5

National Competitiveness

There is now a clear understanding, particularly among countries in the Organization for Economic Cooperation and Development1 (OECD) and the so-called developing countries, that science and technology (S&T) buttressed by innovation (STI) are essential pillars of economic growth, and that advanced materials are a critical one of these pillars. Sanford L. Moskowitz, in his book Advanced Materials Innovation, Managing Global Technology in the 21st Century,2 estimates that over three-quarters of all economic growth by 2030 to 2050 will be attributable to the development and application of advanced materials and that investments in materials research (MR) are tied directly to national competitiveness and economic prosperity. He also argues that never has the potential of MR seemed so important and crucial to human existence as it does for the 21st century, and he then explores the key questions that determine whether or not an MR invention becomes a robust market technology. Speed of innovation and commercialization are identified as key current issues facing MR, brought about by narrating stories of important 20th and 21st century innovations based on MR. In his book, he projects the impact of advanced material from 1980 to 2050 for information and computer technology, energy, biotechnology and health care, transportation, construction and infrastructure, and manufacturing.

___________________

1 An intergovernmental economic organization with 36 member countries, founded in 1961 to stimulate economic progress and world trade.

2 See S.L. Moskowitz, 2016, Advanced Materials Innovation: Managing Global Technology in the 21st Century, Wiley, https://www.wiley.com.

As can be understood from his book, MR is a critical underpinning to economic growth as well as national competitiveness, wealth and trade, health and well-being, and national defense. The impacts that MR has had on emerging technologies, national needs, and science have been important to date, and they are expected to become even more critical as researchers move through the digital and information age and face current and future global challenges. Many of the world’s larger nations and economies have recognized this relationship, and recent trends show that today many nations have developed and articulated national investment strategies to ensure robust progress in MR for national competitiveness in a global economy. In some cases, these national strategies target specific national needs, and are internal to the nation; in others, collaborations have begun to be included in the investment tactics.

5.1 AMOUNTS AND DIRECTIONS

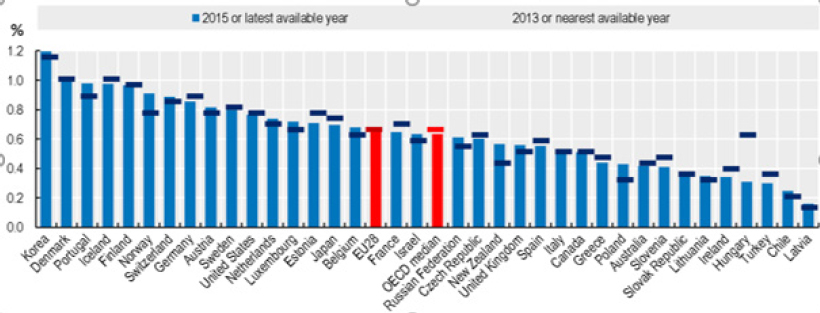

Given the economic importance of materials science, most advanced and developing nations have instituted national strategies for MR and for bringing its findings to the marketplace as rapidly as possible. Experience has taught us that fundamental research is an essential component of innovations that eventually spawn new industries and feed economic growth, so most national strategies seek to articulate and support research programs that run from fundamental to applied. Data about investments in materials science specifically are hard to obtain, but there are comprehensive sets of data about overall investments in S&T, which MR should follow at least approximately. Figure 5.1 shows overall government budget appropriations and outlays for research and development (R&D) for 2013 and 2015.

Here are some general trends:3

- Overall R&D capability (original wording in the OECD report is capacity, which in French is often translated as “capability”) in the world has doubled in the past 15 years, with an increasing share of the growth attributable to increased business expenditures.

- Several emerging economies, China’s in particular, have significantly increased R&D spending.

- Overall spending on publicly funded R&D (i.e., not including private and industrial R&D) shows a convergence toward 0.4 percent to 0.9 percent of Gross Domestic Product (GDP). Data in the report from OECD4 shows Korea in the lead, with government R&D spending of 1.2 percent of GDP

___________________

3 Organisation for Economic Co-operation and Development, OECD Science, Technology, and Innovation Outlook 2016, http://www.oecd.org/sti/.

4 Ibid.

in 2013-2015, and the United States as number 11 at about 0.8 percent. It should be noted that more than half of the U.S. government-supported R&D is defense related. U.S. spending is down from about 1 percent of GDP in 2008 and 2011. This decrease is, however, balanced by an increase in private investment. In 2015, the total R&D budget of the United States was $495 billion, about 67 percent provided by industry and 24 percent by the federal government (the rest by nonfederal government, higher education, and nonprofit organizations), and the total budget for basic research was $83 billion, about 44 percent provided by the federal government and 27 percent by industry.5 In 2009, China, with the second largest science base in the world, spent about $154 billion gross (government and industry) on R&D, less than the European Union (EU; $298 billion) and the United States ($408 billion) and slightly more than Japan ($154 billion).6 By 2015, China’s expenditures expanded to $409 billion, while that of the United States increased to only $496.6 billion and those of the EU and Japan increased to $386 billion and $170 billion, respectively.7

___________________

5 National Science Foundation, 2018, NSF Science and Engineering Indicators 2018, https://www.nsf.gov/statistics/2018/nsb20181/.

6 National Science Foundation, 2012, NSF Science and Engineering Indicators 2012, Arlington, Va.

7 National Science Foundation, 2018, NSF Science and Engineering Indicators 2018, https://www.nsf.gov/statistics/2018/nsb20181/.

- There is a general shift in research policy agendas toward environmental and societal challenges (e.g., the EU Horizon 2020 framework program), in particular achieving sustainable growth. This shift, however, is unlikely to displace the long-standing emphasis on public science’s contributions to national competitiveness. Nevertheless, the trend over the next 15 years is toward a greater emphasis on support for thematic, mission-oriented research, and it is likely that universities will play a greater role in this kind of research.

- There is an increasing emphasis on interdisciplinary research, such as synthetic biology and neuroscience.

- Strengthening of public research infrastructure, which has benefited most from international cooperation, is among the top STI priorities in the majority of countries.

- Innovation has become a more significant imperative in policy development.

- Many governments have shifted or plan to shift attention and support away from public research toward business innovation and entrepreneurship

5.2 A GLOBAL PERSPECTIVE

MR and innovation in materials science and engineering are now a worldwide enterprise that are essential to both the word economy and to that of individual regions and countries. In general, the world benefits from this globalization in which important new ideas come from small countries (e.g., Skype from Estonia8) as well as larger ones. Aware that fostering innovation and technological advance in materials science and engineering increases the probability of thriving in this global environment, individual countries and the EU have developed programs and institutions to support materials research and development. In planning U.S. support for MR in the future, it is useful to know what other countries are doing to assess our relative strengths, weaknesses, and gaps, to identify possible areas for collaboration, and to learn from policy innovations of others. This section provides an overview of MR policies and planning in a representative group of countries and the EU.

There have been a number of assessments of future trends in STI that identify transformative technologies. An OECD report synthesizes the reports from

___________________

8 Skype was founded in 2003 by Niklas Zennström, from Sweden, and Janus Friis, from Denmark. The Skype software was created by Estonians Ahti Heinla, Priit Kasesalu, and Jaan Tallinn. The first public beta version was released on August 29, 2003.

Canada,9 the EU,10 Germany,11 the United Kingdom,12 the Russian Federation,13 and Finland.14 The report lists 10 cutting-edge technologies; among them are the Internet of Things (IoT), artificial intelligence (AI), neurotechnologies, nano/microsatellites, additive manufacturing (AM), advanced energy storage, synthetic biology, and blockchain. At least six of these have substantial materials science component. The original country reports often featured materials science more explicitly (e.g., Canada—nanotechnology and materials science; EU—physical science and manufacturing enabling technologies; United Kingdom—advanced materials).

What follows provides more in-depth overviews of materials science and engineering in representative European (Finland, France, Germany, and the United Kingdom) and Asian (China, Japan, and Korea) countries and the EU (which has agencies and resources separate from those of its member states). A broad and well-established trend emerges: the mature Western countries and Japan are seeing their share of the world’s economies diminish and that of most Asian countries increase. This has caused the former to reassess their strategies for supporting materials science, tying those strategies more closely to economic development and stressing the importance of rapid conversion of knowledge into innovation. There is a clear realization that economic competition among nations will only increase in an extremely dynamic and unstable geopolitical climate. Although India is not included in this study, it is noteworthy that India’s 2018 investment in materials has increased.15

Information that was readily available to the committee varied widely in content and format from country to country (the EU can be viewed as a “country” for the current purposes), and it proved, given the committee’s time constraints,

___________________

9 See Government of Canada, “Policy Horizons,” https://horizons.gc.ca/en/home/, accessed January 7, 2018.

10 European Commission, 2015, Preparing the Commission for Future Opportunities: Foresight Network Fiches 2030: Working Document, http://globaltrends.thedialogue.org/publication/preparing-the-commission-for-future-opportunities-foresight-network-fiches-2030/.

11 A. Zweck, D. Holtmannspötter, M. Braun, K. Cuhls, M. Hirt, and S. Kimpeler, 2015, Forschungsund Technologieperspektiven 2030: Ergebnisband 2 zur Suchphase von BMBF-Foresight Zyklus II, https://www.vditz.de/fileadmin/media/VDI_Band_101_C1.pdf.

12 U.K. Government Office for Science, 2012, Technology and Innovation Futures: UK Growth Opportunities for the 2020s—2012 Refresh, https://www.gov.uk/government/collections/foresight-projects.

13 A. Sokolov and A. Chulok, 2012, Russian Science and Technology Foresight—2030: Key features and first results, Foresight and STI Governance (Foresight-Russia till No. 3/2015) 6(1):12-25.

14 R. Linturi, O. Kuusi, and T. Ahlqvist, 2014, 100 Opportunities for Finland and the world: Radical Technology Inquirer (RTI) for anticipation/evaluation of technological breakthroughs (English edition), Publication of the Committee for the Future, Parliament of Finland 11:2014.

15 See K.V. Venkatasubramanian, 2018, “India’s Science and Technology Funding Raised Marginally: Proposed Budget Emphasizes Information Technology and Health Care Instead of Basic Science,” Chemical and Engineering News, February 6, https://cen.acs.org/articles/96/web/2018/02/Indias-science-technology-funding-raised.html.

unrealistic to provide a common and uniform format for each of the country sections below. These sections do, however, strive to provide a reliable picture of national planning and priorities for MR in each of the selected countries.

5.2.1 European Union

The EU provides support for individual researchers, multimember consortia, and European science and engineering infrastructure. Its support is in general separate from that provided by individual European countries, whose programs are treated independently in this report. The EU prepares in-depth reports on S&T around the world and on strategies for their development among its member nations. Advanced materials is one of the key enabling technologies identified by the European Commission. Together with advanced manufacturing, it underpins almost all other key enabling and industrial technologies.16 The Materials Science and Engineering (MS&E) Expert Committee (MatSEEC) identified the need and value of knowledge and technology transfer in MS&E in Europe. In July 2017, the European Commission published a summary17 of 11 recommendations based on results of the interim evaluation of Horizon 2020 and other documents and reports: “Our main message, and vision, is that investing in research and innovation is increasingly crucial for shaping a better European future in a rapidly globalizing world, where success depends ever more on the production and conversion of knowledge into innovation.” Major initiatives include EuMaT—European Platform for Advanced Engineering Materials and Technologies—and ESF—the European Science Foundation. EuMat covers all elements of the life cycle of an industrial product, from design, development, raw materials, processing, qualification, and eventually decommissioning.

EuMaT’s primary objective is to “produce the Strategic Research Agenda that, with appropriate involvement of industry and other main stakeholders, will provide bases” for identification of needs and establishment of priorities in the area of advanced materials and technologies.18 The latest version of this report is the 2017 third edition.

___________________

16 European Commission, 2011, High-Level Expert Group on Key Enabling Technologies: Final Report, June, http://ec.europa.eu/DocsRoom/documents/11283/attachments/1/translations/en/renditions/native.

17 European Commission, 2017, LAB-FAB-APP: Investing in the European Future We Want: Report of the Independent High Level Group on Maximising the Impact of EU Research & Innovation Pro-grammes, http://ec.europa.eu/research/evaluations/pdf/archive/other_reports_studies_and_documents/hlg_2017_report.pdf.

18 Quote from the EuMat website at http://www.eumat.eu.

- It seeks to promote the development of new materials technology that enables the design, production, and use of innovative products with enhanced performance and new functions. Other targets are to protect the environment, to capture existing knowledge, to train future professionals, and to acquire capability and capacity to develop new generation of materials.

- It identifies eight critical focus areas, each with defined working groups: (1) modeling and multiscale; (2) materials for energy; (3) nanomaterials and nanostructured materials for functional and multifunctional applications; (4) knowledge-based structural and functional materials; (5) life cycle, impacts, and risks; (6) materials for information and communication technologies; (7) biomaterials; and (8) raw materials. Each has defined R&D priorities for 10- to 15-year horizons.

- Its overall policy is directed toward the achievement and maintenance of leadership and global competitiveness in advanced engineering materials. EuMaT works with other major organizations via collaboration and networking with the main European organization in this space such as the European Materials Research Society, the Federation of European Materials Societies, and the European Materials Forum. Involvement of industry is through participation in the governing boards. The Alliance for Materials (A4M) was created to ensure a value chain approach to improve speed of implementation of innovations in Europe that address grand societal challenges. It intends to be a single platform for all relevant initiatives, but not an overall structure to merge the R&D community; it is enabling versus controlling.

In ESF, MatSEEC is an independent science-based committee of more than 20 experts active in materials science and its applications, materials engineering and technologies, and related fields of science and research management. Committee members are nominated by their member institutions, and they maintain strong links with their nominating organizations and their respective scientific communities. The aim of MatSEEC is to enhance the visibility and value of materials science and engineering in Europe, help define new strategic goals, and evaluate options and perspectives covering all aspects of the field.19

The EU’s most recent centralized investment for future technology including MR is Horizon 2020, which is reported to be the largest EU program ever in research and innovation spanning nearly €80 billion over 7 years (2014 to 2020). The investment recognizes that additional private investment will be attracted by the program, which targets taking great ideas from the lab to the market. Economic

___________________

19 See Earth & Space Research, “Oceanographic Research,” http://www.esr.org, accessed August 2, 2018.

growth and job creation is one of the key goals, and emphasis is on science excellence, industrial leadership, and tackling societal challenges. The program is structured to reduce red tape and response time to enable more rapid investments and results. Horizon 2020 is the financial instrument implementing the Innovation Union, a Europe 2020 flagship initiative aimed at securing Europe’s global competitiveness.

5.2.2 Finland

Finland is a small country, but it strives to create a knowledge-based future, and its planning has some interesting twists. The Academy of Finland, part of the Finnish Ministry of Education, Science and Culture, is the primary agency for funding research. Its Strategic Research Council funds research that has societal impact. Centers of excellence have been funded since 1995. TEKES is Finland’s funding agency for innovation, and it works directly with EU’s Horizon 2020 program.

A focus of government funding is basic and applied research that has global impact, with an emphasis on science with societal impact. Overarching decisions guide national funding for research. The theme in 2017 was “Changing Society and Citizenship in a State of Global Flux” and for 2018 “Reform or Wither—Resources and Solutions.” The cross-thematic focus areas for both years are information in decision making and execution, and sustainable growth in society.20

The Strategic Government Program of the Prime Minister, which was launched in 2015, is based on five strategic priorities: (1) employment and competitiveness; (2) knowledge and education; (3) well-being and health care; (4) bioeconomy and clean technologies; and (5) digitalization, experimentation, and deregulation. Specific focus areas in MR include adaptation and resilience for sustainable growth, keys to sustainable growth, nanoscience and nanotechnology, and energy-related science.

Of note are Finland’s international interactions. The Academy of Finland engages in global cooperation with research funding agencies; it organized joint calls together with Brazil (Sao Paolo Research Foundation) on MR and with India (Department of Science and Technology) on energy research, and it is active in the Joint Committees of the Nordic Research Councils. It also encourages submission of proposals from international scientists on competitive grants, as long as they have a Finnish host and collaborator.

___________________

20 See Finnish Government, 2016, “The Government Adopted Strategic Research Themes for 2017-2018,” press release, October 6, https://valtioneuvosto.fi/en/article/-/asset_publisher/10616/valtioneuvosto-paatti-teemat-strategiselle-tutkimukselle-vuosiksi-2017-2018.

5.2.3 France

The primary institution for the support of fundamental materials research in France is the CNRS (Centre National de la Recherche Scientifique), with a total budget of 3.30 billion euros in 2016, through its Chemistry, Engineering Sciences, and Physics divisions. The CEA (French Alternative Energies and Atomic Energy Commission) through its Renewable Energies sector also provides some support. The bulk of the CNRS support goes to university research departments, whereas that of CEA is concentrated in centralized research establishments like the Saclay Nuclear Research Center.

France’s government promotes innovation for overall growth through its STI policy. In 2013, France launched the Innovation 2030 Commission21 to identify the major challenges the world will face in 2030 and key areas with significant implications for the French economy. The commission identified six pillars to put France on the road to long-term prosperity and employment: (1) energy storage, (2) recycling of metals, (3) development of marine resources, (4) plant proteins and plant chemistry, (5) personalized medicine, and (6) the silver economy—innovation in the service of longevity.

France also leverages cluster strategies, and it established the European Cluster Collaboration Platform22 (EMC2) in 2005 as an industrial cluster on advanced manufacturing that is motivated by investment in innovation as a key part of economic prosperity. Although the focus is manufacturing, materials and new materials are included, as is processing. A unique feature is an integration across market segments—aeronautics, naval, ground transportation, and energy—and a focus on creating synergies between members for research. EMC2 activities are enhanced by the infrared thermography Jules Verne.23 Funding is both public and private. EMC2 leads a network of small business enterprises and major industrial groups focusing on the key markets and technologies: aeronautics, automotive, energy, environment and green technologies, maritime, materials, metal processing and manufacturing, production technology, railway, and transport infrastructure. In 2016, its total budget for R&D was 1.4 billion euros, of which 523 million euros were public funds.24

___________________

21 See Direction Générale des Entreprises, “The Innovation 2030 Commission,” updated July 30, 2013, https://www.entreprises.gouv.fr/innovation-2030/the-innovation-2030-commission?language=en-gb.

22 European Union, “EMC2: European Cluster Collaboration Platform,” https://www.clustercollaboration.eu/cluster-organisations/emc2, accessed November 21, 2018.

23 French Institutes of Technology, “Institute of Shared Technology Research,” https://www.irt-julesverne.fr/, accessed November 21, 2018.

24 European Union, “EMC2: European Cluster Collaboration Platform,” https://www.clustercollaboration.eu/cluster-organisations/emc2, accessed November 21, 2018.

5.2.4 Germany

Germany’s investment in MR comes from two major programs: the German Ministry of Research (BMBF), “From Materials to Innovation,” and the German Research Foundation, “Materials Science.” In 2006, the German government created a plan called High-Tech Strategy25 whose focus evolves over time; while initially attending to the market potential of specific technology areas, it later concentrated on society’s need to develop and implement forward-looking approaches to policies (2010) and more recently on “civil society” alongside industry and research, and a number of new topics in which MR can be found (such as the digital economy and society, a sustainable economy and energy system, the innovative workplace and civil security). As part of this plan, Germany increased R&D expenditures from 8.5 billion euros in 2000 to 14 billion euros in 2013.

Federal investments employ a variety of strategies and initiatives aimed at ensuring Germany has the scientific, technological, and economical foundation to meet future challenges. A current focus is on new instruments to fund innovation; strengthen cooperation between enterprises, universities, and research institutions; and enhance society’s active involvement in STI.

Germany’s foundation of unique funding models is well established and has benefited their country’s MR. There is a high level of coordination of R&D across organizations and industry; academies play an active role. Continuous research support of academics is a part of faculty appointments, which enables strong research programs. Funding models address specific niches spanning basic through applied research. The Max Planck Society is world renowned, and its support complements research projects at universities. The Helmholtz Institutes focus on supporting large facilities (€3 million to €6 million annually per institute with federal support). The Fraunhofer Institutes, the largest umbrella organization for applied research in Europe, conducts applied research for both private and public enterprises, as well as for the general benefit of the public. The Fraunhofer Institutes are unique in that they conduct research under contract for industry, the service sector, and public administration in addition to offering information and services. The MP326 is noted as one of the most famous inventions coming from the institutes. Their ability to bridge the so-called valley of death27 by bringing industry needs to research projects has been recognized in key MR arenas such as manufacturing automation. The Leibniz Association connects independent research institutes that address issues of international societal importance, spanning the humanities and

___________________

25 HTS—Hightech-Strategie.

26 MP3 is an audio coding format for digital audio. Originally defined as the audio format of the MPEG-1 standard.

27 “Valley of death” is a slang phrase used in venture capital to refer to the period of time from when a start-up firm receives an initial capital contribution to when it begins generating revenues.

social sciences and economics through spatial and life sciences to mathematics, natural sciences, engineering, and environmental research. The German Federation of Industrial Research Associations promotes R&D on behalf of small and medium-size enterprises (SMEs). The association, active at the national and the European level, is organized by industry and increases the competitive strength of SMEs by supporting the application of R&D. German states (Länder) and municipalities also fund and operate research institutes that support state research activities; advances in photovoltaics, renewable fuels, battery technology, and fuel cells are an example of MR benefiting from such an investment (Centre for Solar Energy and Hydrogen Research Baden-Württemberg).

Germany is responsible for introducing the concept of Industry 4.0,28 often referred to as the Fourth Industrial Revolution, which follows the first steamhydropower, the second electrical, and the third IT revolutions. Industry 4.0 envisions Cyber-Physical Systems comprised of “smart machines, storage systems, and production facilities capable of autonomously exchanging information, triggering actions and controlling each other independently,” designed to impart “a new level of organization and control of the entire value chain” to include custody over the full product life cycle.29 This vision, related to the IoT, although in its infancy is believed by many to be the future of manufacturing, and it is being promoted by the industrial world and, in particular, by China. It is not surprising that AM is considered a part of the Fourth Industrial Revolution.

5.2.5 United Kingdom

The United Kingdom’s centralized investment in MR has been shaped by its potential exit from the EU. The major government funding agencies for MR include the Engineering and Physical Sciences Research Council, Ministry of Defense: Materials and Structures Technology, and the recent Innovate UK: Manufacturing and Materials.

The United Kingdom’s industrial strategy is based on four pillars: clean growth, AI and data economy, future of mobility, and aging society. A specific goal is to raise the R&D investment from 1.7 percent to 2.4 percent of GDP by 2027. A focus on MR is within the pillars, especially evident in the clean growth pillar section—efficient

___________________

28 Communication Promoters Group of the Industry-Science Research Alliance and the National Academy of Science and Engineering, 2013, Securing the Future of German Manufacturing Industry: Recommendations for Implementing the Strategic Initiative INDUSTRIE 4.0: Final Report of the Industrie 4.0 Working Group, Secretariat of the Platform Industrie 4.0, Frankfurt, Germany, April.

29 U. Eul, Fraunhofer IMWS, “Materials Data Space—Werkstoffstrategie für Industrie 4.0 Eine Initiative des Fraunhofer-Verbundes MATERIALS - Werkstoffe/Bauteile,” presentation, April 26, 2017, https://www.materials.fraunhofer.de/content/dam/materials/dokumente/MDS/EuL%20-%20Materals%20Data%20Space%20Initiative%20HMI%202017_UE.pdf.

new materials, which states “use of renewable biological resources to produce food, materials and energy.” Noteworthy in the UK strategy is focus on regional research clusters, including materials-related themes: Manchester—advanced materials; Liverpool—materials chemistry. Unique factors for UK MR include a government-established Advanced Materials Leadership Council to advise on where investments have greatest impact. A Materials Exchange Research Forum operated by EPSCR is a platform for coordinating research.

In November 2015, the Knowledge Transfer Network of the United Kingdom published a thorough review, “Survey of Market Needs and Growth Potential: Advanced Materials Study,” that both identifies important materials areas for future growth and the resources and weakness of the United Kingdom in the areas in question. The five priority areas identified in the survey are (1) materials for transport, (2) materials for health care, (3) materials for energy, (4) materials for ICT, and (5) materials for demanding environments. For each of these areas, the survey discusses specific material needs, UK capacity to develop and exploit relevant technologies; immediate, medium-term, and longer-term trends and drivers; gaps in the UK industrial capacity; market growth opportunities; R&D/support infrastructure; international relationships; and global market trends.

5.2.6 China

China’s “Made in China 2025” is an industrial master plan, based on the “Industry 4.0” concept introduced in Germany, to make China an industrial superpower in the coming decades. Among its goals are a comprehensive upgrade of manufacturing in China to be innovation-driven, more efficient and integrated, emphasize quality over quantity, and raise the domestic content of core components of and materials to 40 percent by 2020 and to 70 percent by 2025. It highlights 10 priority sectors: (1) new information technology, (2) automated machine tools and robotics, (3) aerospace and aeronautical equipment, (4) maritime equipment and high-tech shipping, (5) modern rails transport equipment, (6) new-energy vehicles and equipment, (7) power equipment, (8) agricultural equipment, (9) new materials, and (10) biopharma and advanced products.30

Although “materials” appear explicitly only in item (9), materials will play an important role in many of the other items, especially if the stated goals of domestic content are reached. There is little doubt that this program has the potential to change the world landscape of industrial and thus materials production and substantially increase competition with current leaders in manufacturing.

___________________

30 M. Kuo, 2017, “What Is Your State’s China Strategy?,” RealClear World, May 8, https://www.realclearworld.com/articles/2017/05/08/what_is_your_states_china_strategy.html.

Current plans, extending to 2020, call for China to pay more attention to the basic research in materials science, the exploration in the frontier areas, and to multidisciplinary research on national economic, social, and technological development and major needs. The Ministry of Science and Technology has allocated about 19 billion yuan ($3 billion) in 2016-2020 in areas of strategic electronic materials, key basic materials, biomedical materials and tissue replacement, nanometer science, additive manufacturing and laser manufacturing, and material genetic engineering. The National Natural Science Foundation of China plans to support about 4 billion yuan ($640 million) in this time period, across metal materials, inorganic nonmetallic materials, and organic polymer materials, including biomedical polymer materials. Much of the funding is aligned to investment in student programs.

China’s centralized investment in MR focuses on projects that advance the economy and achieve independence from foreign suppliers. Specific areas of investment include aircraft engines, structural materials, electronic materials, energy materials, biomaterials, transportation, and quantum materials.

MR is strongly funded by the Ministry of Science and Technology, National Science Foundation of China, local and industrial sources, and sources focused on facilities for characterization and advanced manufacturing. The National Outline for Medium-and-Long-Term Scientific and Technological Development (2006-2020), released in 2006, identifies major special projects involving strategically important products, critical common technologies, and major engineering projects in line with national objectives. Projects are designed to enable scientific and technological progress, leapfrog developments in overall productivity, and address China’s strategic gaps.

Of note is the dramatic and effective return on centralized investment in China. Substantial government funding in MR has resulted in recruitment of talented researchers from around the world. Materials science papers from Chinese researchers tripled between 2006 and 2015. One in every 10 papers in 2015 was in materials science.31

Over the past decade, China has built an impressive array of advanced state-of-the-art measurement facilities, including three synchrotrons (NSRL-Hefei, BSRF-Beijing, and SSRF-Shanghai), an advanced research neutron reactor (CARR-Beijing), and a spallation neutron source (CSNS-Dongwan, Guangdong). In addition, the Chinese government, through the National Development and Reform Commission and Ministry of Science and Technology, has approved the plan to establish three comprehensive National Science Centers. These “Science Cities” are the Beijing Huairo Center, the Shanghai International Science and Technology Innovation Center at Zhangjiang, and the Hefei Comprehensive National Science Center. It has just been announced that there will be a fourth Comprehensive

___________________

31 P. Tian, 2017, China’s blue-chip future, Nature 545:S54-S57.

National Science Center at Xi’an. The Beijing Center at Huairou ($1.5 billion) “will focus on areas of great advantages (to China), including materials science, space science, atmospheric environmental science, earth science, information and intelligence and life science.” The new “Science City” is located on a 3,000-acre plot donated by the city government. There will be a new Beijing Advanced Photon Source, a Synergetic Extreme Condition User Facility, the Earth System Simulator (to be started in 2018 or 2019), and the extreme condition platform. The Chinese Academy is organizing several other platforms; among them, the Institute of Physics leads the construction of materials genome (40,000 m2) and lithium-ion battery (80,000 m2) platforms. Beijing City funds all the constructions and instruments for these two platforms, ~ 0.9 billion CNY (~130 million USD), so these two platforms will be operational next year. The materials genome platform is composed of three parts: material computations and data analyses, high-throughput syntheses and fast characterizations, and instruments R&D and technical support. Fifty new appointments will be made to staff the materials genome platform. The new campus of the University of the Chinese Academy of Sciences is located in the “educational zone” of the Huairou Science City.

5.2.7 South Korea

South Korea’s recent national investment in MR largely addresses commercialization. Its investment in scientific and technological R&D (government and private) for 2016 was sixth in the world (after the United States, China, Japan, Germany, and France) and one of the highest in the world in terms of percentage of GDP at 4.23 percent. In spite of its high investment in R&D, its return is low—with only a 20 percent rate of successful commercialization compared to about 70 percent for the United States and the United Kingdom and 54 percent for Japan. To address this gap, Korea has established a new “Government R&D Innovation Plan”32 to reform its R&D ecosystem so that “investments will lead to profit and business achievements.” Reorganization of R&D support systems to place greater emphasis on SMEs is part of the plan, as is the creation of a user-oriented optimal environment for research. MR will certainly benefit from this foundation.

Principal funding sources for science research in Korea include the National Research Council for Science and Technology (NST), which supports 25 Institutes, of which the following strongly support materials science: Korea Institute of Science and Technology (KIST), Korea Basic Science Institute (KBSI), Electronics and Telecommunications Research Institute, Korea Institute of Machinery and Materials

___________________

32 See Republic of Korea, Ministry of Science and ICT, “Government R&D Innovation Plan: Development of Korean Science and Technology”, http://english.msit.go.kr/cms/english/pl/policies2/__icsFiles/afieldfile/2015/11/11/Government%20RnD%20Innovation%20Plan.pdf, accessed July 9, 2018.

(KIMM), and Korea Institute of Materials Science (KIMS). Others government sources of MR funding may include the Ministries of Science, ICT and Future Planning; Trade, Industry, and Energy; National Defense; Environment; and Education.

Of note in the new plan is a clear division between the roles of the government and the private sector, with the government focusing on fundamental technologies and future growth drivers and the private sector focusing on commercialization. In addition, Korea plans to establish programs that will guarantee SMEs access to personnel and equipment in universities and government-backed research institutes (GBRIs) and will follow the effective German Fraunhofer model.

5.2.8 Japan

The Council for Science, Technology, and Innovation (CSTI) published Japan’s Fifth Basic Plan for Science and Technology (S&T).33 The ¥26 trillion (~230 billion USD), 5-year plan promotes a 10-year forward outlook focused on creating Society 5.0, also called the “Super Smart Society.” This concept is that of “a human-centered society that balances economic advancement with the resolution of social problems by a system that highly integrates cyberspace and physical space.” While the plan does not include R&D priorities at a detailed level, it outlines the ambition of the government to identify important broad research areas that will spur system innovation, raise Japan’s global position, and create enthusiasm among its aging citizenry.

A clear trend in the fifth plan, in relation to earlier plans, is the use of concepts such as “open science,” “networked science,” and “citizen science,” displaying an ambition by Japan to open up the country’s system for research and innovation. The plan recognizes that barriers for human resource mobility between universities and industry are hampering innovation and Japan’s global position. While promoting collaboration between universities and corporate researchers, the government has also set some aggressive goals for 2020: they place added emphasis on strategic intellectual property (IP) management and standardization, look to double the number of license agreements on university patents, and want to increase the rate of initial public offering (IPO) cases regarding venture companies. A clearly stated goal of the plan is to have government, academia, and industry work together to transform Japan into “the most innovation-friendly country in the world.”

Overall, the plan contains unusually sharp warnings that Japan is dropping in S&T competitiveness. This issue is addressed through improved political

___________________

33 See J. Iwamatsu, 2016, “The Japanese Science, Technology and Innovation Policy,” Bureau of Science, Technology and Innovation, Cabinet Office, Government of Japan, June 28, https://www.hrk.de/fileadmin/redaktion/hrk/02-Dokumente/02-07-Internationales/02-07-15-Asien/02-07-15-3-Japan/Iwamatsu_Cabinet_Office_Government_of_Japan_.pdf.

coordination between and within departments and research ministries, as well as a clearer focus on the basic components of the R&D-system that can drive Japan’s open innovation model. The plan contains a number of numerical goals related to research for the coming 5 years and identifies several technology areas, such as bio- and nanotechnology, the IoT, and AI as important multidisciplinary enablers.

In alignment with the basic policies spelled out by CSTI’s plan, 14 Japanese ministries set the policies, basic strategy, and budget allocations related to S&T. These include the well-known Ministry of Education, Culture, Sports, Science, and Technology (MEXT), as well as 12 others with a lower degree of immediate relevance to MR and innovation. Investment areas that have been called out as priorities include energy, next-generation infrastructures, local resources, and health and medical.

In addition to the national S&T initiatives and what has already been discussed here, CSTI has selected two organizations (SIP and IMPACT) to promote and drive specific elements of this multidisciplinary open collaboration. They have estimated operating budgets of ¥50 billion per year and ¥55 billion per year, respectively.

- SIP, or the cross-ministerial Strategic Innovation Promotion program, promotes focused, end-to-end R&D, from basic research to practical application and commercialization. It also provides an IP management system that will facilitate the strategic corporate use of research results from SIP programs. Program directors are selected by invitation from top-class leaders out of industry and academia and are asked to manage programs from a cross-ministerial perspective.

Of the 12 S&T themes SIP manages, the two largest with a strong grounding in MR and innovation are the Structural Materials for Innovation (SM4I) and Next-Generation Power Electronics programs. These programs are approximately ¥3.5 billion per year and ¥2.2 billion per year, respectively. SM4I looks to develop ultrastrong and ultralight heat-resistant materials for aviation, such as CFRPs, alloys, intermetallics, and ceramic-coatings, and accelerate their development and adoption through advanced computer science that correctly predicts complex material behavior. The Power Electronics program aims to use next-generation materials, such as silicon carbide and gallium nitride, to spread the adoption of improved electronics that result in a leap forward for energy management and efficiency.

- IMPACT, or Impulsing Paradigm Change Through Disruptive Technologies Program, looks to create disruptive innovations that revolutionize industries and society through high-risk/high-impact R&D. It is modeled after both the U.S. Defense Advanced Research Projects Agency model and Japanese FIRST (Funding Program for World-Leading Innovative R&D on Science and Technology) model. Armed with bold authority and budgets, IMPACT

program managers will set high targets for bringing about major changes to society and industry, will select research teams that provide optimum R&D capability, and will lead projects aimed at achieving disruptive innovation. IMPACT’s “theme 1,” a release from constraints on resources and innovation in “monozukuri (manufacturing)” capabilities, appears to have the tightest alignment to MR and innovation. It looks to achieve the low-cost production of high value-added materials and products through high-precision processing.

Drilling down to the next level of S&T impact and funding, Japan retains the globally renowned National Institute of Advanced Industrial Science and Technology (AIST), one of the largest public research organizations in Japan. AIST’s Electronics and Manufacturing Department (~16 percent with 320 researchers) explores nanoelectronics, photonics, advanced manufacturing, spintronics, flexible electronics, and ubiquitous microelectrical mechanical systems (MEMS) and microengineering. AIST’s Materials and Chemistry Department (~20 percent with 415 researchers) studies nanomaterials, carbon nanotube applications, and the computational design of advanced functional materials.

To promote closer collaborations between universities and industry as called out by the fifth plan, AIST has created and is growing two new collaboration strategies. For materials and chemistry, these include the following:

- The concept of an open innovation laboratory (or OIL), with a collaborative research base located on a university campus. For now, OPERANDO-OIL and Mathematics for Advanced Materials (MathAM-OIL) are in service. The latter is applying advanced simulation and an inverse-problem analysis to material development to rapidly derive a material’s structure based on its desired functions to expedite the material development cycle.

- Collaborative Research Laboratories (CRLs), bearing partner company names, to conduct R&D more closely related to the strategies of companies. For now, there are three in service related to materials, the Zeon-AIST Nanotube CRL, looking to accelerate the scaling of carbon nanotube production, the TEL—AIST CRL for advanced materials and processes for electronics and manufacturing, and the NGK Spark Plus-AIST CRL for health care materials.

Based on Japan’s fifth Basic Plan for S&T, AIST plans to establish more than 10 OILs by fiscal year 2020. It is reasonable to forecast that additional CRLs will be created as the new S&T strategy and funding from the fifth Basic Plan marry with the S&T interests of would-be Japanese industrial sponsors.

5.3 CASE STUDIES

A sense of the dynamical, international nature of MR can best be appreciated with the aid of case studies that show how important advances often begin with initial ideas being developed in one country, followed by necessary development in a second, and finally commercialized in a third. In the current state of rapid change with Industry 4.0 on the horizon, countries with relatively less developed MR experience can leapfrog past old techniques to world leadership in the new. This section will present brief case histories highlighting these trends.

5.3.1 Case 1—Flat Panel Liquid Crystal Displays

This is by now a fairly old story, played out over more than three decades, but it is illustrative of how the mélange of great creativity, unwillingness to abandon old ways, persistence, and missed opportunities determine the course of development of new products. Liquid crystals, which flow like a liquid yet exhibit anisotropy like a crystal, were first discovered by Fredrich Reintzer in 1888. Although E. Merck of Darmstadt sold liquid crystals for analytical purposes as early as 1907, they were far from the mainstream of scientific research, with only a few institutions studying them by 1960. In the early 1960s, RCA began a program to study liquid crystals with the eventual idea of developing a “hang-on-the-wall television.” Although it did not succeed in that, it did produce the first liquid crystal display (LCD) using a dynamical light scattering mode to turn pixels on and off. RCA, with strong investment in CRTs and “silicon,” abandoned any attempts to commercialize the technology and this effort was then taken up—and then also abandoned—by small U.S. start-ups. RCA was, however, inadvertently associated with the development of the twisted-nematic display that eventually led to today’s flat-screen displays. It was invented by an RCA employee, Wolfgang Helfrich, who left RCA to work for Hoffmann-La Roche in 1970, and almost simultaneously by James Fergason, then at the Liquid Crystal Institute at Kent State University in Ohio. Europe, particularly the United Kingdom, would get involved with the technology by creating new types of liquid crystal materials, which were stable at room temperature, in its chemical laboratories but it was Japan that eventually succeeded.

Companies such as Sharp had sent its engineers to the United States to learn all it could from RCA and other U.S. companies about the LCD. Japan succeeded in eventually commercializing the technology, in part, because of its business culture—based on the importance of cooperation between firms (the “Keiretsu” system) in contrast to the individualistic, highly competitive nature of U.S. business. The scaling up of the LCD to flat panel displays for computers and large-screen TVs was a very complex and very expensive process. U.S. companies large and small shied away from spending so much on such a risky proposition (their perceived risk

was high). In Japan, however, the government worked with different companies to create the flat panel display—this cooperative effort allowed capital and talent to be pooled in a way that could not be done in the United States. Moreover, companies in Japan tended to be large and diversified, and revenue streams from other commercial areas allowed these firms to work with other companies on this one project without having to worry about overall cash flow. Government aid also helped soften the blow (so here CEOs of Japanese companies had low perceived risk). By the first decade of the 21st century, Japan’s government and the constellation of companies that it coordinated on this national effort were able to show the world it could do what the mighty United States could not, succeed in commercializing these displays. Other Asian countries—especially South Korea—followed Japan’s lead, and together the region has become the world’s hub for flat panel display technology. In this way, Asia took a largely American invention and found a way to tap the commercial potential in it.34

Lessons from this example include the following: (1) breakthrough applications often require advances and new ideas in many different fields, (2) persistence and vision are often the determining factor in actually bringing a product to market, and (3) such persistence and vision often rest on a few individuals. In addition, the sequence of necessary advances often occurs in different countries. In the liquid crystal case, the idea of a flat display and how it would work was the first essential step, but that idea could not come to realization without the advances in chemistry that provided room-temperature-stable liquid crystals. Advances in semiconductor technology were the final essential ingredient for the successful development of the amazing displays we now take for granted.

5.3.2 Case 2—Additive Manufacturing in Aerospace

In the past 5 years, AM has in a sense come into its own in aerospace.35 The four major jet engine manufacturers, Rolls-Royce, Pratt and Whitney, General Electric, and Safran Aircraft Engines, have begun to produce aircraft engines with additive-manufactured components that reduce weight, number of parts, and development time. NASA in collaboration with Space-X is developing additive-manufactured rocket engines, and companies around the world are using AM to make reduced-weight plane seats, helicopter engines, and flying-car bodies. The manufacturers of aircraft engines had gained experience using AM to prototype

___________________

34 Based on communication with S.L. Moskowitz, author of Advanced Materials Innovation: Managing Global Technology in the 21st Century,” Wiley, 2016. See Chapters 11 and 12 for the case study of LCDs and flat panel displays.

35 National Research Council, 2014, Limited Affordable Low-Volume Manufacturing: Summary of a Workshop, The National Academies Press, Washington, D.C.

parts as far back as the late 1980s. The story of development of the leading-edge aviation propulsion (LEAP) engine by CFM, the joint GE Aviation- Safran Aircraft Engine, is documented in an online GE report.36 The CFM team designed a new engine that would dramatically reduce fuel consumption and emissions. Its design of fuel nozzles had an interior structure that was so complex that to make it would have required more than 20 parts that would have to be welded together, an almost impossible task. Mohammad Ehteshami, then head of engineering for GE Aviation, went to Morris Technologies, a local Cincinnati company that pioneered the use of metallic AM and that made prototypes for GE projects, to investigate whether it could use AM for mass production of a complex part. A nickel alloy prototype of the intricate nozzle tip exceeded all expectations: it combined all 20 parts into one and weighed 25 percent less than an ordinary nozzle and was more than five times as durable. GE Aviation acquired Morris Technologies in 2012, and in 2016 it spent more than $1 billion to buy controlling stakes in Sweden’s Arcam AB and Germany’s Concept Laser, two leading manufacturers of industrial 3D printers. In 2013, it also acquired the Italian firm Avio Aero, which now has one of the most advanced 3D manufacturing facilities in Europe, and it is already making parts for the TiAl turbine blades for the GE9X—the largest jet engine ever built. GE set up other AM factories in Auburn, Alabama, and established the Additive Training Center near Cincinnati and the Center for Additive Technologies Advancement near Pittsburgh.

There are several lessons to be learned from the development of AM as essential component of advanced manufacturing of complex parts: (1) At one level, this is a common story: a new idea often takes 30 or so years to mature, but when it does it can have a profound effect. (2) Access to advanced technology by large companies is more often than not obtained by the purchase of smaller and often more nimble companies. (3) Good ideas and international companies are not subject to national or geographic boundaries—a lesson that should be remembered as China works its way up the technological ladder.

5.3.3 Case 3—Permanent Magnets on the World Market

Permanent neodymium-iron (Nd2Fe14B) magnets are the strongest currently known, with extensive uses in motors, speakers, cell phones, wind turbines, hybrid cars—the list goes on. They were first discovered independently by different methods by General Motors in the United States and Sumitomo Special Metals (eventually acquired by Hitachi) in Japan in 1984 in response to increasing cost of

___________________

36 See T. Kellner, 2017, “An Epiphany of Disruption: GE Additive Chief Explains How 3D Printing Will Upend Manufacturing,” GE Reports, November 13, https://www.ge.com/reports/epiphany-disruption-ge-additive-chief-explains-3d-printing-will-upend-manufacturing/.

samarium in the then-standard SmCo magnet. The new material quickly became the industry standard, with dozens of firms engaged in its production. China has controlled production of rare-earth metals since at least the 1990s. By 2005 or so, because of strong demand and active enforcement of environmental policies, the price of rare earths increased considerably, putting pressure on both producers and purchasers of permanent magnets. The result was a shuttering of many producers and a flight of those who remained to Asia to be closer both to supplies and customers in the booming Asian economies. By 2008, there were no producers of Nd magnets in the United States. The situation was and continues to be complicated by litigation over patent violations (Hitachi, which holds most of the patents on Nd magnets, and Chinese firms) and imposition of unfair market barriers (Chinese firms against Hitachi) working through the U.S. court system.

The United States is, of course, aware of the magnet problem, and it would prefer not to have to rely so completely on a single technology or single material provider for something as increasingly important as permanent magnets. The Department of Energy (DOE) has in fact funded research on alternatives materials for magnets through a DOE Advanced Research Projects Agency-Energy (ARPA-E) program, but no viable replacement has been found. On the other hand, DOE-supported research on AM has developed a process that produces better magnet performance with less material (see Box 2.6).

The take-away from this case study is that forces beyond science and engineering often determine the fate of local commercialization of superior materials and their processing.

5.3.4 Case 4—Photovoltaics

Photovoltaics (PVs) are semiconductor materials37 that convert light (in particular from the sun) to electricity. They are becoming an increasingly important component of electric power grids around the world, with 302 gigawatts (GW—billion watts) of capacity in 2016 or about 1.3 to 1.8 percent of the world’s electric power consumption, and an exponential rate of increase over the period 1992 to 2017. The first patent for a solar cell was awarded to (Russel Ohl) Bell Laboratories in 1946, and the first practical crystalline solar cell was realized in 1954, again at Bell Labs. Crystalline (c-Si) and polycrystalline silicon (poly-Si) remain the dominant material for PV cells, with 95 percent of the market in 2013. There are, however, two PV materials, CdTe discovered at RCA in 195438 and Cu(InG)Se (CIGS) studied at

___________________

37 U.S. Department of Energy, National Renewable Energy Laboratory, “Solar Photovoltaic Technology Basics,” https://www.nrel.gov/research/re-photovoltaics.html, accessed September 24, 2018.

38 N.H.F. Beebe, 2018, “A Bibliography of Publications in Centaurus: An International Journal of the History of Science and its Cultural Aspects,” http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.464.3790&rep=rep1&type=pdf.

Boeing in the 1980s39 have found commercial application and show some promise for the future. Unlike silicon, CdTe and CIGS are prepared as thin films on a substrate. These three materials all have peak efficiencies above 20 percent.

From 1946 through 1997, the United States dominated both research in and applications of PVs. In 1977, President Jimmy Carter established what was to become the National Renewable Energy Laboratory (NREL) in Golden, Colorado, which, among other things, provides independent verification of efficiencies of solar cells. By the 1980s and through the 1990s, PVs found applications in off-the-grid standalone power systems and in consumer products like watches and calculators. By 1996, the United States had 77 MW of solar PV capacity, and focus had begun to shift to grid-connected rooftop systems.

In 1995, the city of Kobe in Japan experienced an earthquake that led to severe power outages that paralyzed the entire neighboring electrical infrastructure. PV systems provided temporary replacement power. In the same year, the experimental Monje Nuclear Power Plant developed a sodium leak that forced a shutdown and that led to massive public outrage. These two events led to Japan’s decision to invest heavily in PV power generation, and it quickly became a world leader, with 1.132 GW of PV capacity by 2004. Following its Renewable Energy Act of 2000, Germany displaced Japan as the world PV leader in 2005, a position it held until it was in turn displaced by China in 2015. China’s 5-year plan of 2015 set a goal of 100 GW of PV power by 2020, a goal that it exceeded in 2017, with a capacity of 131 GW.

Fluctuating national agendas and normal market fluctuations have created challenges for manufacturers of PVs, in many cases leaving them in bankruptcy. The 2000 decision of Germany to favor development of PV systems and the decision of China to begin investing in them and subsidizing their production led to an increase in demand for silicon by 75 percent. The result was a severe shortage in silicon and an increase in its price from $30/kg to $80/kg and even $400/kg for long-term contracts forcing the solar industry to idle about 25 percent of its cell and module manufacturing capacity. The polysilicon industry responded with technological improvements and investment in more capacity. The result was then overcapacity for silicon production and a drop in price to $15/kg, forcing some producers to suspend production or exit the sector. By 2013, the ratio of actual output of PV silicon to production capacity was still only at 63 percent. This overcapacity led to increasingly inexpensive exports from China to the United States, and then to U.S. allegations of Chinese dumping of solar products, followed by the imposition of tariffs in 2012 and to a similar move by the EU a year later. China responded with antidumping tariffs of 57 percent on U.S. polysilicon producers.

The story of thin film PVs provides a cautionary tale about commercialization

___________________

39 See R. Ellingson, “Photovoltaic Technology for CIGS and Related Materials,” http://astro1.panet.utoledo.edu/~relling2/teach/archives/6980.4400.2012/20120322_PHYS_6980_4400_CIGS.pdf, accessed April 25, 2019.

of high-tech materials. Solyndra, a company founded in 2005, developed a technology for solar panels in which thin CIGS films were rolled and encapsulated in specially designed cylinders allowing, it was argued, for the panels to absorb energy in all directions. By 2009, following a near high point in the price of polysilicon (~$400/kg in 2008), Solyndra posted a revenue of $100 million and the future, with a $535 million government loan40 under the American Recovery and Reinvestment Act, looked bright. But the future was planned without sufficient attention to increasing polysilicon production, which caused the price of polysilicon to fall to about $50/kg by the time the government loan was approved. Orders fell, and Solyndra declared bankruptcy in 2011, laying off 1,100 people.41 The story of Nanosolar, a company started in 2002, is similar. It developed a CIGS PV ink that it spread on a flexible substrate whereupon nanoparticles in the ink aligned under a self-assembly process. In December 2007, it started solar cell production in its San Jose factory, and by February 2012, it had reached a production capacity of 115 MW per year, but in the end its total actual production was only 50 MW.42 Like Solyndra, it went out of business (in 2013) because its product could not compete with cheaper silicon.

There are, of course, U.S. and U.S.-based international companies that have survived the feast-and-famine cycle of silicon availability and foreign competition. These include the following:

- SunPower (60 percent owned by Total S.A.)—crystalline Si technology and 2015 production capacity (mostly in the Philippines and Germany) of almost 400 MW/yr;

- First Solar—CdTe technology, with total installation of more than 17 GW of power worldwide and 2015 production capacity of 143 MW/year;

- Evergreen Solar—polycrystalline Si and 2015 production capacity of 103 MW/year; and

- Tesla Energy (merger SolarCity and Tesla), now a player with “Gigafactory 2” producing cells and panels in partnership with Panasonic in Buffalo.

The status of PV use and investment continues its state of competition and flux with the contested U.S. imposition in February 7, 2018, of 30 percent tariffs (to decrease to 15 percent by 2021) on c-Si PV cells and modules and the announcement

___________________

40 The loan was a political scandal for the Obama administration.

41Washington Post, 2011, “A History of Solyndra”, September 13, https://www.washingtonpost.com/politics/a-history-of-solyndra/2011/09/13/gIQA1r5qQK_story.html?noredirect=on&utm_term=.f4a99225064e.

42 Wesoff, Eric. “Nanosolar, thin-film solar hype firm, officially dead.” Greentech Media 12 (2013).

by China of a 12 to 15 percent cut in the Feed-in Tariff43 for projects installed after June 2018.

In spite of the complicated economics (and politics), PV electric power development will continue, and research will lead to improvements in efficiency and to new device structures. Research into CdTe and CIGS films continues; also, new perovskite and organic PV solar cells show considerable promise.

5.3.5 Case 5—LithiumIon Batteries

Lithium batteries were first proposed and realized by Stanley Whittingham while working for Exxon in the 1970s, although G.N. Lewis had initiated some explorations in the early 1900s. Lithium is the lightest of all metals, has the greatest electrochemical potential, and provides the largest specific energy per weight. With lithium metal as the anode, the safety issues owing to its reactivity and inherent instability were obvious, as were the problems associated with the formation of lithium dendrites, which grew with repeated cycling and short-circuited the batteries. Research shifted to nonmetallic materials using intercalated lithium ions. The final product, which is now called the Li-ion battery, has had a transformational impact on personal electronics and on personal mobility, affecting communication, computation, entertainment, information, transportation, and the fundamental ways in which people interact with one another and with information. The first successful Li-ion batteries were commercialized by Sony in 1991. Estimates in 2017 of the global market for Li-ion batteries are approximately $25 billion, with consumer electronics being the largest application, followed by automotive, industrial, and energy storage.44 Growth of 12 percent per year has been forecast.

Since the initial inventions, the energy density of Li-ion batteries has improved and continues to improve at a rate of 5-10 percent per year due directly to progressive improvements achieved through advanced materials science research, carried out across a broad spectrum of university, major industry, start-up company, and government national laboratories. The trajectory of key innovations to date is a fascinating sequence of both discovery and design.

Sony used a soft carbon host structure (coke) in the first commercial battery containing lithium at the anode instead of metallic lithium, although the quest for Li-metal anodes continues today owing to the higher energy density attainable. Thus, the initial concept of the Li-metal anode was ultimately abandoned for a soft-carbon intercalation anode, which was itself abandoned for a hard-carbon anode and then a graphite anode, the evolution based primarily on the interaction that

___________________

43 A mechanism to accelerate investment in renewable energy through long-term contracts.

44 See Global Market Insights, “Lithium Ion Battery Market Size By Components,” https://www.gminsights.com/industry-analysis/lithium-ion-battery-market, accessed April 25, 2019.

these carbon materials have with the organic liquid electrolyte that is the medium through which ions are transferred between electrodes during discharging and recharging. On the cathode side, much credit goes to Goodenough and co-workers for the development of a new class of cathode materials, layered transition-metal oxides, such as LixCoO2, first reported in 1980. In 1996, Goodenough and coworkers proposed LiFePO4 and other phospho-olivines (lithium metal phosphates with the same structure as mineral olivine) as positive electrode materials. In 2002, Yet-Ming Chiang and his group at the Massachusetts Institute of Technology showed a substantial improvement in the performance of Li-ion batteries, boosting the material’s conductivity by doping it with aluminum, niobium, and zirconium. In 2004, Chiang again increased performance by utilizing iron(III) phosphate particles of less than 100 nanometers in diameter. This decreased particle density almost 100-fold, increased the positive electrode’s surface area, and improved capacity and performance. Commercialization led to a rapid growth in the market for higher capacity Li-ion batteries. The Materials Genome Initiative has had a major impact in trying to develop ideas to go beyond Li-ion, such as the use of divalent ions that, all other things being equal (which they are not), would increase the energy density by a factor of 2. Likewise, silicon anodes are being actively explored for their greater lithium binding capacity than graphite. Yet another important area of materials development is in the electrolytes, particularly in the development of solid electrolytes that both eliminate flammable organic liquid electrolytes and provide a physical barrier to dendrite short-circuiting.

This steady progress in MR has led not only to steady improvement in performance, but also a steady decrease in costs of manufacturing. In 1994, the cost to manufacture Li-ion in the standard 18650 rechargeable cylindrical cell was more than $10 and the capacity was 1100 mA-h. In 2001, the price dropped to below $3, while the capacity rose to 1900 mA-h. Today, high-energy-density 18650 cells deliver more than 3000 mA-h, and the costs are dropping further. Cost reduction, increased specific energy, and the absence of toxic material paved the road to make Li-ion the universally accepted battery for portable applications, heavy industries, electric power trains, and satellites.45

5.4 SCIENCE DIPLOMACY WITH INDUSTRIAL AND HOMELAND SECURITY

The findings in this decadal survey stress the need for continued international collaboration—especially as facilities become larger, more complex, and expensive. The findings also point out the need for the United States to not lose its strength in

___________________

45 Case 5, adapted in part from G. Crabtree, E. Kocs, and L. Trahey, 2015, The energy-storage frontier: Lithium-ion batteries and beyond, MRS Bulletin 40:1067.

worldwide leadership in MR, because access to international facilities and front-line research findings would then become more challenging. These two findings are intimately related: The United States will lose its ability to be involved in front-line international collaborations if U.S. research erodes. The committee points out here that these international collaborations bring up an ever-rising challenge: How does the United States maintain international research while maintaining U.S. homeland and industrial security?

The committee has recently seen some of our governmental research laboratories prohibit its research employees from attending conferences in China and the U.S. Department of the Treasury forbidding attendance of U.S. researchers to a conference abroad.46 There are many additional examples of U.S. researchers being blocked from international travel, and it is also becoming increasingly challenging for foreign scientists to travel to the United States and for Chinese graduate students, in certain research areas, to obtain more than a 1-year student visa.47

Note that in the early 1960s, U.S. physicists went to visit their counterparts in the Soviet Union—and that was during the heart of the Cold War, with both sides being heavily armed in nuclear weapons. These interactions played a formative role in substantially changing and growing theoretical condensed matter physics. During all of these interactions, continuing into the late 1980s, scientists were not only carefully watched but also remained vigilant in sharing only the most basic of their physics to move the fields forward, together.

Ceasing international collaborations will put the United States at a great disadvantage for MR, from the most fundamental to the most applied industrial research. In the past, scientists knew how to write papers, discuss research, and present talks; sharing what needed to be shared, while keeping any sensitive materials confidential. But times have changed—and cyber security has raised new challenges. In this new age, using one’s laptop or phone, or even checking e-mail, are possible security risks while traveling internationally; and there is a need to be mindful of international visitors to the United States. These new challenges also apply to industrial security within the United States.

5.5 A NATIONAL PERSPECTIVE

There was a time when R&D programs in the United States could be planned and carried out without regard to programs in other countries. That has not been the case for some time now, and today many of the MR programs in the rest of the

___________________

46 W.E. Pickett and L.H. Greene, 2018, “Hard Line on Sanctions Harms Science Diplomacy,” APS News, March, Volume 27, Number 3.

47 J. Mervis, 2018, “More Restrictive U.S. Policy on Chinese Graduate Student Visas Raises Alarm,” ScienceMag.org, June 11, doi:10.1126/science.aau4407.

world are already competitive with those of the United States or on their way to being so. This competition has been highlighted in the five case studies above that act as snapshots highlighting the issue. Most of the OECD and developing countries have specific plans to modify and upgrade their MR investments and planning, usually with an eye to economic competitiveness. China has the most aggressive program, Made in China 2025, which seeks to transform that country into a high-tech powerhouse that dominates industries like robotics, advanced information technology, aviation, and new energy vehicles. In this context, it can be argued that all MR in the United States should be viewed through the lens of the conflict between seeking mutual benefit through international sharing and cooperation on the one hand and maintaining or improving U.S. leadership positions on the other. Indeed, several findings of previous sections mention the need for action to maintain U.S. leadership.

Regarding cooperation, there is one area (in addition to climate change) for which there is a desperate need for international cooperation, and that is in problems related to the life cycle of materials. Most of the country reports in this section include some plans to study and confront these problems, and one might expect that international cooperation would be welcome. The problems of uncontrolled disposal of modern materials affect the whole planet. Plastic bottles and bags, and the nanoscale particles that they break into, cover vast swaths of the oceans and are eaten by unsuspecting birds and fish, whose veins become clogged with nanoparticles.

5.6 FINDINGS AND RECOMMENDATIONS

Key Finding: Intense competition among developed and developing nations for leadership in the modern economic drivers, including smart manufacturing and materials science, will grow over the coming decade.

Key Recommendation: The U.S. government, with input from all agencies supporting materials research, should take coordinated steps beginning in 2020 to fully assess the threat of increased worldwide competition to its leadership in materials science and in advanced and smart manufacturing. The assessment program, which should be established on a permanent basis, should also define a strategy by 2022 to combat this threat.

Recommendation: Given that this competition is and will be a reality for the foreseeable future, the U.S. government, with input from all agencies supporting materials research, should take coordinated steps beginning in 2022 to define our priorities in materials science and engineering to continue

highquality research, facilitate economic development, and protect our intellectual property.

Finding: Countries across the globe have understood that materials science drives national economies, that competition to produce high-end products is ever increasing, and that only those countries that invest in materials research and development infrastructure will remain competitive in the world economy.

Recommendation: The U.S. government should fund and pursue a strategybased permanent program of robust investment focused on materials science and smart manufacturing that will allow us to maintain our position as a world leader in materials science and not to fall behind our many competitors.

Finding: International scientific collaboration and science diplomacy is vital to U.S. success in fundamental and applied materials research. In some cases, scientists are forbidden to travel between countries. While many U.S. researchers understand how to protect sensitive material, with the increasing prevalence of cyber espionage, this understanding needs to be updated.

Recommendation: In order to maintain international collaborations, the United States must allocate funds to develop methods to educate our researchers on how to be vigilant in maintaining security both while traveling abroad and when welcoming international colleagues to the United States. Such education would also be crucial for maintaining industrial security within the United States.

This page intentionally left blank.