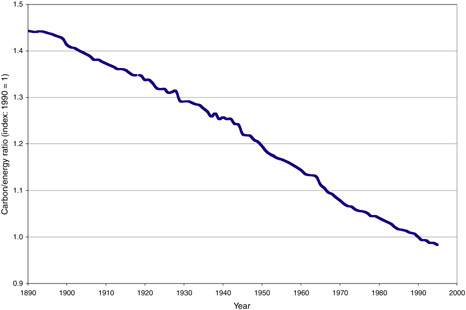

This substitution, together with the rise of knowledge-based industries, has caused a general reduction in the carbon intensity of the global economy—the amount of carbon released to the atmosphere per unit of primary energy—as shown in Figure 2-5. Even if no changes are made to the current energy infrastructure, this decline will probably continue into the future, driven by continued interfuel substitution and by the ongoing shift in the balance of value creation from heavy industry to a knowledge-based economy. Nevertheless, world carbon emissions continue to rise, despite this drop in carbon intensity, as economic growth outpaces business-as-usual improvements in both energy efficiency and carbon intensity (see Figure 2-6; EIA, 2003). The amount of carbon emitted varies widely around the globe, but its survival time in the lower atmosphere is sufficiently long that it is spread around by wind and becomes evenly mixed spatially across latitudes and longitudes (NRC, 2001b). The remainder of this chapter and the rest of the report, however, concentrate on hydrogen technology policies specifically for the United States.

MOTIVATION AND POLICY CONTEXT: PUBLIC BENEFITS OF A HYDROGEN ENERGY SYSTEM

Two public goals—environmental quality, especially the reduction of greenhouse gas emissions, and energy security—provide the policy foundation for the hydrogen programs of the DOE (DOE, 2003a). The first of these goals

FIGURE 2-5 Carbon intensity of global primary energy consumption, 1890 to 1995. SOURCE: Adapted from Arnulf Grübler, data available online at http://www.iiasa.ac.at/~gruebler/Data/TechnologyAndGlobalChange/. Accessed November 15, 2003.

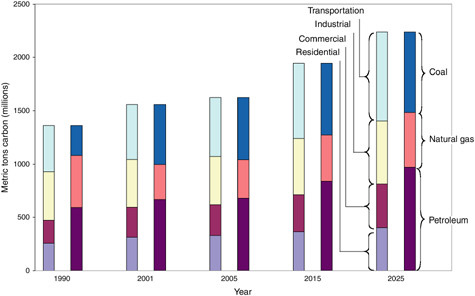

FIGURE 2-6 Trends and projections in U.S. carbon emissions, by sector and by fuel, 1990 to 2025. SOURCE: EIA (2003).

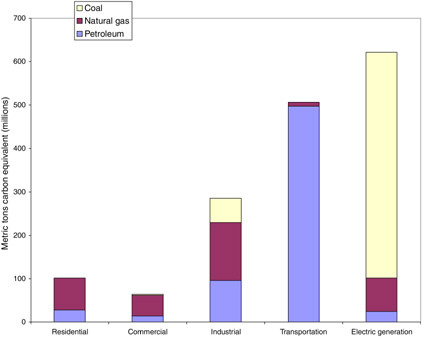

seeks to reduce emissions of criteria pollutants1 and the anticipated releases of carbon dioxide (and other greenhouse gases) into the atmosphere. In the United States, two intermediate demand sectors stand out as the source of much of the energy-related carbon: those involving (1) the burning of coal to produce electricity and (2) the burning of petroleum in transportation fuels (see Figure 2-7). Any hydrogen-based energy system must address these sectors in order to achieve the full environmental benefit of hydrogen energy. The second policy goal seeks to enhance national security by reducing the nation’s dependence on fuels imported from insecure regions of the world and on increasingly imported liquefied natural gas. These policy goals set two of the criteria that the committee used to weigh competing energy systems and technologies.

The dual policy goals described above intersect in the transportation sector, which has become the focus of much of the DOE hydrogen program (DOE, 2003a). Present-day transportation in the United States relies almost exclusively on petroleum and contributes an amount of carbon to the atmosphere nearly equal to that from coal used in electric power production (see Figure 2-7). Thus, in principle, the substitution of hydrogen for petroleum in ground transportation would benefit both goals. The benefits, however, accrue to the respective goals quite differently.

Consider, for example, a kilogram of hydrogen, produced in a way that does not emit carbon, displacing about 1.67 gallons of gasoline2 at some future time when hydrogen gains a meaningful share of the motor fuel market (in the committee’s scenarios presented in Chapter 6, sometime in the period 2025 to 2050). With regard to CO2 emissions, the benefit would be direct: the carbon that would otherwise have been emitted from the displaced gasoline is kept from the atmosphere. But with regard to energy security, the situation becomes more complex. This is so because the first petroleum displaced is as likely to come from high-cost foreign and domestic producers as from the low-cost Persian Gulf producers. Indeed, the market share of the Persian Gulf producers might actually rise as their higher-cost competitors are displaced. Thus, the most meaningful security gains could be achieved only if hydrogen were to displace essentially all petroleum used in ground transportation—around

|

1 |

Criteria pollutants are air pollutants (e.g., lead, sulfur dioxide, and so forth) emitted from numerous or diverse stationary or mobile sources for which National Ambient Air Quality Standards have been set to protect human health and public welfare. |

|

2 |

A gasoline hybrid electric vehicle having fuel economy of 45 miles per gallon would travel as far on 1.67 gallons of gasoline as would a fuel cell vehicle on 1 kilogram of hydrogen, assuming that the efficiency of the latter is 75 miles per kilogram of hydrogen. The committee’s assumptions about efficiencies for the different vehicle and power plant types are discussed further in Chapter 3. |

FIGURE 2-7 U.S. emissions of carbon dioxide, by sector and fuels, 2000. SOURCE: EIA (2002).

2040 to 2050 as depicted in the scenarios in Chapter 6. Off-setting this possibility somewhat, the economic effects of an oil supply disruption could diminish in direct proportion to the share of the world economy dependent on oil.

These dual policy objectives also carry broader implications for hydrogen development strategies. With respect to environmental quality, for example, using natural gas in preference to coal without carbon sequestration as a feedstock for hydrogen production would result in lower carbon emissions. This advantage of natural gas can be made greater at large production scale,3 at which carbon capture is likely to be most economic—a proposition that may not be true of natural gas reformers at distributed scale. But long-term use of natural gas as a hydrogen-producing feedstock does not solve the security concern if that gas is imported from unstable regions.

Like electricity, hydrogen is not a primary energy source, although it is a high-quality energy carrier. Large-scale manufacturing of hydrogen from a primary energy source such as coal would imply, for example, a resurgence of coal production with increased carbon emissions unless the co-produced CO2 were captured and sequestered. In effect, capture and sequestration could separate carbon intensity from carbon release (see Chapter 7).

SCOPE OF THE TRANSITION TO A HYDROGEN ENERGY SYSTEM

The scope of change that would be required poses some of the largest challenges to the transition to a hydrogen energy system. Both the supply side (the technologies and resources that produce hydrogen) and the demand side (the technologies and devices that convert hydrogen to services desired in the marketplace) must undergo a fundamental transformation. The one will not work without the other. This has not been the case in previous energy transitions. In promoting nuclear power, for example, the government simply sought to add a potentially attractive new power source. The rest of the electric power system remained the same, and customers’ use of electricity went unaffected. Similarly, government intervention has become significant in protecting some industry segments (tax concessions for

domestic oil production, for example), promoting others (wind subsidies, for example), or shaping the performance of others (regulations on the mining and burning of coal, for example). But in no prior case has the government attempted to promote the replacement of an entire, mature, networked energy infrastructure before market forces did the job. The magnitude of change required if a meaningful fraction of the U.S. energy system is to shift to hydrogen exceeds by a wide margin that of previous transitions in which the government has intervened. This raises the question of whether research, development, and demonstration programs will be sufficient or whether additional policy measures might be required.

The interlocked nature of the current energy infrastructure—the systems that produce and distribute energy and the devices to convert that energy into useful services—presents a challenge to policy makers seeking to promote a complete fuel change. The components of this challenge include these:

-

Both the new hydrogen production systems and the devices to convert that hydrogen into services that consumers will freely purchase must be developed in parallel. Neither serves any purpose without the other.

-

The incumbent technologies do not stand still, but continue to improve in performance, albeit within the envelope of the other components of the energy system—for example, more fuel-efficient internal combustion engine (ICE) vehicles and hybrid propulsion systems that make better use of the existing fueling infrastructure.

-

The cost of the current energy infrastructure is already sunk, which increases the barrier to new technologies that require new infrastructure. In addition, selected components of the current energy structure benefit from economic subsidies and favorable regulation.

-

New hydrogen-based technologies will require a transition period during which old and new systems must operate simultaneously. During this transition, neither system is likely to function at peak efficiency.

These factors all tend to lock in the current energy infrastructure and pose severe competitive challenges for a society that would rely on markets to allocate economic resources.

COMPETITIVE CHALLENGES

Any future hydrogen energy system will be subject to market preferences and to competition from other energy carriers and among hydrogen feedstocks. The choices that a market economy makes about its energy services will influence the utilization of hydrogen and hydrogen feedstocks and the attributes of the hydrogen end-use technologies. As discussed in the subsections below, the issues that frame the competitive challenge in using hydrogen include the following:

-

Energy demand. In what situations would the use of hydrogen offer the greatest economic advantage? The greatest environmental and security advantage?

-

Energy supply. How should hydrogen be produced from primary resources, such as coal, methane, nuclear, and renewable energy (solar, wind, and so forth)? What environmental consequences and trade-offs arise from its production from each resource?

-

Logistics and infrastructure. How can a storage-and-delivery infrastructure best connect the demand for hydrogen with its supply and ensure the public safety?

-

Transition. How can the mature, highly integrated energy system of the United States make the transition to a hydrogen economy?

Energy Demand

The world economy currently consumes about 42 million tons of hydrogen per year. About 60 percent of this becomes feedstock for ammonia production and subsequent use in fertilizer (ORNL, 2003). Petroleum refining consumes another 23 percent,4 chiefly to remove sulfur and to upgrade the heavier fractions into more valuable products. Another 9 percent is used to manufacture methanol (ORNL, 2003), and the remainder goes for chemical, metallurgical, and space purposes (Holt, 2003). The United States produces about 9 million tons of hydrogen per year, 7.5 million tons of which are consumed at the place of manufacture. The remaining 1.5 million tons are considered “merchant” hydrogen.5

If a transition from the use of hydrogen in industrial markets to a broader hydrogen economy is to occur, devices that use hydrogen (e.g., fuel cells) must compete successfully with devices that use competing fuels (e.g., hybrid propulsion systems). Equally important, hydrogen must compete successfully with electricity and secondary fuels (e.g., gasoline, diesel fuel, and methanol). The following discussion of energy demand considers both of these issues—market preferences and energy competition.

Market Preferences in Energy

The nature of the competition in which hydrogen would be engaged is shaped by the unique role of energy in the economy: the demand for energy is not a final demand, but rather derives from the demand for other goods and services. Both the amount of primary energy used and the physical characteristics of the final energy carrier (e.g., gasoline, methane, electricity, or possibly hydrogen) depend on the devices that convert energy into products (e.g., cars, furnaces, air conditioners, telephones, and computers) or ser-

vices (e.g., transportation, heating, cooling, communications, and computing).

In a market economy, the amount of energy used depends on trade-offs among desirable attributes such as the following:

-

The cost of building greater efficiency into the device, relative to the subsequent (and discounted) benefits in fuel saving;

-

The value of time versus the cost of the energy needed to save time—for example, motor trips take longer when people drive at a relatively fuel-efficient 55 mph rather than at the less efficient 70 mph, but the lower speed costs drivers a valuable resource, their time; and

-

The price of the energy input seen by the particular consumer as distinct from its cost to produce—for example, electric energy consumed during peak hours costs more to produce than that consumed at other times of day, yet the price is the same at all times.

The physical characteristics of the final energy carrier depend on the nature of the service that the market demands. In transportation, for example, the need for fuels with high energy density and rapid refueling strongly favors liquid hydrocarbons, mostly derived from petroleum. By contrast, devices such as computers operate with electric energy, which can be made from a variety of fuels (e.g., coal, natural gas, nuclear, and petroleum) including less-energy-dense fuels, as well as gaseous and solid fuels.

Various preferential interventions in the form of taxes, subsidies, and regulations also influence consumer prices, and hence consumer behavior. At the same time, however, the cost of important external effects, such as the stress on the global climatic system or lower national security, are also excluded from the prices that influence consumer trade-offs. And if the full cost of the mine-to-waste cycle needed to provide an energy-based service does not appear in the price of that service, then it will be consumed inefficiently.

Competition and Synergy

If large quantities of hydrogen can be produced at competitive costs and without undue carbon release, the use of hydrogen would offer marked advantages in the competition with other secondary fuels. First, hydrogen is likely to burn more cleanly in combustion engines. Second, hydrogen is better matched to fuel cell use than competing fuels are; and the fuel cell could become the disruptive technology that will transform the energy system and enable hydrogen to displace petroleum and carbon-releasing fuel cycles. If cost-effective and durable fuel cell vehicles can be developed, they could prove attractive to manufacturers, marketers, and consumers insofar as they can achieve the following:

-

Replace mechanical/hydraulic subsystems with electric energy delivered by wire, potentially improving efficiency and opening up the design envelope;

-

Reduce manufacturing costs as manufacturers are able to use fewer vehicle platforms; and

-

Enable the vehicle to offer mobile, high-power electricity, which could provide accessories and on-vehicle services more effectively than could alternatives.

However, gasoline hybrid electric vehicles (GHEVs) can offer many of these attractive features while at the same time retaining the current fuel infrastructure. Even though GHEVs cannot achieve the fuel efficiency envisioned for fuel cell vehicles (FCVs) and despite the significant cost of battery replacement, some consumers might find that the convenience of the familiar “gas station” offsets these disadvantages well into any hydrogen transition. This suggests that fuel cell vehicles will face stiff market competition from hybrids for many years into the future.

In a fuel cell vehicle, hydrogen produces electricity, which is converted electromechanically into torque in the wheels which drives the vehicle; in effect, hydrogen fuel powers a mobile electric generator. In a mature hydrogen infrastructure, new synergies might be found in large-scale production and distribution. One visionary concept is the national Energy Supergrid, advanced by Chauncey Starr, founder and emeritus president of the Electric Power Research Institute. This supergrid would combine hydrogen and electric energy in two components: (1) a network of superconducting, high-voltage, direct current cables for power transmission, with (2) liquid hydrogen as the coolant required to maintain superconductivity in the cables. The electric power and hydrogen would be supplied from nuclear and renewable energy power plants spaced along the grid. Electric energy would exit the system at various taps, connecting into the existing power grid. The hydrogen would also be tapped to provide a readily available fuel for automotive or other use (National Energy Supergrid Workshop Report, 2002). On a smaller scale, others have proposed similar hydrogen-electric projects as a way to move renewable energy from remote sources to markets—for example, from wind farms in North Dakota to load centers like Chicago.

Hydrogen might also enjoy a synergistic relationship with renewable energy. The chief difficulty with many renewable technologies is the intermittency of the resource itself—the Sun doesn’t always shine or the wind always blow, and when they do they are variable. But if sufficiently low-cost hydrogen storage could be developed, hydrogen might provide a pathway to market for renewable energy because it could be manufactured whenever sufficient energy was available. The problem of intermittency would be mitigated, because the stored hydrogen could be used to produce electricity during times when sunlight or wind was not available.

Finally, hydrogen might compete directly with electricity as an energy carrier, with each using a separate production

and distribution system. This competition can be analyzed in terms of a specific application—for example, energy storage on board an automobile. Here, hydrogen enjoys a distinct advantage over electricity, even if grid electricity might be less expensive than hydrogen. This advantage derives from energy storage—in its current state of development, the battery technology needed to make grid electricity applicable to mobile uses is unable to provide vehicles with the range, power, and convenience that consumers require. If, however, battery technology were to achieve a major breakthrough, then the availability of relatively inexpensive energy from the grid would put hydrogen at a competitive disadvantage. Even without improved batteries, electricity from an on-board generator is available in several hybrid vehicles now on the market. The resulting fuel economy of these hybrid vehicles is substantially higher than that achievable with conventional vehicles. As this technology gains manufacturing scale, it will prove a formidable competitor for hydrogen, especially at the beginning of any transition. However, hybrid vehicle technology seems unlikely to match the ultimate performance of the hydrogen fuel cell vehicle, if all of the relevant technologies are successfully developed.

Energy Supply

The U.S. energy system has evolved over the past century into a massive infrastructure involving extraction, processing, transportation, and end-use equipment. The replacement value of the current system and related end-use equipment would be in the multi-trillion-dollar range.6 Major changes to the system have typically taken decades. If hydrogen is to succeed as a fuel, it must be in the context of this energy system. For example, insofar as hydrogen may compete with petroleum, it faces an established infrastructure of 161 oil refineries, 2,000 oil storage terminals, roughly 220,000 miles of crude oil and oil products lines, and more than 175,000 gasoline service stations (NRC, 2002). Much of this infrastructure would have to be replaced or heavily modified if hydrogen is to become the dominant fuel for the highway transportation sector. (A description of the U.S. energy system is presented in Appendix F.)

Hydrogen production technologies based on various primary energy resources—renewable energy resources,7 carbonaceous fuel resources, and nuclear energy—would compete for market share in an envisioned hydrogen economy. Each promises advantages, involves uncertainties, and raises currently unresolved issues. The technologies for producing hydrogen from these various primary resources can be deployed at varying scales of production, and in Chapter 5 the committee presents its analysis of total supply chain costs for hydrogen generation at three illustrative scales of pro-duction—central station, midsize, and distributed.8 The following subsections present an overview of the attributes associated with the various production scales, and primary energy sources and associated technologies for hydrogen generation at each scale are discussed.

Central Station (Very Large Scale)

At very large scale, around a gigawatt and above, the principal supply options include carbonaceous fuels and nuclear energy. About 100 such plants would be able to supply the current world demand for hydrogen, about 42 million tons per year (ORNL, 2003), and about 20 such plants would be able to supply the current U.S. demand for hydrogen of about 9 million tons per year.

With regard to a carbonaceous feedstock, hydrogen could be manufactured from natural gas or coal. The carbon would be converted into synthesis gas (syngas—CO + H2)—used either for combustion for electricity generation or for further chemical processing into hydrogen and CO2, which can be captured for sequestration. The chief advantage of this approach is the abundance of domestic coal: the United States has the world’s largest recoverable coal reserves, sufficient to manufacture hydrogen for a very long time. The large scale of operation would yield attractive economies of scale. In contrast, natural gas will increasingly have to be imported, raising new energy security concerns.

Two salient issues would arise from the use of carbonaceous fuels as a major source of hydrogen. The first is concerned with whether the carbon really can be captured and sequestered in a manner that is both environmentally acceptable9 and cost-effective. If this cannot be achieved, hydrogen production from carbonaceous fuel resources, particularly coal, offers none of the sought-after large reductions in (net) carbon emissions. The second issue derives from the scale of operation. Demand for hydrogen must be sufficient to justify investment in a large-scale plant, and a matching distribution infrastructure would be required. In addition, a satisfactory means for bulk storage of hydrogen would have

|

6 |

For example, replacing existing electric generators with new units averaging $1000 per kilowatt (electric) would cost about $800 billion. A new transmission system, at $1 million per mile, would cost $160 billion. Oil refineries and pipelines would be several hundred billion dollars more. The natural gas transmission and distribution systems would also cost hundreds of billions. Then add the cost of replacing all of the factories, buildings, and vehicles that are designed for a specific type of fuel. Clearly, a detailed calculation would show a total value of multi-trillion dollars (NRC, 2002). |

|

7 |

Strictly speaking, the primary energy resource is the Sun for solar renewable energy (e.g., photovoltaic) and wind energy. Renewable energy is a primary resource for hydrogen in the sense that hydrogen is the product of chemical processes using renewable feedstocks (e.g., biomass) or of electrolysis of water powered by renewable electricity sources. |

|

8 |

In the committee’s analysis, central station plants are assumed to produce hydrogen on average 1,080,000 kilograms per day (kg/d); midsize plants, 21,600 kg/d; and distributed facilities, 432 kg/d. (See Chapter 5.) |

|

9 |

As used in this report, the term “environmentally acceptable” implies a high probability that the carbon will not leak into the atmosphere during processing and handling, that it will remain sequestered from the atmosphere essentially in perpetuity, and that it will not cause adverse side effects, such as harmful chemical reactions, while so sequestered. |

to be found. A transitional strategy to address these requirements must precede the move to producing hydrogen fuel in very large scale plants.

Nuclear energy could produce hydrogen in one of three ways: (1) through electrolysis, the splitting of water molecules with electricity generated by dedicated nuclear power plants; (2) through process heat provided by advanced high-temperature reactors for the steam reforming of methane; or (3) through a thermochemical cycle, such as the sulfur-iodine process. Among the three, the issue of carbon capture and storage arises only for steam reforming; otherwise, the nuclear option is carbon-free. Scale, however, remains an issue, as it does for the large coal plants. In addition, delays in the development and deployment cycle for nuclear plants might arise from concerns with the storage and disposal of nuclear fuels, the security of nuclear facilities against terrorist attack, and the siting and licensing of nuclear facilities. These issues could prolong the time to realization of a full-scale hydrogen economy.

Midsize Scale

At midsize scale, a few tens of megawatts, both natural gas and renewable energy technologies offer production possibilities. Megawatt-scale production is especially attractive for biomass-based energy sources. Natural gas production at this scale could provide an efficient response to early market demand for hydrogen, but could not offer sufficient scale economies to compete effectively in mature hydrogen markets.

Distributed Scale

At the distributed end of the size range, large-scale pipeline systems would not be required because hydrogen production could be colocated with hydrogen dispensing and/or use. Distributed production might rely on primary energy from renewable resources, to the extent that those could be located reasonably near the point of use. Alternatively, grid electricity, possibly used during off-peak hours, might serve as the energy source. A distributed approach offers clear advantages during a transition from the current energy infrastructure, although it might not be sustainable in a mature hydrogen economy.

The advantages of distributed production during a transition are economic. The costs of a large-scale hydrogen logistic system, which many analysts believe will dominate a mature hydrogen economy, could be deferred until the demand for hydrogen increased sufficiently. This would mitigate the problem of “lumpy” investment—large production and distribution facilities that provide economies of scale but lead to underused capital while the demand for their output catches up. In contrast, distributed production systems could be installed rapidly as the demand for hydrogen increased, thus allowing hydrogen production to grow at a pace reasonably matched with hydrogen demand. Instead of static economies of scale, distributed production would rely on dynamic economies of scale in the manufacture of small hydrogen conversion and storage devices. Nevertheless, the cost of hydrogen compared with that of gasoline would likely be more expensive during this transition phase (see Chapters 5 and 6).

One major disadvantage of distributed production is environmental. If the hydrogen were produced by small-scale electrolysis and if the energy inputs to the electrolyzer were to come from the grid, the carbon consequences would be the same as for any other use of electric energy on a per kilowatt basis. If the hydrogen were produced by small-scale reformers, the collection of the carbon and its shipment to a sequestration site might prove an insurmountable challenge. Indeed, distributed-scale production in a mature hydrogen economy might require a costly reverse-logistic system to move the carbon captured from the dispersed production sites to the places of sequestration if the environmental benefits are to be achieved. The cost of a dispersed capture and disposal system might make distributed production unattractive in a mature hydrogen economy. During a transition period, however, the carbon from distributed production could simply be vented while the economic advantages of scalability and demand-following investment served to start the hydrogen economy.

Logistics and Infrastructure Issues

Between the production of hydrogen at any scale and the use of hydrogen in an energy device, the following series of logistic operations will exist:

-

Packaging. The hydrogen must be put into a form suitable for shipping. This form might be a compressed gas, a liquid, some form of hydride, or some chemical compound.

-

Distribution. The hydrogen must be moved to the point of use. Pipelines, pipes, roads, and railroads are typical shipping modes.

-

Dispensing. The hydrogen must be transferred from the care of retailers into the care of consumers.

-

Storage. In the interval between production and use, the hydrogen must be stored. Pressurized containers or cryogenic containers typify current practices.

With the technologies now available, many of these logistic steps themselves become significant consumers of energy; some analyses suggest that logistic costs will dominate the economics of any hydrogen energy system (Boessel et al., 2003). This consideration emphasizes the importance of viewing R&D objectives in the context of complete proto-typical hydrogen energy systems rather than in isolation (NRC, 2003b).

Transition Issues

The transition to a hydrogen economy is unlikely to be achieved through the linear substitution of hydrogen com-

ponents for their counterparts in the current energy infrastructure. Consider refueling, for example. It might emerge that refueling systems for hydrogen vehicles would become entirely modular, so that refueling would be more like purchasing and loading a videocassette into a recorder than filling a present-day automobile with gasoline. That could result in the flourishing of customer advantages and business models quite distinct from those common to the current fuels infrastructure.

Indeed, the ultimate timing and configuration of a mature hydrogen economy cannot be known, because they turn on resolution of the four pivotal questions discussed at the end of the chapter. Thus, the DOE might have its greatest impact by leading the private economy toward transition strategies rather than to ultimate visions of an energy infrastructure markedly different from the one now in place.

Developing Strategies for the Transition

The set of technologies and business models capable of beginning a transition to the hydrogen economy might be very different from those that would be most desirable in a mature energy system. This possibility challenges the DOE to maintain its focus on the goals to be achieved by the hydrogen economy, but also to cultivate flexibility, learning, and responsiveness in assisting the transition pathways leading to it.

Subsidies

As part of a transition strategy, some form of buy-down of the cost of technology might be required in order to initiate and accelerate the pace of transition. An example might be a set of temporary subsidies to encourage the early adoption of hydrogen technology; they could be phased out once scale economies had been achieved and mainstream markets opened. The societal benefits of promoting a more rapid transition to hydrogen might justify this use of subsidies. The challenge for any subsidization strategy would be to support the kind of “game-changing” technologies that can actually deliver public benefits. Otherwise, buy-down tends to become an entitlement, entrenching the subsidized rather than accelerating systemic change.

Regulatory and Social Issues

Public apprehensions regarding hydrogen must be addressed early in a transition—otherwise the hydrogen economy might never reach the steady state. Of these concerns, safety appears to be foremost. To be sure, hazards exist with the current fuels infrastructure—there can be natural gas explosions in homes, or auto fires, for example. However, the public has grown accustomed to the possibility of these hazards, and the relevant safety precautions are widely known. By contrast, hydrogen’s distinct properties lead to distinct safety issues (see Chapter 9).

Safety issues cut across all segments of the hydrogen economy and become operational in two forms: concern with loss of human life and property, and codes and standards that shape the configuration and location of hydrogen facilities and vehicles. Much evidence demonstrates that hydrogen can be manufactured and used in professionally managed systems with acceptable safety. The concerns arise from prospects of its widespread use in the consumer economy, where careful handling and proper maintenance cannot be fully ensured.

Technology demonstrations might mitigate public skepticism, both by displaying the merits of the technology and by educating local officials regarding emergency response procedures and effective zoning codes. Beyond that remains the issue of how DOE R&D programs can best inform, and in turn be informed by, state and local authorities.

None of these precautions, however, can compensate for the casual approach that some consumers will inevitably take to their own safety. Engineering aimed at reducing the possibilities for mishandling can help lower the number of accidents but can never preclude them all. Some hydrogen logistic systems will prove superior in allowing a more benign consumer interface, and the issue for the DOE will be to identify and promote these systems.

Finally, the successful sequestration of massive quantities of carbon may be essential for any hydrogen economy that makes more than transitional use of carbonaceous fuels. The history of radioactive waste disposal suggests that dedicated opposition can overcome general public acceptance of a technology and its waste disposal plan. Thus, even energy systems that now appear to enjoy widespread acceptance can become vulnerable to delays and costly false starts. The carbon sequestration issue falls into that category (see Chapter 7).

Technology Development for the Transition

Much of the policy analysis now performed on the subject speaks to hydrogen supply and demand under steady-state conditions. But if an effective transition cannot be achieved, neither can the benefits of the steady state. Thus, technologies and policies developed explicitly for a transition remain important, even if they do not carry over into the mature hydrogen economy. This issue of how to effect the transition has several dimensions:

-

Should the DOE seek to guide the transition into the pathways it selects, or should it let development be guided principally by the industrial stakeholders?

-

In either case, how can the DOE know which transitional technologies to develop?

-

What assumptions should be made regarding the success of pivotal technologies such as carbon capture and sequestration?

-

What incentives will entrepreneurs and investors in the interim technologies need before they commit their capital resources?

ENERGY USE IN THE TRANSPORTATION SECTOR

In order to examine the potential demand for hydrogen, it is necessary to examine the ways in which hydrogen would be used in the economy. Two generic uses were considered by the committee—those of hydrogen as a fuel for transportation vehicles and hydrogen as a fuel for electricity generation. The committee’s analysis focused on the first of these two potential uses of hydrogen. In particular, the committee examined the use of hydrogen as a fuel for light-duty vehicles (i.e., passenger cars, pickup trucks, vans, and sport utility vehicles), as this is where most of the DOE’s hydrogen research is focused. With respect to the use of hydrogen for electricity generation, the committee notes the difficulty that such use would have competing with natural gas turbines. (See the discussion earlier in this chapter, in the section entitled “Competitive Challenges,” as well as in Chapter 3.)

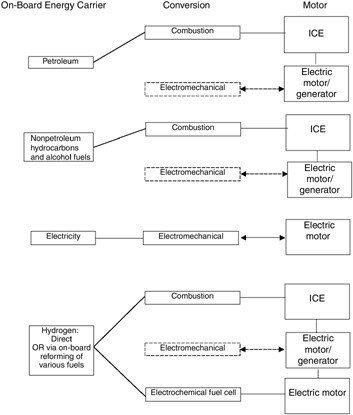

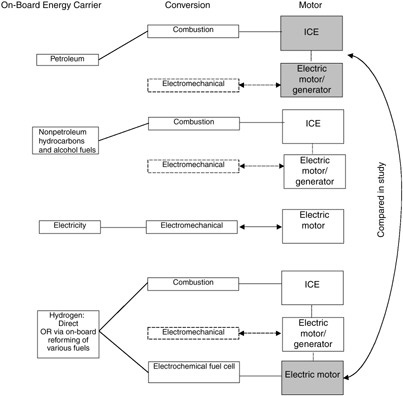

In order for hydrogen to compete successfully as a fuel for light-duty vehicles, vehicle manufacturers and purchasers must believe that hydrogen-fueled vehicles offer advantages over the available light-duty-vehicle alternatives. Those alternatives could involve diverse possibilities of energy carriers and the particular vehicle technologies that utilize them.10Figure 2-8 illustrates the possible combinations of energy carriers and vehicle technologies that could conceivably characterize the future vehicle stock for personal transportation in the United States.

In successive columns, Figure 2-8 shows three distinctions among the possible combinations of energy carriers and technologies. Storage on board the vehicle, with periodic refueling, has been the norm for personal passenger vehicles, trucks, buses, and aircraft, and that is the committee’s approach to light-duty vehicles. Various gaseous, liquid, or solid fuels could be supplied to the vehicle. In the first column, “on-board energy carriers” distinguish the various forms of energy that could be supplied to the vehicle.

Currently, most light-duty vehicles are fueled by petroleum products, primarily gasoline and secondarily diesel fuel, although some vehicles are fueled by nonpetroleum hydrocarbons and alcohol fuels. Compressed natural gas and propane are routinely used to fuel light-duty vehicles. Among alcohol fuels, ethanol is used in light-duty vehicles, and methanol has been widely discussed as an alternative. Hydrocarbons can be used in combination with alcohol fuels, such as gasoline with ethanol. Bio-based diesel fuel currently exists in the marketplace. Another generic alternative is electricity supplied to the vehicle. That electricity is then converted and stored in the form of electrochemical energy in a battery, or mechanical energy in a flywheel. The last energy carrier in the column is the alternative that the committee examined, molecular hydrogen.

The last two columns in Figure 2-8 denote the conversion process (second column) applied to the energy carrier by the motor (third column). Fuels such as petroleum products, nonpetroleum hydrocarbons, alcohols, or molecular hydrogen could be converted to mechanical power through a combustion cycle. The current generation of internal combustion engines could be used, or advanced combustion techniques could conceivably transform such engines. (Hydrogen internal combustion engines were not analyzed, since the committee determined that in North America the demand for hydrogen was more likely to be due to fuel cell vehicles.11) Alternatively, each of these fuels could be used to generate on-board electricity, most likely through an electrochemical conversion device, such as a fuel cell. Within the realm of imagination would be microturbines that use the fuels to generate electricity that would be used directly in electric motors to propel the vehicle.

Hybrids of electric and combustion processes could also be used. Currently, hybrid electric vehicle technology combines the combustion of petroleum products (gasoline or diesel), over a wide range of degrees of hybridization, with electric motors for propulsion. Hybrids could be created for any of the other fuels. Hybrids of fuel cells and batteries are under consideration today.

The locus of competition, therefore, could be both among fuels supplied to the vehicles and among vehicle technologies that use those fuels. Thus, if molecular hydrogen were widely available as a fuel source for light-duty vehicles, the competition would be between fuel cell vehicles and internal combustion vehicles using hydrogen, and perhaps other technologies that use hydrogen as a fuel. And molecular hydrogen in these vehicles would compete with the direct use of electricity, and with the use of petroleum products, nonpetroleum hydrocarbons, and alcohols, either combusted or electrochemically converted to electricity.

Some of the technologies discussed above have been well developed already, some need significant developmental work, some require technological breakthroughs for success, and presumably some require initial conceptualization. Just as there is a high degree of uncertainty about the success of hydrogen technologies, there is a high degree of uncertainty about the success of those alternative technologies that require technological breakthroughs, and even more for technologies that have yet to be conceptualized! For example, possible future reductions in the cost and increases in the range of batteries could ultimately make dedicated electric vehicles, with batteries charged from grid-supplied electricity, much less expensive and more practical than they are

FIGURE 2-8 Possible combinations of on-board fuels and conversion technologies for personal transportation. NOTE: ICE = internal combustion engine.

currently. There is much uncertainty about whether such technologies would ultimately lead to vehicles that are less costly and more convenient than fuel cell vehicles.

For this study, the committee was not able to examine all of the options that may shape the future competition. Figure 2-9 illustrates the comparisons that were developed within this study. In particular, the committee focused on the competition between vehicles with on-board storage: fuel cell vehicles supplied by molecular hydrogen in competition with internal combustion, gasoline-fueled vehicles, either as conventional vehicles or as gasoline hybrid electric vehicles.

FOUR PIVOTAL QUESTIONS

From the foregoing analysis, the following four pivotal questions emerge as decisive:

-

When will vehicular fuel cells achieve the durability, efficiency, cost, and performance needed to gain a meaningful share of the automotive market? The future demand for hydrogen depends on the answer.

-

Can carbon be captured and sequestered in a manner that provides adequate environmental protection but allows hydrogen to remain cost-competitive? The entire future of carbonaceous fuels in a hydrogen economy may depend on the answer.

-

Can vehicular hydrogen storage systems be developed that offer cost and safety equivalent to that of fuels in use today? The future of transportation uses depends on the answer.

-

Can an economic transition to an entirely new energy infrastructure, both the supply and the demand side, be achieved in the face of competition from the accustomed benefits of the current infrastructure? The future of the hydrogen economy depends on the answer.

FIGURE 2-9 Combinations of fuels and conversion technologies analyzed in this report. The committee conducted cost analyses of hydrogen fuel converted electrochemically in fuel cells versus gasoline use in internal combustion engines (ICEs) in standard and hybrid configurations. Other combinations of fuels and energy conversion technology are discussed in the report.