1

Introduction and Overview1

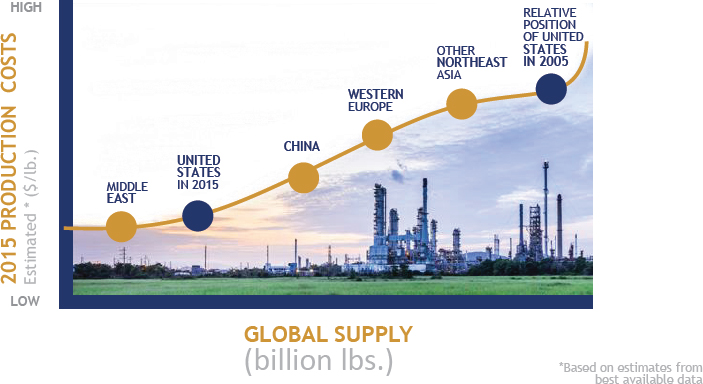

A decade ago, the U.S. chemical industry was in decline. Of the more than 40 chemical manufacturing plants being built worldwide in the mid-2000s with more than $1 billion in capitalization, none were under construction in the United States. Today, as a result of abundant domestic supplies of affordable natural gas and natural gas liquids2 resulting from the dramatic rise in shale gas production, the U.S. chemical industry has gone from the world’s highest-cost producer in 2005 to among the lowest-cost producers today (see Figure 1-1). According to the American Chemistry Council (ACC) estimates, as of September 2015 companies from around the world have announced 246 projects and $153 billion in potential capital investments in U.S. chemical-processing facilities (ACC, 2016), up from 97 projects and $72 billion as of March 2013 (ACC, 2013). Largely as a result of the shale gas boom, U.S. jobs related to plastics manufacturing alone are expected to grow by 462,000, or more than 20 percent over the next decade (ACC, 2015a).

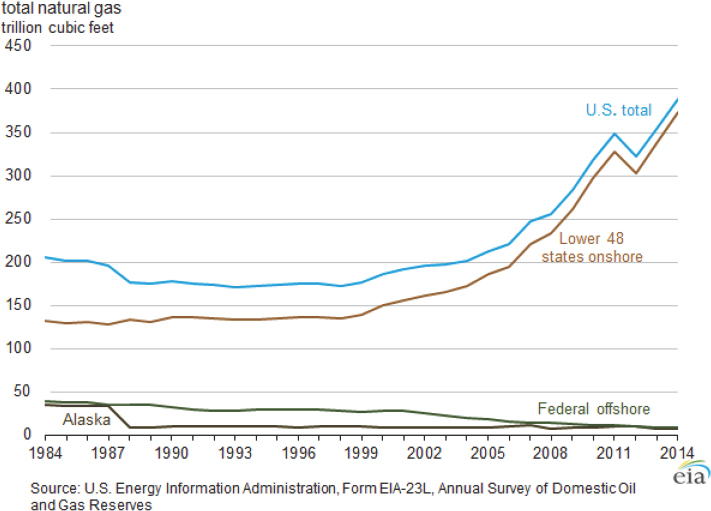

The U.S. Energy Information Administration (EIA) estimated proven U.S. reserves of natural gas and natural gas liquids as of December 31, 2014, to be 388.8 trillion cubic feet, an increase of 8.8 percent over the prior

___________________

1 The Proceedings of a Workshop summarizes the views expressed by individual workshop participants. While the committee is responsible for the overall quality and accuracy of the Proceedings of a Workshop as a record of what transpired at the workshop, the views contained in the report are not necessarily those of all workshop participants, the committee, or the National Academies of Sciences, Engineering, and Medicine.

2 Natural gas liquids consist primarily of ethane, propane, and butane.

SOURCE: ACC, 2016.

year’s estimate and nearly double that of 10 years earlier (see Figure 1-2). This increase is primarily the result of the ability to extract hydrocarbons from shale deposits using a combination of horizontal drilling and hydraulic fracturing. Production of natural gas and natural gas liquids from these reserves has also soared over the past decade and is forecast to continue to rise (EIA, 2016). As a result, the U.S. chemical industry is in the process of switching from naphtha, derived from crude oil, as its major feedstock to natural gas and natural gas liquids. In order to maximize the benefits and take advantage of today’s inexpensive source of natural gas and natural gas liquids to create investments and jobs in the United States, it is important to develop new and more efficient processes related to catalytic conversion of natural gas to higher value materials.

OPPORTUNITIES FOR CATALYSIS

The low cost and increased supply of natural gas and natural gas liquids in the United States provides an opportunity to discover and develop new catalysts and processes to enable the direct conversion of natural gas and natural gas liquids into value-added chemicals with a lower carbon footprint. The economic implications of developing advanced technologies to utilize and process natural gas and natural gas liquids for chemical production could be significant, as commodity, intermediate, and fine chemicals represent a higher-economic-value use of shale gas compared

SOURCE: EIA, 2015.

with its use as a fuel.3 The shift from heavier petroleum-based feedstocks to lighter shale gas sources has created opportunities for the U.S. petrochemical industry, but it has also changed the relative availability and cost of certain chemicals. For example, while the cost of ethylene has dropped, the prices of butadiene and aromatic chemicals such as benzene and toluene—all byproducts of naphtha/oil cracking to produce ethylene—have increased as supplies have become constrained with the shift from naphtha to natural gas feedstocks (DeRosa and Allen, 2015). While the prices of butadiene and BTX swing with time and demand, the trend is toward lower production of these chemicals as more ethane and natural gas liquids are used to produce olefins. As a result, there is an increasing demand for on-purpose, catalytically-driven routes to convert natural gas liquids into these industrially important chemical intermediates. In order to maximize the benefits and take advantage of today’s inexpen-

___________________

3 Economic return from various uses of shale gas should trend similarly to returns from use of oil. While less than 4 percent of oil consumed in the United States is used for production of petrochemical products that use generates close to half of the pre-tax revenue derived from each barrel of oil utilized in the United States (Duff, 2012).

sive source of natural gas and natural gas liquids to create investments and jobs in the United States, it is important to develop new and more efficient processes related to catalytic conversion of natural gas to higher value materials. Because natural gas and natural gas liquids are abundant and lower in cost than equivalent oil-based feedstocks, along with the almost unique situation with large reserves and existing pipelines and other infrastructure, new catalytic processes would give advantage to U.S. producers of chemicals and plastics, and allow for the retention of the value of the carbon in natural gas, rather than burning the gas for its caloric value, which typically is the lowest value use.

CHARGE TO THE COMMITTEE

To better understand the opportunities for catalysis research in an era of shifting feedstocks for chemical production and to identify the gaps in the current research portfolio, the National Academies of Sciences, Engineering, and Medicine’s Board on Chemical Sciences and Technology conducted an interactive, multidisciplinary public 2-day workshop on March 7–8, 2016, in Washington, DC, and focused on identifying gaps and opportunities in catalysis research in an era of shifting feedstocks for chemical production (see Box 1-1).

The goal of this workshop was to identify advances in catalysis that can enable the United States to fully realize the potential of the shale gas revolution for the U.S. chemical industry and, as a result, to help target the efforts of U.S. researchers and funding agencies on those areas of science and technology development that are most critical to achieving these advances. It is the hope of the committee that this workshop will provide a basis for designing research that will lead to the development of new catalysts for converting methane, ethane, and other natural gas liquids into higher-value chemical intermediates under moderate conditions or that enable new routes to chemicals traditionally produced as byproducts of crude oil refining.

STRUCTURE OF THE PROCEEDINGS OF A WORKSHOP

While the committee is responsible for the overall quality and accuracy of the Proceedings of a Workshop as a record of what transpired at the workshop, the views contained in the Proceedings of a Workshop are not necessarily those of all workshop participants, the committee, or the National Academies of Sciences, Engineering, and Medicine. In accordance with the policies of the Academies, the workshop did not attempt to establish any consensus conclusions or recommendations about needs and future directions, focusing instead on challenges and opportunities identified by the speakers and workshop participants.

Chapter 2 provides an overview of the shale gas boom and its implications for the U.S. chemical industry and catalysis, while Chapter 3 discusses the key messages of two presentations on potential opportunities for chemical and biological catalysis to enable the more efficient use of shale gas components as feedstocks for value-added chemical production. Chapter 3 also recounts the reports from four working groups that discussed the challenges and opportunities for converting methane to useful feedstocks and value-added products. Chapter 4 reviews key advances in catalytic conversion of ethane and propane and summarizes the reports from four working groups that discussed the challenges and opportunities in this area, as well as some of the emerging opportunities for novel approaches to natural gas conversion, including the use of nontraditional oxidants. Chapter 5 provides a review of a panel session on environmental issues related to shale gas conversion into value-added products, and Chapter 6 summarizes the key lessons learned from the 2 days of presentations and discussions.

This page intentionally left blank.