PANEL III

STATE AND REGIONAL INITIATIVES

Moderator:

Ed Paisley

Center for American Progress

Clusters Growing in Pennsylvania

Rebecca Bagley Pennsylvania Department of Community and Economic Development

The mission statement for the Technology Investment Office (TIO) in Pennsylvania, she said, did not use “innovation” in its title. Instead, its objective is “to serve as a catalyst for growth and competitiveness for Pennsylvania companies and universities through technology-based economic development initiatives, including funding, partnerships, and support services.” Its customers include pre-revenue, emerging, and mature companies, as well as universities, community organizations, and investment partners. “We collaborate with everyone,” she said. The TIO, she said, does not just manage grants, but takes “an extremely active role. Really, the goal is collaboration, and clusters are just what we fund, supporting companies at every stage.”

She said there were four pillars of technology-based economic development: innovation, capital, workforce, and support services. But the ideas that fuel innovation, she said, can come from the private sector, state government, or the federal government.

Primary Industry Clusters

The primary industry clusters supported by the TIO are biosciences, nanotechnology, manufacturing (including seven centers of the Manufacturing Extension Program), alternative energy, and telecom/information technology. “I sort of joke that this is everything we can find,” she said. “Collaboration and those four pillars bring these clusters together.” Alternative energy was especially strong, she said, since the state had recently set aside $650 million, which could now be used to match stimulus money. In the biosciences, the state had strength in large pharmaceutical companies (including two of the top 10 NIH grant recipients). But it did not have venture capital or seed-stage

activity, so the TIO used tobacco settlement money to create three life sciences “greenhouses” across the state. These are designed to find and develop technologies from universities and to invest in VC funds, of which there are now 32 in their portfolio. This allows the state government to brand the region, she said, and address the biotech sector with one cohesive voice. It also allowed the TIO to see what resources the region had, where the gaps were, and how they could be filled.

She described technology investment as a process with five stages:

- Concept: The idea for the company is hatched.

- Formation: The company begins to establish itself and its product, hiring employees and winning customers.

- Growth: the company grows with increased pace.

- Maturity: The company has an established customer base and flattening growth.

- Reinvention: The company takes action to seek new market opportunities.

She summarized the many programs supported by the state, saying that the objective common to all of them was “articulating to people what we do.” Returning to the biosciences, she noted that the federal role could be especially important, since six of the largest pharmaceutical companies in world are located within 50 miles of Philadelphia. “But some are in New Jersey and Delaware,” she said. “So if federal programs can fund innovation by region, we can have a really robust cluster.” The same would be true for the area between Pittsburgh and Cleveland. “But this is tough for states to do,” she said, “because we can’t spend taxpayer money outside our borders.”

Gaining and Losing Momentum

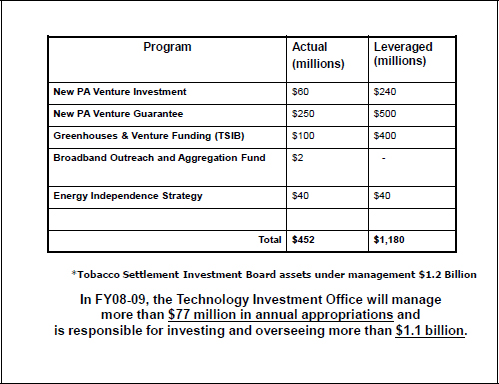

She said that the TIO had raised a total of $452 million in actual funding, which had been leveraged to a total of $1.18 billion. The TIO in FY2008-2009 had managed more than $77 million in annual appropriations and was responsible for investing and overseeing more than $1.1 billion. Now, she said, that process was losing momentum in the recession, with the Senate contemplating a budget cut of 60 percent. “We had gained a lot of momentum over last eight to 10 years,” she said “but now we may lose a lot from lack of funding.”

Another successful cluster, she said was the Pennsylvania energy cluster. Governor Rendell and the legislature had taken steps before the recession to invest nearly $915 million to spur the alternative energy economy. Funds distributed since 2003 and new legislation, such as the Alternative Energy Investment Fund, she said, would ensure that the commonwealth would be a national leader in this emerging sector for years to come. Since 2003, state investments in this sector had funded 564 projects that had created and retained more than 8,300 jobs.

FIGURE 2 Technology investment: Funds under management.

SOURCE: Rebecca Bagley, Presentation at June 3, 2009, National Academies Symposium on “Growing Innovation Clusters for American Prosperity.”

Fortunate Timing for Job Creation

The state had also created an Alternative Energy Investment Fund, enacted in July 2008 for infrastructure that was needed to support the energy cluster. The act provided $650 million in funding and tax credits for alternative energy and conservation. The strategy was to tie together the expertise of existing industries with research being done in universities and support it through infrastructure development. “The timing was lucky,” she said. “This will also create many jobs.” The fund was divided into two streams: $500 million in bond funding, $20 million in annual funding and tax credits over seven years, and $10 million in the eighth year.

The state had also funded an alternative development investment program to be managed by Ben Franklin Technology Partners, the state’s TBED organization. This fund received $40 million in assistance for energy-related investments to support early-stage activities. “This fund,” she said, “is near and dear to my heart. It lets us do management support, translational support, incubator support services, and company investment—to make sure we’re developing new companies.”

She closed on the topic of metrics, which had been discussed by several participants, some of whom suggested that no useful metrics had yet been developed for early-stage firms. “I don’t agree,” she said. “We have a methodology, and we survey all of our companies. Nor everyone likes it, but the questions are consistent. We went through a year-long process. A lot of that came out of my feeling that there had to be a way to measure these collaborations and all of these soft things that happen in technology-based development. We brought together 100 people we’d funded, hired an economist, broke up into groups, talked about what to measure and how. The Penn State survey center helped us. We ended up with 10 metrics, including jobs created and jobs retained, which most people ask. The one question they weren’t asking was how many new companies were formed. There are problems with data that we can debate, but I think new company formation is something we that can hang our hats on and is something unique to us. Jobs come from that, and that connection has held up pretty well with other people’s numbers. If you talk about those new companies in relation to jobs and salaries, we think you have something meaningful.”

Building and Branding Clusters: Lessons from Kansas and Philadelphia

Richard Bendis Innovation America

Mr. Bendis said that he was first involved in designing cluster formation in Kansas in 1999-2000, “before cluster strategies became the vogue. So we can look back and see which Kansas clusters have worked and which have not.”

He noted that in discussing the public sector’s role and where it should it intervene, one change since 2000 had been a migration away from the concept of “technology-based economic development” (TBED) toward one of “innovation-based economic development” (IBED). While the goals of TBED tended to focus on natural resources, brick-andmortar projects, and business parks, the goals of IBED were clusters, networks, innovation and technology products “intervening at the margins of the private sector.”

The flows of financial and intellectual capital, he said, now have the following objectives:

- Address the current economic transition.

- Capture more benefits of investments in research, development, and higher education.

- Build a stronger entrepreneurial culture.

- Help existing industries modernize.

- Diversify the economy.

- Create jobs.

- Innovate.

Despite the fundamental differences between the structures of the private and public sector, he continued, government does have an essential role in moving society closer to the objectives of IBED.

Specifically, it is government’s role to sustain the following:

- A healthy, educated public.

- Structures for job creation, economic health, knowledge worker development.

- World leadership in science, technology, engineering, and mathematics (STEM).

- Improved environmental quality and sustainable development.

- National infrastructure for information technology.

- Enhanced national security.

Government’s Responsibility to Involve Itself Deeply

To support these objectives, he said, the federal government has a particular responsibility to involve itself deeply in science and technology. The government is uniquely positioned to maintain a long-term vision and provide the support to sustain it. Government can also identify gaps and trends, and catalyze activities through strategic investments and partnering. With its breadth of agency expertise, it can sustain a balanced and flexible R&D investment portfolio and encourage private sector innovation through agency partnerships and incentive programs.

He offered more detail on the evolution of economic development. Traditional economic development, he said, sought advantage in such areas as natural resources, highways or rail systems, proximity of manufacturing and markets, and low production costs. They sought to develop value by investing in such structures as business parks and manufacturing facilities attracted by tax, land, and other incentives. They were led by long-standing organizations such as chambers of commerce and economic development commissions.

New Features of Modern Economic Development

IBED, by contrast, looks very different. Companies now compete through collaborative membership in clusters. They develop specialized talent through networking, liaisons with academic partners, and quick adaptation to market conditions. The key value offered by an IBED company is knowledge, which is gained through access to research and workforce competencies. The lead organizations tend to be innovation intermediaries, innovation based economic developers, or other entities

that may evolve rapidly or assemble on an ad hoc basis for new projects or programs.

Several additional features serve to more fully define IBED, he said. First is human connectivity, which emphasizes new forms of cooperation. Another feature is the public-private partnership, in which the missions of education, industry, and government are seen as inseparable. Finally, a cluster of more specific features emerges from an analysis of IBED best practices, including longevity, bipartisan support, continuous reinvention, private-sector involvement, accountability, and effective leadership. The clusters themselves, which might be considered the essential structure of IBED, embody all of these features and can uniquely concentrate knowledge assets, host globally competitive firms, create high-wage jobs, and attract scarce global talent and investment.

The Kansas Experience

He turned to his experience with the Kansas Technology Enterprise Corporation, or KTEC, which is a quasi-public body, funded through the state lottery, with the following mission: “To create, grow, and expand Kansas enterprises through technological innovation.” It was founded in 1986 as a holding company that managed a portfolio of programs, investments, subsidiaries, and affiliates operating as for-profit and not-for-profit entities. It is directed by a 20-member, industry-led board representing the legislature, government, universities, and the private sector.

In 2000, Mr. Bendis helped lead an assessment of the program to gauge its accomplishments after 12 years of operation. A standardized rating system was developed to determine the level of “capacity and opportunity” for critical technologies. The plan recognized “that Kansas is a flyover state,” he said, which meant that the study should not expect “class I research institutions or the presence of a large venture capital community. We had to link our strategic plan to local and national opportunities that matched the capacities in the region. We developed a Strategic Assessment Framework to see how Kansas ranked against national and global opportunities, based on the capacities it had at the local level.”

The assessment found that the state had high capacity ratings in four areas: human biosciences, agriculture and agricultural biotechnology, information and communications technology, and aviation. The researchers decided, in consultation with four universities, that biotech and biosciences were the strongest clusters, followed by information and communications technology. Agriculture was judged to have high capacity but not large opportunity. Aviation was judged to be an important cluster, but one whose growth prospects were seen to be

limited.1 The study also identified three “enabling clusters” that could limited. support some or all of the primary clusters: nanotechnology, manufacturing technology, and polymers.

The next step was to make policy recommendations based on the study’s framework and assumptions. The concluding recommendation, which constituted a “broad guideline,” was that “each state, country, or region must adjust and prioritize policies according to its individual context.” The study also recommended several objectives, especially the improvement of competitiveness of key industrial sectors—those identified as having high capacity. It was decided not to compete with emerging nanotechnology clusters, or with SEMATECH, because the state did not have sufficient infrastructure. “We chose to build on existing capacity and strengths,” he said.

In terms of structure, the Kansas Technology Enterprise Corporation had a portfolio of research and investment programs that it leveraged heavily with SBIR and business assistance programs. Instead of creating business incubators, it created innovation and commercialization corporations, linked them together, and recruited managers with national experience in venture capital to create regional early-stage investment funds.

Lessons and Results from Kansas

Mr. Bendis said that the study of the Kansas experience produced several organizational lessons that others might find useful:

- Begin with a clear articulation of the problem.

- Recruit or identify a respected, experienced, and patient “champion” to see the program through to completion.

- Develop a public-private partnership as a priority from the outset.

- Focus on tasks with a good chance of success; don’t waste resources where success is unlikely.

Ten years after the study, in 2009, the KTEC had produced the following organizational results:

- The Kansas BioScience Authority was created, without federal help, and funded at the level of $581 million to support innovative life science startups and research in Kansas.

- The National Agricultural Biosecurity Center was created in 2008, funded on a competitive basis with $500 million.

________________

1Wichita, often called the “Aircraft Capital of the World,” is the manufacturing base of Cessna, Hawker Beechcraft, Bombardier Learjet, Spirit AeroSystems, and Boeing Integrated Defense Systems. <http://www.wingsoverkansas.com/about/>.

- A new National Institute for Aviation Research was created to focus on creation new composites.

- A Software and Technology Association of Kansas was established to advocate for Kansas’ software and IT sector. A problem here, he said, was that IT companies did not feel a strong need to collaborate. His advice was “not to waste your limited resources on an industry cluster that thinks it can support itself.”

He then turned to Innovation Philadelphia (IP), a public-private partnership that differed from KTEC in spanning 3 states and 11 counties. Greater Philadelphia was judged to be at an economic crossroads, he said, and at risk of losing its status as a top-tier economic center. Innovation Philadelphia had goals similar to those of KTEC, beginning in 2002 with a cluster analysis for both the region and the city. An Innovation and Entrepreneurial Index indicated “more resources than most people thought we had,” and our glass, rather than being empty, was truly more than half-full.

In Philadelphia, A Need for a Roadmap

One challenge, he said, was the need for all participants to identify who their natural partners were in order to generate both an urban and regional perspective. Hence, a primary need was greater coordination and collaboration among all parties. This required not another economic development plan, but an umbrella roadmap to coordinate disparate and often competing activities. IP launched a research program with both qualitative approaches (one-on-one interviews) and quantitative tools (prior studies, federal funding data, private-sector R&D spending). This was done in partnership with the greater Philadelphia Chamber of Commerce and the city. A plan was produced in 90 days after the primary research and regional market analysis had been completed. This plan indicated that the primary strength in the city were financial services firms, while in the counties the strength was distributed among chemicals, pharmaceuticals, education, and biotechnology.

Critical ingredients of success included the willingness of civic, business, and political leaders to work on Hot Teams, each one consisting of members from academia, government, small and large innovative businesses, venture capital, as well as each geographical region represented. These leaders were willing to hold “feet to the fire” when necessary to catalyze collaboration. “We had respected leaders that served as a high-level oversight committee in the process,” he said, “so this was not just an exercise. Each one agreed to put vital resources and time into it.”

The group began with seven “prime targets of opportunity,” which it reduced to five based on concentration of assets and leadership. Today, “through a process of self-elimination,” there are three active clusters: Biomedicine (pharma is greater Philadelphia’s number one industry),

nanotechnology (including the Ben Franklin Technology Partners and Mid-Atlantic Nanotechnology Alliance), and “The Creative Economy,” which is the primary cluster that Innovation Philadelphia supports today and is a major employment cluster in the Philadelphia region.

Regional Branding and Marketing

The core actions of IP, he said, began with regional branding and marketing.

“You need to market your strengths,” he said, “so people know what you’re strengths are doing. The organizations also shared a common investment review process and shared due diligence procedures. Qualities that worked for both KTEC and IP included a focused and integrated approach, private sector leadership, operation of the efforts as a business, managing investments for ROI, flexibility, and with accountability.

He concluded by reviewing the need for such cluster activity. Paramount was the early-stage funding crisis in America, in which the “valley of death is wider and deeper than it’s ever been,” he said. “Just to have proof of concept isn’t enough these days. Now you need proof of relevance and a product that’s market-ready before you can get the attention of funders.”

He closed by recommending a new National Innovation Framework for the United States, an idea he had presented in December to the presidential transition team. The centerpiece was a $2 billion National Innovation Seed Fund that consisted of a Fund of Funds and a technical assistance grant fund; the latter provided entrepreneurial support and services to portfolio companies and fund managers. It also called for a new public-private innovation intermediary to accelerate the growth of the innovation economy and oversee the National Innovation Seed Fund. He said he had just met the day before with a working group for an innovation coalition seeking to raise innovation to a higher priority level within the Obama administration.

Innovation and entrepreneurship will be critical to accelerate America’s recovery from this economic recession. Innovative small entrepreneurial businesses that are supported by state and regional IBED programs and organizations will create the new knowledge-based jobs of the future.

Virginia Industry Cluster Analysis

John Mathieson SRI International

Mr. Mathiesson observed at the outset that “economic development people and S&T people don’t really speak the same language. One group speaks in terms of jobs and investments, the other in terms of funding for research and publications and maybe patents. From our perspective,” he said, “you have to look at one through the eyes of the other, back and forth.”

Virginia, he said has suffered from what had been called the “Dutch disease.” For the Netherlands, resources of offshore gas long provided sufficient wealth that the country did little to develop other industries. “In Virginia, we suffer from easy access to Washington, D.C., which drives the entire economy.”

An Overdependence on the Federal Market

To address this “disease,” Mr. Mathieson’s group did a state-wide examination of clusters. It found that like most states, Virginia’s economy was dominated by service industries. “Roughly two-thirds of the economy is there only to serve the local population,” he said. “You really have to focus on export-type industries.” Several technology and knowledge-based sectors stood out for their high levels of employment: life sciences and medicine (337,000 workers), research and engineering services (162,000 workers), and IT services (140,000 workers). Analysis of employment concentration ratio by cluster again revealed that key employers are IT, research and engineering, aerospace, defense, national security, and telecommunications. But all of these sectors owed their large numbers to easy access to the federal market.

Weak Innovation Resources

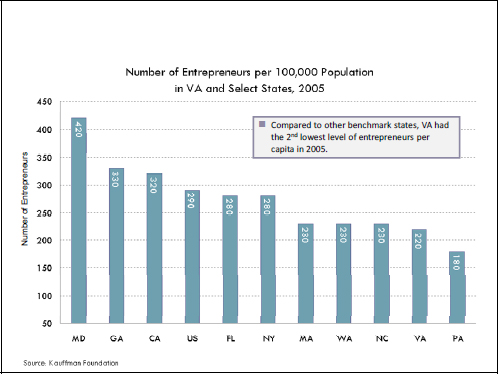

They also benchmarked Virginia’s innovation foundations, which revealed that “the commonwealth has a lot more going for it than it’s getting a bang out of,” he said. In financial resources, the state was doing well in STTR and SBIR awards, but small business loans and venture capital investment were weak compared to nine other benchmark states. Human resources were very strong as measured by educational level, but almost all qualified graduates work for the federal government or federal contractors rather than owning their own businesses. Innovation resources, he said, were “pretty weak,” other than those associated with federal R&D. The state was at the bottom of its comparison group for patents issued per 100,000 residents, and close to the bottom for entrepreneurs per 100,000 residents. Total R&D as a share of gross state

FIGURE 3 Innovation economy outcomes: Entrepreneurs per capita.

SOURCE: John Mathieson, Presentation at June 3, 2009, National Academies Symposium on “Growing Innovation Clusters for American Prosperity.”

product was about average. “So Virginia isn’t getting much for the incredible assets it has.”

Mr. Mathieson reviewed what the state could do to support high-potential technologies through various targeted interventions. It had become clear during the study that resources for R&D and technology were limited, “so you really do have to pick winners.” He agreed with the earlier comment that everyone, from the National Science Foundation to corporations, picks winners, and that a state is no different.

The study put the high-potential technologies through a “winnowing process” of five screening criteria. It identified several clusters in biomedical sciences and health care, including point-of-care diagnostics and computational technologies. The state was very strong in IT, and investments in IT would have benefits for health care, cyber security, and many other kinds of technology. Other technology-based industry clusters included chemicals and materials, clean energy and environment, and transportation and logistics, each with its own set of high-potential technologies.

Little Entrepreneurial Activity

Mr. Mathieson also examined the major cluster of biomedical sciences and health care by mapping economic growth against R&D locations, using publications, patents, and major research facilities by sector and by region. This review revealed considerable assets in terms of innovation and research facilities, but—again—little entrepreneurial activity. Another map showed the state’s IT assets. This revealed a “huge concentration,” he said, “higher than any other state.” Most of this concentration was in northern Virginia, because of both the huge federal market and the large number of internet-based companies that have grown or moved there. A similar exercise was performed for energy and environment, including research centers and concentrations of employment.

One conclusion was that “stove piping” was a major impediment to innovation in the state. “Everyone wants to do their own thing: national labs, large companies, etc. We identified gaps and then did case studies of other state programs that might help us enhance research excellence at universities and increase our bang for the buck. Promoting innovation is not just a matter of spending research dollars.”

A second conclusion was that the state had very little public-private collaboration. “You need to use experts as key players,” he said. And finally, Virginia needed to enhance entrepreneurship and access to capital. “As I mentioned,” he said, “the universities are really not hotbeds of entrepreneurial activity. They’re feeder systems to the big contractors and the federal government.”

After looking at the case studies, Mr. Mathiesson came up with a series of lessons learned:

- Highlight collaboration as a central component of all programs.

- Use industry and technology experts as key players in decision-making.

- Seek to leverage multiple sources of funding.

- Clarify key economic development objectives and milestones.

- Maintain strong systems of accountability.

- Use flexible tactics that allow for long-term adaptivity.

- Measure innovation progress.

In closing, he offered an overview of the need for innovation strategies. First, states must expand knowledge-based industries to compete nationally and globally. In OECD countries, knowledge-based industries are growing 20 percent faster than all industries, and salaries in those industries are 20 percent higher than in all industries. At the same time, manufacturing is following agriculture in its dwindling employment base, and some large service sectors, such as housing and

retail, are poised to repeat this pattern. “You have to look at innovation as your sweet spot,” he said.

An Innovation Initiative to ‘Transform the State’

In the case of Virginia, many industries depend on the federal market. While this is important and will not go away, he said, it does not reflect innovation in the true sense. The commonwealth has enormous assets but has not achieved its potential. “An initiative to stimulate innovation and catalyze collaboration among the groups,” he said, “can transform the state. This initiative must enhance research excellence, engage the private sector, nurture entrepreneurship and access to capital, and support technologies with the greatest economic potential.

To take on this task, Mr. Mathieson concluded, the state had created the Virginia Innovation Alliance (VIA), a public-private partnership endorsed by the governor and cabinet but placed on hold during the recession. The VIA was specifically designed to catalyze technology, generate desired outcomes, and evaluate those outcomes. “You can map out metrics at different points along the value chain,” he said, “both in terms of innovation and its outcomes. The outcomes you want are well known: cluster health and growth, jobs, investments. We want to gain political support that transcends administrations, which is why it would be led by the private sector. We want to increase collaboration among stakeholders, and sustain centers of excellence in technology. If we do all these things and do them right, Virginia will become a model innovation economy.”

The Washington State Innovation Economy

Egils Milbergs Washington Economic Development Commission

Mr. Milbergs began optimistically with the thought that “a crisis is a wonderful time to rethink and reinvent. In Washington State, we don’t like the term ‘economic recovery,’ because it implies going back to the same old ways. We don’t want a recovery, we want something new. This recession will be the mother of the innovation economy of the 21st century.”

He followed this thought with three caveats:

- “The federal government can get things wrong. We are wary of too-rapid spending, because it has the potential to distort local and regional economies. We want to take advantage of resources, but have to be thoughtful how we use them.”

- “Cluster analysis can get things wrong. It gives you backward-looking data about where you have been. It doesn’t tell you where you’re going.”

- “The most important process in building an innovation economy is not the money; it’s the relationships and the time to build those relationships. We need leaders to sit around the table and think things through and actually implement some of the strategies we’ve heard about.”

He said that the state, which spends about $3 billion a year on economic development, stands to receive $7 to $8 billion from the stimulus package. “We have to think about how to spend those monies,” he said, “because we don’t want to produce our own bubble.”

He said that in his opinion, the most important metric for innovation success is the experience of the consumer. “The most important way to create jobs is by creating customer satisfaction.” Washington State depends on consumers, he said, and on innovation. The state does not have much government involvement, and the private sector has adopted the goal of making Washington “the most attractive environment in the world for private industry.”

To do so, he said, the state is planning a new model for economic development.

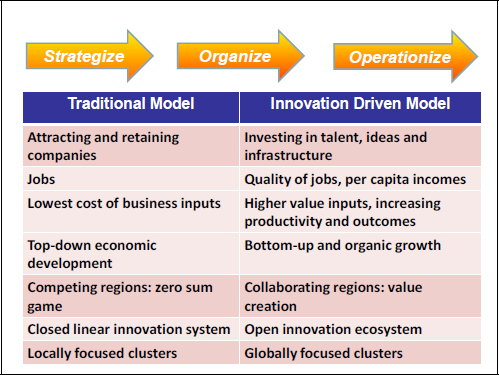

Toward a New Model of Economic Development

This model will make substantial changes from traditional economic development. He said that the major features of the traditional model have been the following:

- Investment in attracting and retaining companies.

- Creating jobs.

- Emphasizing low-cost inputs, especially labor.

- Developing the economy from the top down.

- Regarding different regions as competitive, and economic development as a zero-sum game.

- Supporting a closed and linear innovation system.

- Supporting local clusters.

An innovation-driven model, by contrast, would have the following features:

- Investment in talent, ideas, and infrastructure.

- Creating high quality, high-income jobs.

- Using high-value inputs that increase productivity and outcomes.

- Developing the economy from the bottom up, building on ideas and knowledge.

FIGURE 4 New model for economic development.

SOURCE: Egils Milbergs, Presentation at June 3, 2009, National Academies Symposium on “Growing Innovation Clusters for American Prosperity.”

- Regarding the regions as partners and the entire state as a toolbox for growth.

- Supporting an open and networked innovation ecosystem.

- Supporting global clusters.

He stressed a key feature of the innovation-driven model—the exchange of cheap inputs for high-value inputs. Traditional planning, he said, would opt for cheap labor based on cost alone. An innovation-based approach, by contrast, would see the advantages of well-trained employees who are qualified to contribute not just labor but also ideas and leadership, which are the basis for bottom-up productivity in the knowledge-based economy.

Key Drivers of Innovation: Talent, Investment, Infrastructure

The key drivers of innovation and growth, he continued, are talent, investment, and infrastructure. Educating and training young talent is an increased challenge during today’s financial crisis, he said, but necessary

to sustain innovation. Investment is needed to diversify the R&D base and to ignite local innovation and entrepreneurship. Investments in infrastructure are needed to create a “smart, clean, and green” economy, which eventually functions without oil. He noted that 70 percent of his state’s electricity is produced by hydroelectric plants at low rates, a valuable economic advantage.

Mr. Milbergs said that the state’s key industry clusters were diverse and strong, including agriculture (the wine industry had grown from a handful of vineyards 20 years ago to more than 600 today); health services, centered in Spokane; the beginnings of a smart grid; information technology; aerospace; alternative energy, “Silicon Forest”2; defense; and film production. In 2007, the Innovation Partnership Zones (IPZ) program was created by Gov. Gregoire and the state legislature as part of the state’s efforts to stimulate industry clusters within specific geographic areas. He said that the Puget Sound “tech universe,” one of the strongest zones, had already spawned 719 companies.

Philanthropy as a Wealth Creator

A new wealth-creating sector in Washington, he said, had been catalyzed by the Bill and Melinda Gates Foundation, whose endowment exceeds the size of the combined venture capital firms of the United States. This Global Health Ecosystem partners with some 160 organizations, mostly nonprofits, that operate in nearly 100 countries. “As they are trying to solve about 20 major disease problems,” he said, “they are also creating a health ecosystem that’s going to be sustainable. This is a recent example of philanthropy as a wealth creator.

One of the objectives of the Washington Economic Development Commission, he said, was to connect the regions of the Washington innovation ecosystem. He described a “Glimmers of Hope” virtual tour of Washington’s innovation clusters whose purpose was to learn about the visions of each cluster, as well as their financial plans. Anyone, he said, could “follow the ‘tour’ via the Internet, communicate with it, invest in it, comment, collaborate, and even use the output.” Eventually, he said, this process will connect the regions, so that the entire state can function as a “toolbox” or a “social and economic laboratory of democracy.” By building such a system, he said, the state would have an economic model of how inputs drive the business environment and how the business environment creates wealth, jobs, and ultimately state revenues.

_______________________

2A cluster of high-technology firms exist in the area of Portland, Oregon, and southwest Washington.

He closed with a time-honored quotation about innovation: “The best way to predict the future is to invent it.”3

_______________________

3This quote is attributed to Alan Kay, a developer of the object-oriented programming language Smalltalk invented at Xerox PARC in the early 1970s. Smalltalk was the inspiration for the graphical user interface pioneered by Apple Computer. A more extensive version of the quote is: “Don’t worry about what anybody else is going to do…. The best way to predict the future is to invent it. Really smart people with reasonable funding can do just about anything that doesn't violate too many of Newton's laws!” <http://www.smalltalk.org/alankay.html>.