2

Transformation of the Retail Sector

This chapter describes recent changes in the retail sector, highlighting several important shifts since the 1990s in the way the sector is structured and the nature of the goods and services it provides. The chapter then considers these sectoral shifts and the way they extend or challenge the traditional definition of the retail sector. Finally, it turns to look at trends related to the retail sector from current statistical series to see what picture they provide of this sectoral transformation.

During the panel’s workshop, four of the seven sessions provided an overview of important recent changes in the retail sector.1 The first session considered the transformation from the perspective of researchers who study the sector. The second session considered the transformation from the perspective of industry representatives, focusing on participants who could provide a detailed understanding of the way the retail supply chain is being restructured. The sixth session looked at some of the trends in the sector that are revealed in analyses of firm-level data. Finally, the seventh session considered the importance of global value chains in the production of goods and services related to retail and the insights these provide about the way retail is changing.

___________________

1 See Appendix A for the workshop agenda, including the panelists and moderators who participated in each session.

RECENT CHANGES IN THE RETAIL SECTOR

This section describes seven different but related changes in the retail sector, discussing each in turn. These changes capture the ways the sector is transforming that could be reflected in the government measures of the retail sector.

Collectively, these seven changes also illustrate a fundamental characteristic of the retail sector, which is its intensely dynamic nature. Without knowing in advance what new changes may appear in the future, it is a near-certainty that further changes of this magnitude will continue to appear to further challenge available measures of retail employment and labor productivity. So, while the seven changes discussed are important for the sector in the recent past and highlight important measurement challenges to address, they also illustrate the types of far-reaching change that will continue into the future in new and unexpected ways beyond the specific changes discussed here.

Rise of Warehouse Clubs and Supercenters

Since the 1990s, there has been a large shift toward warehouse clubs and supercenters (NAICS 452311)2 at the expense of department stores (Hortaçsu and Syverson, 2015). Both formats are classified as general merchandise stores (NAICS 452), which represent one-fifth of total employment in the retail sector, 3.0 million out of 15.7 million employees.3 Over the first two decades of this century, while employment in retail overall and in general merchandise stores stayed roughly constant,4 there was a large shift in employment within general merchandise: department store employment decreased by 0.7 million while employment in general merchandise stores, including warehouse clubs and supercenters, increased by 0.9 million.5 This shift moved department stores from 62 to 36 percent of employment in the

___________________

2 Industry statistics in the United States are classified according to the North America Industry Classification System (NAICS). In the 2017 version of NAICS, there are 12 retail trade industries at the 3-digit level, 27 at the 4-digit level, and 66 at the 6-digit level. Warehouse clubs and supercenters are coded as 452311 in the 2017 release of NAICS and as 45291 in the 2012 release.

3 3.0 million employees for general merchandise stores (NAICS 452) compared to 15.7 million for retail overall (NAICS 44-45), seasonally adjusted data for January 2020 [August 5, 2020] from https://data.bls.gov.

4 Seasonally adjusted employment in January 2000 was 2.8 million for general merchandise stores and 15.2 million for retail overall.

5 Seasonally adjusted employment in department stores (NAICS 4522) decreased from 1.73 million to 1.08 million from January 2000 to January 2020, while the corresponding employment in general merchandise stores, including warehouse clubs and supercenters (NAICS 4523), increased from 1.08 to 1.97 million.

general merchandise sector. The shift appears even more strikingly in sales figures, with department stores declining from 60 percent of total sales in the general merchandise sector in January 2000 to 18 percent in January 2020.6 Warehouse clubs and supercenters are now the largest subindustry in general merchandise stores (NAICS 452).

The warehouse club and supercenter format moves some of the traditional functions of the warehouse into the store itself, providing inventory storage directly in the store. In addition, the shift moves toward a format that provides a lower level of customer service than is provided by traditional department stores and also includes food sales, which are not part of traditional department stores.

Rise of E-Commerce

The shift toward e-commerce is another important change in the retail sector (for a recent overview see Lafontaine and Sivadasan, forthcoming). Until recently, however, e-commerce remained a small part of retail overall, despite high growth rates. For example, nonstore retailers (NAICS 454) represented only 2.9 percent of total retail employment and only 7.9 percent of total retail sales in January 2010.7 Total sales in nonstore retailers surpassed sales in general merchandise stores, including warehouse clubs and superstores, only in 2015.8 According to the Census Bureau, e-commerce as a percentage of total sales grew from 0.6 percent in 1999 to 16.1 percent in the second quarter of 2020.9

As e-commerce has grown in recent years, it has become increasingly difficult to separate out the e-commerce portion of the industry. Most e-commerce could be identified within the nonstore retailer category as of 2013 (Hortaçsu and Syverson, 2015, p. 96), but e-commerce is becoming so pervasive that it is now not only difficult to clearly identify individual firms as predominantly e-commerce firms, but also often impossible to clearly classify individual retail sales as either e-commerce or not. The focus now for many retail firms is to adopt an “omni-channel” strategy, whereby they provide both e-commerce and in-store “channels” for customers to learn about and buy products. Customers frequently combine channels within a single purchase, sometimes reading online descriptions and reviews before

___________________

6 Seasonally adjusted sales data for January 2000 and 2020. See https://www.census.gov/retail/mrts/historic_releases.html for department stores (2012 NAICS 4521).

7 Seasonally adjusted employment of 0.416 million out of 14.4 million in January 2010 and seasonally adjusted sales of $27.3 billion out of $346 billion for the same month.

8 See https://www.census.gov/retail/mrts/historic_releases.html.

9 U.S. Census Bureau. (2020). Census Bureau Provides Data on Fast-Growing Retail E-Commerce. November 24. See https://www.census.gov/library/stories/2020/11/share-ofonline-retail-sales-soaring.html.

inspecting a product in a store and purchasing it, but other times first seeing the product in a store and then later ordering it online after making comparisons across vendors.

The rise of e-commerce can be thought of as extending retail services in two different ways. First, e-commerce incorporates a set of warehouse services into the online store itself, providing customers with access to a vast range of inventory that goes far beyond the range of inventory that a brick-and-mortar store can physically stock. Second, e-commerce also extends the services provided by the retailer into a consumer’s home, replacing some of the shopping and delivery services that consumers have until only recently provided for themselves. Providing these extended retail services has required the creation of substantial computing and demand analysis functions that are associated with the headquarters of large retailers and that produce substantial intangible assets that are essential to the success of these firms.

While e-commerce extends retail services, the digital technology that makes e-commerce possible also takes away a number of key retail services from the physical store itself, including providing information to customers about the products that are available, accepting the customer’s payment to execute the purchase, and providing the product to the customer upon purchase. Those services are not only removed from the physical store, but also sometimes no longer directly provided by the retailer at all. For example, a freight company may contract with a retailer to manage inventory, interact with customers to execute purchases, and deliver products, operating under the retailer’s own brand.

The section further below on responses to the COVID-19 crisis describes the substantial acceleration of e-commerce that has occurred in response to the pandemic.

Digital Transformation of Retail Goods

Digital technology has not only allowed e-commerce but also transformed the form of many retail goods themselves. Books, music, and video provide clear examples of this transformation, with products that used to be sold as physical goods now largely transformed into digital downloads that may be either sold or rented. Of course, the renting of retail products has existed for a long time, notably for car leasing and formal wear. However, digital technology has made it increasingly feasible to expand the rental markets for other consumer goods, such as a much broader range of clothing (e.g., Rent the Runway).

A few statistics provide an illustration of the range of these changes. Revenue from e-books and downloaded audio books totaled $3.25 billion in 2019, representing 12.5 percent of total publishing industry revenue,

up from 7.3 percent in 2015. Between 2015 and 2019, e-book and downloaded audio book revenue increased by 61 percent.10 Expenditures on video and audio streaming and rental, as a proportion of total expenditures on video and audio, have increased from 22.3 percent in 2000 to 32.5 percent in 2010 to 66.5 percent in 2019.11 For comparison, expenditures on motor vehicle rental and leasing as a proportion of total expenditures on new motor vehicles, including sales, rentals, and leasing, have fluctuated between 13 and 23 percent since 1994 without a clear trend, after increasing from below 2 percent in the 1980s.12

Imports of Retail Goods and Services

Imports of retail goods and services are also transforming the sector. For example, four large retailers (Walmart, Target, Home Depot, and Lowe’s) accounted for almost 10 percent of U.S. imports by volume in 2018.13 These large firms import directly, providing their own import distribution centers. Some product categories—such as toys, furniture, clothing, and electronics—are heavily dependent on imports. Imports of consumer goods totaled $1.19 trillion in 2007, having grown 3.7 times from the value of $319 billion in 1992 (Smith, 2019).14 Consumer imports in 2007 represented almost a quarter of total retail and food services sales of $4.4 trillion.15

Given the complexity of global supply chains, it can be difficult to identify the domestic and imported portions of a good’s value, whether it comes directly from a domestic or foreign manufacturer. Complex products, such as motor vehicles and consumer electronics, often include components sourced from several different countries. In addition, the value of many imports includes intellectual property, which may actually be owned by the importing U.S. firm. Despite the complexity of many products, a number

___________________

10 Revenue figures provided by the American Association of Publishers. See https://publishers.org/news/aap-statshot-annual-report-book-publishing-revenues-up-slightly-to-25-93-billion-in-2019.

11 BEA, nominal Personal Consumption Expenditures, comparing nominal expenditures on video and audio streaming and rental with total nominal expenditures on video and audio streaming and rental along with recording media. Calculated from the underlying detail tables for Personal Consumption Expenditures, see https://apps.bea.gov/iTable/index_nipa.cfm.

12 BEA, nominal Personal Consumption Expenditures, comparing nominal expenditures on motor vehicle leasing, motor vehicle rental, and new motor vehicles. Calculated from the underlying detail tables for Personal Consumption Expenditures, see https://apps.bea.gov/iTable/index_nipa.cfm.

13 See https://www.joc.com/maritime-news/top-100-us-importer-and-exporter-rankings-2018_20190530.html, cited by Dominic Smith at the panel’s workshop.

14 Both figures reported in 2007 dollars.

15 See https://www.census.gov/retail/mrts/www/mrtssales92-present.xls.

of international organizations and researchers have developed global input-output estimates of their global value chains.16

In addition to imports of the retail goods for sale in the United States, some portion of retail services can also be outsourced by retail firms. For example, L.L. Bean carries out much of its back-office work in Costa Rica.17

Role of Large Firms in the Retail Transformation

The four changes previously mentioned have been driven by national and regional multi-unit retail firms, which lead productivity growth in the industry and represent most of the sector’s growth in sales and employment (Foster et al., 2016). Sales of the eight largest retail firms as a percentage of all retail sales rose from 11.7 percent to 19.5 percent from 1997 to 2012.18 Single-unit retail firms still account for roughly 60 percent of retail establishments, but only 30 percent of retail sales.19

Large firms pose a challenge to developing statistics by industry, since their level of integration indicates clear economies of scale and scope that go across their divisions. Fundamentally, this means that some inputs—at a minimum, each firm’s management—are contributing to multiple outputs in a way that cannot easily be apportioned for statistics or reproduced by single-unit firms. For firms that have retail divisions in addition to other divisions—such as manufacturing, warehousing, or transportation—it is hard to appropriately attribute the common inputs that are contributing to the retail portion of the firm.

Despite the increasing role played by large firms over the past several decades, the digital systems that have become pervasive over this same period now allow retailers to outsource many retail functions to other providers, including customer interaction and order fulfillment. These systems increasingly allow any retailer to reproduce the same quality and speed in customer interaction and order fulfillment that a company like Amazon can provide. This suggests that the transformation that has been driven by

___________________

16 See work by the Organisation for Economic Co-operation and Development with the World Trade Organization, https://www.oecd.org/sti/ind/measuring-trade-in-value-added.htm; by the Global Trade Analysis Project, see https://www.gtap.agecon.purdue.edu/; and by the World Input-Output Database, http://www.wiod.org/home.

17 Cited by Marshall Reinsdorf at the panel’s workshop.

18 Census Bureau, Economic Census of Retail Trade: Establishment and Firm Size (Including Legal Form of Organization), 1997 Economic Census, Retail Trade, Subject Series, Issued October 2000, EC97R44S-SZ, Table 6, page 197, see https://www2.census.gov/library/publications/economic-census/1997/retail-trade/97r44-sz.pdf, for 1997; and https://data.census.gov/cedsci/table?q=EC1244&tid=ECNSIZE2012.EC1244SSSZ6&hidePreview=true for 2012.

19 John Haltiwanger at the panel’s workshop.

the large retail firms over the past couple decades is now being extended in a way that smaller retailers can use, with implications throughout the entire sector.

Increased Product Variety

A number of changes in the retail sector already discussed have contributed to a general change reflected across the sector in making more products available to consumers and providing new retail services to help consumers navigate and take advantage of growing product variety. This can be seen in the sheer number of products offered at warehouse clubs and supercenters, which has increased again with the rise of e-commerce, where nonstore retailers can offer a huge range of products beyond the limits of a physical store. At the same time, inventory management software and online search and recommendations systems allow consumers to identify and obtain specific products from the vast array offered for sale, powerfully extending the service that retailers have always provided in presenting and organizing products for consumers to consider purchasing. These services include the ability of consumers to easily compare prices and customer reviews and to have their purchases delivered directly and quickly to their homes, making it possible for them to access a larger variety of products while simultaneously reducing shopping time, travel costs, and prices.

Changes in Response to COVID-19

This project was carried out virtually while the United States, along with much of the rest of the world, was struggling to find a successful response to the COVID-19 pandemic. That context highlighted changes that the pandemic had already brought to the retail sector and might bring in the future, beyond the temporary closure of many retail stores during the initial response, which in many cases may become permanent.

Dramatic changes in e-commerce occurred during the first two quarters of the COVID-19 crisis. E-commerce sales increased by 31.9 percent from the first quarter to the second quarter of 2020, and e-commerce sales in the third quarter of 2020 were 36.7 percent larger than in the third quarter of 2019.20 E-commerce in the second and third quarters of 2020 represented 16.1 percent and 14.3 percent of total U.S. retail sales, respectively, compared to 11.8 percent in the first quarter of 2020. Relatedly, there has been a surprising surge in applications for new businesses during the COVID-19 crisis, dominated by an increase in applications for nonstore retailers.21

___________________

20 See https://www.census.gov/retail/mrts/www/data/pdf/ec_current.pdf.

These patterns suggest that the COVID-19 crisis has accelerated the long-run trend toward a greater role for e-commerce in retail trade.

HOW RECENT RETAIL CHANGES RELATE TO THE BASIC DEFINITION OF THE SECTOR

The different changes that have occurred in the retail sector sometimes raise the question of whether the transformed activities should still be classified as belonging to retail. This question is raised with particular urgency by e-commerce, where a growing number of firms now provide some aspects of retail services without identifying themselves as retail firms. Does a freight company that subcontracts with a retailer to provide customer service and order fulfillment services effectively become a retail establishment in some sense? The digital transformation of some traditional retail goods poses similar questions. Should books or videos that are now provided as digital downloads or as part of a larger subscription service be included as part of the retail sector? We discuss these two questions in turn.

Relation of Retail to Other Industries

The potential difficulty in deciding whether some firms belong to the retail classification leads to a consideration of the essential characteristics that define the retail sector. Retail is often identified as facing the final consumer and distributing “retail-like products” without transforming them. The definition used by NAICS notes that retail provides services that are “incidental to the sale of merchandise” and that retail “is the final step in the distribution of merchandise.”22 The NAICS definition further notes that “the buying of goods for resale is a characteristic of retail trade establishments that particularly distinguishes them from establishments in the agriculture, manufacturing, and construction industries.”

Thus, a farm, manufacturer, or housing developer that sells directly to the public is not considered to be a retailer because each of these businesses produces what it sells, rather than buying products for resale. Wholesale trade is also distinguished from retail trade, because wholesalers “are not usually organized to serve the general public.” The NAICS definition notes that “dealers of durable nonconsumer goods, such as farm machinery and heavy-duty trucks, are included in wholesale trade even if they often sell these products in single units” and even though they are often sold to the final (business) purchaser. The NAICS definition also provides examples of “incidental” services that are sometimes provided by retailers, including

___________________

22 See https://www.census.gov/naics/?input=44&chart=2017&details=44.

“the provision of after-sales services, such as repair and installation” in the cases of “new automobile dealers, electronics and appliance stores, and musical instrument and supplies stores.” Some processing activities are also considered “incidental” to the retailing function such as “optical goods stores that do in-store grinding of lenses, and meat and seafood markets.” Thus, the existing definitions identify retailers as those who purchase goods for resale to the general public with limited transformation of those goods.

Traditionally, a relatively stable wholesale sector moved goods between manufacturers and retailers without directly interfacing with final consumers. The warehousing sector stored goods in the transition from manufacturer to final consumer, and the transportation sector moved goods between manufacturer, wholesaler, retailer, and final consumer. As noted above, large retailers today often directly provide wholesale services (including direct importing), along with related warehousing and transportation functions. Retailers may outsource some of the services related to retail, such as customer service or order fulfillment, either to specialized firms operating invisibly under the umbrella of the retailer’s brand or to other retailers like Amazon. In some cases, a retailer may outsource order fulfillment to a manufacturer, who may deliver directly to the consumer without the retailer ever taking possession of the good and holding it in inventory.

As a result of these transformations, large retailers have often added functions performed by the wholesale, warehousing, and transportation industries, and they may also have outsourced some retail services to specialized providers. Nevertheless, they still largely provide the defining function of purchasing goods for resale to the general public with limited transformation. In that sense, the traditional definition of retail trade still applies to large retailers, even after these transformations, as much as it applies to traditional single-unit retailers that use the wholesale, warehousing, and transportation sectors in the traditional ways. However, the internal cost structure of large and small retailers and the functions provided by their employees are likely to be quite different. A large retailer may obtain goods at a lower cost directly from the manufacturer (domestic or foreign), but then provide various wholesale, warehousing, and transportation services internally that a traditional single-unit retailer would have to pay for. At the same time, a large retailer may outsource some traditional retail services, like customer service, that a traditional single-unit retailer provides directly. These different arrangements of purchased and produced services need to be reflected to provide meaningful comparisons of employment and productivity across large and small retailers that can apply as the sector continues to evolve.

CONCLUSION 2-1: The traditional definition of retail trade applies to the large retailers that have become increasingly important over the past few decades as well as it applies to more traditional small retailers. However, the cost structures of these two types of firms can be quite different. Large retailers often provide wholesale, warehousing, and transportation services directly, whereas small retailers usually purchase these services. In addition, large retailers sometimes outsource some traditional retail services, such as customer service and order fulfilment, whereas small retailers usually provide these services directly. Defining retail output as the quantity of goods sold will understate the contribution of retailers that provide high levels of service.

Range of Goods and Services Included in the Retail Sector

One aspect of the transformation on the goods side involves digital versions of products, such as books and videos, that were previously provided physically. In cases where the digital versions are provided by a retailer (such as Amazon) as well as a publisher, the standard retail definition would classify the sales as occurring in the retail sector, recognizing that goods can be considered to be intangible (Reinsdorf and Slaughter, 2009). Of course, if the digital books were sold by the publisher, the sale would be counted within the information industry (NAICS 51), but that is no different from other sales occurring directly from manufacturers. However, if digital goods are leased rather than sold, then they no longer fall under the definition of retail, instead moving to rental and leasing services (NAICS 532), which includes automobile leasing and various other types of leasing, such as formal wear, home health equipment, and office machinery.

On the retail services side, e-commerce has replaced some of the shopping and delivery services that consumers have until recently provided for themselves (Mandel, 2017). This type of shift is not novel; in earlier periods, deliveries of this type were sometimes standard, as when retailers provided home delivery of milk. However, this shifting in the types of services provided by the retail sector can make it difficult to interpret changes that are occurring in measured employment and productivity. Specifically, the extra services can produce an increase in employment and therefore possibly suggest a decrease in productivity unless the output measure recognizes that a greater level of service is being provided, as reflected in the significant reduction in unpaid shopping hours reported by the American Time Use Survey.23

These two changes, which involve shifts from activities inside the traditional retail definition to activities outside that definition or vice

___________________

versa—movement of some products from sales to leasing, and shifts in the direct labor provided by consumers—underline potential challenges to collecting meaningful statistics during a period of sector change. These types of changes are not novel and occur in other sectors as well as retail, but their effects may be extensive enough in retail that it is worth the extra effort to understand their role in affecting employment and productivity. Since both involve shifts related to what is included in the retail category, understanding the effects of these changes on employment and productivity would require analyses that combine or compare information from inside and outside the traditional retail category.

CONCLUSION 2-2: In cases where the recent transformation in the retail sector has shifted some retail services outside the traditional definition of the sector (e.g., by moving from sales to leasing of some products like clothes or movies) or brought some services into retail that were formerly outside the traditional definition (e.g., by delivering purchases that consumers previously purchased at a store), an understanding of the employment and productivity effects of the changes will require analyses that compare services inside and outside the retail sector.

Beyond these examples, there are further expansions in the types of goods and services offered by large retailers that go well beyond the traditional retail sector, such as the provision of cloud computing by Amazon and of consumer health services by Walmart. Under the standard NAICS classification system, these products would be classified in other industries (NAICS 518 and 621, respectively). The only difficulty that might arise concerns the extent to which large firms operating in multiple industries necessarily comingle work related to those different industries, at a minimum with respect to the contribution of the firms’ management. This situation necessarily requires some approximation in allocating inputs to different industries, though that is a challenge throughout the economic statistical system and is not specific to the retail transformation.

THE RETAIL TRANSFORMATION AS SEEN IN EXISTING STATISTICAL SERIES

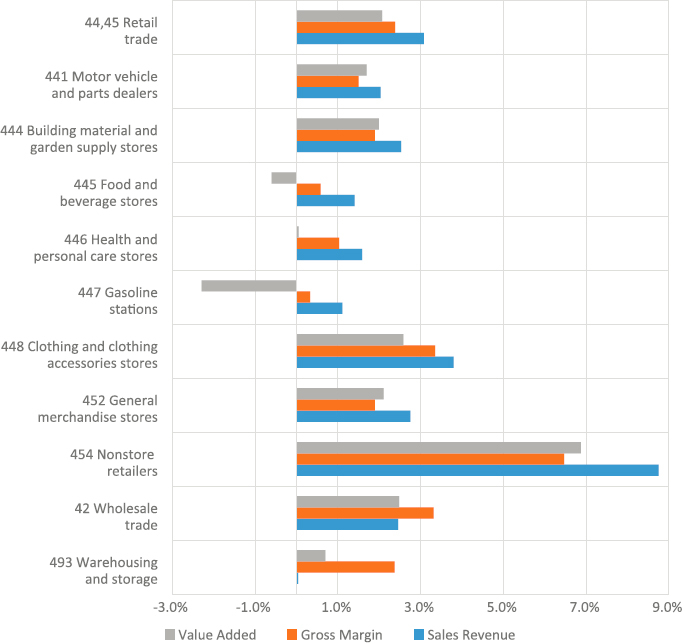

As a starting point in considering the statistical challenge of portraying and understanding the retail transformation, Figure 2-1 illustrates the sector’s labor productivity as measured by three different statistical series. In each case, the series looks at the average annual change in labor productivity over the 21-year period from 1997 to 2018, where labor productivity

SOURCES: Output measured by sales revenue from U.S. Bureau of Labor Statistics (BLS), Division of Industry Productivity Studies. Labor productivity calculated by dividing change in output by change in hours worked, using hours data from BLS (BLS data from https://www.bls.gov/lpc/lpc_by_industry_and_measure.xlsx using the “Output” and “Hours” fields for the sale revenue and hours indices, respectively). Output measured by gross margin and value added from U.S. Bureau of Economic Analysis, Industry Data webpage (using the “Chain-Type Quantity Index” for both gross output and value added). All series provided in Appendix B.

is defined as the real output in the sector divided by the hours worked.24 The three series define retail output in different ways: (1) as total sales revenue; (2) as the difference between sales revenue and the cost of goods

___________________

24Appendix B, which contains the underlying data, also breaks the series at 2007, which shows the slowdown in retail labor productivity growth that occurred from the first decade (1997-2007) to the second (2007-2018).

sold (gross margin); and (3) as the difference between sales revenue and the cost of all purchased inputs (value added), with nominal values deflated by appropriate price indices in each case. Labor productivity growth rates are provided for the retail sector overall, along with the major three-digit retail subindustries, and they are provided as well for two other sectors for comparison: wholesale trade and warehousing.

The data underlying these series are discussed in Chapter 3, but the focus in this chapter is simply on comparisons of the qualitative picture of the sector that emerges from the changes discussed above and the quantitative picture that emerges from the different statistical series

The changes experienced by retail over the past few decades suggest that the sector is highly competitive and is undergoing substantial change and reorganization. As discussed earlier, the changes described involve warehouse clubs and superstores (a part of general merchandise, NAICS 452), e-commerce (concentrated in NAICS 454 in earlier periods and expanded to NAICS 493 in more recent periods), digital goods, imports, and large firms, along with some more recent changes brought about by COVID-19.

By contrast, the three statistical series describe a sector where annual labor productivity growth averaged 2.1 to 3.1 percent per year over the two decades from 1997 to 2018. This growth in labor productivity was not substantially different from the 2.1 percent growth in labor productivity for the nonfarm business sector over this period.25 Despite the similarity across the three estimates, the cumulative differences in these growth rates over the 21-year period are substantial, with the sales revenue measure reflecting a cumulative labor productivity increase of 92.5 percent, compared to the 56.5 percent increase that emerges from the value-added measure.26 The range across these three figures reflects meaningfully different pictures of the labor productivity growth in the retail sector.

The one retail subindustry that clearly stands out for its labor productivity performance is the nonstore sector, where labor productivity was more than twice as large as for the retail sector as a whole. However, for general merchandise stores, which saw substantial restructuring in the decline of department stores and the rise of warehouse clubs and supercenters, productivity changes look no different than for the rest of the retail sector in the three statistical series.

Another observation of note in Figure 2-1 is the cases where there is a clear divergence in the picture provided by the different statistical series: Food and beverage stores (NAICS 445) and gasoline stations (NAICS 447)

___________________

25 Haver Analytics database, nonfarm business sector, real output per hour of all persons, Bureau of Labor Statistics, annualized percent growth based on annual data, 1997-2018.

26 See Appendix B.

both show labor productivity falling when measured using value added, but rising when using sales revenue or gross margin. Similarly, health and personal care stores (NAICS 446) show zero labor productivity when measured using value added, compared to rising productivity when measured using sales revenue or gross margin.

There is no way for the other changes discussed above to be directly reflected in Figure 2-1. The subindustry breakdowns do not align with changes in digital goods and services, imports, or the role of large firms.

Table 2-1 provides several indicators besides labor productivity that show the extent of some of the changes discussed in the retail sector. The

TABLE 2-1 Several Indicators of the Retail Transformation, 1997-2019 (percentage)

| 1997 | 2002 | 2007 | 2012 | 2017 | 2019 | |

|---|---|---|---|---|---|---|

| Warehouse and supercenter share of total retail sales | 4.6 | 7.3 | 9.3 | 10.9 | 10.8 | 10.6 |

| Nonstore retailer share of total retail sales | 5.1 | 6.1 | 7.7 | 9.5 | 12.5 | 14.6 |

| Employment share in firms with <500 employees | 42.9 | 39.0 | 35.9 | 35.2 | ||

| Employment share in firms with 10,000+ employees | 44.6 | 49.7 | 52.3 | 53.5 | ||

| Share of total retail sales for 8 largest retail firms | 11.7 | 15.3 | 17.5 | 19.5 | ||

| E-commerce share of sales: | ||||||

| Music and video | 12.3 | 41.2 | 76.5 | |||

| Books and magazines | 9.1 | 22.1 | 41.1 | |||

| Computers and software | 18.7 | 30.3 | 32.9 | |||

| Food and beverages | 0.2 | 0.7 | 0.9 | |||

SOURCES: Sales data from BLS, https://www.bls.gov/lpc/lpc_by_industry_and_measure.xlsx, using the Value of Production field for NAICS 45231 (General merchandise, including warehouses and supercenters), NAICS 454 (Nonstore retailers), and NAICS 44, 45 (Retail trade). Employment data from Census Bureau, Statistic of US Business (SUSB), https://www.census.gov/programs-surveys/susb/data/tables.html, for Retail Trade. Revenue share of 8 largest firms from Census Bureau, Economic Census of Retail Trade, https://www.census.gov/programssurveys/economic-census/data/tables.html. E-commerce share of sales calculated in Hortaçsu and Syverson, 2015, Table 1, “by dividing the sum of the product category’s e-commerce sales within and outside Electronic Shopping and Mail-Order Houses (ESMOH) by the sum of total ESMOH sales of the product and total sales of the product’s corresponding retail industry.” Chad Syverson generously provided the underlying data points for the series. The 2012 value for computers and software is missing in the series and is calculated in the table as the average of 2011 and 2013.

first pair of figures shows the shift in the share of total retail sales in the subset of general merchandise stores that includes warehouse clubs and supercenters (NAICS 45231) and in nonstore retailers (NAICS 454). In both cases, the share of total retail sales in these types of outlets more than doubles over two decades, and the shift is large in relation to overall retail sales. The second set of figures shows the shift in the employment share in small (< 500 employees) and large (10,000+ employees) firms, with a shift of 8 percentage points in overall retail employment from small to large firms over a 15-year period. It also shows the shift in revenue of the largest eight retail firms over an earlier (but overlapping) 15-year period. Finally, the third set of figures shows estimates of the e-commerce share of sales in different product categories over a single decade, with substantial shifts to e-commerce in some product categories—music and video, books and magazines—and very small shifts in others, especially in food and beverages.

This page intentionally left blank.