5

Successful Efforts to Address Challenges

The workshop’s second panel session featured five presentations describing the approaches taken to address various pieces of health insurance literacy. Dara Taylor, director of Community Catalyst’s Expanding Coverage through Consumer Assistance Program, described a successful approach for supporting navigators. Erin Hemlin, national director of training and consumer education at Young Invincibles, discussed the successful strategies her program uses to reach the young and healthy. Robert Krughoff, president of Consumers’ Checkbook’s Center for the Study of Services, spoke about the tools his organization developed for comparing health plan information. Amy Cueva, co-founder and chief experience officer of Mad*Pow, reviewed the user-centered design approach her team uses to design readable medical bills and other materials for consumers. The final panelist, Renée Bougard, a project scientist in the National Network Coordinating Office at the National Library of Medicine, spoke about the important role that libraries and librarians can play in providing understandable information of consumers on health and health insurance. Bernard Rosof moderated an open discussion among the workshop participants after the presentations.

SUPPORTING THE NAVIGATOR1

Community Catalyst, explained Taylor, is a national nonprofit advocacy organization that works with national, state, and local consumer organizations, policy makers, and foundations to build consumer and community leadership to improve the health care system.

The organization supports consumer advocacy networks that impact state and federal health care policy and ensures consumers have a seat at the table as health care decisions are made. The organization works in more than 40 states, with a primary focus on health issue campaigns, such as access to dental care, preventing substance abuse, and hospital community health benefit programs. Community Catalyst also supports health system transformations and provides support to health insurance enrollment assisters.

Enrollment assistance programs exist in every state. They are staffed by different types of enrollment assisters: navigators, in-person assisters, and certified application counselors, Taylor explained. In addition, federally qualified health centers also have enrollment assisters on staff. For the purposes of this presentation, Taylor referred to all of these as enrollment assisters, and characterized them as individuals who need to have a good understanding of how to conduct policy analysis so they can explain the different regulations, the tax implications, and the ways in which the marketplace and the ACA as a whole impacts a consumer. “They almost have to have legal expertise,” said Taylor. Most assisters do not have legal expertise. It is not necessary, but a testament to the complexity of the enrollment circumstances that assisters face with individual consumers, Taylor said.

According to Taylor, assisters need to be personable individuals so that consumers feel comfortable sharing personal information related to their finances and health status. She said the best assisters function in some respects like a community organizer in that they are out in the community, conducting face-to-face forums, engaging community organizations and businesses, passing out flyers, and working to get the word out to the uninsured in the community. Assisters also develop referral networks for their clients. “This is a unique individual that we are talking about here,” said Taylor. “They need to have a varying skill set that the average everyday person may not possess.”

The most successful and by Taylor’s estimation the most popular resource that Community Catalyst provides to the assister community program is an online, password-protected resource called In the Loop. This network, which is co-managed by the National Health Law Program, has

___________________

1 This section is based on the presentation by Dara Taylor, director of Community Catalyst’s Expanding Coverage through Consumer Assistance Program, and the statements have not been endorsed or verified by the National Academies of Sciences, Engineering, and Medicine.

more than 4,400 members from all 50 states and the District of Columbia. This network is only for assisters and health policy experts, said Taylor, and is not open to agents, brokers, insurance carriers, or state or federal policy makers. “It is focused on the nonprofit enrollment assister,” she explained.

Members can post questions for the online community and in real time get an answer on how to deal with whatever challenging situation they may be confronted with at the time. An enrollment assister in Montana, for example, can post a question she believes is unique to Montana, and another assister from Alabama may chime in with the same issue. “We monitor the site and when we see those types of common things come up, we summarize those challenges weekly and share them with the White House, the IRS [Internal Revenue Service], HHS, and various policy officials,” said Taylor. In this respect, In the Loop serves as a communication loop among assisters within and across states that helps the entire community improve how it works with consumers and addresses their problems.

The amount of training that assisters need to do their job well cannot be understated, said Taylor. The initial certification process is fairly basic, she said. “It talks about ACA and the marketplace, but it does not provide specific information that you need to know on how to enroll a consumer,” she explained. For that reason, she believes it is important that the type of trainings she and her colleagues have developed be spread across the country. “The only reason we in Missouri are able to provide this type of hands-on and robust training to the enrollment community is because of the significant investment of the Missouri Foundation for Health,” said Taylor. Funding for this effort comes from the $1.8 million the state receives from the federal government, additional funding from the federally qualified health centers, and $5 million annually from the Missouri Foundation for Health.

In Missouri, Community Catalyst provides one-on-one technical support via phone, email, and face-to-face trainings. It provides additional training on the federal government’s and state’s certification and licensing requirements and has created a broad learning community through webinars, conference calls, and face-to-face meetings. “These serve as a space for the enrollment assisters to talk about the strategies that have worked and those that have not worked,” said Taylor. These lessons, she said, are helping the assisters plan for the fourth open enrollment period. Community Catalyst also provides trainings on marketplace policy issues and creates consumer-facing materials for the assisters to use along with fact sheets, talking points, and lists of frequently asked questions (FAQs) with accompanying answers. It also provides health literacy and health insurance literacy support, explained Taylor.

She noted that the role of assisters is changing as the ACA moves into its fourth year of enrollment. As was mentioned previously, assisters are

now helping clients learn how to use their new insurance to access the health care system. With that comes an increased emphasis on health literacy and health insurance literacy, said Taylor, as well as the need to have an expanded expertise in broad insurance coverage. Going forward, she said, there is a need for more assisters on the ground, as well as continued support for In the Loop or other mechanisms that enable assisters to have their questions answered and to share useful solutions they have developed to common problems. More extensive training approaches need to be disseminated nationwide, and additional trainings will be needed to help assisters with their developing roles as navigators for more than just insurance enrollment, she concluded. Assisters also need additional resources on health literacy and health insurance literacy.

ATTRACTING THE “YOUNG INVINCIBLES”2

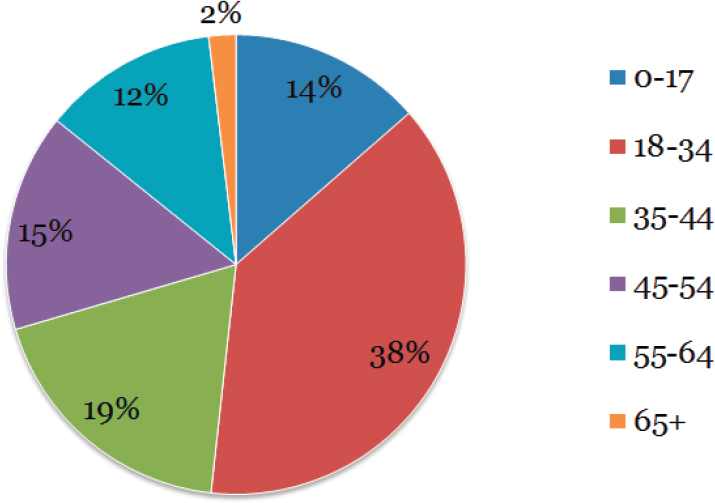

The Young Invincibles, explained Erin Hemlin, is a research and advocacy group that works for the economic advancement of young adults ages 18-34. The organization’s priority issues are access to health care, access to higher education, college affordability, and some workforce protection and security issues too. Young Invincibles was founded in large part because of the ACA, said Hemlin, by students at Georgetown Law School who had been paying attention to the health care reform debate as it was happening in Congress in 2009 and who believed there was no discussion about how the ACA was going to affect young people. Young Invincibles, she said, played an important role in creating the ACA provision that enables young adults to remain on their parents’ health insurance plans until age 26, which she said has been shown to be one of the most popular parts of the law. She noted, too, that prior to the passage of the ACA, young people were uninsured at higher rates than any other group, at approximately 28 percent nationwide. As of September 2015, some 38 percent of the remaining uninsured are ages 18-24 (see Figure 5-1). Among young adults of color, that percentage is even higher, said Hemlin.

Once the ACA was enacted, Young Invincibles began focusing on educating millennials and the organizations that serve young adults about new health insurance coverage options and to mobilize young adults to enroll in coverage. Its campaign, called Healthy Young America, began in 2012 and built a coalition of nearly 2,000 partners that has now held some 200 health care events around the country, directly served more than 20,000 people, and reached more than 2 million people online, mostly

___________________

2 This section is based on the presentation by Erin Hemlin, national director of training and consumer education at Young Invincibles, and the statements have not been endorsed or verified by the National Academies of Sciences, Engineering, and Medicine.

SOURCE: Presentation by Hemlin, July 21, 2016.

through social media and email. One of its biggest events is the National Youth Enrollment Day, the latest of which was held on January 21, 2016. Young Invincibles partners with the White House and HHS to hold this event annually during open enrollment as a means of getting all the groups working on ACA education and outreach to focus their attention on young people for 1 day. “We hold it about 2 weeks before the deadline of each open enrollment period to get those young people who tend to procrastinate to pay attention to what is going on before that deadline hits,” explained Hemlin.

The first two National Youth Enrollment Day events attempted to create an atmosphere of celebration and portrayed getting health care as a rite of passage in life. The events featured music and food trucks in addition to having assisters and health care organizations available to help with health and health insurance questions. Assisters also set up appointments for enrollment or in some cases enrolled people onsite. “We did it that way to take away some of the intimidation factor,” said Hemlin. “Once we got them to the table, then it was a little bit easier to walk them through that process.”

Going forward, the challenge of reaching the remaining uninsured will

increase now that the “low-hanging fruit” are in the system. In addition, the media’s attention to the problem has decreased and will likely be pushed aside by this year’s election coverage, said Hemlin. Another consistent problem for young people is that the open enrollment period occurs when many young adults are either in school or are working part-time, seasonal jobs to make ends meet during the holiday season. On the other hand, there are factors that could increase enrollment among young adults. To start, Young Invincibles and other organizations focusing on young adults have the experience they gained during the preceding open enrollment periods, as well as the strong partnerships that have developed during the initial years of the ACA. In addition, said Hemlin, young adults attach less political stigma to the ACA and are now seeing health insurance as a validator of adulthood and hearing positive stories from their compatriots who have become newly insured. “Young people are talking to young people about the importance of health insurance and this has been a huge advantage in doing some of this work,” said Hemlin.

In addition to peer-to-peer outreach, Young Invincibles relies on key messengers and trusted partners, such as parents, community colleges, employers in the retail and service industries, job fairs, faith leaders, partners at historically black colleges and universities and Hispanic-serving institutions, safety net programs, transition centers, and tax prep providers. “Young people are very unlikely to come in to us, so we have to go find them where they are working, where they go to school, where they are socializing, and where they are going to church,” said Hemlin. Community colleges, for example, have been fertile ground for enrollment efforts given their large number of non-traditional students who are typically a little older and have full-time or part-time jobs. Bars and restaurants also have proven to be good recruitment centers, particularly when they are congregated in neighborhoods. In addition, word spreads quickly through the restaurant worker community, so success in one restaurant or bar trickles down through the rest of the community, said Hemlin.

Messaging is important to young adults, and Young Invincibles’ messaging efforts have focused on affordability, the benefits of having insurance, financial security, financial assistance and tax credits, and the individual mandate and penalty. One of the benefits stressed in these messages is the free preventive care that now comes with every insurance plan. Messaging also highlights the fact that young adults end up in the emergency department more than any other age group other than the elderly, so having insurance is a matter of financial security.

Over the past year, Young Invincibles has been working on health insurance literacy, which is low among young adults who have limited experience with the health care system and who have generally been healthy. From the experience she and her colleagues have had with young people,

even those who have had health insurance have a low understanding of how their insurance works. This campaign, called #HealthyAdulting, aims to increase health insurance literacy rates among young adults through consumer education and digital engagement that promote use of health insurance and preventive care and retaining coverage, explained Hemlin. To inform this campaign, Young Invincibles held a series of focus groups in six cities across the nation to get an idea of what young people understand and do not understand about health insurance, what kind of messaging would work, what they want to know, and when they want to know it. “We were trying to find that health care access point of when this information would be most useful for young people so they would retain it and take action,” said Hemlin.

Some of what Hemlin and her team learned from these focus groups was not surprising, she said. Young people were confused about terminology, for example. They had a basic idea of what a premium is, but concepts such as deductibles, co-pays, co-insurance, networks, and out-of-pocket maximums were confusing. How to file claims, where to go to find care and cost comparisons, and the differences among providers were mysteries. “That was what we expected to hear, so that was not too alarming,” said Hemlin. What was surprising was the substantial lack of understanding about preventive care. To some, for example, preventive care was not consistently staying up late or eating the healthier options at a fast food restaurant. Similarly, many young adults had no idea about the financial assistance that was available.

One finding from the focus groups was that the term “free preventive care” does not resonate with young adults, but when they were given examples of what preventive care is, they saw the value and were excited they could access these services for free. Another lesson was that many young adults believe the doctor’s office is a place for treatment, not prevention, and that doctors do not have the time to explain prevention. Hemlin recounted that one young woman said a doctor will suggest losing weight, but not offer any ideas on how to do so. “Education goes both ways and there is work to be done on the provider side as well when talking about health literacy,” said Hemlin. “It is going to take work from both consumers and the health care system to build a culture of wellness.”

Once the focus groups were complete, Young Invincibles created a workshop-based health insurance literacy curriculum that it has been running for several months. These workshops explain health insurance basics and terminology, how to select a doctor from a plan’s provider directory and make an appointment, what is free and not free under the provisions of a health plan, and how to choose a plan on one’s own. In addition, the workshops offer healthy living tips. While the workshops do use some PowerPoints, they try to be as interactive as possible by using a fictional

character that goes through all types of health care scenarios. There is also a free Young Invincibles mobile app, HealthYI, that includes much of the information presented in the workshops, including a glossary of terms, an FAQ, a health checklist, and the ability to ask a question from a health care expert. The app also incorporates the ZocDoc mobile app that allows users to find a doctor and schedule appointments.

COMPARING PLAN INFORMATION3

Consumers’ Checkbook is a nonprofit organization that for more than 40 years has been producing websites and publications rating all kinds of services, including doctors, hospitals, and auto and homeowners’ insurance. Most relevant to this conversation, said Robert Krughoff, is the organization’s research and user feedback associated with the Guide to Health Plans that it has published for the past 36 years for the eight million employees and retirees covered by the more than 250 plans in the Federal Employees Health Benefits Program. In addition, Consumers’ Checkbook has built and hosted plan comparison tools to serve consumers choosing insurance on exchanges serving five states.

Noting that he and his colleagues have written and spoken widely on the features needed in a good plan comparison tool, Krughoff then listed the key features of a good tool. These include the following:

- Total Cost: A single dollar-amount actuarial estimate of average total cost (premium plus out of pocket) for people like the user in terms of age, family size, health status, and possibly other characteristics

- Risk of High Cost: The total cost a user might experience in a very high-expense year and the likelihood someone like the user will have such a year

- Doctors in Plan: An all-plan provider directory that lets the user immediately see for each plan whether it has doctors the user wants without having to find and dig into each plan’s directory and that also lets the user see overall measures of each plan’s network depth to provide a sense of availability of providers that a user cannot anticipate needing

- Plan Quality Comparison: A summary rating of each plan’s care and service quality, allowing the user to drill down for details and

___________________

3 This section is based on the presentation by Robert Krughoff, president of the Center for the Study of Services at Consumers’ Checkbook, and the statements have not been endorsed or verified by the National Academies of Sciences, Engineering, and Medicine.

personalize the summary score according to what quality dimensions matter most to the user

Comparing cost is a big challenge, said Krughoff, because having a list of deductibles, co-pays, and out-of-pocket limits is not enough. Even health care experts, he said, cannot on their own figure out whether a plan with a $200 deductible and $10,000 out-of-pocket limit is a better choice for themselves than a plan with a $1,000 deductible and a $4,000 out-of-pocket limit, and that is before adding in co-pays and co-insurance. The so-called known-usage model allows users to compare plans by asking how many doctor visits, prescriptions, and other expenses they expect over the next year. However, it ignores the very expensive and unexpected heart attack, auto accident, or other medical emergency, so it is not sufficient for plan-comparing costs.

The model that Consumers’ Checkbook has used for the past 36 years calculates for each plan a single-dollar-amount actuarial estimate of average total out-of-pocket costs for someone like the user, explained Krughoff, who added that the Medicare Plan Finder tool released a few years ago adopted a similar model. “We use population data on health care usage and expenses for tens of thousands of consumers from the Medical Expenditure Panel Survey database and from some other sources to do this,” said Krughoff. “We run those different probabilities and different profiles of use against the benefit package of each plan and come up with a weighted average for somebody like you.”

Some tools, he noted, make simplifications that are not helpful and in some cases are misleading. For example, during the first two open enrollment periods, the federally facilitated marketplace sorted plans on the basis of premiums, implying this was the right basis for choosing a plan. However, said Krughoff, there are numerous cases where families could save thousands of dollars by choosing a plan with a higher premium but lower deductible, lower co-insurance, and lower out-of-pocket costs of other kinds. In the same way, sorting plans solely based on deductible, whether they are bronze-, silver-, or gold-level plans, and other shortcuts can be equally wasteful, he said.

Another problem with some tools used during the first 2 years of the ACA, Krughoff said, is that they employed filters, such as filtering out plans that do not include specific doctors, plans the user would actually prefer, without the user knowing it. Allowing only a few standardized plan models, the approach that California has used, may restrict choice and innovation while not eliminating the need to compare plans across these models, said Krughoff.

During the initial open enrollment periods, Healthcare.gov and most state marketplace websites were unhelpful. They lacked the key features

that Consumers’ Checkbook had been recommending for years, so, at a substantial unreimbursed cost, Consumers’ Checkbook established and hosted its own tool as a model in Illinois, said Krughoff. That tool, he said, won the Robert Wood Johnson Foundation’s Plan Choice Challenge Award. Since then, the features that Consumers’ Checkbook and others such as Consumer Reports have recommended have been picked up by various exchanges.

Nonetheless, more change is needed, he said. The Healthcare.gov marketplace website, for example, has a new total cost estimate feature, but it is not clear whether it allows sufficiently for accidents and unanticipated health problems. It also does not let the user compare total costs between a normal year and a high-cost year, and it does not allow the user to see a large number of plans on the same screen, forcing users to remember or write down the information on each plan in order to compare multiple plans. “You should be able to go through those choices very quickly, and if a comparison tool is done right, you can,” said Krughoff.

The Healthcare.gov version for most states will not include quality measures this coming year, although that is in the works, he said. Healthcare.gov will allow the user to see if specific doctors are in each plan, but there is no measure of overall network breadth for each plan that would give the user a sense of provider availability for an unanticipated need.

Consumers’ Checkbook has also created a video tour within its comparison tool to help users learn how to use the tool, and the tool is designed to be used without knowing much about insurance, which Krughoff said is a big deal. “People do not want to spend a lot of time knowing about insurance,” he said. “You want to find a way to figure out the most important things to show people, to make sure they see those things and understand those things.”

The Consumers’ Checkbook tool has users input their age and the age of all family members, their overall self-reported health status, major procedures they know they may need, and financial information related to eligibility for Medicaid, the Children’s Health Insurance Program, subsidies, and tax credits. Users can input the names of a few physicians if that matters to them. The tool then prepares a list of plans available in the user’s location based on zip code. For each plan, the tool includes the estimated average total cost, including premium and out-of-pocket costs, for someone like the user in both a “normal” year and a high health care usage year, quality measures, and whether the user’s desired doctors are in each plan. It also creates a bar graph for each plan showing what percentage of doctors whose offices are near the user’s home are in the plan. At every step of the process, short videos are available to provide an explanation if needed.

The quality measure, Krughoff explained in closing, uses the overall rating by surveyed members as a default. However, there is a personaliza-

tion feature that allows the user to explore other aspects of quality, and to personalize the overall quality ratings based on the specific dimensions of quality that matter most to the user.

HUMAN-CENTERED DESIGN TO PRODUCE A READABLE MEDICAL BILL4

“I am a designer and a self-proclaimed health insurance nerd,” said Cueva. “I think we have an important opportunity to impact the lives of many people and that drives the work we do at Mad*Pow.” Mad*Pow’s purpose, she explained, is to help improve health, help people achieve financial well-being, and help them learn and connect. Its human-centered design process, which focuses on building empathy for the people it serves, involves all stakeholders in qualitative research and ethnography to gain a better understanding of their real needs and wants and what drives meaning and value in the context of their actual lives. “With the information we get out of research, we get the inspiration to then envision a better experience for them,” said Cueva. “We are envisioning that experience delivered through every touch point they may have throughout an experience or in terms of their interaction with the organization.” That interaction, she added, can be person to person, in the physical environment, and via digital email, text, print, and all other media for communication.

Mad*Pow’s research process related to health dives into behavior change and how to leverage technology, motivational psychology, game mechanics, behavioral economics, and anything else she and her colleagues can access to help people achieve the healthy behaviors that they want to achieve, explained Cueva. Along with trying to induce behavior change in people, Mad*Pow is also looking at transforming the health care system. “How do we help health organizations form and grow their innovation practices?” she asked. “How do we apply the design process to designing the organization so that we are able to design and deliver improved experiences?”

Seven years ago, Cueva’s interest in health led to Mad*Pow founding the HxRefactored conference to explore the overlap of health and design and address the challenge of using human-centered design to help improve health experiences. This annual conference, held in Boston, attracts some 500 people to explore the relationship between design and topics such as health literacy, behavior change, and health insurance. In the spring of 2016, Mad*Pow launched the Center for Health Experience Design to serve

___________________

4 This section is based on the presentation by Amy Cueva, co-founder and chief experience officer of Mad*Pow, and the statements have not been endorsed or verified by the National Academies of Sciences, Engineering, and Medicine.

as a resource, including providing training and coaching, to the health care industry for human-centered design. The other purpose of the center is to serve as a conduit for collaboration among organizations across the health care ecosystem who are serving the same patient populations. The hypothesis here, she said, is that working and aligning forces could accomplish more for these populations in terms of improving the health care experience. Currently, the center is organizing design projects in mental health and addiction recovery, clinician burnout, prevention, and chronic disease reversal. “We are looking at envisioning health experiences for the future and creating a culture of health,” said Cueva.

As an aside, Cueva mentioned that many organizations are starting to realize the value of design. She cited a study from the Design Management Institute showing that the stock market performance of organizations that had demonstrated a commitment to design exceeded those that did not by 228 percent over 10 years. “This is not just fluff. It is good business and can be meaningful on the nonprofit and government levels as well,” said Cueva. She also noted that organizations tend to follow a pattern where they first think of design as “hitting it with the pretty stick”—focusing on esthetics and branding only, then turning to what she called stick designs—ones that hit people over the head with a lack of subtlety, and then come to understand that good design creates intuitive experiences that enable users to accomplish what they want easily, then very mature organizations ultimately end up fostering a culture where the people they serve are at the focus of the design.

In all of her experiences working with a variety of organizations, she has found that the eventual experience is a by-product of how an organization is set up internally to deliver that experience. “If it is a mess of silos and there is zero collaboration, the experience is going to be affected,” said Cueva. She sees this in health care, where patients are largely left on their own to figure out how to navigate through this complex ecosystem. “What we are trying to do is piece things together for them, working collaboratively across the ecosystem under the premise that shared values and shared action will equal shared profit, both financial and social,” said Cueva. She noted that companies in the health ecosystem are waking up to the notion that what is good for the people they serve is actually good for their business. “Increased satisfaction is going to lead to increased retention,” she explained. She also said that many of the health-related organizations Mad*Pow works with, including health insurance companies, are wanting to become a better partner in health for the people they serve.

Some of the projects she and her team have worked on include decision support and maternity care. Mad*Pow is working with a major pharmacy chain to use the pharmacy as an important touch point to help people navigate the health care enterprise, and it is working with the Centers for

Disease Control and Prevention on HIV medication adherence and how to help patients with HIV track adherence and improve it. They are also working on a project for a leading insurance company to build digital health coaches that their clients can access on their smartphones to help them identify the healthy behaviors they want to work toward and help them achieve their goals.

A website that Mad*Pow designed, WelcometoAetna.com, introduces new members coming from insurance marketplaces to some key health concepts, insurance language, and resources they will need to understand their insurance. Her team is also working with community health plans on member billing to help reduce frustration and help people resolve billing questions.

From thousands of interviews with patients, consumers, and health insurance clients, Cueva has identified a few common themes with regard to consumer expectations:

- Give me access to the best options to keep me healthy.

- Save me money without sacrificing quality.

- Make things easy to understand. Answer my questions easily.

- Be easy to do business with; do the work for me.

- If there is something I should know, tell me proactively.

- Keep up with my expectations for experience excellence.

Health insurance companies struggle with many of these, she said, particularly in comparison to the experiences consumers have with companies such as Amazon or others that have invested heavily in good, consumer-oriented design.

Currently, Cueva and her colleagues are working with HHS and Health 2.0 to meet one aspect of Secretary Burwell’s challenge to improve patient experiences by redesigning the medical bill that patients receive. “One of the primary frustration points for patients is the state of medical bills,” said Cueva. “For one episode of care they are receiving multiple bills from the physician group, from the ambulance, from the emergency department. They do not know why they are receiving multiple bills and they do not know if their insurance company has paid a claim yet.” In addition, patients receive an Explanation of Benefits that is just as confusing. “If somebody is dealing with a chronic condition or serious episode, this can increase their anxiety, which can have detrimental health effects, as we know,” she added.

Confusion about medical bills also arises when people do not understand their health insurance plan and receive bills for more money than expected. Deductibles seem to be a particular problem. “Deductibles are a fantasy until you get the bill in the mail,” said Cueva. “That is when they become real, and that is when some people will avoid getting care along

their treatment path going forward if they cannot deal with the bills they already have.”

The Secretary’s challenge, co-sponsored by AARP, was launched at the Datapalooza event on May 9, 2016, and will close on August 10, she said. Two winners will be announced5 at the 10th Annual Health 2.0 Fall Conference in September 2016 and awarded cash prizes of up to $10,000. As of the time of this workshop, Mad*Pow had received more than 400 preapplications from teams around the country who expressed their intent to submit entries. “We are going to get a lot of participation and we cannot wait to see the results,” said Cueva.

Many factors contribute to the problem patients are having, she explained. One is the bill itself. She noted there are federal guidelines for what should be on a credit card bill, but no guidelines for what information should be on a medical bill. As a result, medical bills are filled with jargon that patients cannot understand and are missing key information that would help them understand. Another factor is the lack of understanding about insurance. The medical billing experience, said Cueva, starts with plan selection and moves into estimating cost of care. She commented that anyone who has ever been at a hospital or doctor’s office and asked how much a visit or procedure is going to cost knows the standard response. “They look at you like you are from another planet,” she said.

Referring to the contest, Cueva said that one grand prize will be awarded for a redesigned medical bill, and the other will go to a more disruptive innovation approach to transforming the medical billing process. An example of the latter solution, one she made a point of noting that she is neither for nor against, is that a patient could go to the health insurance company website, plug in the procedure needed, get the price, and prepay for the procedure. In such a model, there would be no bill at all, though a risk-averse health organization might be challenged by such a process, she said.

Criteria for judging the entries will be how well information and data are being used. Usability and understandability will be important criteria. So, too, will evidence that a human-centered design process was used to develop the solution, that is, did the designers involve the people who will be affected by the solution in the creation of the solution? Going into the contest, both Mad*Pow and HHS wanted to make sure the patient voice was represented in any solution. To help the contestants, Mad*Pow conducted a survey and qualitative interviews with patients, insurance compa-

___________________

5 The winners of the “A Bill You Can Understand” design and innovation challenge are as follows. RadNet won Prize 1: Easiest Bill to Understand. Sequence won Prize 2: Transformational Approach to redesigning the billing process. Winning designs can be viewed at www.abillyoucanunderstand.com (accessed January 31, 2017).

nies, and health care systems to create a research report identifying the top problems and how people feel about medical bills and billing (Mad*Pow, 2016).

Another important judging criterion is whether the solutions were market ready. HHS, she explained, has lined up five pilot partners—Cambia Health Solutions, Geisinger, Integris, MetroHealth, and University of Utah Health Care—to take the outcomes of the challenge and implement them in whole or in part. In fact, she said, one of these systems has launched an initiative to redesign its medical bill. In that respect, she said, the challenge has already succeeded in stimulating innovation.

Turning back to the research report, Cueva cited verbatim some comments from consumers:

- “The system is too complicated for me to change.”

- “Our system is completely insane and I hope it collapses soon. A new more sensible system might arise from the ashes.”

- “No one could tell me what the procedure would cost. Zero transparency.”

- “I finally gave up and paid the bills, still not knowing what they were for.”

- “I contacted both the provider and insurer to tell them about an error, which took 2 months to resolve. I should charge for my time.”

- “Patients don’t want separate bills from the hospital, nursing, doctors. We want one statement that shows everything we owe for that service.”

Of the patients responding to the survey, 52 percent did not do anything prior to their health care visit to research the cost of their impending care, and 61 percent rated their medical bills as confusing or very confusing. In addition, 46 percent said their actions did not clear their frustration with their bill, and 56 percent were hesitant about seeking additional medical care after their experience with medical bills. The research also identified the seven top concerns of patients:

- Patients do not know what they do not know

- Volume of communication

- Understandability

- Terminology

- Timing

- Financial planning

- Trust

NOTE: FSA = flexible spending account.

SOURCE: Presentation by Cueva, July 21, 2016.

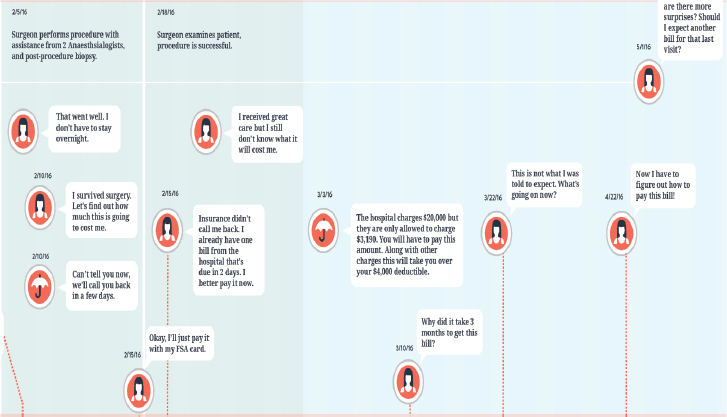

In addition to the research report, contestants received a diagram of the medical billing ecosystem and some examples of bills and benefit statements. Mad*Pow also mapped the patient journey to show how patients flow through this ecosystem (see Figure 5-2) and provided that map to contestants, too, along with some design guidelines and published literature on human-centered design and health literacy. In closing, she said she hoped she could address the roundtable again after the outcomes from this challenge have been announced.

LIBRARIES AND LIBRARIANS AS TRUSTED ACA INFORMATION SOURCES6

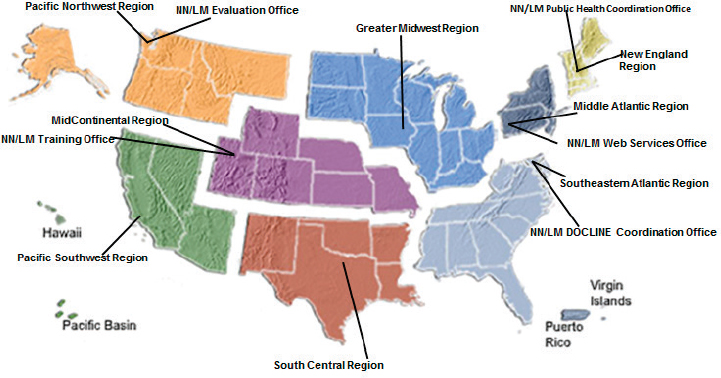

Beginning the final presentation of this session, Renée Bougard gave an overview of the National Network of Libraries of Medicine (NN/LM), an organization of more than 6,400 members that is administered by eight regional academic health sciences libraries (see Figure 5-3) under a cooperative agreement with the National Library of Medicine, a part of NIH. The

___________________

6 This section is based on the presentation by Renée Bougard, a project scientist in the National Network Coordinating Office at the National Library of Medicine, and the statements have not been endorsed or verified by the National Academies of Sciences, Engineering, and Medicine.

SOURCE: Presentation by Bougard, July 21, 2016.

NN/LM includes libraries at academic health sciences centers, hospitals, universities, and community colleges, as well as community- and faith-based organizations that provide health information to consumers. The mission of the NN/LM, said Bougard, is to provide access to health information for all health professionals in the United States, as well as the public, to enable them to make informed decisions about their health. “What we really do is provide access through outreach and training, ensuring that everyone in the United States has access to quality health information,” she said. “The NN/LM mission and work I will describe today support the National Library of Medicine’s goal of ‘Trusted Information Services that Promote Health Literacy and the Reduction of Health Disparities Worldwide.’”

Eight Regional Medical Libraries administerthe NN/LM:

- University of Pittsburgh Health Sciences Library, Middle Atlantic Region

- University of Maryland Health Sciences and Human Services Library in Baltimore, Southeastern Atlantic Region

- University of Iowa Health Sciences Library in Iowa City, Greater Midwest Region

- University of Utah Health Sciences Library in Salt Lake City, Mid-Continental Region

- University of North Texas Health Sciences Library in Fort Worth, South Central Region

- University of Washington Health Sciences Library in Seattle, Pacific Northwest Region

- University of California at Los Angeles Biomedical Library in Los Angeles, Pacific Southwest Region

- University of Massachusetts Health Sciences Library in Worcester, New England Region

In addition to administering the Regional Medical Library program, each of the Regional Medical Libraries supports sharing, curating, and annotating biomedical big data, said Bougard. As part of the outreach mission, each Regional Medical Library develops programs and services to make quality health information available and accessible to health professionals, the public health workforce, and the public within its Region. She explained that this is accomplished through grants to Network members to support training and exhibits at health fairs and conferences. There are also five national offices that coordinate evaluation, training, and information access for state public health departments.

A 2011 Institute of Museum and Library Services study (Swan et al., 2014) found that an estimated 37 percent of library computer users, or approximately 28 million people each year, use computers in public libraries and seek assistance from public librarians for information on medical conditions, finding health care providers, and wellness, said Bougard. “Public libraries are present in almost every community and in general are perceived as trustworthy and helpful,” said Bougard. She added that, as providers of Internet access for people who lack Internet connections at home, it was reasonable to anticipate that individuals would turn to public libraries for information on obtaining health insurance at the start of the open enrollment in October 2013. In some cases, said Bougard, public librarians even became navigators.

When the ACA was signed into law, a national collaboration involving CMS, the Institute of Museum and Library Services, NN/LM, and WebJunction, an online community that supports learning and training for library staff, created online resources and community contacts that library staffs would need to respond to questions regarding health insurance options and health-related questions. A panel session with representatives from the four collaborators was held at the American Library Association conference in June 2013. A breakout session was also held, in anticipation of the October launch of the ACA marketplaces, so that these representatives could meet with librarians to find out what tools and information they would need in order to answer questions from the public regarding enrollment.

CMS and the Institute of Museum and Library Services led the collaboration. CMS developed materials and training for health navigators,

as well as enrollment information for the public that would appear on Healthcare.gov. WebJunction developed a Health Happens in Libraries webinar series and also rebroadcast the American Library Association panel session in July 2013 for all U.S. libraries. WebJunction continued to host ACA-related webinars and developed information for public libraries on how they could prepare to meet the community needs regarding the ACA, explained Bougard.

NN/LM has a history of collaborating with public libraries and community-based organizations to provide access to quality health information for the public and of promoting health literacy, Bougard noted. The eight Regional Medical Libraries contacted each one of the state libraries in their region to offer training to public libraries on ACA materials and to work with them to train library staff on locating quality health information. Among the resources they focused on were the National Library of Medicine’s MedlinePlus and NIH’s SeniorHealth websites. In addition, each of the Regional Medical Libraries developed a webpage linking users to ACA information, including state-specific information, and many Regional Medical Libraries held webinars for their Network members to update them on the latest ACA information available. The webinars were open to all interested parties, but they were specifically geared toward the public libraries, said Bougard.

She then described a few examples of the projects and activities that came out of these efforts to promote the ACA with the help of the nation’s libraries (Collins, 2015):

- The University of Iowa Library held 12 sessions of a course—Public Library Reference and the Affordable Care Act: Helping Your Patrons Navigate the ACA—designed to familiarize public librarians in surrounding counties with what was happening with ACA and NLM resources.

- The California Library and the Pacific Southwest Regional Medical Library collaborated on a toolkit for public librarians throughout California entitled Finding Health and Wellness at the Library: A Consumer Health Toolkit for Library Staff.

- The East Brunswick, New Jersey, Public Library participated in a segment on a local cable television program to promote how the library was supporting the ACA. Some 8,000 people viewed that broadcast.

- The University of Pittsburgh Health Sciences Library partnered with the Upstate Health Sciences Library in Syracuse to offer a symposium for librarians: The Affordable Care Act: Access to Care—Libraries Making a Difference.

- The Gallatin County Detention Center in Bozeman, Montana, received funding from the Pacific Northwest Regional Medical Library to promote health insurance and enrollment literacy with inmates so that when they were released from the jail they could obtain health insurance.

In closing, Bougard said that libraries have a role in promoting the ACA. “They have provided the public with information needed to obtain health insurance, and in some cases they have provided the technological means for obtaining health insurance. They have also provided access to quality health information for those individuals who have come to the library seeking information regarding health care issues.” She encouraged anyone seeking a potential partner for outreach and education to consider contacting his or her Regional Medical Library for assistance and engaging his or her local public library.

DISCUSSION

Winston Wong opened the discussion session by asking if the nation is trying to sell the same product to the young invincibles and the “old and decrepit.” “If we are, that might be a losing proposition,” said Wong. He wondered if there had been any intentional thinking about the vernacular that resonates with those who have remained on the sidelines and have not yet signed up for health insurance. “For example, when we are talking to a group of people who are sitting on the sidelines, is it more attractive to talk about group purchasing or crowd sourcing as a way to frame the question of why insurance as a national imperative is important to spread risk?” Cueva responded by acknowledging the importance of that question and said that messaging comes down to understanding what will resonate with the focus population and customizing the experience based on the understanding. “In order to design for all, we can come up with a very homogenized experience, and there is risk in that,” said Cueva.

Krughoff also agreed with Wong’s comment and said, “There is not going to be one answer for everybody either in terms of what we say, how we say it, or how we reach people, how we get their attention.” There are, however, core ideas and concepts that everyone wants to understand, such as cost and provider availability, and the challenge is making those resonate as real using the appropriate message and medium for reaching specific demographics.

Cindy Brach asked Taylor if there were any health literacy recommendations or implications in the information she collected for meeting with patient navigators. Taylor replied that she believes the majority of the challenges in this area are rooted in health literacy in terms of what is

identified at the local level. For example, consumers receive letters rejecting their application for coverage through the marketplace because they have not submitted the correct documentation or information about income or immigration status, but these letters may not give enough information to the consumer to correct any omissions. “We are hearing that that is a problem across the country because the notices are the same from the marketplace,” said Taylor. “Those are the types of things that we send back up to HHS.” She added that this is completely a health literacy problem, and she and her colleagues are flagging those parts of the document that are not clear and understandable by the average consumer. In response, HHS has been making changes to these documents since the start of the first open enrollment period in 2013, a response that Taylor applauded.

Linda Harris from HHS wanted to add some behind-the-scene details to the medical bill challenge Cueva described. An HHS working group on health literacy put together criteria for the challenge, she said, and the working group screened the entries reducing the 400 applicants to the smaller number that the judges will be reviewing. Cueva added there were as many as 30 organizations, including Community Catalyst, that contributed to creating the challenge.

Michael Paasche-Orlow said he had found in some usability studies he has conducted that 40 percent of the people seen at his clinic do not know how to use a computer mouse. “We are not on the same page at all when we think about the user interface that is needed and the creative possibilities that need to be brought into that space where it is actually intuitive for the people,” he said. As an example, he said he has been using avatars as one approach to usability, and some people come in and wave to the avatar and expect that to trigger a response from the computer. He has concluded that designers need to rethink what is intuitive. Cueva replied that the key to universal design is to design for extremes. “If we design for extremes—the family that has 16 children and the person who lives on an island and has to take a boat everywhere we will make things better for everybody,” she said.

Ruth Parker asked Krughoff, who had noted that he addressed the roundtable 3 years earlier, how much progress had been made on incorporating the four key components of a good comparison tool into the tools available for consumers. Krughoff replied that there has been some progress on all four components. The federally facilitated marketplace tool, for example, now has a total cost figure that the consumer can use, though it is not an automatic calculation. “How good that cost figure is and how much it relates to your particular circumstance is not there yet, but at least it is on the table with regard to the provider directory,” said Krughoff.

Eric Ellsworth from Consumers’ Checkbook added that the data that inform marketplace provider directories have some problems with accuracy, which he said reflects the fact that much of the information is still designed

to flow between the provider and insurer rather than between the provider and consumer. “A potent example of this is that you cannot identify your plan in a unique way like you can with the serial number on your TV,” said Ellsworth. The result, he said, is that when consumers go to ZocDoc to find out if a provider is in their network, they have to first know which plan version they have. “The fact that Healthcare.gov forced the release of provider directories was a profoundly positive step in that it changed people’s expectations,” said Ellsworth. “They really started thinking that they should be able to look up a doctor. Hopefully that will continue.” He added that progress is also needed when it comes to formulary listings, where, again consumers need to know exactly which version of a drug they take.

Jay Duhig from AbbVie Inc. asked Cueva if there were plans to compile lessons learned from the 400 entries in the competition and to use some of them as examples of how human-centered design works. Cueva responded that the plan is to publish patterns and findings gleaned from reviewing all 400 entries. One thing she would like to do is pull together information and resources on how to design the best plan selection tool. “What would the best experience be like or what are all the available resources?” she asked. She did note that there are many different types of designs. One, called research-inspired design, first asks people what they want and need and then translates that information into a design. Another form of design is called genius design, which is what Steve Jobs did at Apple with the iPhone. “If you ask somebody if they need their entire music collection in their pocket, they would look at you like you were crazy,” she said, yet that was what Jobs envisioned. “The winning entry may have been inspired by research to come up with a genius approach, or they may have very meticulously figured out what different folks need, found the patterns, and gone from there.”