3

Tools and Methods to Support Decision-Making

This chapter discusses various tools, methods, and approaches for incorporating sustainability concepts into assessments used to support US Environmental Protection Agency (EPA) decision making. It provides a more-detailed discussion of a small subset of the tools to illustrate what the committee believes are particularly valuable attributes of tools for informing sustainability considerations. Our discussion of this subset is intended to emphasize a major theme of this report: the identification of and development of sustainability assessment tools needs to be considered as an adaptive process of trial and error, learning by experimentation, and continuous re-evaluation of the tools. In short, EPA needs to consider the development and application of tools to inform sustainability as an on-going process, not an endpoint that is achieved prior to the integration of sustainability into decision making. In subsequent chapters, case studies are presented to consider the specific application of tools and methods for incorporating sustainability concepts into assessments used to support EPA decision making.

As discussed in Chapter 1, NRC (2011a) (known also as the Green Book) recommended that EPA develop a suite of tools for use in the Sustainability Assessment and Management (SAM) approach for assessing environmental, economic, and social aspects of activities to be undertaken by the agency. The Green Book also recommended that, collectively, the tools should provide the ability to analyze present and future consequences of various decision options. In addition, it recommended the tools should have the capability to show distributional effects (e.g., costs and benefits) of alternative options, particularly for vulnerable or disadvantaged groups and ecosystems. To reap the benefits from the application of these tools in a sustainability context, systems thinking is needed.

Generally, systems thinking involves a comprehensive understanding of the mechanisms and feedback effects of interrelated parts or subsystems that work together – in either a coordinated or uncoordinated fashion – to perform a function.1 From an operational perspective, “applying a systems approach to sustainability provides a rigorous way to analyze the potential consequences of human intervention…it may reveal how actions taken by industry and consumers affect the environment, how efforts to protect the environment impact industry and consumers, or how impacts on one system can affect others and the larger whole” (EPA 2013a, p. 11). Understanding such connections has long been a central tenet of industrial ecology (Allenby 2006). Also, “cradle-to-cradle” (rather than “cradle-to-grave”) design tenets popularized by McDonough and Braungart with the slogan “waste equals food” (McDonough and Braungart 1998, 2002) and The Natural Step Framework for Strategic Sustainable Development (Natural Step 2014) attest to the idea that business operations are deeply integrated into natural systems – and vice versa. At the core is the principle that waste (or output) from one system can be used as feedstock (or input) to another. Moreover, systems thinking applies at the product system level. Life cycle assessment (LCA) approaches have advanced over the last 20 years to provide a methodological framework for ensuring that

____________________

1See Holling (2001), Meadows (2008), and EPA (2013a) for a more detailed explanation of systems thinking.

an improvement in one sustainability issue (for example, energy consumption) would not create an unanticipated impact in another area or life cycle stage. Systems thinking is already core to successful programs such as Design for Environment (DfE), in which LCA is an integral component (see Chapter 4). EPA programs, such as DfE, provide the agency with the opportunity to build on the foundation of existing knowledge in order to infuse systems thinking into agency decisions and actions. System thinking at national, region, community, company, value chain, product category, and product levels is one of the fundamental premises behind a successful implementation of sustainability concepts into EPA decision making processes.

ESTABLISHING THE LEVEL OF ANALYSIS NEEDED FOR AN ACTIVITY

Chapter 2 discussed the wide range of EPA’s activities in which sustainability considerations could be incorporated at multiple levels of activity. However, not all applications of the sustainability assessment tools need to be done at the same scope and level of detail. It would be impractical to apply the formal SAM approach to every narrow routine decision, such as permitting decisions on air emissions, that may affect small geographic areas. On the other hand, decisions that likely will have high impact for one or more sustainability pillars (such as a national policy decision or a power plant facility siting) would probably benefit from the SAM process.

EPA faces the challenge of incorporating sustainability tools and approaches into decision-making processes at an appropriately selected level of detail to assure that the systematic consideration of the three pillars of sustainability is assured. An important component of this challenge is to establish boundaries for the analysis in geographic extent and time. A sustainability screening approach, using a minimum input of data for rapid analysis, can help determine whether to undertake the SAM approach for any particular activity. If it is determined that this process should be undertaken, the screening tool could also provide guidance on the appropriate analytical tools to apply and on the appropriate degree of depth and scope of the analysis needed. Screening will help avoid undue delays in taking action to address environmental problems. It can determine the range and magnitude of potential impacts. The committee realizes that it will take time, resources and experience to incorporate sustainability broadly into EPA’s activities. Chapter 7 discusses several kinds of major activities in which EPA has substantial opportunities to apply sustainability tools and approaches.

THE ENVIRONMENTAL PROTECTION AGENCY’S SUSTAINABILITY ANALYTICS REPORT

Scores of analytic tools and methods to support decision-making at EPA and elsewhere have been proposed and developed (e.g., EPA 2014h). Some of these tools have been tested and frequently applied for the purpose of considering more-sustainable uses of the environment and natural resources. Other tools could become more useful with additional development. In its recent report Sustainability Analytics: Assessment Tools and Approaches (referred to as the Analytics report), EPA summarizes 22 types of tools and methods used by the agency; it categorizes them under the pillars of sustainability: economic (4 types), environmental (10 types), and social (8 types) (EPA 2013a).2 (A glossary of tools and approaches that was developed from the Analytics report is presented in Appendix D of this report.) The Analytics report also demonstrates the application of the tools by using 24 illustrative examples on topics which are similar to some of the case studies presented later in this report. The tools being considered include decision tools into which sustainability concepts can be incorporated. The tools do not operate at the same level of specificity; some are quite general while others could be used as part of another tool. For example, futures methods may be used in an economic benefit-cost analysis.

____________________

2Although the report shows 2013 as the publication year, it was not released to the public until 2014 while the committee was conducting its study.

EPA’s Analytics report notes that it does not represent a comprehensive list of tools, but instead discusses tools recommended by subject matter experts across the agency. The report also indicates that it does not provide in-depth instructions for applying each assessment tool or approach, and it does not set policy or dictate a process for implementing sustainability concepts using any of the tools in the Analytics report (EPA 2013a). In addition, the report indicates “As these assessment tools and approaches are developed and applied, Sustainability Analytics will evolve: the assessment tools and approaches included in it will be more fully described; additional tools and approaches will be identified; and, information about sustainability metrics, indicators, datasets and indices will be included” (EPA 2013a, p 8). EPA has taken a good first step in developing this initial Analytics report. It provides a reasonable and informed baseline survey of sustainability tools.

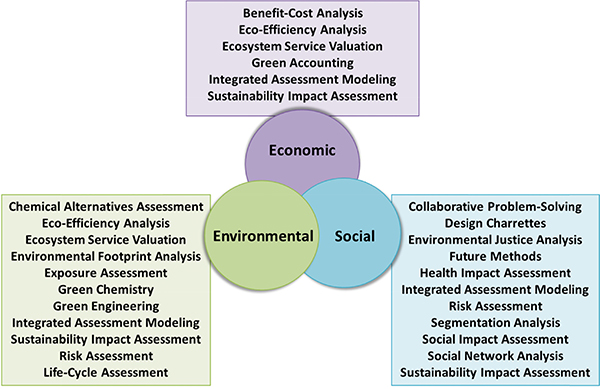

The tools listed in the Analytics report for each of the pillars are generally categorized by the discipline within which they were developed. A similar categorization was used in a presentation to the committee by EPA officials (see Figure 3-1). Thus, the tools in the economic pillar are identified as those coming from the discipline of economics and include use of economic methods such as monetization or valuation. Tools presented in the social pillar category are focused on societal impacts as well as engaging the public in decision making, and are commonly associated with sociology, anthropology, political science, and geography. The tools listed in the environmental pillar category consider specific assessments for chemicals and alternatives as well as broader system-wide assessment tools. Many of these come from engineering and environmental sciences. While this categorization of tools may be useful for historical context in some instances and the Analytics repo t indicates the application of tools can involve more than one pillar, the identification of a tool with a specific pillar is potentially very misleading. For example, the report presents benefit-cost analysis (BCA) in the pillar of economics, which suggests it focusses exclusively or largely on that discipline, but BCA has long been used to inform decisions relevant to the environmental and social pillar as well (EPA 2014h). This categorization in the Analytics report is inconsistent with the report’s discussion of BCA, which acknowledges that valuation of nonmarket goods is an important part of BCA. The Analytics report also notes that environmental effects which cannot be monetized should be listed and considered in decisions. Given the importance of BCA and its potential for informing all three pillars, the committee chose it as one of the tools for more-detailed discussion in this chapter.

FIGURE 3-1 EPA’s categorization of tools into single pillars of sustainability. Source: Trovato and Shaw 2013.

Another example of how the Analytics report presents a limited breadth of possible contributions for a tool is related to life-cycle assessment (LCA). In the report, LCA is defined as applying only to products. However, LCA is able to represent an accounting of the inventory and effects of products, processes, or systems, and there have been a wide array of developments with respect to LCA approaches, databases, and applications. The Analytics report does not mention EPA’s substantial investment in LCA, including database development and impact assessment, primarily in the Office of Research and Development. Applications of LCA in EPA program offices have been more limited. A discussion of the other current development and application efforts of LCA would be useful, noting, for instance, that EPA is represented in an interagency group that focuses on LCA, including the General Services Administration and the US Department of Agriculture. There have also been substantial efforts by international organizations, such as the UN Environment Programme (UNEP) and the Society of Environmental Toxicology and Chemistry (SETAC), and private organizations to apply and adapt LCA.

The Analytics report indicates that the tools and approaches currently included should not be considered the only tools that could be applied to a particular activity. It also indicates additional tools and approaches will be added as it evolves. A potentially important tool that is currently not included is the recently developed approach for considering the social cost of carbon (SCC), which has aspects of economic tools similar to BCA. SCC is an estimate of the monetized damage (usually expressed on a per ton basis) associated with the effects of an incremental increase in greenhouse gas (GHG) emissions and based on a particular climate-change scenario at a particular point in the future. Integrated assessment models, which are used to produce such estimates, rely on assumptions about the relationship between GHG emissions and temperature change and temperature and associated damages (NRC 2010). Given the prominence of climate mitigation issues for EPA and the fact that the social cost of carbon focusses explicitly on future benefits and costs of current decisions–a significant component of sustainability–its inclusion in the Analytics report in the near future is important (see additional discussion later in this chapter). Another omission from the report is a discussion of the role of managing uncertainty and variability with decision support tools. Failure to understand and address uncertainty and variability in the application of decision support tools can lead to an inappropriate interpretation of results. Their consideration in a sustainability context is discussed later in this chapter.

In the Analytics report, the link between the tool and how it can be used to provide information to support decision making related to sustainability is often not made. For example, the report did not explain explicitly how ecosystem services valuation can inform sustainability and how it could do so more effectively with additional research and development. Furthermore, the report needs to include more discussion of tradeoff situations where one or more of the sustainability pillars could be at odds with one another (e.g., achieving more environmental sustainability for future generations may result in less economic activity that can affect low income members of the current population disproportionately). As discussed in the Green Book, sustainability tools will need to inform decisions involving considerations of tradeoffs (as well as synergies). Further discussion of this context in the Analytics report is warranted.

EPA’s sustainability analytics report should be considered a living document with appropriate updates on a regular schedule. Future versions of the report should provide additional discussion of integrative applications of the tools and how a tool can be used to provide information to support decision making involving tradeoffs, where one or more sustainability pillars could be at odds with one another. New tools identified would be added. (Recommendation 3a)

SUSTAINABILITY TOOLS AND METHODS ASSESSMENT

Some tools and approaches presented in the Analytics report are well developed and have been widely used throughout EPA, and others are in the development stage or have been used within the agency only recently. Although the Analytics report discusses the strengths and limits of specific tools, it does not apply a consistent set of criteria across all of the tools. Doing so would help identify opportunities for improvement and identify considerations in selecting tools for a particular activity. To illustrate the appli-

cation of a consistent set of criteria, the committee rated each tool presented in the Analytics report, based on the members’ experience and expertise, and by applying seven general criteria in a qualitative manner that are relevant to the current state of development and use of the tools for sustainability analyses.

• Documentation - how well documented the tool is, by existing references available about the method or potential applications.

• Accepted Use - the degree of consensus among stakeholders and the scientific community of how the method should be employed.

• Maturity - the extent to which the scientific basis for the tool has been developed to support a particular type of decision.

• Software - the availability of software in the public domain to support applications of the tool.

• Screening - suitability of the tool for screening-level analyses to inform subsequent decisions about the appropriate depth of additional analyses.

• Data - extent to which adequate data exist, or will likely soon exist, to support tool development and application.

• Extent of Usage - assessment of the overall role of the tool in EPA decision making to date.

The committee’s rating of the tools in Appendix E should be viewed as an example of the type of ongoing assessment needed to develop and refine a full suite of sustainability assessment tools. Because the exercise may have been influenced by the degree of the committee’s familiarity with the extent of development of some of the tools, the rating results should not be used as a basis for excluding any tool from consideration or for selecting the appropriate tools for a given EPA decision.

The committee finds that the tools differ widely in the underlying amount of R&D and other support generally available or in EPA. A ratings exercise may be useful for identifying priority R&D areas for tools planned to be foundational in the EPA decision suite going forward. For tools that EPA sees as strategically valuable, ongoing R&D support will be needed to help attain the visions expressed in EPA’s strategic plan.

Future efforts by EPA to track and categorize tools, e.g., in future updates to the Sustainability Analytics report, could adopt similar or entirely different criteria. A useful addition to criteria would be associated with the applicability of tools in certain contexts. In general, applicability of a tool in a sustainability context is a major criterion relative to the others considered. However, applicability was not included in the committee’s rating exercise because its determination is context specific. All of the tools are potentially applicable, but each tool has various strengths, limitations, and data requirements that influence whether they are actually applicable to a particular issue. Assessment of applicability is complicated by specific instances of tools (e.g., life cycle assessment in general could be applicable to many decisions, but specific LCA software tools or methods may be applicable in only specific contexts).

Various tools listed in the Figure 1-1 and Appendix E are inherently integrative across sustainability pillars, and it is not surprising then that there was significant appreciation of them by the committee. The perceived high performance of these tools (including BCA, exposure assessment, risk assessment, and LCA) by the committee suggests that continued integration of tools in support of EPA decision making are likely to lead to higher overall value. The committee’s rating exercise helped to frame its discussion of the tools, and led to a focus on a subset of them.

In general, a small number of tools is relied on much more than others, and these largely have more solid scientific bases for their use. These tools are mature, accepted, have data, and EPA continues to use them in its decision processes. The committee thus considers them to be particularly promising with respect to their applicability by EPA for use in supporting integrative sustainability decisions, particularly in the near term. Even though there is a range in the extent to which the tools have been developed and applied within EPA, it is important to note that the committee does not consider that a hierarchy of tools exists with respect to selection. Choosing a tool should be based on the needs for a particular application. It may be useful for EPA going forward to evaluate the sustainability tools by using a consistent set of

criteria selected by the agency, along with periodic updating of EPA's view and use of relevant sustainability tools (e.g., in future iterations of the Sustainability Analytics report).

EPA should consider using a consistent set of criteria to evaluate the tools and carry out assessment exercises that are similar to the one conducted by the committee with the agency’s own internal users of these tools, or a larger set of external stakeholders for corroboration. The assessments should help to identify opportunities for improvement and identify considerations in selecting tools for particular activities. (Recommendation 3b)

INDIVIDUAL TOOLS AND APPROACHES

The committee chose a small set of tools for discussion in this section to illustrate particularly valuable attributes for informing sustainability concepts. The discussion considers how sustainability considerations are currently incorporated into the use of these tools, and how sustainability could be incorporated to a greater extent with additional research and development. Our discussion of particular tools should not be interpreted to mean those tools are most appropriate, or that tools not discussed are inappropriate.

Risk Assessment

In 1981, the first article of the first issue of Risk Analysis, An International Journal, by Stanley Kaplan and John Garrick (1981) defined risk assessment. The essence of their paper was to address three questions:

1. What can go wrong?

2. What are the chances that something with serious consequences will go wrong?

3. What are the consequences if something does go wrong?

Later analysts (for example, Greenberg et al. 2012) added three other questions that address risk management:

4. How can consequences be prevented or reduced?

5. How can recovery be enhanced, if the scenario occurs?

6. How can key local officials, expert staff, and the public be informed to reduce concern and increase trust and confidence?

Risk assessment is thus a tool for evaluating the relative merits of various options for managing risk. It can be applied in an engineered-systems context to assess possible effects due to a system failure (e.g., a tailings storage facilities at power plants). It can also be applied in a public health context to address health effects resulting from exposures to chemical contaminants or some other stressor. Ecologic risk assessments evaluate the likelihood that adverse effects to ecosystems including plant or animal communities would result from exposures to environmental stressors. Risk assessment is also applied to episodic natural events (e.g., hurricanes and floods) and harmful human acts (e.g., terrorism).

Risk assessment and risk management have been integral to EPA’s decision-making (especially with respect to regulations to protect human health) to assess the potential consequences of options it is considering (see Box 3-1). In general, EPA has focused its risk-based decisions on reducing risk in response to human or ecologic exposures to individual stressors (usually single chemicals or pollutants) in particular environmental media). Previous NRC studies have provided detailed advice on the risk assessment and risk management framework (e.g., NRC 1983, 1994, 2009). NRC (1983) elucidated a four-step process for risk assessment: hazard identification, dose-response assessment, exposure assessment, and risk characterization.

BOX 3-1 Examples of EPA Actions Informed by Risk Assessments

• Pesticide usage restrictions.

• Hazardous waste site remediation goals and approaches.

• Regulation of hazardous materials usage, storage and disposal.

• National ambient air quality standards.

• Emissions standards for hazardous air pollutants.

• Ambient water quality criteria for surface waters.

Source: EPA (2014i, p 1).

BOX 3-2 Recommended Principles for Uncertainty and Variability Analysis

1. Risk assessments should provide a quantitative, or at least qualitative, description of uncertainty and variability consistent with available data. The information required to conduct detailed uncertainty analyses may not be available in many situations.

2. In addition to characterizing the full population at risk, attention should be directed to vulnerable individuals and subpopulations that may be particularly susceptible or more highly exposed.

3. The depth, extent, and detail of the uncertainty and variability analyses should be commensurate with the importance and nature of the decision to be informed by the risk assessment and with what is valued in a decision. This may best be achieved by early engagement of assessors, managers, and stakeholders in the nature and objectives of the risk assessment and terms of reference (which must be clearly defined).

4. The risk assessment should compile or otherwise characterize the types, sources, extent, and magnitude of variability and substantial uncertainties associated with the assessment. To the extent feasible, there should be homologous treatment of uncertainties among the different components of a risk assessment and among different policy options being compared.

5. To maximize public understanding of and participation in risk-related decision-making, a risk assessment should explain the basis and results of the uncertainty analysis with sufficient clarity to be understood by the public and decision-makers. The uncertainty assessment should not be a significant source of delay in the release of an assessment.

6. Uncertainty and variability should be kept conceptually separate in the risk characterization.

aSource: NRC 2009, p. 120.

Uncertainty in quantitative risk assessments (such as those carried out using computational models) can arise from a lack or incompleteness of information, as well as incorrect information. Uncertainty analysis is rooted in understanding the level of confidence associated with a particular decision and the causes of the uncertainties. Uncertainty analysis is typically quantitative, and at the simplest level can be implemented by considering ranges for model input data (variables and parameters). Advanced uncertainty analysis methods could include simulation, in which statistical distributions for model values are used to produce a range of possible outcomes. As mentioned previously, variability is often considered along with uncertainty. It refers to actual differences in attributes due to heterogeneity or diversity in the system being considered. NRC (2009) also recommended principles for uncertainty and variability in a risk assessment context (see Box 3-2) but the principles are generally useful and relevant when considering the issues in the entire suite of EPA sustainability tools.

How Are Sustainability Considerations Currently Incorporated?

The Green Book found that the four-step risk assessment process, as envisioned by NRC (1983), is an important component and tool used to inform decisions in the SAM approach. Risk assessment can be used to inform considerations of sustainability concepts by estimating whether, and to what extent, public health or the environment will be affected if an action is taken. The Green Book recommended that EPA include risk assessment as a tool, when appropriate, as a key input into its sustainability decision making.

However, it is not always possible to address complex risk-related considerations quantitatively with the risk assessment approaches typically used by EPA. The approaches EPA relies upon have important limitations, including requiring large amounts of information and analyses, being applied mostly to existing problems rather than striving to prevent potential future problems from occurring, and taking excessive amounts of time to execute–particularly at the national level–when data are lacking (see NRC 2009 and 2011b for further discussion of the limitations).

Many of the broader public-health and environmental-health questions EPA is facing include multiple exposures to complex mixtures of chemicals. The traditional RA-RM approach does not adequately address this concern, particularly for communities that are especially vulnerable to environmental exposures by socio-economic stressors and disproportionate past exposures.

How Can Sustainability Considerations Be Incorporated Better?

In recognition of the limitations in approaching these complex issues, EPA has attempted to widen the context in which risk assessment is performed to include the early consideration of a broad range of decision options, and the cumulative threats of multiple social, environmental, and economic stressors to public health and the environment. In 2003, EPA released guidelines for cumulative risk assessments that include combined risks posed by aggregate exposure to multiple stressors–aggregate exposure includes all routes, pathways, and sources of exposure to a given agent or stressor (EPA 2003). However, there is substantial uncertainty in the approaches and the data for understanding outcomes for cumulative risks (EPA 2013b).

In addition, NRC (2009) pointed to the need for EPA risk assessments to take into account foreseeable consequences of possible decisions, including substitution risks (for example, considering the risks resulting from replacing one chemical used in commerce by another) and the potential for adverse outcomes associated with choices that might be taken by individuals affected by EPA’s decision.

Research and Data Needs

New techniques are needed for broader characterizations of cumulative risks to better account for the full range of environmental stressors, particularly for environmental justice analyses (see Chapter 6). A broadening of the risk assessment and risk management paradigm raises the need for screening-level risk-assessment tools (such as databases, computer software, and other modeling resources) (NRC 2009). For example, the integration of risk assessment with LCA would allow EPA to consider a fuller range of issues relevant to a decision (see discussion later in this chapter).

Characterizing and reducing uncertainty throughout the risk analysis process is a major challenge. Given limited agency budgets, it is essential that EPA be more decisive about what outcomes are more likely to occur and those that are likely to be consequential in order for it to compare tradeoffs.

Without narrowing uncertainty, it is difficult to assess, in a broad manner, the advantages and disadvantages of options, for example, about processes used to manufacture a chemical or how to evaluate a proposed site for drilling for oil and gas production. EPA needs to quickly scope from possible events, to their likelihoods and then to their consequences in order to identify major hazards.

There is also a challenge for risk managers to assess the effectiveness of investments in reducing risks from environmental exposures, rebounding from episodic events, and communicating these to stakeholders. This will be especially important for decisions concerning climate adaptation. North et al. (2014) discusses processes for stakeholder and public engagement in the context of managing environmental risks. In addition, NRC (2008) assesses whether, and under what conditions, public participation achieves the outcomes desired.

For consideration of impacts on a regional scale, for example, one needs to know not only the expected economic consequences of an event or exposures to stressors, along with their uncertainties, but also the consequences of investing in various levels of prevention. EPA and other major federal agencies have been stimulating research in these areas, but it has become even more imperative because of the increasing pace of emerging challenges (see Chapter 6). The committee further discusses the relationship of risk assessment and risk management decision making to sustainability approaches in Chapter 7.

Welfare Analysis: Benefit-Cost Analysis and Cost-Effectiveness Analysis

Economic benefit-cost analysis (BCA)3 and cost-effectiveness analysis (CEA) have been used for many decades to organize and evaluate information in support of decision making. Many textbooks provide overviews and definitions (e.g., Boardman et al. 2010). The conceptual foundations are described in an OECD document as:

“The essential theoretical foundations of CBA [benefit-cost analysis] are: benefits are defined as increases in human wellbeing (utility) and costs are defined as reductions in human wellbeing. For a project or policy to qualify on cost-benefit grounds, its social benefits must exceed its social costs. “Society” is simply the sum of individuals” (OECD, 2006, pp. 16-17].

CEA is concerned with how to get societal benefits at the lowest cost possible. For example, reducing pollution or saving lives is qualitatively a benefit, and might be measured in terms of tons avoided or lives saved (but neither are valued in dollars). The key contribution is being able to describe "cost per unit of effectiveness" without full monetization. It is possible to have multiple endpoints of interest for cost-effectiveness comparisons so that more than one criterion can be evaluated. CEA differs from BCA in that it considers only the cost of achieving a given set of improvements and provides a metric for identifying the lowest cost strategy to achieve this given gain. CEA and BCA can provide useful information for decision making whether or not potential effects of interest are monetized. However, when a decision is related to a regulation, which prescribes a level of control or expenditure, CEA would be more appropriate.

How Are Sustainability Considerations Currently Incorporated?

A strict decision rule of adopting programs or policies that “pass” a benefit-cost test is consistent with an economic efficiency criterion, but may fail broader sustainability considerations. Even when other criteria are used in decision making, BCA and CEA tools provide valuable information to decision makers. Indeed, a well-established reason for not adhering to a strict benefit-cost analysis occurs when the program or policy has significant distributional concerns, i.e., the costs and benefits are not equally felt across income, geographic, or racial groups (Arrow et al. 1996). One of the benefits of BCA and CEA analyses is that they inherently help connect stakeholders to net effects (e.g., who the winners and losers are, who has to economically sacrifice to make others better off). This is a key consideration when thinking about sustainability.

____________________

3The concepts of benefit-cost analysis (BCA) and cost-benefit analysis (CBA) are identical and used interchangeably.

A second reason commonly given for not adopting a strict benefit-cost test is that there are times when all ecosystem or environmental benefits cannot be monetized so that a decision rule that uses only monetized values risks adopting a policy that does not improve human wellbeing. An important recommendation of OMB (Circular A-94), also contained in EPA guidelines, is that all effects of a program or policy, whether they can be monetized or not, need to be clearly documented in either a BCA or CEA. This is another key tool in the context of sustainability and can be used as a general guide on how to qualitatively and quantitatively assess other sustainability metrics (for example see discussion below on ecosystem services valuation). It can also help when developing analyses of tradeoffs. Specifically, best practices in BCA recognize that there is a hierarchy of aspects that can be monetized, some that can be measured but not easily monetized, and some for which even measurement remains a challenge.

BCA and CEA are best considered tools for organizing information in transparent ways so that decision makers can understand the ramifications of their actions, regardless of the ultimate decision criterion they employ in choosing an action. Thus, BCA can provide information to support decision making within all three pillars of sustainability.

Sustainability has been defined in economics as a commitment to recognizing the welfare of future generations and to address intra-generational equity. Common distinctions are made between weak sustainability (a commitment to maintain a nondeclining or given standard of living over time) or strong sustainability (a commitment to preserve the stock of critical natural assets such as exhaustible or slowly renewable natural resources). See Pezzey (1992); Solow (1993); Stavins, et al. (2003) for definitions of these concepts.

Approaches that can be used to incorporate both weak and strong sustainability concepts in welfare analyses include:

• Use of distributionally weighted BCA (Boardman et al., 2010).

• Use of multiple discount rates (EPA 2014h).

• Inclusion of ecosystem or environmental impacts consideration even when impacts cannot be quantified or when monetary values are not assigned to quantified impacts (EPA 2014h).

• Presentation of the net benefits of a project broken down to reflect subpopulations of specific interest for social equity or environmental justice concerns such as income classes, geographic areas, racial groups, etc. (Farrow 2011).

• Economic Impact Analysis (such as, changes in prices, profits, plant closures, or employment) and distributional assessments (impacts on small businesses and cities, environmental justice analysis) (EPA 2014h).

• Consideration of multiple alternatives during the initial scoping of alternatives (EPA 2014h).

A recent and rather important development in the area of BCA is its emerging application to measures being considered for climate change mitigation. As mentioned previously, the sustainability tool for this purpose is SCC that is being used to incorporate the social benefits of reducing carbon dioxide (CO2) emissions into BCAs of regulatory actions that may have otherwise small impacts, but when combined with many other small impacts, lead to large cumulative global impacts. The SCC is an estimate of the monetized damages associated with an incremental increase in carbon emissions in a given year. The purpose of SCC estimates is to allow federal, state, and local agencies to evaluate and incorporate climate mitigation measures in their planning activities. The choice of discount rate is an important step in the computation of the SCC because it includes consideration of damages from climate change that are expected to occur far in the future, often to future generations. A scientific debate on the logic and ethical basis for choosing a discount rate in long time horizon problems has emerged (Arrow et al., 2013). EPA research into the appropriate choice of discount rate for its policies and programs is important. See Box 3-3 for additional details.

A May 2013 technical support document (TSD) prepared by the federal Interagency Working Group on Social Cost of Carbon provides detailed information on the range of values of the social cost of carbon (SCC) that can be used (US Interagency Working Group on Social Cost of Carbon 2013). The SCC values (in 2007 dollars per metric ton of carbon dioxide) are averaged values from the application of three peer-reviewed integrated assessment models (IAMs); an IAM is a sustainability analytics tool included in the Analytics report.

The 2013 TSD provides updated values from the 2010 TSD (US Interagency Working Group on Social Cost of Carbon 2010) of SCC at discount rates of 2.5%, 3%, and 5% and a value that represents a 95th-percentile SCC estimate for all three IAMs at a 3% discount rate. That fourth value is included to represent greater than expected effects of temperature change. Considerations in choosing the appropriate discount rate for evaluating environmental problems, such as climate change, that are long-term and intergenerational are mentioned elsewhere in this chapter.

The SCC estimates in the 2013 TSD report are 50–70% higher than those reported in the 2010 TSD; this reflects updating of information in the IAMs. The substantial changes in revised model estimates over the short period of 3 years indicate the rapid increase in knowledge of the science and economics of climate change. Equally important, the changes reflect many uncertainties involved in the model estimates, which should be reduced as data and models improve.

In addition, a number of major private-sector companies are using internal carbon pricing as a strategic tool in their business planning (also see Chapter 5) (CDP 2014).

In the environmental pillar there has been a significant and ongoing scholarly effort to measure and monetize ecosystem services. EPA Guidelines for BCA already provide solid guidance on this issue. They suggest that the benefits of a change be expressed in physical or natural units, consistent with the view of reflecting all environmental changes, even if they cannot be monetized.

How Can Sustainability Considerations Be Incorporated Better?

Incorporation of sustainability considerations with the use of BCA and CEA can be enhanced through the following activities:

• When undertaking BCA projects with intergenerational impacts, consider using the lowest reasonable discount rate following the advice of Arrow et al. (2013)

• Use the most up to date SCC estimates when undertaking BCAs for major rules and regulations dealing with climate mitigation measures.

• Consider the extent to which costs and benefits vary among income, socioeconomic, racial, urban/rural, gender, and other class distinctions.

• Present costs and benefits estimates by income, age, race, and other relevant factors in CEAs, RIAs and other economic assessment that the agency uses. The purpose is to make those tools more useful in describing what groups will be most affected by a decision (e.g., regulation, permit, or cleanup action).

• For large projects or programs, when considering alternatives at the beginning of an analysis, identify at least one alternative that is specifically focused on concepts of sustainability.

• When doing ex-post BCA, include a discussion of whether there were alternatives that were not considered that might have achieved similar net benefits, but would have been more sustainable (e.g., would have has less impact on nonrenewable resources, would have generated fewer greenhouse gases while achieving the goal, or would have had less impact on a disadvantaged population). This approach would help focus on sustainability considerations for future planning.

Research and Data Needs

EPA should develop guidelines for preparing a sustainability assessment analogous to its Guidelines for Preparing Economic Analysis (EPA 2014h). (Recommendation 3c)

Developing the guidelines could be accomplished, particularly in the short run, by adding a chapter to the existing guidelines that addresses sustainability tools and their inclusion in BCA. It will be important for EPA to identify a home for the responsibility to maintain and update this guidance.

In its consideration of ex-ante modeling approaches for CEA, Fell and Linn (2013) provides a useful discussion of corresponding data needs.

Life-Cycle Assessment

LCA approaches to decision making involve consideration of all relevant aspects of a system over its life cycle (McDonough and Braungart 2002, SAIC 2006, and Hellwig and Canals 2014). The purpose of life-cycle approaches is to provide information to ensure that actions will not have unexpected or unanticipated effects elsewhere in the product system (such as a different life-cycle stage) or different effects (such as unexpected material-acquisition demands to increase energy efficiency). LCA also helps to ensure that users are aware that the implications of decisions are not isolated but are part of a larger system, improving the entire system—not just a single part of the system—for a longer term (UNEP/SETAC LCI 2004).

One may visualize the approaches along a continuum from qualitative screening (which provides early direction to a decision-making process) to semiquantitative assessment (which helps to substantiate improvement and effects along the system) to quantitative assessment (which provides confidence that the proposed actions or decisions will create improvements). The aquatic-toxicity field might offer an analogue. Early in an analysis of the potential effects of a chemical on the environment, a practitioner usually conducts a screening LC50 study that provides the general range of concentrations that should be used in a definitive LC50 study.4 Similarly, a screening-level LC study can be used to help to define the effects or life-cycle stages for which additional data collection is warranted.

As mentioned previously, LCA is listed as one of the tools in EPA's Analytics report, but it is defined as applying only to products. More broadly, LCA is able to represent an accounting of the inventory and effects of products, processes, or systems. LCA comprises multiple steps that eventually lead to a life-cycle inventory (LCI) that sums the flows by environmental compartment for any chosen effects over the life cycle (such as total carbon dioxide emissions to air). A later step, life-cycle impact assessment (LCIA), transforms the inventory flows (such as carbon dioxide and sulfur dioxide emissions and energy use) into such effects as global-warming potential and acidification. Various methods of impact assessment, including the EPA-led TRACI (tools for the reduction and assessment of chemical and other environmental impacts) method (Bare 2011) relevant to the United States, are available in support of LCA studies. LCA methods can also be used to measure costs of assessing economic performance, but this application is in an earlier stage of development than the environmental applications.

LCA examines the potential effects associated with a product, process, or system. It can be combined with risk assessment to provide risk estimates over an entire life cycle rather than at a particular point. It can also be used to perform attributional analyses (to estimate effects associated with an existing product) and consequential analyses (to estimate effects associated with introduction of a new product into an economic system).

International Organization for Standardization (ISO) LCA standards 14040/14044 (2006) form the core approach for conducting an LCA study. They are also the basis of many related activities, such as carbon-footprinting protocols developed by the World Resources Institute/World Business Council on Sustainable Development and water-footprinting standards developed by ISO. Although it is not a con-

____________________

4An LC50 is the concentration of a substance in an environmental medium that kills 50% of the test organisms.

ceptually difficult method, LCA requires rigorous consideration of boundaries, flows, inventories, and effects. The formalization of the international standards provides a valuable technical foundation that does not exist for many of the other methods mentioned. However, the ISO LCA standard is not a recipe for performing LCA; rather, the standard provides the basic principles for and guidance on conducting an LCA study. One of the key elements of the standards is the importance of the Goal and Scope Definition element, the first step. In this element, there needs to be agreement on the purpose, intended audience and applications, boundary conditions, scope, and other key planning considerations. The ISO standards allow flexibility so that if the purpose of a study is to inform initial direction in identifying risks and opportunities, there can be leeway in boundaries and data quality. However, if the purpose of a study is to make an external claim about the superiority of one product over another or about their equivalence, additional requirements must be met.

Another critical design parameter is the choice and definition of a functional unit, for which effects are expressed as quantities per unit (for example, per kilowatt–hour of electricity) for the study. LCA is often used to explore inventories, effects, and opportunities in a relative fashion, for example, compared with previous design of a product system or of a competitor.

Recent decisions in the retail and green-building sectors, for example, have created a rapid increase in the application of LCA approaches in the United States. The increase has resulted in simplified computer-aided design tools. Moreover, EPA is taking a leadership role in an intergovernment group to advance the interoperability of national databases as part of a global network.

Finally, one of the most pressing applications of LCA is in support of public policy and decision-making. As LCA and its underlying databases and methods have matured, the desire to use it in support of major decisions has grown. For example, LCA was used in support of the federal renewable fuels standard to estimate the life-cycle carbon emissions of conventional and biobased fuels (see the biofuels case study in Chapter 4 for more information).

How Are Sustainability Considerations Currently Incorporated?

Although LCA approaches can be used to consider all sustainability pillars, studies using this tool usually have not considered all three pillars. UNEP/SETAC (2013) concluded that life-cycle sustainability assessments are possible; however, methodological improvements are needed, including data production and acquisition, and formats for communication of results (Valdivia et al. 2013). In terms of economics, LCA studies have considered the life cycle cost of the product or system in question (e.g., improvements in energy efficiency, roads, and other infrastructure), which has helped to reinforce life cycle thinking by ensuring that first costs and recurring costs are considered. The life cycle community views that LCA consist of four phases (goal and scope definition, inventory, impact, and interpretation). These studies seek to translate LCA inventories into common impact metrics, and also have used the ISO LCA Standard to normalize these metrics into a per-capita basis, within the normalization portion of life cycle impact assessment. There have been efforts underway to add life cycle costing to some studies, but this is still early in the maturity of applying LCA. Moreover, some research is underway to explore how to incorporate social impacts into LCA studies.

Social and socio-economic LCA (S-LCA) aims to assess the social and socio-economic aspects of products and their potential positive and negative impacts along their life cycle encompassing extraction and processing of raw materials; manufacturing; distribution; use; re-use; maintenance; recycling; and final disposal. S-LCA differs from other social impacts assessment techniques by its objects (products and services) and its scope (the entire life cycle). S-LCA usually targets direct effects (positive or negative) on stakeholders during the life cycle of a product. The effects may be linked to the behaviors of enterprises, socio-economic processes, or impacts on social capital. Depending on the scope of the study, indirect impacts on stakeholders may also be considered.

Guidelines for Social Life Cycle Assessment of Products (UNEP/SETAC 2009) provides direction for stakeholders engaging in the assessment of social and socio-economic impacts of product life cycles.

Benoit, et al (2013) explored the initial development of a social hotspots database (SHDB) that provides social risk information on 22 themes within 5 social impact categories: labor rights and decent work, health and safety, human rights, governance, and community impacts.

How Can Sustainability Considerations Be Incorporated Better?

There are various ways in which EPA could ensure that LCA is incorporated into sustainability assessments better:

• Strive to make LCI and LCIA results more readily comparable across pillars, such as by estimating costs associated with life-cycle impacts.

• Urge studies to go beyond mere LCIs and proceed to LCIAs, and interpretation of the implications of various design or technology options.

• Develop ways in which social issues, such as equity or environmental justice, could be assessed. As part of an overall sustainability tool box, monitor and engage in an understanding of the current development of S-LCA methodology and begin to pilot its applications.

Research and Data Needs

Over the last 20 years, EPA, other government agencies, industry, and life cycle practitioners have made considerable advances in the LCA methodology through their own efforts as well as efforts by efforts lead by SETAC, ISO and UNEP/SETAC Life cycle Initiative. In parallel, the life cycle data bases have grown rapidly as the demand for life cycle information to assess the potential trade-offs of multi-impacts (e.g., energy, water, GHG, and others) along a product’s life cycle from material acquisition, manufacturing, logistics, use and end of life disposition.

The US Department of Agriculture (USDA), in collaboration with EPA, is leading the development of a ‘digital commons’ data base. The goal in developing the database is to provide open access LCA datasets and tools. The project is intended to make North American LCA data more accessible to the community of researchers, policy-makers, industry process engineers, and LCA practitioners. The initial focus is on providing data for use in LCAs of food, biofuels, and a variety of other bioproducts.

Complementary to the government-led data base efforts, industry associations have been collecting generic life cycle data on chemicals, plastics and other materials to inform decisions concerning raw materials acquisition through the end of initial processing (often referred to as cradle to gate). Companies that need more site-specific data or supplier specific data are collecting and using a combination of site-specific and generic data to inform product-design and materials-selection decisions.

Also, EPA and USDA are collaborating with the United Nations Environment Programme (UNEP) to develop a vision, guiding principles, and an approach for implementing a voluntary international network to promote LCA data accessibility, interoperability and applications. This effort builds on previous collaborations between EPA and the UNEP/SETAC Life cycle Initiative to develop Global Guidance Principles for Life Cycle Assessment Databases.

While LCIA methods have been developed, the US impact assessment methods have not received as much resources for research and development as those in Europe. Further development of the US-based TRACI method needs to be undertaken.

In recognition of the range of LCA approaches from qualitative to quantitative, additional guidance should be developed and implemented to illustrate how the approaches can be used in EPA decision-making. The guidance should address the combined application of risk assessment and LCA for evaluating the relative merits of various options for managing risk associated with the entire life cycle of products, processes, or systems. (Recommendation 3d)

The committee also notes that while some LCA studies have considered robust treatment of risk and uncertainty using probabilistic methods, most studies remain deterministic.

EPA should disseminate educational tools and examples that describe this additional quantitative step. (Recommendation 3e)

This would make rigorous LCA more commonplace and more worthy of use in emerging areas of sustainability assessment and public policy analysis.

The section above describes extensions of EPA guidance documents in support of BCA. While EPA has made various online LCA references available (e.g., the "EPA 101" documentation) (EPA 2014i), they are mostly summaries of general information on the ISO standard.

EPA should enhance the documentation by applying the same "identification-quantification-monetization" framework, used in describing BCA and CEA, to facilitate the adoption of a life cycle perspective in scoping problems and optimize the use of LCA as a sustainability tools. (Recommendation 3f)

This would help ensure that the potential impacts are considered, even if the LCA methods are not able to quantify or monetize them.

EPA should promote and support the development of new datasets relevant to major agency decisions, such as those associated with water and land use. (Recommendation 3g)

EPA is encouraged to continue its leadership role in the recently formed inter-governmental LCA platform group, whose initial purpose is to develop and advance the inter-operability of a database network.

Valuation of Ecosystem Services

The term ecosystem services refers to the benefits society receives from the spectrum of resources and processes provided by ecosystems through their functions–the interactions of plants, animals, and microbes with the environment (NRC, 2011a; NRC, 2013a). Ecosystem services is only one of the approaches that can be used to assess ecosystem sustainability, explicitly linking ecosystem structure and function to human reliance and values. Ecosystem system services valuation is the process of measuring values associated with changes in an ecosystem, its components, and the services it provides to human well-being (NRC 2004a). The valuation of ecosystem services is relevant to the area of welfare economics because ecosystem services include market and nonmarket goods. However, the ecological underpinnings of these services and the appreciation of these services to humans warrants a separate discussion in the context of sustainability. The services provided by ecosystems are generally divided into four categories: provisioning services (e.g., food, fiber, drinking water); regulating services (e.g., flood protection and pest control); cultural services (e.g., spiritual and aesthetic benefits); and, supporting services (e.g., soil formation, primary productivity) (MEA 2005). Ecosystem service studies have tended to focus on small changes in an ecosystem, but large-scale studies of ecosystem services such as Costanza et al. (1990) sought to monetize the value of wide scale changes in ecosystem services. EPA SAB (2009) recommends these steps for conducting ecosystem service valuation:

• Formulate the valuation problem and choose policy options to be considered, given the context within which the tool will be applied;

• Identify the significant biophysical responses that could result from the different options;

• Identify the responses in the ecosystem and its services that are socially important (have social value);

• Predict the responses in the ecosystem and relevant ecosystem services in biophysical terms that link to human/social impacts and hence to values; and,

• Characterize, represent, or measure the value of responses in the ecosystem and its relevant services in monetary or non-monetary terms. As with benefit cost analysis, non-market valuation of ecosystem services is an important and critical step (EPA 2014k).

By enabling policy makers to account for the services ecosystems provide, this tool informs planning, priority setting, and rule making, and can contribute to decision making based on sustainability grounds. In the past, EPA has used the concept of adversity of effects to public welfare (and, its link to ecosystem services valuation) in its review of secondary National Ambient Air Quality Standards (NAAQS) for ozone through vegetation damage related to ozone as well for secondary NAAQS for fine airborne particles relating to visibility degradation. More recently, EPA’s 2012 proposal to establish NAAQS for oxides of sulfur and oxides of nitrogen to protect aquatic and terrestrial ecosystems relied heavily on monetized as well as non-monetized valuation of ecosystem services derived from attainment of the proposed standards (77 Fed. Reg. 20218 [2012]). Future incorporation of ecosystem services valuation into the sustainability context is expected to strengthen the EPA decision making process that has generally emphasized human health benefits through risk assessment and risk management paradigm.

How Are Sustainability Considerations Currently Incorporated?

EPA has developed a number of programs and guidance documents regarding valuing ecosystem services. These documents include the development of ecological production functions and procedures for developing ecosystem services valuation (EPA 2014k). This body of work provides a strong basis from which EPA can continue to lead the development of ecosystem services valuation. Those efforts illustrate a recognition of the importance of identifying the full suite of ecosystem services, not just those that are easily measured and valued. Nonetheless there remains inadequate understanding of many of the production relationships and values associated with the more difficult to measure services.

How the Valuation Process Could Be Incorporated Better

A number of steps can be taken to advance the science of ecosystem service valuation. However, for many ecosystem services there may be insufficient understanding of the ecological production functions or the societal values associated with those services, diminishing their consideration in sustainability analyses. For valuation of specific services, there may be considerable variation among different societal groups whose inclusion is necessary to ensure an equitable distribution of benefits (NRC 2012a).

Future Research and Data Needs

EPA should continue to develop ecosystem service valuations to characterize, quantify, and monetize the types of ecosystem services contributions that have been difficult to valuate in the past (e.g., value of nutrient cycling and biodiversity). (Recommendation 3h)

EPA and other federal agencies should support efforts to develop new approaches to evaluate the effects on ecosystem services of national, regional, or local actions in ways that valuation methods can incorporate. (Recommendation 3i)

In particular, R&D needs to focus on the development and use of ecological production functions that can estimate how effects on the structure and function of ecosystems will affect the provision of ecosystem services that are directly relevant and useful to the public.

Where ecological production functions do not exist, R&D should seek to improve upon and strengthen the current methods based on ecological indicators. (Recommendation 3j)

EPA’s R&D efforts should focus on developing and implementing the broader suite of applicable valuation methods including economic methods; measures of attitudes, preferences, and intentions; decision science approaches; and ecosystem benefit indicators and metrics. (Recommendation 3k)

Such methods then could be employed in identifying services of importance to the public (as noted above), better capturing the full range of contributions stemming from ecosystem protection.

TOOLS, UNCERTAINTY, AND TRADEOFFS

The effective use of tools to incorporate sustainability considerations into EPA activities partly depends upon how their use recognizes and deals with uncertainty and thus helps decision-makers understand tradeoffs among options. Tradeoffs are the part of the decision-making process that requires balancing advantages and disadvantages of alternatives. In the case of sustainability, the ability to inform tradeoff decisions depends upon the capacity of the analyst to use the tools to isolate and describe key advantages and disadvantages of choices with respect to economic, environmental, and social aspects. Uncertainty and the ability to make well-informed tradeoff decisions are inexorably linked. If uncertainty is too great, there may be insufficient confidence to use a tool for decision-making purposes. Although the results of sustainability analyses are associated with uncertainty, it is important to understand how the tools can help to inform decisions. Assessment of climate change effects is a useful example. Many relevant decisions will need to be made, including those related to adaptation, despite uncertain knowledge about effects, geographic distribution, and costs.

A good way of illustrating the relationships between tools, uncertainty, and tradeoffs is with a hypothetical example (see Box 3-4). When sustainability tools produce results, decision-makers can make tradeoffs among the economic, environmental, and social consequences associated with each option, including changing the final design to a hybrid of the last two options. What is critical is that the decision-makers understand the uncertainty in the output produced by each tool, and highlighting these in their deliberations as they consider the next few years and the next 25, or so. In the case described Box 3-4, the key large uncertainties are likely to be exposure, representativeness of the population engaged compared to the potential user community, and the economic cost versus benefits of the reuse options as the impact the next three years versus the next 25 years.

Many decisions that involve sustainability involve considerations that go beyond the local scale to regional, national or even global. Decisions involving sustainability that are related to global climate change, for example, are marked by major uncertainty because some places will likely benefit (at least in the short term) and others will likely be devastated or experience a new normal. Nevertheless, even for these mega scale issues, analysts need to try to put appropriate uncertainty bands around their use of environmental, social and economic tools over spans that will range from a few years to perhaps a century. The tradeoffs clearly become even more difficult to make as the geographical and temporal scales expand.

KEY CONCLUSIONS AND RECOMMENDATIONS

Conclusion 3.1: The broad array of sustainability tools and approaches presented in EPA’s sustainability analytics report are potentially applicable in assessing possible social, environmental and economic outcomes within EPA’s decision-making context. Although some tools and approaches are more advanced and further developed than others, there is no hierarchy of tools with respect to selection. The applicability of the tool depends on the context of the problem.

BOX 3-4 An Hypothetical Waste Site

The future use of a large abandoned landfill in a suburban town is being discussed. It is not a Superfund site. Chemical contaminants flowed from the site into the underground aquifer, and public access to the site is not permitted. There are different views about what to do with the site. One is to do nothing. The second is to install a pump-and-treat system to contain the underground water contamination. The third is to incorporate pump-and-treat but to reclaim the site for walking and biking and as a meeting place for local environmental officials.

To make an informed choice from among the no-action, pump-and-treat, and light-redevelopment options, data need to be gathered and interpreted. The initial tools are exposure assessment, risk analysis, and environmental-footprint analysis. Uncertainty becomes an issue because unless there are good data about the location and concentration of the contamination, where it is heading, and at what speed, there is high uncertainty about how many people could be exposed by drinking water from the aquifer or by using the site for recreation. The above environmental tools are essential to determine whether the site needs to be remediated to keep local water supplies from being contaminated now and in the foreseeable future—in other words, to have a safe potable-water supply. The decision is likely to affect thinking about further development of the site, so the initial key uncertainty is in prediction of exposure; if the uncertainty is too high, it will be hard to make tradeoffs among the three options.

Social tools, most notably segmentation analysis and network analysis, are used to determine the size and attributes of the community—including the public, business, and not-for-profits—that support each of the three options. If it is a small site and the expected effects are localized, this is likely to be done with several focus groups or public meetings. The uncertainty here is related to the representativeness of the community included in the focus groups and public meetings. Public meetings are not usually attended by a representative group of community members. What would happen if millions of dollars were invested in a sustainable recreation site with a green building for a meeting place, and then few people used it? It is essential that some effort be made to increase the certainty that the stakeholders are representative of the body of potential users. One way to increase confidence is to build a collaborative process and use charrettes to determine whether there is a consensus about a plan for a sustainable green site on the abandoned landfill.

Economic tools are essential. BCA can be used to evaluate whether the benefits to the local population from using the site for hiking, for biking, and as a meeting place are likely to exceed the costs, but these estimates will be uncertain because they depend on the preferences of current residents and may not reflect future citizens’ preferences (25 years hence) or a wide array of variables that can change future benefits and costs, such as general economic conditions in the region, development of other recreation sites in the region, and changing population attributes of the citizenry.

Recommendation 3.1.1: EPA should use concepts of sustainability to strengthen a systems-thinking approach in using current and future tools and approaches, as necessary, to support EPA decision-making. The agency has many opportunities to incorporate sustainability considerations by applying those tools and approaches across the spectrum of its activities and it should do so rapidly.

Recommendation 3.1.2: For every major decision, EPA should incorporate a strategy with the goal of assessing the three dimensions of sustainability in an integrated manner. EPA should apply tools and approaches in a manner best suited to the type of problem being addressed. The selection of a particular tool for an application should be informed by the type, adequacy, and availability of data needed and other criteria identified by the committee.

Conclusion 3.2: EPA has taken a good first step in developing the 2013 version of the Sustainability Analytics report. It provides a reasonable and informed baseline survey of sustainability tools.

Recommendation 3.2.1: EPA should arrange for the use of a publicly available Internet-based mechanism (for example, an electronic wiki) to track updates about existing and emerging tools. This process should allow visitors to suggest updates to documentation for existing tools and identify new tools for EPA’s consideration. Such a mechanism would help the agency update its tool descriptions and applications for specific tools in a more timely manner.

EPA’s sustainability analytics report should be considered a living document with appropriate updates on a regular schedule. Future versions of the report should provide additional discussion of integrative applications of the tools and how a tool can be used to provide information to support decision making involving tradeoffs, where one or more sustainability pillars could be at odds with one another. New tools identified would be added. (Recommendation 3a)

Recommendation 3.2.2: EPA should consider using a consistent set of criteria to evaluate the tools and carry out assessment exercises that are similar to the one conducted by the committee with the agency’s own internal users of these tools, or a larger set of external stakeholders for corroboration. The assessments should help to identify opportunities for improvement and identify considerations in selecting tools for particular activities. (See Recommendation 3b)

Recommendation 3.2.3: A potentially important tool that is currently not included in the sustainability analytics report is the recently developed approach for considering the social cost of carbon (SCC). Given the prominence of climate-change mitigation issues for EPA and the fact that SCC focusses explicitly on future benefits and costs of current decisions–a significant component of sustainability–EPA should include it in its sustainability analytics report in the near future.

Conclusion 3.3: Various sustainability tools (such as benefit-cost analysis, life cycle assessment, and risk assessment) have been identified by EPA and agreed upon by the committee as being more mature and pervasive than others. The historical development of these tools and EPA's adoption of them into decision making serves as exemplars for the other tools. These mature tools also can continue to be improved through EPA's guidance and support.

Recommendation 3.3.1: EPA should develop guidelines for preparing a sustainability assessment analogous to its Guidelines for Preparing Economic Analysis (EPA 2014h). Developing the guidelines could be accomplished, particularly in the short run, by adding a chapter to the existing guidelines that addresses sustainability tools and their inclusion in BCA. It will be important for EPA to identify a home for the responsibility to maintain and update this guidance. (See Recommendation 3c)

Recommendation 3.3.2: To facilitate the further use of life cycle thinking and the development and deployment of life cycle assessment, EPA should continue educational and research support programs to develop and implement guidance that illustrates how a range of qualitative to quantitative LCA approaches can be utilized within EPA decision making. The quantitative guidance should include applications of combined probabilistic risk assessment and LCA approaches, which can be used in concert to examine a fuller range of issues relevant to a decision. (See Recommendations 3d-3f)

Recommendation 3.3.3: To facilitate the further development of LCA methods, EPA should collaborate with other federal agencies, the private sector, and other non-governmental organizations to promote and support the development of new datasets for LCA relevant to major agency decisions, such as water and land use, and continue development of and encourage use of life cycle impact assessment methods (e.g., TRACI). (See Recommendation 3g)

Recommendation 3.3.4: EPA should continue to develop ecosystem service valuations to characterize, quantify, and monetize the types of ecosystem services that have been difficult to valuate in the past (e.g., value of nutrient cycling and biodiversity). In particular, these efforts should focus on the development and use of ecological production functions that can estimate how effects on the structure and function of ecosystems will affect the provision of ecosystem services that are directly relevant and useful to the public. Where ecological production functions do not exist, R&D efforts should seek to improve upon and strengthen the current methods based on ecological indicators. (See Recommendations 3h-3k)